Opening the mailbox in our inflation-free economy, I found the following had been forwarded from my mother’s old address in Maryland:

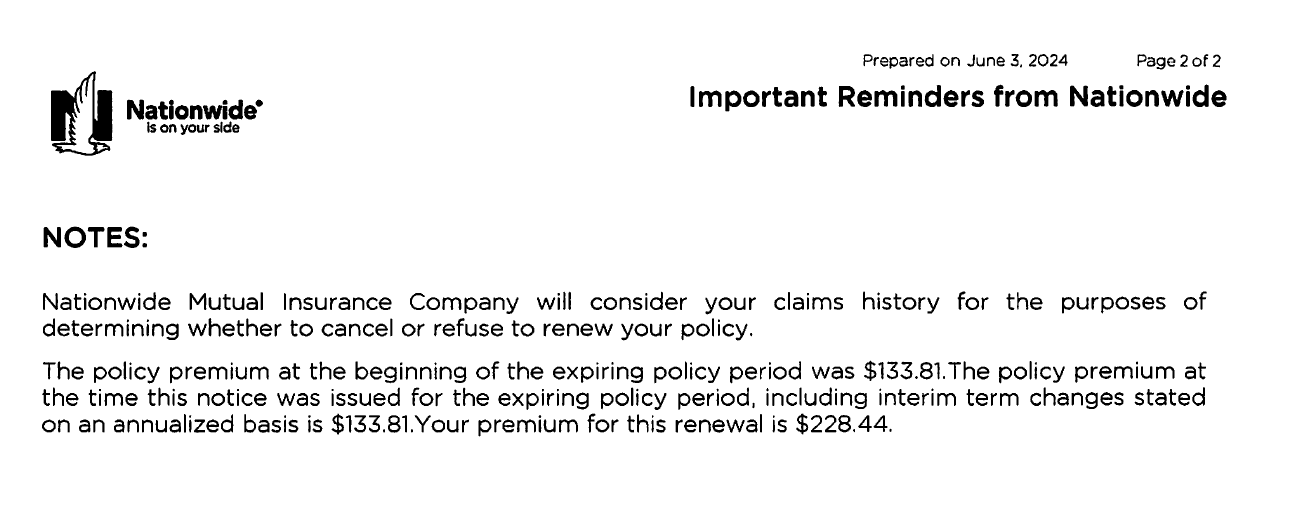

This is a $1 million Maryland-based umbrella policy for mom, whose underlying auto policy was canceled some years ago (my father died in 2021, shortly after receiving the second Pfizer COVID vaccine shot and stopped driving a few years before that). The increase from $133.81 to $228.44 in a year is a 71 percent annual inflation rate.

I canceled the policy because (a) it isn’t valid if the policyholder lacks underlying insurance, (b) I don’t expect mom to do a lot of physical damage with her walker, and (c) $1 million isn’t enough to cover even a tiny fraction of the damages ladled out by juries when a non-physical injury is found (see E. Jean Carroll, for example, who suffered $83 million in damage to her reputation when her veracity was questioned).

In other news from our inflation-free economy… “Nationwide says it’s dropping thousands of pet insurance policies due to inflation” (CNN):

Nationwide Pet, the country’s largest provider of pet insurance, says it is dropping about 100,000 policies between now and next summer to keep up with spiraling costs in vet care.

The move comes as other types of insurance, from homeowners to vehicles, are increasingly becoming harder to obtain for many Americans.

“Inflation in the cost of veterinary care and other factors have led to recent underwriting changes and the withdrawal of some products in some states — difficult actions that are necessary to ensure a financially sustainable future for our pet insurance line of business,” Nationwide said in an announcement last week.

I can’t figure out which 100,000 policies they’d choose to drop. If inflation in vet costs is a nationwide (so to speak) phenomenon, how does it help to pick certain policies to drop and others to keep? By breed? Age of dog?

Smart guys are investing in insurance companies & oil companies. Guess insurance has flexibility to raise rates. Hurricane season didn’t end well for them in 2006.

Insurance companies made big profits in 2006, 2005, 2004, etc. See the numbers in https://www.nbcnews.com/news/amp/wbna17800923

Umbrella policies are a form of reinsurance. I think the driver of the rate increases for umbrella policies could be the number of cases that exceed the limits of other insurances. For example, if more car insurance cases exceed their limits (which I believe are relatively low, around $300k or so), the costs are borne by the umbrella insurer.

My car and condo insurance premiums were up this year, but not by much. My umbrella rate was much, much higher.

Veterinary insurance providers don’t benefit from government protection and government dollars. They act rationally. They probably drop the pets that are most likely to get sick according to their medical history. It’s better to drop existing long-term customers with pets that you suspect are going to produce big bills, and enroll young healthy pets.

I’m paying $400/yr for a $300K umbrella liability policy w/ Lloyd’s of London.

The Keynesians / MMTers / Krugmans keep shouting that everything is great. You can play with the numbers all you want – but you can’t fool us. Keynesian economics is broken – the government never stops spending and borrowing- it will never balance itself – why? Because Keynesians ignore the fact that the voters will never vote for higher taxes and will always vote for more freebies – which politicians will tell them is forever possible and they can always find an economist to back them up on their bullshit. The game is rigged, the connected chronies get first dibs on the low interest rate money that gets printed and use it to buy real assets to keep a store a value, while the common man suffers, because inflation is stealing the value of his salary. Sure, according to the Keynesians they keep him employed – but now his wife also needs to work, and then they both need 2 jobs to stay afloat.

We’re living in a gangster’s paradise… hopefully we wake up.