COVID-19 killed most of America’s old people and now Social Security is insolvent

Social Security’s impending insolvency is in the news lately. The system that provided Ida May Fuller with benefits that were 1000X what she paid in tax was apparently not sustainable (even Charles Ponzi couldn’t keep a scheme like that going forever!).

We were previously informed that 1 million healthy over-65 Americans had been killed by COVID-19. These people had at least 5-10 years to live, during which time they’d be receiving monthly Social Security payments. I wondered about this back in 2021 with Wave of death among the elderly bankrupts Social Security and quoted CNBC:

The Social Security trust fund most Americans rely on for their retirement will run out of money in 12 years, one year sooner than expected, according to an annual government report.

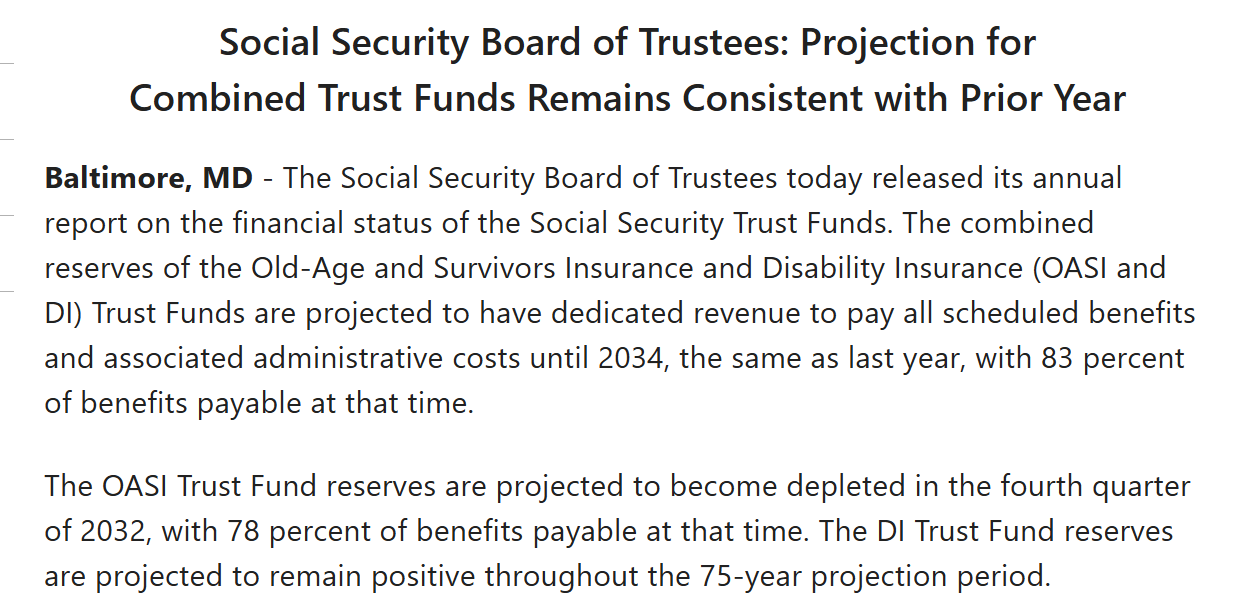

Social Security payments would be cut, or young people further enslaved to taxation, in 2033, in other words (2021+12). Apparently, some of those killed by COVID-19 have risen from the grave and are collecting benefits once again because the “trust fund runs out” date has moved up from 2033 to 2032 (source):

It is confusing because the above official source implies that full benefits are paid until 2034. The media, on the other hand, is reporting Social Security payments would be cut, or young people further enslaved to taxation, in 2032.

What do progressives think about this? A Maskachusetts friend who previously loved whatever Democrat thought leaders, such as AOC, Ilhan Omar, and Bernie Sanders were dishing out, objected on Facebook to losing his monthly checks:

I have been reading about the concept of “means testing” for social security recipients. This means taking it away from successful people. Well, I am okay with the government taking away my social security if the government will simply return to me all the money I paid in over the last 50 years.

One of his financially savvy friends pointed out that “Every single adult worker” would be better off if they could have kept their Social Security taxes and invested it in the S&P 500. My response:

Social Security calculates and publishes internal rates of return periodically. These are in real dollars (adjusted for inflation). Very low earners who are married can get an 8% real return, comparable to the past 50 years of the S&P 500. Median earners get less than 2% (single man), 2.5% (single woman), or 4% (one-earner married couple). Someone at the income limit gets only about 0.6% real return (single man), 1% (single woman), 0.85% (two-earner couple), or 2.3% (one-earner married couple). So you could consider Social Security to be part of the U.S.’s transferist welfare state. It transfers money from high earners to low earners. It also transfers money from men to women and from those who weren’t successful in the marriage market to those who were successful. … So maybe [our mutual friend] will feel better about Social Security if he stops thinking about it as something designed to benefit him and instead as something designed to help him transfer money to low-income Americans and women

(note that the SSA doesn’t calculate or publish an IRR for nonbinary Americans)

What do readers think is going to happen? Benefits get preserved for anyone already claiming them, but drastically cut for anyone who hasn’t gone on Social Security yet? Benefits get cut for everyone? Social Security tax extended to infinite levels of earned income instead of being capped? Society Security tax extended to “unearned income” such as dividends and interest? (if the money isn’t “earned” then fairness dictates that the government should take 100 percent of it) Elon’s unearned $1 trillion gets confiscated and that plugs the hole? Robots get taxed as if they were human workers and 12.4% of the cost of buying and operating a robot must be given to Social Security?

A lot of my friends are between 62 and 67 (“full retirement age” for their cohort). Would they be better off getting on Social Security before they hit 67 or 70 (max benefit age) so as to be part of the “we don’t want to take anything away from these Boomers who are already relying on it” class?

(We can also look at Medicare, the federal government’s most expensive program (even larger than our off-the-charts enormous military!). Most proposals to cheat everyone who previously paid into it say that most or all of the stealing will be done from those under 55, e.g., by making them wait until 67 rather than 65 to receive any benefits.)

Related:

Full post, including comments