Number of Americans dependent on food stamps has been reduced from 17 million in 2000 to only 42 million today

Josh Hawley, a senator who calls himself a “Republican”, in the New York Times:

Millions of Americans rely on food assistance just to get by. The program often known as food stamps — officially it’s now called the Supplemental Nutrition Assistance Program, or SNAP — is a lifeline that permits the needy to purchase basic food items at the grocery store. Last year, SNAP enrollees hit about 42 million. That’s over 12 percent of the American population.

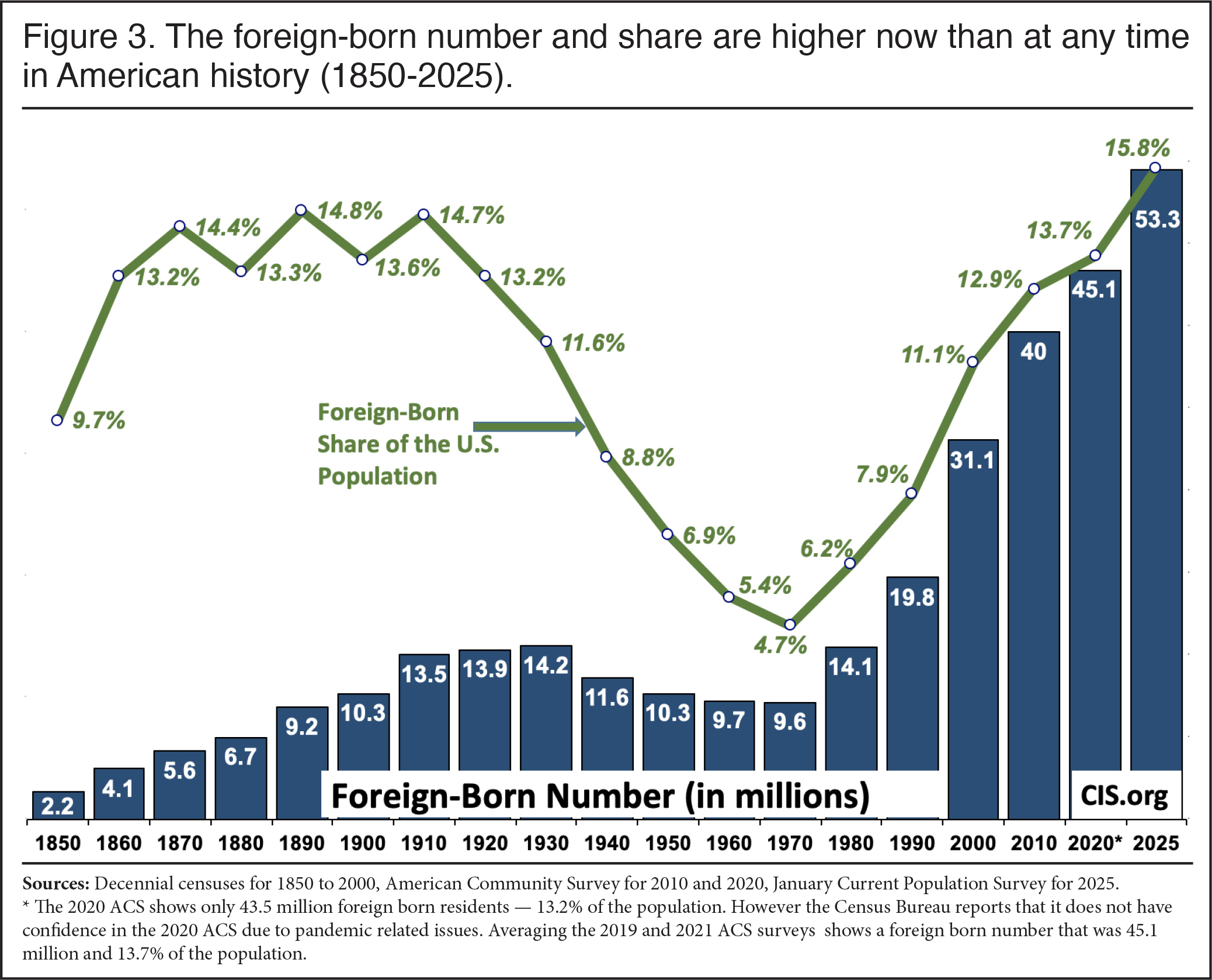

We’re informed that low-skill migrants make America rich. America has never been richer in migrants (CIS):

We’re informed that government spending on poverty relief reduces the number of poor people. The federal government spends more than $100 billion per year of workers’ (chumps’) tax dollars on SNAP. How much larger was the group of helpless government-dependent Americans 25 years ago before the most recent $trillions had been spent on SNAP? According to the USDA, the number of food stamp-dependent Americans in 2000 was… 17 million:

In other words, in the past 25 years the number of Americans who’ve become dependent on food welfare exceeds the population of Taiwan (23 million), where all of the world’s highest-tech integrated circuits and bicycles are made. The Google says that while we managed to grow our food-welfare-dependent population by more than 2X, TSMC grew its market value from $40 billion to over $1 trillion.

(Note that the 42 million Americans who are enrolled in SNAP/EBT shouldn’t be taken as an estimate of the number of Americans receiving what used to be called “welfare”. There are about 78 million Americans currently on Medicaid, for example. Maybe the discrepancy is that a multi-member welfare household shows up just once for SNAP and multiple times for Medicaid? Or some people getting taxpayer-funded food are getting it via programs with other names (see chart below)?)

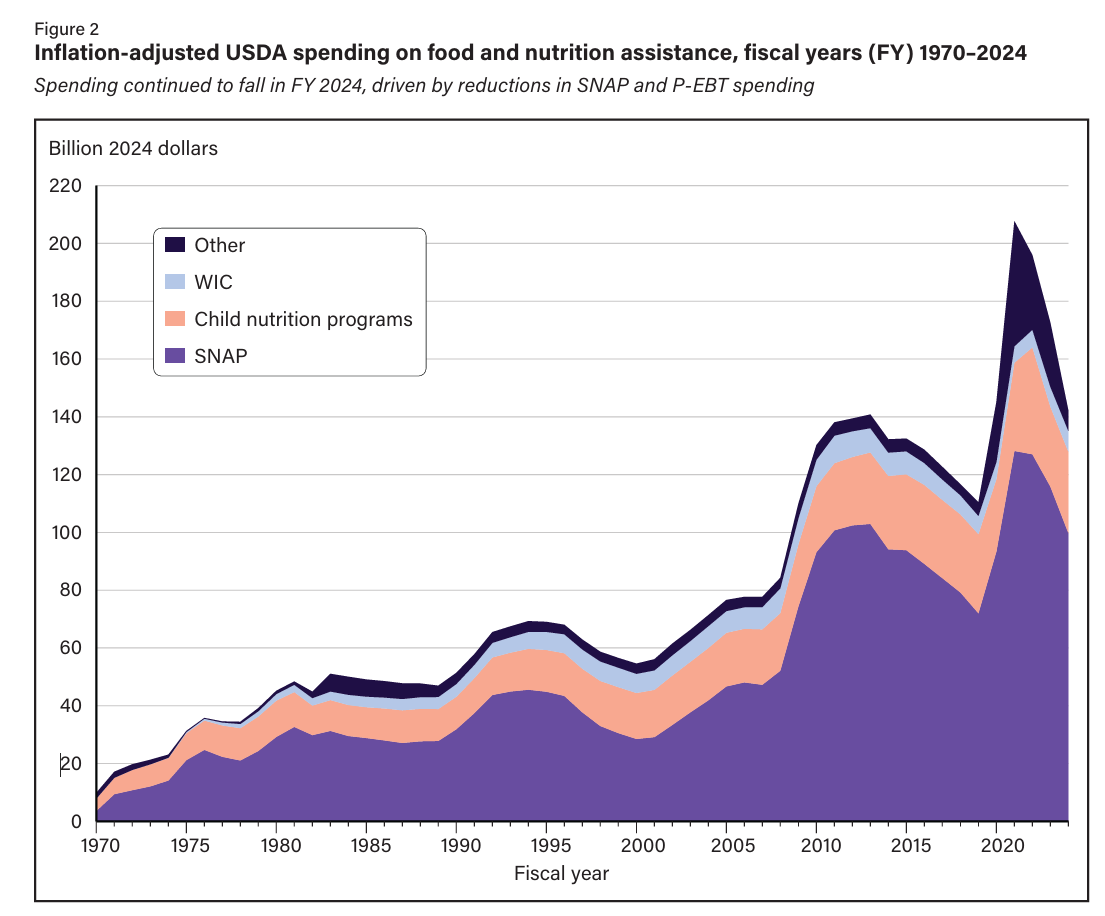

Inflation-adjusted spending seems to have grown by about 14X since 1970 (USDA):