Can Spain get rich by selling the Ceuta migrants to other EU nations?

Spain has been in the news lately due to an influx of enrichers via its Ceuta colony in North Africa:

We’re informed that low-skill migrants make any European nation richer both economically and culturally. If that weren’t true, there would be no reason for Europe to accept even one low-skill migrant (acceptance of migrants can’t be based on humanitarian grounds; Sudan has a population of 52 million, for example, and it makes no sense to provide four generations of welfare to a handful of Sudanese in Europe while providing nothing to 52 million Sudanese in Sudan).

After one bounteous day, Spain is now in possession of roughly 60,000 additional migrants (BBC). Can Spain now offer these enrichers to other EU nations for a reasonable processing and transportation fee? At 60,000 migrants per day, even $20,000 per migrant yields a $438 billion/year revenue stream.

Bizarrely, the head of the EU says that enrichers are “unacceptable”! Europe previously wanted to be enriched, which is why some European nations are now 25% migrants or children of migrants, but Europe no longer wants to become culturally and economically richer?

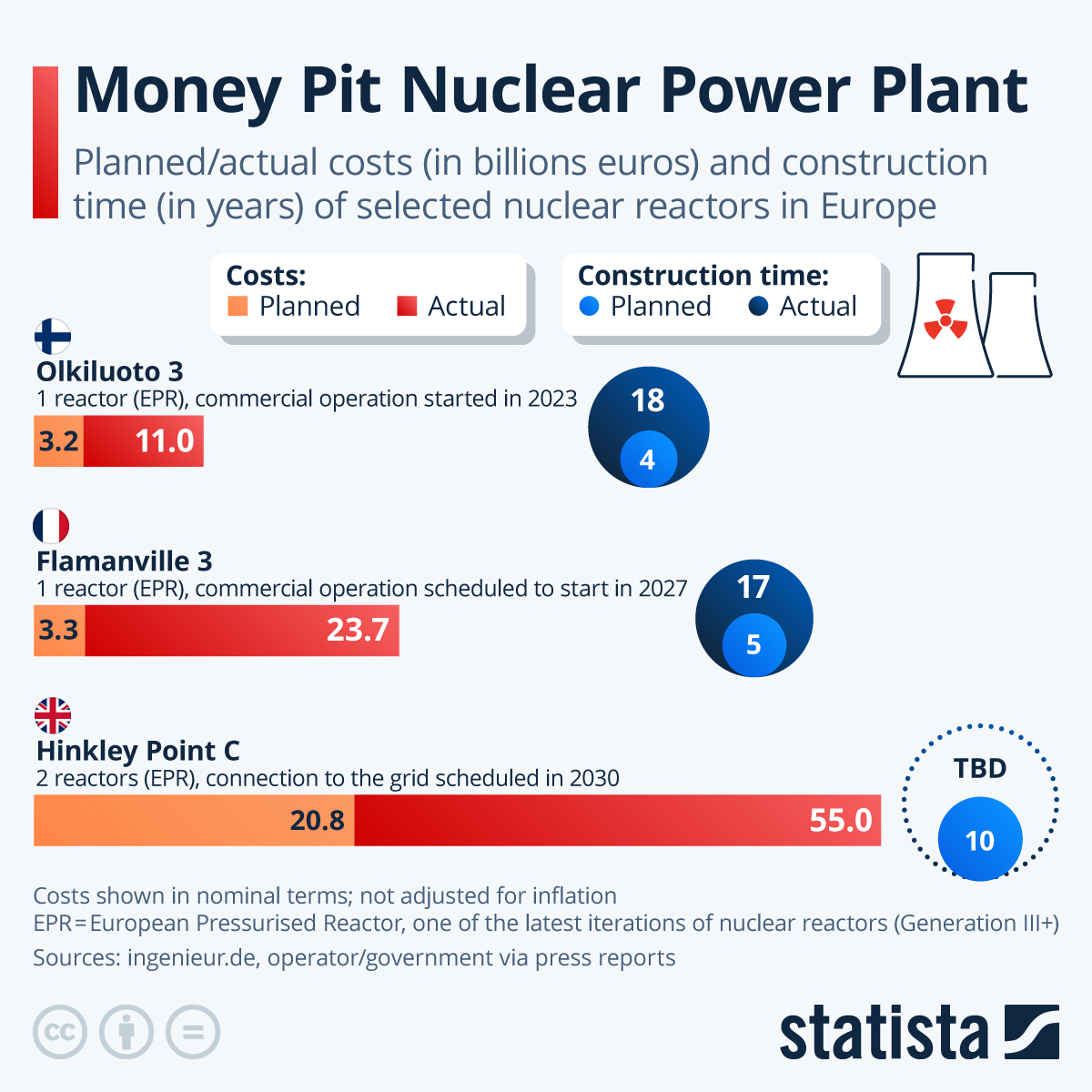

Here’s the same leader saying that €10 billion in tax dollars are going to be spent on data centers because, presumably, private companies are underinvesting in AI?

Could Spain fund a massive collection of data centers by selling migrants to France, Germany, Italy, Poland, Sweden, and other EU nations? Retail electricity rates in Spain are more than 2X what consumers in the efficient U.S. states pay so it doesn’t seem like the most obvious place for AI cogitation.

Ceuta-based lawyer Manuel Jurado said: “Like the rest of the residents here we’re living through this situation with a feeling of complete uncertainty. There are people everywhere and there’s violence now in the city.

“I understand these young migrants have arrived here looking for a better life but there are legal mechanisms that offer that security both for them and for us.

The “looking for a better life” as a justification for immigration into a welfare state is confusing. By this standard, shouldn’t anyone anywhere in the world whose spending power is less than whatever a welfare state, such as the U.S. or any of the headline EU countries, be entitled to move? If it’s “a better life” to be on welfare in Maskachusetts or Spain than to live in Yemen, for example, shouldn’t at least 40 million Yemenis be entitled to migrate to Maskachusetts or Spain?

Full post, including comments