As an index fund investor, I used to (indirectly) buy stocks that had been public for a while and only of companies that made a profit. The rules have apparently been tossed so now I will be a(n indirect) SpaceX shareholder. NYT:

Nasdaq, the exchange where SpaceX plans to list its stock, announced a rule change in May to allow “fast entry” into the Nasdaq-100 index by large private companies like SpaceX that go public.

Others followed. FTSE Russell recently altered its methodology, which will result in listing SpaceX in its indexes within a week of its going public.

The changes mean a large swath of index funds — which millions of Americans own in their retirement funds, pension plans and personal portfolios — are poised to hold SpaceX shares soon after the company goes public. Anthropic and OpenAI, the artificial intelligence start-ups that are planning to go public this year, would also land in index funds quickly, potentially exposing everyday investors to more financial risk whether they like it or not.

“It’s historically unprecedented,” said John Polonis, a former Wall Street lawyer who worked at J.P. Morgan and now offers financial analysis on social media. “You can try to reorient your retirement accounts to avoid funds invested in A.I. companies, but most people aren’t going to be doing that. They’re kind of left out in the dust here.”

Is there any integrity left on Wall Street?

One index provider has declined to budge. On Thursday, Standard & Poor’s said it would not change its criteria for inclusion in the S&P 500, one of the most-followed indexes, meaning SpaceX will not be eligible for inclusion until at least mid-2027. Standard & Poor’s said it had determined that exceptions to its rules “should not be granted solely based on market capitalization.”

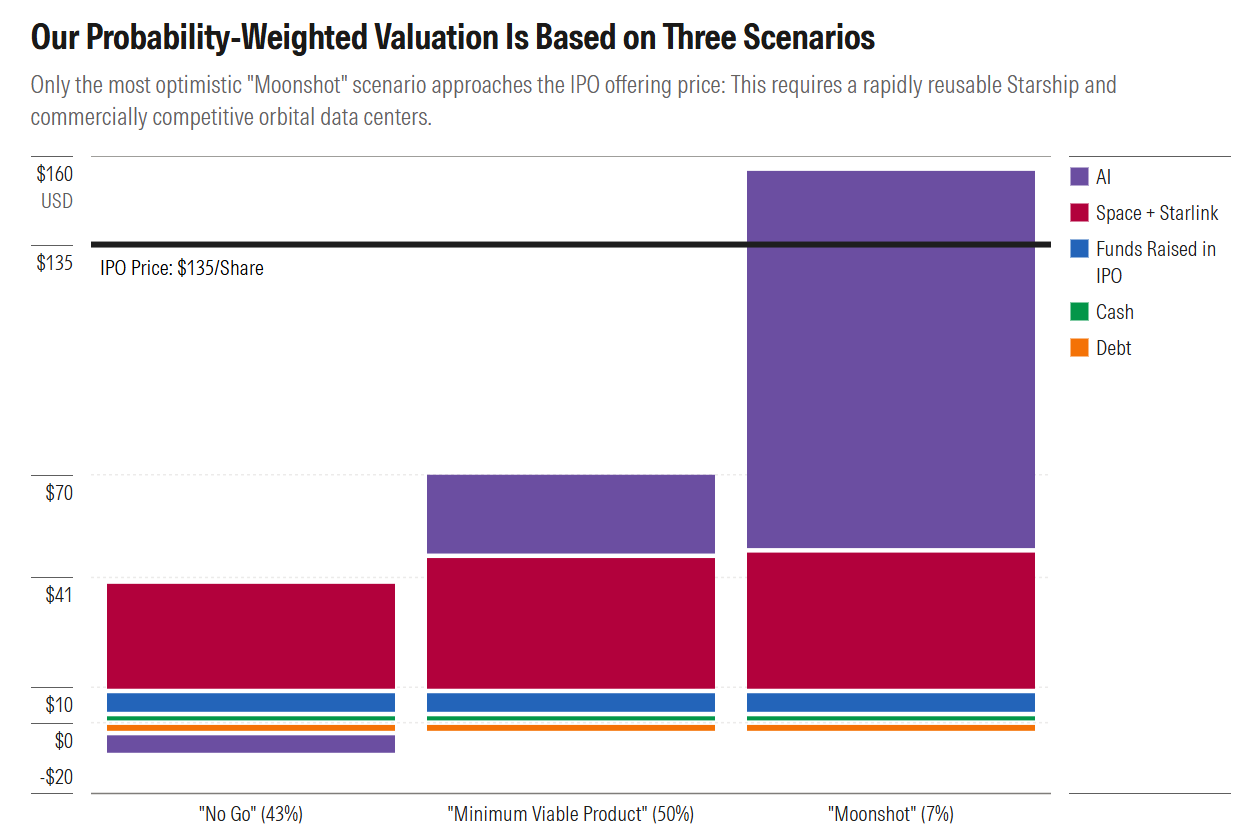

What’s the long-term value estimate for this company? Humans cluster in metro areas, thus making fiber Internet and cell towers better than Starlink for most of us. ChatGPT: “roughly 75–85% of people worldwide who have at least a global middle-class/consumer-class standard of living live in urban, suburban, or peri-urban areas. I’d use 80% as the best single-number answer.”

SpaceX has the best rocket tech, but unless you’re Iran and want to kill infidels worldwide how many rockets do you need? Maybe the answer is military use of space rather than sending up packages that will rain down on the enemies of the righteous? But military equipment for use in space is incredibly expensive and takes forever to develop and build. Does a cheaper launch capability matter for the U.S. Department of War?

Elon says space makes sense for data centers, but I have a tough enough time maintaining the computer on my desk. If we want solar power and cheap land why isn’t Arizona, a Texas ranch, or central Florida a more sensible location?

How about the value of going to Mars? If a spaceship could accelerate continuously and indefinitely at 1g and decelerate at 1g how long would it take humans to get to Mars from Earth, all the while experiencing Earth-like gravity? Prof. Dr. ChatGPT, PhD Physics says 2-5 days. That would be an awesome tourism business. But, of course, SpaceX has no technology like that.

Perhaps the answer to the orbital-level valuation for SpaceX is that the company is run by a woman and we’re informed that female-led companies outperform their male-led peers. TIME:

Readers: What will SpaceX be worth five or ten years from now (in 2026 dollars)? What will have been seen as the main driver of value?

I’ll go first… because I believe in efficient markets, SpaceX in five years will be worth its IPO price plus 4% real return annually (about 21% over the IPO price). A narrow majority of the value will be from Starlink. (Note that this is like a probability expectation. I’m pretty sure that something dramatically good or dramatically bad will happen to SpaceX, but I can’t predict which is more likely and therefore my guess is right at the center. Analogous to the expected value of a coin flip game for $1 being $1 even though we know it will either be $0 or $2 and can’t be $1.)

A professional investor friend says that SpaceX would be a good buy at the IPO price because of the high percentage of retail purchases. “These retail investors come back in and support the price even after the inevitable post-IPO slump,” he said. “The more retail the better, contrary to previous prevailing wisdom.” If he had access to a large bock of SpaceX at the IPO price and without a lock-up, he would buy the block and sell it after a few days (i.e., right when a lot of index funds will be buying!).

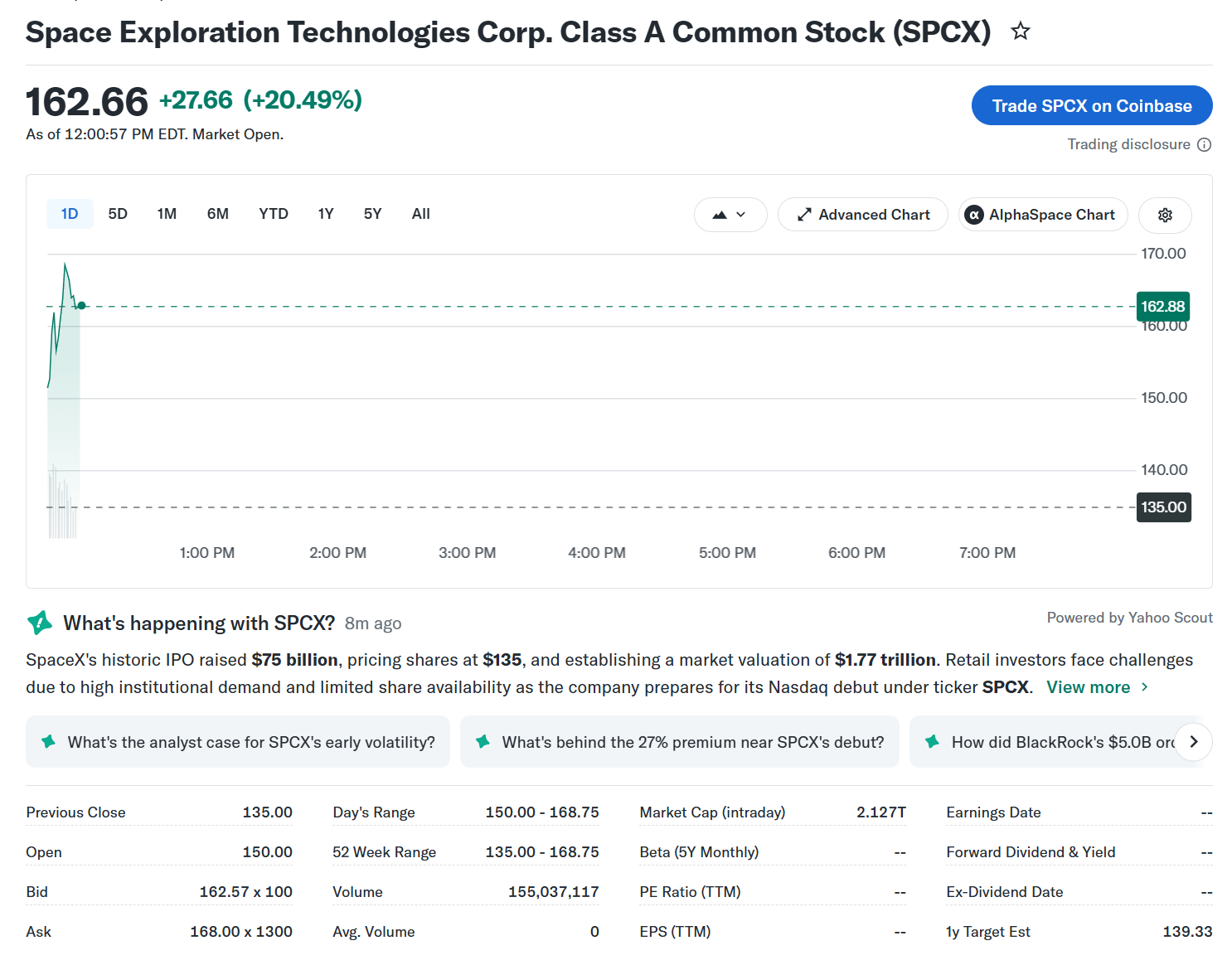

“SpaceX IPO Is Said to Be More Than Four Times Oversubscribed” (Bloomberg, June 10):

SpaceX’s initial public offering has attracted demand for more than four times the available shares, according to people familiar with the matter, ahead of the Elon Musk-led rocket, satellite and artificial intelligence firm stopping taking orders.

SpaceX’s IPO is set to price June 11 and trade the following day. The company is offering 555.6 million shares at a fixed price of $135 each, which would raise about $75 billion, and value it at about $1.8 trillion.

I’m confused by the above. It says “set to price June 11” and the article is dated June 10. How was the price of $135/share already known on June 10? Separately, if the offering is oversubscribed by 4X, doesn’t that suggest the price is being set way too low? What about the duty to protect SpaceX’s existing shareholders by not giving away shares at such a low price that there are 4X as many buyers as shares? To avoid this abuse of shareholders, Google did a Dutch auction at its IPO (Google AI)

Google’s historic August 2004 Initial Public Offering (IPO) famously utilized a modified Dutch auction instead of the traditional wall street underwriting process. In this method, instead of investment banks setting a fixed price, individual and institutional investors bid directly on how many shares they wanted and the price they were willing to pay.

This is explained in “How I Did It: Google’s CEO on the Enduring Lessons of a Quirky IPO” (Harvard Business Review) by Eric Schmidt:

In mid-August the bidding began, based on our published expected IPO price range of $106 to $135 a share. … There weren’t a lot of orders, and to be frank, we wondered if we’d made a mistake in choosing an auction-based approach. The offers that did come in were at or below the low end of the range we’d anticipated. When the bidding period ended, it was clear that we weren’t going to be able to sell all the shares we had planned to sell in the price range we wanted. I met with the board to discuss whether we should delay our IPO and hope to get a higher price later. Our underwriters believed that we could close the IPO with a price around $80 to $90 a share if we reduced the number of shares for sale—a disappointing outcome. In the end we decided to close the IPO for a number of reasons, the most important being that it was time to put this chapter behind us and get back to running our business. So on August 18 we agreed to price it at $85 a share.

Perhaps this is the answer. Google expected to get more via an auction and got less. See also “Google shares took off, but the auction didn’t” (CNBC, 2014):

The rationale was simple: Take the short-term gains away from Wall Street and big money and give at least some ownership to the many consumers whose obsessive use of the search engine had allowed it to grow from a garage start-up into a multibillion-dollar phenomenon in half a decade.

But instead of pioneering a new formula for IPOs, with investment banks and big investment shops ceding control to the issuing companies and a wider universe of investors, the Google deal remains a historical anomaly.

Experts offer up two main explanations. The first is that auctions are risky. Banks get paid handsomely (7 percent of the offering amount is typical) to sell a deal to their clients, and in the process make sure prospective investors understand the business, competitive landscape and the state of the market. Through that work, they find what investors are willing to pay, so companies can be fairly confident that there’s adequate demand at the set price. An auction, meanwhile, is more like an investors’ Wild West.

The second reason is that Google’s offering wasn’t a real auction, but more of a hybrid. After all, there was clearly enough investor demand to price the stock at closer to $100, because that’s where the stock opened, but at the last minute lead underwriters Morgan Stanley and dropped it to $85. The low end of the expected range had been $108.

David Golden, a banker at JPMorgan, one of the many banks that served as an underwriter for the IPO, said the big investors decided just before the offering that without a reduction in price, they’d wait until the stock started trading and buy it on the open market rather than pay $100 a share or more in the IPO.

“Lo and behold, it was set at $85 a share, which built in a 15 to 18 percent profit that banks like to deliver to big institutional investors and that investors like to receive,” said Golden, who is now a managing partner at Revolution Ventures in San Francisco. Institutions “want to know that when they’re buying risky, illiquid securities, they’re going to have a built-in gain.”

Full post, including comments