New York City (and maybe the state as well) are generating outrage by proposing to tax residential real estate that isn’t a primary residence at a higher rate than the same property would pay if occupied by somewho who was a full-time NYC resident.

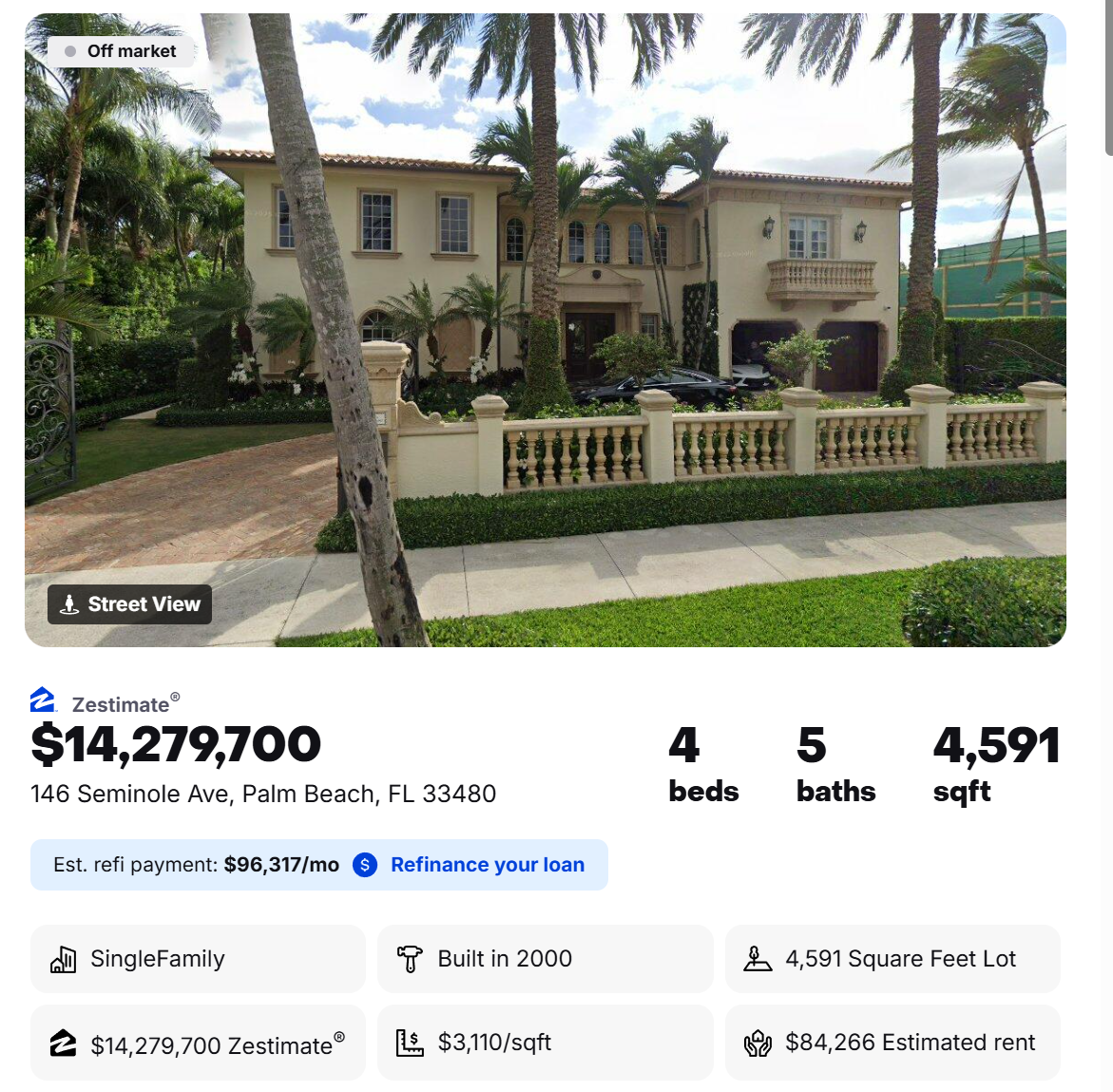

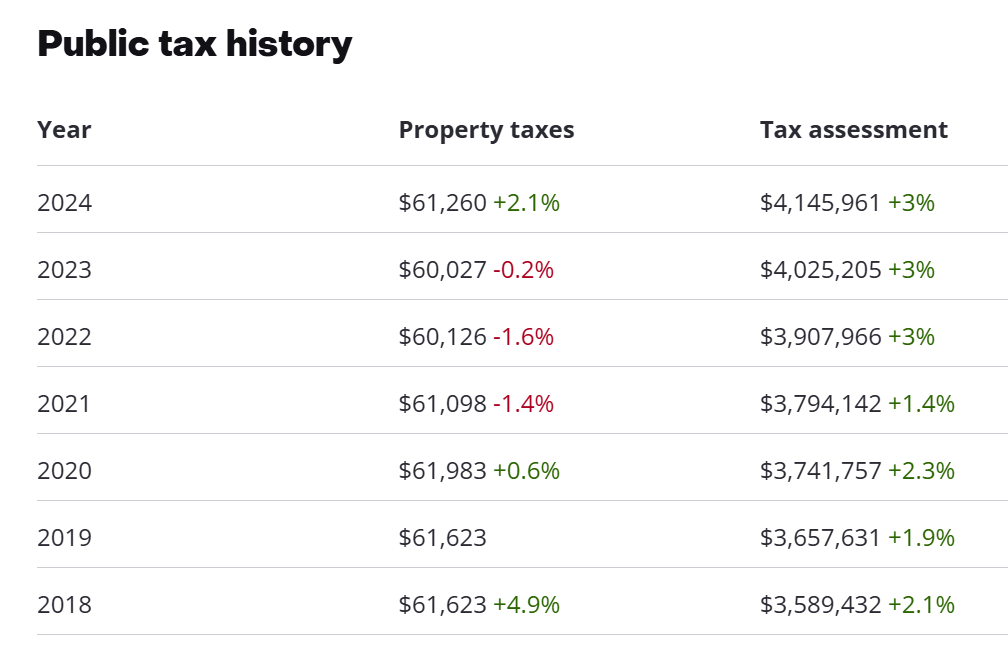

What other city or state indulges in this outrageous abuse of society’s successful? Florida! Let’s look at starter homes in Palm Beach. Here’s one that was purchased for $4.45 million in 2011 and is today worth $14.3 million (Zillow).

The tax assessment is still less than the purchase price, presumably due to the fact that the assessed value for a “homestead” (primary residence) can’t go up more than 3 percent or the increase in CPI, whichever is lower:

If there were an identical house next door and it sold for $14 million to someone who used it only 4 months per year, the town/county could collect property tax on the full value, i.e., 3X the tax rate paid by the primary resident.

A surcharge for part-time residents generates outrage. A discount for full-time residents doesn’t upset anyone. NYC could have doubled property tax rates, with state permission, and then offered a steep discount for anyone who pays resident NYC income tax.

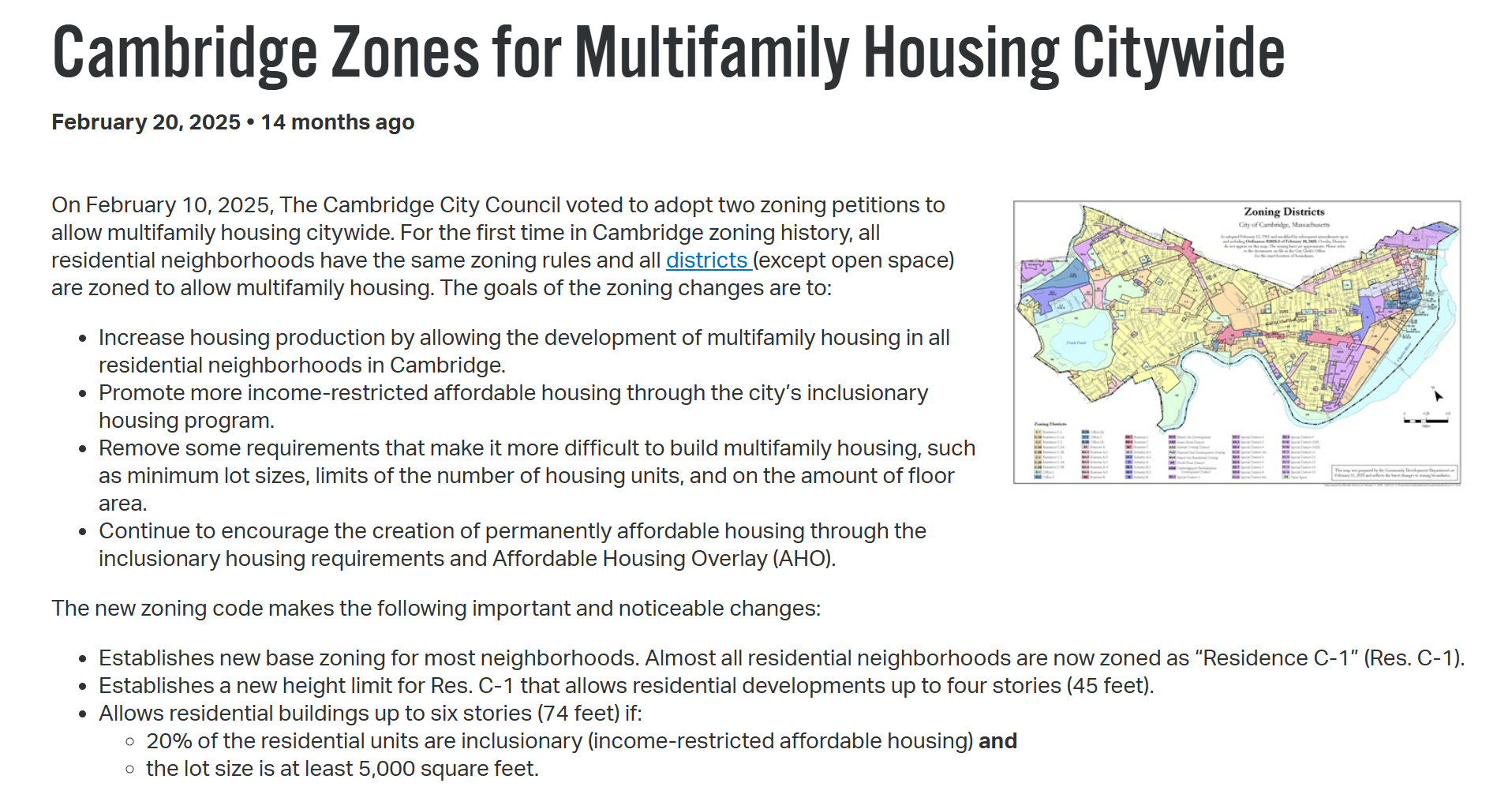

As part of cleaning out my old Harvard Square condo, I learned that the City of Cambridge has embarked on a plan to increase population density, a rare situation in which the people who advocate for open borders also do something about accommodating the new arrivals and their kids and grandkids.

Starting in 2025, the city began allowing developers to build 6-story apartment buildings/condos in neighborhoods that had formerly been restricted to single-family houses:

There is no requirement that the new apartment buildings be anywhere near public transit or that they make any provision for parking (i.e., competition for street parking spaces is about to hit Olympic Team levels, though maybe the Tesla Robotaxi will ameliorate the issue?).

I talked to a lady who lives in West Cambridge, which has a suburban feel. “A developer bought an 1890 Victorian house and is putting up a 54-unit building,” said said. “It’s 1.2 miles from the nearest T stop. There’s hardly any bus service except at rush hour. There won’t be any off-street parking built as part of this.” How do the Biden-Harris voters in the neighborhood feel about living next to people receiving subsidized housing (20 percent of the units must be “inclusionary”, i.e., rented or sold at below-market rates to the fortunate few)? “They’re fighting the project tooth and nail by claiming that the old house is historic and can’t be demolished.”

I remain mystified as to how those who decry “inequality” can support these programs in which a handful of people are selected to pay nothing or almost nothing for housing while the vast majority of others who are equally situated in terms of income, etc., are doomed to pay market rates (i.e., live 45 minutes away from anywhere that is considered nice).

Most of Cambridge is poorly served by public transit. The subway stations are widely separated. The subway itself doesn’t run fast or go most of the places that people need to go. Bus service is slow and infrequent, though the former “Dudley bus” was renamed in 2020 to “Nubian Station bus” (background). Google AI:

Nubian refers to an indigenous ethnic group and the ancient civilization from the Nile valley region spanning southern Egypt and northern Sudan. It describes people, languages, and cultures originating from this area, which is known for a history dating back to 3100 BC. It is also used informally to describe Black culture, people with dark skin, or specific livestock breeds.

Can anyone think of an example of a portion of an American metro area, population 2 million or larger, that has been built up to an average 6-story height, or higher, that doesn’t have horrific traffic jams? The advocates for higher density seem to assume that everyone in young, healthy, fit, childless, and happy to walk 1.2 miles through slush and/or in 10-degree temps. Or perhaps that the fit young parents will bundle their young children up like Eskimos and load them into $7,000 Dutch cargo bikes that get stolen every six months.

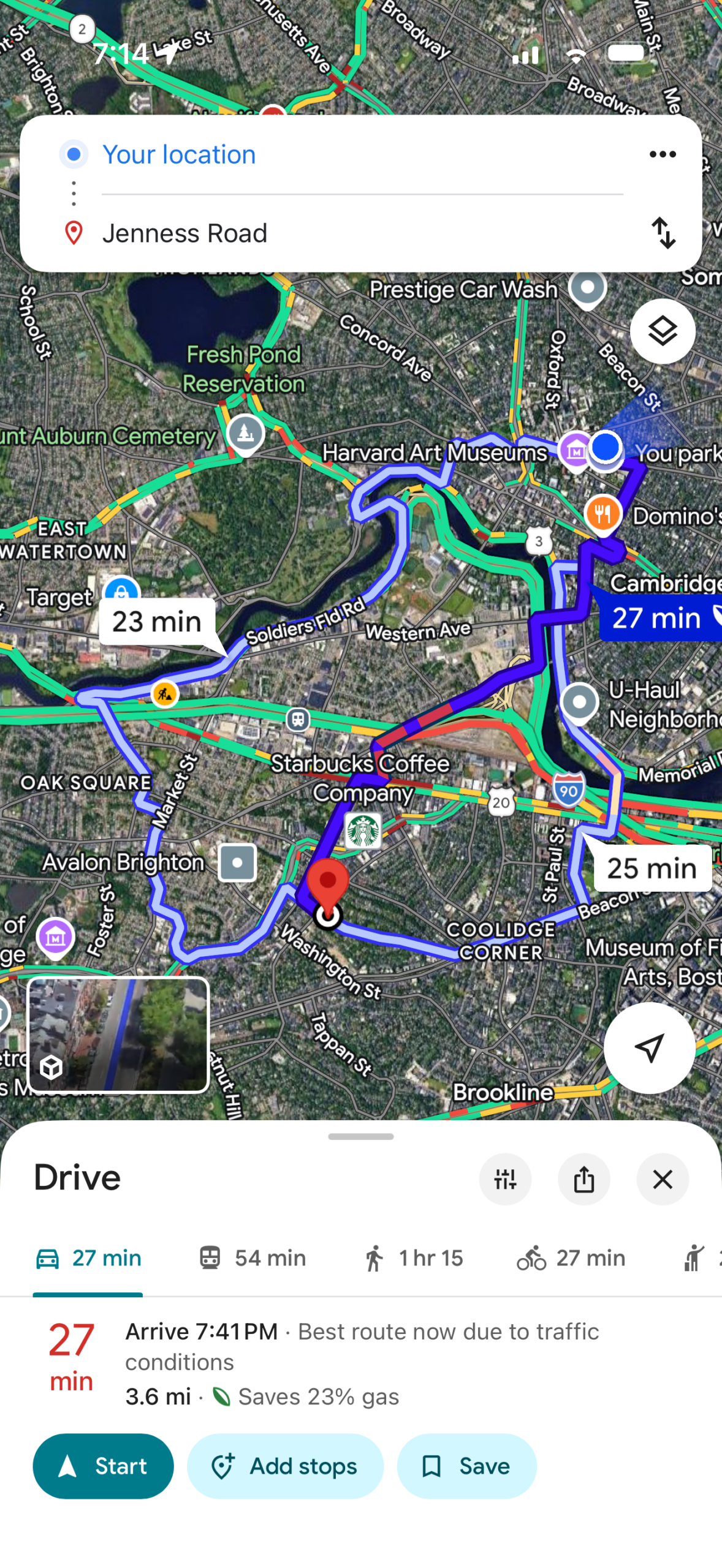

Trying to get to a friend’s house in Brookline from practically on top of the Harvard Square T station at 7:14 pm, i.e., after rush hour:

It was 54 minutes by public transit and add another 15 minutes for a more typical Cambridge location that wasn’t so close to the T. This should be a 15-minute drive, which shows you how much the mobility of people in the Boston area has been reduced by roads being narrowed, more people getting cars, population growth, etc.

Florida’s migration patterns are changing dramatically. Residents in their prime working years are heading to other states, often citing affordability concerns. At the same time, the stream of people arriving from other states is shrinking.

Meanwhile, an influx of wealthy people from other states—turbocharged during the pandemic—has helped drive up home prices. Inflation in parts of Florida outpaced the national average over the past decade and home-insurance rates soared.

These side-by-side trends could spell trouble for a state whose economy relies on continued population growth and real-estate development.

“The affordability picture has changed in Florida almost more than anywhere else in the country,” said Eric Finnigan, vice president of demographics research at John Burns Research & Consulting.

First, note the assumption that underlies almost all American politics: infinite growth should be the goal. (Never mind that growth without limit in an organism, and without regard to available resources, is known as “cancer”.)

Second, the WSJ implicitly assumes that a place that is affordable is better than a place that is unaffordable for median-income residents.

Third, the WSJ lumps all of “Florida” together. Florida is about the same size as all of New England. The WSJ wouldn’t lump together Boston and western Maskachusetts, much less Bridgeport, Connecticut and Houlton, Maine. (It’s still possible to get a brand-new single-family house in central Florida for less than $300,000, though the same can’t be said for coastal Florida; the house will be about 1500 square feet, which is the size of the house I grew up in (family of five) and with the added advantage that Floridians don’t need as much indoor space.) The most convenient housing for a SpaceX or Blue Origin engineer is in Titusville, where a decent (not new) house can be purchased for $300,000 (relocation guide).

Fourth, the WSJ assumes that the market is full of stupid people who bid up the prices of houses in places that aren’t desirable. Single-family home prices are $10.15 million in Palm Beach and $212,000 in Dearborn Heights, Michigan, where Ayman Ghazali mostly peacefully lived. From this we can infer that living among Iraqi and Lebanese immigrants in Dearborn Heights is better than living among Manhattan immigrants in Palm Beach (perhaps not an unreasonable inference!).

Maybe in a country with a shared language and culture it would make sense to try to find an inexpensive place to live. However, in a country that is jammed with low-skill migrants from all of the world’s most violent and dysfunctional societies (our asylum-based immigration system ensures that someone from Switzerland or Japan goes to the back of the line), isn’t it actually an advantage from a typical native-born perspective that a place is out of reach for the median present-day American? Google AI: “Newport Beach has lower racial diversity and worse racial disparity across various indicators compared to the average for California cities.” Given the stratospheric real estate prices, it seems that a lot of people are willing to pay for low racial diversity and “worse racial disparity”. As of 2021, the town was supposedly 85 percent white (source):

The Dallas metro area is more affordable than most parts of the US with jobs, which has enabled a mostly-immigrant community of 130,000 Muslims to set up more than 60 mosques and lay out EPIC City, “a master-planned Islamic community-centered residential development project”. Non-Muslim Americans who don’t want to hear the muezzin calling five times per day might prefer to spend more on a house that is in an area that is “unaffordable” to immigrants from Syria, Egypt, Afghanistan, and Somalia.

We could take this to an extreme. Aspen, Colorado is absurdly unaffordable for the median worker. My friend doesn’t like Aspen (see An actual skier goes to Aspen to ski), but apparently a lot of people do like it. Would we say that Dearborn Heights, Michigan is a better place to live than Aspen? That Aspen is bad because the population isn’t growing 3% per year like Gaza’s or Somalia’s? (Maybe Gaza and the West Bank are the ultimate examples of affordability. US and EU taxpayers pay for all of the basics, e.g., shelter, food, health care, education, etc. Nobody needs to work. Hamas-ruled Gaza is a model society by Ivy League standards, but wouldn’t the typical American rather be in St. Barts, Aspen, or Nantucket (all of which rank near the bottom for affordability on a median income)?) We could also consider a massive public housing project in Chicago or New York City. They’re “affordable” by definition since no tenant is charged more than 30% of his/her/zir/their income (often 30% of $0 since the tenants aren’t stupid!). Would a typical American prefer to live in the 6000-person Queensbridge Houses (“well known for its contributions to hip hop and rap music”; “a problem with drug dealers and drug users”) or in Atherton, California (population 7,000; home to Larry Ellison before he spent $450 million to escape to Florida)?

In short, given the continued flood of low-skill migrants (70 million since 1976) maybe “affordability” shouldn’t be the goal for any city or state that seeks to maintain a pleasant environment.

Happy National Fair Housing Month (“A Fundamental Right, Year-Round”; for Americans dumb enough to work: the “fundamental right” is to pay taxes so that others can relax in public housing) to those who celebrate.

Recent message from a friend who was smart enough to sell everything in Maskachusetts and buy in Texas in early 2009:

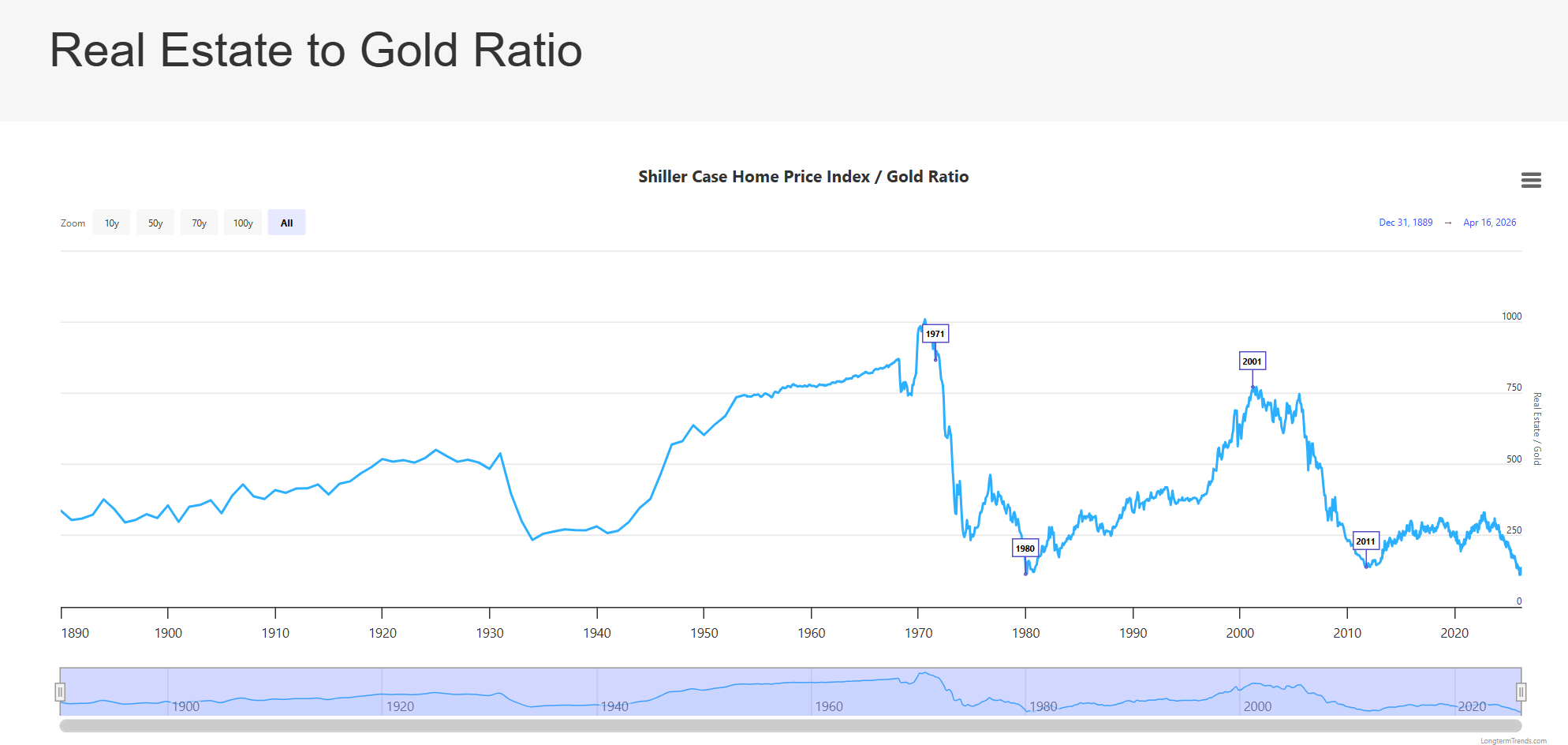

My contrarian view: Real Estate prices are at an all time low….. if measured in gold

Given that peasants can’t afford to buy at current prices/mortgage rates, my first reaction was “this is dumb”. On the other hand, I think my friend is closing in on billionaire status due to his previous real estate investments so maybe it is me who is dumb.

There is some support for his theory from this chart (source):

Does this make sense, though? Gold can be purchased by anyone in the world as an investment or for decoration. It is easy to transport. Residential real estate is impossible to transport and most of it has to be purchased by or rented by someone who lives where the real estate is. Rich people in Switzerland, India, San Francisco, Miami, and Singapore might buy up all of the world’s gold, but they’re not going to pay anything for a house in Detroit.

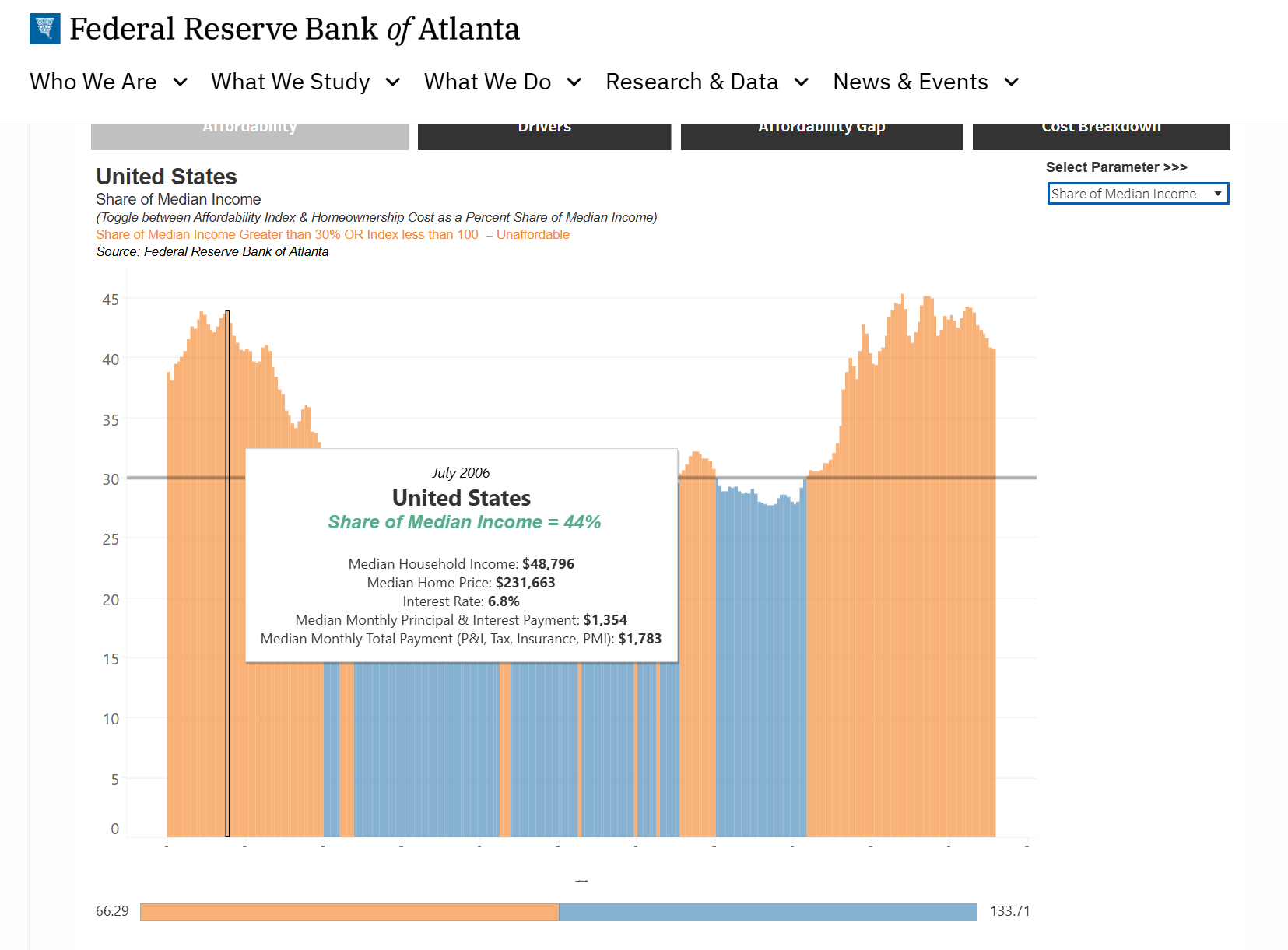

We’re now at a point where it takes 40-45% of a median household income to pay the mortgage on a median-priced house (source), i.e., back to the situation circa 2006 at the peak of the real estate bubble that burst in 2008:

This reflects the prevalance of two-income households since it looks at median household income. In the old days, the man worked and the woman stayed home (those days were so old we could tell the difference between a man and a woman!). Now everyone is in the workforce, except those smart enough to live in public housing, and the monetary fruits of all that extra toil are scooped up by real property owners. Median household income is a mixture of single-income and dual-income households. Houses are priced right now to be a stretch for the median household, which I guess means that they’re affordable for median two-income households and entirely unaffordable for a median one-income household. I asked ChatGPT “What’s the difference in median household income for one-income vs. two-income households?” and it came back with $70,137 for one-earner “family” and $127,256 for two-earner families from Census ACS data, cautioning that “Family is narrower than household. A household can be one person, roommates, an unmarried couple, etc., while a family is related people living together.” It added “For context, the overall 2024 median household income was $83,730.”

So… I’m pretty sure that my friend is wrong, which makes me+Google+ChatGPT smarter than a billionaire! There’s a first time for everything.

Also from my friend, bad news for people who love open borders and/or high birthrates, both of which necessitate new housing construction:

on the construction side, prices went crazy during [coronapanic] and never came down. It is now about 50% more expensive to build anything as compared to 2019.

During our two weeks in Ft. Lauderdale we learned that a beachfront house costs between $3 and $8 million. Most of these are approximately the same height above sea level as a crushproof cigarette pack. If the seas are rising up to swallow Florida, as the climate change doomsayers predict is imminent, why are these houses still worth so much?

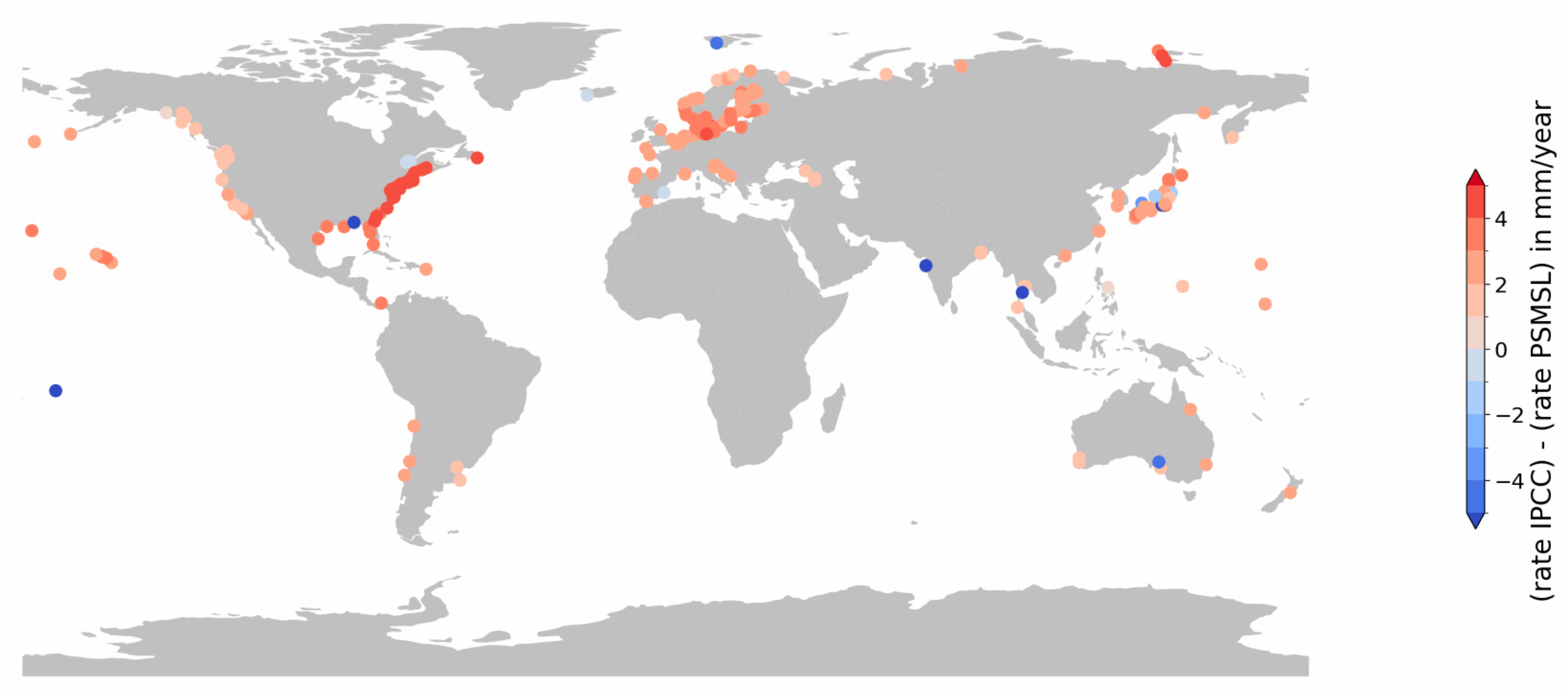

The beachfront houses of Ft. Lauderdale aren’t worth $3-8 million anymore, just as the Climate Doomers predicted. The price to live in a house that Science proves will be swept away soon is $5-40 million. Is there any new Science that could explain this meteoric rise in the nominal price? “A Global Perspective on Local Sea Level Changes” (Journal of Marine Science and Engineering 2025) looks at IPCC predictions vs. observations. The paper says that sea level worldwide is rising at about 1.5 mm per year. How does that compare with the Climate Doom narrative from the IPCC? The authors say that the observed sea level rise is somewhat lower than predicted and dramatically lower for Florida: “the overestimation along the Atlantic coast of North America is 4 mm/year to 5 mm/year; the highest overestimation found anywhere”.

The authors found little evidence of acceleration of sea level rise (Conclusions), but the same section seems to contradict the above map: “Empirically derived long-term rates of sea level rise in 2020 were in majority found to be in excess of the contemporary projected rates of rise. The current generation of projections can therefore be considered conservative”. Maybe someone here can read this more carefully and figure out how most of the rates based on local measurements are lower than the model predictions while at the same time the model predictions are “conservative” regarding doom.

[Global mean sea level] GMSL from tide gauges and altimetry observations increased from 1.4 mm yr–1 over the period 1901–1990 to 2.1 mm yr–1 over the period 1970–2015 to 3.2 mm yr–1 over the period 1993–2015 to 3.6 mm yr–1 over the period 2006–2015.

GMSL will rise between 0.43 m (0.29–0.59 m, likely range; RCP2.6) and 0.84 m (0.61–1.10 m, likelyrange; RCP8.5) by 2100 (medium confidence) relative to 1986–2005.

If we take the 1.5 mm/year rate of the new paper and a 50-year time horizon for beachfront house ownership, the sea level rises 3 inches in Fort Lauderdale over the next 50 years. If we use the 3.6 mm/year rate, the sea level rises 7 inches. In other words, the acceleration prediction by the IPCC would need to materialize in order for the sea level to rise by half a meter (20 inches).

Our house is at 11′ above sea level (approximately 3 miles inland within Abacoa) so I think we need a rise of about 7′ (2 meters) before it becomes impractical to occupy (need a bit of buffer to handle storm surges). Even under the Doomiest Doomer’s prediction, that will take so long that the house will have required reconstruction, potentially elevated by a few feet, purely due to age.

From September 2024, WSJ, regarding a (present-day) sea level house too shabby to be left standing:

(Imagine the environmental impact of dumping all of those almost-new solar panels into a landfill!)

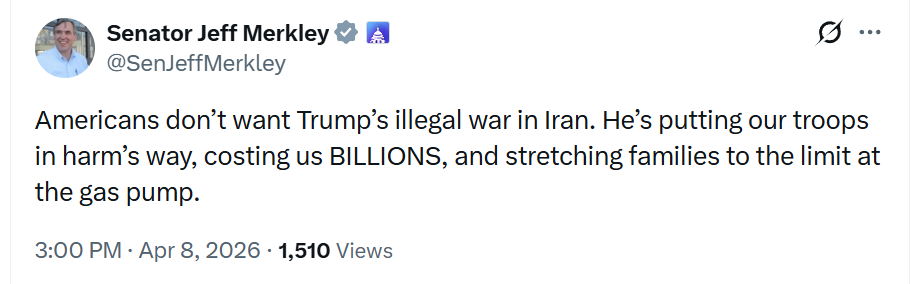

Finally, let’s look at the climate change alarmists. Here’s Democrat Senator Merkley saying “Climate chaos is the existential threat of our time. We need bold climate action now, before it’s too late” less than a year ago:

(Curiously, the tweet complaining about “Trump’s illegal war” was posted a day after Trump had announced the U.S.’s surrender to Iran (“ceasefire”), i.e., when the war was already over.)

The influential National Association of Realtors and several brokerages were ordered to pay damages to home sellers who said they were forced to pay excessive fees to real estate agents.

A federal jury ruled on Tuesday that the powerful National Association of Realtors and several large brokerages had conspired to artificially inflate the commissions paid to real estate agents, a decision that could radically alter the home-buying process in the United States.

… under the verdict, the sellers would no longer be required to pay their buyers’ agents, and agents would be free to set their own commission rates, which could be slashed in half or less. For example, a home seller with a $1 million home can now pay as much as $60,000 in agent commissions — $30,000 to their agent and $30,000 to the buyers’ agent.

Leading real-estate brokerage Compass said it has agreed to acquire rival Anywhere Real Estate for $1.6 billion, the clearest sign yet that a long stretch of lackluster home sales is sparking industry consolidation.

The all-stock transaction would create a new industry giant with an enterprise value of about $10 billion, including debt, in one of the largest deals ever in the residential brokerage industry.

Compass and Anywhere were already the first- and second-biggest brokerages by volume in 2024, respectively, according to RealTrends. Compass has about 40,000 agents, while Anywhere has about 51,000 agents at brokerages it owns and another 250,000 agents at its franchises.

I’m trying to figure out why the U.S. has antitrust laws if something like this is allowed to occur.

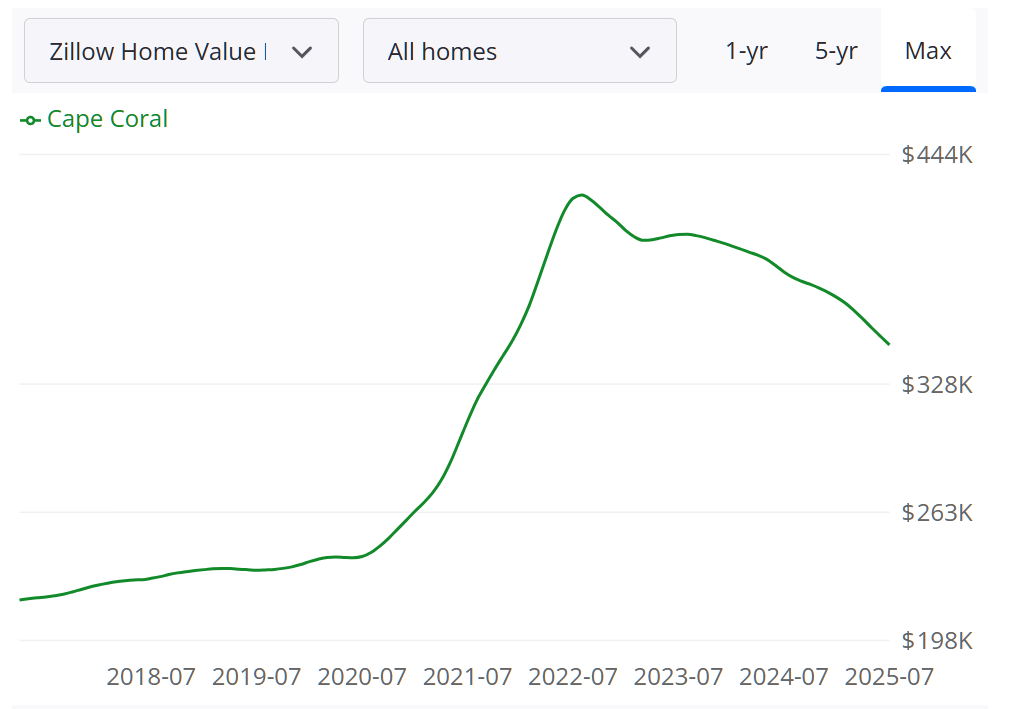

New York-based journalists love to write about how New York taxpayers shouldn’t flee to Florida and skip paying 14.8 percent state/city income tax, 8.9 percent sales tax, and 16 percent estate tax (vs. 6-7 percent sales tax in FL and 0 percent income/estate). Here’s a recent example, “The Worst Housing Market in America Is Now Florida’s Cape Coral”:

The median home price soared nearly 75% to $419,000 in three years, transforming the character of this middle-income community that for decades has catered to retirees and small investors. … Home prices for Cape Coral-Fort Myers have tumbled 11% in the two years through May

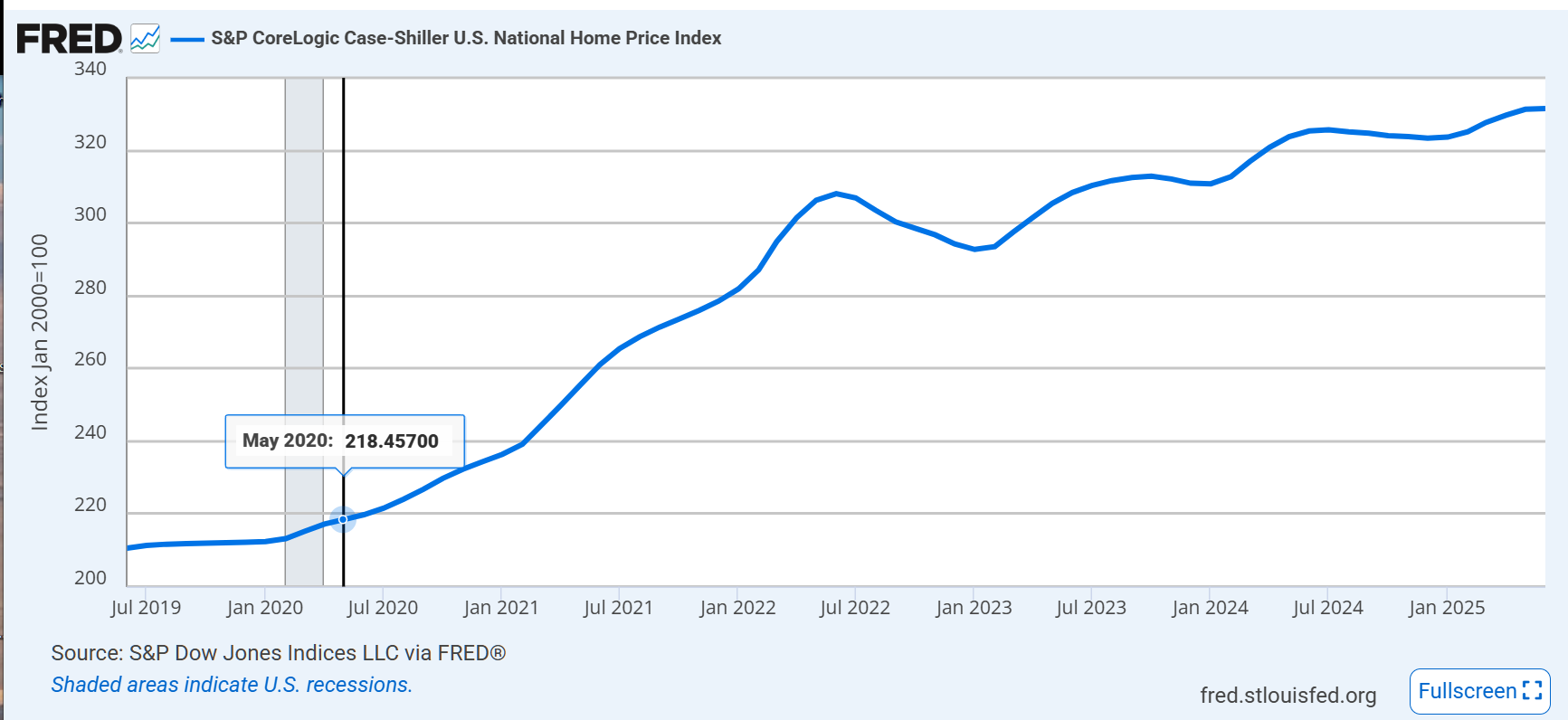

So the prices went up about 56 percent, over a five-year period. That’s before adjusting for Bidenflation. What happened in the U.S. overall? Prices went from 218 to 331 (source), a rise in nominal dollars of 52 percent:

In other words, for people who bought a house five years ago (the average tenure in a house for an American is about 12 years), what the WSJ calls “the worst housing market in America” outperformed the U.S. residential real estate market overall.

What Zillow shows is that the Cape Coral market was more volatile than the national average:

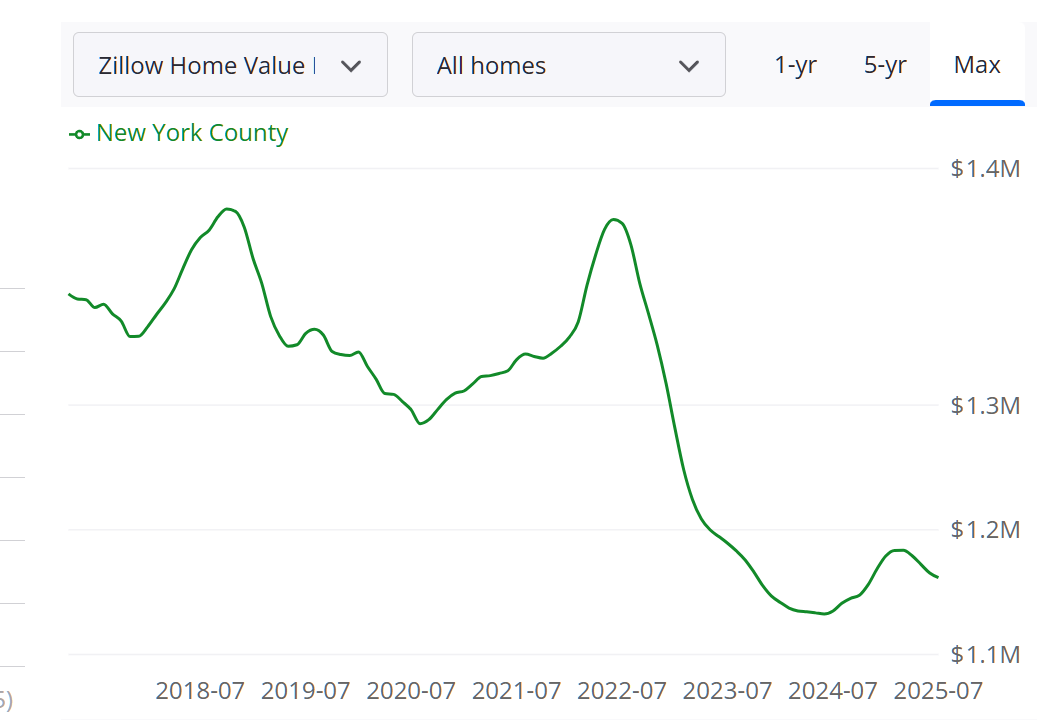

So Cape Coral actually has been a bad market for home-flippers who had the misfortune to buy in at the peak, but for the typical Cape Coral homeowner it has been a better market (albeit, not by much) than the average U.S. real estate market. What about for the elites who put the Wall Street Journal together? How has their Manhattan real estate done by comparison? Zillow:

(“New York County”=Manhattan)

So Cape Coral is objectively speaking the worst housing market in the U.S. (reported as fact/news by the Wall Street Journal rather than as opinion). At the same time, people who owned property in Manhattan fared far worse over the past 6 years or almost any time window within those 6 years.

“Naples Estate Sells for $225 Million in One of the Country’s Priciest Home Sales” (Wall Street Journal, April 25, 2025): A waterfront estate in Naples, Fla., has sold for $225 million, the second-highest home-sale price in U.S. history and a record for the state of Florida. … The DeGroote sale comes amid a rapid-fire spate of major transactions for Florida, where real-estate values have skyrocketed.

An aviation connection owns 250 apartments in the middle of the country. I asked him whether he’d lost a lot of money during coronapanic when nobody had to pay rent and he was barred by order of the CDC from evicting anyone. “No,” he said. “Nearly all of my tenants kept paying and, in fact, many of them applied for and received government assistance to pay their rent. I already had 20 percent Section 8 vouchers and ended up with about half of my income coming from the government.”

He took the opportunity to refinance his properties at a 2 percent rate and also substantially raised the rents that he was charging (i.e., his costs fell and his revenue soared). He estimates that his property doubled in nominal value between 2019 and today. He raised rents by 50 percent.

Who else got rich? “The local car dealer [in his small town] bought a Phenom 300 and a Bell 407” (that’s $15 million worth of aircraft; the Phenom 300 is made by Embraer in Brazil)

What else has been working for him? Open borders. “I love having Latinos as tenants,” he said (sorry about the hateful failure to use proper English (“Latinx”), but it is a direct quote), “but sad to say that the English-speaking tenants get upset if there are too many Latinos in their complex. They complain about Mexican music being played and noise. I don’t want to be racist and exclude people on the basis of being Hispanic because it makes other tenants upset.” Has the rising cost of labor eroded his increased profit margin from the 50 percent rent boost? “No,” he replied. “White people have pretty much stopped working, but there are plenty of hard-working Latinos. I wish that I spoke Spanish because then I could do a better job explaining what I need.”

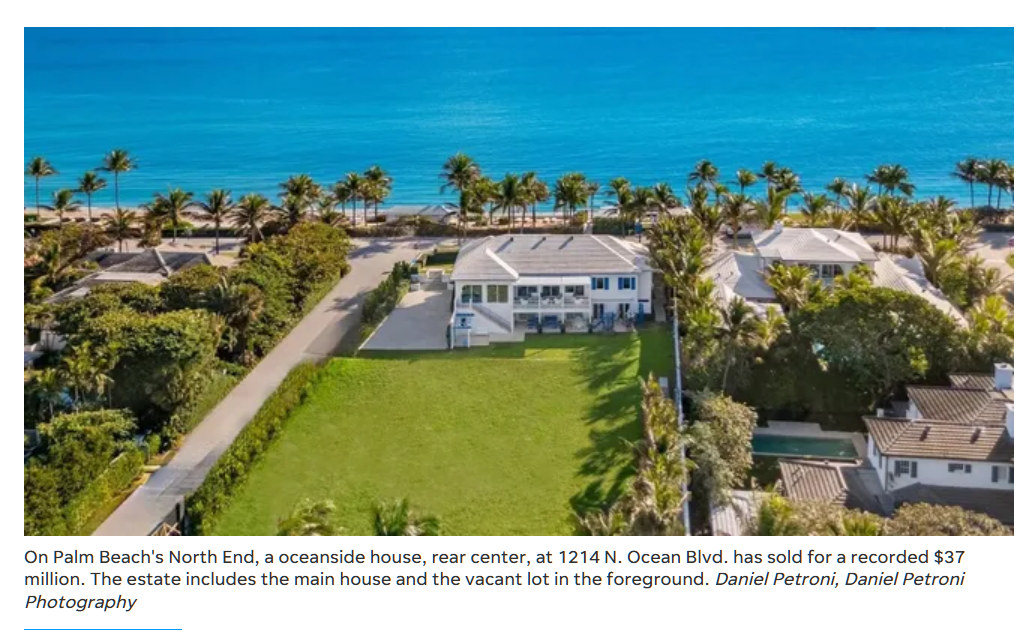

A never-lived-in oceanfront mansion that quietly sold for $110 million last year is to be torn down and replaced with a new property.

The mansion, built in 2016 at 1071 N. Ocean Blvd, Palm Beach, is owned by a company linked to cosmetics billionaire William P. Lauder.

He owns an empty lot next door and is believed to want to combine both parcels of land before building his dream home, just six miles from former President Trump’s Mar-a-Lago.

The home was originally purchased for $40.42 million by Philadelphia businessman Vahan Gureghian and his wife, Danielle, an attorney, but they never moved in.

There is even room for a two-lane bowling alley in the basement – although it’s soon to be destroyed by the wrecker’s ball.

He purchased that lot, at 1063 N Ocean Blvd, for $25.4 million in April 2020 at which point he demolished the existing home which had stood there since the early 1960s.

(What kind of engineering was involved to make a watertight basement? Almost nobody in Florida has one.)

To make our envy even more intense, the article includes a photo of the dilapidated eyesore:

What does the guy who is throwing out a 6-year-old 36,000-square-foot house have to say about our beloved planet? A 2021 talk from the committed environmentalist:

During the pandemic, concerns about the environment have intensified and Lauder noted that, at this point, sustainability is no longer a choice for companies.

“We have to think about what we make and sell from cradle to grave,” he noted. “How can we get more recycled material in our packaging? How can we reduce the use of plastic and other components that end up in landfills?”

The entire house will go into a landfill, but that’s okay because very little of it is plastic?

It’s all about the Science:

Sustainability and science go hand-in-hand. Lauder said…

The Estée Lauder Companies (ELC) announced on November 2nd that it has achieved Net Zero emissions and sourced 100% renewable electricity globally for its direct operations, reaching the target it set on joining RE1001.

Building upon this achievement, the company has also met its goal to set science-based emissions reduction targets for its direct operations and value chain, positioning the company to take even more decisive action against climate change in the coming decade.

The Estée Lauder Companies commits to reduce absolute scope 1 and 2 GHG emissions 50% by 2030 from a 2018 base year. This target is consistent with reductions required to keep warming to 1.5°C, the most ambitious goal of the Paris Agreement. The Estée Lauder Companies also commits to reduce scope 3 GHG emissions from purchased goods and services, upstream transportation and distribution, and business travel 60% per unit revenue over the same timeframe.

It was Science who said “toss that 6-year-old house into the landfill”!

So we started off sick with envy, but ended up learning something profound about the role that each of us can play in saving Spaceship Earth.

As loyal readers are aware, when it comes to homeownership I am a hater. The culture of homeownership is a huge drag on the U.S. economy, in my view, for the following reasons:

homeowners spend a lot of time working as amateur property managers, e.g., arranging maintenance or actually performing maintenance, that is much more efficiently done 100-600 units at a time

the high transaction costs, e.g., 5 percent real estate commission, discourage people from moving in response to the availability of better job opportunities

(This is not to say that I hate the single-family home as a living space. But I would think we’d be way more productive as a society if our single-family homes were owned commercially and managed professionally or, at the very least, owned in a condo-style arrangement where we didn’t have to touch anything beyond the interior.)

The “high transaction costs” in the second bullet point above are now vastly higher due to 2022 having become the Year of Mortgage Rate Drama. Someone who locked in a 3% rate, either via an initial purchase or a refinance, is sitting on an annuity that ends the minute he/she/ze/they decides to sell the house and move closer to where the better jobs are, potentially eliminating all of the economic benefit of switching jobs.

Housing inventory has risen from record lows earlier this year as more homes sit on the market longer. But the number of newly listed homes in the four weeks ended Sept. 11 fell 19% year-over-year, according to real-estate brokerage Redfin Corp. That is an indication that sellers who don’t need to sell are staying on the sidelines, economists say.

Larry and Corina Lewis of Tarrytown, N.Y., have two children and expect to need a bigger home in the next few years. But their current 30-year mortgage rate is 2.75%.

“The thought of giving this up in order to pay double in interest, that’s a nauseating thought for me,” Mr. Lewis said. Even if the average mortgage rate falls from its current level, he said, “I still don’t see it ever getting quite that low.”

The lack of housing inventory is one of the major reasons home prices have remained near record highs, despite seven straight months of declining sales as interest rates have roughly doubled since the start of the year.

Economists say it is difficult to predict how much the increase in mortgage rates could reduce home listings, because rates haven’t climbed this rapidly in decades.

Related:

“More Residents Looking to Leave San Francisco Than Any Other Major U.S. City, Report Finds” (Mansion Global (sister publication to WSJ), 9/20/2022): Despite life returning in force to big cities across the U.S., residents are still looking to leave them, and in even greater numbers than they were last year … In July and August, residents of San Francisco were the biggest flight risk. All told, San Francisco had a net outflow of 40,432 over the two summer months, a measure of how many more Redfin users looked to leave the city rather than move to it. Next on the list was Los Angeles with a net outflow of 34,832, followed by New York at 26,786. Washington, D.C., and Boston rounded out the top five. [Other than extended periods of public school closure, what do these cities have in common?] Miami was the most popular migration destination, “continuing a year-plus streak of the South Florida metro taking the number-one spot,” the report said.

Speaking of South Florida, here’s a fan of relocation to Jupiter. Mindy the Crippler’s priorities for a neighborhood are squirrels, rabbits, squirrels, rabbits, and, more importantly, squirrels: