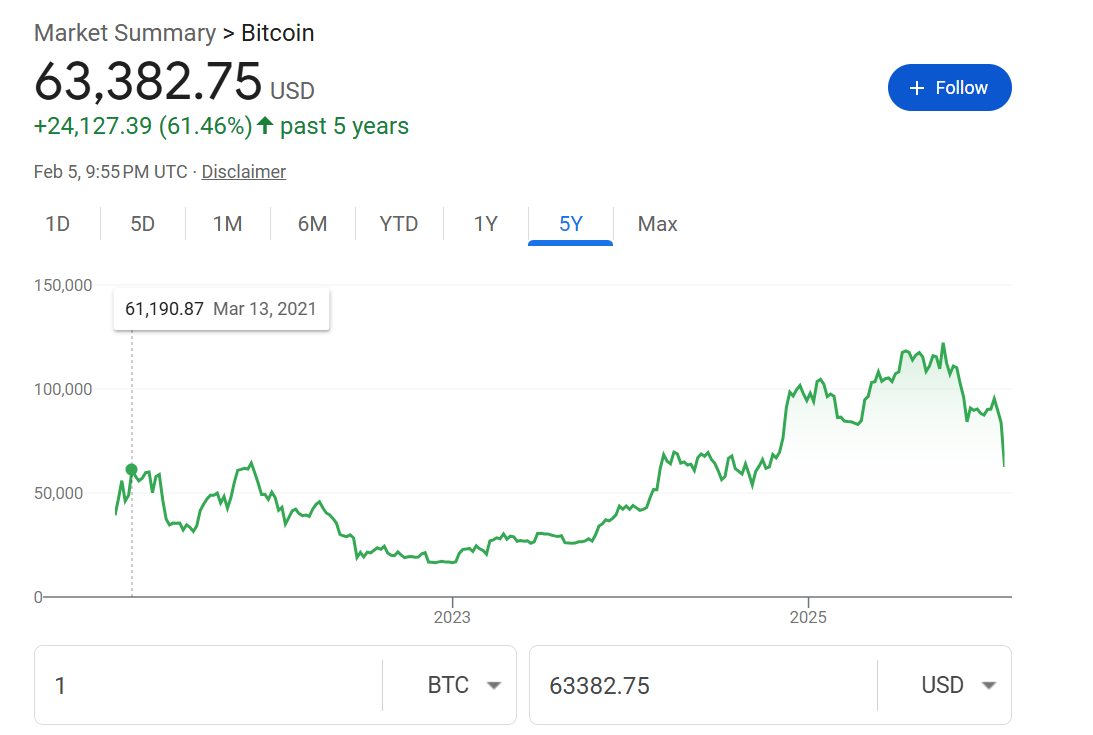

The news in the Bitcoin world isn’t all bad. The tensor processing units (proprietary Google LLM chips) behind Gemini 3.0 fixed our Bitcoin v. Medical School page just in time for the Big Slide:

(adjusted for Bidenflation, Bitcoin is now down substantially from the mid-March 2021 price when everyone was filled with hope regarding the Biden-Harris administration leading us forward and out of the bad times of the Trump dictatorship (v1.0))

I wonder what this means for the Cirrus waiting list and aircraft values in general. A crypto investor seems like a natural personal airplane customer: (a) independent personality, (b) not averse to irrational purchases, (3) maybe a need to go back and forth to Puerto Rico frequently.

Stake in the ground: I’m not going to sell any Bitcoin!

Separately: “This Bitcoin crash is worse than a divorce. I lost half of my money and my wife is still around.” (source)

Readers: who has favorite X posts to share? I’ll start:

In times of market turmoil and geopolitical tension, you need to find safe assets… pic.twitter.com/2Y5GUHyDS5

Countries still have intelligence, counterintelligence, and all of the other Cold War-era espionage systems, right? How is it possible for Government A to have a secret that Government B wants? What stops Government B from

publicizing a Signal tip line

taking messages from a cash-hungry employee of Government A

after determining that the messages, and any attached documents, are genuine, paying out some cryptocurrency to the rat

? In the old days it was difficult to betray one’s government. A military officer would have to find a way to meet a foreign government’s spies, not get followed to the meeting spot, receive a briefcase full of cash or trust that money had been deposited into a Swiss bank account, etc. Today, on the other hand, unless Government A has a way to read Signal messages on every device and also map its citizens to crypto wallets how can Government A prevent its officials and employees from selling secrets?

Loosely related… imagine how inflated a Californian’s head would have to be for him/her/zir/them to imagine that he/she/ze/they was an expert on “the preservation of Democracy” (from Los Angeles):

• It has destabilized society. Society works best if people can be satisfied from working a normal job for normal wages. People will be less inclined to be satisfied with this, if they see their…

[Bitcoin and similar have] given utility to some individuals, by making them rich. But since no new service or good has been created in the world, this comes at the price of making everyone else a little poorer.

Can this be true? Crypto has burned up a huge amount of electricity so it made at least some electric utilities richer as well as holders of crypto currency becoming richer. Sam Bankman-Fried and at least one of his sex partners are making the prison-industrial complex a little richer. But would the world overall be better off if crypto had never been developed or used? Think of all of the important mRNA vaccines we could have enjoyed if some of our best and brightest minds weren’t sidetracked into crypto fever.

The same author on X explains why we have to hear 24/7 hype from Bitcoin holders whereas those who own Malaysian ringgit are mostly peaceful: “… for people who hold it, it is pure economic advantage to hype it. This predictably creates a landscape of self-reinforcing hype.”

A problem I have with cryptocurrency, is that for people who hold it, it is pure economic advantage to hype it. This predictably creates a landscape of self-reinforcing hype.

It will also be in people's interest to uncritically promote the hype. And so on.

“LUIGI hits all-time high at $60M market cap after Luigi Mangione’s arrest for murder” (Crypto News): The Luigi Inu (LUIGI) token first started gaining traction following Mangione’s arrest in Altoona, Pennsylvania and charged on Dec 9. The token’s market cap reached $29 million before it rocketed higher to $60 million, after the arrest was confirmed. Originally launched by anonymous crypto traders, the token is trending on Raydium, the automated market maker built on Solana. The connection between Mangione and the memecoin lies in the fact that his arrest and the subsequent media attention have significantly boosted the token’s popularity and value.

A sad day for Joe Biden’s second-largest donor (NYT):

Could the federal government reduce the budget deficit by selling license plates and other collectibles made by Sam Bankman-Fried? If he’s going to be in prison for at least a few years why not start up a line of Effective Altruism plates at $5,000, each one signed by Mr. Bankman-Fried? (partnership with the states, of course, and some of the profits shared with each state that participates)

Separately, when and by which president might Sam Bankman-Fried be pardoned?

Also, with Bitcoin now at $70,000, is it possible that Bankman-Fried, if left alone, could have paid everyone back? FTX melted down in November 2022 when Bitcoin was worth about $20,000. What if Bitcoin had gradually moved from its $65,000 November 2021 price to today’s $70,000? Would FTX have been okay despite the diversions of funds and the girlfriend’s investment decisions?

Let’s see if I got the Sam Bankman-Fried (SBF) trial right… All of the co-conspirators who enabled the fraud at FTX agreed to testify against SBF in exchange for reduced punishment. They all then testified that everything was SBF’s fault and they were helpless puppets (somehow incapable of quitting FTX or exposing the fraud before it got bigger). Now SBF has been found guilty and will be sentenced to up to 110 years in prison in March 2024.

Over the four weeks of his trial, Bankman-Fried watched a parade of people he once considered his closest confidantes testify against him. They included friends from math camp and MIT who became his co-founders; and, critically, his ex-girlfriend and trusted business adviser, 28-year-old Caroline Ellison.

The most damning evidence against Bankman-Fried came from Ellison, who testified for the prosecution over three days.

As both the CEO of Alameda and Bankman-Fried’s romantic partner for two years, Ellison was uniquely positioned to comment on what was happening within the tight inner circle of Alameda and FTX executives, many of whom lived together in a $30 million luxury apartment in the Bahamas.

Ellison’s at times emotional testimony offered a narrative of events in which virtually every decision at both Alameda and FTX came down to Bankman-Fried, who founded and was the majority owner of both firms. A common refrain from Ellison, when asked who directed her to carry out various actions, criminal or otherwise, was a variation on the words “Sam did.”

From reading early reports on the meltdown, I got the impression that it was Ms. Ellison’s investment losses that had created the necessity for the fraud. Did that turn out to be false?

What happens to all of the co-conspirators, without whom SBF couldn’t have stolen a dime? Back in December, the New York Post predicted that Caroline Ellison might get off with probation.

‘I’ve had cooperating witnesses who did get jail time, but it’s the exception not the rule.’

When Wang testified, prosecutors asked at the end of their examination how many years he was hoping to be sentenced. “Ideally hoping for no time,” he replied, which prompted some quiet laughter in the courtroom.

If this plays out as predicted, do we think it is fair? One altruist goes to prison for 100 years while co-conspirators who stole at least $millions for themselves are free to move on to the next scam? If SBF’s guilt had been challenging to establish, maybe this would make sense in some practical way, but it didn’t seem like a tough case for prosecutors to make.

Related:

“SBF’s mom told him to ‘avoid’ disclosing millions in FTX donations to her pro-Dem PAC: suit” (New York Post, Sept 22, 2023): Bankman-Fried has been accused by federal prosecutors of funneling $100 million in political donations through “straw donors” including Nishad Singh, the former head of engineering at FTX and sister company Alameda Research, and Ryan Salame, another former top executive at the company.

Lawyers, accountants, consultants, cryptocurrency analysts and other professionals have racked up more than $700 million in fees since last year from the bankruptcies of five major crypto firms, including the digital currency exchange FTX, according to a New York Times analysis of court records. That sum is likely to grow significantly as the cases unfold over the coming months.

A man who arrived in New York City two months ago from Venezuela has randomly attacked at least three strangers and two cops, and gotten arrested – and released – six times on 14 different charges, police and sources said.

Daniel Hernandez Martinez, 29, arrived on June 27 and allegedly committed his first crime the following day.

On Aug. 21, he violently attacked a woman in Midtown, cops said. He “grabbed a stranger by the hair, dragged her across the floor and kicked her,” and smashed her phone on West 45th Street around 1 a.m., court documents show.

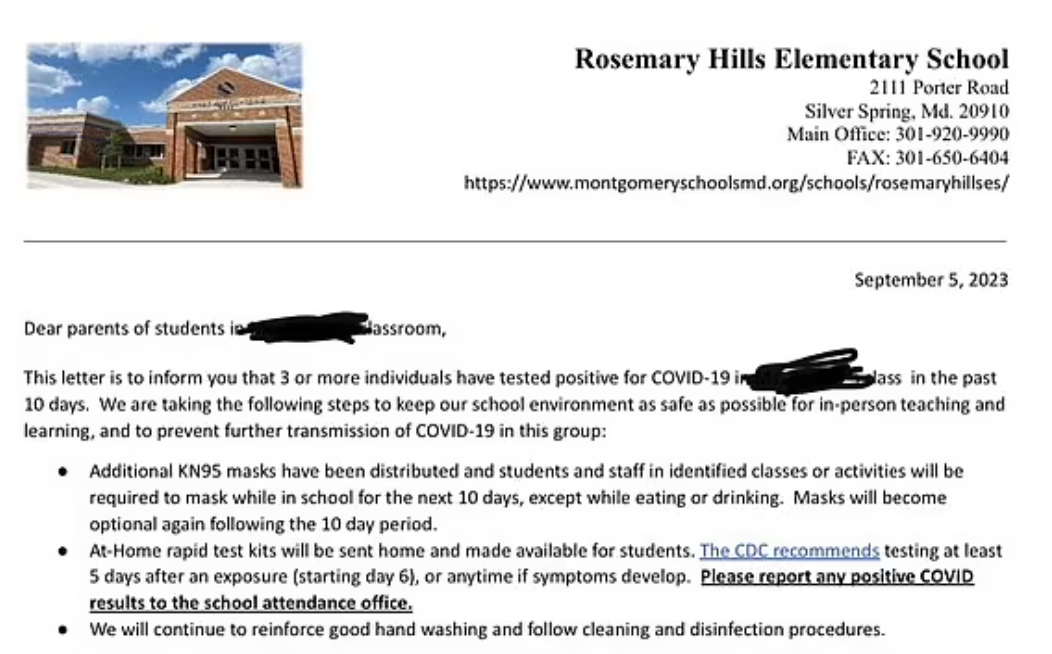

In a letter sent to parents on Tuesday, Rosemary Hills Elementary School principal Rebecca Irwin Kennedy said she made the move after ‘three or more individuals’ caught the virus in the last ten days.

She demanded students don thick N95 masks to ‘keep our school environment as safe as possible’, despite a recent study finding the mask may expose users to dangerous levels of toxic chemicals.

And while even embattled medical guru Dr Anthony Fauci admits there is a lack of evidence the masks stop the spread of Covid, Kennedy told parents the N95s will only become optional after 10 days.

This is my old school district, as it happens, Montgomery County Public Schools. It’s interesting that there is no explanation of how SARS-CoV-2 will be stopped if the students remove their masks “while eating or drinking”. The letter from the principal doesn’t mention any changes to lunch procedures. So the kids all sit in the classroom together wearing masks and then they all sit together at lunch not wearing masks?

What the Maryland principal did, of course, would be illegal under Florida law. Not contrary to a governor’s order, but illegal under a statute passed by the legislature. Third graders in Florida could tell the fearful Fauci-denying adults where to put their N95 masks.

It’s been two months since Sam Bankman-Fried returned to the U.S. (BBC). How is my prediction that Joe Biden will appoint him as U.S. Treasury Secretary and that he will be confirmed by Senate Democrats looking? Any other news from this cryptocurrency trailblazer?

Most of the $121 million in real estate that Mr. Bankman-Fried and his Stanford professor parents owned is within gated communities, according to my friends in Nassau, but they did drive me, in January, to see the police station and courthouse:

The locals say that the prison where our future Treasury Secretary was held is not worth the 20-minute drive for a photo. “All that you can see is a wall with a sign.”

How is everyone’s favorite Effective Altruist doing? Regardless of how the legal and financial situation gets untangled, I’m wondering about the linguistic aspects. Could “Bankman-Fried” become an English verb?

“I’m going to try to Bankman-Fried the investors” would mean to tell people about one’s charitable and political plans for wealth to be acquired using their money.

“I Bankman-Frieded the local election” would mean “gave money to ensure a Democrat victory.”

We can also look at Sam Bankman-Fried’s mom explaining complex ethical issues and how they could be handled (“Frieded”?):

(A 2014 Stanford Center for Ethics in Society presentation. The tax-exempt institution for exchanging ideas seems to have decided that it wouldn’t be Tethical to allow comments from viewers. As a test, I posted the following:

Great to have Sam Bankman-Fried’s mom’s perspective on this complex topic. I am running a bank right now and am trying to figure out whether it is ethical to steal all of the money that customers have deposited with me. I need some help from the big brains of Stanford.

Sam Bankman-Fried must have had a few loose $millions, in the same way that many of us have $500 credit balances in miscellaneous accounts that we’ve forgotten about. Why didn’t he gather these up and fly to Moscow as soon as the stories broke regarding his crimes?

Plainly Harvey Weinstein is not going to be working in Hollywood again. In any event, at age 65 he has reached normal retirement age. If he stays in the U.S. he risks prosecution for whatever happened during meetings with actresses in California, Connecticut, New York, and perhaps some other states. Even if evidence against him is weak, what prosecutor could resist becoming famous by bringing charges? (See Window into American criminal justice system from the daycare sexual abuse trials of the 1980s for some stuff that influences prosecutors in deciding whether to pursue a case.)

Harvey could probably beat the “beyond a reasonable doubt” rap a few times, given that most of the situations were private encounters and there were no unbiased witnesses. … Why would a 65-year-old with money want to stick around to spend the remaining years of his life as a defendant?

Harvey, of course, did not take the advice from my blog. On May 25, 2018, therefore, he was forced to turn himself in to the NYC police and surrender his passport. Harvey Weinstein will be in prison for the rest of his life rather than seeing if foreign actresses have the same flexible attitude about what is reasonable to do with a fat old guy in exchange for a role as American actresses had.

Perhaps Sam Bankman-Fried does not read this blog, but why wasn’t it obvious to him that he would likely have a much better life going forward in Moscow than in a U.S. prison? (It seems safe to assume that the Russians wouldn’t be in any hurry to extradite the 2nd largest donor to Joe Biden and wouldn’t cry about some American crypto enthusiasts losing $billions. And perhaps even Joe Biden and fellow Democrats who got money from SBF wouldn’t be inclined to pressure the Russians to send him back either.)

The front desk gals at the Marriott in Moscow (2017) where Bankman-Fried would have been welcomed:

The downtown Moscow shopping mall where he could replace all of the stuff that he left behind in mom and dad’s Bahamas houses:

Sam Bankman-Fried was notable for his ethical approach to doing business, particularly “effective altruism”. New York Times, May 2022:

He lives modestly for a billionaire and has pledged to give away virtually his entire fortune, which currently stands at $21.2 billion, according to Forbes. A growing force in political fund-raising, he has a super PAC that recently gave more than $10 million to a Democratic congressional candidate who supports some of his philanthropic priorities. … a straight-talking brainiac willing to embrace regulation of his nascent industry and criticize its worst excesses.

Both Mr. Bankman-Fried’s parents are Stanford Law School professors who have studied utilitarianism, an ethical framework that calls for decisions calculated to secure the greatest happiness for the greatest number of people. “It’s the kind of thing we’d discuss in the house,” said Mr. Bankman-Fried’s father, Joseph Bankman.

As might be expected for a young man raised on dinner-table discussions of moral theory, Mr. Bankman-Fried is also an admirer of Peter Singer, the Princeton University philosopher widely considered the intellectual father of “effective altruism,” an approach to philanthropy in which donors strategize to maximize the impact of their giving.

Mr. Singer, whose scholarship helped inspire the movement, said he has gotten to know Mr. Bankman-Fried over the years and called his philanthropy “wonderful and really quite amazing.”

(Speaking of those donations to Democrats, will Joe Biden and other politicians refund the money that they received, fraudulently, from FTX customers? The Securities and Exchange Commission says that FTX and Sam Bankman-Fried were stealing money from customers all the time:

in reality, Bankman-Fried orchestrated a years-long fraud to conceal from FTX’s investors (1) the undisclosed diversion of FTX customers’ funds to Alameda Research LLC, his privately-held crypto hedge fund; (2) the undisclosed special treatment afforded to Alameda on the FTX platform, including providing Alameda with a virtually unlimited “line of credit” funded by the platform’s customers

The Democrats are now in the position of Ponzi scheme investors who got paid from other investors and the typical remedy for that is clawback. Joe Biden and fellow Democrats would return their ill-gotten money so that the small depositors at FTX can get some of their money back.)

Who could have predicted all of this? The writers of the HBO series Silicon Valley! In Season 6, which aired in 2018, Gavin Belson, the Hooli founder, introduces a hollow code of ethics for tech companies: “tethics”. Facebook and other California behemoths eagerly sign onto these empty words.