The Florida Democratic primary for Senate is on August 18. One baffling aspect: Alex Vindman not only moved to Florida during the tyranny of Ron DeSantis (in 2023), but now the foreign-born carpetbagger is trying to take away a Black woman’s job in the Senate primary. Vindman says that he has a 15-year-old daughter:

I'm running for Senate to lower your costs.

So that young people like my 15-year-old daughter can afford to build a life in Florida. So that people on fixed incomes like my 94-year-old dad can afford to stay here. pic.twitter.com/HaQqU95FRG

Why would a noble liberal migrant move to Florida? He talks, above, about a 15-year-old daughter. The goal is for this girl to stay in tax-free Florida for the rest of her life, thus denying the virtuous Democratic-ruled states of much-needed tax revenue. Said daughter can’t be safe in Florida because life-saving abortion care isn’t available after 6 weeks of a pregnant person’s pregnancy (Vindman is on record as a passionate supporter of abortion care). Because she’s under 18, life-saving gender-affirming care isn’t available. Vindman is literally killing his/her/zir/their daughter. State law won’t change to became safe even if the carpetbagger wins the Senate seat.

Most confusing, for a member of a party that champions the advancement of Americans identifying as “women” and the advancement of Americans identifying as “Black”, the apparently white male carpetbagger is trying to take away the important Senate job from a Black woman:

The number of leadership jobs in the U.S. is more or less constant (absolutely constant with respect to the number of senators). The only way for members of victimhood groups to advance is for white heterosexual males to retreat into subordinate roles. How can there reasonably be even a single white heterosexual cisgender male running for any office as a Democrat? And how could a virtuous Democrat reasonably make the decision, in 2023, to move to any Red State? (Vindman even moved an elderly parent to Florida, thus avoiding paying state estate tax and preserving the “generational wealth” that Democrats oppose.)

Early voting has begun for the Florida primary election. I’m registered as a Republican (can’t go back to the Party of Fauci!) and the choices are a little unsettling.

Choosing a governor would be easy if Ron DeSantis had endorsed someone, but the GOAT has kept quiet.

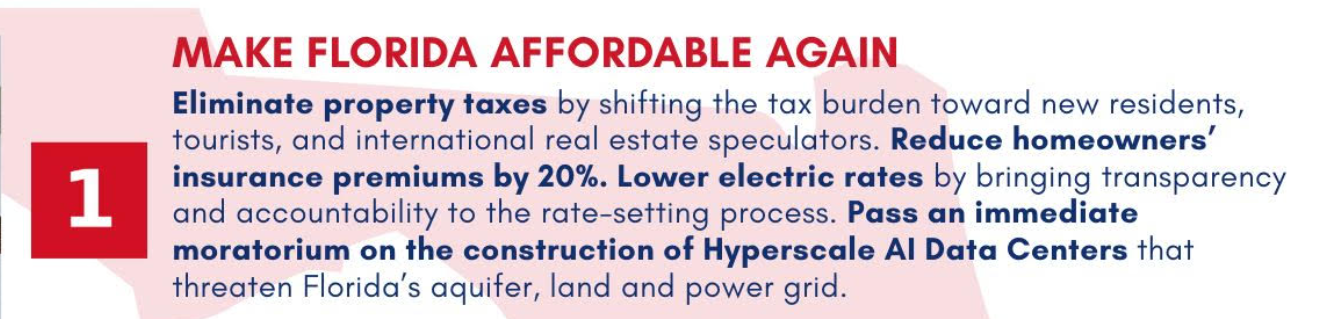

Let’s start with Paul Renner. He attended a liberal arts college, served in the Navy, and then went to University of Florida law school. He was Speaker of the House during part of the DeSantis administration. His campaign web site frankly is either the work of an insane person or, perhaps, a smart person who believes that everyone who reads it is stupid.

“Shift the tax burden to international real estate speculators”? How can that work in most of Florida’s 67 counties? International buyers are supposedly roughly 5% of the total dollar volume in Florida, but they’re heavily concentrated in a handful of counties.

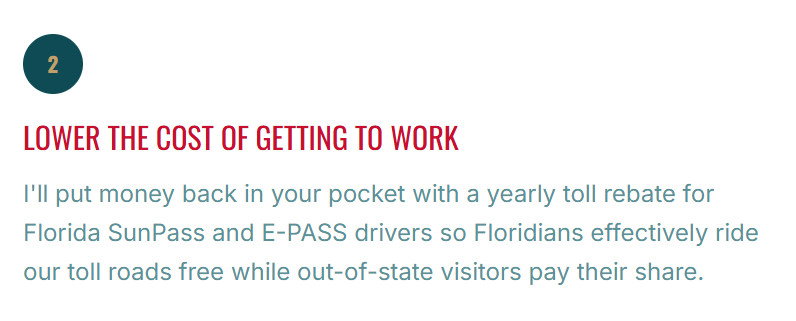

Jay Collins is the current Lieutenant Governor, appointed about a year ago by Ron DeSantis when Jeanette Nuñez left to become head of Florida International University. He has a distinguished military career, including serving as a Green Beret. His campaign site is a little less insane. He wants to exempt a larger amount of homestead residents’ home value from property tax, which I think is a terrible idea (there is already a huge discrepancy between what long-term residents pay and what new arrivals or second-home owners pay because homesteads are taxed at their purchase price plus a maximum of 3% per year appreciation or CPI, whichever is less; DeSantis is at risk of losing his GOAT title, in my view, for trying to further derange Florida’s property tax system via a ballot question in November.).

This seems like a terrible idea for anyone who hates traffic jams:

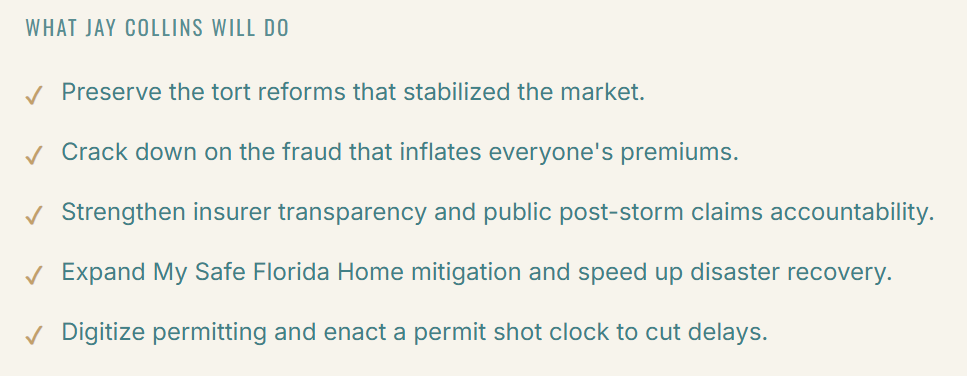

Collins promises to lower insurance costs, but not by a specific percentage and mostly via the “tort reforms” (making it tougher to sue insurers and get all legal fees paid) that were enacted in 2022 and actually did bring down premiums:

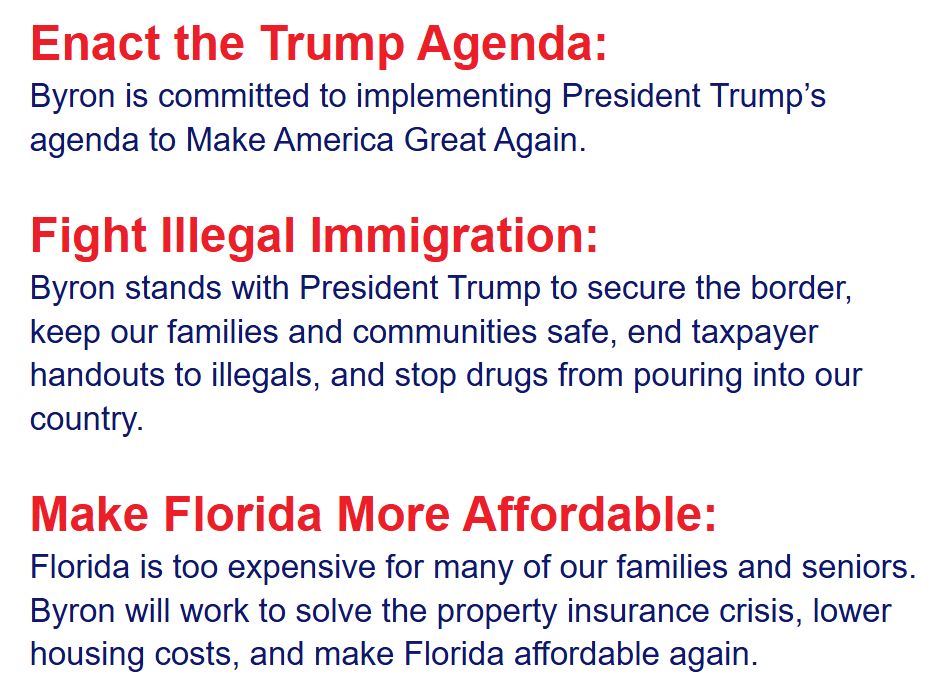

Next we turn to Byron Donalds, currently in Congress representing some of the world’s richest people (Naples, Sanibel), which is ironic because Wikipedia says that he grew up in Crown Heights, Brooklyn under the care of “his single mother.” His issues page:

“Enact the Trump Agenda”? How is the governor of Florida going to surrender to the Islamic Republic of Iran?

“Make America Great Again”? That actually works against Florida’s interests. What helps Florida is when New York City, Boston, Chicago, San Francisco, and Los Angeles fall apart and/or go into a Fauci-suggested lockdown. If the foregoing centers of American wealth were as nice as West Palm Beach and Sarasota, there would be no reason for rich people to move to Florida.

“taxpayer handouts to illegals”? Florida doesn’t do a lot in this area, I don’t think, other than pay for health care when the undocumented show up at emergency rooms (and how would we cut that off?). The real solution, though, would be to help the undocumented migrate onward to New York and Maskachusetts where they’re guaranteed a taxpayer-funded lifestyle. Donalds doesn’t seem to propose that.

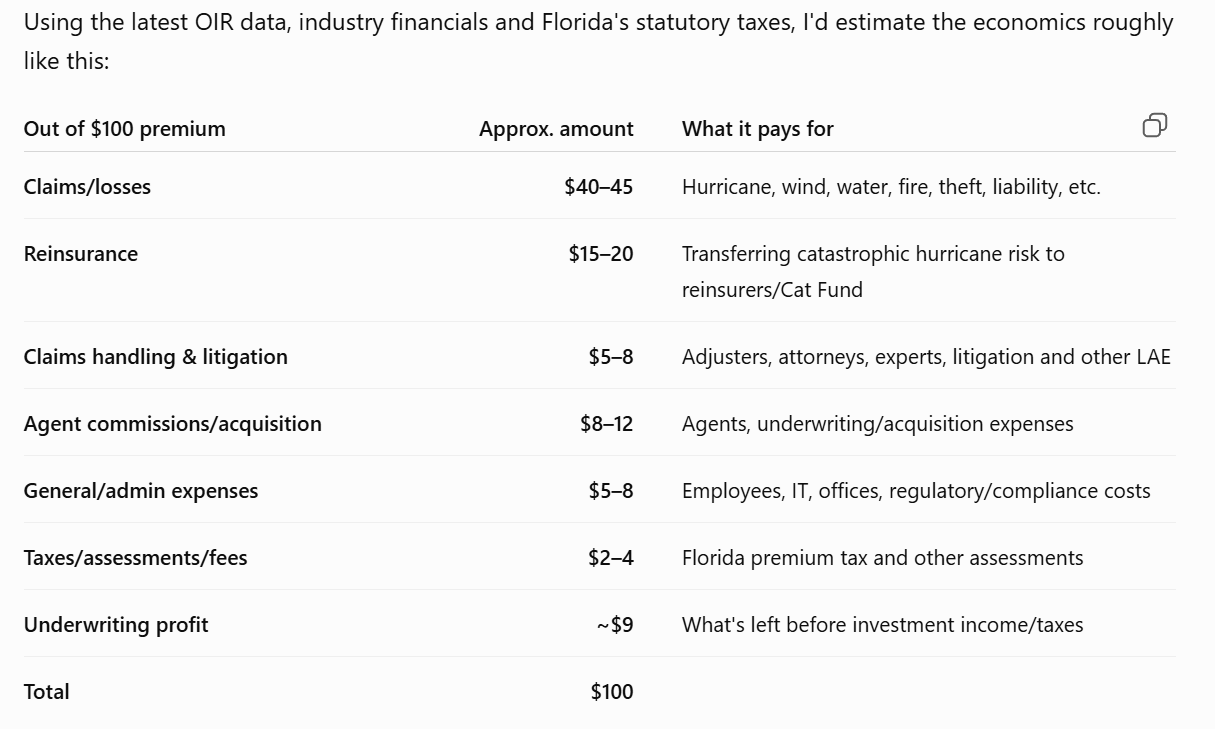

“property insurance crisis”? Maybe we could lose another 10% on premiums if all disputes between homeowners and insurers were moved into a specialized and streamlined resolution system staffed by arbitrators who actually knew something about home construction and repair. Beyond that, though, how is it a “crisis” if rates are higher than in some other states because of hurricane risk? ChatGPT’s estimates of available juice to squeeze from the insurance lemon:

(Look how expensive agents are! Maybe this is an argument for socialism. If there were just one insurance company, run by the state, rates could come down by about 20% because there would be no agents and no underwriting profit! What could go wrong?)

I hate to say that the candidate endorsed by Donald Trump is the least insane of the above, but perhaps he is! Mostly, I’m saddened that the only way to win an election in the U.S. seems to be promising people free stuff, absurd stuff, and impossible stuff. Average IQ in the U.S. is falling, but maybe this isn’t a new phenomenon. After all, when Lyndon Johnson and Congress in the 1960s decided to simultaneously expand the welfare state (Medicaid, Medicare, public housing, food stamps) open the borders (Hart-Celler), that was implicitly a promise that the U.S. would be infinitely rich forever. When FDR and Congress set up Social Security in the 1930s and paid the first beneficiary 1000X what she’d contributed via taxes that was tantamount to a “free lunch” promise.

The choice for Senate is much simpler. DeSantis-appointed fifth-generation Floridian Ashley Moody is the incumbent and everyone seems to like her. (Well, maybe the undocumented don’t like her because she’s in favor of border security and, when that fails, ICE. If she were in the Islamic Republic of Michigan running against Abdulrahman Mohamed El-Sayed she’d probably try to deport him to Egypt.)

Wilton Simpson is running to retain his job as Agriculture Commissioner. I won’t be voting for his opponent, Matt Taylor, because he styles himself “Matt the Welder” and that reminds me of “Graham Platner the Oyster Farmer.” Also, Matt the Welder is opposed to “government aerial mosquito spraying”, according to ChatGPT. One of the great things about our life in Florida has been that we’ve cut our DEET use by 90% compared to when we lived in the Boston suburbs (tick-infested 7 months per year and horrific mosquitos for 3-4 months per year). If Palm Beach County wants to use an Airbus A380 filled with whatever kills mosquitos I am all for it! (see Indigenous Peoples’ Day and the Mosquito for a recommendation of a great book on how horrible this insect is; see also Kill them all (mosquitoes) with genetic engineering and let God sort out the mutant survivors) Note that ChatGPT might be hallucinating/lying. Taylor seems to be hostile to herbicides and perhaps some of his supporters assume that he will also be hostile to insecticides. Regardless, “welder” is too close to “oyster farmer” for comfort, unless of course one is a progressive female looking for some action…

There’s also a race for a judge. Schnelle Tonge v. Jacob Noble. Ms. Tonge is endorsed by a lot of Palm Beach County officials while Mr. Noble is endorsed by the police. Noble seems to have a lot more litigation experience, e.g., he’s admitted to practice at the U.S. Supreme Court, a federal appeals court, and three federal district courts.

Update: I biked over to Florida Atlantic University’s Jupiter (Abacoa) campus and voted early. There was a substantial staff and nobody in line. I was offered the opportunity to use the voting machine, which ultimately prints a paper ballot, in English, Spanish, or Haitian Creole. It seems that, in our infinite political wisdom, we’ve created a huge class of eligible voters (U.S. citizens) who can’t understand the most basic English. ChatGPT explains that someone might be a birthright citizen and never learn English due to being taken back to Haiti or wherever as a baby. The anchor baby returns at age 18, let’s suppose, and decides to vote. We also hand out citizenship to people who are over 50 without requiring them to pass the English test that is normally required for naturalization. Finally, unlike Australia, which bars the entry of the disabled as likely to become a burden on their overstressed health care system, “a qualifying physical or developmental disability or mental impairment can exempt a naturalization applicant from the English requirement.”

Once we’ve filled the United States with citizens who don’t speak English, a federal law requires that we facilitate votes from those completely-disconnected-from-legacy-Americans-by-language citizens. The Voting Rights Act, Section 203:

… citizens of language minorities have been effectively excluded from participation in the electoral process. Among other factors, the denial of the right to vote of such minority group citizens is ordinarily directly related to the unequal educational opportunities afforded them resulting in high illiteracy and low voting participation.

The language minority provisions of the Voting Rights Act require that when a covered state or political subdivision provides registration or voting notices, forms, instructions, assistance, or other materials or information relating to the electoral process, including ballots, it shall provide them in the language of the applicable minority group as well as in the English language.

The requirements of the law are straightforward: all election information that is available in English must also be available in the minority language so that all citizens will have an effective opportunity to register, learn the details of the elections, and cast a free and effective ballot.

There is some discrimination, according to the Justice Department!

Covered language minorities are limited to American Indians, Asian Americans, Alaskan Natives, and Spanish-heritage citizens – the groups that Congress found to have faced barriers in the political process.

Why not Arabic for the noble enrichers of Dearborn, Michigan who’ve brought their parents over? “Chinese” is the second-largest non-English language spoken at home after Spanish (Census), but no provisions are made to facilitate voting by immigrants from China or Chinese anchor babies who’ve recently shown up as adults.

It surprises me that the U.S. hasn’t completely melted down. The lowest-earning 50 percent of eligible voters pay 3 percent of federal income tax (i.e., they receive a 97 percent discount on the federal government services that they can vote to receive; it would make sense for them to vote for a daily federal government delivery of popcorn even if they think they’ll eat it just once per month). We make huge efforts to gather votes from people who aren’t able to speak English, who have a “mental impairment” (I guess that’s consistent with the 100% disabled Graham Platner almost being elected Senator), and who may have lived in the U.S. for only a few months (the anchor-baby-returns-to-birthplace scenario)), and who aren’t interested enough in or informed enough about voting to zip over to the polls (sending out vote-by-mail packages to everyone).

The Florida primary election is in a couple of weeks so right around now is when most Floridians will start thinking about their choices. Here’s a proposal by the leading Democrat, David Jolly (until yesterday, a Republican!), to set up, without legislative approval, a massive state-run insurance company for hurricane and wind damage:

Florida’s homeowners insurance market has collapsed, and families are paying the price. On day one, I’ll introduce a state catastrophic fund to remove hurricane and wind coverage from the private market, protect homeowners, and cut insurance costs by 60 to 70%. Florida can lead… pic.twitter.com/I2s8q0Tgq3

Unless insurance companies are making 60-70% profits right now, the only way that the state-run enterprise that Mx. Jolly proposes to start can cut costs by 60-70% is by transferring those costs from Florida homeowners to Florida renters (i.e., it will lose money over the years, but get topped up periodically by infusions of tax dollars that are collected from a combination of homeowners (who get them back via this subsidized insurance) and renters (who don’t get any money back)).

This makes Jolly the inverse of Ayatollah Mamdani, whose rent freeze steals from property owners (landlords) and gives it to renters in the form of rent that gets lower every year relative to the market and lower also in real dollars because “frozen” means not adjusted even for CPI inflation. I suppose that there are also some similarities with the Mamdani Caliphate, e.g., (1) voters will easily accept the idea that a state-run enterprise, e.g., Mamdani’s city grocery stores, can have lower costs than a private enterprise, and (2) voters are eager to vote for a politician who promises to transfer wealth from some other group into their own pockets.

Maybe insurance companies actually do make 60-70% profits in Florida? Here’s our Florida-centric homeowner’s insurance company’s KBRA risk rating report. It looks like they broke even in 2022 (Hurricane Ian) and made a 10% profit in 2025 (no hurricanes made landfall anywhere in the U.S.).

(The state-run enterprise, especially if private insurance is outlawed as the tweet seems to suggest, could perhaps also steal from homeowners in low-risk areas, e.g., central Florida, and give to homeowners in high-risk coastal areas. That could be accomplished by smoothing out what should be massive rate differences between these types of neighborhoods. One more possibility is stealing from people who live in new houses by overcharging them and using that surplus to undercharge people in old hurricane-vulnerable houses.)

Finally, as a minor fact-check point in a field (politics) where nobody cares about facts, the Florida homeowners insurance market has not actually collapsed. Rates are trending down, especially after inflation adjustment, after some legislative changes during the DeSantis administration that cut back on litigation between homeowners and insurers.

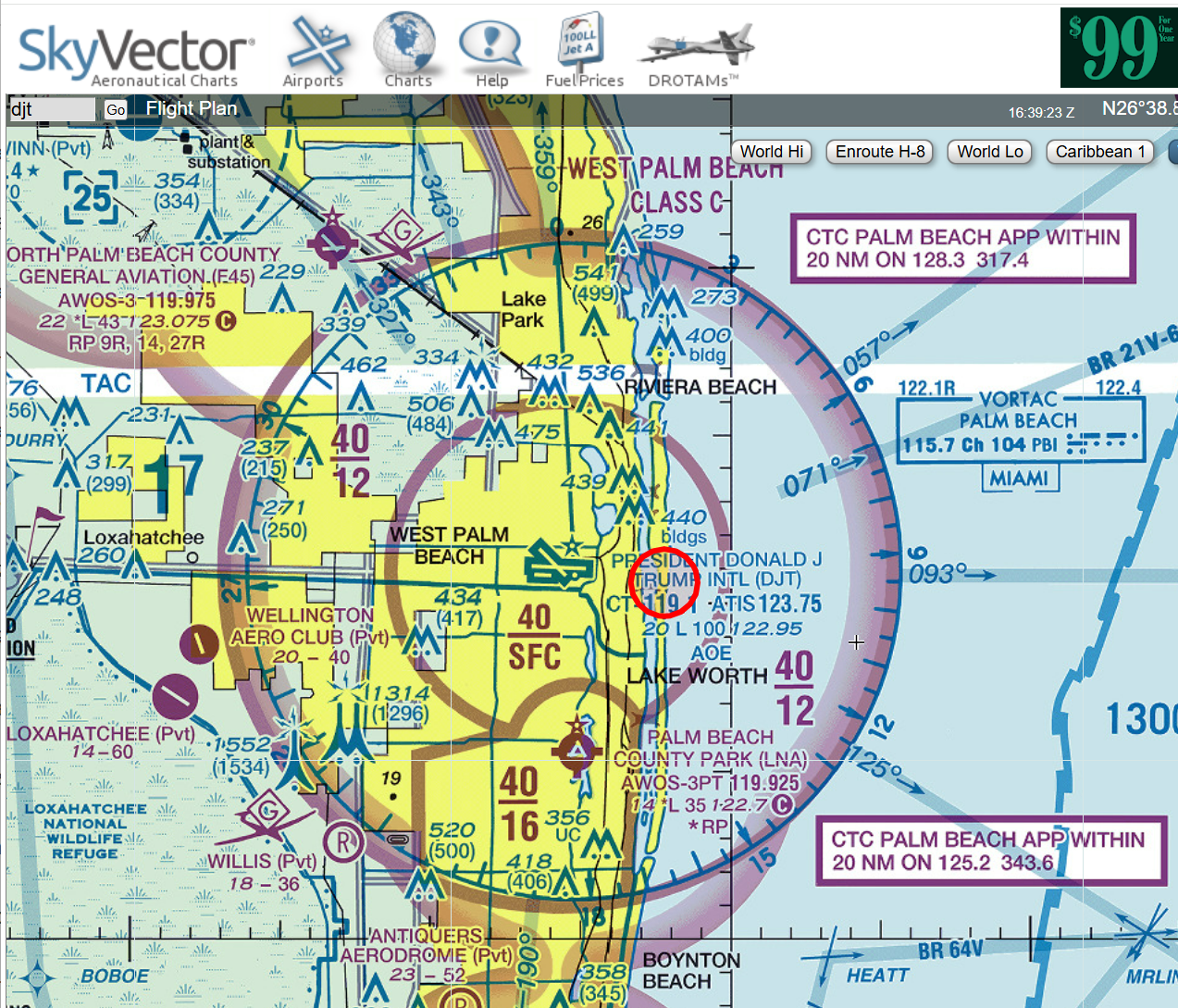

Photos from Day 2 (yesterday) of PBI’s reincarnation as DJT (“Donald J. Trump International Airport”)…

A nod to Donald Trump’s famous passion for fine art:

Purely functional signage:

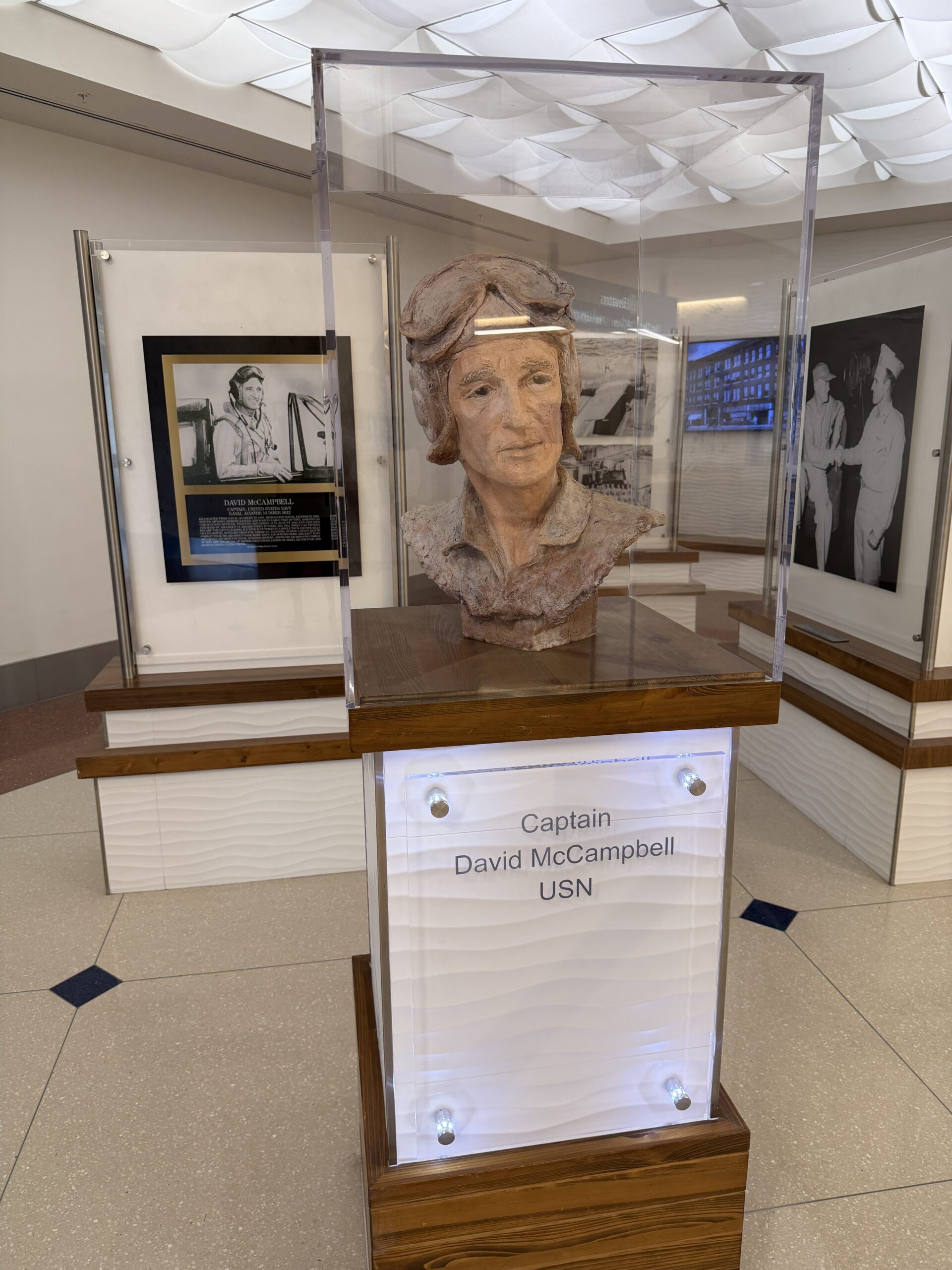

Note that the (1988) terminal remains dedicated to Navy fighter pilot David McCampbell, who became famous by shooting down airplanes (maybe not the best possibility to remind passengers of as they check their bags?) and then retired to Palm Beach County:

The history of the airport is preserved:

The renaming is a rather bizarre turn of events given that Trump has been the airport’s worst enemy ever since he purchased Mar-a-Lago, notably in obstructing the expansion of 10R/28L to accommodate “real airplanes” and, thus, add flights (now it is just 3214×75′ vs. 10001×150′ for 10L/28R). Mar-a-Lago is indeed almost directly in line with 10R so Trump’s fight against the airport wasn’t irrational. This article describes a history of conflict going back to 1995:

A 1995 lawsuit by Trump over airport noise ended with the county agreeing to lease Trump the land where he later built Trump International Golf Club. A 2010 lawsuit by Trump over airport noise was dismissed.

Here’s the geometry that makes the conflict inevitable:

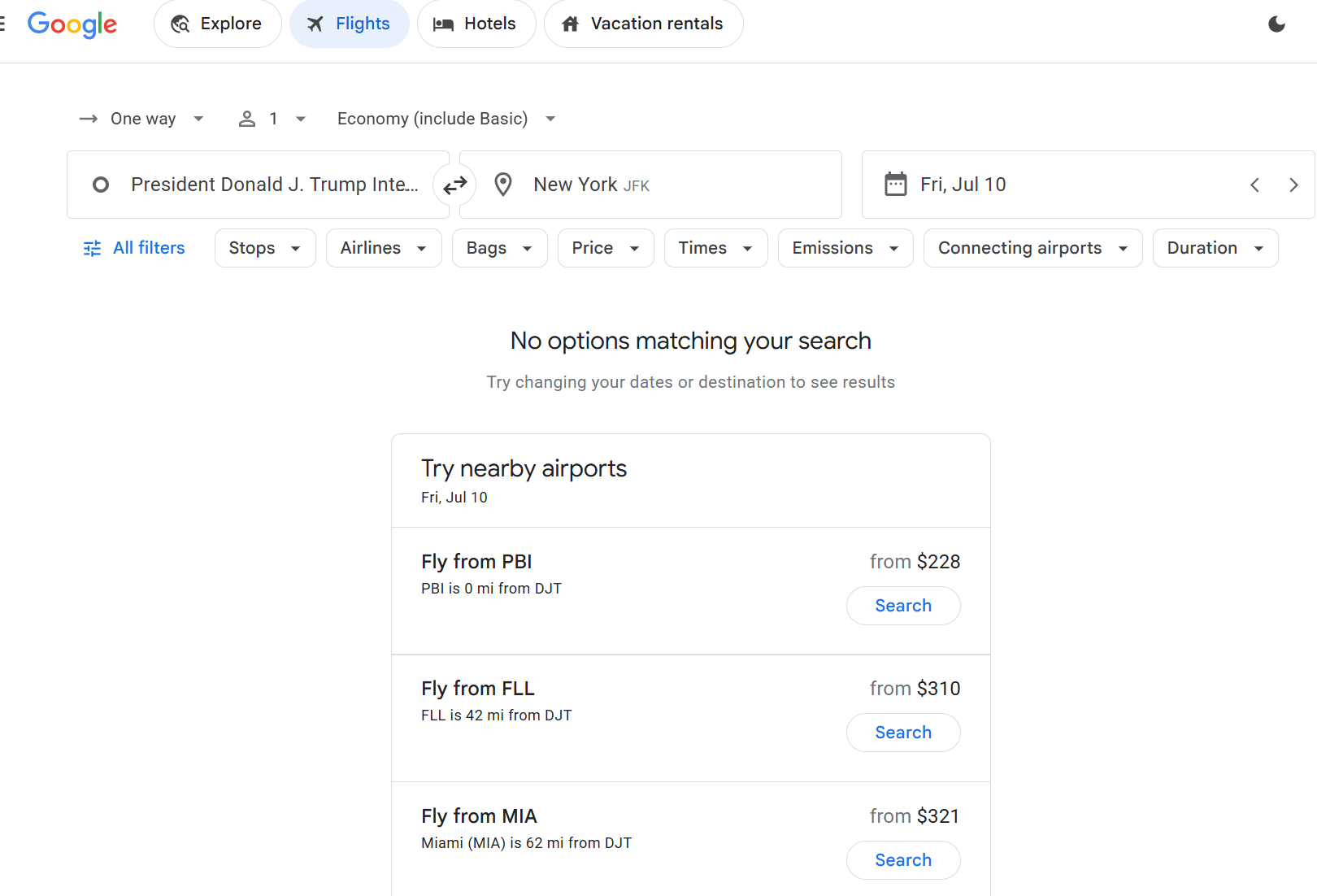

Today is a dark day for billionaire Democrats who’ve been avoiding New York City and New York State income tax by living 183 days per year in Palm Beach. Their Gulfstreams are now parked at “DJT”, President Donald J. Trump International Airport. Google is #Resisting. If you say that you want to fly from an airport named after the worst U.S. president ever to one named after the best U.S. president ever (JFK gave us the Cuban Missile Crisis, the Vietnam War, and open borders (Lyndon Johnson had to finish the last two)), Google Flights responds that nothing is available and that one must fly instead from “PBI”:

(Maybe because the IATA code won’t officially update until August? On the third hand, the site could silently fix the discrepancy and simply display flights from what is still “PBI” for baggage tags.)

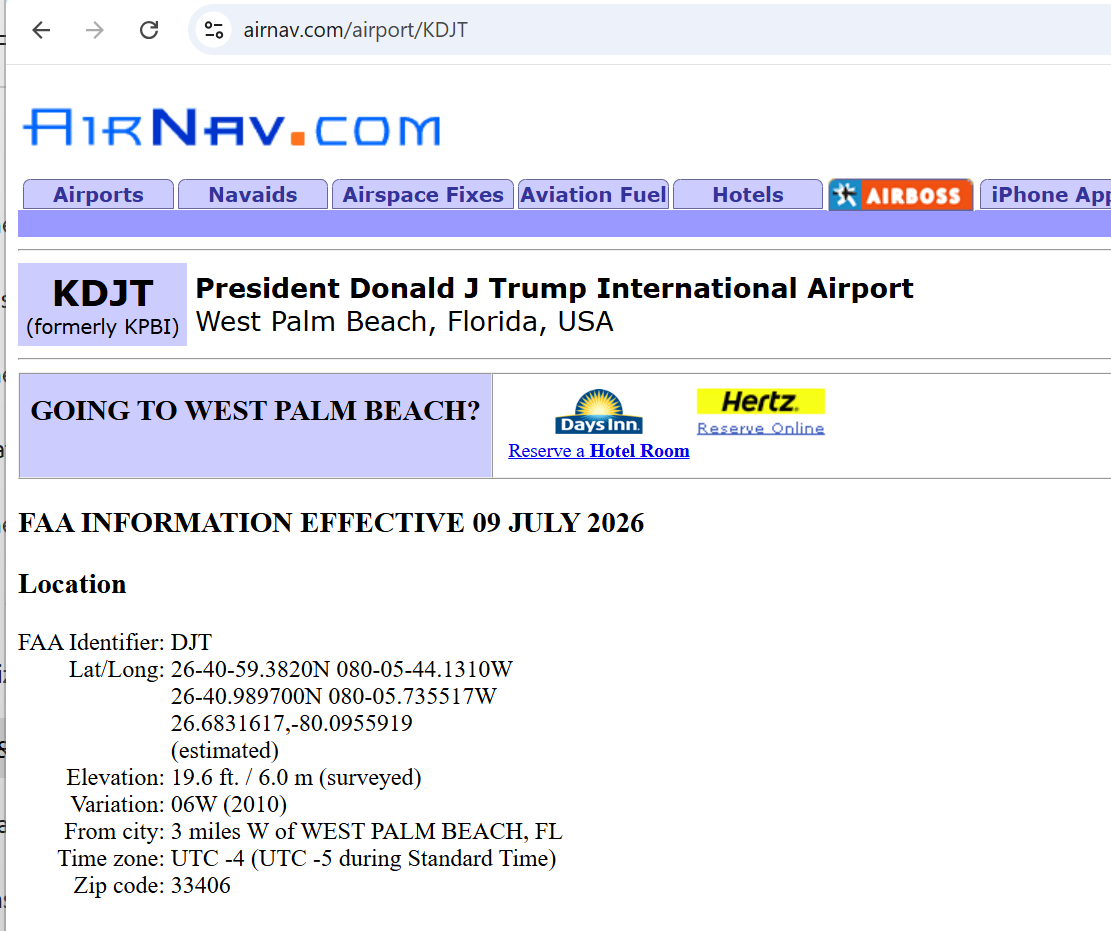

Airnav’s budget is smaller than Google’s, but their site is fully up to date with today’s change:

Garmin pilot shows that a new FAA VFR chart is apparently available:

Just a few more minutes of Pride and there won’t be any 2SLGBTQQIA+ holidays until Nonbinary Awareness Week begins in 13 days.

Here’s a typical celebration in our neighborhood: “Congratulations to Rice-Bound Britton”.

Separately, does it make sense to congratulate Bitton for choosing a $100,000/year school, even one that absurdly claims to be “ranked as a best value in higher education”? If Britton got into Rice she surely would have qualified for the Bright Futures scholarship, thus cutting University of Florida tuition to $0 from $6700/year. She probably would have qualified for the Benacquisto Scholarship, which also pays for housing, food, textbooks, fees, etc. Rice is ranked #17 by US News while University of Florida is ranked #30. Rice ranks higher, but is it $400,000 higher? ChatGPT, asked which school has the better climate: “For a typical August–May school year, I’d pick Gainesville, FL as the better climate overall, especially for kids and outdoor life. Houston has milder winters, but Gainesville has a more pleasant fall–spring stretch, cooler nights, less big-city heat-island effect, and a less flood-prone feel.” I personally love the art museums of Houston, but can’t remember seeing college kids in them. Air quality is, of course, much better in Gainesville since Floridians don’t spend all of their time and energy refining petroleum.

ChatGPT says that UF is stronger than Rice for undergraduates in some areas, including nuclear engineering (maybe now that we’ve surrendered to the Iranians they will send their future bomb developers to UF?), pre-vet, anything agricultural (AI-proof?), accounting, real estate/construction/development (AI-proof?), education, pre-health other than pre-med, materials engineering, etc. In a lot of engineering disciplines, our AI overlord says that the schools are close, but presumably Rice is less of a herd experience.

Europeans object to being mocked for their lack of air conditioning on the grounds that, pre-Climate Change, there were at most a few weeks per year when they would have wanted to use it. Note that this is partly due to European tolerance for a wider range of indoor temps than we spoiled Americans. They probably wouldn’t turn on A/C until their interiors were 8-10 degrees warmer than what would motivate an American to open up the WiFi thermostat app on his/her/zir/their phone.

Because of American profligacy with fossil fuels, Europe now has brutal heat waves (example from 1911; one that afflicted Paris in 1757) that make their decision to reject A/C appear stupid, but in reality they are the smart/wise ones.

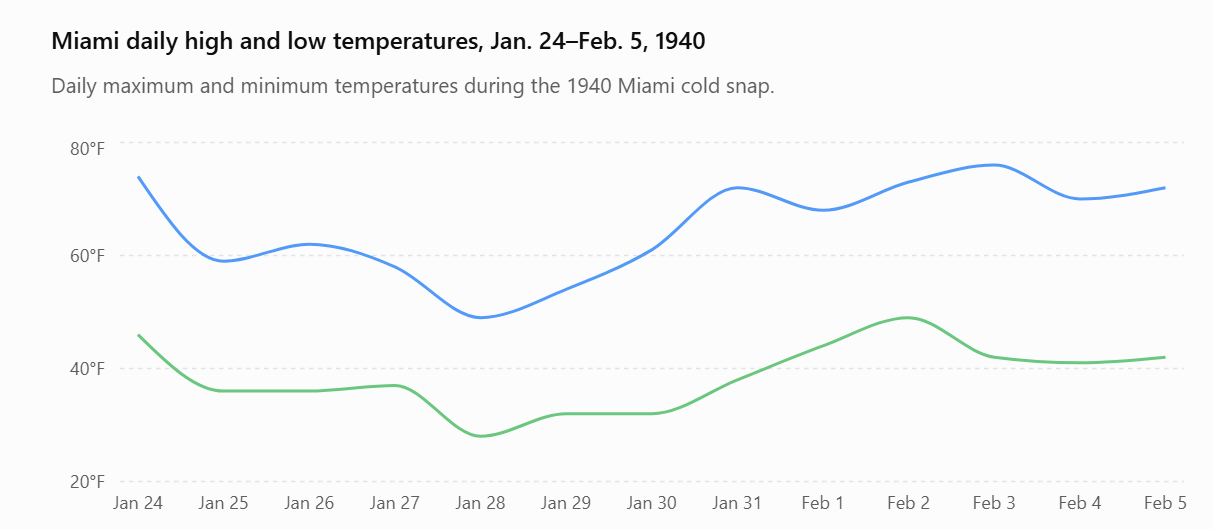

Maybe, however, there is an analogous situation here in the U.S.: should a house in South Florida be equipped with heat? Outdoor temps drop below a comfortable room temperature for only a few weeks per year, analogous to outdoor temps being higher than room temp in Europe for only a few weeks per year. Houses are well insulated in South Florida because they’re almost all new. There is no historical weather that could reduce the indoor temp of a modern South Florida house to a dangerously cold level. Just as Europeans say that they can deal with typical heat by closing shutters, opening windows, jumping in the local canal, etc., a South Floridian without heat during a severe cold weather event could dig through the closet for a sweater and long pants, use an electric blanket or mattress pad at night, etc. Here’s one of the most extreme cold events that ChatGPT managed to find for Miami, which included a low of 28 degrees:

Running heat in South Florida is incredibly wasteful because (1) it is usually a resistive “heat strip” inside the air handler (the latest houses have fully insulated refrigerant lines in both directions and, therefore, heat pump heating capability), and (2) whatever heat is added to the house will eventually have to be pumped back out using electricity for cooling.

What is the observed behavior? Every house, by code, is built with heat capability. People turn on the heat as soon as they feel uncomfortable. As noted above, the latest houses even have heat pumps, maybe due to federal government tax incentives that encourage this super-wasteful-in-south-florida investment ($thousands extra in capital that lasts 15 years to save a couple of $hundred in electricity every few years).

If Climate Change were to cause South Florida to be subjected to a Maskachusetts-style December, Floridians wouldn’t die like the stoic Europeans. Nor would they get into a brawl at Walmart over space heaters. Houses here are already equipped to handle a multi-day freeze. The damage would be limited to higher FP&L bills (still, probably much lower than in MA, though, because rates here in FL are about one-third per kWh of what my friends who’ve remained Righteous are paying!).

As noted above, we could also explain the apparent difference in preparedness as due to a difference in tolerance for discomfort, with Americans being the wimps!

Related:

Art Palm Beach (cavernous yet nice-and-warm convention center despite record-low (for the dates) overnight freezing temps in the middle of a two-week cold spell, the most extreme since 2010)

Here’s a disturbing proposal from a politician whose policies I generally agree with:

Today in Tampa, I outlined the Save Our Homes from Excessive Property Taxes plan that will eliminate taxes on homesteads.

Property tax revenue collected by local governments has nearly doubled in the past seven years (from $32 billion to $60 billion) and is expected to reach an… pic.twitter.com/3ZcexD9L7X

While I don’t enjoy paying property tax, the idea that the majority of Floridians eligible to vote will soon pay nothing seems like a recipe for much faster growth in county/local government spending. (Many Florida voters already pay next to nothing because they’re taxed on the original purchase price and perhaps that is what accounts for the rapid rise in county spending that Gov. DeSantis decries.)

If the majority of Floridians aren’t paying property tax, won’t they vote for every blue sky spending dream that counties and cities put forward? That’s how it works at the federal level. The majority pay either nothing or next to nothing and have voted the U.S. into the world’s largest or second largest welfare state, as a percentage of GDP (we vie with France for the title). Even if a homeowner who isn’t taxed receives only 1 penny of benefit for every additional $1 million spent it would still be rational for him or her to vote for increased spending.

Is there a method to Ron DeSantis’s apparent madness? I’m sure that he understands politics much better than I do, but I am struggling to find merit in narrowing the tax base and feel that the experiment has already been run on the American people. If the goal is limiting county spending, why not a state-imposed limit on county/local government spending? Take the 75th percentile of per-capita spending in 2025 and impose that as a limit, adjusted annually for inflation, on all Florida counties. A county that is already over the limit would have five years to come down into alignment with the law. This might force counties to eliminate affordable housing subsidies, for example, which have the potential to be infinitely expensive as well as certainly unequal (some people get below-market-rate housing; others, equally virtuous and equally situated, are forced to pay market rates).

Maybe the method in the apparent madness is that homesteaded property isn’t that important to county budgets, e.g., for Miami-Dade just 7 percent of the total budget. ChatGPT says it is 9 percent of the total Palm Beach County budget. Both of these counties have a lot of commercial real estate, but property tax as a whole isn’t the lion’s share of the budget as I would have expected.

Miami-Dade: Residential homesteaded property tax is about ~$0.88 billion — just 6.9% of the $12.9 billion FY 2025‑26 budge. Removing it entirely leaves 12BB to spend: Miami-Dade last operated at less than 12BB in FY ‘23‑24. So you could eliminate completely and still operate at… https://t.co/dbwU06Hs8J

Republicans in general seem to be competing with Democrats in the “make the rich pay for everything” department. As noted above, I don’t see how this can work in a democracy where the people paying nothing have the right to vote for unlimited enhancements to whatever they’re receiving from a government funded by a minority that can be trivially out-voted. Maybe it can work in California and New York City where AI and Wall Street actually do generate infinite wealth on a recurring basis, but Florida isn’t home to NVIDIA and the AI companies that use NVIDIA chips.

New York City (and maybe the state as well) are generating outrage by proposing to tax residential real estate that isn’t a primary residence at a higher rate than the same property would pay if occupied by somewho who was a full-time NYC resident.

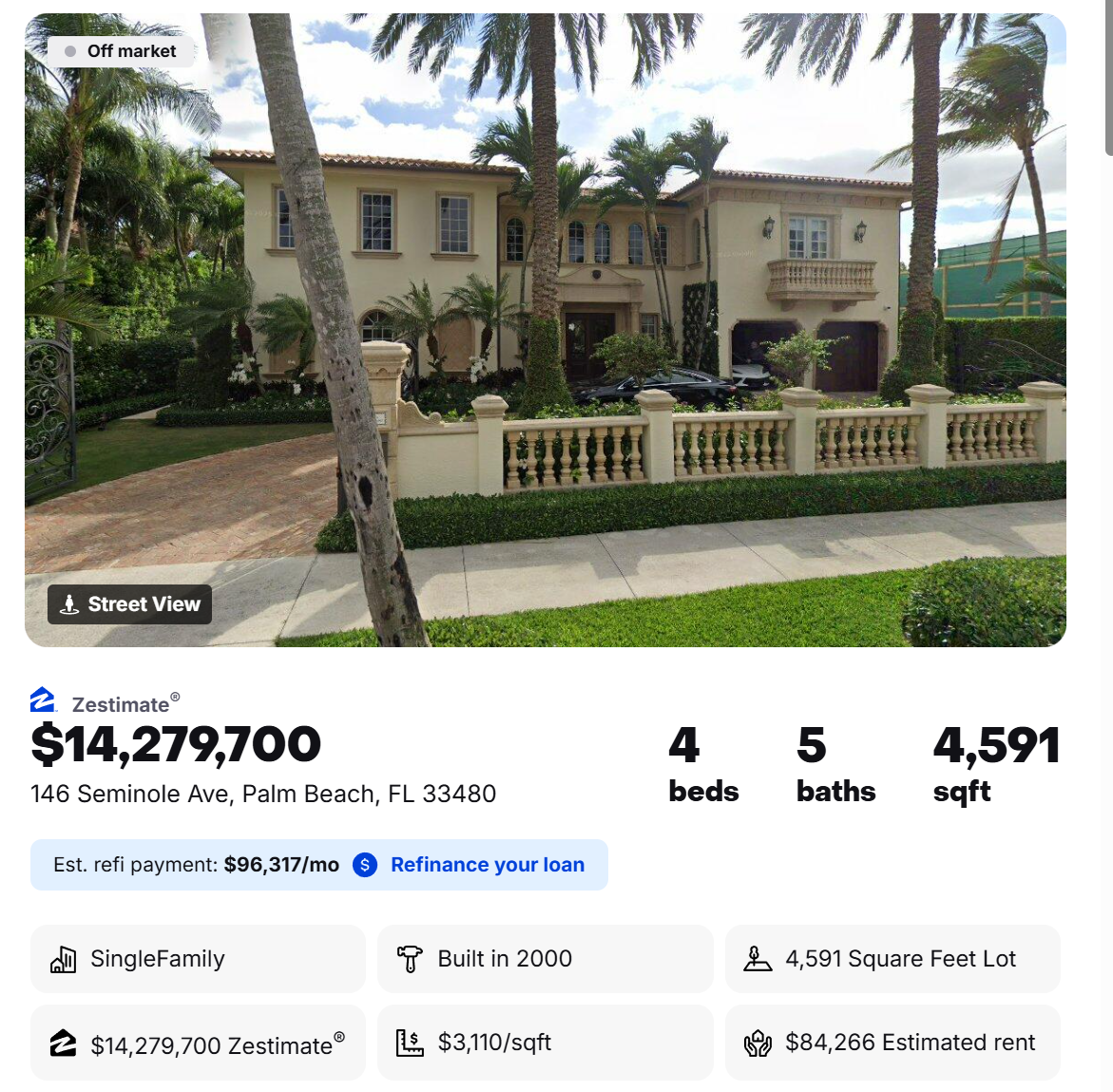

What other city or state indulges in this outrageous abuse of society’s successful? Florida! Let’s look at starter homes in Palm Beach. Here’s one that was purchased for $4.45 million in 2011 and is today worth $14.3 million (Zillow).

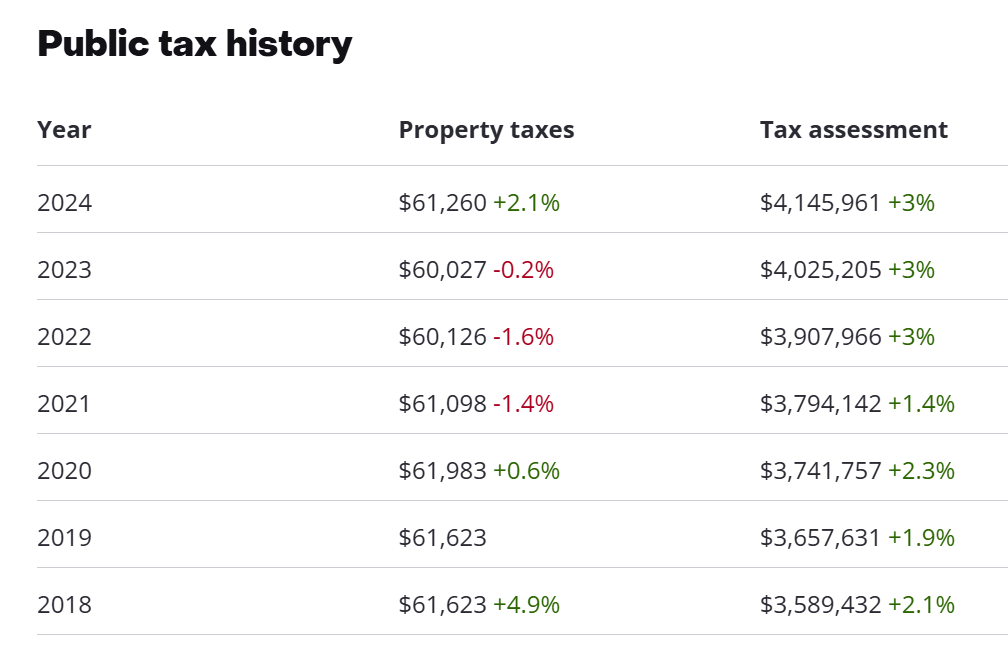

The tax assessment is still less than the purchase price, presumably due to the fact that the assessed value for a “homestead” (primary residence) can’t go up more than 3 percent or the increase in CPI, whichever is lower:

If there were an identical house next door and it sold for $14 million to someone who used it only 4 months per year, the town/county could collect property tax on the full value, i.e., 3X the tax rate paid by the primary resident.

A surcharge for part-time residents generates outrage. A discount for full-time residents doesn’t upset anyone. NYC could have doubled property tax rates, with state permission, and then offered a steep discount for anyone who pays resident NYC income tax.

Happy Middle of Hurricane Preparedness Week for those who celebrate…

Conventional insurance companies such as State Farm have mostly walked away from insuring coastal South Florida due to a combination of litigation risk (“Prior to the reforms, Florida accounted for more than 72% of the nation’s homeowners claim-related litigation in 2023, despite representing only 10% of US homeowners claims.”) and hurricane risk. Our house is about 2.5 miles from the ocean, but it is still redlined by the insurance companies most people have heard of. Here are the options for insurance:

a Florida-only carrier that turns most of its premium over to reinsurance

a “non-admitted” specialty company that isn’t regulated by the state and that may have unfavorable terms, including penalties for early cancellation and even a “wind exclusion” (i.e., they pay nothing in the event of the most obvious risk: hurricanes). (This option is so expensive and dumb that I won’t cover it here.)

a “high-net-worth” (HNW) carrier such as Chubb (mostly rejects additional Florida risk; famous for a low loss ratio (payments as a percentage of premium collected)), Vault, PURE, and Berkley One (despite the name, these are available to peasants whose house is worth less than a Palm Beach starter home ($10 million))

The cost of HNW insurance is 2-4X what a Florida-only company might quote.

Nearly all Florida insurance includes at least a 2% wind exclusion. If the dwelling value is $1 million, in other words, the homeowner pays the first $20,000 of any hurricane-related loss. Thus, the vast majority of customers with hurricane damage will receive nothing from their insurer because the typical hurricane damage might involve only some blown-off roof tiles or shingles. The band of likely serious damage from a Category 4 or 5 hurricane making landfall is 20-60 miles, e.g., for Hurricane Andrew in 1992 that resulted in major changes to the Florida building code or Hurricane Michael in 2018 that damaged Tyndall Air Force Base. Note that this exclusion results in the HNW policies paying less after what would be typical hurricane damage because HNW companies write for 2X the dwelling value on the same house.

The Florida-only carriers are typically unrated by AM Best, the standard rater for insurers. It has been historically rare for an insurer rated A or better by AM Best to fail. Florida insurers get rated by Demotech. How well does it work for an insurance company to have all of its customers in Florida? According to ChatGPT, nearly all of the Florida-only companies that have gone insolvent had A ratings from Demotech (i.e., the ratings were worthless in terms of distinguishing the vulnerable carriers from the solid ones or, perhaps, the solvency of a carrier simply depended on their luck regarding how many customers were in a hurricane destruction zone).

Insolvency after a major hurricane doesn’t work the way that one would think, with the failed insurance company realizing that it is doomed to failure and going into a bankruptcy-style process where every claimant gets paid a percentage of his or her full claim amount. Instead, the insurance company, even after a major hurricane, pays claims as they’re made and adjusted at 100%. When the company runs out of money they turn out the rest of the claims to the Florida Insurance Guaranty Association (FIGA), which will pay up to $500,000 for a destroyed house. So… the customer with a major loss either gets 100% or a fixed $500,000. The more complex the claim, the less likely it is to be paid. ChatGPT says that it is reasonable to assume a 10 percent chance of insolvency for a Florida-only carrier in the event of a major hurricane. The most recent insolvency that triggered a FIGA payout was of United Property & Casualty Insurance Company in February 2023. That’s three hurricane seasons ago. Since then we’ve had some hurricanes, but none anywhere near as costly within Florida as 2022’s Hurricane Ian. Let’s use a 20 percent risk of insolvency if a house is damaged to policy limits and a 10 percent risk of insolvency if a house is damaged to half of the limits.

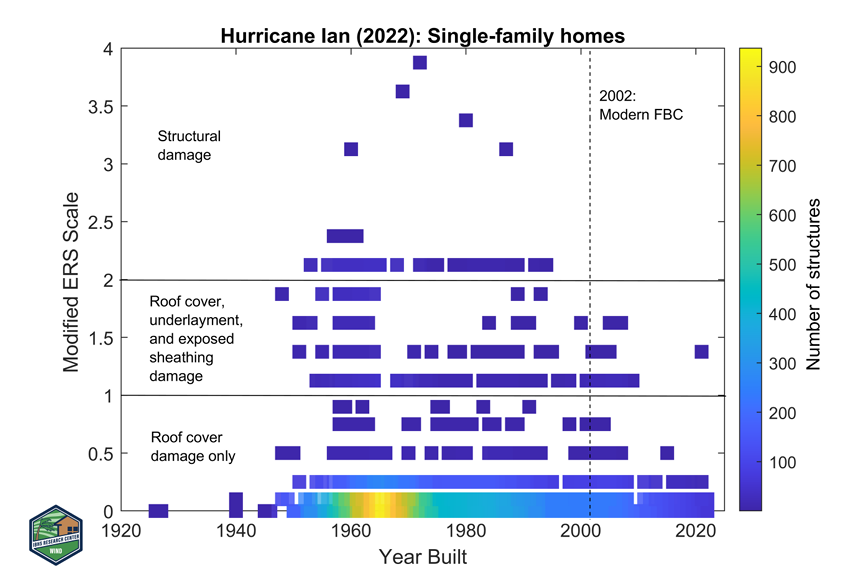

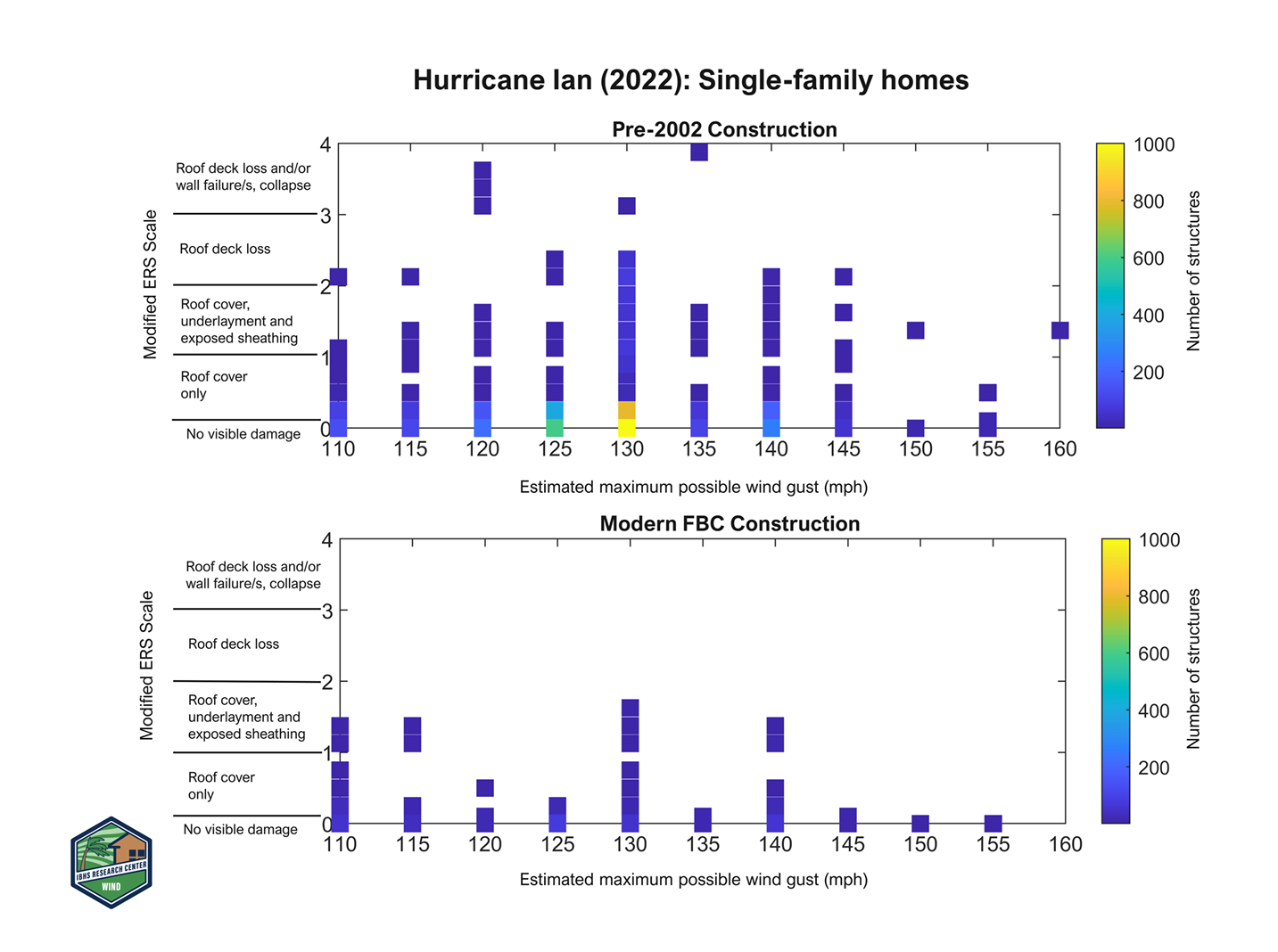

What is the risk of a total loss or serious damage? Gemini starts off by saying that it is pretty high, with 300,000-400,000 single-family homes in South Florida either substantially damaged or destroyed by hurricanes over the past 50 years. That’s out of about 2.7 million homes in South Florida today, but only an average of 1.7 million homes over the 50-year period. (ChatGPT estimates this number as only about half of Gemini’s figure; our future AI overlords are smarter than humans, but equally inconsistent?) So a homeowner’s insurance company has about at least a 1 in 7 chance of making a big payout? Not exactly. First, we have to separate out the houses that were damaged by flooding or storm surge, between 120,000 and 180,000. Homeowner’s doesn’t pay for flood damage. Now we’re down to a risk of about 1 in 10 over 50 years. What about the fact that Florida established a strict statewide building code in 2002, hoping to avoid a repeat of the Hurricane Andrew aftermath, roughly 25,524 homes destroyed and 101,241 damaged (Insurance Information Institute). Gemini:

In major storms like Hurricane Michael (2018) and Hurricane Ian (2022), structural engineers found that homes built to the 2002 code (or later) suffered roughly 80% to 90% less wind damage than their older neighbors.

IBHS evaluated 3,646 single-family homes, 327 light commercial buildings, and 230 multifamily structures [after Hurricane Ian] using aerial and street-level imagery. … Homes built before 2002 had structural damage levels nearly 2x higher, and 2.3x higher in areas with peak winds above 130 mph.

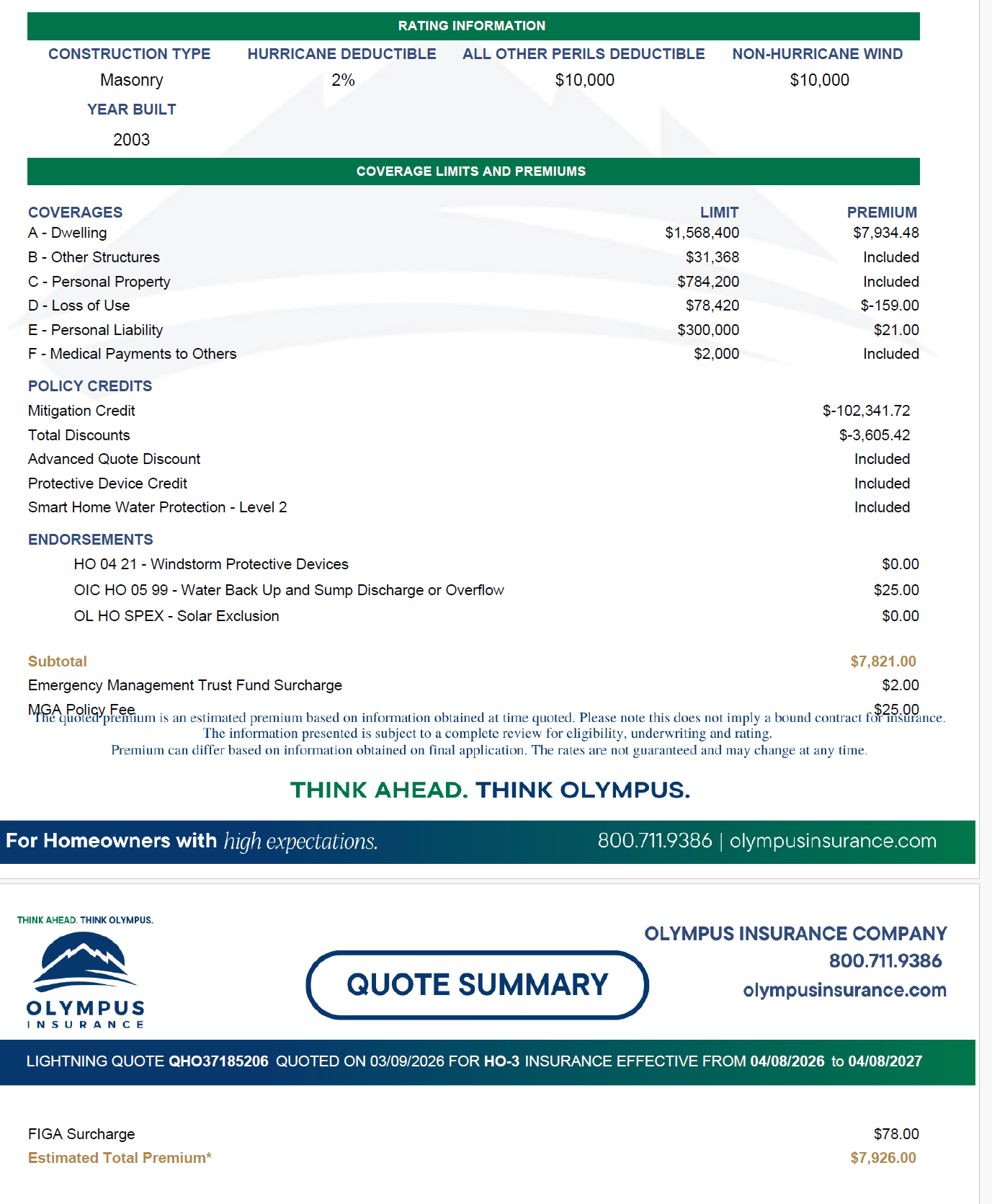

It looks as though no post-2002 house actually lost the plywood sheathing supporting the roof, but at least some had exposed sheathing and, presumably, water damage as a result. A companion report from the same organization says that asphalt shingles were the weak point, metal roofs were the best (12% damaged), and tile roofs weren’t significantly damaged except those more than 20 years old (“no tile roofs assessed that had greater than 50% roof cover damage” and “the small number of roofs with greater than 25% cover damage … These roofs were all 20 years or older”). Our 2003 house has a one-year-old tile roof with two layers of “peel and stick” underneath. If the tiles are blown off, but the peel-and-stick underlayment survives then we’re looking at a $120,000 insurance claim to put a new tile roof on the house (maybe less if the underlayment isn’t too old and can be retained).

ChatGPT says that 4-6 Cat 4/5 hurricanes hit the Miami-to-Stuart coastline every 100 years. Let’s take this distance as 108 miles. If you assume that the zone of total destruction is 20 miles wide then a typical house gets destroyed roughly every 110 years. If the destruction zone widens to 40 miles, the interval between destruction is 55 years. The most recent major hurricane to hit Palm Beach County was in 1949, 77 years ago, but we could use the 55-year estimate to make the high-net-worth companies look more attractive.

[We’ll ignore tornado risk. A tornado could destroy or seriously damage a house, of course, but it wouldn’t affect an insurer’s solvency because a tornado is local. This is a 1 in 100,000-year event for a typical South Florida house, according to AI.]

As noted above, one quirk of the HNW policies is that they force buyers to pay to insure the full rebuild cost of a house, which for a 2003 house like ours is much more than the house is worth. Imagine if we insured our five-year-old Honda Odyssey for the cost of a brand new Honda Odyssey. Why would we want to do that when what is actually at risk is only about half that number? A neighbor has Chubb and they would pay him over $4 million for the house and contents in the event of a total loss (maybe $5 million if we add “loss of use”). His house has a Zestimate of $1.8 million, has its original roof and non-impact windows, and sits on a lot that should be worth at least $500,000 if the house were razed. The contents of the house aren’t valuable. So he has perhaps $1.5 million that could conceivably be lost under his $4+ million policy. (Note that the neighbor won’t get the high dwelling value unless he actually does rebuild, an irrational choice to make compared to simply moving to a similar house and letting a professional real estate developer deal with the wreck. If the family moves to a $1.8 million house a few blocks away, he gets paid only about $1.3 million (the depreciated value of the structure).

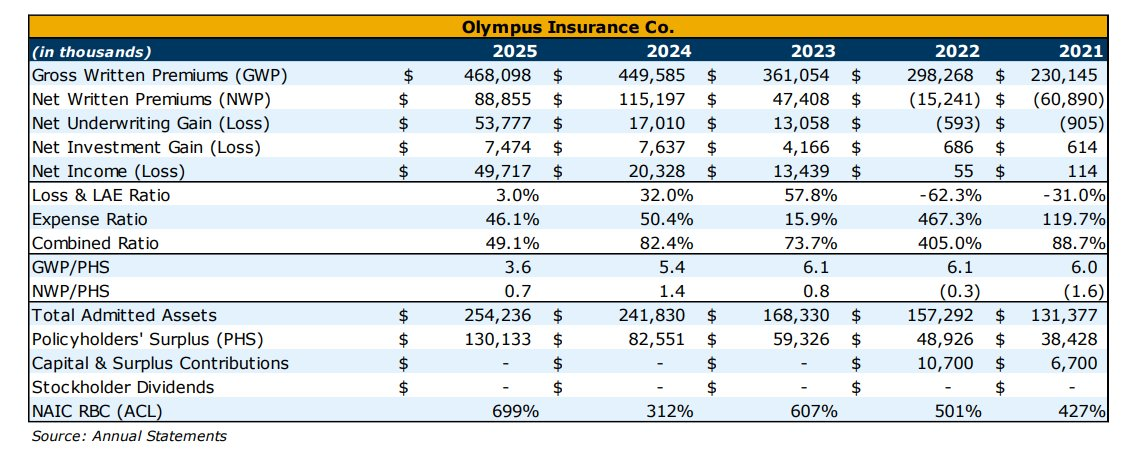

Let’s have a look at a couple of quotes. Below is one from Olympus, a Florida-based company that was founded in 2007, i.e., 19 years ago. Whoever started the company should buy lottery tickets because it was founded right at the beginning the 2006-2015 “no hurricanes making landfall” period. That said, the company has survived the following hurricanes that did make landfall in Florida:

Hermine (2016)

Irma (2017)

Michael (2018)

Ian (2022)

Idalia (2023)

Helene (2024)

Milton (2024)

Furthermore, Olympus is unusual in being rated by KBRA, which is significantly more stringent than Demotech. Olympus is rated BBB+ by KBRA (over the minimum BBB accepted by Fannie Mae; it’s ironic that the enterprise that generated the largest insolvency in U.S. history, requiring $150+ billion in tax dollars as a bailout, closely scrutinizes insurance companies). For the handful of companies that are rated by both KBRA and AM Best, the ratings seem to be similar.

Could they survive a repeat of the 1949 hurricane that came right into Jupiter? (the most recent major hurricane to make landfall in Palm Beach County) There doesn’t seem to be any way to find out. An insurance company with 50,000 customers, each of which is on its own square mile within the 53,625-square-mile state of Florida is going to be much less stressed by a hurricane that hits Fort Lauderdale than one whose 50,000 customers are all in Broward County, for example. (Broward County was last hit by a major hurricane in 1947, though Hurricane Wilma, Category 2, did about $4 billion in insured damage in 2005.) The information on risk concentration by company is nowhere to be found. In theory, the reinsurers who agree to do business with the companies are looking at this and maybe the regulators.

It is difficult to have faith in regulation when one hears about Florida-based Slide Insurance. The founder and his wife siphoned off $50 million in compensation out of a total profit of $288 million in 2023-4 (source). Based on this, it seems that an insurance company could pay out all of its profits to employees and shareholders during 15 lucky years without major hurricanes affecting its territory and then fold up its tent after a Hurricane Andrew-type event occurs. ChatGPT: “There’s no strict statutory cap tying executive pay to solvency. … As long as they stay above minimum surplus requirements, they’re compliant. But those minimums may not cover a true tail event (e.g., Andrew-scale).” People with inexpensive-by-Florida-standards houses will still do okay with $500,000 from FIGA, of course, so this is a great example of privatized profits and socialized losses.

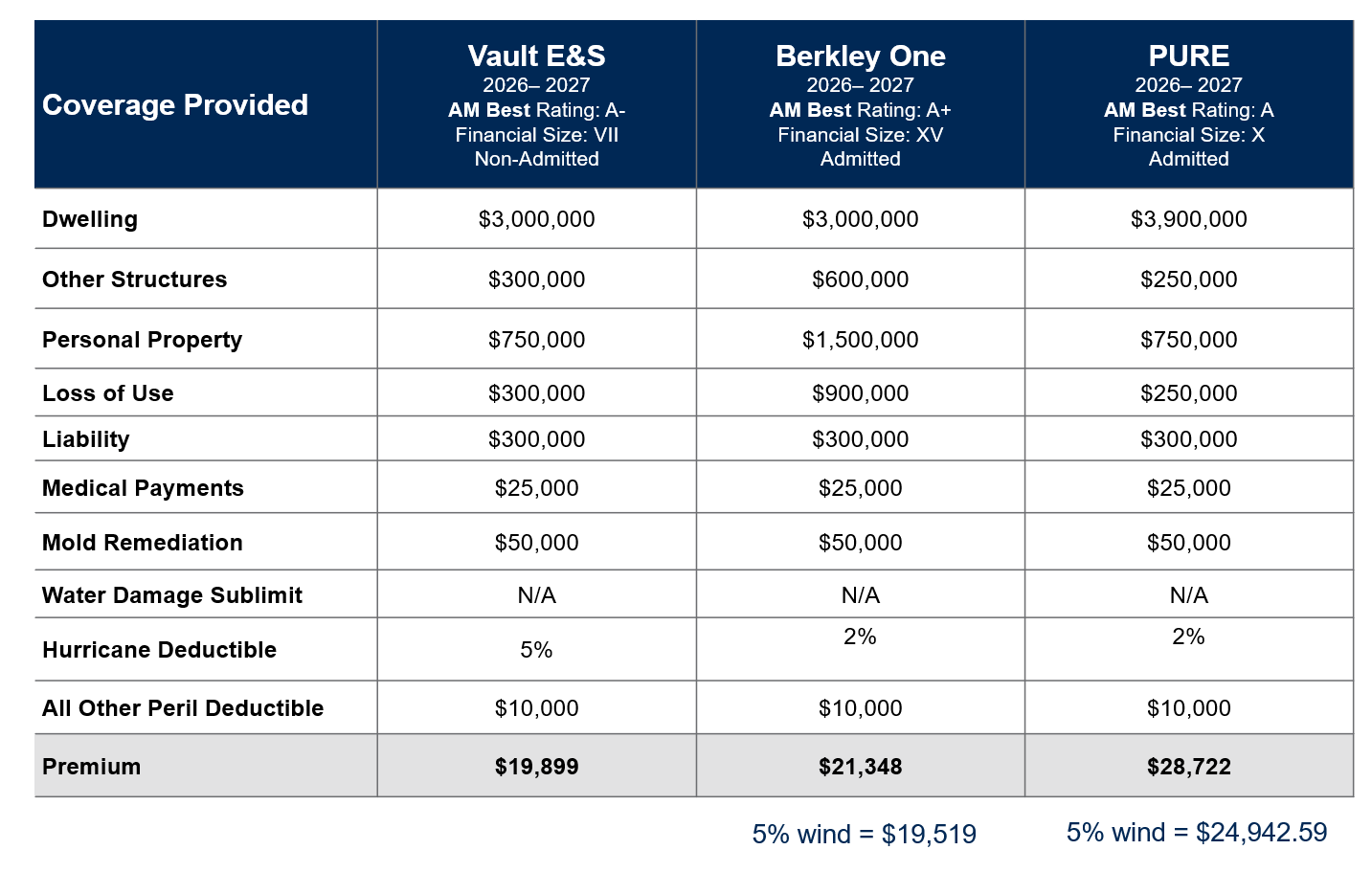

What did the high-net-worth companies have to offer?

Notice the PURE quote with a 5% wind exclusion. If our roof were destroyed, but didn’t leak, and we lost 7 or 8 of our impact glass windows they would still pay nothing because the wind deductible would be $195,000. In a “medium bad” event, the Olympus policy at less than one third the cost could easily pay 2X because of the deductible being only 2% of a much lower dwelling value.