More than 36 square miles of Pacific Palisades were burned, which is a tragedy, of course, but also an opportunity for California’s central planners. We are informed that California is suffering from a housing crisis, an affordable housing crisis, a crisis of unhoused people, and a crisis of housing for noble undocumented migrants. Also that housing is a human right. Californians, if they were sincere in their principles and commitment to solving these crises, could use eminent domain to buy the burned square miles (at whatever the raw land value was prior to the fire) and develop it as a cluster of fireproof (and earthquake-proof) concrete-and-steel high-rises. Built to the same density as Manhattan of 73,000 people per square mile, this would become home to 2.6 million people. If we assume 3 people per unit, the county and state would be building approximately 870,000 units. “Housing Underproduction in California: 2023” says “California must build 3.5 million housing units by 2025 to end the state’s housing shortage”. In other words, a project of this nature would solve about 1/4 of California’s housing problems.

Could Californians afford it? In City rebuilding costs from the Halifax explosion we learned that it cost roughly $555,000 per unit at pre-Biden prices to build in Boston (assuming free land). Adjusted for Bidenflation, California’s higher costs, and the need to pay for the land let’s assume $1.5 million per unit. The total cost would then be $1.3 trillion, but let’s assume that not all of the units are given away free to noble no-income and low-income residents. Perhaps half the cost is eventually recovered via rent or sales. Thus, the total cost is $650 billion. Divided by California’s 39 million people, this works out to less than $17,000 per Californian, which seems like a small price to pay to take a big chunk out of the housing shortage/crisis and also reduce fire risk going forward (concrete and steel won’t burn and homeless encampments have been a source of recent fires (NBC)).

I’m so old that I mail out hardcopy Christmas/New Year’s/Kwanzaa cards. Quite a few friends hadn’t received them by New Year’s, which seemed odd because I’d put nearly all into a mailbox before Christmas.

One friend sent me a picture of the card that he received in Berkeley, California on January 4. It was postmarked December 23. That’s nearly two full weeks for the check to be in the mail, admittedly minus two days on which USPS employees don’t work (Christmas and New Year’s).

Maybe because I used an OSIRIS-REx stamp rather than a Kwanzaa stamp?

I’ve seen various progressives on X expressing a combination of rage and fear regarding the possibility that Donald Trump and his hated Republican junta will attempt to privatize the USPS. To figure out how bad this would be, perhaps we should start by considering what would happen if the USPS were simply eliminated. We would then have no mail, right? This is the same logic that is applied when we arrest migrant drug dealers. As soon as we have all of the drug dealer in prison there will be no more drugs sold. There is no chance that new migrants will walk across the border and begin dealing drugs into a lucrative open market (nor that any native-born American will start a career as a drug dealer).

What actually would happen? Delivering junk mail seems to be lucrative. My guess is that some company that already visits most houses in the U.S., e.g., Amazon, FedEx, or UPS, would start up a junk mail delivery service. Maybe there would be a printer in the delivery van so that physical documents didn’t have to be transported. First class mail delivery would get way more expensive and, perhaps, faster. This would lead to a lot of restructuring. No more hardcopy bills for $5 from health care providers. Americans who live in extremely remote settlements would need to pay for the “last leg” of delivery (maybe their settlement would do this on a bulk basis and fund it via property tax).

Of course, Americans will never give up on the USPS just as we won’t give up on the penny. So the above is just a thought experiment. But maybe USPS could be privatized as post offices in some other countries have been. In that case maybe they would adopt some of the above tweaks, e.g., an amazing printer inside the vehicle so that “junk mail” didn’t get “mailed”, a much higher price for the handful of first class letters that anyone still needs to send (I would adapt by switching to all-electronic cards).

Anecdote: About 25 years ago I went to Argentina. My Argentine friend said “Don’t bother to send postcards. They’ll never get to the U.S. It can take two weeks for a first class letter to arrive domestically in Argentina. The post office is a disaster.” I ignored his advice, of course, and had some fun trying to figure out how to buy stamps and use the post office to send cards to my mom. All of the postcards arrived in the U.S. after…. about two weeks.

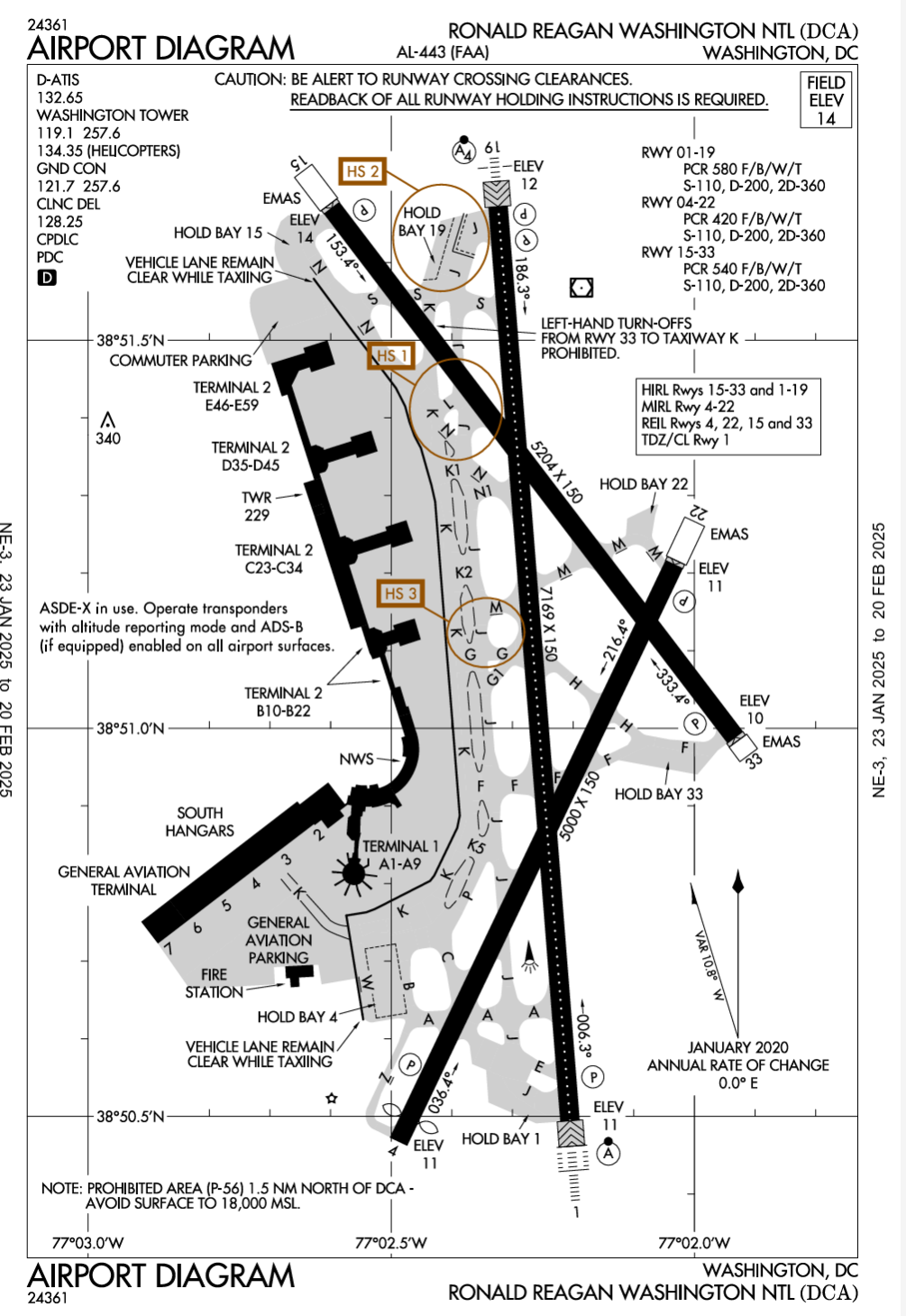

Friends have been asking me about this evening’s crash between a U.S. military Black Hawk helicopter and a Canadair Regional Jet (CRJ) that was on final approach to DCA (Reagan National).

It’s a terrible tragedy, of course, and has led to speculation on X regarding terrorism. A review of the ATC recording shows that there was plenty of room for human error. Because the liveatc.net server is overwhelmed right now, I copied over the relevant recording of DCA Tower. Note that military aircraft communicate via UHF and, therefore, we will hear Tower talk to the Black Hawk, but not the Black Hawk talking to the Tower.

Below is the airport diagram. The Potomac River is to the right and above. Runway 33 begins at the center right of the drawing near the “Elev 10” (10′ above sea level) and “EMAS” (Engineered Materials Arresting System, designed to stop a plane overrunning opposite-direction Runway 15). The runway name of “33” indicates that an aircraft landing on it would be pointing roughly magnetic 330 (333 in this case) or northwest.

At 12:20 Bluestreak 5307, a CRJ-700, checks in and is cleared to land Runway 1 after rejecting an ATC-proposed change to 33 (“unable”). At 12:57 Bluestreak 5342, another CRJ-700, checks in and accepts a modified clearance to land Runway 33 (helps ATC get more departures out). At 13:50, the Tower says that winds are from 330 (northwest) at 15 knots, gusting 25 knots (will be bumpy in a helicopter).

At 15:05 there is some communication with PAT25 (the Black Hawk). At 15:50, Tower tells PAT25 about the CRJ’s lateral and vertical location and also where it is heading (“PAT25 traffic is south of the Woodrow Wilson Bridge a CRJ at 1200′ [landing?] Runway 33”). After an inaudible-to-us reply from the Black Hawk on UHF, the Tower says “visual separation approved” (this approval can be given in Class B airspace only if an aircraft says that it has positively identified another aircraft; we were given this approval every 5 minutes or so when operating our Robinson R44 helicopters in Boston Class B airspace for photo and sightseeing tours over the city; it was necessary because we were within a certain number of miles of the airliners even though we were never anywhere near the approach or departure paths of the jets).

At 17:25, DCA Tower asks PAT25, “Do you have the CRJ in sight?” (in hindsight, would have been much better if Tower had asked “Do you have the CRJ at your 10 o’clock in sight?”) Presumably the Black Hawk pilots answer in the affirmative, having seen or continuing to see what they believe to be the CRJ that ATC is talking about, but we can’t hear this on a recording of the VHF traffic. DCA Tower then instructs the Black Hawk to pass behind the CRJ (might require a slight turn or slowdown).

At 17:47, we hear background conversation in the Tower (a reaction to the crash, perhaps).

At 18:10, American Airlines 3130 is told to go around. The recording for the next few minutes indicates some rough times inside the Tower.

It’s too early to say definitively what caused the crash, of course. However, it seems that there were multiple jets in the air and even multiple CRJs. It is easy to see airplanes, especially airlines, at night, but not necessarily easy to tell a CRJ from an ERJ or a CRJ from an Airbus A319. A two-pilot crew in a Black Hawk would almost surely be able to avoid a crash with an airliner had they seen it more than 1.5 minutes earlier, which they say they did. Thus, the most plausible explanation is that the Black Hawk crew and DCA Tower were talking about two different airliners (i.e., talking past each other).

So… there were some excellent humans with excellent training in the airliner, in the Tower, and in the Black Hawk. Everyone was operating in the most restrictive low-altitude airspace (Class B) that we have in the U.S. and under time-tested rules that have ensured safety despite congestion. At the same time, however, we have the limitations of a natural language (English) and the human brain, which may latch onto and commit to the first plausible airliner that it sees.

A few potentially complicating factors:

Black Hawk pilots will fly with helmets, which reduce peripheral vision.

Black Hawk pilots may use night vision goggles (NVGs), which make it easier to see dark stuff on the ground but harder to see brightly lit objects, such as a CRJ in landing configuration. NVGs dramatically reduce peripheral vision (Update: Pete Hegseth says that they were using NVGs)

Military aircraft sometimes use modern standard ADS-B transponders that transmit x,y,z position, airspeed, and direction, but perhaps not always, and therefore the collision warnings provided by modern avionics might not be triggered

Airliner Traffic Collision Avoidance System (TCAS) has some inhibitions below 1000′ and below 500′ so as not to distract pilots during landing, so even if the Black Hawk had its ADS-B transponder on the airliner’s avionics might have inhibited a collision warning

Visual clutter from all of the city lights; it’s easier to pick out airports and aircraft at night in places where there aren’t brightly lit buildings, parking lots, and towers

For those who aren’t regular readers of this blog: I’m an FAA-certificated helicopter instructor as well as a former CRJ pilot for a Delta Airlines subsidiary. Landing and taking off at DCA were part of the Delta job. I also teach an aeronautical engineering class at MIT. I have never flown a Black Hawk, but I have trained experienced Army Black Hawk pilots to fly the Robinson R44. I have spent hundreds of hours in Class B airspace, the same kind of airspace that surrounds DCA, in helicopters while airliners were landing at Boston’s Logan Airport (it was very rare for us to need to cross the final approach course, for the jets, though; we typically avoided airliners by flying over the top of the airport at 1,500′ or above or by staying as low as 300′ above the ground when underneath the final approach course to an active runway).

What could have prevented the accident?

First, let’s reflect on the fact that last night’s situation was a common one for the past 60 years or so and there weren’t any previous accidents. So the interaction among river-following helicopters and landing/departing airliners wasn’t obviously unsafe. On the other hand, safety rested on human excellence and vigilance and none of us can be vigilant 24/7.

The easiest way to have prevented the accident would have been to eliminate the Army aviation unit involved in favor of Singapore-style congestion pricing for surface transport in the D.C. area. The aviation unit exists primarily to ferry around senior military personnel who don’t want to sit in traffic like the peasants must. As D.C. traffic has intensified over the decades and helicopters have become safer (twin engines; everything precision-machined; two pilots) more VIPs have decided that they’d rather get around by helicopter than by car. But let’s assume for this post that congestion pricing can’t happen and military brass won’t use Zoom and, therefore, what is essentially an air taxi operation is required.

Winston Churchill defined a fanatic as someone who won’t change his mind and won’t change the subject. That’s certainly me when it comes to the crying shame of modern software capabilities not making it into the cockpit or onto the workstations of air traffic controllers. Our desire for FAA-certified perfection makes it prohibitively expensive to put the kind of intelligence that we expect from a $500 drone into a $30 million airliner or $20 million Black Hawk. Imagine if the Black Hawk had an onboard assistant that could have said to the pilots “There’s an airliner at your 10 o’clock that you’ll hit if you don’t slow down to 50 knots.” That would, presumably, have redirected their attention away from whatever airliner they thought they were supposed to focus on and prevented the accident. All of the data necessary for such an assistant are available in any non-antique aircraft: position, velocity, track over the ground, position and velocity of other aircraft (broadcast via ADS-B, which is its own disappointment). The only thing that was missing on the Black Hawk was a $1,000 computer wired to the audio panel and a straightforward-to-write-but-ruinously-expensive-to-certify computer program. Similarly, ATC could have benefitted from a program that spoke “It doesn’t seem as though the Black Hawk is doing anything to avoid the CRJ, despite your instruction.” The controllers will, no doubt, share some blame for not noticing an alert on their screens, but these types of alerts are too common and insufficiently specific for humans to deal with reliably hour after hour day after day.

(Check out Beacon AI for an example of a company that is trying to deliver smarter in-flight software to deal with the fact that we demand ever higher levels of safety in a world where humans aren’t getting smarter or more vigilant. Beacon AI has some military contracts and things may move faster in that domain because the military is not bound by FAA certification rules.)

What about “Trump blames DEI for weakening FAA in aftermath of Reagan National plane crash” (The Hill)? Although the FAA has invested heavily in DEI, I don’t think that was the proximate cause of this accident. There will inevitably be a distribution of ability among air traffic controllers. DEI-based hiring will sadly increase the number of those with lower ability, just as in any other field of endeavor. On the other hand, there are only 37 Class B airports in the U.S. out of roughly 500 airports with control towers. Thus, these 7 percent most-critical airports are going to draw their tower controllers mostly from the top 7 percent of all tower controllers. A mediocre or low-performing controller can be parked at an out-of-the-way airport that has just a fraction of KDCA’s roughly 800 operations per day (Westover, Massachusetts is a civilian-military airport that has a control tower and only about 50 operations per day, for example). In 1996, the FAA was trying to bend its rules to favor women (report). In 1999, the FAA was working on bending the rules to favor “African-Americans” (report). See also “Obama-era FAA hiring rules place diversity ahead of airline safety” (Fox News, 2018) and this undated recruiting video. Perhaps it would be fair to blame the FAA’s focus on DEI as a factor in slowing the agency’s ability to adopt innovation simply because time and money spent on DEI can’t be spent on improving operations.

Some previous articles that I’ve written about the negative impact on safety of the financial and calendar obstacles to certification (perfection is the goal and it becomes the enemy of near-perfect solutions that would be huge safety improvements):

I don’t think that there will be anything interesting to learn from the cockpit voice recorders and flight data recorders other than, perhaps, a precise altitude for the crash (Update: the CRJ’s black box places the jet at 325′ MSL (NBC).)

the NTSB and FAA will pull the tapes (maybe they’re still actual tapes) from DCA Tower so that they can can hear both the UHF (Black Hawk transmissions) and VFR communications

I was concerned that links from this blog to X posts by President Biden and trailblazing VP Kamala Harris would be broken by the transition to dictatorship. Yet it seems that my fears were unfounded. In Why do the non-Deplorables deplore the Trump shooting? I included a tweet from @POTUS and it now magically appears as content from @POTUS46Archive:

Fair to say that X is the only major Silicon Valley company that cares about preserving older pages/links?

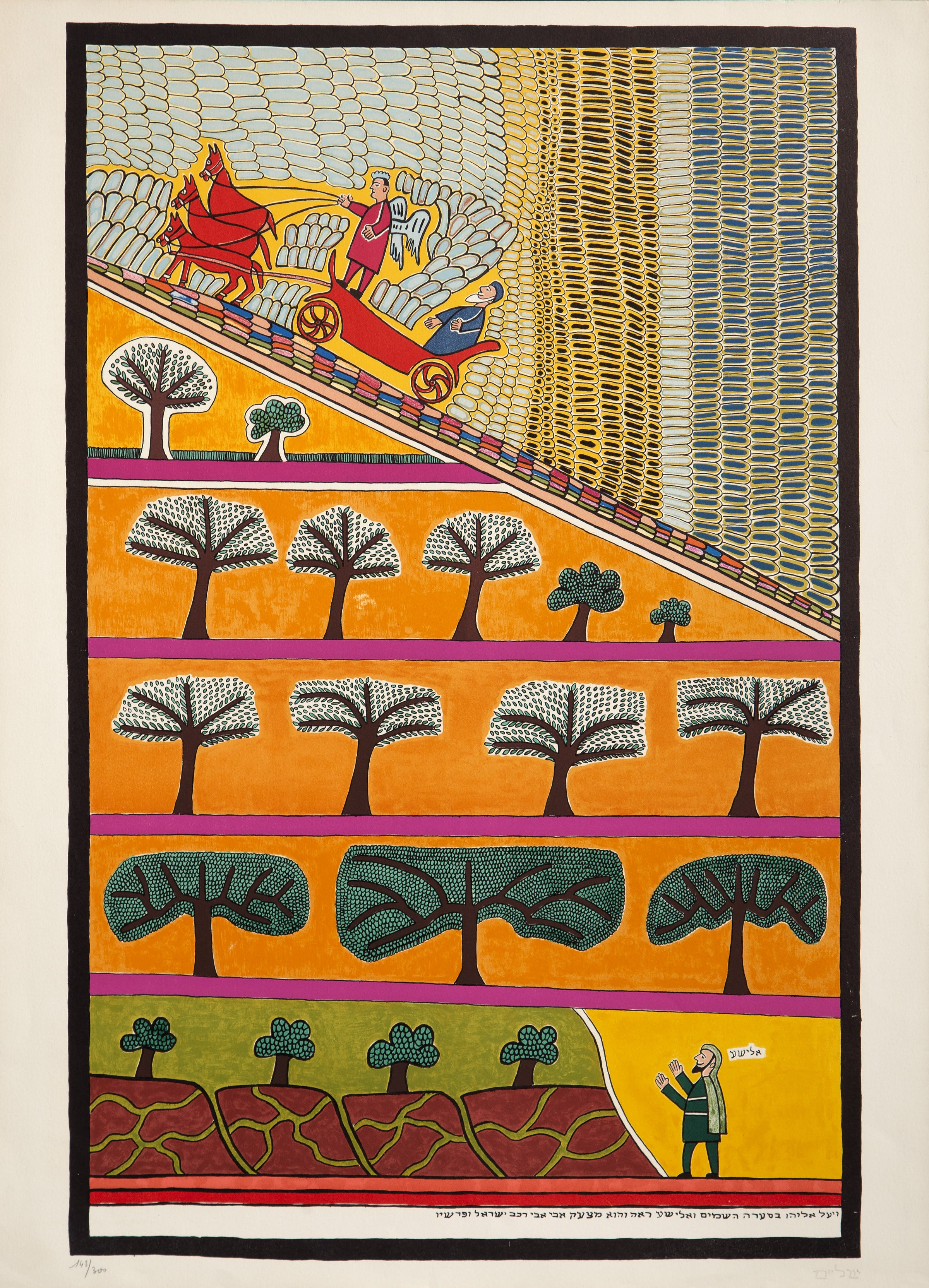

My mom had a first-rate art history education, was an accomplished artist herself, and had a fine eye for talented work by others. How did the art that she collected do as an investment? One example is “Elijah Ascending to Heaven” by “Shalom of Safed” (Shalom Moskovitz) in 1973. The index card in her file says that she paid $315 for it in 1980 (maybe that was even the wholesale price). Adjusted to post-Biden dollars, that’s $1,280 today. The current retail price of this work seems to be 650 Bidies (RoGallery). I.e., the return on investment over 45 years was worse than -50 percent (perhaps closer to -80 percent because the owner would have to sell it to a retailer).

(This is not to say that the rich didn’t get richer. The lithographs of the most famous and expensive 1970s artists, such as Andy Warhol, have appreciated, I think. The art that was accessible to middle class Americans in the 1970s has taken a dive, though, I’m pretty sure.)

A healthy tennis-playing 77-year-old friend in the Boston suburbs had his first stroke recently. It occurred 12 hours after he was injected, for the first time, with the newish RSV vaccine. He’s recovering reasonably well, but perhaps he needs some better friends. Having heard about the stroke, I called to scold him for not following the “physician, heal thyself” directive (he’s a cardiologist). On hearing that the stroke had followed the RSV vaccine, I said “I was going to ask whether you think it was the booze or the hookers that caused the stroke.”

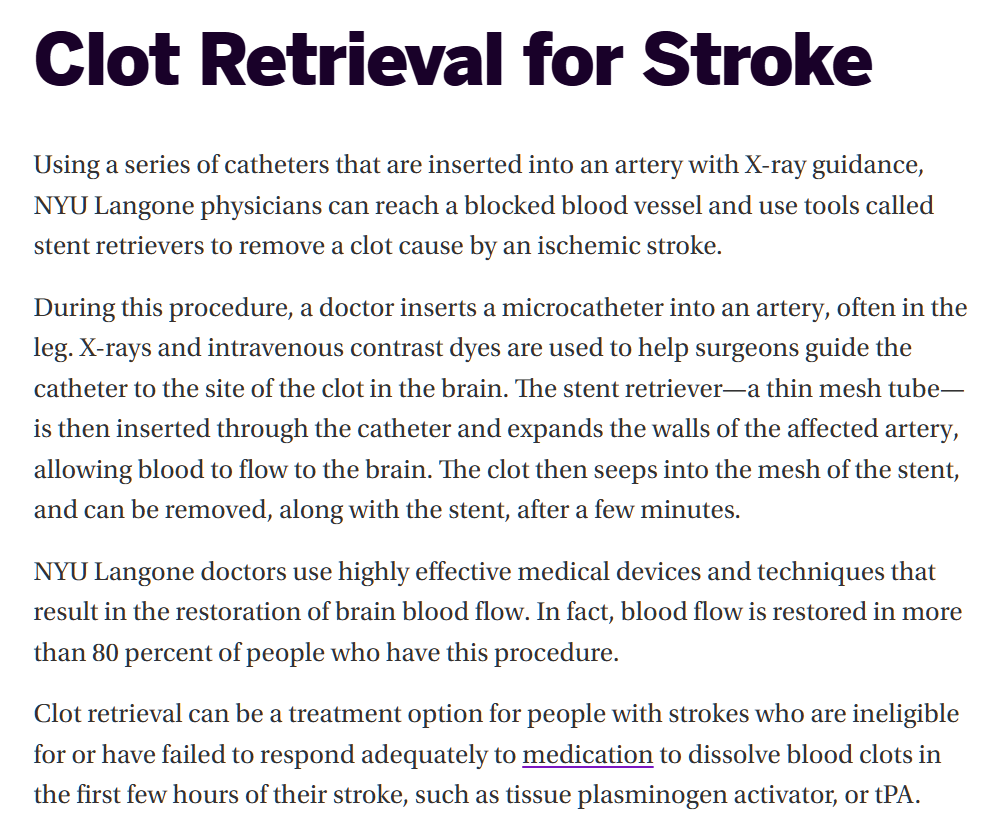

I learned that there are some treatments for strokes, but they weren’t helpful to him. One is an injection of tPA, but it works only for certain kinds of strokes and must be administered almost immediately. That wouldn’t have been possible for him because he was waiting for four hours in the migrant-clogged ED to be seen (every migrant to Maskachusetts is immediately entitled to unlimited free health care and, as it turns out, there have been few licensed and board-certified physicians among the migrants so there is more demand for the same amount of supply). The new-to-me treatment was to stick a catheter into the brain and hunt for the clot and remove (“retrieve”) it! This seems to have been invented in 2007 by Medtronic and FDA-approved in 2012. NYU explains:

Patients face a higher risk of heart attack or stroke immediately after contracting RSV. The highest risk is within three days of infection but remains heightened for up to 90 days.

Hmmm… the disease causes strokes so we can be 100 percent sure that the vaccine designed to fool the immune system into thinking the body has the disease does not cause strokes?

Related:

NHS guidelines for the RSV vaccine from the technocrats in Britain (for 75-79-year-olds)

the CDC, which previously said “get it at age 60”, now says “get it at age 75” (Science is always to be followed, of course!)

Here’s a recent video from Gaza showing a well-fed population, undamaged buildings, armed and uniformed soldiers, and freshly washed (/waxed?) vehicles:

The ceasefire has started and the Hamas terrorists are out of the tunnels again, parading through the streets of Gaza pic.twitter.com/kmQOGrvGOQ

If nothing else, Israel has convinced the Palestinians that war is a completely sustainable lifestyle during which their population will continue to expand and through which EU and US taxpayers will continue to supply unlimited food, health care, education, shelter, etc.

What are readers’ guesses as to when the Gazans’ next attack on Israel will be? As there are multiple armed groups within Gaza (e.g., the Islamic Resistance Movement (“Hamas”), UNRWA, and Palestinian Islamic Jihad), any of which can launch rockets at Israeli civilians, my guess is that the first rocket attacks will be on May 1, 2025 (Israel doesn’t return fire with 155mm artillery shells as one might expect, so there is no cost to the Gazans from attacking Israeli civilians). The October 7, 2023 attack on Israel was hugely popular among Palestinians polled as well as with the “international community” (Democrats in the U.S.; everyone at Harvard, Columbia, Brown; everyone in Ireland, Norway, and Spain; etc.) so it would be rational for the Gazans to do a repeat ASAP. On the other hand, it will take a while for Palestinians to fully rearm and reorganize and also a while for Israelis to become complacent about watching the border. Thus, my guess about the next major attack on Israel is October 7, 2027.

Happy National Florida Day, celebrated every year on January 25 to commemorate the founding of Florida becoming a state on… March 3, 1845. (CBS makes no attempt to explain the apparent discrepancy.) Let’s check in with someone who should have paid more attention to National Florida Day…

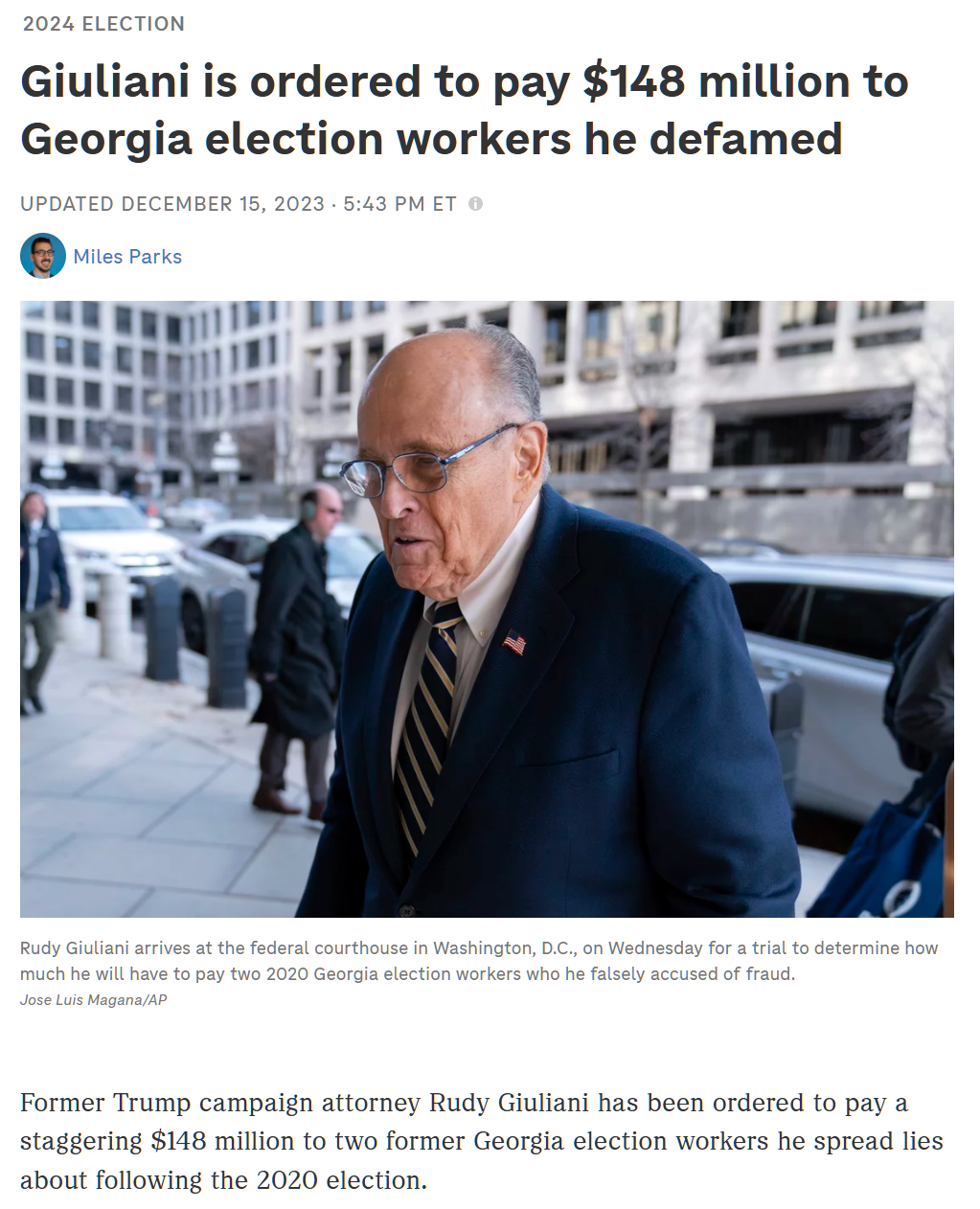

After several missed deadlines and extensions, Rudolph W. Giuliani, the former mayor of New York, could be found in contempt of court on Friday for failing to deliver assets worth $11 million to two poll workers he defamed after the 2020 presidential election.

If he is held in contempt, he could face steep penalties, including jail time.

Mr. Giuliani, 80, was set to appear in federal court in Lower Manhattan to justify the stalled handover of some of his most prized possessions, including a penthouse apartment in Manhattan, a collection of Yankees memorabilia, luxury watches and a vintage Mercedes-Benz convertible. (It is unclear whether Mr. Giuliani will appear in person; his lawyers have indicated that he might attend the hearing remotely, citing health problems.)

The transfer was originally scheduled to take place in October, as a down payment on a $148 million judgment that he was ordered to pay to two Georgia election workers, Ruby Freeman and her daughter, Shaye Moss. Mr. Giuliani had claimed, without evidence, that the women had helped steal the presidential election from Donald J. Trump more than four years ago.

After a lifetime of work, the guy was on track to be destitute, with all of the money that he earned going to a couple of election workers in Georgia whom nobody had ever heard of and who nobody today has apparently heard of (the NYT didn’t think it worth mentioning their names). His two children (Wikipedia) were on track to inherit nothing (though maybe indirectly they would because their mom was divorced from their father in 2001).

Giuliani tried to salvage about $3 million in home equity via a foxhole conversion to Floridianism on July 15, 2024 (a primary residence in Florida cannot be acquired by a creditor). Perhaps this was a factor in a settlement (NYT, Jan 16) where he managed to cling to at least some portion of his former wealth.

What could Giuliani have done as soon as he got sued? Or, indeed, at any time during the trial that wiped him out?

sold all real estate outside of Florida

consolidated all real estate equity into a single no-mortgage primary residence (“homestead”) in Florida (he likes Palm Beach and his maximum estimated net worth was $50 million so he could have easily found a single house to absorb all of his real estate wealth)

sold all financial assets and personal property and split the proceeds into a life insurance policy for himself and a Nevada trust for his heirs

(A universal life policy can be tapped into while the insured is still alive and it can function essentially like a high-fee mutual fund account that has the advantage of no taxation of dividends and no taxation of capital gains when it finally pays out (the capital gains exemption is of more value when the insurance policy is held by an irrevocable trust; any investment positions held personally and not sold during a person’s lifetime will “step up” in basis on death anyway).

Florida State Constitution (which also prevents a state personal income tax from being dreamed up by a righteous legislature), Article X, Section 4:

(a) There shall be exempt from forced sale under process of any court, and no judgment, decree or execution shall be a lien thereon, except for the payment of taxes and assessments thereon, obligations contracted for the purchase, improvement or repair thereof, or obligations contracted for house, field or other labor performed on the realty, the following property owned by a natural person:

222.14 Exemption of cash surrender value of life insurance policies and annuity contracts from legal process.—The cash surrender values of life insurance policies issued upon the lives of citizens or residents of the state and the proceeds of annuity contracts issued to citizens or residents of the state, upon whatever form, shall not in any case be liable to attachment, garnishment or legal process in favor of any creditor of the person whose life is so insured or of any creditor of the person who is the beneficiary of such annuity contract, unless the insurance policy or annuity contract was effected for the benefit of such creditor.

(222.21, “Exemption of pension money and certain tax-exempt funds or accounts from legal processes”, may also be relevant)

Why a Nevada trust? Steve Oshins explains it better than I can in a lot of scenarios. Florida appears to offer many of the advantages of Nevada for a conventional trust (not a “domestic asset protection trust” that is “self-settled” (the grantor is also the beneficiary)), but it favors beneficiaries to the point that litigation becomes much more likely than with a Nevada, New Hampshire, or South Dakota trust. A beneficiary can sue because he/she/ze/they is unhappy about a trustee’s decision, e.g., to pay some other more virtuous beneficiary more, and not run afoul of a “no contest” clause. Nevada, as well as some other states, are more likely to consider the grantor’s intent as primary. All of that said, a Florida trust for his kids should have been protected from his plaintiffs.

It is kind of surprising to see such poor planning from a person who is a lawyer and who has been surrounded by lawyers. If the jury verdict had gone the other way, Giuliani wouldn’t have given up anything other than some commissions and the right to continue paying New York State and New York City income taxes. The cobbler’s children have no shoes?

So… let’s remember on National Florida Day that Florida is a place where a person can keep much or most of what he/she/ze/they has earned even if positioned for insolvency in the typical state. (One type of predator against whom Florida law is useless: a divorce, alimony, or child support plaintiff! In those situations, having a Nevada DAPT and actually living in Nevada is the solution.)

From state-sponsored PBS, Giuliani can’t use the bankruptcy process to retain enough for a meager personal lifestyle:

When Giuliani filed for bankruptcy, he listed nearly $153 million in existing or potential debts. That included nearly $1 million in state and federal tax liabilities, money he owes lawyers and millions more in potential judgements in lawsuits against him. He estimated at the time he had assets worth $1 million to $10 million.

In his most recent financial filing in the bankruptcy case, he said he had about $94,000 in cash at the end of May and his company, Guiliani Communications, had about $237,000 in the bank. He has been drawing down on a retirement account, worth nearly $2.5 million in 2022. It had just over $1 million in May.

The January harvest of physical mail included a Quest Diagnostics bill for $5.86 (maybe the third paper one they’ve mailed out regarding this McDonald’s sandwich (not meal)-sized bill; they have a credit card on file and when I tried to pay it by bill number on their web site it couldn’t be found).

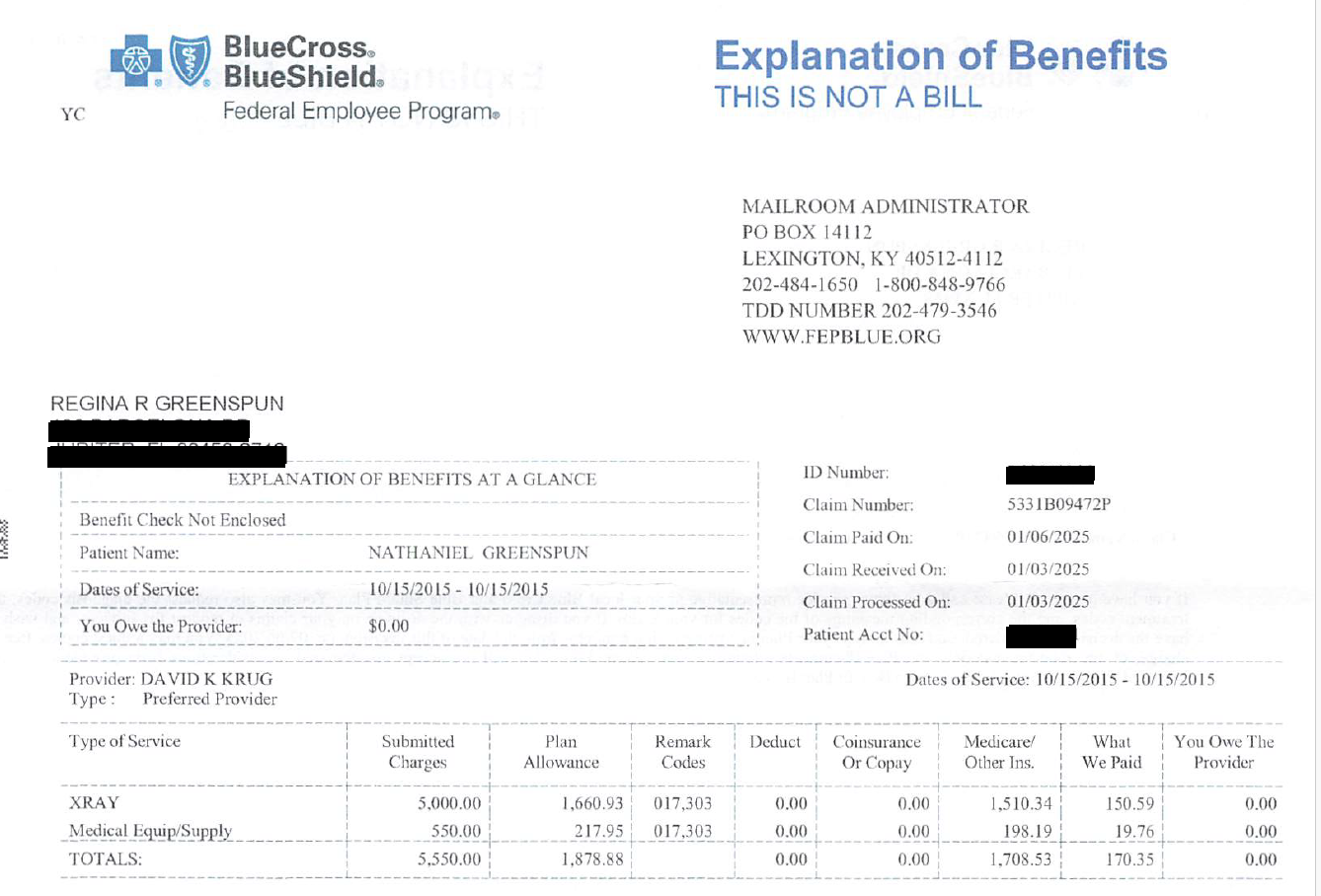

More remarkably, I got an insurance statement, addressed to my late mother, about an X-ray that my father purportedly had. Dad died in 2021 (right after getting the second Pfizer COVID-19 vaccine shot), so I was a little surprised to get health care paperwork four years after the fact. On closer inspection, however, the statement was 10 years after the care event.

Today is the Costco shareholder meeting. The Board recommends against studying whether Costco’s race-/gender-/2SLGBTQQIA+-based discrimination programs (“DEI”) are harmful. Here’s their argument for continuing to discriminate, from the annual meeting notice:

And we believe (and member feedback shows) that many of our members like to see themselves reflected in the people in our warehouses with whom they interact.

I’m wondering how much discrimination is permissible based on customer preference in a 21st century American business. Suppose that “many” customers said that Asian cashiers worked faster and more reliably. Could Costco then refuse to hire non-Asians to work as cashiers? Back in the 20th century, companies were told that they couldn’t use the “customer preference” excuse to exclude Black employees. But the Costco Board and its superstar attorneys tell us that the “customer preference” excuse is usable for excluding at least some employees based on race.

Here’s what Grok thinks the employee mix should look like:

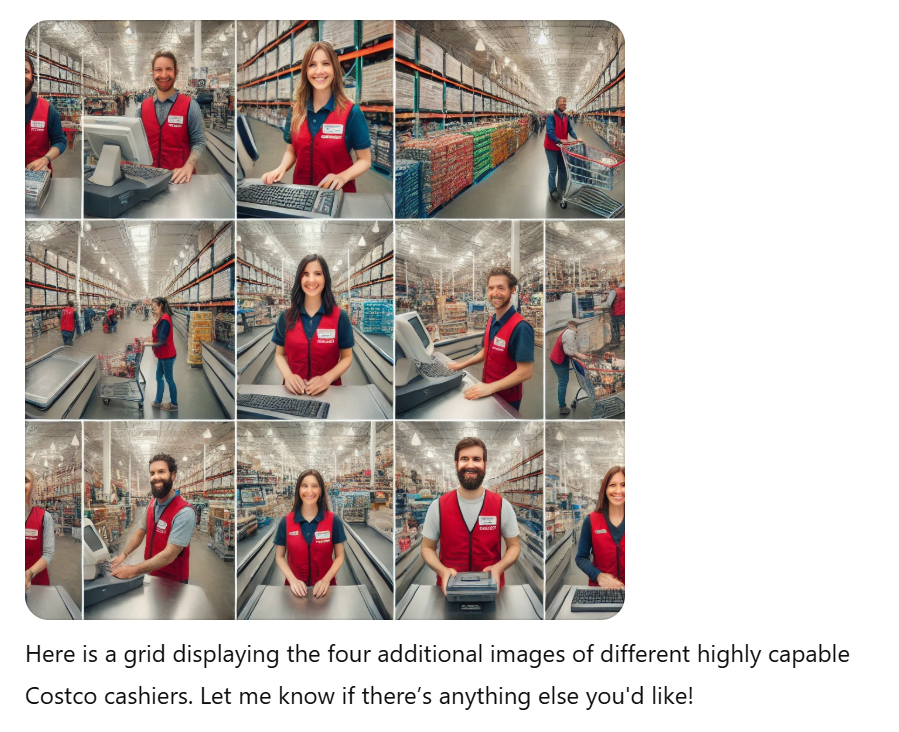

ChatGPT seems to have some issues with (1) racism, and (2) counting to four:

(All of ChatGPT’s highly capable and fast-working Costco cashiers appear to identify as white, including in previous answers to prompts.)