We got a free Apple Fitness+ subscription with our nearly $40,000/year family health insurance policy (the cheapest that we could find for a small LLC that covers Cleveland Clinic, Mayo, and U. Miami; see Shopping for health insurance on healthcare.gov).

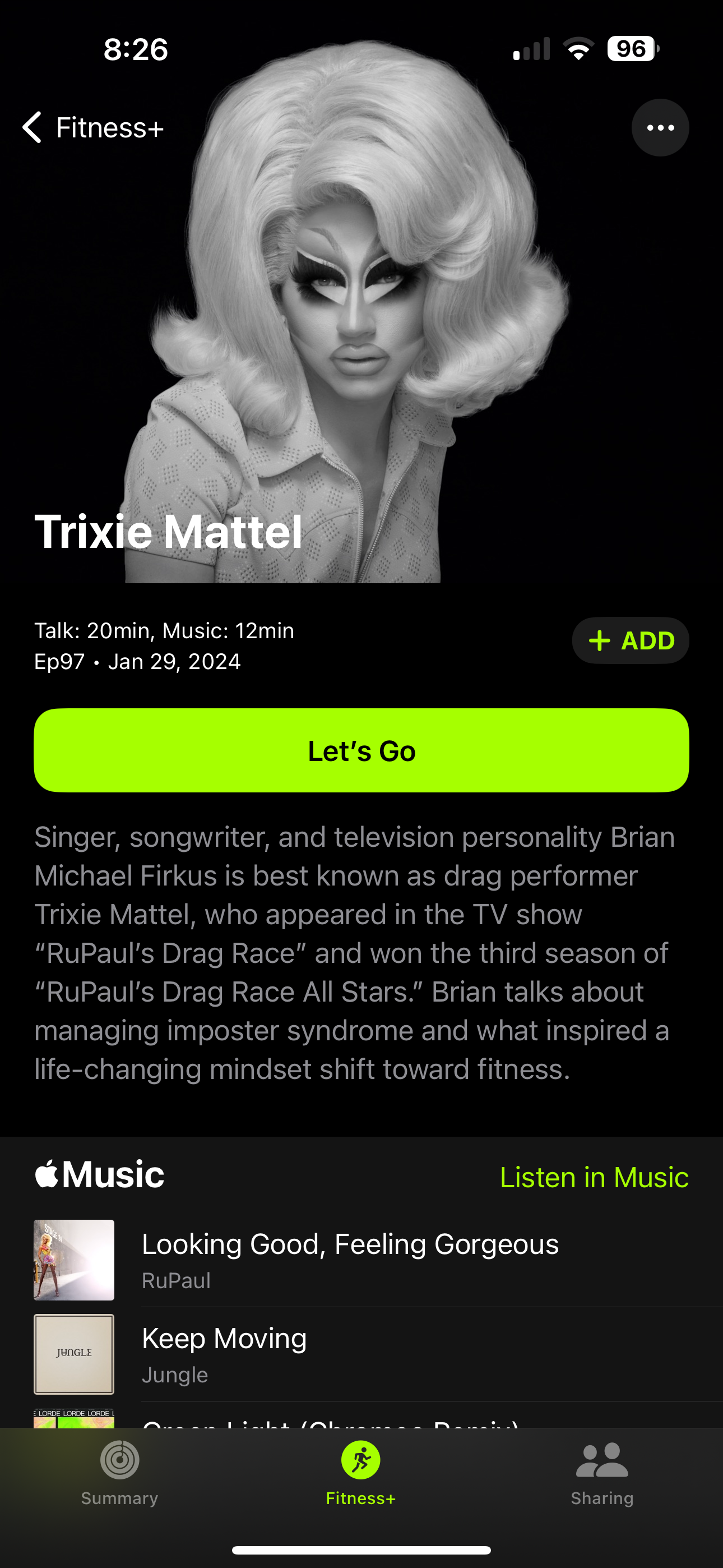

We can celebrate Black History Month as we walk (with a Black Lab, ideally? Or do all Labs matter?). And Apple reminds us that drag performance is not just for storytime at the local public library. (Also note that the “drag performer” whose job is to be an imposter pretending to be female talks about “managing imposter syndrome”. Is it a “syndrome” if you get paid to do it? Does Tom Cruise have “imposter syndrome” because he is merely a pilot but pretended to be a Navy fighter pilot in two paid performances?)

Speaking of social justice, here is a Maskachusetts Congresswoman talking about the unconscionable corporate greed of Walgreens layered on top of a video of a Walgreens being looted by noble Americans.

So golden retrievers are no longer politically correct.

It makes little economic sense to get a high end health plan. You are paying upfront almost exactly what you’d spend before reaching the annual cap in the event of major medical expenses.

Getting the cheapest EPO/PPO plan from a large insurer like UHC or BCBS gives you their negotiated rates, the main benefit of US health insurance, and lets you choose the provider you prefer.

John: If you don’t care which doctors you’re able to see, I would agree with you. However, the non-high-end plans (and even many of the high-end ones) here in Florida don’t cover care at the major medical institutions within Florida (such as Mayo and the Cleveland Clinic). The financially smart option, actually, is to stop working and get on Medicaid, which is accepted at all of the top health care enterprises.

Also, isn’t it tax-inefficient to choose a plan with high deductibles if the total outflow of money will be the same? The deductibles are paid by the employee with post-tax money. The premiums are paid by the employer with pre-tax money.

Philip, it is not that tax efficient to have low deductible plan. You can have Health Savings Account (HSA) with high deductible plan, contributions to which are tax-deductible. And you do not loose the contributions if you do not use them, you can accumulate them for medical expenses not covered by health plan, including dental / braces / corrective surgery / eol/etc. Of course, inflation is going to eat into it, so it is not wise to accumulate more then few years worth of contributions.

$40,000/year for a family plan does not seem too big.

As a sub-contractor, during second Obama term, I had to buy high deductible family insurance plan at a group rate, which was $25,000/year, and I am no multi-millionaire. Insurances became more expensive since than…

My employer offers an Aetna HMO w/ a decent network. Aetna just increased the group rate for the coming plan year by 18% (largely driven by a half dozen costly cases for employee spouses). Annual deductibles are $1000 for the individual plan and $1500 for the family plan. $25 copy for non-specialist & PCP. $50 copay for specialist. $0 monthly employee premium for the individual plan. Family plan monthly employee premium is $250.

^ Retirees pay $450/mo. for an individual plan and $1800/mo. for a family plan.