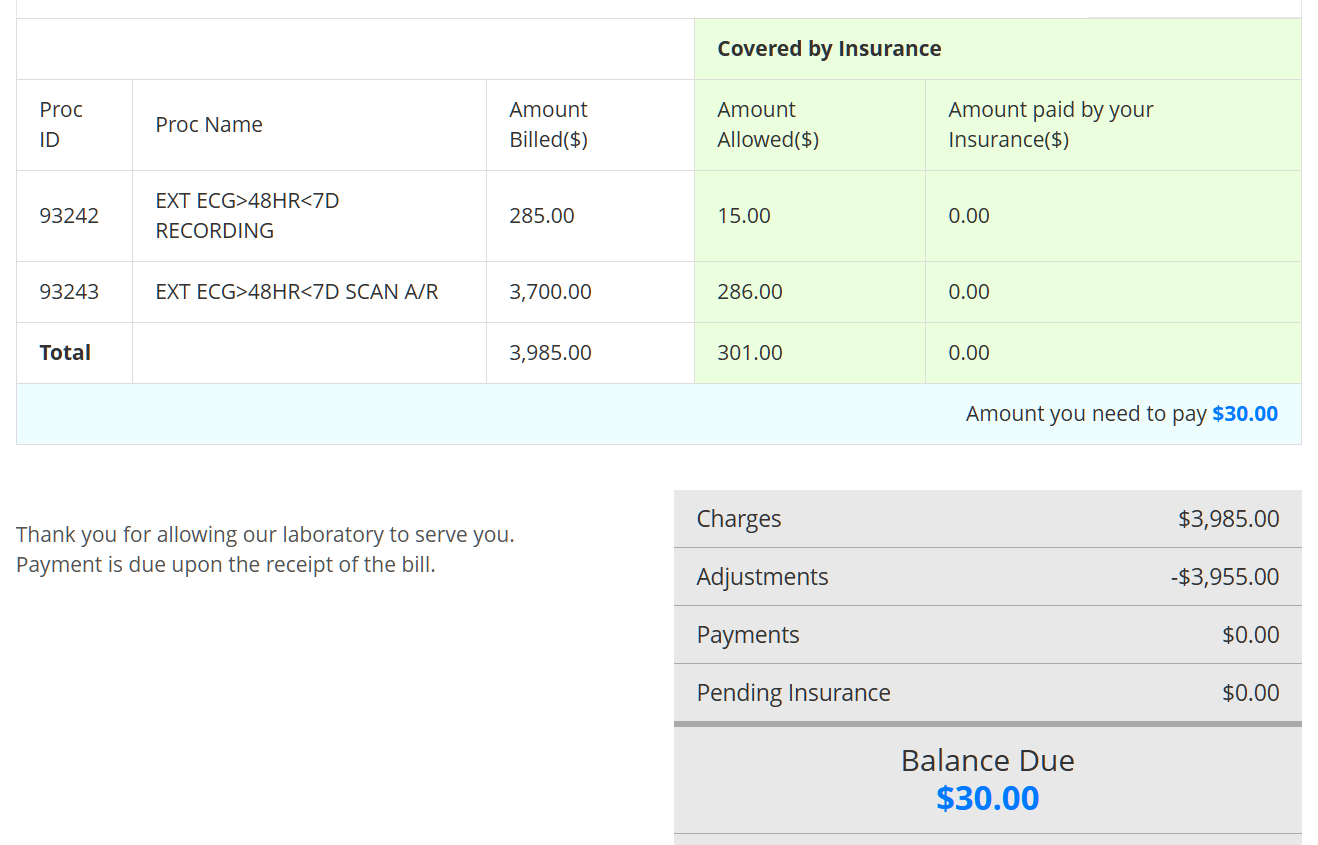

Here’s an August 2024 bill for a walk-around heart monitor that was used by a patient in February 2024:

The price to an uninsured person would have been more than 10X the real price of the service ($3985 vs. $331).

I still can’t understand how it is legal for health care providers to lie in wait for the unwary uninsured patients and hope that someone slips through the cracks somehow and becomes liable for more than 10X the regular price for a service.

I’m convinced that more than 90 percent of the medical bill bankruptcies and disputes in the U.S. would be eliminated if the Feds established a “If you want to feed from the Medicare/Medicaid trough, you can’t bill an uninsured patient more than a 15 percent premium over the Medicare price” rule.

Meanwhile, Chinese men woke up to find they would no longer be retiring at 60 but now 63. Chinese women discovered they would no longer retire at 55 but 58. A story of things to come, as regards US.

Theoretically, all the money goes to malpractice lawsuits & expert witnesses. Wonder who the over 65 heart patient is.

“Chinese men woke up to find they would no longer be retiring at 60 but now 63.”

In 2011, the Florida Retirement System (for hybrid defined benefit/defined contribution retirement plan) for all FL state & county workers and many municipal workers) increased the full retirement age (for non-public safety workers) from 62 to 65 years of age. Public safety “heroes” can still retire at age 55 w/ at least 8 years of chair time.

I am baffled at how medical providers can get away with this, legally. Under traditional contract law, the customer has to have an understanding of the fees. My auto mechanic gives me a written estimate in advance. When the medical providers sue their patients into bankruptcy, what happens when the patients tell the judge that they never agreed to the specific charges?

Philip, you’re absolutely right. The real question is: how do such obviously absurd and abusive practices remain legal? In my view, there isn’t enough public pressure to change the system, and many benefit from the current state of affairs—healthcare represents almost 20% of the GDP.

The level of ignorance about the true nature of healthcare in this country never ceases to amaze me. Many Medicare recipients oppose “socialized medicine” and “single-payer systems.” Plenty of workers who see $20k per year taken from their paychecks believe that “the cost of healthcare is covered by my employer.” Medicaid recipients, of course, don’t care about the costs. So, who is left?

Oddly enough, once I visited a specialist at a hospital where the indifferent worker failed to record my insurance, which was Blue Cross Blue Shield from a state government job.

The hospital sent me a bill to the effect of “We see that you are uninsured, so here’s a cash discount,” and the discounted rate was less than the BCBS “network rate.”

It’s strange.

The ACA is also a scam because the sum of the premiums and out of pocket maximum is a very significant portion of income…say 30% (I don’t have the numbers in front of me), but people making say $20k/year are having to choose between rent and food and are not in a position of spending 30% of their income on healthcare.

I’m not a fan of the ACA (it does not deal with the central issue of healthcare in the US: cost). However, I believe ACA is substantially free for someone who makes $20-30/year.

Many uninsured patients (recent arrived migrants, for example) don’t pay. The hospital is better off offering a “payable rate” than collecting zero. Now, if you have assets… you’ll have to pay the “customary charges” or face the consequences.

It pays to be poor!

Anonymous, your belief is wrong!

In the $20k-$30k, the premiums could be about $275/month and the out of pocket maximum several thousand additionally.

It is only “almost free” for people very close to the poverty line at $13k. Up to $50k it is like an extremely progressive tax. The only way to make it work is to either stay below $15k/year or so or make several multiples of $50k so that the cost, while considerable, is manageable.

You could both be right. I think that Obamacare subsidies (not “welfare”!) vary quite a bit from state to state.

I know in FL, if you earn a very low income, something like less than $17,000 per year (MAGI) as an individual, you won’t qualify for an ACA plan. The intent is that such an individual is to go in Medicaid. But FL is one of the states that did not expand Medicaid eligibility. So this FL resident low-income earner will not qualify for either Medicaid or ACA.

And ACA subsidies phase out at about 70K MAGA (individual).

At least this were all true about two years ago when I extensively experimented on healthcare.gov

Actually, with ACA you don’t have to be poor to take advantage of the subsidies. It is income based, so you can have millions and still pay little.

https://www.cnbc.com/2016/01/27/theyre-millionaires-and-they-get-obamacare-subsidies.html

Anon: A friend was living in a $2 million house in suburban Boston, which the bureaucrats handing out free health care could easily have found out by looking up his address in Zillow. He entered accurate numbers into the Maskachusetts Health Connector web site (the state’s own Obamacare site) and it popped out that he was eligible for MassHealth, the state’s version of Medicaid. The forms never asked “Do you have more than $10 million sitting in stocks?” His health insurance bill went from about $30,000/year (two adults and two kids) in pre-Biden money to $3/month. Being on MassHealth meant that every doctor and hospital was now available so he never needed to search for an “in-network” provider again.

Healthcare in the US is a casino and the users are not the house. Actually, it is a casino subsidized by taxpayers.