From Pedro Domingos, a CS prof at University of Washington, the best current explanation for stratospheric stock market valuations:

Oracle’s main business these days is promising vast amounts of cloud computing it doesn’t have to AI companies who don’t know how they’ll pay for it.

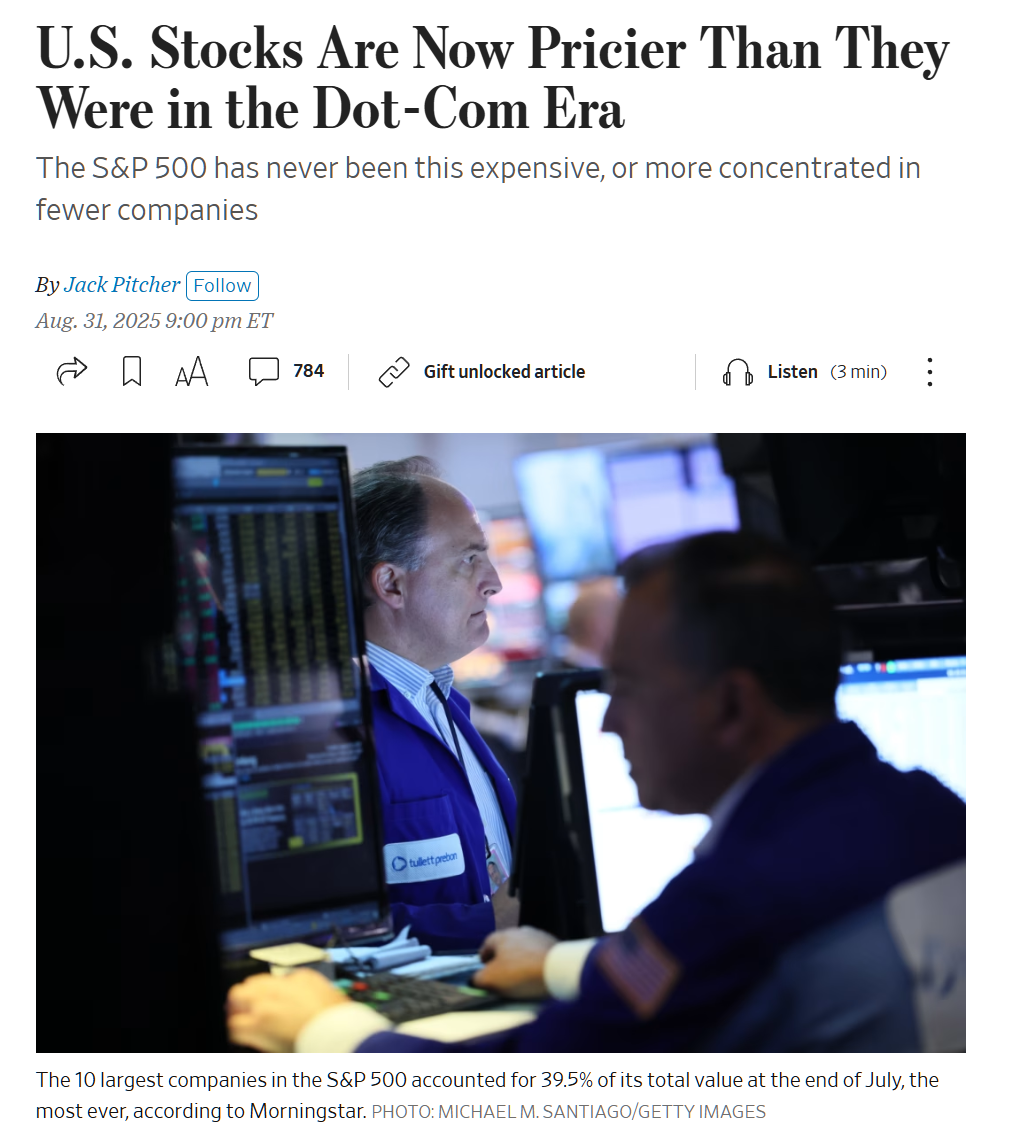

WSJ, a month ago:

The S&P 500 currently trades at 22.5 times its projected earnings over the next 12 months, compared with the average of 16.8 times since 2000. … The 10 largest companies in the S&P 500 accounted for 39.5% of its total value at the end of July, the most ever…

How badly beaten up did investors who bought into stocks at a high P/E ratio get? I asked Grok “Consider an investor who purchased the S&P 500 in February 2000. What annual return on investment would he or she have received through August 2025 vs. an investor who bought in August 2002 and held through August 2025?” and learned that the “Peak P/E ratio” investor (bought before the dotcom bubble burst) would have earned a compound annual growth rate (CAGR) of about 6.3% vs 8.9% for an investor who bought at a more reasonable P/E ratio in August 2002. This difference is close to the difference between investing from 2002-2025 in wired U.S. (9%) vs. tired Europe (5.7%).

If it is considered troubling by WSJ then it is a sure sign to invest in US equities. WSJ was not troubled by unrealistic, infinity of second order valuations (since they were loosing money) IPOs valuations during IPO fraud of the 1990th. I was troubled, invested accordingly and mostly did not get burned, with an exception.

It feels like the eternal question is this, if the stock market is overvalued what is the alternative? Especially since for so many people, the potential investments are defined by the options presented by their 401K program which I think can be boiled down to stocks, bonds, and maybe something like a REIT.

For small money, individual investors what options do we have?

And then, maybe the stock market is overvalued because future inflation is priced in? That is, the only investment advice I really believe is, in inflationary times go to equities.

Daniel: inflation paranoia is the reason I am 100% in equities and 0% bonds. Governments have figured out that their subjects can’t think straight when it comes to inflation adjustment (“money illusion”) so 2-5% inflation always makes everyone feel better about their financial situation.

Not investment advice but my winner this year is gold. (Or rather, funds investing in gold miners.)

No other place to put money, with interest rates headed back to 0, houses out of reach. It’s possible earnings inflate & catch up to the market cap. Another outcome is the S&P going sideways. We don’t know how far it’s going to rise before the big correction but there will definitely be a correction of at least 30%. The difference is there’s no cash on the sidelines to buy the dip, as there was 5 years ago.

The S&P is still behind the nikkei 225 before it permanently lost 75%. Both indexes were concentrated in a few stonks. The Nikkei was the only index so far to never recover in a generation. The lion kingdom is still 50% in cash, having lived through the fixed income craze of the 2000’s, the rental property craze of the 2010’s & the index fund craze of today. A 75% drop wouldn’t be too bad if you’re up 100% as most animals are or if your total investment is 4x more than you’ll ever need.

At the risk of doing the cliche thing of basic financial advisor arithmetic:

A 3% return difference, compounded over 25 years is roughly a double (6% vs 9% annually).

The bear market from peak to trough ’00 to ’02 roughly cut the market in half, at the absolute extremes.

Someone who rebalanced to value or bonds in ’00 would have outperformed an indexer, provided they moved back into equities once tech-media-telecom dropped from 50% to 15% of the market in ’02. “Rebalancing to value” is key here; it doesn’t have to be cash and it doesn’t have to be forever.

If you really don’t need any cash flow from investments for 25 years, by all means stick to 100% index funds.

I studied machine learning under Pedro. Smart guy – ele está sempre bem vestido. In stark contrast to all the other CS profs at UW for so many reasons. In the darkest parts of the lockdown he was the rare voice of reason and an uncomfortable truth to the UW admin. Tenure is a good thing.