“Head of Harvard’s Endowment Tells Board He Plans to Retire” (Wall Street Journal), regarding a manager paid over $6 million per year:

N.P. “Narv” Narvekar, the head of Harvard University’s nearly $57 billion endowment, recently told the endowment’s board he plans to retire, according to people familiar with the discussions. He has served nearly a decade in the post.

In the past three years, Harvard earned an annualized return of 8.1%, a rate that topped that of Ivy League rivals Yale and Princeton and which placed it in a tie for fourth among a group of 12 top schools, according to financial technology company Markov Processes International.

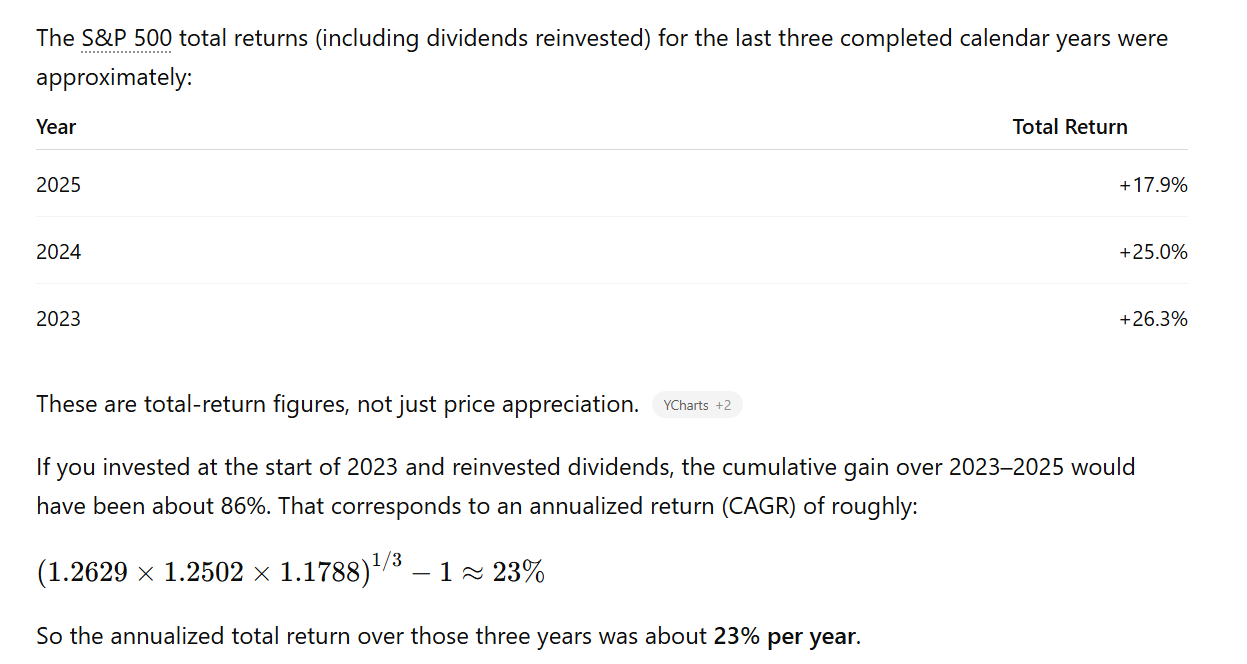

The Wall Street Journal doesn’t bother to ask Edward Tufte’s question, “Compared to What?” But ChatGPT can come to the rescue:

In other words, one can get paid $6 million per year for dramatic underperformance relative to the simplest imaginable investment strategy, dumping everything into the S&P 500 (a 23% annual return vs. the 8% achieved by Mr. Narvekar and subordinates). That’s a career almost as good as “receptionist in NVIDIA branch office”!

It’s actually worse than that, how much did Harvard spend to achieve that unimpressive rate of return? The financial services industry has to be one of the greatest scams in the world, parasitically siphoning money off from trusts, pension funds, and retirement accounts in order to label themselves geniuses and deliver worse rates of return than blind monkeys throwing darts.

Finbro bastards. How dare they keep my 401(K) inflated, and expect a big cut of the proceeds? And (keep this low on the QT), when I lived in NYC, there was more weed smoke around Wall Street than in the dorms of NYU. Let’s call them druggies too, using performance enhancing drugs like coke and cannabis. I’d smoke less weed too if I didn’t live off the damn parasites.

Did this guy have a supervisor? I would have PIP-ed him after a couple years.

I didn’t go to MIT and I don’t have any idea who Tufte is (although I did get a 36 math on the ACT) — however, shouldn’t the title be “Harvard geniuses underperform the S&P 500 by 15 *percentage points* per year” or “Harvard geniuses underperform the S&P 500 by a *factor of 4X* per year”. The Internet is an outrage engine, we have to feed it the right diet.

It would be interesting to really understand how Harvard came up with 8.1% number since about 41% of the Harvard endowment’s portfolio is in “private equity,” i.e., assets that are not valued by the market but by valuation “experts,” i.e. accountants benchmarking against supposed comparable in the public markets or constructing some sort of discounted cash flow model that goes out many years. Both methodologies can be easily manipulated. So PE is typically overvalued in a portfolio, one reason being that the accountants who value it are hired by the manager or the board overseeing the manager and won’t keep their jobs for long if they make the manager look incompetent. With PE you only know whether it has been valued correctly when it is sold. PE was and still is a big fad in endowment portfolios popularized by David Swenson of Yale, now departed. A google search of The Yale Model will come up with lots of info on Yale now trying to sell its PE. And if Yale is trying to sell its PE you can bet Harvard is also. And others. And if everyone is running for the exits, well you can bet that the prices they will realize will not be all that terrific – probably less than the carrying value of the assets. So the 8.1% number is probably overstated. Which may be a reason why this guy is exiting before the accountants insist on some large mark downs.

So…you wouldn’t have PIP-ed him? 🙂 I’d be suspicious of returns much higher than the market as well, as evidence of recklessness.

It does bring up the question “quis custodiet ipsos custodes?” Is there an independent auditor on the board and the manager (aside from Phil here)? It does seem like “you can’t beat the market, but hedge against it” in a long term, conservative endowment like this would be the policy of the university itself.

> A google search of The Yale Model will come up with lots of info on Yale now trying to sell its PE.

My search engine yielded:

https://en.wikipedia.org/wiki/David_F._Swensen#/media/File:Pioneering_Investor_David_Swensen_in_1997,_R.I.P._(51164762029).jpg

Looks like he had a unicorn horn bud on his forehead.

The lion kingdom got a 6% return, to reduce the risk. If you’re heavily in BRK, which was once the media darling, you haven’t seen a sunny day in 1 year, but a lot of animals can’t afford a 30-50% drop in the short term.

Do lions use Brave browser to surf their financial results? Do the girls in your pride pick the stocks?

https://en.wikipedia.org/wiki/Brave_(web_browser)

> Brave browser

Eich was PIP-ed for believing a marriage was between a man and a woman. Not sure if he was PIP-ed at his new company for his views on the Covid-emic. In a woke world, he was a Brave man, going around exercising his right to free speech.

https://en.wikipedia.org/wiki/Brendan_Eich#Brave_Software

> After 11 days as CEO, Eich resigned on April 3, 2014, and left Mozilla after public outrage.

Outrage made him and outrage ejected him.

“the simplest imaginable investment strategy, dumping everything into the S&P 500 (a 23% annual return vs. the 8% achieved by Mr. Narvekar”

But what is the risk adjusted return of the Harvard portfolio vs the S&P 500? Maybe a CAGR of 8.1% is good. But, as mentioned above, the expenses (including the salary and overhead for this Narv guy and his lackeys) will cut that 8.1% down.

DP: Given that Harvard is almost 400 years old and is attempting to retain hegemony for another 400 years, why would the school want to give up significant expected return in exchange for a risk reduction? They wouldn’t be able to ride out a 2008-style short-term market crash?

So there was this investor who, back in the day, used to hang around the brokerage and watch the tape or whatever. Come to find that the firm only hires Harvard grads as broker associates. “Why is this?” he asks the partner/broker. “Are they all that smarter than the fellas from Princeton or Yale?”

“Naah. It’s just that, when the analysts come up with a recommended trade, and it goes south, only the Harvard guys can talk the customer into believing they made the right call and to stay the course. They’re great schmoozers.”

You can always tell a Harvard man. But you can’t tell him much.

CCR, what about Harvard’s great women? Does Claudine Gay have anything meaningful to “tell” us?

This is an interesting read, as an adjunct to Phil’s teaching:

https://en.wikipedia.org/wiki/Harvard_University_endowment

The endowment has over 14,000 funds — how can they even keep track of all those? Looks like they had a Yalie woman, Jane Mendillo, with the excellent timing of hiring on during the Great Recession of ’08. Another former leader:

> Jack Meyer managed HMC from 1990 to September 30, 2005, beginning with an endowment worth $4.8 billion and ending with a value of $25.9 billion (including new contributions). During the last decade of his tenure, the endowment earned an annualized return of 15.9%.

From the horse’s mouth:

https://www.hmc.harvard.edu/about/#history

> Being an early entrant and bringing long-term focus has often allowed us to establish unique investment positions in less crowded areas. As a result, our portfolio has significantly outperformed a typical 60/40 stock/bond portfolio and the average endowment portfolio.

Narv was previously at Columbia, and his MBA was from Penn. “Ivy League, keep it in the family.”