Social Security’s impending insolvency is in the news lately. The system that provided Ida May Fuller with benefits that were 1000X what she paid in tax was apparently not sustainable (even Charles Ponzi couldn’t keep a scheme like that going forever!).

We were previously informed that 1 million healthy over-65 Americans had been killed by COVID-19. These people had at least 5-10 years to live, during which time they’d be receiving monthly Social Security payments. I wondered about this back in 2021 with Wave of death among the elderly bankrupts Social Security and quoted CNBC:

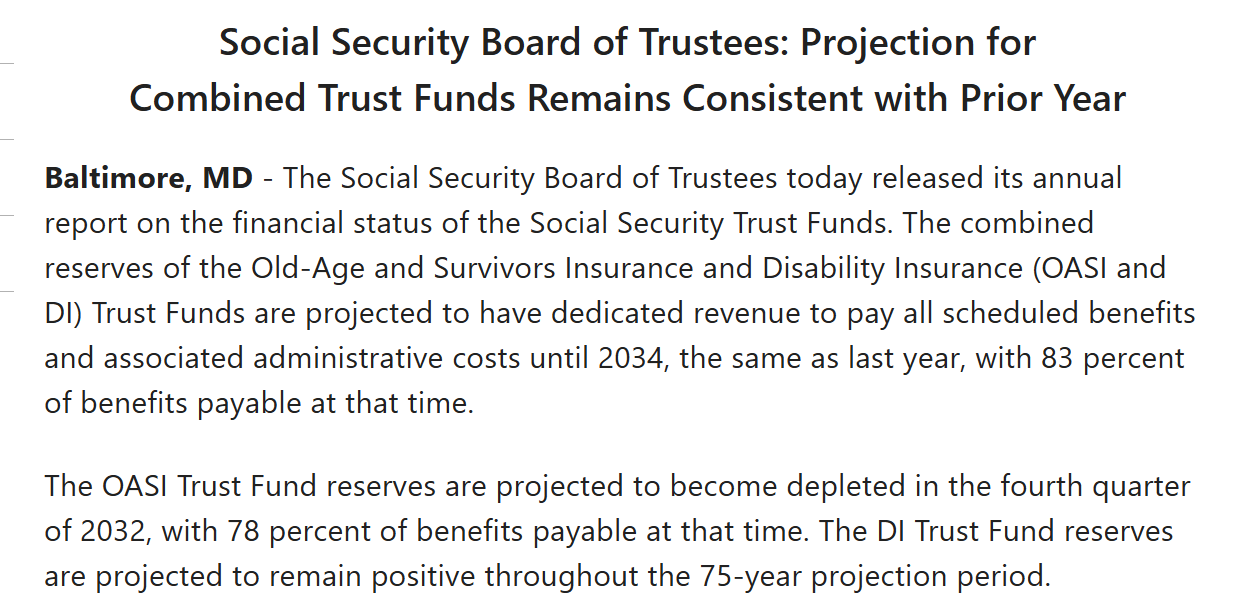

The Social Security trust fund most Americans rely on for their retirement will run out of money in 12 years, one year sooner than expected, according to an annual government report.

Social Security payments would be cut, or young people further enslaved to taxation, in 2033, in other words (2021+12). Apparently, some of those killed by COVID-19 have risen from the grave and are collecting benefits once again because the “trust fund runs out” date has moved up from 2033 to 2032 (source):

It is confusing because the above official source implies that full benefits are paid until 2034. The media, on the other hand, is reporting Social Security payments would be cut, or young people further enslaved to taxation, in 2032.

What do progressives think about this? A Maskachusetts friend who previously loved whatever Democrat thought leaders, such as AOC, Ilhan Omar, and Bernie Sanders were dishing out, objected on Facebook to losing his monthly checks:

I have been reading about the concept of “means testing” for social security recipients. This means taking it away from successful people. Well, I am okay with the government taking away my social security if the government will simply return to me all the money I paid in over the last 50 years.

One of his financially savvy friends pointed out that “Every single adult worker” would be better off if they could have kept their Social Security taxes and invested it in the S&P 500. My response:

Social Security calculates and publishes internal rates of return periodically. These are in real dollars (adjusted for inflation). Very low earners who are married can get an 8% real return, comparable to the past 50 years of the S&P 500. Median earners get less than 2% (single man), 2.5% (single woman), or 4% (one-earner married couple). Someone at the income limit gets only about 0.6% real return (single man), 1% (single woman), 0.85% (two-earner couple), or 2.3% (one-earner married couple). So you could consider Social Security to be part of the U.S.’s transferist welfare state. It transfers money from high earners to low earners. It also transfers money from men to women and from those who weren’t successful in the marriage market to those who were successful. … So maybe [our mutual friend] will feel better about Social Security if he stops thinking about it as something designed to benefit him and instead as something designed to help him transfer money to low-income Americans and women

(note that the SSA doesn’t calculate or publish an IRR for nonbinary Americans)

What do readers think is going to happen? Benefits get preserved for anyone already claiming them, but drastically cut for anyone who hasn’t gone on Social Security yet? Benefits get cut for everyone? Social Security tax extended to infinite levels of earned income instead of being capped? Society Security tax extended to “unearned income” such as dividends and interest? (if the money isn’t “earned” then fairness dictates that the government should take 100 percent of it) Elon’s unearned $1 trillion gets confiscated and that plugs the hole? Robots get taxed as if they were human workers and 12.4% of the cost of buying and operating a robot must be given to Social Security?

A lot of my friends are between 62 and 67 (“full retirement age” for their cohort). Would they be better off getting on Social Security before they hit 67 or 70 (max benefit age) so as to be part of the “we don’t want to take anything away from these Boomers who are already relying on it” class?

(We can also look at Medicare, the federal government’s most expensive program (even larger than our off-the-charts enormous military!). Most proposals to cheat everyone who previously paid into it say that most or all of the stealing will be done from those under 55, e.g., by making them wait until 67 rather than 65 to receive any benefits.)

Related:

Since generation X is the smallest group of voters, they’ll lose the most benefits. Anyone born after 1968 & before 1980 is going to get shafted.

No-one on finance tube is taking it before 70 anymore. They’re treating it like an emergency fund. This takes away the market risk.

I think that every time any group of people can screw you and get away with it they will screw you. So if those in power think that it is politically expedient to cut benefits of those who already paid more then they are expected to receive based on average life expectancy, like most of Gen X office peasants, they will. If not, then amount of Social Security taxable earned income will rise exponentially. Anyway it has been rising steadily over the years. A politicians could say, let’s give Social Security benefits to everyone, without income limit, and not to have taxable income amount limit. Today Sanders suggests it, tomorrow Trump will tell that is an art of the deal. If I live average lifespan, I will not be able to recoup what I paid in Social Security taxes even not adjusted for inflation. So if I put it in Treasuries instead I’d much better off. In the old country I expected to be screwed by the government. Here we can expect be screwed by the duly elected government in free way.

I’m almost 62, and will likely retire in a year or two. The talking heads suggest that I wait until 70 to take SS, to get the higher payout. As I am also “successful”, I plan to take it as early as possible, because it seems to me that one piece of the likely financial solution will be to means test the benefits, and I want to get something before they zero me out.

Anon: It’s going to be like college admissions. Any family that saves gets financially murdered by the for-profit non-profit college with needs-based financial aid. Any family that squanders gets rewarded.

Social Security is easy to fix with minimal impact to existing recipients. Select from the following changes:

https://www.crfb.org/socialsecurityreformer/

Medicare suffers from shrinking payer to beneficiary ratios and the continuing inflation of healthcare costs.

Both require political will, notably in short supply for both parties.

Stalin would have no problem fixing social security

This might be a sleeper issue in the 2028 election and will certainly be an issue in 2032. Worth considering…

I think there will be a grand compromise in the end and sleight of hand will be part of the solution. E.g. redefine income taxes on ss payouts as “ss taxes” and use them to plug the hole in the trust fund.

That said “compromise” is likely to be ugly and people are right to prepare. Higher income cutoff on ss taxes most likely as the upper middle class gets hit hardest. Means testing and benefits cuts possible.

Don’t forget that there will be tens of millions of “New Americans” who will likely be grandfathered into fullbbenefits despite never paying. This will be the demand from one side as part of a compromise.

There is already means testing on medicare benefits (IRMAA – Income Related Monthly Adjustment Amounts), so why not the same on SS.

Or do away w/ means testing entirely and import millions and millions more immigrants to save Social Security and Medicare for all the aging and dying legacy Americans. Am I right, WSJ?

See https://www.aporiamagazine.com/p/immigration-does-not-solve-population

The thing is: immigrants age too. This means that while immigration can definitely reverse population decline, it can’t do much for population aging. Assuming immigrant age-structure and fertility remain constant, the difference in the working-age share of the population in 2060 between zero net migration and 2019 levels of migration in the United States is… 2% (57% vs 59%).

Because immigrants get older, trying to keep old-age dependency ratios constant this way is a fool’s errand. This can become farcical: maintaining 1995 South Korean age-dependency ratios would require about 100 million immigrants… per year, for a total of 5.1 billion by 2050. Needless to say, there are not 5.1 billion people on Earth who want to move to South Korea and are as productive as the average South Korean, which is the hidden premise in all proposals for using immigration to address old-age dependency ratios. I doubt there are even 5.1 million.

Democracies naturally tend towards vote-buying, and paying off current voters with the earnings of future generations who cannot vote is a winning strategy. This creates a Ponzi scheme in which huge fractions of state budgets are redistributed from current workers to retirees in ways that require an ever-growing number of workers to be sustainable. Productivity gains don’t usually help, because the expected living standards of retirees, often enforced by law, rise with productivity.

The “solution” to population ageing embraced by most European and Anglosphere governments has been allowing immigration to keep pension costs manageable. We’ve already seen that immigration barely matters for population aging, but there’s an even simpler reason why this doesn’t work: immigrants and their children are a fiscal cost, not a benefit.

This means low earners are even more of a fiscal drag in the US than they are in Europe. The median immigrant household5 uses more welfare programs6 and earns less than the median American household. If the median immigrant household were a fiscal positive, this would imply the median American household is a fiscal positive. But given the colossal size of the budget deficit, this simply cannot be true.

Immigration is good for one thing, according to that Aporia article: “With that in mind, in which Western countries do immigrants and their descendants support left-wing parties that want to expand state spending? All of them.”