It’s Juneteenth and Black Americans are celebrating the end of slavery.

(Except, of course, for the millions of Black Americans who are immigrants and who have no relationship to the roughly 400,000 African slaves who were imported to British North America/the U.S. And also not Black Americans in service jobs who have to work today while whites who work for the government, nonprofits (also government!), and Big Tech are relaxing with pay.)

A friend is also celebrating freedom this week because he finally unloaded his old house in Maskachusetts. He moved to Florida a year ago, but the market for high-end houses in MA is slow and he had some work to do on the place. It might have been inadvertently smart to sell the house in a tax year after he was completely gone. The new Massachusetts Millionaire’s Tax applies only to MA-source income. So he will owe tax only on the capital gain in 2026 and that should be under $1 million after the $500,000 exclusion for a married couple. Note that the “gain” is entirely fictitious and disappears once you adjust his purchase price for 19 years of official CPI. It would actually be a significant loss in real terms if adjusted for CPI as previously calculated, i.e., before the “owners’ equivalent rent” scam (see also “Summers: Inflation Reached 18% In 2022 Using The Government’s Previous Formula” (Forbes)). If he’d sold in the year that he moved, the rest of his income would have pushed the total well over $1 million and he’d be paying tax (on a loss in real dollars!) at the 9% rate rather than 5%.

Is my friend free, free at last from Maskachusetts state taxes? Not quite. Selling real estate is considered “Massachusetts source income” and, therefore, MA state income tax is owed. So many rich people are bailing out on paying for whatever Gov. Maura Healey and Boston Mayor Michelle Wu have dreamed up that the state is fearful it won’t get its pound of flesh from those who’d fled. There is a new law that requires the withholding of likely capital gains tax at the time of the sale. It applies only if the seller is a nonresident, i.e., has moved to tax-free New Hampshire or tax-free Florida.

Starting November 1, 2025, a withholding agent is required to file a Form NRW for every real estate transaction when the gross sales price is $1,000,000 or more. If the seller (aka, Transferor) is a nonresident or a business with no continuing Massachusetts presence, the withholding agent may also be required to withhold tax.

The withholding rules on sales or exchanges of real estate generally require a withholding agent to withhold an amount reasonably equivalent to the personal income tax or corporate excise, as applicable, that will be due on the net gain from a non-resident’s sale or exchange of Massachusetts real property. Non-resident sellers (or other transferors of property) include individuals and business corporations with no continuing Massachusetts business presence.

(The new regulation drives up costs to both buyers and sellers, incidentally. The lawyers on both sides now have to be paid to review the forms relating to this new law (grew from 2 pages in 2025 to 3 pages in 2026). A lawyer on one side has to be paid about $300 to file the form with the DOR.)

I wonder if this could be the foot in the door for a more general state exit tax, e.g., something like the federal exit tax on people who renounce U.S. citizenship. Someone fleeing NY, MA, or CA would have to pay tax on all unrealized capital gains at the time of the move to a different state.

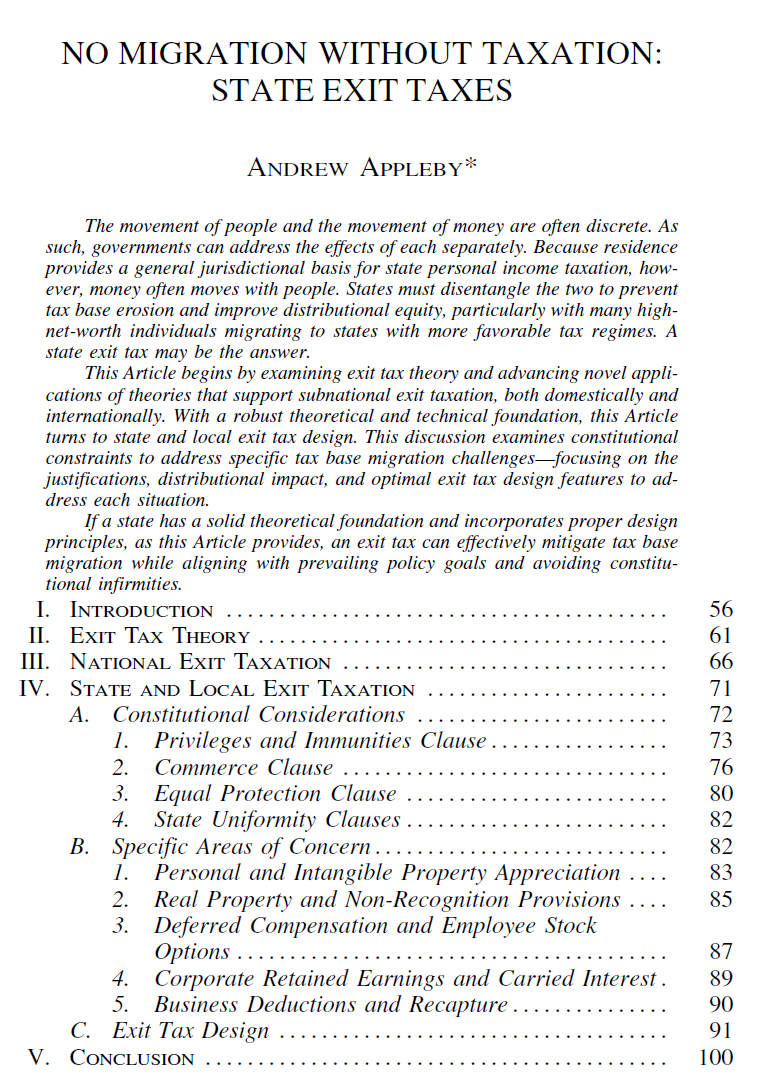

Here’s a Harvard Journal on Legislation article, “NO MIGRATION WITHOUT TAXATION: STATE EXIT TAXES”:

The author starts from the proposition that it was living in, e.g., Massachusetts, that enabled a person to make money. Only because the taxpayer lived in Boston was he/she/ze/they able to buy stock in ASML (Dutch) and Novo Nordisk (Danish) and, therefore, he/she/ze/they should have to pay capital gains tax on these stocks before fleeing to Florida.

If a taxing jurisdiction provides benefits to a taxpayer that allow the taxpayer to generate income, that jurisdiction should have the ability to impose tax on the resulting income … The problem arises with taxpayer mobility. If a taxing jurisdiction has a strict realization requirement, all the income that accrued within that jurisdiction could migrate to another jurisdiction along with the taxpayer before the realization event occurs. The taxing jurisdiction that provided the benefits that facilitated the income would lose the ability to tax it. The resulting tax revenue would inure to a different taxing jurisdiction that did not deserve it, or more commonly, would be eliminated through simple tax planning strategies.

The benefit theory’s fundamental premise is that individuals generate their income and wealth because the government provides economic, physical, and legal infrastructure; protection of property; and other facets of an “orderly, civilized society.”

(Obama’s “You didn’t build that”; why isn’t the fair tax rate 100% then?)

A state exit tax may not be entirely tax neutral, but it moves the overall tax regime toward neutrality. A state’s existing personal income tax regime without an exit tax creates a strong incentive to migrate out of the state before realizing income or gain, as discussed in Section IV.B. Imposing a tax on the gain that accrued while the taxpayer resided in the state removes that tax incentive to migrating out of the state, thus making the migration decision more tax neutral. With an exit tax that deems an exit to constitute a realization event, the detriment to migration is essentially just one of timing. The taxpayer can stay in the state and pay tax when there is a true realization event or leave the state and pay tax now. As discussed above, however, this assertion relies on an unavoidable realization event if the taxpayer remains in the state.

(This would certainly discourage people from moving. If they stay in a high-tax state they can avoid paying tax on unrealized capital gains for decades or perhaps forever (steps up at death). If they migrate, on the other hand, they must immediately pay tax on unrealized gains.)

The article seems to have been written in 2021, i.e., before the Mamdani Caliphate was established. However, the author has some specific guidance for how Ayatollah Mamdani could get cash from those who flee only as far as the Hamptons or Westchester County:

Although this Article’s focus is state exit taxes, there are localities that could similarly benefit from an exit tax regime. Interstate migration is quite easy, while intrastate migration is even easier, which leaves many localities such as New York City, San Francisco, and Seattle particularly vulnerable. The options are fewer for localities, even those with the power to impose an income tax, and many localities’ best option is piggybacking on a state exit tax. Localities could attempt to impose their own freestanding exit taxes, or creative exit tax alternatives that impose property tax or some other tax and grant credits in future years for the additional tax paid only if the taxpayer still resides in the state. These standalone options, however, are difficult to administer and susceptible to challenge.

The glorious conclusion:

States cannot prevent people from moving, but states can prevent the tax base from moving with them.

Where is the law professor who wants to save Maskachusetts, California, and New York while starving Florida of its daily fresh supply of rich people? Is he/she/ze/they in Cambridge, along with the journal’s publisher? In Brooklyn, perhaps? Maybe in San Francisco at Kamala Harris’s old law school? Remarkably, at the time he wrote the article, Professor Andrew Appleby was a professor at Stetson University College of Law, which is in Gulfport, Florida (Tampa metro area). He’s now moved to University of Tennessee, i.e., to another tax-free state that prospers when rich-but-mismanaged states in the Northeast raise tax rates. So.. the taxpayers of Tennessee are paying this guy to promote the idea that New York should impose a crippling tax on anyone who is thinking of moving to Tennessee and start paying property and sales taxes in TN.

Separately, consider that the modern economy has a winner-take-all aspect for companies (Apple and NVIDIA,), individuals (Jeff Bezos and any woman who manages to get him into Family Court), and geographical areas (Silicon Valley, San Francisco’s Cerebral Valley (the LLM companies), and NYC for finance). If the geographical areas that have won 90% of the income are able to prevent people from moving away via exit taxation then the places that currently get a few scraps won’t get anything at all. Although politicians and residents of the “winner places” love to talk about their passion for reducing inequality, I have a feeling that they’ll try to scoop up that last 10% with an exit tax, just as the Tennessee-taxpayer-supported professor suggests.

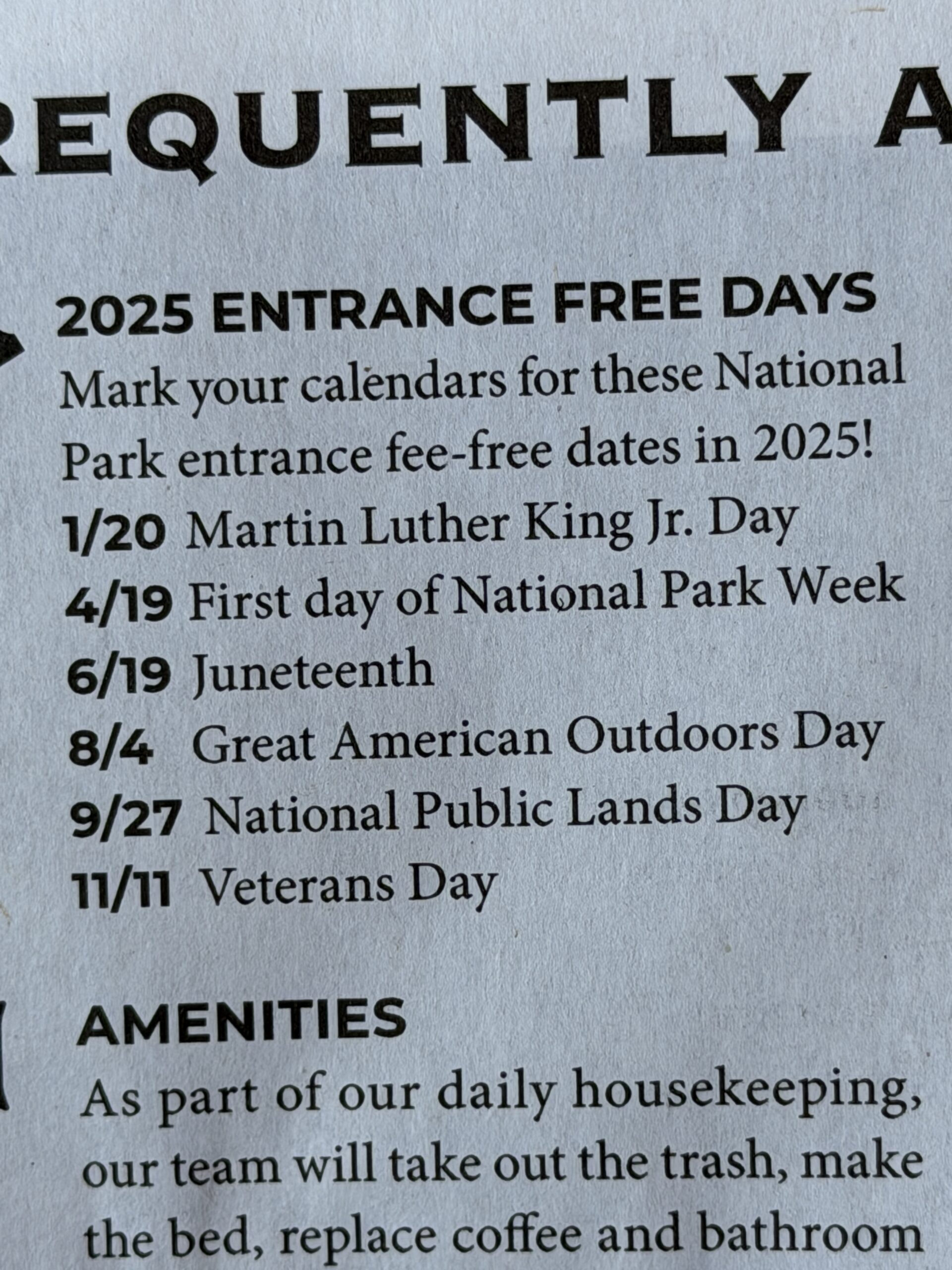

Loosely related, anyone who can afford $1,000/day for hotels, food, etc. could have visited our national parks today for free in 2025 (sign in our Olympic National Park hotel; of course, the promised daily housekeeping never occurred!):

Not so in 2026 because the Hater in Chief substituted Flag Day and Independence Day weekend for MLK, Jr. Day and Juneteenth.

https://en.wikipedia.org/wiki/Expatriation_tax#Germany

In December 1931, the Reich Flight Tax was implemented as part of a larger emergency decree with the goal of stemming capital flight during the unstable interwar period. After the Nazis seized power in 1933, the Nazi government largely used the tax to confiscate assets from persecuted people (mostly Jews) who sought to flee Nazi Germany.

My parents had to short sell their house for a significant loss, after a major unexpected health decline. $1,499,999 in capital gains is but a dream for the average blog commenter.

In Soviet terminology, traitors of the peoples’ republic of MA ate MA bread and lard but listened to fake FL capitalist propaganda.

> anyone who can afford $1,000/day for hotels, food, etc. could have visited our national parks today for free

You joke, but 15% more people visited already insanely crowded Banff national park when the entrance was free vs $10/day (hotel rooms $700+). It was probably the same people who will wait in line 30 minutes for a free pancake breakfast during Stampede.