Back in September 2012 I wrote a posting about California’s state government spending $327 million to build a seemingly straightforward web site where consumers could go to find health insurance plans. The web site is now up and running.

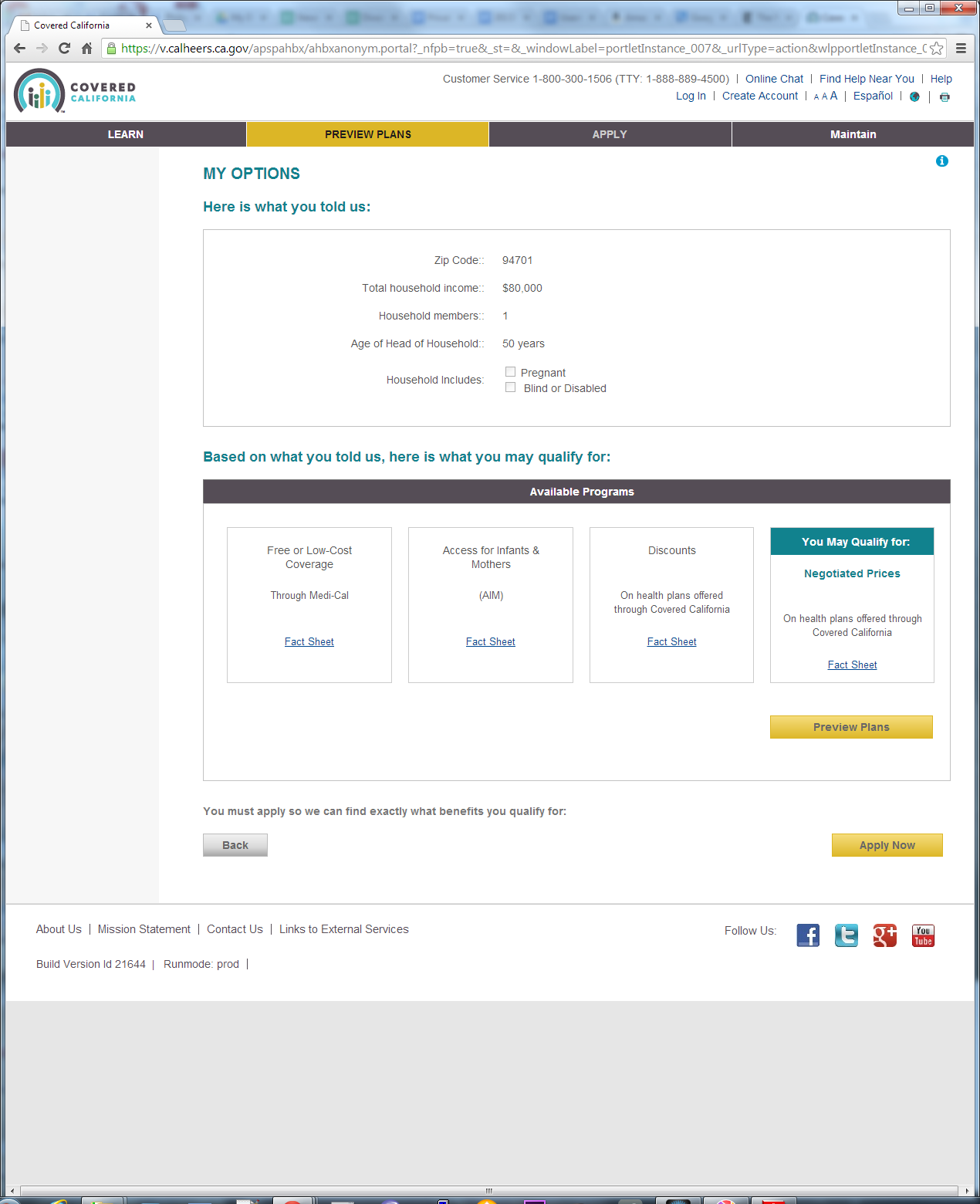

I told the site that I lived in Berkeley, earned $80,000 per year, and was a single 50-year-old who was neither pregnant nor disabled (click on image below to enlarge):

The site helpfully told me that I may qualify for free coverage through Medi-Cal, but the linked-to fact sheet says that it is for “an individual who earned less than $15,856 [per year]”. I was also offered “Access for Infants & Mothers” though it was unclear how this could apply to a household with one adult. In any case the linked-to fact sheet says that it is for “income between $3,256 – $4,884 per month for a family of 3.”

In other words, for $327 million the government purchased a computer program unable to determine that $80,000 is more than $15,856.

All that money didn’t help them design a responsive site and that’s true of several other states as well, which are slow, have crashed or even aren’t done yet.

From an article today “Opening of health insurance exchange in California cursed and celebrated” in the San Jose Mercury News:

“One should plan on reading a great book while attempting to use the website,” suggested user Mark Gaubatz, a Cupertino small-business owner. “Check for a possible website response between chapters.”

EXCHANGE GLITCHES AROUND THE U.S.

Colorado: Website won’t be fully functional this month

Hawaii: Site didn’t allow comparison of plans and prices

Illinois: Computer screens told users that system was unavailable

Minnesota: Site delayed several hours

New Hampshire: Site stopped working

Rhode Island: Site temporarily crashed

Washington: Site used Twitter to thank users for their patience

I tried going to DC’s exchange web site. What purpose is served in forcing me to create an account to browse plans? When I go to stores I don’t have to tell them my name and email address just to browse their wares. I also don’t understand how their cost estimate calculator works. If I type in that I am 50 years old and earn $80,000/year then it presents me with three sample plans. The “bronze” plan has a monthly premium of $393 and an annual cost of “total annual cost” of $6,964. I’ll save you doing the math — $393 * 12 = $4,716. I don’t understand it. The “silver” and “gold” plans don’t add up either. I’m sure there is a reason but it’s not explained anywhere that I can see.

Shhhh. Philip, you’re supposed to be paying attention to the government shutdown and not notice things like this.

Hmm, as I read it, the only “available” option for the hypothetical you is the one with the “You May Qualify for” banner. Displaying the others is just sloppy coding.

Clicking further to the “Browse Plans” page rewards you with an information display disaster. You are only allowed to view one plan’s information at a time. I guess you’re supposed to write the information onto a sheet of paper (or manually copy it into your own spreadsheet) in order to effectively compare them. Where’s Edward Tufte when you need him? (Probably moving to Canada in order to escape the whole fiasco…)

Not surprised in the least. The federal governments main mission is to employ mostly incompetent Democrats at levels way beyond their capabilities and pay them at a rate much higher then they would get in the private sector.

I’ve worked for a number of tech companies that do business with the feds and from time to time they would send out a contingent to inspect our work. The group would usually consist of around ten people with one person who was competent while the rest would stand around, nodding their heads and pretending they had a clue.

It’s sad that our country has come to this.

I don’t get this. We do much, much more (somewhat similar) work for our clients for much, much less money without the apparent shoddiness (which we would’nt provide and our clients wouldn’t accept).

Free website, free healthcare; it’s all free. Yay!

it’s free info, right? public domain, all that? maybe someone should undertake to build a better site as a public service – could be individual/s, non-profit org, academic project – complaining, blaming, all fine – but then do something

Fraud, waste, and abuse to the extreme.

The only thing not surprising is amount paid for this waste of taxpayer dollars. I’ll never understand why people continually allow the .gov sector to steal more and more money this way.

Sometimes it seems you’ve picked on the government a little too much. This kind of incompetence is actually more of the norm than exception with large, established organizations, regardless of public or private ownership.

I think the idea of a public, transparent, accessible exchange is an excellent idea to attack the hugely inefficient U.S. health care system. I remember your post about insurance company and a doctor office spending more effort and time on paper pushing than actually providing care. Without actual competitive choice for consumers or government intervention, the system would remain status quo.

Is it a good idea for a state government to spend $327 million dollar to build a website? Probably not. One can even argue no sane entity should spend that much, at least not up front, to open up what essentially is just a web database of insurance plans.

But was it a good idea for HP to buy Palm for a billion dollar and Autonomy for ten? Was it a good idea for Microsoft to buy Skype for $8.5 Billion? Was it a good idea to Time Warner to merge with AOL for $164 billion of stocks? The list of worthless write-offs in the corporate world would run just as long as the government’s.

Insurance exchange is a good idea, this might be a rough start, but at least it’s a start. Considering health care accounts for about 18% of our GDP ($15 Trillion in 2012), the initial investment is minuscule compare to the possible cost saving.

That said, perhaps the government could lean more on private sector to build its system. Perhaps let a few developers bid for the project or fund a few start-ups and keep the one that performs the best. On the other hand, Yahoo paid a billion dollar for Tumblr, how much can you expect to buy from the private sector for just $327 million?

In NYC, we got one better in the infamous “CityTime” fraud scandal. The CityTime project started under the Giuliani administration with the goal of streamlining timekeeping of NYC employees at a projected cost of $60M, but by 2010 when the NYC Comptroller sounded the alarm on this debacle it was revealed that Citytime was over budget to the tune of $600M, and CityTime still did not work. What escapes me is that the current NYC mayor, Michael Bloomberg, holder of Johns Hopkins electrical engineering degree and a Harvard MBA could let the project go this far over budget. (Amazing, but true.). Moreover, radio station WNYC reports on their web page, “Under Mayor Bloomberg, the contract ballooned from $63 million where it had started out in the Giuliani years , to more than $700 million. Federal prosecutors now say at least $600 million of that was “tainted.” At every level, federal prosecutors allege grafters had honeycombed CityTime in to a paragon of corruption.” How hard can keeping time records be to program and input into a database from employee smart phones and desktop PC’s? I know that there are lots of employees, at remote locations, with lots of time codes, but a $600M overrun? Holy Crap!

But here is also another “cherry” we can mention while were on the subject of superlative incompetent waste: the Ferry Point Park Golf course project. Also a brainchild of former NYC Mayor Rudolph Giuliani, the plan was to build a golf course on a sanitary landfill (i.e. a garbage dump) alongside the Bronx-Whitestone Bridge and on the shore of the East River, in the Bronx. Initially the project was slated to cost $22M. When cost overruns got out of control and the original developer bailed out, Donald Trump was brought in to take over the golf course concession and make the program work. The NY Post reports, “By the time it opens, the city will have spent nearly $100 million to prepare the holes for the turnover to Trump, who has spent millions more on the grounds.” But Mr. Trump will not have to pay much more for his part of the deal, as GolfWeek reports, “Attention also has focused on the payment schedule, with Trump agreeing to waive any fees for the first four years and then paying the larger of $300,000 or 7 percent of annual gross revenue, with the payments gradually scaled up in Year 20 to $470,000 or 10 percent of gross revenues, whichever is greater.” As for NYC residents’ $100M investment, well they get to play golf, at least on days when the deal with Trump allows usage of the golf course by the public. Under the Deal with Trump, he gets exclusive use of the golf course on some days of the week for the exclusive use of trump’s clients. Will Bronx local residents be lining up play golf for the projected $125 greens fee? You tell me.