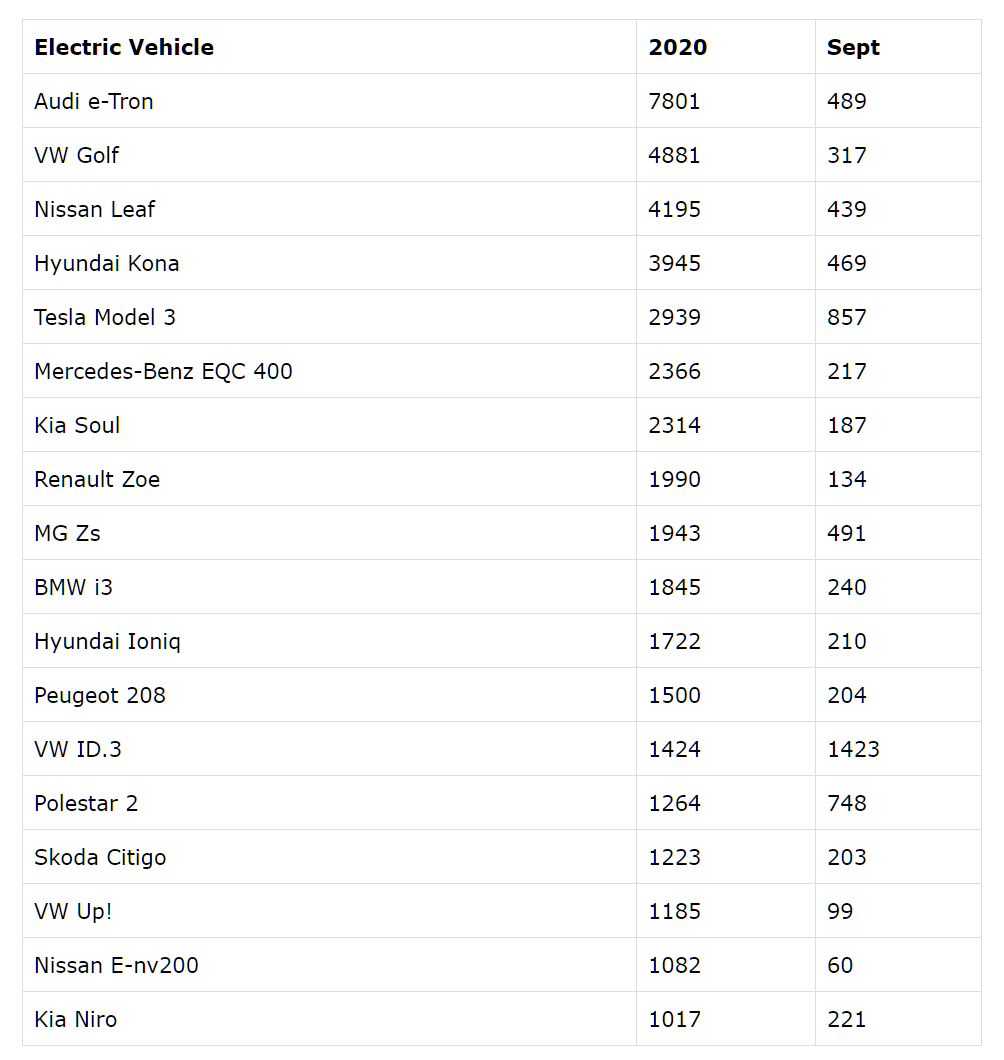

From “Tesla Is Being Overtaken” (Seeking Alpha, written by a guy who is short TSLA), electric car registrations in Norway:

YTD, there have been 51,115 EV registrations in Norway, and Tesla EVs have accounted for about 7% of that total. This compares with Tesla’s worldwide market share of EV unit sales estimated at 16% in 2019. In 2019, Tesla registered 16,738 vehicles through September in Norway. This year, with only a few days left in September, Tesla has registered only 3,613 – a decline of 78%.

How about a lead in battery tech?

For example, when it comes to batteries, easily the largest cost in producing an EV, VW isn’t messing around trying to redesign batteries themselves. They negotiated a massive contract with the large battery suppliers at a big discount, and let them figure out how to cut costs. And so while Tesla will likely get under that key $100/kwh threshold if/when their new battery design is successfully implemented, VW is already there. A VW company executive revealed to The New York Times last year that the company already pays less than $100/kwh for its batteries. GM has also introduced it’s Ultium battery, also reportedly costing less than $100/kwh, with specs similar to Tesla’s current batteries. GM will include the Ultium batteries in it’s upcoming launch of several new EV models.

I don’t like to think that markets are wrong, but how can Tesla continue to be so much more valuable than any other car company? And if the stock market is right, why is the consumer market for EVs in Norway now 93 percent non-Tesla?

Related:

Maybe for the same reason Apple is still around and dominates the market in terms of “luxury items” (vs. commodities)? Company has better control of its own infrastructure. Maybe I’d look at profit per vehicle instead of simply the number sold? Major automakers could afford to sell an eCar at a loss (not sure that they do) in order to gain market share, whereas Tesla really cannot. Also see: https://cleantechnica.com/2020/01/12/teslas-full-stack-disruption/

PaulG: But Tesla has no profit per vehicle, since they’ve almost always lost money, no?

And how is Tesla a “luxury item” when it is not as comfortable (interior noise, suspension compliance) as our Honda?

Won’t the “luxury” electric cars likely be the same brands as luxury gas-powered cars? Lexus, Mercedes, BMW, et al?

> how can Tesla continue to be so much more valuable than any other car company?

Personally I would bet it will be a very long time until cars can reliably self-drive in rain, much less fog or snow, but this guy thinks otherwise. Some interesting comments, too.

https://www.cringely.com/2020/09/17/tesla-won-the-self-driving-car-war-they-just-arent-telling-us/

Phil, have you read Hall’s “Where’s My Flying Car?” A lot of the book examines the various paths to a flying car, and the mechanics of flight feature prominently. Curious to hear your take someday.

The stock market is political just like everything else, just like healthcare, the NFL and all sports and entertainment, the universities, you name it, it’s political.

Only liberal tech companies go up and Exxon gets kicked out of the Dow.

It will reverse course, who knows when.

Is Warren Ludford a real person or really a certified flight instructor in Boston who swears by Honda minivans? What kind of dog does Warren Ludford have?

It does sound like a fake name!

> I don’t like to think that markets are wrong

Phil – you don’t really believe in the efficient markets hypothesis, do you?

One read through of Bob Shiller’s paper “Do Stock Prices Move Too Much to Be Justified by Subsequent Changes in Dividends?” should dispel any notion that the EMH is true.

Same goes for the concepts of “beta” and “CAPM.”

Modern finance “theory” is utter nonsense.

James: I believe that the markets are efficient enough that it is almost impossible for anyone to make money by active trading. Also, the market does have a way of proving itself right even when irrational. Tesla shares are so valuable that the company can get more money any time it wants by selling a few shares. Even if their ROI is negative, they still might end up being able to invest crazy huge amounts in R&D.

Maybe a better answer is that I believe that the markets are smarter than I am! I would have shorted Tesla years ago if I were an active trader. And look where the stock is today!

There’s nothing new in the battery universe except manufacturing efficiencies. The basic energy density situation has not improved significantly. They can make them cheaper with better manufacturing, etc., but it’s still a big load of stuff to haul around. And recycling is up to the crystal ball of whatever wizard you care to listen to.

I had a brief conversation with a girl at a convenience store tonight. She had red hair and two piercings in her nose, tattoos on both arms. She was nice, greeted me when I walked in, and said: “So how are you tonight?”

I said: I’m talking about electric vehicles on the internet with an MIT engineer. I think the battery recycling is going to be a big determinant of how many EVs automakers can sell in the next few years.

She said: What’s an electrical vehicle?

I said: You know, like a hybrid, but really one that doesn’t run on gas, a pure electric vehicle.

She said: Oh, those are awesome, they’re going to save the planet with those.

I said: But what about the batteries, don’t they have to recycle the batteries to prevent even more damage to the environment?

She said (and I am not kidding): They have batteries?

No joke. This is at a convenience store/gas station. Obviously the educational system in Massachusetts is working perfectly.

> Maybe a better answer is that I believe that the markets are smarter than I am! I would have shorted Tesla years ago if I were an active trader. And look where the stock is today!

Yes that would have been a stupid move. Shorting Tesla was (and is) mega-expensive from a risk/reward perspective.

Public markets tend toward disequilibrium, or as Charlie Munger says “it’s like a mob at a football game!”

Quants don’t seem to understand this idea, which is why I could purchase June 19 2020 690 calls for $1.40 each 10 months in advance of the expiration date.

Simple Bayes would tell you this was a badly mispriced bet!

The valuation of existing car manufacturers is tied to enormous capital investments into the non-electric car technology. One can imagine a plausible story where these investments currently have negative value.

Here’s an example — Tesla is building a new factory in the German state of Brandenburg, in the part of Germany with quite low labor costs (it’s within a commuting distance from Poland in case the pesky Germans will demand better work conditions). Whereas VW is completely unionized and must pay the pensions of all the highly-qualified engineers who spent 40 years improving bensin and diesel engines.

This being Europe, the German state is the one paying the pensions of all those retired engineers. And VW already capitalized on the cheaper workforce to the East ever since they bought Skoda in 1991.