From 2013, Should we short Twitter?

Folks: It has come to my attention that Twitter has gone public at a valuation of $18 billion. The company has modest revenue (about $600 million per year) and no profit. Is it a short?

What is the explanation for how this service can make enough profit ($1 billion per year?) to justify an $18 billion valuation? It doesn’t seem like a natural advertising medium. Given the possibility of distributing information for free via Facebook or Google+, Twitter does not seem to offer a unique capability to users.

Generally I am a believer in the efficient-market hypothesis but I can’t understand this one.

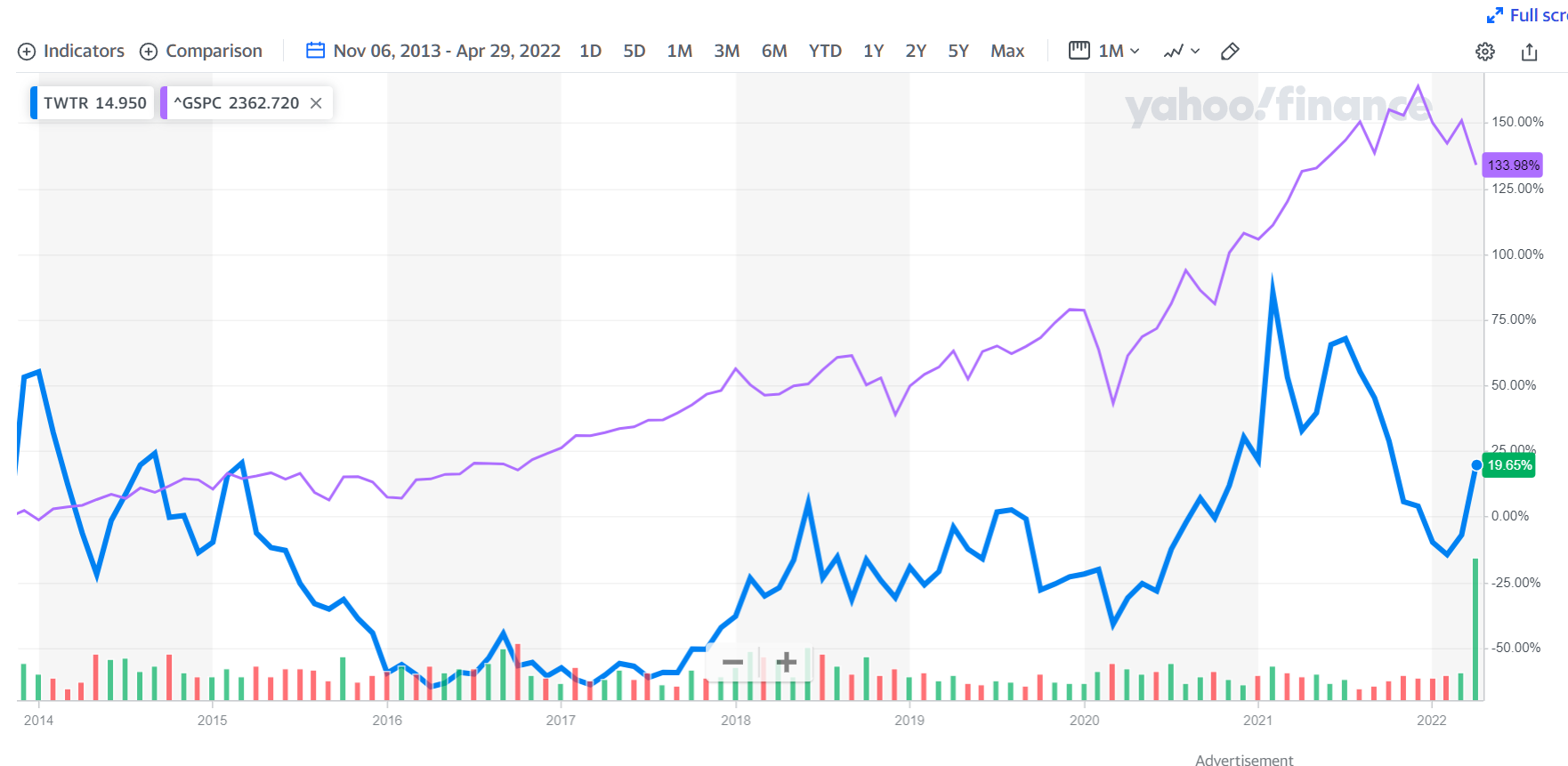

What if one had shorted Twitter to buy the S&P 500? The following chart isn’t complete because the S&P 500 pays a dividend while Twitter did not. If we use Yahoo! Finance to create a custom chart starting on the date of my post,

The S&P has gone up 134 percent (and paid a dividend of 2 percent per year?) while Twitter is worth 20 percent more than on November 6, 2013. Note the lift in 2020 after the government made most non-screen-based activities illegal, but even that wasn’t enough to bring Twitter’s performance even with the S&P 500.

(I’m wondering if the market cap number I cited in my blog post was inaccurate. Elon Musk is paying $44 billion for the company and the stock price is only barely higher. Either the $18 billion number was wrong (maybe it was the initial pre-bounce IPO target price?) or Twitter has issued a ton more shares since November 2013 (acquisitions? to enrich executives and board members?).)

Twitter isn’t about profit. It’s about control. Read up on Lord Beaverbrook using the Daily Express newspaper to increase his political power, for an example from a century ago. Although Beaverbrook did manage to make good money from running the newspaper, also!

How is google + doing?

Better than CNN+ ! Some remnants are still around.

TS: I didn’t realize that Google was so devoted to cancel culture that it would cancel so many of its own services between 2013 and now!

I don’t follow Twitter, but a quick search seems to show the issuance of a lot of new shares in 2014:

https://www.macrotrends.net/stocks/charts/TWTR/twitter/shares-outstanding#:~:text=Twitter%202021%20shares%20outstanding%20were,a%201.66%25%20increase%20from%202018.

Please don’t confuse me with an oracle or an investment guru (not that anyone would) but this confirms my hunch about Twitter when I first saw it. I thought: “Who needs glorified Internet Relay Chat?” Apparently a lot of people like it, because it helps drive that all important Narrative now, but I didn’t think it would be a stock like Amazon. My gut instinct appears to have been correct.

When you consider the sheer amount of *totally wasted hours* spent by otherwise sentient, quasi-intelligent, high-value type people, I think a good case can be made that Twitter is a massive NET LOSS for the American economy. God knows how many hours have gone completely down the drain.

In other Twitter news, this meme says it all:

https://i.ibb.co/3yNxdDN/MISINFORMATION-ON-TWITTER.jpg

“the efficient-market hypothesis”

The Economist, writing about Musk and Twitter when he first upped his stake, referred to the “Elon market hypothesis” whereby a stock should be valued according to how closely it’s linked to Musk.