Happy National Insurance Awareness Day to those who celebrate. (And Happy Pride to everyone else.)

From a friend in the Boston suburbs:

My kids got hit by a Haitian immigrant. The car is totaled. I am talking to his insurance company and they tell me, yeah so he is only insured up to $10,000 (damage to third parties).

(His teenagers were driving a minivan and weren’t hurt, fortunately. The migrant hit them from behind so his car would have needed to go through two empty rows of seats before reaching the children in the front seats.)

It turns out that the noble enricher was overinsured by Maskachusetts standards:

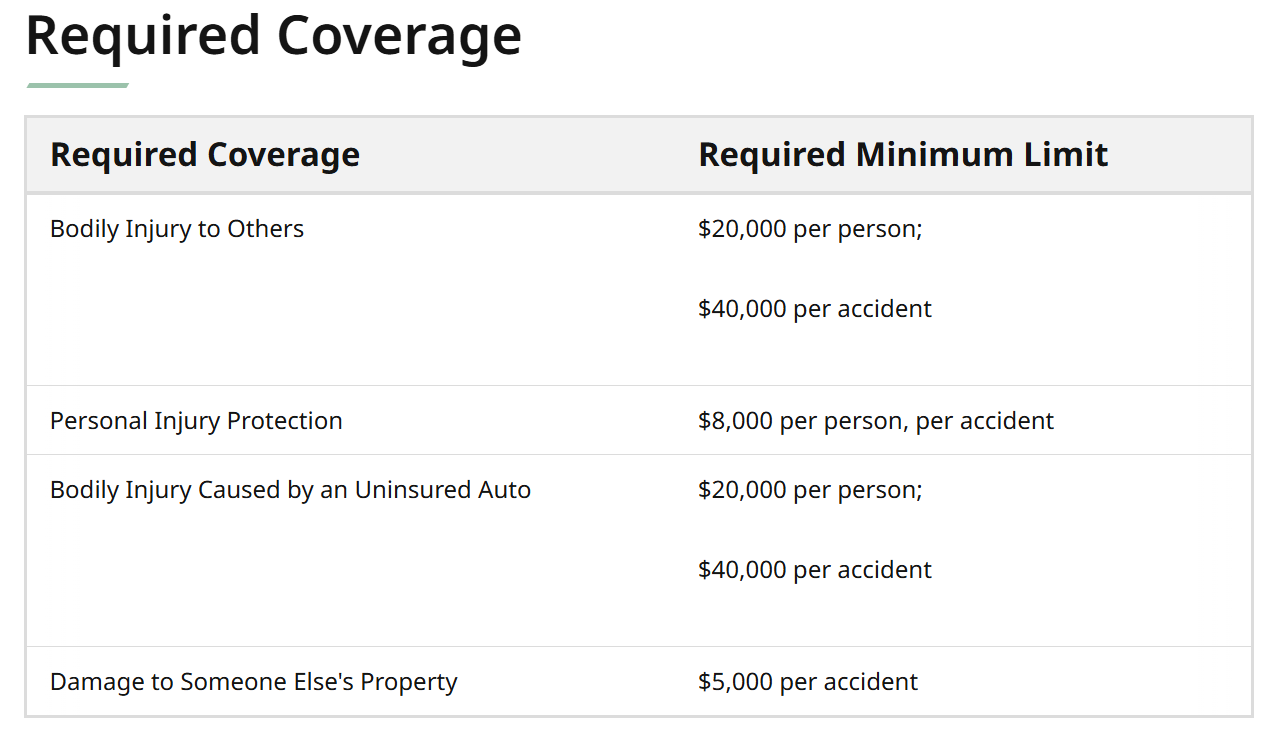

State governments love to regulate. They have a structure in place for requiring car insurance. Why are these limits set ridiculously low? It would be almost impossible to crash into someone else’s car and do less than $5,000 in damage. Things are complicated to some extent by the “no-fault” idea, but wouldn’t it make more sense to have minimum insurance set at the average cost of a car, e.g., if a driver hits a parked car and there is no doubt whose fault it is, or at the average cost of repairing a house after a car hits it?

How much damage was done by the Haitian whose presence in the U.S. makes all of us better off?

Progressive said they would pay $11k for the totaled [2012] Sienna and said they would arrange for me to come and sign papers. They called back and said that MA law requires that they run a check on me before issuing me any checks to make sure I don’t have any outstanding child support. It would then be deducted from my settlement

Even hitting a 13-year-old car did damage more than 2X the minimum! Separately, note that the tragic car destruction could have been a welcome payday for a family court entrepreneur. Finally, note the astounding value of a 13-year-old minivan!

Related:

- Progressive Insurance is Progressive (2022)

- Progressive Insurance abandons its Progressive Values (2023; I switched to State Farm that year)

Good question. Answer: Because the incentive to regulate is political and the politicians only reap rewards when passing regulations (headlines, political resume item), not by ensuring existing regulations are updated and enforced. If anything the pressure is opposite: a tax dollar spent on enforcing and updating old regulations (likely passed by someone else!) is not available to be spent on shiny new initiatives that a politician can take credit for. This is actually a pervasive problem.

It resembles, I’d argue, the problem with academic research: the incentives (to academics) for novel findings in prestigious journals are many. The incentives to falsify/verify someone else’s finding are minimal in the positive and numerous in the negative.

We all want to be glorious builders, preferably on green field. None of us want to be maintainers. The real question is how to fix THAT.

Yes, it’s because these limits are not tied to inflation so it would take an act of the state legislature to raise them; no one wants to spend the political capital to do so so they generally aren’t raised. In a similar vein, the NJMVC can’t raise fees on drivers either, so it only costs $46.50 per year to register your car (up to 2700 lbs) to be street legal for one year; I don’t think the amount has done up in my adult lifetime. Of course, they don’t charge more for heavier drivers…