How’s SpaceX doing on its second trading day? The most expert experts on stocks in the United States work at Morningstar. They value the company at $63/share and say that if everything went perfect, it could be worth $154. From last week:

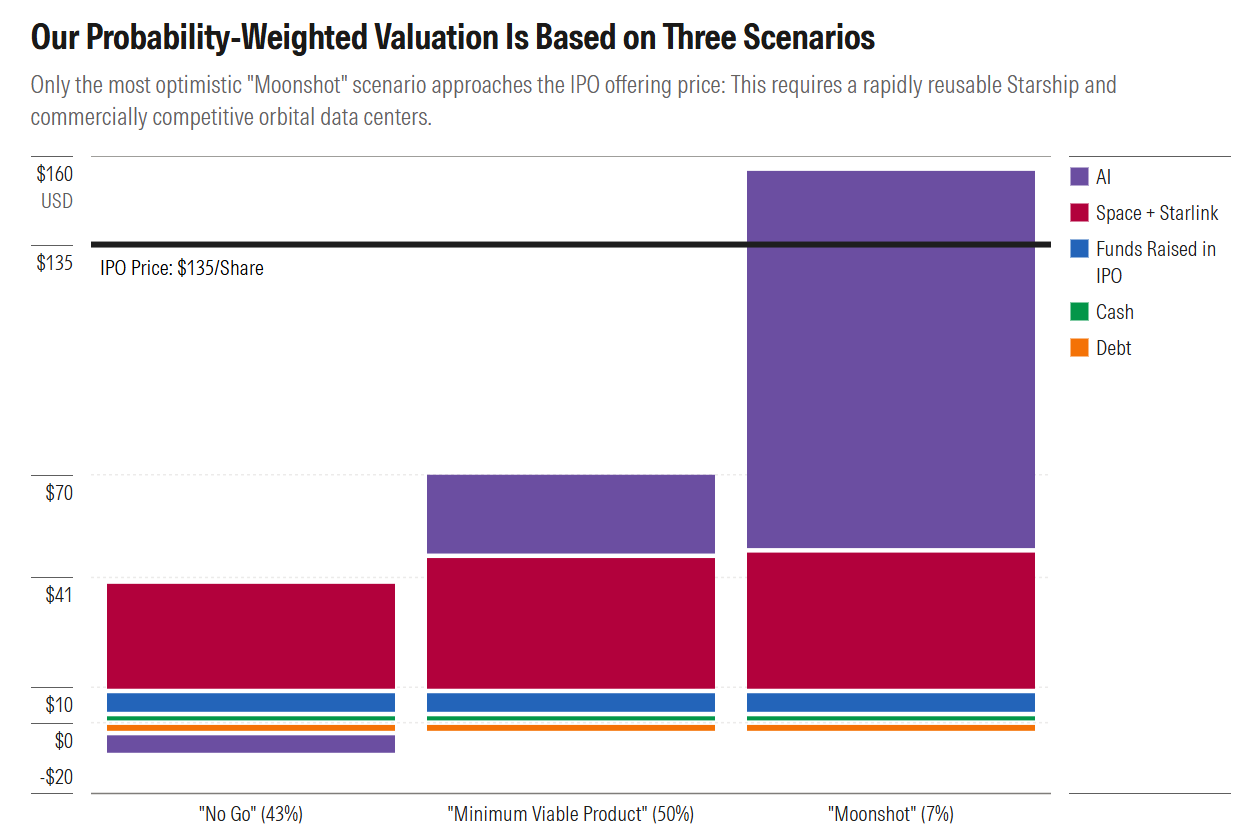

We value SpaceX SPCX at $63 per share, a 53% discount to the upcoming IPO’s offering price. Our valuation is the result of mathematics more than skepticism. With such a wide range of possible outcomes for the company’s financial future, we created forecasts and valuations for three scenarios and probability-weighted them.

Even at $63 per share, we give SpaceX a lot of benefit of the doubt in two of the three scenarios, in which we assume the company can achieve a rapidly reusable Starship rocket enabling multiple launches per week and successfully commercialize data centers in space. Neither of these engineering problems has been solved, and we don’t expect them to be until at least 2028.

In our most optimistic “moonshot” scenario, the company would be worth $1.97 trillion, or $154 a share. That’s 14% above the offering price and a level the shares might even reach in the short term after their public launch, given widespread investor enthusiasm about SpaceX, artificial intelligence infrastructure, and the IPO. However, we assign this scenario, in which both Starship is reusable and scaled orbital data centers are highly successful, a 7% chance of happening, which is one reason our final fair value estimate of $63 is much lower than $154.

We could try to figure out how accurate Morningstar was with Tesla when Tesla was the same size ($19 billion/year in revenue) as SpaceX is now. That takes us back to 2018. Tesla stock was at $20/share vs. $400 now (adjusted for 15:1 in splits, but not for Bidenflation). ChatGPT:

Morningstar was not recommending Tesla as a buy in 2018. In ordinary buy/hold/sell language, their view was closer to sell/avoid for much of the year, or at least don’t buy at the market price. … Morningstar’s 2018 stance was “don’t buy”; in buy/hold/sell terms, it was closer to “sell” than “hold,” especially around the August 2018 $420 buyout episode.

(Keep in mind that $420 pre-splits was a $28/share offer in terms of today’s shares.)

Democrats such as Bernie Sanders who are envious that Elon Musk is a trillionaire now have a Science-based way to catch up. They say that expert advice should be followed without question, e.g., if an expert-crafted response to a virus killing Americans at a median age of 82 is to close schools for 8-year-olds for 18 months. A leveraged bet that SpaceX stock will fall to the Morningstar-estimated value could make at least $billions if not $trillions in profit.

Loosely related…

Wow! Now I have two trusted investment advisors! ChatGPT and Morningstar.

Tesla’s stock price seems disconnected from Tesla’s business performance. At 15x gross revenue and 250x net earnings, its wildly overpriced by conventional valuations. And yet the party keeps going?

Anon, FYI most of the valuation embedded in Tesla stock right now is attributable to humanoid robots (Optimus) and Autonomous Driving (essentially AI for driving and robotaxis). These businesses have not begun to produce substantial earnings and cash flow, but if successful (?) could be very large, highly profitable and durable cash flow streams in future years. You might spend some time researching these areas and it will likely become apparent what is going on. Recall that stocks are valued based on the discounted future cash flows of the enterprise, not some static value of current earnings/cash flow.

R&AM: isn’t it tough to value Tesla based on Optimus? There are a lot of people all over the world trying to build humanoid robots. It’s tough to know if Tesla is way ahead of the pack. Autonomous driving… they are way ahead of the pack in terms of deployment. But what if one of the companies using https://www.nvidia.com/en-us/solutions/autonomous-vehicles/ made a practical competitive system?

https://insideevs.com/news/767000/tesla-fsd-outperforms-chinese-brands/

shows Tesla still ahead. But for Tesla to grow into its valuation it needs to stay ahead and there is a risk that they won’t. If all automakers end up with substantially similar capabilities then Tesla’s value, minus Optimus, should go back towards the automaker industry average (as a multiple of earnings).

Phil, two thoughts:

1) There is a saying “that’s what makes a market.”

2) You are quick to be skeptical, as was apparent in your SpaceX note last week. You may be correct, but rather than suggesting “it’s tough to know” and “…there is a risk they won’t” without any logic, it might be more interesting to elucidate us all on the humanoid robot market and why Tesla will or won’t be successful, no? FYI, your comments noted above apply to *ANY* stock. You certainly have more of a background in technology than most people (maybe all) reading your blog! Start a conversation with some interesting facts (who are the competitors, and what are they doing etc.?)!

R&AM: I don’t know enough about Tesla’s position in humanoid robots to begin to speculate about whether they will be the long-term leader! But even if they are #1 right now that doesn’t create enormous barriers to entry for competitors. I guess Tesla’s massive market cap and associated ability to raise money cheaply could be a huge competitive advantage compared to almost every other company. (Maybe this is why Apple can’t be unseated in the smartphone world. Apple has so much money that even if they’re only one third as efficient in developing the next phone they can still easily afford to make a better phone than anyone else.

Do the above concerns apply to any stock? Consider an oil company called “GretaCo”. It has a bunch of leases, wells, etc. Some other oil company might find better/cheaper places to get oil, but that doesn’t render GretaCo’s assets dramatically less profitable. Or look at the Kroger supermarket (KR), which has tracked the S&P 500 fairly closely. Even if Ayatollah Mamdani delivers on his dream of building city-owned supermarkets, Kroger should continue making similar profits from its existing locations. I think it is fair to say that the above concerns apply to almost any stock that is currently selling for more than 100X trailing revenue, as SpaceX is!

Meanwhile, SpaceX just hit $230 in overnight trading. That gives a $3T market cap, more than Microsoft or Apple. Bubble?

https://www.zerohedge.com/markets/spacex-erupts-after-hours-trading-soaring-above-210-and-surpassing-apples-market-cap

Paging Dr. Damodaran (“dean” of valuation from last week’s post). Dear sir, what happened with your “valuation” model?

Sorry, but my “model” value of $1.3T was a bit off. Did I mention I did my PhD with Claudine Gay?

Interesting that their three scenarios are only different on the “AI” portion

Our mom & pop startup can’t raise any more funding because investors just want to buy SPCX. Right now, he’s on an acquisition spree, trying to get in front of the language model boom. They expect to merge Tesla & EverythingX eventually. The company is going to change names.

This business of consolidating ever more of the economy in monolithic holding companies has only grown since AIG. Taxpayers were only ordered to pay a measly $180B to keep that place afloat. If EverythingX ever does crash below $65, taxpayers better open their wallets wide.

You raise a good point. SpaceX was already too big to fail on its first day as a public company! That said, I don’t think that SpaceX has too much debt. They owed $29 billion in May 2026 (see https://www.morningstar.com/stocks/spacexs-ipo-filing-big-spending-big-losses ) and $20 billion of that is being paid off with proceeds from the IPO (not to say “proceeds from the public chumps!”; see https://www.trendingtopics.eu/spacex-pulls-in-75-billion-in-mega-ipo-20-billion-to-repay-debt/ ). Ergo, it is tough to see a scenario in which a SpaceX bailout costs much more than $10 billion (their remaining debt). GM got a bailout to cover its defined-benefit pension obligations to union members. SpaceX presumably offers only 401k and, therefore, can’t get too far out over its skis in pension obligations.

“If EverythingX ever does crash below $65, taxpayers better open their wallets wide.”

The taxpayers will be safe under Pres. AOC!

Nobody has caused more losses than Benjamin Graham. No matter how many times these guys lose their shirt, especially with tech companies, they never question whether their model is wrong. They are not just wrong about future stock prices but these companies inevitably make profits that prove the IPO evaluation to be a huge undervaluation. SpaceX is easily going to make $10 trillion in profits in the next fifty years, maybe $100 trillion. It’s true that the biggest reason they are wrong is they either don’t account for inflation or they ludicrously underestimate it. But also revenue is a lagging indicator in technology. IBM is earning more now than when they actually mattered. Profits lag even further behind revenue. Facebook’s market cap at IPO in 2012 was $100 billion. They weren’t profitable yet. Facebook’s revenue last year was $200 billion and profits were $60 billion, just in one year. SpaceX has actual value, if they execute on reusable starships, data centers in Space, etc, they are going to quite easily make $500 billion in profit per year ten years from now. The stock price is going to have the greater fool effect on top of that. Twenty years from now, $1000 invested in SpaceX will probably be worth minimum $10 million in today’s purchasing power.

Benjamin Graham was right about airlines though. Are you saying that SpaceX will worth over 10 quadrillion dollars? All publicly traded companies’ market capitalization is under 160 trillion dollars. In 30 years, their capitalization not likely reach 1 quadrillion in today dollars.

All for Tesla success, but we need more then to populate Mars for such valuation.

Tony: https://en.wikipedia.org/wiki/Benjamin_Graham does say that the man would have hated today’s tech companies, which refuse to pay dividends and instead reinvest (more tax-efficient in today’s high-tax environment, if nothing else). “Graham’s investment performance was approximately a ~20% annualized return over 1936 to 1956. The overall market performance for the same time period was 12.2% annually on average.” So he was pretty well adapted to his time and place, apparently. The U.S. was a heavily regulated government-strangled economy back then, though. If Graham were still alive and mentally sharp, maybe he would have changed his tune after the Ford-Carter-Reagan deregulation period that allowed companies to grow at rates previously considered insane. (Graham died at 82 in 1976, just as Gerald Ford and Congress were beginning to dismantle some of the regulation that protected inefficiency and enabled companies to be fat, dumb, and happy.)

Separately, check out https://beyondbengraham.com/ from the great investor’s granddaughter.

https://beyondbengraham.com/3-ben-grahams-origin-story/ says that he was an immigrant. Ergo, we are informed by Science that his influence on the U.S. must be net positive.

> Our valuation is the result of mathematics more than skepticism.

I have a few problems with these Math-based predictors:

1. Has there been a stock for which they failed to have any opinion on? Why is silence not a totally fine option?

2. Just like Dr. G searched for their previous record. Do they ever cite their own correct and incorrect predictions? It’s common in Science to get things wrong and then accept it, and correct it. Why not follow that rule of Math and become more Math based?

3. Do they ever cite conflicts of interest, like is cited in engineering/science?

I never understood the meaning of “data-driven”, “math based”, etc., to me they just sound like words crafted by these analysts so that the readers can justify their decisions, and suggest others that they also should follow these analysts because they are doing something new.

If you’d like to see a classic example of what I am saying, it’s the following (reduce the volume before playing the video). Note that he’s totally sincere, and was in the Indian Revenue Service, which is quite difficult to get into, and I am not trying to make fun of him. I am just pointing out how using buzz-words without understanding what they mean leads to ignorance and not knowledge.