Bloedel Reserve, a model (I hope) for rich douches everywhere

Back in 2023 I wondered Where are the gardens and museums created by the Silicon Valley rich? That’s still a good question, in my opinion. Elon Musk is a trillionaire. In addition to voluntarily paying whatever taxes Elizabeth Warren deems fair, why hasn’t he built off-the-charts open-to-the-public gardens near his spaceports? It’s Elon Musk’s birthday today so maybe he will decide to think about the little people for once…

Earlier in June 2026, we visited the Bloedel Reserve, a 140-acre garden surrounding a fancy house that was all built by a lumber executive and his wife. It’s on Bainbridge Island, a suburb of Seattle made possible by the ferry system.

After they got too old to really use it, they turned it over to the public. Walk through the swamp:

Then over the bridge:

Then through the ferns:

Then arrive at what passed for a “mansion” in the days before trillionaires:

If you’re not a Floridian insistent on warm water, it’s a beautiful view from their back yard:

Everyone needs a Japanese tea house and garden to accompany it:

Speaking of Japanese, how about a moss garden like Saihō-ji in Kyoto?

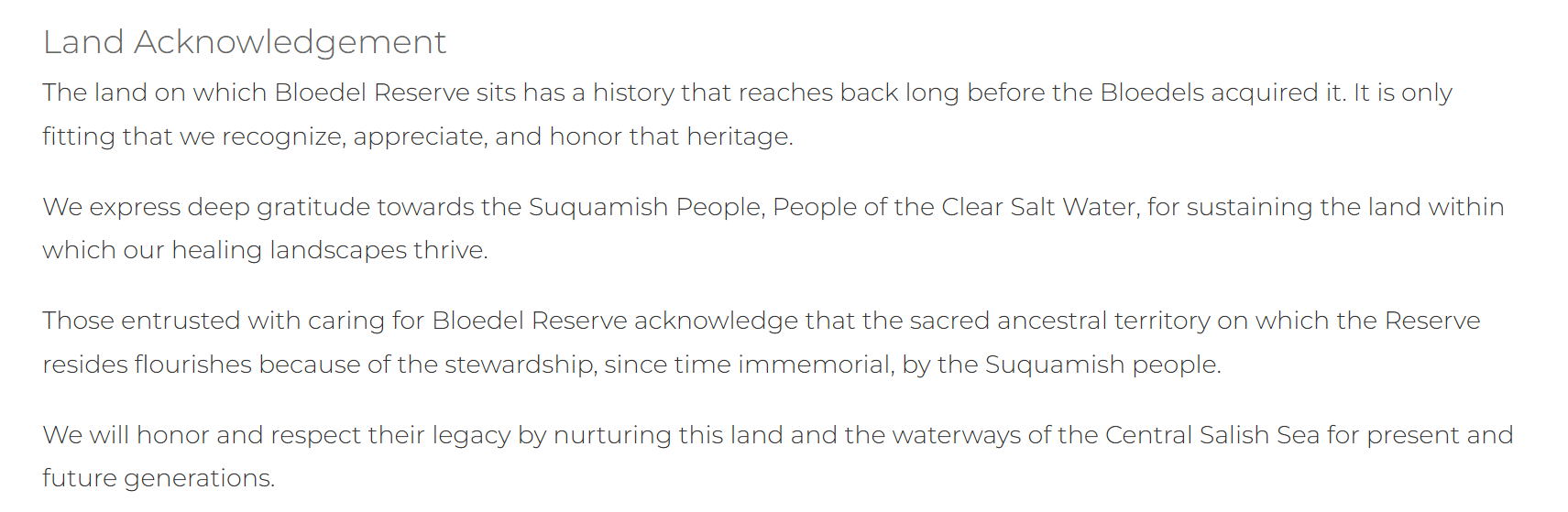

Land Acknowledgement

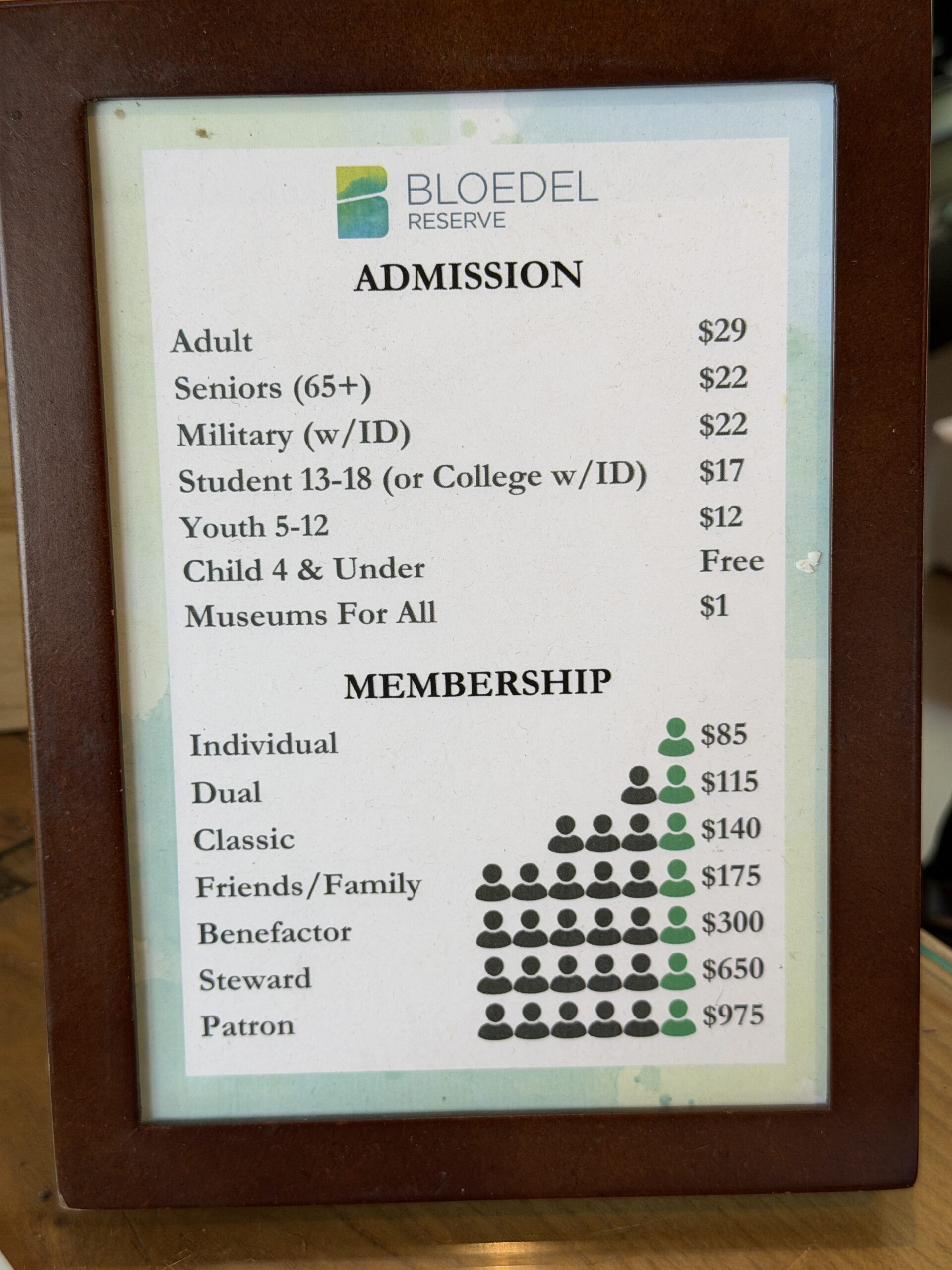

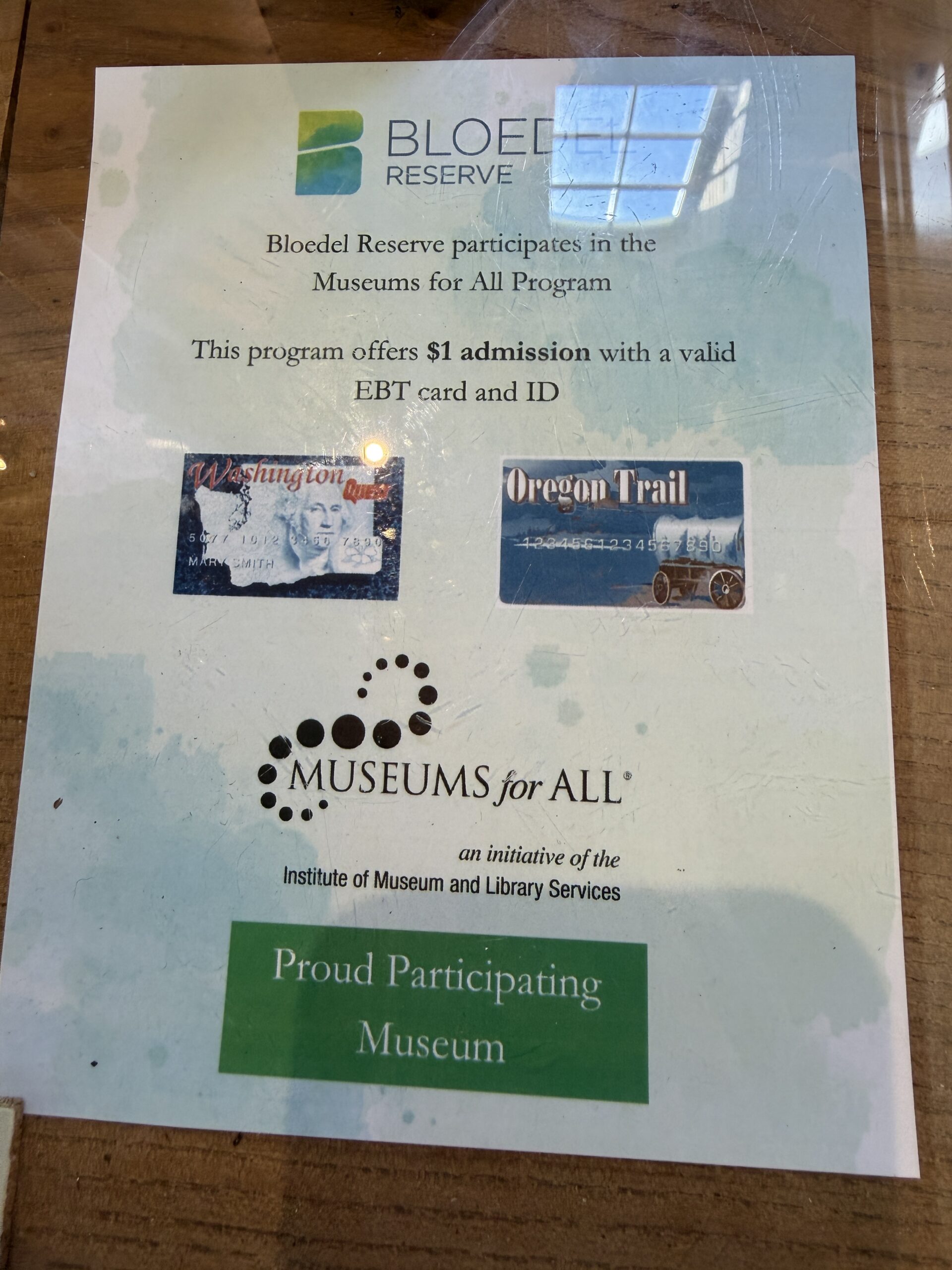

The nonprofit that runs the garden admits that the land is stolen. Instead of giving it back to the rightful owners, however, they will somehow “honor” the rightful owners by charging everyone, including the rightful owners, $29 to enter (or $1 for those on welfare who show up with their SNAP card). Reserve in advance because they limit the number of people per hour who enter, a coronapanic innovation that they decided to maintain (or maybe they’re still trying to promote social distancing?).

Who is today’s Anti-Bloedel? I nominated succcessful divorce plaintiff MacKenzie Scott Bezos. Wokipedia says that she gave $26.3 billion to various non-profit organizations, including universities, since 2020. This money, nearly 100% of which was unrealized capital gains, was never taxed by the U.S. Treasury or Washington State (with its fresh new capital gains tax that gave us Jeff Bezos, the Starbucks billionaire who said he wanted to pay more tax, et al.), has apparently disappeared without even a ripple in the waters of the various lakes of crises facing the U.S. Perhaps some nonprofit executives have enjoyed higher salaries as a consequence, but the issues she claimed to care about at the outset of her giving (“racial equality, LGBTQ+ equality, democracy, and climate change”) have all gotten worse. Elon Musk ran away with all of the money and he isn’t Black. Scott Weiner, who represents the full Rainbow Flag spectrum, was recently attacked in San Francisco. Donald Trump was elected to a second term as President (proof that “democracy” doesn’t exist in the U.S.). Climate change, as evidenced by the fully baked Europeans, has gotten far worse. If Sam Bankman-Fried was an “effective altruist” maybe MacKenzie Scott Bezos can be characterized as an “ineffective altruist”? Or maybe altruism simply isn’t effective in the aggregate?

Here’s hoping that MacKenzie Scott Bezos will build herself a magnificent mansion with gardens and, following her death in 2070 (she identifies as female and, therefore, due to all of the disadvantages that women suffer, is likely to live only to age 100), will donate it to the public.

Full post, including comments