What’s happened since then? Are nearly all of the jihadis and their supporters out of prison by now? “Most of the Paris attackers were French and Belgian born citizens of Moroccan and Algerian backgrounds…” Salah Abdeslam, a Belgian man who chickened out and did not detonate his suicide vest, was sentenced to “life in prison”, but “life” doesn’t necessarily mean “life” in progressive societies.

How’s Europe doing now compared to then? Did a few years of meekly complying with lockdowns and mask orders calm Europeans down, including the jihadis? The Wikipedia page “Islamic terrorism in Europe” doesn’t seem to list attacks after 2021.

Politico says that the attacks substantially boosted government power:

The attacks forever changed the country and its politics, tipping the balance of protecting civil liberties versus ensuring public safety in favor of the latter.

Since 2015, France has passed a slew of laws meant to ensure such an event could never happen again. Members of parliament have expanded the state’s surveillance powers and its ability to impose restrictive measures without prior judicial approval. They’ve also reshaped France’s immigration policy and oversight of religious — particularly Muslim — organizations.

The French loss of liberty seems to be evidence for my theory that immigration from disparate cultures is inconsistent with liberty. If residents of a country don’t share a common language, culture, or religion, the only way for the rulers of that country to ensure safety is by taking away their subjects’ rights, e.g., the right to privacy or the right to own a gun.

Related:

Gonzalez v. Google LLC, a case decided by the U.S. Supreme Court in 2023 regarding the extent to which YouTube could be held responsible for showing jihad-related content to European Muslims who would otherwise have been entirely peaceful or at least mostly peaceful

Nationwide, two people died and more than 190 were injured, according to a provisional tally from the French interior ministry. More than 260 cars were burned and more than 500 people were detained.

Sporadic riots aren’t uncommon in France after major sports events, or even on New Year’s Eve. Officials for a time published a yearly tally of how many cars were burned during New Year’s riots, until they decided that the public numbers were encouraging more burnings.

Even in the mostly-peaceful BLM protests here in the U.S. I don’t think that 260 cars were burned (though maybe our tireless investigative journalists couldn’t be troubled to tally up the destruction?). Why are the French so passionate about torching cars?

I recently caught up with a friend who bailed out of Brooklyn in August 2020. He retired in 2019 after a couple of moderately successful startups (by NY standards, not by NVIDIA/OpenAI standards). He, his wife, and two kids (now 6th and 8th grade) moved to a beautiful historical downtown of a small city in Spain (population 220,000) that is 30 minutes from the beach (admittedly cold/wet for most of the year; he’s not fighting it out with expat Brits on the Mediterranean coast).

He pays $1400/month for a five-bedroom apartment that is 180 square meters (1940 square feet) and children attend public school (as in Maskachusetts, and unlike in Florida, they teach to only one level. There is no gifted education and the teachers’ attitude to a kid who says everything is easy is “That’s great; you won’t have to work hard”. Nobody obsessively preps to gain admission to university). I asked about the cost of living, specifically health insurance:

Expats are required to get private health insurance, but that doesn’t mean what Americans think it means. In New York, my family’s insurance cost me about $25,000 in 2019. Here, it’s currently about $3,500. Point of comparison: a couple of years ago, I had a heart attack. The public hospital treated me (even though as an expat, I’m not part of the national healthcare system) and billed me afterwards. My private insurance informed me that because I’d gone to a public hospital, I had zero coverage. The total bill for ER admission, an ambulance ride, angioplasty with two stents, and three days in the coronary ICU came to about $3,000.

Mid-range cars are similar, but replace all the above-average-size ones (pickups and full-size SUV’s) with below-average-size ones (compact cars like the Audi A1 or Skoda Fabia). Since those cars retail between €20k – €30k, I’m guessing that brings the average price down. Not sure what a Tacoma or Suburban costs these days.

Groceries are way cheaper than the US — or at least than NYC. I don’t really know what food costs outside New York. I bought apples yesterday for about $1/pound; I think in New York it’s a lot more. A sandwich and a beer come to about €5; a prix-fixe lunch menu (very common here) runs €12 – €20; wine is €2 – €3 a glass; but an entree at dinner could go as high as €30, depending what you choose. Of course, you can pay more if you try; there are fine-dining restaurants that cost far more.

There is nothing that he misses about Brooklyn and his friends who are still there say that the quality of life in many Brooklyn neighborhoods and also in Manhattan has deteriorated dramatically. The heart attack is cautionary. He’s younger than I am and his lifestyle must be vastly superior and more relaxed.

A friend in the Netherlands is a little crazy and is now head of a household (the term is still vaguely sensible there) with four pre-K children. Here’s his report:

Things are going surprisingly well. It’s actually possible to have a ton of kids running around just like our forebears did. The neighbor’s kid shows up everyday to help out.

Me: “Just for a few hours? What do you pay for that, out of curiosity? Here I don’t think you can get anyone decent for less than $25/hr and probably $30/hr if you wanted to lure a high school kid away from obsessive college prep. How old is your helper?”

we pay E10 per hour. She’s still in high school. We don’t need more than a few hours. In the morning, they all go to the child care which is a few minutes walk from here and they come back at 6pm. She’s very young, though. I think 15 or something.

Me: 15 isn’t young. Stalin’s girlfriend when he was 35 and in Siberian exile was 14. Maybe she was 13.

In March 1914 Josef Stalin – a Georgian cobbler’s son known to friends as Soso and comrades as Koba – was sentenced for his revolutionary activities by the Tsar to exile close to the Arctic Circle in a tiny hamlet named Kureika.

The place was a freezing hellhole, an isolated twilight world cut off from humanity in winter by the daylong darkness.

In Kureika, only the reindeer, snowfoxes and Tungus indigenous tribesmen could really function in deep midwinter. Everyone wore reindeer fur.

The hamlet contained 67 villagers – 38 men and 29 women – all packed into just eight ramshackle izbas or wooden peasant shacks.

Among them were seven orphans from the same family – the Pereprygins – of whom the youngest was 13-year-old Lidia.

She immediately noticed Stalin, not just because of his good looks but also because he was hopelessly underdressed with only a light coat.

Before long, he was sporting the full local outfit – from boots to hat – of reindeer fur, all of it provided by Lidia Pereprygina.

Stalin in those days was slim, attractive, charming, an accomplished poet and educated in the priesthood, but also a pitiless Marxist terrorist and brutal gangster boss – a Red Godfather who had funded Lenin’s Bolsheviks with a series of audaciously bloody acts of bank robbery, piracy and racketeering.

Some time in the early summer of 1914, the 35-year-old Stalin embarked on an affair with Lidia.

While not admitting to anything explicit in her memoirs, we catch a glimpse in them of Stalin and Lidia together staggering from drinking bout to drinking bout, because she writes of their drunken dancing and singsongs: “In his spare time, Stalin like to go to evening dances – he could be very jolly too. He loved to sing and dance.”

Separately, today is the anniversary of Josef Stalin’s death in 1953. Imagine the disappointment of people who were alive 72 years ago and thought that they’d seen the last of Stalin-style dictatorship reading today’s New York Times and learning that an even worse dictator has seized control of the U.S.

Circling back to the Netherlands and my friend, I think that all of the doom stories coming out of Europe still leave room for us to admit that most European countries provide a lot more support for the traditional nuclear family. Marrying the government in Europe leads to a much crummier lifestyle than here (admittedly, working at the median wage in Europe does too!). All of the family court profiteering that works so well here (e.g., having sex with an already-married high-income person, divorcing a medium-income spouse, etc.) leads to just a subsistence income there. The U.S. provides economic incentives for parents of young children to split up (or never get together to begin with) while Europe mostly provides economic incentives for parents of young children to stay together and, as a consequence, the traditional two-biological-parent household is more common in Europe (some stats). At this point, most of Europe is a terrible place to make money, obviously, (the whole continent will be worth less than NVIDIA if present trends continue?) but for someone who already has money and wants to spend a summer over there with a 10 Euro/hour helper maybe it makes sense?

Today is the 80th anniversary of the Yalta Conference, in which the UK, US, and Soviet Union agreed on plans to force German civilians to work as slaves for years after the war. Clearing minefields was a popular assignment (popular with the assigners, that is) and also agricultural labor (i.e., American president FDR was carrying on in the rich American Democrat tradition of agricultural slave labor). This post looks at the question of whether the benefits of this slave labor justified, for the UK, the costs of going to war and staying at war.

I’ve been listening to When the Sea Came Alive: An Oral History of D-Day, in which participants describe the heroism of the British and their Allies during the 1944 Normandy invasion (also the cheerful and willing collaboration of most people in France). It’s a worthwhile book, but it doesn’t explain why the British sacrifice was worth it other than “Nazis are bad.”

Let’s back up to 1900. Is it fair to say that the UK circa 1900 was the most successful and richest country in the history of humanity? The sun never set on the British Empire, which included India. The Royal Navy was the world’s most powerful. Compare to today. The UK is a predominantly Islamic society (measured by hours spent on religious activities) jammed with low-skill immigrants. Wages are absurdly low by U.S. standards. GDP per capita is lower than in the poorest U.S. states. After decades of open borders, the core English part of the UK lacks cultural cohesion. The main project of the UK seems to have been assembling humans from the world’s most violent and dysfunctional societies and expecting that they and their descendants won’t behave in a violent or dysfunctional manner once parked in the UK. The result is the Southport stabbings (by a young UK-born Rwandan) and the Rotherham child sexual exploitation scandal and similar. The trajectory of the UK from 1900 to the present looks like that of a country that lost multiple wars, each one having drained away its resources and treasure and each one resulting in the country being occupied by millions of non-British people.

What if the UK had never fought World War I? (As the victors, we typically think of Germany as the aggressor but it was the UK, without ever having been attacked, that declared war on Germany in 1914.) Let’s assume that Germany would, therefore, have attained all of its war goals. Would that have been worse than what the UK has done to itself? Germany’s goals in WWI were to steal some territory from neighboring countries, especially ports, but certainly not to take anything from the UK other than perhaps a competitive edge in colonizing far-away places that the UK didn’t hold onto even after ostensibly “winning” WWI. By not entering the war, the UK would have avoided the death of 6 percent of its male population (nearly 1 million men, though let’s keep in mind Hillary Clinton’s trenchant observation that “Women have always been the primary victims of war.”) and preserved a huge amount of treasure that it could have applied to beefing up its home defense and Royal Navy. Perhaps even more important, would the German people have elected Adolf Hitler if Germany had won WWI? The Nazis represented a dramatic change from previous German governments and a big part of Hitler’s appeal was that he would turn around the downward trajectory of the loss of WWI and the humiliation of the Treaty of Versailles. Without the British stepping in to fight WWI, therefore, they wouldn’t have had to consider whether to fight WWII. The UK would have needed to coexist with a more powerful Germany, but not a Germany with a plan to dominate all of Europe. Maybe a more powerful Germany could have pushed the UK aside in some of its colonial ambitions, but the UK lost all of its colonies in the “fight WWI and WWII” case.

The “fight WWI, but leave the Nazis alone and don’t fight WWII” analysis is a little tougher. Hitler supposedly didn’t want to fight the English, whom he admired. He envisioned a German-dominated European union (not too different from today’s “European Union”, including the idea of Jew-/Israel-hatred in most parts of Europe) and, even after the British declared war (without having been attacked in any way), a negotiated peace with the UK (see the background section of Operation Sea Lion in Wokipedia). If the British had used their resources to turn Britain into an island fortress rather than into daily fights with the Germans maybe Germany would never have bothered to bomb or invade the UK (Ireland was neutral regarding the Nazis and Germany never bothered Ireland). The UK might have lost some of its worldwide influence to a more powerful Germany, but the UK has lost all of its worldwide influence in the “fight WWI and WWII” case. As bad as Nazi Germany was, it never did anything so bad that the French weren’t happy to collaborate with the Nazis. Given the huge cost in lives, money, and years of home-front sacrifice, it seems that the UK would be in a better place today if it had let the Germans have a free hand in Europe from 1939 onward.

We can’t even say that the British sacrifices in WWI and WWII defeated the Nazis because we are informed that Nazis today (“far right”) are more numerous than ever and live all over the US and UK. Who wants to explain how the UK’s involvement in WWI and WWII makes rational sense in the light of how things turned out for the UK (i.e., the spectacular decline of the nation).

Related:

Proving that none of my ideas are original, the Journal of Diurnal Epistolary Communication (Daily Mail) published a scholarly work on this subject in 2009… “PETER HITCHENS: If we hadn’t fought World War 2, would we still have a British Empire?”: how come we look back on the Second World War from conditions we might normally associate with defeat and occupation? … We are a second-rate power, rapidly slipping into third-rate status. … We had then, as we have now, no substantial interests in Poland, the Czech lands, the Balkans or – come to that – France, Belgium or the Netherlands. … [regarding WWI] We had gained little and lost much to defend France, our historic enemy, against Germany. In a strange paradox, we had gone to war mainly to save our naval supremacy from a German threat – and ended it by conceding that supremacy to the United States, our ally. … What about the Holocaust? There seems to be a common belief that we went to war to save the Jews of Europe. This is not true. We went to war to save Poland, and then didn’t do so. … When, in 1942, the Germans began their ‘Final Solution’, reliable reports of the outrage were disbelieved or sat on. Later, when the information was beyond doubt, we turned down the opportunity to bomb the railway lines that led to Auschwitz. It is certainly hard to argue that the fate of Europe’s Jews would or could have been any worse than it was if we had stayed out of the war. [Maybe Jews would have been better off if the Nazis hadn’t been opposed in their efforts to dominate Europe. The Germans might have become so strong that they could have forced the UK to give up some of its colonial territory and then Germany would have forced Jews to move there, which was the original Nazi idea (get Jews out of Europe, not kill all Jews).]

How’s the UK doing now that has been properly governed by the pro-Hamas Labour Party for half a year? On track for success?

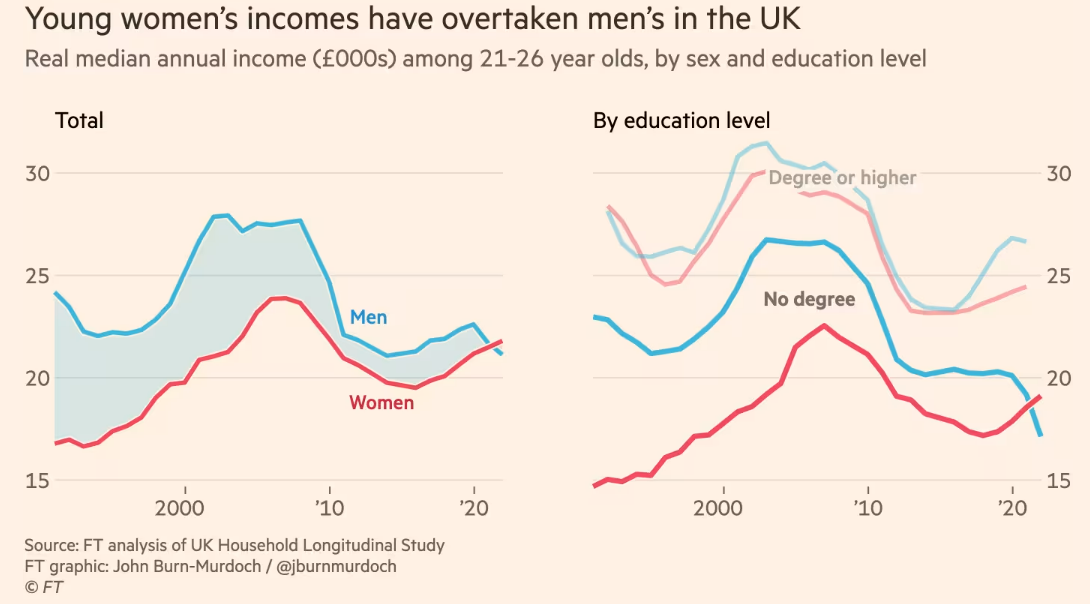

The last 20 years or so don’t seem to have gone well for the Brits. “Young women are starting to leave men behind” (Financial Times, September 2024) was supposed to be a feel-good story about equity (defined as “victimhood group does better than oppressor group”), but mostly the data seem to show that young people of all gender IDs earn less today than they did in the 2000s (after adjusting for the inflation that the government says doesn’t exist):

Maybe it is better in immigrant-rich London than in the left-behind Brexit parts of the UK? The Financial Times data nerd says that Londoners have gotten rich… Londoners who are landlords. Most of the urban hamsters spin on their wheels: “Londoners’ higher salaries relative to the rest of the country are ~entirely consumed by higher housing costs. 15% higher household incomes become ~0% higher after mortgage, rent etc”

All of that leads to something that I think is often under-appreciated outside of the capital:

Londoners’ higher salaries relative to the rest of the country are ~entirely consumed by higher housing costs.

Low-skill immigrants make a country rich. The UK has been at record levels of low-skill immigration for about 20 years. Now that the correct party is in power, is the UK rich or getting rich?

Based on Twitter and the BBC, folks in the UK are upset about “rape gangs”/”grooming gangs” in which Muslim men had sex with a lot of girls from the UK’s legacy population (“white”).

I’m surprised that people are surprised. The UK is an Islamic nation (as mentioned by hours spent in religious observance). How was an Islamic nation supposed to work without traditional Islamic cultural practices, such as (1) a ban on alcohol, (2) women and girls being fully covered (hijab and/or burqa), (3) women and girls carefully monitored by family members, etc.?

Here’s a 2023 BBC article that specifically mentions the un-Islamic availability of alcohol as an enabling factor:

It showed how the gang, comprising men of mostly Pakistani and Afghan heritage, plied girls as young as 13 with alcohol and drugs and passed them around for sex.

Roughly 20 percent of Syrians now live in Europe (Politico), about 4.5 million people plus their descendants. They were entitled to EU residence based on a fear of persecution by the Assad regime, which has now been replaced by the other side (“another side”?). Will there now be a refugee swap? Everyone who was targeted by Assad can now safely return to Syria. Everything who was on Assad’s side will need to seek asylum in the European welfare system. When does the swap happen?

Ten men, mostly Syrian refugees, have been found guilty over the gang rape of a woman outside a German nightclub.

The 2018 attack in the city of Freiburg fuelled anti-foreigner sentiment, with protests by the far right.

The lead defendant was sentenced to five and a half years for the attack – which lasted for more than two hours – while seven others received sentences of up to four years.

The victim, who was 18 at the time, had her drink spiked before being attacked in bushes outside the venue.

Eight of the men on trial were refugees from Syria, while the other three came from Iraq, Afghanistan and Germany.

The Germany-wide statistics on sexual violence were also sobering. An internal study by the German federal law enforcement agency, leaked to a Zurich newspaper, revealed that asylum-seekers have committed some 7,000 sexual assaults (ranging from groping to gang-rape ) between 2015 and 2023. Although they make up only 2.5 per cent of the population, asylum-seekers made up 13.1 per cent of all sexual-assault suspects in 2021.

Same question about the U.S., though on a smaller scale. We have at least 100,000 Syrians and their children who were granted the right to live in the U.S. because of a fear of persecution by the Assad regime. Do they now go back to Syria so that their places in the U.S. can be taken by Assad loyalists? We are informed that the U.S. does not have unlimited capacity for hosting refugees. If so, shouldn’t all of our refugees be those who are actually at risk in their home nations?

We are informed that low-skill migrants make the native-born richer and that, therefore, a country’s borders should be mostly open (albeit never described as “open borders” because that is hate speech/conspiracy theory). We also informed that Europeans don’t want to be rich… ”Europe Grasps for Ways to Stop the Migrant Surge” (WSJ):

The biggest swing in sentiment has been in Germany, long a proponent of generous policies toward refugees. Pressure has been building in recent years as the nation absorbed millions of immigrants, weighing on the welfare system and municipal services. Migration was a key theme in Sunday’s closely watched regional election in Brandenburg, where the governing Social Democrats narrowly beat the far-right Alternative for Germany party, or AfD.

Last week, the coalition government in Berlin reintroduced limited border checks to all neighboring countries, after a knife attack in late August by a failed asylum seeker killed three people in the city of Solingen during a festival to celebrate its 650th anniversary. The attacker was a 26-year-old Syrian with links to Islamic State who had evaded deportation for more than a year after losing his asylum case.

Since the pandemic ended, governments across the continent have struggled to cope with rising numbers of asylum seekers and are grasping for ways to stem the flow, from curbing taxpayer-funded benefits to asylum seekers to striking deals with non-EU countries to temporarily or permanently house would-be refugees.

Last year, a near-record 1.14 million people filed asylum claims in Europe, the highest number since the height of the 2015 migration crisis in Europe, when more than a million Syrians fleeing that country’s civil war entered the bloc.

For nearly everything else that has value in this world there is some kind of market. There is “a bid”, in other words, as the Wall Streeters say. Why hasn’t the U.S. bid to take all of the migrants that Europeans don’t want? We are told that migrants are precious. Why aren’t we offering, for example, to pay Germany $100,000 per migrant and also to pay each migrant $100,000 as a “welcome to America bonus” (on top of the means-tested public housing, means-tested health insurance, SNAP/EBT (“food stamps”), and Obamaphone to which migrants will be entitled)? And if we did offer $200,000 (total) per migrant, wouldn’t we expect to face competition from other countries that seek to be enriched?

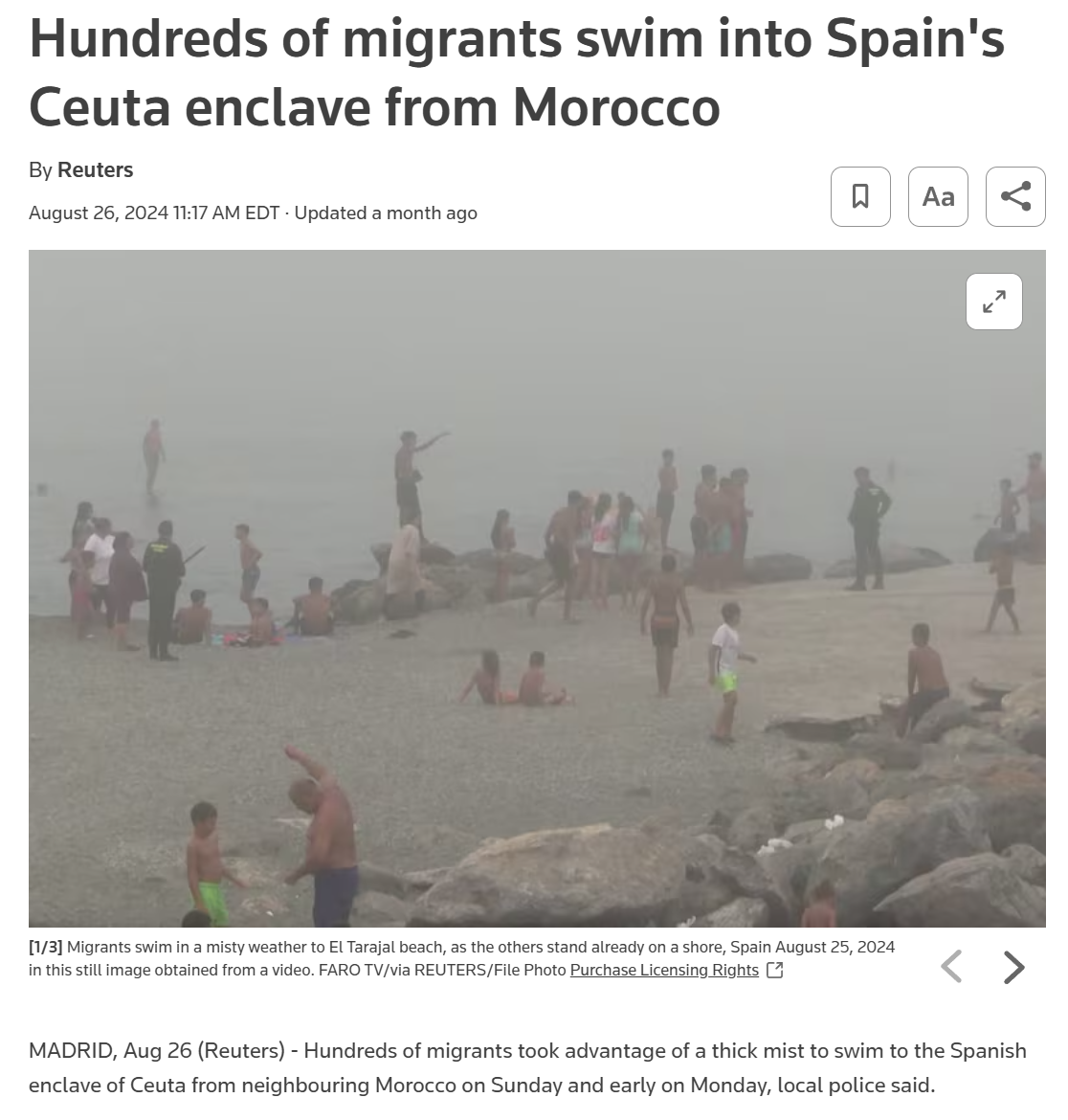

Separately, here’s a Reuters story on a beachhead in Africa that Spain continues to hold (why?). My favorite line is “Moroccan nationals detained during the crossings are immediately sent back to Morocco unless they are underage or seeking asylum, [Cristina Perez, the Spanish government’s representative in Ceuta] said.” Unless the migrants are remarkably unintelligent, why wouldn’t they all claim to fall into one of these categories? Like the U.S. system, the European immigration system seems to be premised on the assumption that humans never lie.

Europe must increase public investment by nearly $900 billion a year in sectors like technology and defense, according to a long-awaited report published Monday in response to growing anxieties about the continent’s economy lagging behind that of the United States and China.

Mr. Draghi said that the European Union needed additional annual investment of up to 800 billion euros ($884 billion) to meet the objectives he laid out in his report. That is equivalent to about 4.5 percent of the European Union’s gross domestic product last year. By comparison, investment under the Marshall Plan from 1948 to 1951 was equivalent to about 1.5 percent of Europe’s economic output.

Conditions that contributed to the continent’s prosperity have changed substantially since the coronavirus pandemic and Russia’s invasion of Ukraine. Cheap Russian gas is no longer available, and energy prices have soared. Those prices have come off their peak, but European companies still pay two to three times more for electricity than U.S. companies, the report found.

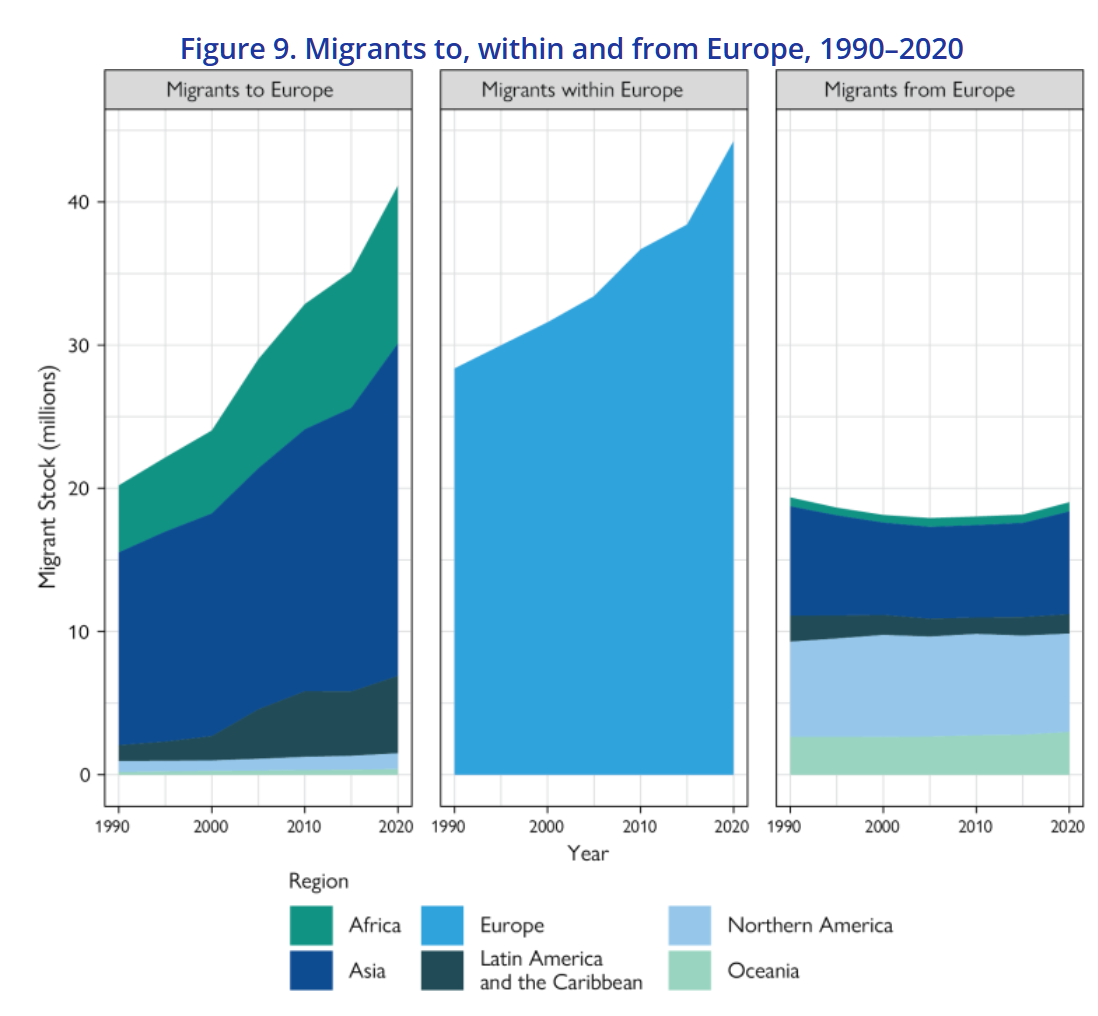

We are informed that low-skill migrants make developed countries rich. Europe has welcomed nearly 50 million non-European migrants (source through 2020).

Why does Europe need more government spending, as a percentage of GDP, to become rich if it was already enriched by low-skill migrants?

German business model was based on:

1. Cheap energy from Russia

2. Cheap subcontractors in Eastern Europe

3. Steadily growing exports to China

All three are gone by now, but German politicians and unions are still mentally stuck in a world that doesn’t exist anymore.

“Our giant welfare state” (Washington Post, 2014), in which we learn that only the French spend a larger percentage of their GDP on government hand-outs

Heritage Foundation on Germany, finding that it spends 50 percent of GDP on government (higher than the U.S., but the U.S. percentage is distorted because we don’t include nominally “private” spending on health care (which is so regulated and mandated by the government that I think it should be included))