Happy Middle of Hurricane Preparedness Week for those who celebrate…

Conventional insurance companies such as State Farm have mostly walked away from insuring coastal South Florida due to a combination of litigation risk (“Prior to the reforms, Florida accounted for more than 72% of the nation’s homeowners claim-related litigation in 2023, despite representing only 10% of US homeowners claims.”) and hurricane risk. Our house is about 2.5 miles from the ocean, but it is still redlined by the insurance companies most people have heard of. Here are the options for insurance:

- a Florida-only carrier that turns most of its premium over to reinsurance

- a “non-admitted” specialty company that isn’t regulated by the state and that may have unfavorable terms, including penalties for early cancellation and even a “wind exclusion” (i.e., they pay nothing in the event of the most obvious risk: hurricanes). (This option is so expensive and dumb that I won’t cover it here.)

- a “high-net-worth” (HNW) carrier such as Chubb (mostly rejects additional Florida risk; famous for a low loss ratio (payments as a percentage of premium collected)), Vault, PURE, and Berkley One (despite the name, these are available to peasants whose house is worth less than a Palm Beach starter home ($10 million))

The cost of HNW insurance is 2-4X what a Florida-only company might quote.

Nearly all Florida insurance includes at least a 2% wind exclusion. If the dwelling value is $1 million, in other words, the homeowner pays the first $20,000 of any hurricane-related loss. Thus, the vast majority of customers with hurricane damage will receive nothing from their insurer because the typical hurricane damage might involve only some blown-off roof tiles or shingles. The band of likely serious damage from a Category 4 or 5 hurricane making landfall is 20-60 miles, e.g., for Hurricane Andrew in 1992 that resulted in major changes to the Florida building code or Hurricane Michael in 2018 that damaged Tyndall Air Force Base. Note that this exclusion results in the HNW policies paying less after what would be typical hurricane damage because HNW companies write for 2X the dwelling value on the same house.

The Florida-only carriers are typically unrated by AM Best, the standard rater for insurers. It has been historically rare for an insurer rated A or better by AM Best to fail. Florida insurers get rated by Demotech. How well does it work for an insurance company to have all of its customers in Florida? According to ChatGPT, nearly all of the Florida-only companies that have gone insolvent had A ratings from Demotech (i.e., the ratings were worthless in terms of distinguishing the vulnerable carriers from the solid ones or, perhaps, the solvency of a carrier simply depended on their luck regarding how many customers were in a hurricane destruction zone).

Insolvency after a major hurricane doesn’t work the way that one would think, with the failed insurance company realizing that it is doomed to failure and going into a bankruptcy-style process where every claimant gets paid a percentage of his or her full claim amount. Instead, the insurance company, even after a major hurricane, pays claims as they’re made and adjusted at 100%. When the company runs out of money they turn out the rest of the claims to the Florida Insurance Guaranty Association (FIGA), which will pay up to $500,000 for a destroyed house. So… the customer with a major loss either gets 100% or a fixed $500,000. The more complex the claim, the less likely it is to be paid. ChatGPT says that it is reasonable to assume a 10 percent chance of insolvency for a Florida-only carrier in the event of a major hurricane. The most recent insolvency that triggered a FIGA payout was of United Property & Casualty Insurance Company in February 2023. That’s three hurricane seasons ago. Since then we’ve had some hurricanes, but none anywhere near as costly within Florida as 2022’s Hurricane Ian. Let’s use a 20 percent risk of insolvency if a house is damaged to policy limits and a 10 percent risk of insolvency if a house is damaged to half of the limits.

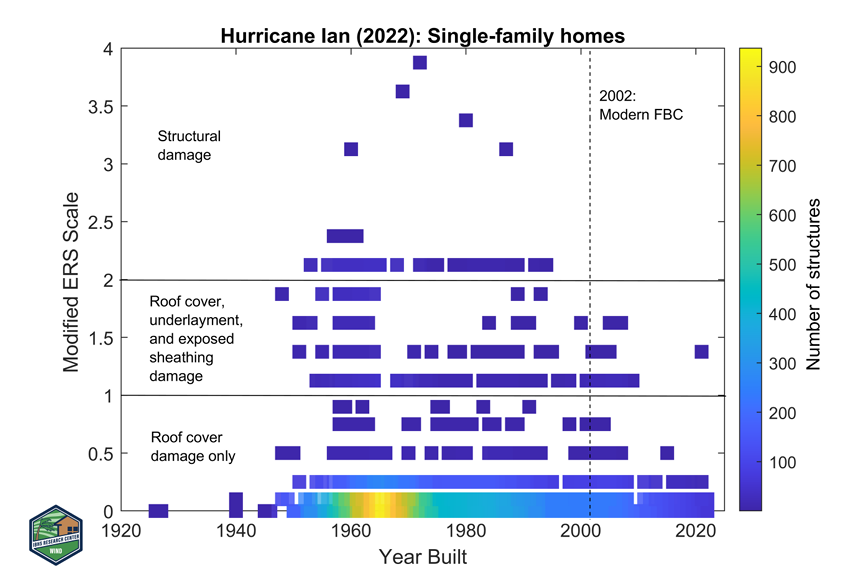

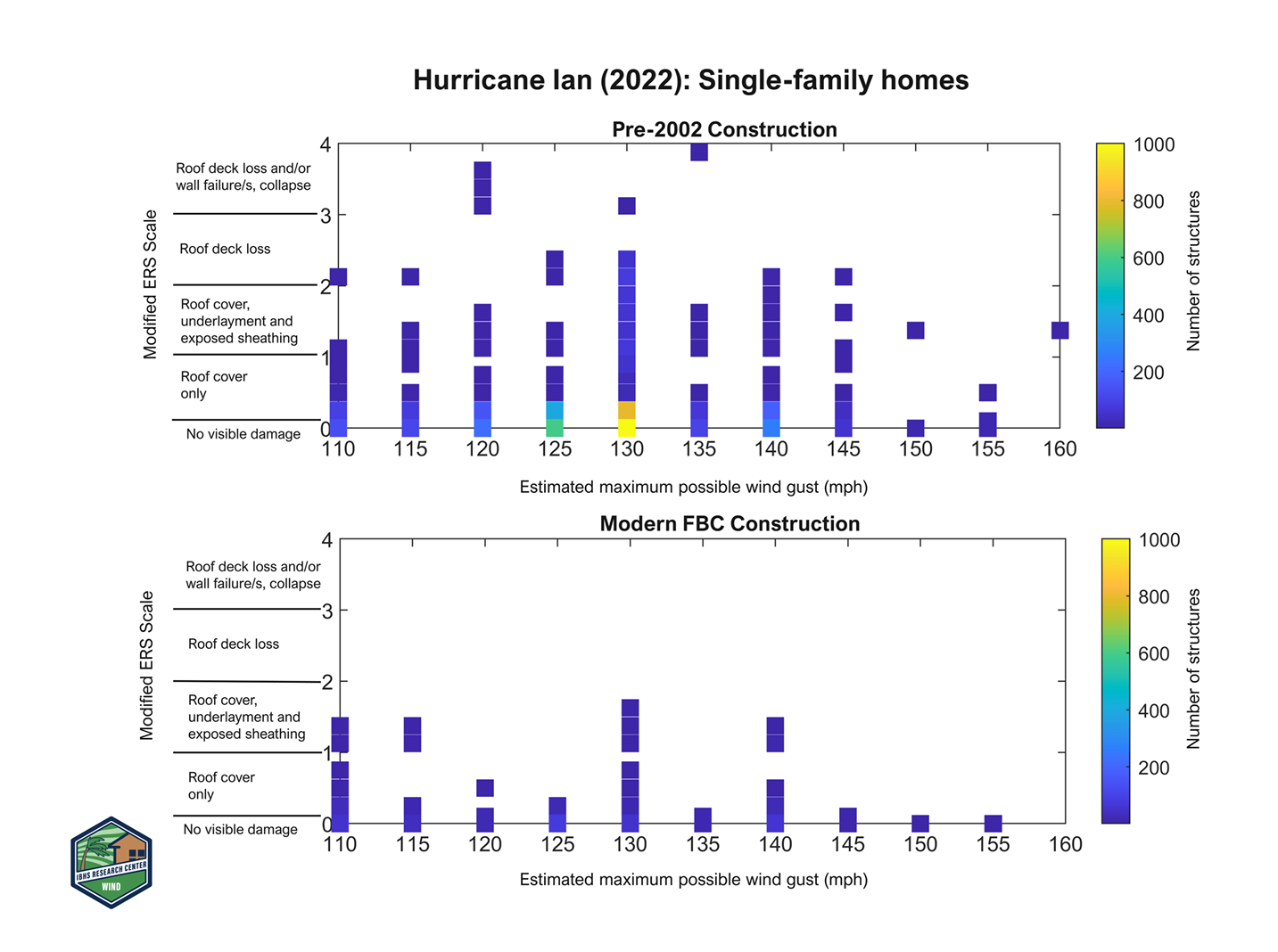

What is the risk of a total loss or serious damage? Gemini starts off by saying that it is pretty high, with 300,000-400,000 single-family homes in South Florida either substantially damaged or destroyed by hurricanes over the past 50 years. That’s out of about 2.7 million homes in South Florida today, but only an average of 1.7 million homes over the 50-year period. (ChatGPT estimates this number as only about half of Gemini’s figure; our future AI overlords are smarter than humans, but equally inconsistent?) So a homeowner’s insurance company has about at least a 1 in 7 chance of making a big payout? Not exactly. First, we have to separate out the houses that were damaged by flooding or storm surge, between 120,000 and 180,000. Homeowner’s doesn’t pay for flood damage. Now we’re down to a risk of about 1 in 10 over 50 years. What about the fact that Florida established a strict statewide building code in 2002, hoping to avoid a repeat of the Hurricane Andrew aftermath, roughly 25,524 homes destroyed and 101,241 damaged (Insurance Information Institute). Gemini:

In major storms like Hurricane Michael (2018) and Hurricane Ian (2022), structural engineers found that homes built to the 2002 code (or later) suffered roughly 80% to 90% less wind damage than their older neighbors.

A report from an insurance institute wasn’t quite as rosy:

IBHS evaluated 3,646 single-family homes, 327 light commercial buildings, and 230 multifamily structures [after Hurricane Ian] using aerial and street-level imagery. … Homes built before 2002 had structural damage levels nearly 2x higher, and 2.3x higher in areas with peak winds above 130 mph.

It looks as though no post-2002 house actually lost the plywood sheathing supporting the roof, but at least some had exposed sheathing and, presumably, water damage as a result. A companion report from the same organization says that asphalt shingles were the weak point, metal roofs were the best (12% damaged), and tile roofs weren’t significantly damaged except those more than 20 years old (“no tile roofs assessed that had greater than 50% roof cover damage” and “the small number of roofs with greater than 25% cover damage … These roofs were all 20 years or older”). Our 2003 house has a one-year-old tile roof with two layers of “peel and stick” underneath. If the tiles are blown off, but the peel-and-stick underlayment survives then we’re looking at a $120,000 insurance claim to put a new tile roof on the house (maybe less if the underlayment isn’t too old and can be retained).

ChatGPT says that 4-6 Cat 4/5 hurricanes hit the Miami-to-Stuart coastline every 100 years. Let’s take this distance as 108 miles. If you assume that the zone of total destruction is 20 miles wide then a typical house gets destroyed roughly every 110 years. If the destruction zone widens to 40 miles, the interval between destruction is 55 years. The most recent major hurricane to hit Palm Beach County was in 1949, 77 years ago, but we could use the 55-year estimate to make the high-net-worth companies look more attractive.

[We’ll ignore tornado risk. A tornado could destroy or seriously damage a house, of course, but it wouldn’t affect an insurer’s solvency because a tornado is local. This is a 1 in 100,000-year event for a typical South Florida house, according to AI.]

As noted above, one quirk of the HNW policies is that they force buyers to pay to insure the full rebuild cost of a house, which for a 2003 house like ours is much more than the house is worth. Imagine if we insured our five-year-old Honda Odyssey for the cost of a brand new Honda Odyssey. Why would we want to do that when what is actually at risk is only about half that number? A neighbor has Chubb and they would pay him over $4 million for the house and contents in the event of a total loss (maybe $5 million if we add “loss of use”). His house has a Zestimate of $1.8 million, has its original roof and non-impact windows, and sits on a lot that should be worth at least $500,000 if the house were razed. The contents of the house aren’t valuable. So he has perhaps $1.5 million that could conceivably be lost under his $4+ million policy. (Note that the neighbor won’t get the high dwelling value unless he actually does rebuild, an irrational choice to make compared to simply moving to a similar house and letting a professional real estate developer deal with the wreck. If the family moves to a $1.8 million house a few blocks away, he gets paid only about $1.3 million (the depreciated value of the structure).

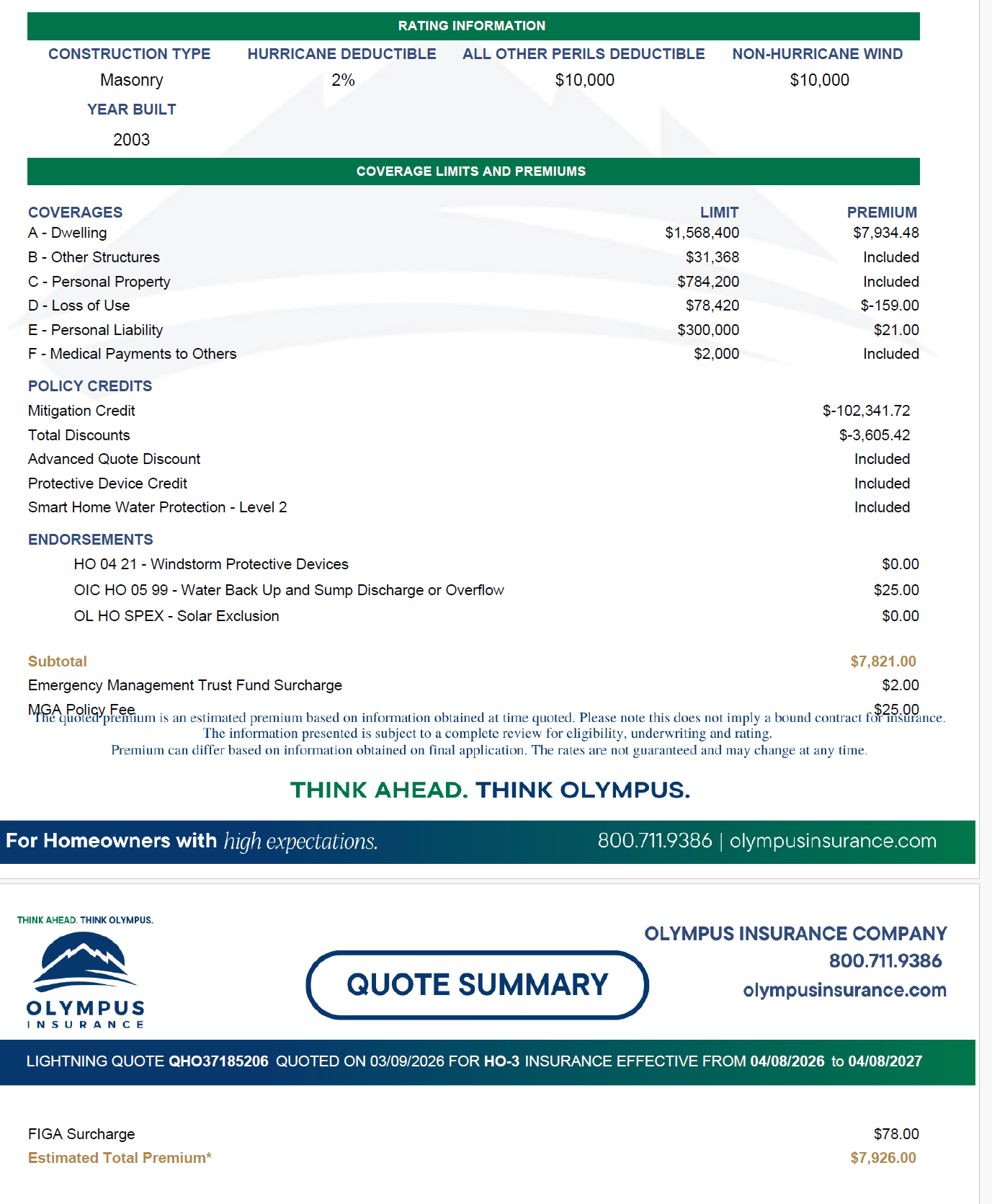

Let’s have a look at a couple of quotes. Below is one from Olympus, a Florida-based company that was founded in 2007, i.e., 19 years ago. Whoever started the company should buy lottery tickets because it was founded right at the beginning the 2006-2015 “no hurricanes making landfall” period. That said, the company has survived the following hurricanes that did make landfall in Florida:

- Hermine (2016)

- Irma (2017)

- Michael (2018)

- Ian (2022)

- Idalia (2023)

- Helene (2024)

- Milton (2024)

Furthermore, Olympus is unusual in being rated by KBRA, which is significantly more stringent than Demotech. Olympus is rated BBB+ by KBRA (over the minimum BBB accepted by Fannie Mae; it’s ironic that the enterprise that generated the largest insolvency in U.S. history, requiring $150+ billion in tax dollars as a bailout, closely scrutinizes insurance companies). For the handful of companies that are rated by both KBRA and AM Best, the ratings seem to be similar.

Could they survive a repeat of the 1949 hurricane that came right into Jupiter? (the most recent major hurricane to make landfall in Palm Beach County) There doesn’t seem to be any way to find out. An insurance company with 50,000 customers, each of which is on its own square mile within the 53,625-square-mile state of Florida is going to be much less stressed by a hurricane that hits Fort Lauderdale than one whose 50,000 customers are all in Broward County, for example. (Broward County was last hit by a major hurricane in 1947, though Hurricane Wilma, Category 2, did about $4 billion in insured damage in 2005.) The information on risk concentration by company is nowhere to be found. In theory, the reinsurers who agree to do business with the companies are looking at this and maybe the regulators.

It is difficult to have faith in regulation when one hears about Florida-based Slide Insurance. The founder and his wife siphoned off $50 million in compensation out of a total profit of $288 million in 2023-4 (source). Based on this, it seems that an insurance company could pay out all of its profits to employees and shareholders during 15 lucky years without major hurricanes affecting its territory and then fold up its tent after a Hurricane Andrew-type event occurs. ChatGPT: “There’s no strict statutory cap tying executive pay to solvency. … As long as they stay above minimum surplus requirements, they’re compliant. But those minimums may not cover a true tail event (e.g., Andrew-scale).” People with inexpensive-by-Florida-standards houses will still do okay with $500,000 from FIGA, of course, so this is a great example of privatized profits and socialized losses.

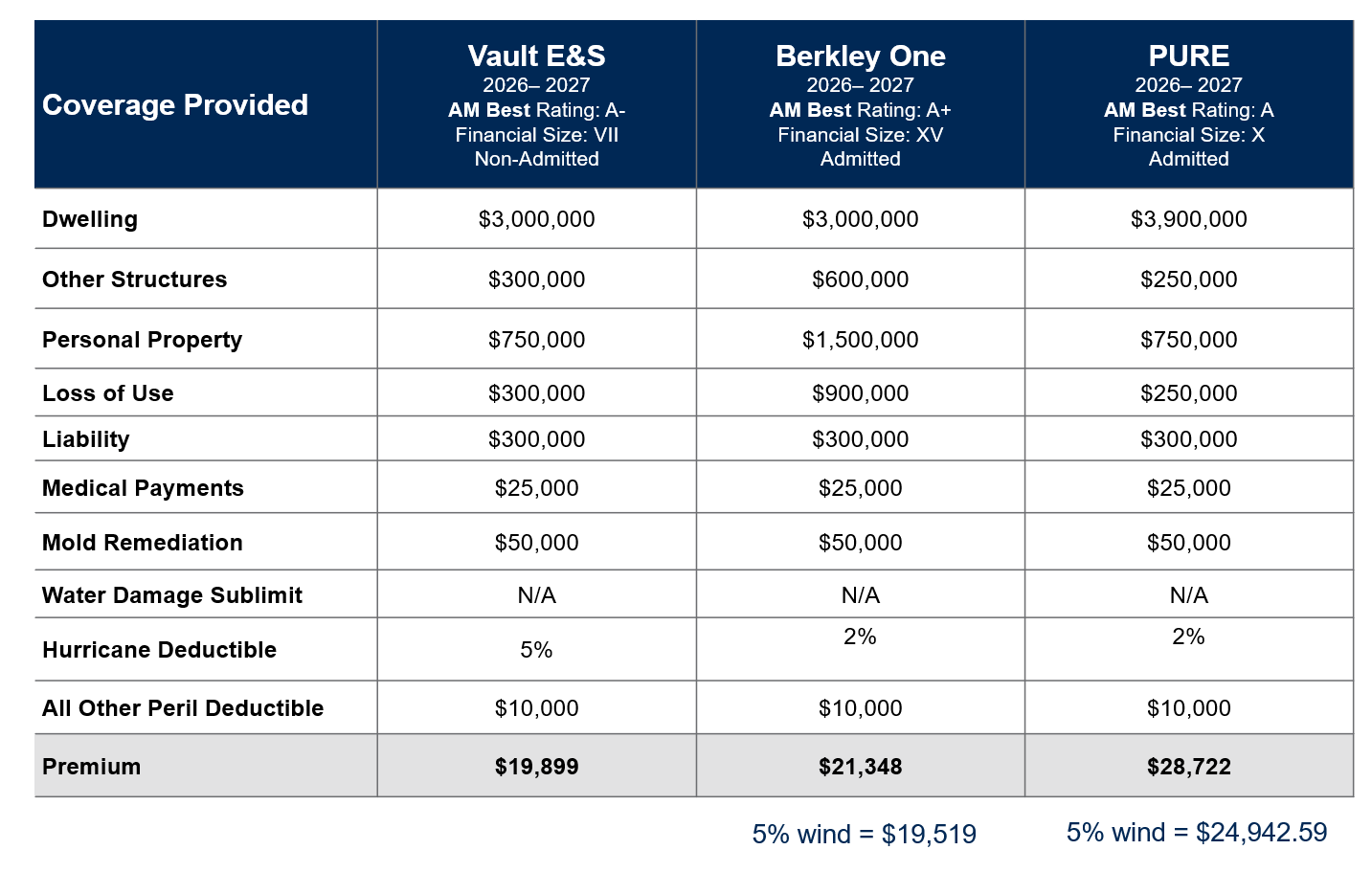

What did the high-net-worth companies have to offer?

Notice the PURE quote with a 5% wind exclusion. If our roof were destroyed, but didn’t leak, and we lost 7 or 8 of our impact glass windows they would still pay nothing because the wind deductible would be $195,000. In a “medium bad” event, the Olympus policy at less than one third the cost could easily pay 2X because of the deductible being only 2% of a much lower dwelling value.

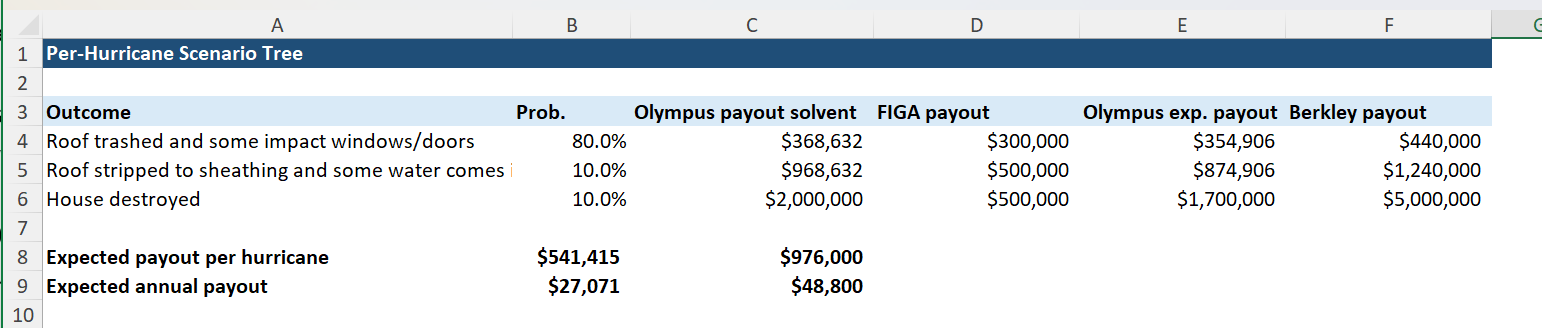

Let’s do a spreadsheet model to compare the Berkeley One policy to Olympus. Let’s assume that climate scientist Prof. Dr. Greta Thunberg, Ph.D. (pre-Queers for Palestine phase) is correct and the frequency and intensity of hurricanes are both increasing. This is contrary to “Changes in Atlantic major hurricane frequency since the late-19th century” (Nature magazine 2021), but it is favorable to the HNW carriers. We thus assume that the destruction zone of a Category 4 or 5 hurricane arrives over our house every 20 years. ChatGPT estimates the probability of a Florida carrier going insolvent in the event of a horrific hurricane season at 15 percent so let’s bump that arbitrarily to 20 percent (Olympus is likely lower risk than other FL-only carriers; see below). We will assume the Berkley One has a 0% chance of being unable to pay claims in full. Here are the assume expected payouts:

- roof trashed and some impact windows/doors need replacement: 80%. Olympus pays $400,000 minus 2% deductible if it is solvent ($300,000 received from FIGA if insolvent); Berkley One pays $500,000 minus 2% deductible (HNW company allows for more expensive contractors)

- roof stripped to sheathing and some water comes in: 10%. Olympus pays $1 million minus 2% deductible if it is solvent ($500,000 from FIGA if not); Berkley One pays $1.3 million minus 2% deductible

- house destroyed: 10%. Olympus pays $2 million if solvent ($500,000 from FIGA if not). Berkley One pays $5 million (luxury rebuild, personal property limit, loss of use).

Does it make sense to pay the extra cost of Berkley One? The answer is… the assumptions are likely wrong. The expected annual payout from both carriers is more than they are respectively charging in premium. This can’t happen from the perspective of someone who worships at the Church of Efficient Markets (e.g., me).

(The Berkley One policy would, of course, make sense for a Thunberg-style climate expert who knew that everyone else was wrong.)

W.R. Berkley reports a loss ratio of 61 percent, i.e., they pay out 61 percent of whatever they collect in premiums. Note that this doesn’t mean they earn a profit of 39 percent; they report a profit of only about 14 percent of premiums, which means their expenses are about 25 percent of premiums (about 10 percent to the agent, for one thing).

(I can’t find data for Olympus, but apparently the high-net-worth companies have lower loss ratios than mass market companies. 65-70% might be typical for a big national insurer. Some of the expenses incurred by HNW insurance might add value to the insured, e.g., consulting services and inspections aimed at reducing the risk of a loss, paying a higher commission to the agent so that the agent can return every call within minutes, etc.)

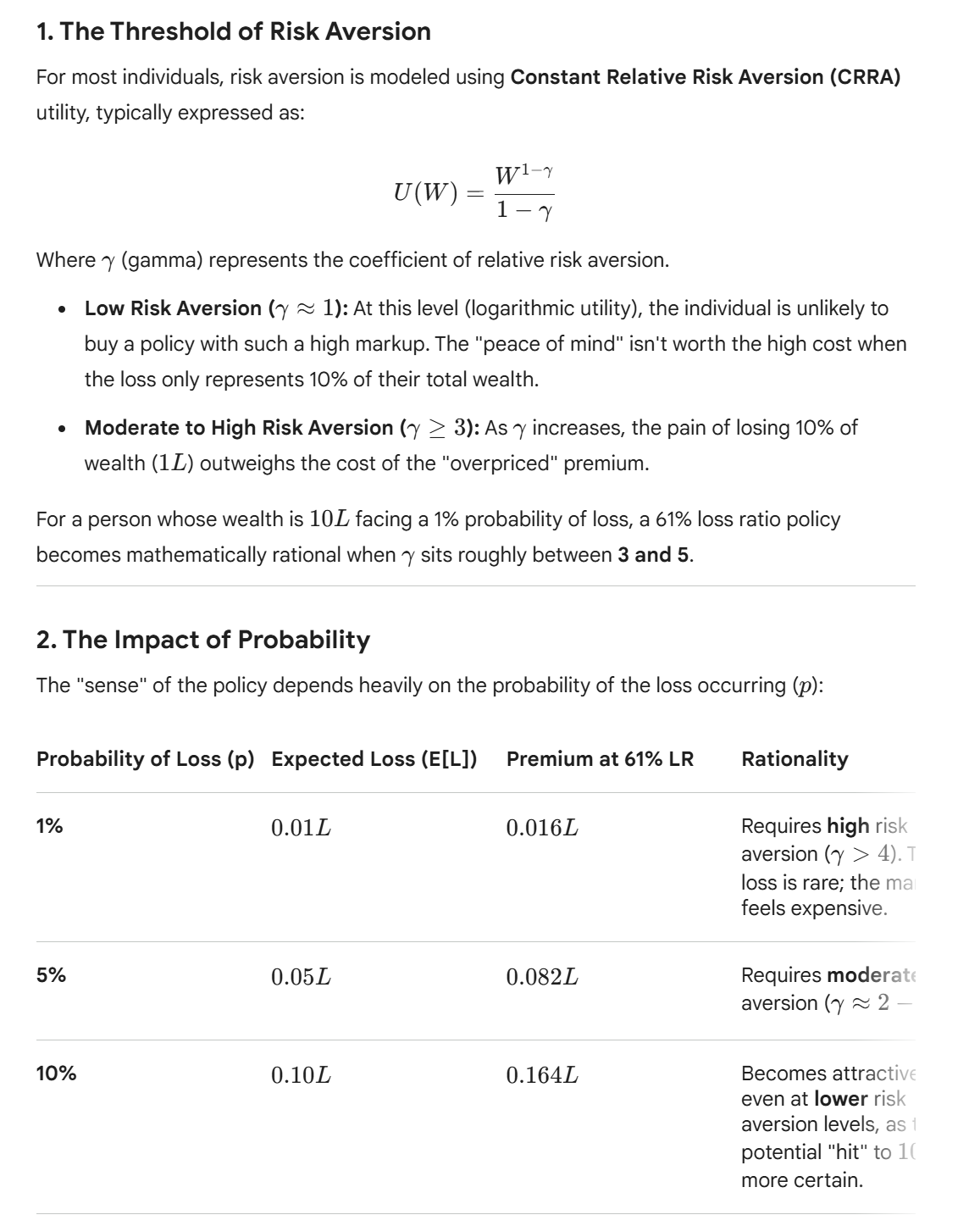

At any loss ratio of less than 100 percent, it would never make sense for a risk-neutral person to buy insurance against an affordable loss. Humans, however, aren’t risk-neutral. We are loss-averse. Prompt to ChatGPT:

Assume a person whose wealth is 10X the potential loss. At what level of risk aversion would it make sense to buy a policy with a 61 percent loss ratio?

You’d have to be an off-the-charts coward! Let’s go back to the Church of Efficient Markets. If people who aren’t forced to buy insurance by their mortgage terms do voluntarily buy insurance, this calculation can’t be correct.

Gemini gives a completely different answer, from the same prompt, that is consistent with human behavior:

When ChatGPT is shown Gemini’s analysis, it corrects its own and comes to agree with Gemini. But this analysis is done with a one-year horizon. What does being a customer for 30 years look like? Gemini:

Over 30 years, the cost of the premiums (the “load”) compounds. If you pay an overpriced premium every year for 30 years, you are almost certain to lose a significant chunk of wealth to the insurance company’s overhead.

If you have $10X$ wealth and the loss is $1X$, the 30-year horizon actually makes self-insurance (not buying the policy) more attractive for most people, provided they are disciplined.

At a 61% loss ratio, the insurance is quite expensive. You would only buy it on a 30-year horizon if you lacked the liquidity to handle the loss at any single point in time—but since you have 10X wealth, you do have the liquidity. Therefore, the higher your wealth-to-loss ratio, the more the “annual” math dominates and suggests you should skip the policy unless your risk aversion gamma is very high.

Annual View: You pay a small premium to avoid a “freak” 10% loss this year.

30-Year View: You realize that over 30 years, you have a high chance of either never having a loss or having one that you’ve already “pre-paid” for through three decades of expensive premiums. Because you have the liquidity (10X), you can afford to “be the house” and keep the 39% markup for yourself.

So… the best financial choice, for someone whose lifestyle won’t be changed by the loss of a house, is to buy no insurance. If forced into buying insurance, the $7,926 Olympus policy is the more rational choice over a long-term horizon. Gemini is particularly impressed by the fact that Olympus was acquired by a larger company, though the policyholders of Olympus don’t have access to the larger company’s capital in case the worst happens:

The most significant change for Olympus is the January 2, 2026, acquisition by SageSure.

- SageSure is a massive player managing $3.2 billion in premium.

- They acquired Olympus specifically to target “mass-affluent” homeowners in Florida.

- They have already secured $120 million in new catastrophe bonds (Abacab Re) specifically for this portfolio.

I like the term “mass-affluent” better than “way too poor to afford a house in Palm Beach or Gables Estates” or “Publix-shopping minivan-driving peasant”. It looks like “mass affluence” starts at a house worth well under $1 million because the Olympus web site says that they cover 80,000 homes for a total value of about $74 billion (this includes “other structures”, personal property, and loss of use). Or maybe these data represent Olympus’s legacy customers and they’re trying to move upscale?

Thanks for bearing with me so far. Maybe there is one area where it could be sensible to pay more for HNW. The non-HNW option seems to be much better aligned with (1) the actual value of the asset being insured, (2) financial responsibility. Suppose, however, that it is simpler and easier to get paid by the HNW company. Chubb is famous for just writing checks, taking the customer’s word for what happened or what something was worth. We don’t have any Damien Hirst pickled sharks or cows that the kids could breach with a baseball bat, but maybe we could expect to save 100 hours of time over 20 years in not arguing with an insurer over the proper amount of a claim? Is that worth paying roughly $240,000 extra in premium? It could be to a Big Law partner or a superstar specialist physician because it works out to $2,400 per hour.

Alas, my time is not worth $2,400 per hour. Ergo… we bought the Olympus policy.

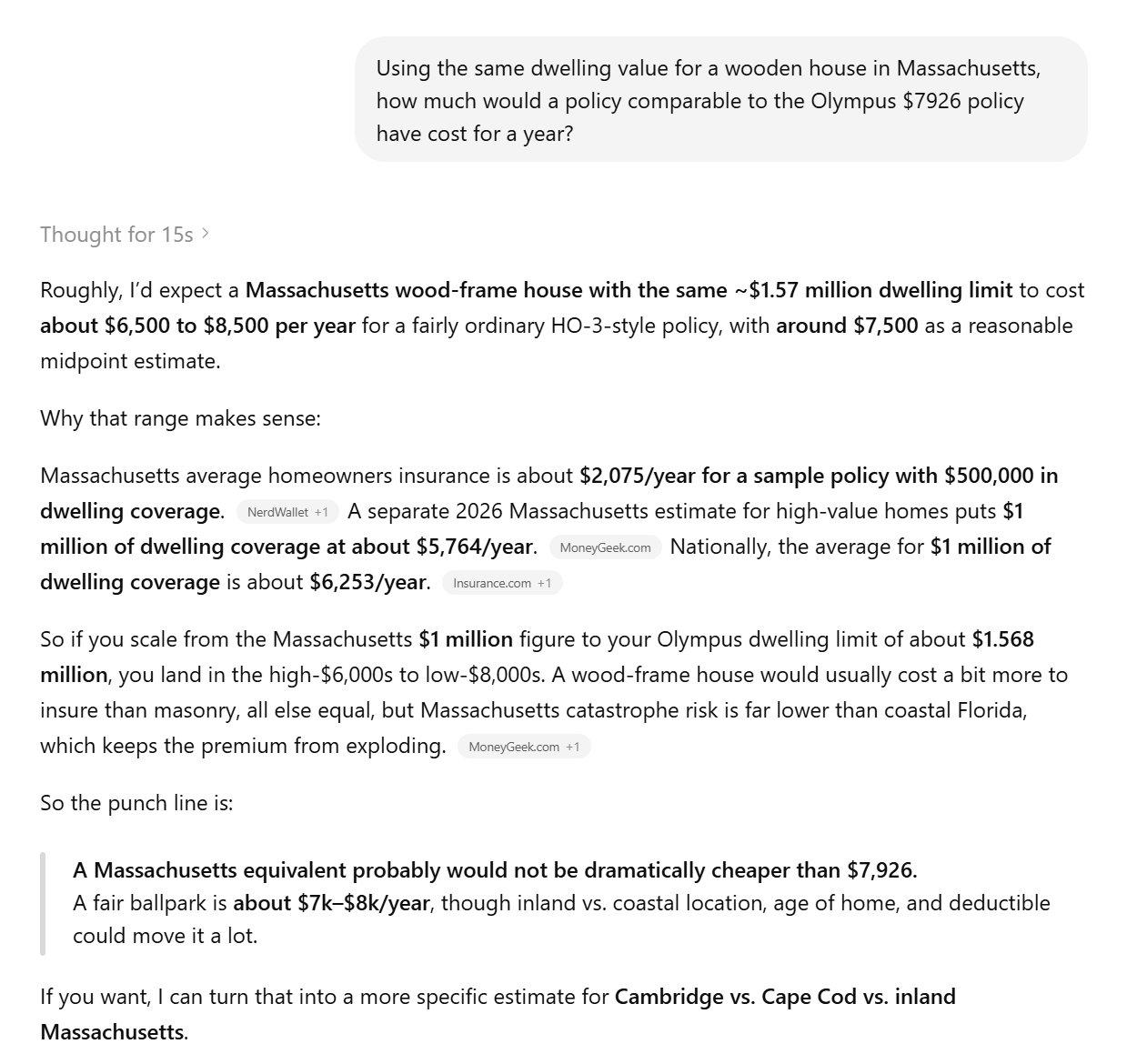

Related… we’re informed that nobody should stop paying taxes in Maskachusetts, New York, Illinois, or California and move to Florida because the cost of homeowner’s insurance in Florida will be more than the 5-13.3% of income that these states collect as state income tax. Homeowner’s insurance in Florida is so expensive, in fact, that it will even undo the benefit from not paying the 16% NY, IL, or MA estate (“death”) tax. I asked ChatGPT what it would cost for a similar policy in Maskachusetts:

ChatGPT says that it would cost about $7,500 for a similar-value insurance policy in MA and that being near the water on Cape Cod would push it up to as high as $13,000 per year.

This might not be a completely fair comparison, though, because people at the same income tend to “live fancier” in Florida. There is no concept of Yankee thrift here. So most likely a person who moved from a $1 million house in MA will end up in $1.5 million house in FL and this could account for the perception that homeowner’s insurance is much costlier for movers. Also, an old wreck of a house in coastal Florida will be more expensive to insure than a comparable old house in Massachusetts because the insurance companies in Florida will add a lot to the price for the age/roof risk.

Answer in the form of a question: Ask your VHNWI advisor? (Although they probably would charge you more than your house is worth just to read this blog article.) I’ve found that the Internet is a less than ideal place to ask for financial advice. YMMV

Ask people who get paid huge commissions for advice on whether to purchase a product that pays a 25% commission to the originating agent? (A lower percent in renewal years.)

And if they had the audacity to charge 25% interest on pay day and title loans, bleeding heart liberals would complain that it was usury. Oh wait… Only on this blog will we see the true plight of the ultra wealthy.

In my limited brain, insurance is betting that you’ll lose and the odds are against you, because someone else has already done the math.

I buy only required insurance and put money where I’m more likely to get it back at some point.

> […] insurance is betting that you’ll lose and the odds are against you, because someone else has already done the math.

That’s an interesting way to think about it. I agree with your conclusion in the next paragraph. But I don’t agree with the “odds are against you”. I think of it in the way of Russian roulette. The odds of one getting shot are low, similar to whether one would really end up using insurance. But the damage if one gets shot is so high that they’d want to get insured.

In 2023 Florida represented 6.8% of the US population, and 7.2% of private dwellings in the US, so a 10% of the total US claims should immediately raise red flags.

I strongly recommend you, like me, move to a geologically stable, weather boring place like Finland (we need young people!). I say weather boring because climate wise it can get fresh in winter, but at no point your roof is in danger unless it is basically falling apart due to age and disrepair.

Moving, not insurance, is the right answer.

Also, depending on your language, the acronym FIGA is especially entertaining.

> we need young people

I’m a young 60, from clean living and idleness, currently in the U.S. — maybe a bit old. But I have a decent trust fund, which enables me to sit around and do nothing all day. Do you need good folks like me? I could fake MS to get MMJ. I loved lounging around streaming Finnish movies during the Corona-demic. I especially liked Kaurismäki’s Proletariat Trio, and I’m a big fan of Kati Outinen. And Mika Häkkinen? Formula 1 GOAT. My Finnish language skills are poor. You could practice your English on me. Also closer to Greta T. Win, win, win for me.

Finland, Finland, Finland

The country where I want to be

Pony trekking or camping or just watching TV

Finland , Finland , Finland

It’s the country for me

— Monty Python, Finlad

Just checked my investments. I’d probably need a decade or so of public assistance to live in Finland. Any room for a refugee from a paternalistic, oppressive colonialist regime? The life of quiet desperation as portrayed in The Match Factory Girl, especially in a low cost of insurance climate refuge, seems ideal for me. Hope there is room and you take non Muslim applicants.

NH: I don’t know what’s ‘paternalistic’ to be honest. But if you mean the same what Gemini outputs:

> Paternalistic describes an authority figure, government, or organization that restricts the freedom or autonomy of subordinates, ostensibly for their own good. It behaves like a strict parent, making decisions for others without their input, combining benevolence with high control. Common examples include mandatory seatbelt laws and employer-provided welfare.

Greta’s home country’s policies seem very paternalistic. The country restricts freedom by giving lower salaries, promoting group culture instead of individualism, at least at work, and, IMO, people who only like groups of very independent-minded people would have a difficult time there. A smart physicist coworker who had lived there for a long time called it a nanny state.

> I don’t know what’s ‘paternalistic’ to be honest

I was making fun of social justice warriors, who don’t want men to run things — a reason to claim refugee status. Pater is Latin for father, and does show the bias in Western culture of the father as the head of the family in the word paternalistic (contrast maternal). The SJWs use “patriarchal” as an insult too. One of Trump’s achievements, actually, is providing some opposing force to the immovable female SJWs. As a low-contributing member of society, I might fit in well in a nanny state, free milk from the teat of the government.

Back to insurance, it seems like some nanny stating and subsidizing in the Citizens insurance program. Too exhausted to look it up.

My father and brother each own 70-y/o single-family homes on FL’s east coast, one block from the ocean. Both were bounced out of FL’s insurer of last resort (Citizens) to Slide last year. Both of them exclude windstorm/hurricane coverage and the annual premiums run about $1200. An additional $2000 for windstorm.

I’m three miles from the ocean, also in a 70 y/o sf FL home, non- flood zone. My prop insurance is $1100 excluding windstorm.

I don’t understand how Citizens makes sense. On the one hand, a state government has almost infinite reserves (the taxpayers!) and a low cost of capital (can issue muni bonds) so if a state were efficient maybe it could underprice all private sector insurers. On the other hand, Citizens by design is going to cover only the very worst risks.

From https://www.clickorlando.com/news/florida/2025/11/25/citizens-property-insurance-drops-to-its-lowest-number-of-policies-since-2019/ :

Yaworsky, however, cautioned last week that the state needs to be careful with depopulation. At least in part, that is because Citizens will have less money coming in with fewer customers. Yet it will need to have enough money to pay claims of remaining customers if hurricanes hit.

“Those properties that will remain in Citizens will be the ones that are, for one reason or another, are the least likely to be insured by the private market, which generally means they’re too risky for one reason or another,” Yaworsky said. “So as we go through this process, it’s very important that we look at that takeout (of policies). It’s very important that we’re mindful that over-depop could actually trigger the assessment we’ve always tried to avoid.”