Our government has provided us with a fresh fictitious inflation report today (the fiction is that a person can rent the same single-family home in the U.S. for 20 years and do so at a cost lower than mortgage, property tax, maintenance, insurance, etc.; “owners’ equivalent rent”).

Conventional advice for retirement saving is to buy at least some bonds rather than hold an all-stock portfolio. How can that work given the miserably low yields on inflation-protected bonds (TIPS) and the payments in nominal dollars that get ravaged by inflation any time our wise politicians feel the need to print money?

“A Yale Professor’s Investment Formula Says You Need More Stocks. See How It Works.” (Wall Street Journal, February 2026):

The formula’s central insight is that the future paychecks and retirement benefits that someone has yet to receive in their life are, when taken as a whole, like a bond because fluctuations in earnings aren’t strongly correlated with stock-market returns. For this 25-year-old, that big, bondlike chunk of future money means they could more easily weather a steep drop in stocks.

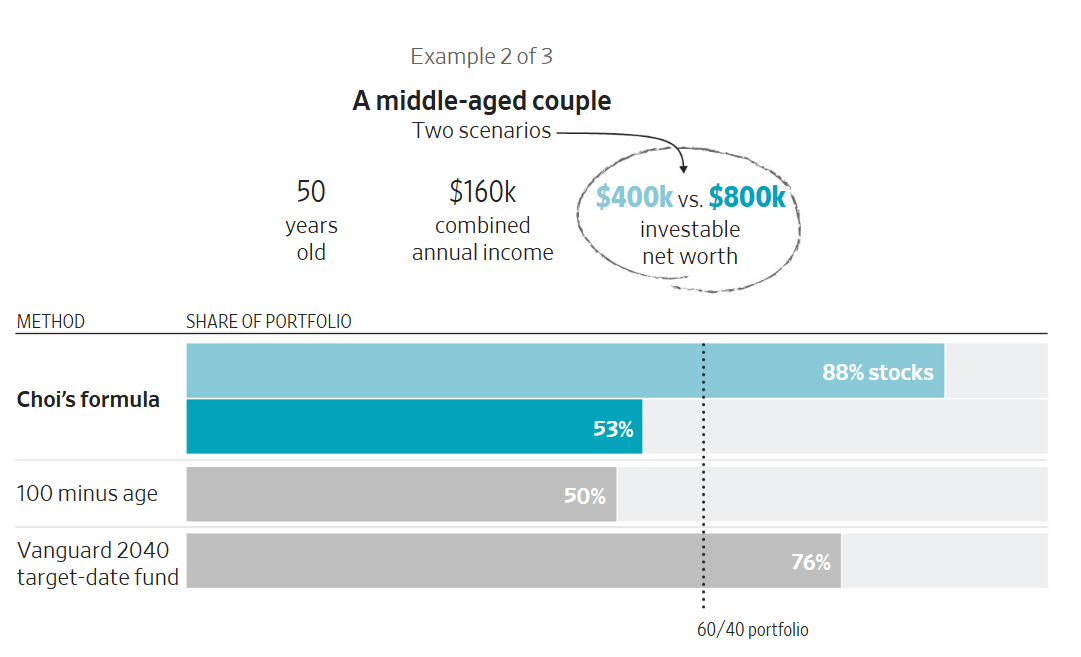

As another example, the way it treats a hypothetical middle-aged couple differs based on the amount they have saved up.

In both scenarios, the formula steers the couple toward a lower equity allocation than it did the 25-year-old, because a smaller share of their lifetime income is still to come.

But it recommends a much lower allocation, 53%, when the couple has twice as much money to invest, because in that scenario upping the equity allocation would alter the risk profile of a larger proportion of their projected lifetime resources.

“It’s more conservative when you have more money saved up,” Choi said.

For a middle-aged couple with what someone in Miami would call “no money” (either $400,000 or $800,000 saved, neither of which will pay for a kitchen renovation), the Yale genius says that two men (it’s the WSJ so both participants in the “couple” must be guys in order that they can eventually form an all-male throuple) should have as much as half their portfolio in bonds (the non-academic non-geniuses at Vanguard give these two guys only 24% bonds):

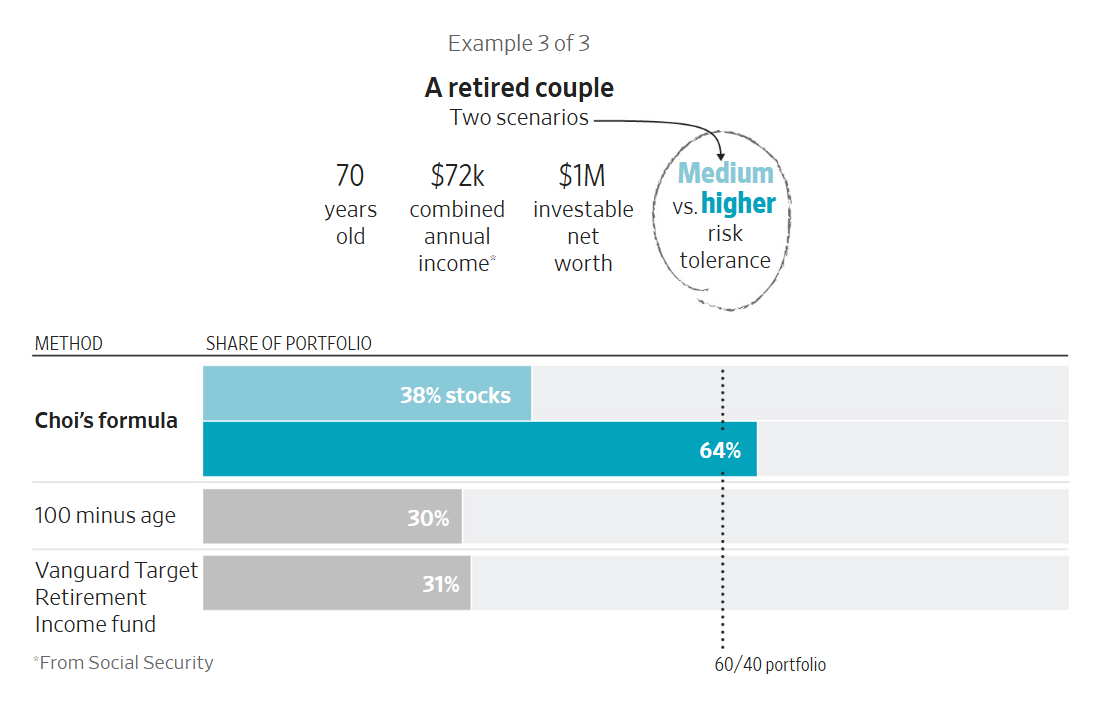

What drops out of this thinking, for people aged 70, is that they should have somewhere between 35 and 70 percent of their investments in bonds:

After living just recently through Bidenflation and having a personal memory of the Jimmy Carter-era inflation (maybe not too different, actually, if CPI were calculated in the same way), this seems intuitively wrong. The 70-year-olds could live to be 100 via GLP-1 and whatever medical miracles LLMs can come up with. The 70-year-olds might care about leaving some money for their children and grandchildren, now forced to compete with 70+ million immigrants with whom the Boomers didn’t have to.

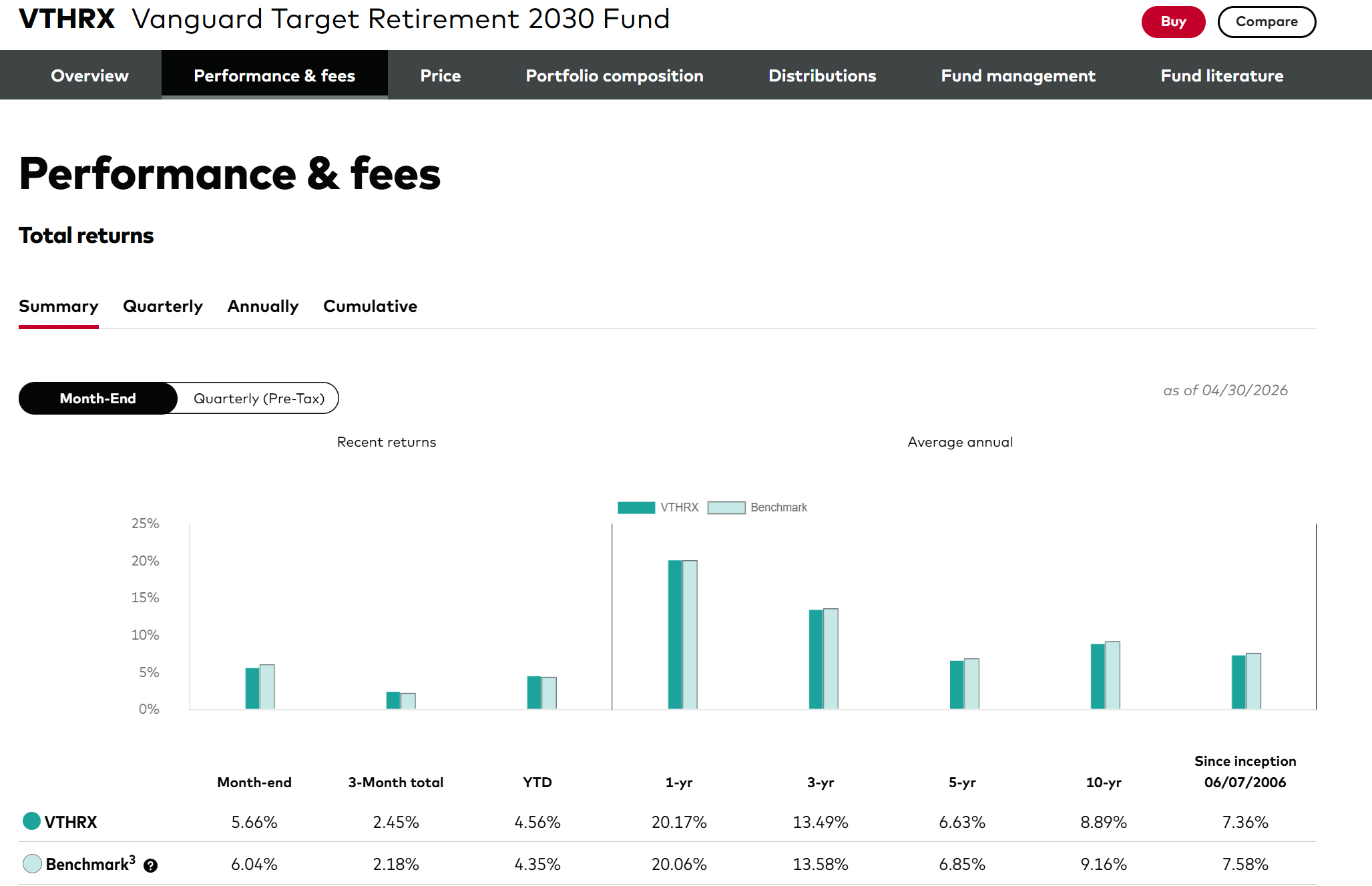

Maybe we can simply look back. The “keep adding bonds with age” strategy is embodied in the Vanguard funds. The Vanguard 2030 fund was created almost exactly 30 years ago. It has returned about 7% per year:

2006 wasn’t a great time to buy an all-stock portfolio, since you had to make it through the Collapse of 2008. Nonetheless, ChatGPT says that SPY has enjoyed a total return (dividends reinvested) of over 11% annually since then. The difference of 4% doesn’t sound huge, but that’s 100 percent of the standard formula of how much a person can spend in retirement from his/her/zir/their assets and not go broke for 30 years. For someone who started with $100,000, the S&P 500 investment would have grown to over $830,000. The same investor in the Vanguard part-bond fund would have only $430,000. That’s the difference between a totally-pimped house in The Villages (the fun center of Elder Florida) and a used/basic house in The Villages.

Note that the above calculations don’t include federal, state, and/or local income taxes that the investor would have had to pay on the dividends received into any non-retirement account. Taxes are worse for the part-bond investor because the yield is taxed as ordinary income and not subject to the qualified dividend discount. Also, stocks deliver much of their return via appreciation rather than by paying dividends. So the corporation may pay income tax, but the investor need not. ChatGPT says the $830,000 stock portfolio would be more like $625,000.

How about all bonds for 20 years? ChatGPT says the return would have been only 3.1% year. The $100,000 would have become $184,000, a laughable $12,000 in appreciation after adjusting for official CPI (i.e., it would have shrunk in terms of the ability to buy and maintain a single-family home). This turns into a real-dollar loss if held in a taxable account, having appreciated to only $144,000 in nominal dollars. The $100,000 became $87,600 in 2006 purchasing power (official CPI).

I’ve always struggled to comprehend why investors are willing to buy bonds priced in nominal dollars, which nearly all bonds are. Someone took the other side of our absurd mortgage, issued at 3.125% just as Bidenflation was gathering a major head of steam in February 2022. I would love to meet that person and ask “What did you think was going to happen?”

Readers: Can someone please sell me on why a typical investor would have even 1% bonds in his/her/zir/their portfolio? Let’s assume we’re talking about a 65-year-old. Because this person has money, it is likely that he/she/ze/they has children (fertility vs. income shows it is Americans with zero income and those with high incomes who have kids; the working class are being bred out of existence). Our hypothetical saver wants to not run out of money even if death comes at 111, which was the age of the oldest person receiving General Motors pension and health care benefits before the company went bankrupt/got bailed out by us in 2009 because they couldn’t pay their union retirees all of the promised pension and health care benefits. Our hypothetical saver would rather leave more than less to his/her/zir/their children and grandchildren. We’ll assume that 30 percent of the saver’s portfolio is in a tax-exempt retirement account. Could the answer be “It makes sense to buy bonds when the S&P 500’s average P/E ratio exceeds a threshold and trade them for stocks when the S&P dips”?

Half of the money printing happened under Trump during 2020. Biden didn’t help it but Trumps policies and new quagmires surely aren’t helping stopping the $100 hamburger turn into a $1000 hamburger.

JT: You’re right, of course. The same thing happened to Jimmy Carter. Johnson’s Great Society and Vietnam War programs were the big drivers of inflation in the 1970s, but things didn’t get out of control until Jimmy Carter arrived in the White House. For our recent inflation, I think that Congress, Obama, and Trump can all legitimately be blamed for the massive deficit spending that everyone decided was reasonable/prudent (and then the Quantitative Easing that was piled on top).

JT, bros like me don’t care bout “inflation.” My SNAP benefits are fully indexed, my Medicaid is paid directly by taxpayers (suckers) etc. Get with the program. If you need some advice, reach out. I’m available all day long every day.

There’s an argument for leveraging taxable investments where interest expense is a deduction, and buying bonds in an IRA where the interest is tax free.

Of course you might need to contribute some of your leveraged equity windfall from the taxable account to the IRA, to make up for the inferior bond returns 😉

Sequence of returns risk affects most everyone below $7M. Basic expenses for the wretched refuse often require selling all their shares during a bear market, especially the poor slobs below $2M. Above $7M, they have enough leftover shares to outlast any bear market.

There are fixed income instruments that beat official inflation numbers.

Living below means while having fun is a must for any investor who is starting from zero or coming from modest means. Not wealthy but never lost money in bear markets. Sell only when trully need to or for a good trade.

I cannot wrap my head around those investment strategies. Sadly, I don’t have a PhD or the sophistication IQ of welfare recipient to confidently invest or live off other peoples hard earned money.

What I do know is that up to 28% of my income goes to welfare spending, and another 18% goes to healthcare, over 45% of what I make that could otherwise have been invested toward my retirement.

The arguments for bonds in a portfolio are that they reduce volatility (risk) in a portfolio and protect against deflation – not that you are going to make a lot of money unless you trade bonds & that is not for amateurs. The right percentage of bonds in a portfolio will vary according to a lot of factors including the investor’s risk aversion, future earnings power and age & could range from 0 to 100%. There is no one size fits all since everyone’s circumstances and risk aversion are different. TIPs in fact hardly have “miserably low” yields. A 10 yr TIPS has a real yield of around 2.169% which is then added to whatever inflation will be over the next ten years. The last time I checked that real yield was toward the high end of TIPs real yields over the last decade or two. TIPs are essentially insurance against unanticipated inflation. The 10 year nominal yields around 4.548% so the break even is 2.37% annual inflation over the next 10 years -i.e. the market for the 10 year treasury is predicting 2.37% annual inflation over the next 10 years. If you want to insure against inflation running over 2.37% annually till 2036 then TIPs are a good choice. They need to go into a tax advantaged account since they otherwise they have negative tax ramifications. As for formulas for shifting between bonds and stocks, one approach is Robert Schiller’s CAPE. Schiller is a professor at Yale and won a Nobel Prize in economics for his work in asset pricing. Schiller is a highly intelligent guy & has a website that has details. I am dubious as to CAPE’s validity and don’t pay it any attention. Though some people do.

Philip,

This is Alex K’s mom, Karen. It’s been a long time since his passing on July 6th, 2023. I have received information on you and your family via Xmas cards, but don’t have that much time to really keep in touch the way Alex would have wanted me to. In any case, we think of you often, I try to read your blogs, to keep reminding me of what Alex said to me right before he died, “Mom,

don’t cry all the time, I am going to a better place now and I will be alright, I promise you. Take caare of Stephen, (his brother{and make a plan, a REAL plan, to provide a secure future for him.

Go to all your health appointments, wear the right shoes all the time, use yuor walker when you need to, use a cane when you need it, tend to your flowers, the hummingbirds like PINK and red, and remember above all, WE WILL MEET AGAIN SOME DAY.”

Philip, please stay in touch, it’s not over yet. More to come.

Kiss Mindy the crippler, Alex Olga, and anyone else I may have forgotten. Happy Florida sunshine, send it up this way!

With fondness and appreciation,

Karen K.

Gosh I’m glad I looked at comments today.

Darn pollen . . .