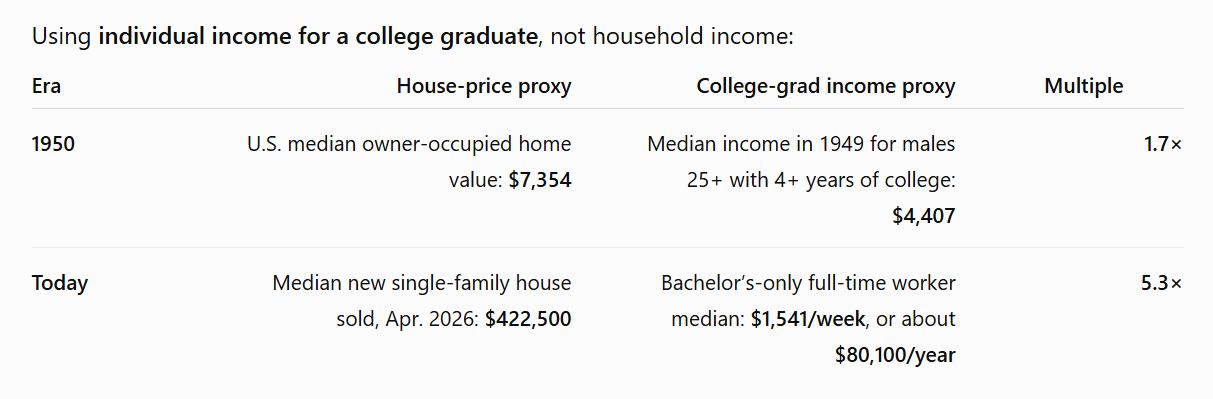

White-collar men in the 1950s often characterized their world as a “rat race”. If college-educated, they competed with only a small subset of Americans for high-paid desk jobs. Men in the 50s did not compete with immigrants because substantial importation of humans into the U.S. stopped in 1924, not to be restarted until President Johnson signed the Hart-Celler Act in 1965 (see below). A house in a safe suburb with good schools and A/C could be purchased, at the end of the 1950s, for about one quarter the cost today (in real dollars; see $112/month to live in a brand-new house in Bowie, Maryland). Relative to income, a house cost about 1.7X annual salary vs. over 5X today (ChatGPT table below). Partly due to this low cost for housing in a safe suburban neighborhood with decent schools ($1+ million today?), a man’s income was generally sufficient to support a wife and 2-3 children as well as himself. Sex outside of marriage was discouraged both legally and socially and, therefore, the man would usually be married before age 25. No-fault divorce (“unilateral” in research parlance) did not exist and, therefore, if the man wasn’t behaving outrageously (beating the wife, drinking heavily, failing to work, having affairs), the wife couldn’t profit via a divorce lawsuit (a divorce might be arranged by mutual agreement, of course). In addition to marital security, the 1950s man often enjoyed a lot of job security from (1) the lack of competition in the labor market, and (2) the tendency of large companies to provide lifetime jobs, which today is limited to government work.

What’s the correct term for what similar men face today? They inhabit a world in which you can’t spit in the street without hitting a college graduate. Men must compete with women for jobs and, despite women being more likely to earn college degrees, be passed over for hiring or promotion when a company decides that “diversity” is its strength. If a female or favored minority human competitor doesn’t take the white-collar man’s job, Claude is ready to replace him. The companies that once offered native-born Americans jobs for life are now home to platoons of H-1B “non-immigrant” immigrants.

A house in a neighborhood with low crime, an orderly familiar culture, and good schools, is about 10X the median college graduate’s income (5X for houses overall, but the typical suburb is no longer a white picket fence idyll). A college education for the kids, so that they can get into the “rat race” that the parents ran, is now 5X more expensive state colleges and 9X more expensive at elite Queers for Palestine-type schools . (ChatGPT on the history of federal government programs to make college more affordable: “GI Bill for veterans in 1944, first general federal student loans in 1958, major modern federal aid framework in 1965, and Pell-style direct grants in 1972/1973”)

Where in the 1950s he likely partnered with a virgin aged 20 (ChatGPT says 10-25% of 1950s brides might have had sex with someone other than their fiancé/husband), today he’s with a 30-year-old veteran of the sexual revolution. If he is persuaded to marry her, she can sue him for divorce a day later for any reason or for no reason. For men who strayed in the 1950s and got sued for a “fault divorce”, the resulting financial drain was primarily alimony and it lasted only a few years because the plaintiff would remarry and that shut down the alimony revenue stream. The risk of losing his role as a father was controllable due to the requirement that a plaintiff find a “fault” ground, such as infidelity. If a man gets sued today because the wife found someone she likes better, the man can lose his “father” role, and access to the young people who used to be his children, due to factors entirely beyond his control. The man’s biggest financial exposure in a divorce lawsuit is typically “child support” (paid to an adult female to spend on whatever she wants, not to a “child”), which can last for 23 years (Massachusetts) or 21 years (New York) even if the plaintiff has married her lover and that lover earns far more than the defendant and even if the lover is the biological father of the child (nytimes: “I pay child support to a biologically intact family, a father and mother, married, who live with their own child.”). (In the cases where alimony is the primary profit from a divorce lawsuit, the defendant might be paying for 50 years because there is no longer any social pressure for the plaintiff to remarry. She can have sex with 100 men and write a magazine article about the “single MILF” lifestyle and this has no impact on her cash entitlement.)

This is not to say that American in the 1950s was better overall, of course. We had been starved of enrichment via immigrants since 1924 and, therefore, weren’t as strong under the “diversity is our strength” axiom. We didn’t have Internet or LLMs for personal use. A 1950s car, though beautiful in our museums today, came out of the factory as a junk heap compared to a 3-year-old Toyota today. We had three TV channels to watch on a 21″ CRT. But in terms of career security and personal life security, the 2020s are inferior to the 1950s. So, returning to the title question… if the 1950s were a “rat race” for white-collar men, how would we characterize the situation today?

Loosely related…

A post on X from an offensively titled username so I’ll just copy the text:

White Americans and Europeans are the ONLY people worldwide that are EXPECTED to compete with the ENTIRE world for jobs.

50+ years ago White men with STEM degrees got good jobs. Things like engineering or applied mathematics guaranteed a good career.

Now we are required to compete against not just our own people, but the brown and black hordes worldwide that are willing to work for pennies.

It was an ECONOMIC CRIME committed against our people.

(I post this not for the truth or falsehood of what the author writes, but for the expression of a feeling of insecurity and, therefore, pressure even worse than the rat race of 50 years ago.)

In other news , the person who is responsible for worst financial bubbles/recessions in modern times(2001 and 2007) died today.

Whoa. Alan Greenspan lived to 100, but that still wasn’t long enough to see SpaceX make a profit!

Not only did Alan live long enough to see SpaceX earned a profit, but it happened two years ago. They earned $791m in 2024 (it’s in the S-1, which you “read”).

FR: Sorry if I was unclear. I didn’t mean to suggest that there was no window of time within its 24 years of existence during which SpaceX had an accounting profit to report. For a company to “make a profit” it actually has to… make a profit. An easy way to look at this is to check for when it has used up any net operating losses from previous years, for example, and thus becomes subject to corporate income tax. Amazon began to make a profit in 2009 (cumulative accounting) or 2010 (used up all of the tax carry-forwards). That’s about 15 years after inception. Check back in with us when SpaceX has at least used up its NOLs (ones from the early days might have expired so even that wouldn’t signal an actual profit)!

https://www.satellitetoday.com/finance/2026/06/03/assessing-spacex-finances-addressable-market-and-the-ai-pitch-ahead-of-ipo/ :

“The most startling number in the S-1 is the accumulated deficit of $41.3 billion as of end of March, which is the running total of losses since inception. We knew SpaceX burned cash, but seeing that number in black and white, alongside a $4.3 billion net loss in just Q1 2026 alone, is a sobering reality check against all the hype.”

Their pre-tax profit in 2024 of $242m has nothing to do with NOLs (pre-tax is before any impact from taxes, including NOLs).

FR: If you think that losing a cumulative $41 billion loss that includes a brief period of the accountants declaring a $242 million profit is an example of a profitable business then I hope you’re buying the 2X leveraged version of SpaceX that is now available (SPCF).

Your comments suggest a common misunderstanding of finance. The value of a stock (owning the equity in a business) is the future cash flows of the business discounted back to today. You clearly don’t believe it was profitable (GAAP P&L profits) in 2024, but any finance expert would assure you that you are mistaken. That said, you might want to also look at the cash flows the business has generated because they are crystal clear. Operating cash flow is considered the gold standard metric for any business because it strips out accounting issues that often distort the P&L and reflects the actual cash being generated by the businesses, which can then be reinvested in the business (capex) or returned to shareholders (by dividends or share repurchases, for example). Cash flow is the only metric an investor owning a stock should care about long-term (because it is what determines the value of a stock as noted above). By that important metric, SpaceX has been highly “profitable.” Operating cash flow was $4.5b, $5.8b, $6.8b in 2023, 2024 and 2025. Why has it been so cash generative? Because two of their three businesses are cash flow machines (Connectivity/Starlink and Space; Connectivity/Starlink had an off-the-charts ebitda margin of 63% in 2025 and revenue growth was 49%). The third business (AI) is very early stage and is not generating profits or cash flow now, just as Connectivity and Space did in prior years as they spent heavily to build those businesses. This phenomena is very common in many businesses (years of investment before the cash flow payoff). If you spend some time reading through the S-1, you may find some other interesting things that would help you understand their businesses. Please don’t consider this (or any of the prior comments) as an endorsement of the stock, but rather as a way to understand the businesses and hence what the future cash flows may or may not be.

How about a simpler standard. A business “makes a profit” if it is rich enough to keep this lady on the payroll: https://nypost.com/2026/06/23/business/woman-who-emptied-knicks-trashcan-on-street-then-stole-it-was-dei-exec-worked-at-jpmorgan-chase/

She certainly looks like a substantial woman, but worried she might weigh on the P&L. That said, perhaps she would be a good “test” pilot on the first Mars flight.

(I appreciate your attempt to educate me regarding SpaceX being a profitable company overall. I would agree that cash flow is important, but note that any business can have a positive OPERATING cash flow if all or most of its costs are capital costs. I think this is what happened with a lot of Enron units after the McKinsey geniuses set up the various compensation schemes that ignored the capital cost for a new or acquired business (a manager could get rewarded for an investment whose ROI was way below the cost of capital and that meant Enron ended up bidding 2X the next highest bidder, for example, to buy a Brazilian utility). Consider a business that invests $100 billion in capital from equity and, as a result, is able to deliver a service to customers at no further cost. It receives $1/year in revenue from delivering the service. This is an example of a business that has a positive operating cash flow. The business would also have a GAAP profit (accounting profit) if whatever has been purchased with the $100 billion doesn’t depreciate, e.g., land. To say that this company “made a profit” for investors probably does not comport with the average person’s understanding of the phrase.)

Google AI: “Elektro Acquisition: Enron successfully outbid its competitors by $300 million to acquire control of Elektro in July 1998, expanding its reach into one of Brazil’s fastest-growing electricity markets”

Just to be clear:

1) I am not saying SpaceX is profitable now (it wasn’t in 2025 and is unlikely to be over the next couple years barring a change strategy related mostly to the investment in the AI business). My original point was refuting your comment that it had never been profitable (it was in 2024 by every measure as I’ve detailed).

2) It may also have negative operating cash flow for periods over the next few years as they spend heavily on the AI business (barring a change in strategy).

3) Could it be wildly profitable now and generate huge operating cash flows immediately and for a long time? Yes, obviously, if they were to shut down the AI business (competition in both Connectivity and Space has been literally blowing up-see Bezos’ recent launch)? The Connectivity and Space business would gush cash flow and would have limited capex requirements (particularly if/when Starship becomes renewable like Falcon, which is why the Space business was gushing even more cash until 2025, when Starship R&D depressed profitability).

4) Would shutting down the AI business now be the correct business decision? Unclear. The AI business and its future cash flows are the key material debate on the stock (not discussions of NOLs and other stuff that dominate online stock chat boards!).

5) One could have asked the same question that you seem hung up on years ago about the Space and Connectivity businesses, which were wildly unprofitable and cash flow negative for years. Would it have been a good business decision to shut them down 10 years ago and liquidate the assets for shareholders? Most anyone who reads the S-1 and looks at the businesses would say absolutely no.

I’m not “hung up” on SpaceX making huge investments now and hoping to reap big revenue/profits down the road. I actually do think it is a great company and agree with you that Blue Origin is underwhelming by comparison (the people I’ve talked to who really understand this say that Blue Origin has tried to make huge leaps all at once and, apparently, mostly failed whereas SpaceX has improved incrementally; also, speaking of huge leaps, I don’t know if there is an explanation for Mr. Bezos’s choice to marry a grandmother-age plastic surgery survivor).

But a great company isn’t necessarily a great investment and that’s really what I’m trying to understand, i.e., what can they do that will grow so big and so fast that the stock will outperform the S&P 500? I’d even settle for understanding what they can do that would enable the stock to perform as well as the S&P 500! I don’t question that this can happen. I just don’t understand the economics of AI data centers, for example, to figure out how.

Again, to be clear, I am not suggesting it will be a great investment. But, you now have all the pieces to analyze the situation just as well as anyone because everyone now has the same information (S-1)! You are 100% correct that a great company isn’t necessarily a great investment. If you want to gain an “understanding of what they can do…” take a look at the earnings/cash flow projections by the major banks (if not, just google them) as a starting point. You will see some wildly optimistic #s and you will see some wildly pessimistic #s for the out-years (5-10 years out). Take a look at those and the #s in the S-1 and do some simple math on the businesses (e.g. #s of launches etc.) and see if you agree/disagree. I think if you do some basic math you will see that if SpaceX even comes close the the higher #s some folks are projecting within their timeframe it will likely outperform the S&P 500 by a lot; conversely, if the lower projections are more realistic it will likely underperform.

Your comments on Blue Origin and Mr. Bezos seem spot on.

FR: Remember that my guess was that today’s market price is more or less the correct price.

“I’ll go first… because I believe in efficient markets, SpaceX in five years will be worth its IPO price plus 4% real return annually (about 21% over the IPO price). A narrow majority of the value will be from Starlink. (Note that this is like a probability expectation. I’m pretty sure that something dramatically good or dramatically bad will happen to SpaceX, but I can’t predict which is more likely and therefore my guess is right at the center. Analogous to the expected value of a coin flip game for $1 being $1 even though we know it will either be $0 or $2 and can’t be $1.)”

(right now the market price is slightly higher than the IPO price, of course, but that’s the “Elon superfan/IPO excitement bump”)

Saying the current price is the correct price doesn’t make me a bear/skeptic. I’m sure that you’re right about the big profits that would be made if SpaceX hugely increases the number of launches, but that just feeds into my question from https://philip.greenspun.com/blog/2026/06/11/i-am-buying-a-lot-of-spacex-stock-what-will-it-be-worth/ of what will be the payloads. I’m not saying that demand for these launches doesn’t exist. I’m saying only that I can’t figure out how space will be used. (I do think that I’m correct about the lack of commercial potential in Mars and likely correct about the comparative economics of space-based data centers vs. Arizona-based and, if so, it would be interesting to see if we can predict what will end up being the mass-market payload.)

I would have more faith in your comment about the “correct price” if you had said “I don’t know what the correct price is because I haven’t analyzed or looked at what the earnings and cash flows will be going forward.” That would be more realistic than the coin flip valuation. As I’ve tried to say, no one “knows” what the correct price is and that’s what makes markets. Educated folks have looked at the numbers and have developed a whole range of opinions. It’s third-grade math that is well within your abilities! Thankfully, SpaceX’s segment disclosure (in the S-1) is very good, which makes it simple to do back-of-the-envelope calculations quickly. As I referenced earlier, here are a couple of 2030 estimates from Goldman Sachs and Morgan Stanley (and yes, these were banks that have been paid by SpaceX as part of the deal…I am not endorsing them). Goldman: revenues $474b and ebitda $352m; Morgan Stanley: revenues $330b and ebitda $230m. They are likely optimistic that soon, but nevertheless if you play with the #s and compare them to the S&P 500, you will see that SPCX stock looks cheap relative to the index (if they are correct). That said, others disagree and have much more bearish #s.

FR: I continue to deny that anyone intelligent can read the S-1 and come up with an accurate prediction of a stock’s future price. Morningstar can read an S-1 as well or better than anyone. They came up with a value of $63 per share after reviewing the S-1 and all other published material (see https://www.morningstar.com/stocks/why-we-think-spacex-ipo-is-overvalued , which was published about three weeks after the S-1).

I heretically deny that EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is meaningful. Consider a company that borrowed $1 billion at 6% to fund a business that generated $1 million/year in profit. They’d have an EBITDA of $1 million despite a real-world loss of at least $60 million (if whatever they bought for $1 billion was depreciating then the real-world loss would be higher).

Four thoughts:

1) Has the Morningstar analyst (Nicolas Owens) had any success forecasting financials?

2) I looked at Nicolas’ stock-picking over the past 3 years. He generated negative alpha of 17.1% in in the ~20 names he covers in his aerospace and defense specialty area. I don’t have a PhD like you, so help me with my math: is that “as well or better” than anyone else?

3) Please heretically use your preferred financial measure (not ebitda) and report back!

4) Loop Nicolas into the conversation when you’ve heretically analyzed SpaceX (it looks like he needs help!).

FR: Negative alpha is common among Wall Street pros (more than half?), but I think it supports my point that careful reading of publicly available and company-released data, including the S-1, isn’t a reliable means toward successful prophecy (predicting future stock prices). https://www.morningstar.com/people/nicolas-owens gives a biography: “Before joining Morningstar in 2002 as an equity analyst, … Owens holds a bachelor’s degree in politics from Princeton University. He also holds a Master of Business Administration in finance and strategic management from the University of Chicago Booth School of Business.” He’s been reading S-1s for at least 24 years. He has an appropriate credential from a Queers for Palestine institution (see https://chicago.suntimes.com/israel-hamas-war/2024/04/29/university-of-chicago-protest-camp-palestine-israel-hamas ). I know some bond investors who’ve made money reading the fine print, e.g., learning that a bond that seems risky is actually secured by some asset/mechanism that others overlooked. I also know some short investors who’ve made money reading the fine print, e.g., by discovering a vulnerability. But the long equity investors I know who’ve outperformed did it with bets regarding products and markets.

To your question about EBITDA, my preferred metrics for corporate health are (1) accounting profit averaged over the past three years (eliminates most of the gimmicks, such as treating expenses as capital (see WorldCom)), and (2) return on invested capital (ROIC; https://www.morganstanley.com/im/publication/insights/articles/article_returnoninvestedcapital.pdf ). NVIDIA has an off-the-charts ROIC right now of 91%. Microsoft is at 21%, just above the S&P 500 average (ignoring banks). SpaceX has a negative ROIC, which is another way of saying that they’ve yet to “make a profit”.

But I don’t think the above metrics are relevant to the SpaceX stock price. Regardless of the current numbers, the company will be worth a lot if either (a) it becomes a key component of the AI boom, or (b) there is a vast amount of payload that makes sense to launch into space (maybe Elon is correct about data centers in space; maybe one of our intelligent readers can predict what will instead be the economically valuable use of orbit).

I think you’re providing a great example of the limits of reading the S-1 and similar documents. You say that you’ve read the S-1 more carefully than I have. But you haven’t been able to provide a guess as to SpaceX’s future valuation (see the comments in https://philip.greenspun.com/blog/2026/06/11/i-am-buying-a-lot-of-spacex-stock-what-will-it-be-worth/ ). Because you can’t estimate the future value of the stock, despite your careful perusal of the S-1, you have no rational basis for buying it or selling it at any price.

On our friend and analyst Nicolas, his abysmal stock picking actually supports the argument that he’s “so bad, he’s good”; if you shorted his buys and purchased his shorts you would handily outperform the index. If he had just flipped coins on every recommendation (as you earlier suggested was one of your methodologies), he would have matched the index (plus or minus, excluding fees and transaction costs). So, it actually suggests he is a “reliable means toward successful prophecy (predicting future stock prices).” Which suggests one should purchase SpaceX stock.

Your ROIC arguments aren’t persuasive for the same reason I noted earlier (though you seem to want it both ways, disclaiming the relevance to SpaceX): a stock represents the future cash flows generated by the business, so focusing on recent ROIC over future cash flows will lead you into stock picking purgatory (with Nicolas).

Your last comment (“regardless of the current numbers…) makes total sense and I think summarizes the future for SpaceX stock perfectly!

Missed your last paragraph (“I think you’re providing…”). To be clear, I have no idea how carefully you’ve read the S-1, but some of your commentary suggests you haven’t really looked carefully at all the moving pieces (and, yes it is a pretty complicated company). I have done some careful analysis of the future financials, but I don’t offer investment advice. I will say that the super bullish #s seem too optimistic and the super bearish #s seem too low (but most of the analysts who will cover the stock haven’t published detailed financials yet; this will happen in a few weeks, which will be interesting). Also, as I said earlier, no person (even Nicolas!) will perfectly forecast SpaceX financials in coming years, but a common approach is to do upside/downside scenarios and to weight them using one’s judgement based on experience to arrive a some sort of reasonable midpoint. Or, in lieu of this approach, just go with the inverse Nicolas approach to stock picking.

> This is not to say that American in the 1950s was better overall, of course. […]

A good way to compare the two times is average the lifespan and the improvements that contribute to its increase. Means of amusement and luxury don’t increase lifespan. Advances in medical science and knowledge do.

NA: Life expectancy cannot be the correct measure of quality if life because women live 5-6 years longer than men and we are informed that women are unfortunate victims and, therefore, entitled to positive discrimination in jobs, government contracting, Social Security internal rate of return, etc. as a class.

philg: Yeah, they live longer, have more IQ compared to men on an average, have more chances of surviving at birth, etc., and men instead of learning from them how to survive longer and other strategies think that they need support! How patriarchal is that, OMG!

It was also more attainable for women to support the entire household in the 1950’s. Watched all the neighbor’s houses in Calif* go from $600k to $3M in the last 26 years & the owners all get replaced by Indians. None of the housing stock built in the last 26 years went to anyone here 26 years ago.

Yet again not a single post goes by without another tirage against no-fault divorce. The biggest damner of your argument is that despite writing a book on the subject and attending conferences, you still ended up marrying someone and she didn’t divorce you. The divorce rate is where it was, apart from a small bump in the 1970s when divorce laws first legalized. Acoustic separation or the belief that marriage is sacrosanct still keeps Americans together. I just don’t understand your arguments.

Anecdotally the only guy I know who got properly screwed was my black maintenance man. That was arguably because he kept throwing aside the court notices and didn’t even get free ChatGPT to take a glance at the papers his crazy ex girlfriend was serving him. I brought up the concept of selling an abortion to an acquaintance moving to LA and she was disgusted by the prospect. She is some kind of practising Christian though.

Why don’t you just stop dooming on marriage sometimes. Women want to get married, settled down, and stay in committed relationships. Most of the time it’s them looking for a ring not guys. The law today has shifted on the concept. If two people don’t want to stay married then how can society force them to stay married? Besides, the religious folk have the religious church/mosque aspect left for them. For them they still take marriage seriously and it’s difficult to dissolve one.

I just don’t get your points

Just adding on. Everybody I talk to is still doing well in America. Frankly even better than before. My barber only works four days a week so she can spend three days a week with her kid. And that’s only with trade school. I’ve gone to the laundromat to see how my hermanos live, it’s not how people live in cage apartments in Hong Kong that’s for sure. No matter how ugly I have been, I have been able to find someone to date. And the occasional bipolar woman will come and find me every one and a half years. The GDP keeps going up, it’s a great country what’s wrong?

@Anonymous Phil wants to go back to a late 1800s society where men were always doing the right things for women. Infact, it was so great that women never needed many rights. Divorce is not needed as women were so happy as men used to take care everything for them.

AA: the original post is about the 1950s vs. today, not the late 1800s. I don’t think that the term “rat race” had come into currency in the 19th century. There wasn’t a lot of white collar work. There weren’t home appliances. Everyone expected to toil in the late 1800s.

Perhaps more importantly, the original post is about the experience of “men”, a term that was well-defined in the 1950s. You seem to be suggesting that the 2020s are better for “women”, a term that in the 1950s was also well-defined and that was disjoint with “men”. This suggestion, if true, does not contradict anything said in the original post. In fact, the original post supports this suggestion by noting that “women” have been getting preference in hiring and government contracting during the intervening decades (“DEI”), despite the fact that this preference would seem to be unconstitutional (14th Amendment’s Equal Protection clause) and despite the fact that the people who implement DEI programs are generally unable to define “women”.

Separately, though it wasn’t part of the original post… the absence of no-fault (unilateral) divorce in the 1950s was not the absence of divorce. A woman who wanted to get rid of her husband for cause was able to do it in a 1950s family court. A woman who wanted to get rid of her husband without cause/fault could also do it, but she’d have to negotiate a split with him. A non-working wife couldn’t go to court unilaterally and expect to continue her marital lifestyle at his expense without his consent, which became the no-fault standard. If she wanted to marry someone else in 1955, for example, she could negotiate a split in which she transitioned from being supported by her current husband to being supported by her new husband. Absent an extremely understanding husband, what was not available was for a wife to choose one or more new sex partners and be financially supported by the discarded husband.

A man who got called away to war was still at some risk. As described in https://philip.greenspun.com/blog/2016/06/23/hogans-heroes-turns-out-to-be-reasonably-accurate/ , women who stayed in the U.S. while their husbands were flying B-17s over Germany during WWII could and did have sex with neighbors/new friends and produce children from those sex acts. Example letter received by a B-17 crewmember while imprisoned by the Germans after being shot down: “Dear Harry, I hope you are broad-minded. I just had a baby. He is such a jolly fellow. He is sending you some cigarettes.”

A high-profile example of pre-no-fault divorce: https://en.wikipedia.org/wiki/Carole_Lombard (1933)

https://archive.is/2TLQH is a New Yorker article from 1933 in which Mary Pickford and Douglas Fairbanks were divorced, presumably by agreement, on the extremely flimsy ground that one of them liked to travel more than the other. “Mary herself made a perfectly clear statement: she said she and her husband were no longer happy.”

Note that the original post doesn’t say that no-fault divorce is good or bad in some universal sense or for people of all current gender IDs (74 at last count). The post is specifically about men and the level of pressure and competition to which they are subject (a lack of security in career or marriage is another form of pressure). The availability of profitable unilateral divorce to the wife reduces a white collar man’s security and increases the pressure on him to success and get ahead of other men (lest the wife change horses, so to speak, mid-stream). If you were to say “But the value of no-fault divorce to women is even greater than the cost to men” that wouldn’t be a contradiction of the original post, which never says anything about the value to women of no-fault divorce.