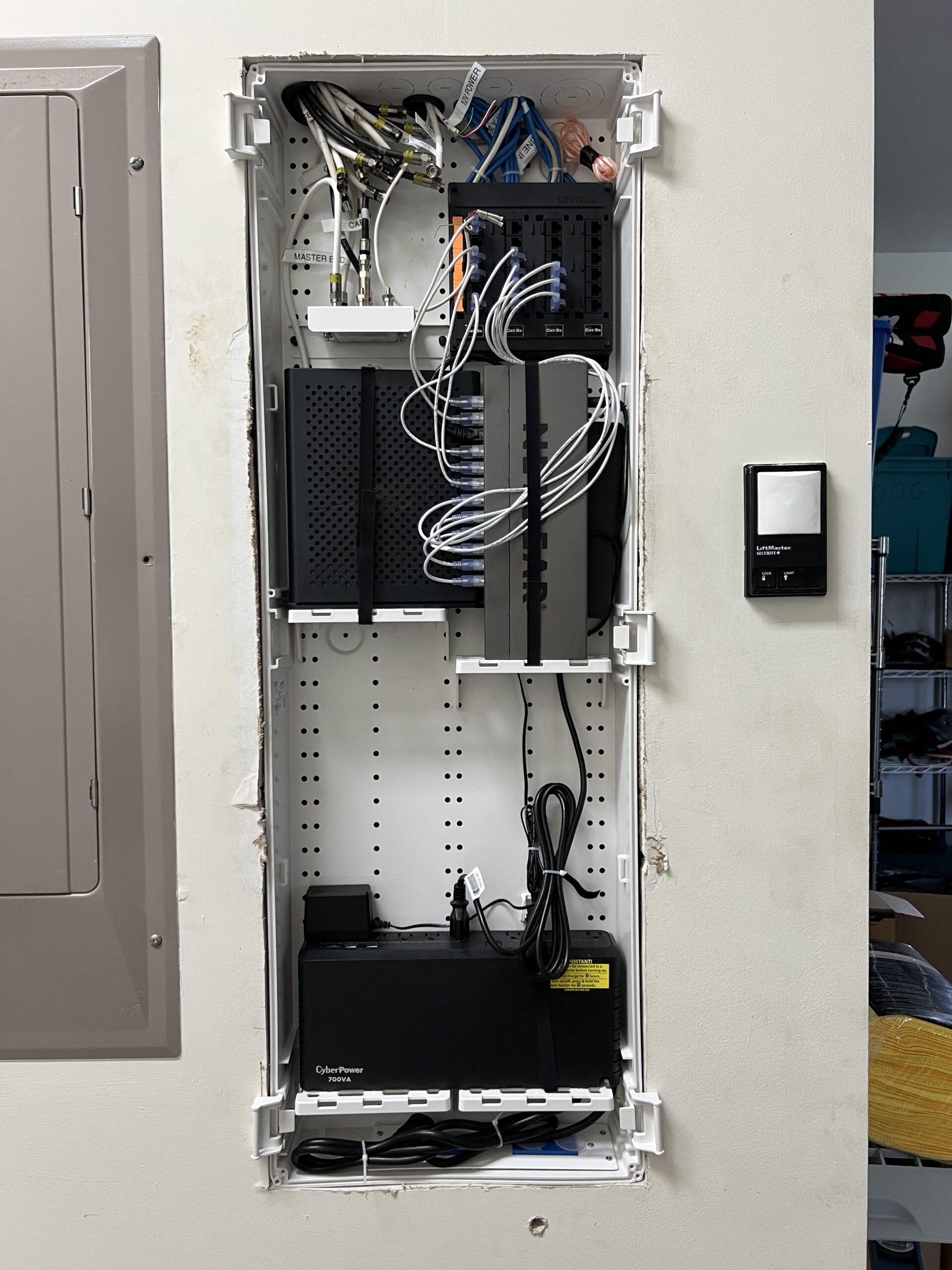

Even an antique house like ours (2003) here in Florida comes with an A/V cabinet (example from Leviton), the natural home of routers, switches, etc. because this is where all of the Cat 5 cables (Cat 5e in our case; Cat 6, obviously, for newer houses (6A is stiffer and maybe builders wouldn’t want to use it?)) to wall plates end. The Florida Power & Light grid has amazing uptime, but our epic afternoon thunderstorms do cause 1-2-second power hiccups. That’s enough time to force a 5-minute reboot of our cable modem (still in an Xfinity coax ghetto here). Having failed to find what I expected to be a wallet-sized lithium-ion-based UPS, I set the cabinet up initially with a CyberPower lead-acid-based uninterruptible power supply (UPS) of absurd weight and capacity given the use case:

The CyberPower began to shut down randomly, despite the low load. Replacing the battery didn’t help. CyberPower did not want to offer a warranty replacement. Another summer arrived and we had a couple of power glitches. I found that Liebert, the storied manufacturer of machine room AC, introduced the Vertiv PUL-350LVT back in May 2026. This costs about $142 at Amazon and can handle 210W, which seemed potentially insufficient given that the Netgear GS116PP PoE switch by itself can supply 183W of output. Due to the lack of a lead-acid battery, the weight is just over 3 lbs. I used a Tapo P110M smart plug to see what the total draw from the cabinet was (cable modem, Omada router, Netgear PoE swtich) and it turned out to be just 72W steady-state (I rebooted most of the Omada access points at the same time and power consumption did not spike). The UPS will keep our home on the Internet for over 10 minutes, therefore, in the event of a serious FPL problem.

Tangent Alert! Maybe we should buy Vertiv stock? No matter who wins the AI and data center wars, Vertiv/Liebert will have to be paid! They’re like Levi’s for gold miners, right down to the 2SLGBTQQIA+ passion:

Why is there “work we need to do to improve”? If Vertiv/Liebert pays employees what they’re worth, what would be an improvement? (paying some employees more than they’re worth?) If Vertiv/Liebert does not pay employees what they’re worth, what stops them from adjusting pay right now?

But I digress…

Returning to the question of lithium-ion to sit behind the small boxes that are critical to home happiness…. so far it works! (I bought it at Amazon, set it up in a few minutes, and simulated a brief outage by unplugging it a day after the install.) The only unknown unknown unknown is what happens if there is a 20-minute outage, the batteries die completely, and then power is restored. Will this thing turn itself back on? When initially plugged into the mains, it did not come on without me pressing and holding the button.

What would be nice to have? How about a small light lithium-ion UPS for a desktop PC with a standard 750-1000W power supply? Instead of the lead-acid monsters designed for max runtime, this would have enough battery for only a 1-minute outage and then a 2-minute orderly shutdown if the outage persisted. Let’s assume kind of a worst-case draw of 1000 watts for all three minutes, which is essentially impossible (GPU-intensive processes would be shut down shortly after the first minute). This could be accomplished with a 12.8 V 10 Ah LiFePO₄ battery, I think, that weighs only 2.7 lbs. and costs $60. It’s about 6x3x4″ in size, though, so my dream of having the UPS built into the PC power supply might not be achievable. (On the third hand, maybe the dream IS achievable. The power supply can have a small LiFePO₄ battery. If mains power dies, the power supply can pull power from the GPU after 5 seconds in order to give the motherboard/CPU/any hard drives another 55 seconds and, then, if the grid is still dark, sufficient time for an orderly shutdown. Maybe the unexpected disappearance of the GPU would cause an LLM or video game to crash, but that’s unlikely to leave any files corrupted.)

The Trump administration has sent the U.S. military to Venezuela (“hundreds of personnel, two warships, fixed and rotary-winged aircraft, and search and rescue teams”), which will, I hope, help with immediate problems. But what about supporting long-term rebuilding of this frenemy? My preferred method for helping afflicted foreign countries is to boost their economies by buying their exports (see Japan Relief: Idea #1 (buy a knife), for example).

What can we buy from Venezuela in the coming months that we wouldn’t have otherwise purchased? ChatGPT says that Venezuelan coffee is “potentially very good, but uneven and hard to find” (old/popular brand available on Amazon), that chocolate made in Venezuela can be good. Franceschi Chocolate, Chocolates El Rey, and Savoy are the recommended brands. Of these, I found only Savoy at Amazon. ChatGPT apparently wants humans to be too drunk to resist its takeover of the planet and consequently recommends rum: Diplomático, Santa Teresa, Pampero, Cacique. Venezuelan seafood is apparently a big export, but tough to find as a consumer.

Since we live in a Latinx-rich environment, I am going to visit some of the local “Hispanic” supermarkets and see what I can find before hoping and praying for chocolate to make it through the mail in summer heat.

My first order… (U.S.-roasted because ChatGPT says that nationalization and state control hasn’t worked out well for the quality of the two big Venezuelan coffee companies, though of course Mamdani-run state enterprises will do better!)

Purchase #2, at Jupiter’s Latinx supermarket (Tapatia):

Note that the above shows 100 percent of the Venezuela-made items available in the store, according to the staff. They had a lot of stuff from Mexico, some from Central America, and not even coffee from Venezuela.

The 11-year-old high-end Carrier system at our old Harvard Square place failed in the hot summer of 2024. It was probably some sort of leak in the outdoor unit, but it was tough to say for sure. In Florida, this would have been repaired for about $6,000 via installation of a new outdoor unit and recharge. In Maskachusetts I got estimates from $24,000 to around $40,000 to replace both air handler and the outdoor unit. (This might have been a $12,000 project in Florida for top-of-the-line variable-speed gear.)

The company that quoted $24,000 was rated 4.9 stars in Google Maps. They’re an authorized Carrier dealer. They said that they needed to do $thousands in additional items in order to satisfy the building inspector. My suggestion that a building permit wasn’t needed because they were just replacing existing equipment was laughed off. They ran new coolant lines and, despite me begging them not to, decided to monkey with the hydroair system that sends hot water up from a basement gas-fired boiler into the attic where the air handler lives. Because the attic is technically unconditioned space, even though it never gets very cold (poor insulation in the old wooden house underneath allows heat to rise), the circulating water must have some antifreeze in it.

When the winter arrived, the hydroair system didn’t work. The only heating was from the heat pump, ruinously expensive at some of the nation’s highest electric rates. The company came back and said that we needed about $10,000 of work. The circulation pump was failed, which is why fluid wasn’t circulating. The boiler was from 2003 and should be trashed. At a minimum, everything attached to the boiler needed to be replaced. I called the plumber who’d installed the boiler. He came by and said “Your HVAC people are idiots. They filled the pipes with 100% glycol, which is too viscous for the pump to move. I drained it and refilled it with 50% glycol like it is supposed to be and everything works fine now. Your boiler doesn’t need any service and is working perfectly.” He sent me a $1300 bill (would have been $500 in Florida, but this guy is kind of a genius and Massachusetts is truly a paradise for anyone competent in the trades).

It’s finally time to sell the old unit. The market for short-term rentals in Cambridge never recovered to its 2019 level. I was never going there except to fix stuff. The family wasn’t interested in spending time in Maskachusetts. What did the lawyers working on the closing find? The HVAC company never closed the building permit that they pulled in 2024 and for which they said that thousands of dollars of extra work were required. (Ultimately, it did get closed, but not without multiple follow-up emails and calls from me. The HVAC company called the inspector and he actually did come by within a week, but he marked it as a “rough inspection”. The permit wasn’t closed and the HVAC company never checked to see if it was closed.)

(Note that the cost to heat and cool this 1400 sqft. condo, thanks to high utility rates in Massachusetts and low quality construction, is actually higher than the cost to heat (one week per year!) and cool (to 72 degrees; no Jimmy Carter austerity here) our 5400 sqft. house in Palm Beach County.)

Loosely related… this lamppost sticker from Harvard Square would make a good tagline for an HVAC business:

Also, a friend’s daughter got into a summer math program at Boston University. She is required to live in a BU dorm as part of this program. Faculty, staff, and students at BU are such experts on Climate Change that there are 31 pages of results from Google when searching for this string on the BU site:

How did the climate change experts prepare their own campus for the brutal heatwaves that are now hitting Boston regularly? (example) They failed to install air conditioning in their dorms.

Happy Middle of Hurricane Preparedness Week for those who celebrate…

Conventional insurance companies such as State Farm have mostly walked away from insuring coastal South Florida due to a combination of litigation risk (“Prior to the reforms, Florida accounted for more than 72% of the nation’s homeowners claim-related litigation in 2023, despite representing only 10% of US homeowners claims.”) and hurricane risk. Our house is about 2.5 miles from the ocean, but it is still redlined by the insurance companies most people have heard of. Here are the options for insurance:

a Florida-only carrier that turns most of its premium over to reinsurance

a “non-admitted” specialty company that isn’t regulated by the state and that may have unfavorable terms, including penalties for early cancellation and even a “wind exclusion” (i.e., they pay nothing in the event of the most obvious risk: hurricanes). (This option is so expensive and dumb that I won’t cover it here.)

a “high-net-worth” (HNW) carrier such as Chubb (mostly rejects additional Florida risk; famous for a low loss ratio (payments as a percentage of premium collected)), Vault, PURE, and Berkley One (despite the name, these are available to peasants whose house is worth less than a Palm Beach starter home ($10 million))

The cost of HNW insurance is 2-4X what a Florida-only company might quote.

Nearly all Florida insurance includes at least a 2% wind exclusion. If the dwelling value is $1 million, in other words, the homeowner pays the first $20,000 of any hurricane-related loss. Thus, the vast majority of customers with hurricane damage will receive nothing from their insurer because the typical hurricane damage might involve only some blown-off roof tiles or shingles. The band of likely serious damage from a Category 4 or 5 hurricane making landfall is 20-60 miles, e.g., for Hurricane Andrew in 1992 that resulted in major changes to the Florida building code or Hurricane Michael in 2018 that damaged Tyndall Air Force Base. Note that this exclusion results in the HNW policies paying less after what would be typical hurricane damage because HNW companies write for 2X the dwelling value on the same house.

The Florida-only carriers are typically unrated by AM Best, the standard rater for insurers. It has been historically rare for an insurer rated A or better by AM Best to fail. Florida insurers get rated by Demotech. How well does it work for an insurance company to have all of its customers in Florida? According to ChatGPT, nearly all of the Florida-only companies that have gone insolvent had A ratings from Demotech (i.e., the ratings were worthless in terms of distinguishing the vulnerable carriers from the solid ones or, perhaps, the solvency of a carrier simply depended on their luck regarding how many customers were in a hurricane destruction zone).

Insolvency after a major hurricane doesn’t work the way that one would think, with the failed insurance company realizing that it is doomed to failure and going into a bankruptcy-style process where every claimant gets paid a percentage of his or her full claim amount. Instead, the insurance company, even after a major hurricane, pays claims as they’re made and adjusted at 100%. When the company runs out of money they turn out the rest of the claims to the Florida Insurance Guaranty Association (FIGA), which will pay up to $500,000 for a destroyed house. So… the customer with a major loss either gets 100% or a fixed $500,000. The more complex the claim, the less likely it is to be paid. ChatGPT says that it is reasonable to assume a 10 percent chance of insolvency for a Florida-only carrier in the event of a major hurricane. The most recent insolvency that triggered a FIGA payout was of United Property & Casualty Insurance Company in February 2023. That’s three hurricane seasons ago. Since then we’ve had some hurricanes, but none anywhere near as costly within Florida as 2022’s Hurricane Ian. Let’s use a 20 percent risk of insolvency if a house is damaged to policy limits and a 10 percent risk of insolvency if a house is damaged to half of the limits.

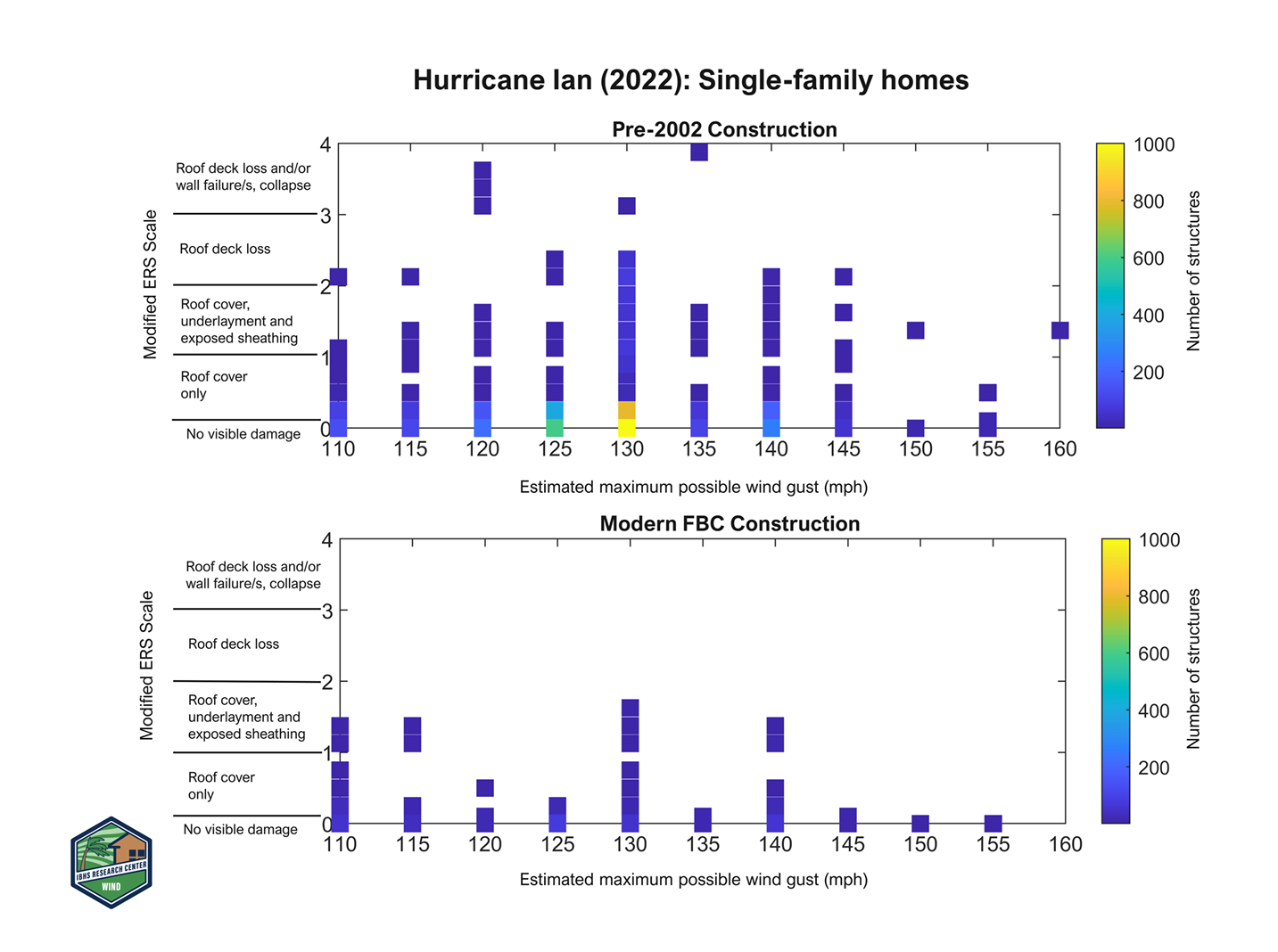

What is the risk of a total loss or serious damage? Gemini starts off by saying that it is pretty high, with 300,000-400,000 single-family homes in South Florida either substantially damaged or destroyed by hurricanes over the past 50 years. That’s out of about 2.7 million homes in South Florida today, but only an average of 1.7 million homes over the 50-year period. (ChatGPT estimates this number as only about half of Gemini’s figure; our future AI overlords are smarter than humans, but equally inconsistent?) So a homeowner’s insurance company has about at least a 1 in 7 chance of making a big payout? Not exactly. First, we have to separate out the houses that were damaged by flooding or storm surge, between 120,000 and 180,000. Homeowner’s doesn’t pay for flood damage. Now we’re down to a risk of about 1 in 10 over 50 years. What about the fact that Florida established a strict statewide building code in 2002, hoping to avoid a repeat of the Hurricane Andrew aftermath, roughly 25,524 homes destroyed and 101,241 damaged (Insurance Information Institute). Gemini:

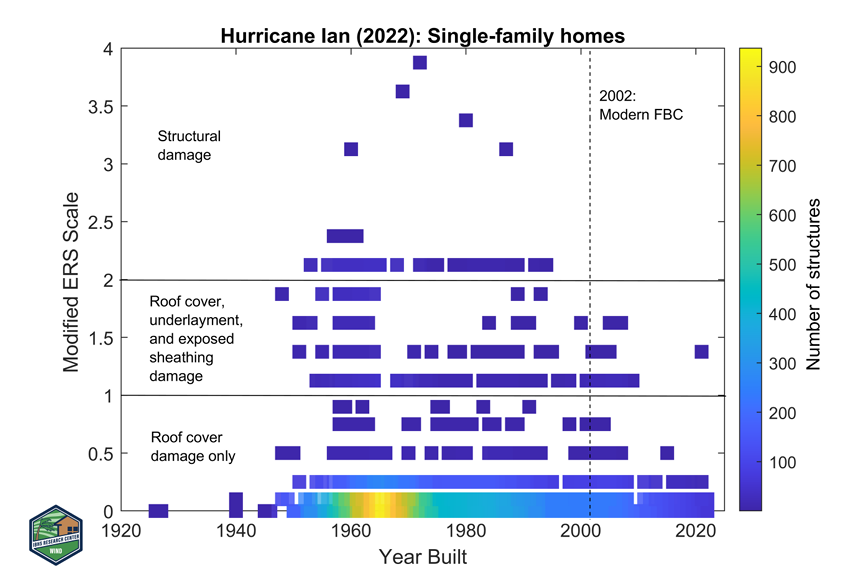

In major storms like Hurricane Michael (2018) and Hurricane Ian (2022), structural engineers found that homes built to the 2002 code (or later) suffered roughly 80% to 90% less wind damage than their older neighbors.

IBHS evaluated 3,646 single-family homes, 327 light commercial buildings, and 230 multifamily structures [after Hurricane Ian] using aerial and street-level imagery. … Homes built before 2002 had structural damage levels nearly 2x higher, and 2.3x higher in areas with peak winds above 130 mph.

It looks as though no post-2002 house actually lost the plywood sheathing supporting the roof, but at least some had exposed sheathing and, presumably, water damage as a result. A companion report from the same organization says that asphalt shingles were the weak point, metal roofs were the best (12% damaged), and tile roofs weren’t significantly damaged except those more than 20 years old (“no tile roofs assessed that had greater than 50% roof cover damage” and “the small number of roofs with greater than 25% cover damage … These roofs were all 20 years or older”). Our 2003 house has a one-year-old tile roof with two layers of “peel and stick” underneath. If the tiles are blown off, but the peel-and-stick underlayment survives then we’re looking at a $120,000 insurance claim to put a new tile roof on the house (maybe less if the underlayment isn’t too old and can be retained).

ChatGPT says that 4-6 Cat 4/5 hurricanes hit the Miami-to-Stuart coastline every 100 years. Let’s take this distance as 108 miles. If you assume that the zone of total destruction is 20 miles wide then a typical house gets destroyed roughly every 110 years. If the destruction zone widens to 40 miles, the interval between destruction is 55 years. The most recent major hurricane to hit Palm Beach County was in 1949, 77 years ago, but we could use the 55-year estimate to make the high-net-worth companies look more attractive.

[We’ll ignore tornado risk. A tornado could destroy or seriously damage a house, of course, but it wouldn’t affect an insurer’s solvency because a tornado is local. This is a 1 in 100,000-year event for a typical South Florida house, according to AI.]

As noted above, one quirk of the HNW policies is that they force buyers to pay to insure the full rebuild cost of a house, which for a 2003 house like ours is much more than the house is worth. Imagine if we insured our five-year-old Honda Odyssey for the cost of a brand new Honda Odyssey. Why would we want to do that when what is actually at risk is only about half that number? A neighbor has Chubb and they would pay him over $4 million for the house and contents in the event of a total loss (maybe $5 million if we add “loss of use”). His house has a Zestimate of $1.8 million, has its original roof and non-impact windows, and sits on a lot that should be worth at least $500,000 if the house were razed. The contents of the house aren’t valuable. So he has perhaps $1.5 million that could conceivably be lost under his $4+ million policy. (Note that the neighbor won’t get the high dwelling value unless he actually does rebuild, an irrational choice to make compared to simply moving to a similar house and letting a professional real estate developer deal with the wreck. If the family moves to a $1.8 million house a few blocks away, he gets paid only about $1.3 million (the depreciated value of the structure).

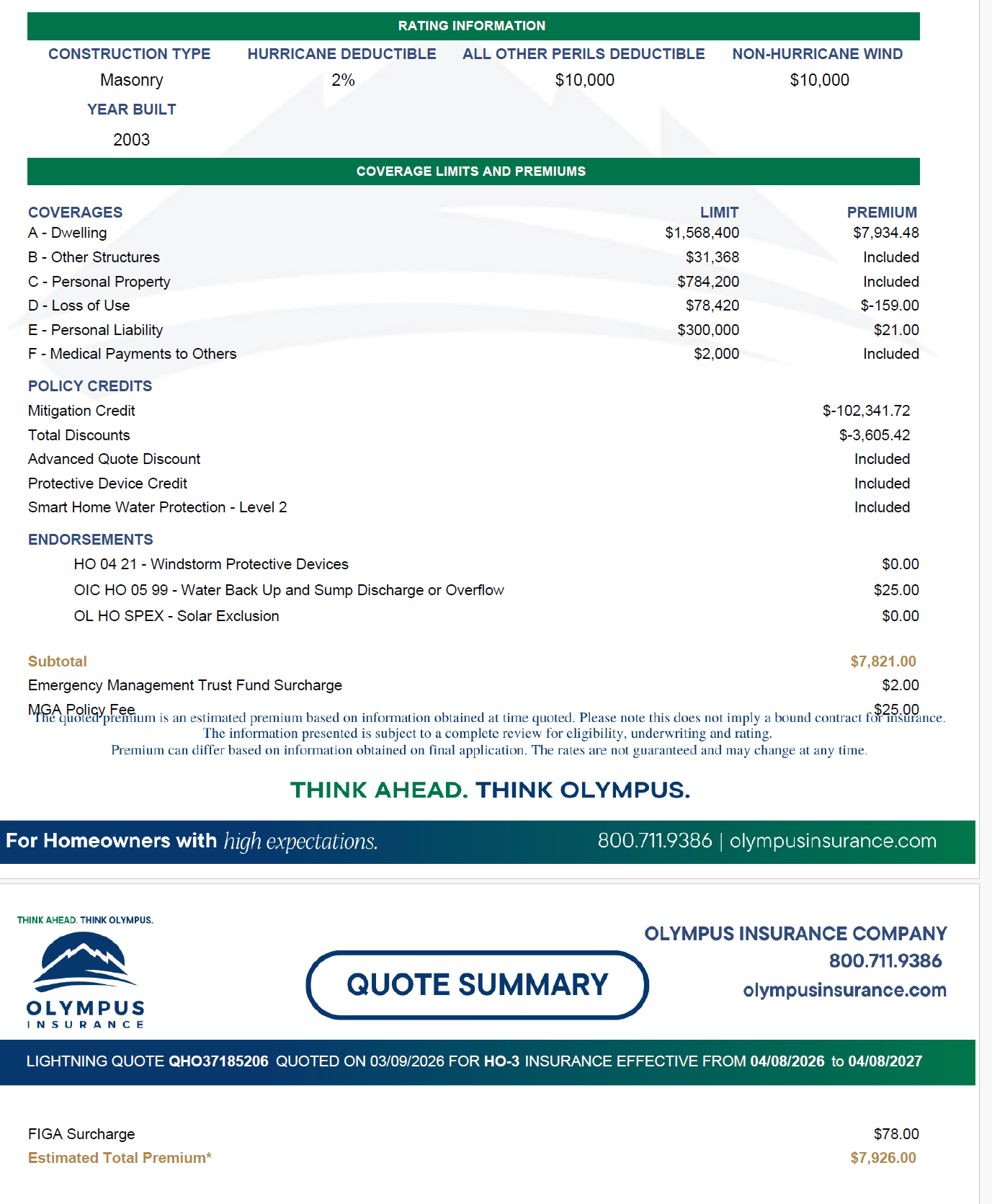

Let’s have a look at a couple of quotes. Below is one from Olympus, a Florida-based company that was founded in 2007, i.e., 19 years ago. Whoever started the company should buy lottery tickets because it was founded right at the beginning the 2006-2015 “no hurricanes making landfall” period. That said, the company has survived the following hurricanes that did make landfall in Florida:

Hermine (2016)

Irma (2017)

Michael (2018)

Ian (2022)

Idalia (2023)

Helene (2024)

Milton (2024)

Furthermore, Olympus is unusual in being rated by KBRA, which is significantly more stringent than Demotech. Olympus is rated BBB+ by KBRA (over the minimum BBB accepted by Fannie Mae; it’s ironic that the enterprise that generated the largest insolvency in U.S. history, requiring $150+ billion in tax dollars as a bailout, closely scrutinizes insurance companies). For the handful of companies that are rated by both KBRA and AM Best, the ratings seem to be similar.

Could they survive a repeat of the 1949 hurricane that came right into Jupiter? (the most recent major hurricane to make landfall in Palm Beach County) There doesn’t seem to be any way to find out. An insurance company with 50,000 customers, each of which is on its own square mile within the 53,625-square-mile state of Florida is going to be much less stressed by a hurricane that hits Fort Lauderdale than one whose 50,000 customers are all in Broward County, for example. (Broward County was last hit by a major hurricane in 1947, though Hurricane Wilma, Category 2, did about $4 billion in insured damage in 2005.) The information on risk concentration by company is nowhere to be found. In theory, the reinsurers who agree to do business with the companies are looking at this and maybe the regulators.

It is difficult to have faith in regulation when one hears about Florida-based Slide Insurance. The founder and his wife siphoned off $50 million in compensation out of a total profit of $288 million in 2023-4 (source). Based on this, it seems that an insurance company could pay out all of its profits to employees and shareholders during 15 lucky years without major hurricanes affecting its territory and then fold up its tent after a Hurricane Andrew-type event occurs. ChatGPT: “There’s no strict statutory cap tying executive pay to solvency. … As long as they stay above minimum surplus requirements, they’re compliant. But those minimums may not cover a true tail event (e.g., Andrew-scale).” People with inexpensive-by-Florida-standards houses will still do okay with $500,000 from FIGA, of course, so this is a great example of privatized profits and socialized losses.

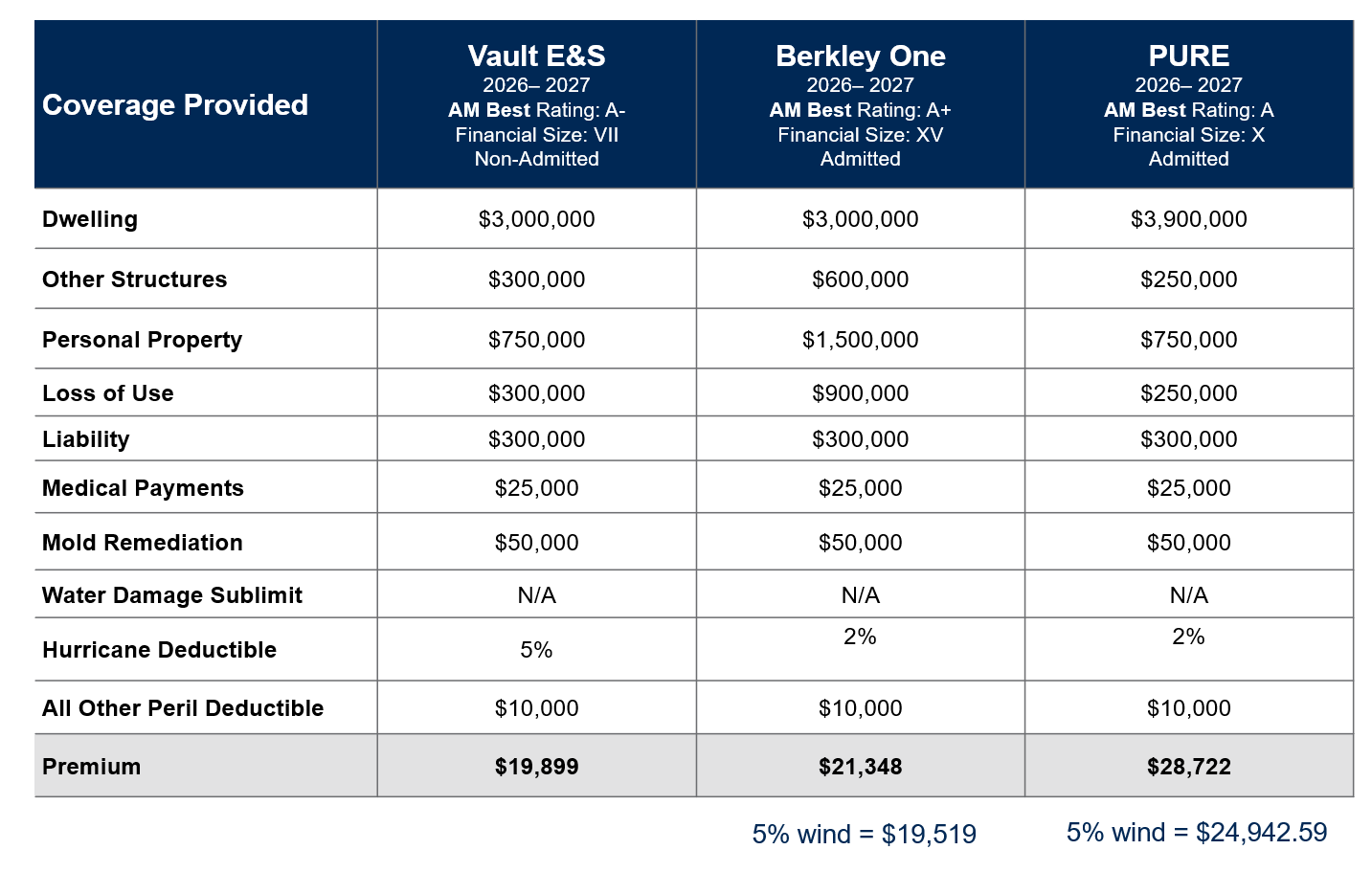

What did the high-net-worth companies have to offer?

Notice the PURE quote with a 5% wind exclusion. If our roof were destroyed, but didn’t leak, and we lost 7 or 8 of our impact glass windows they would still pay nothing because the wind deductible would be $195,000. In a “medium bad” event, the Olympus policy at less than one third the cost could easily pay 2X because of the deductible being only 2% of a much lower dwelling value.

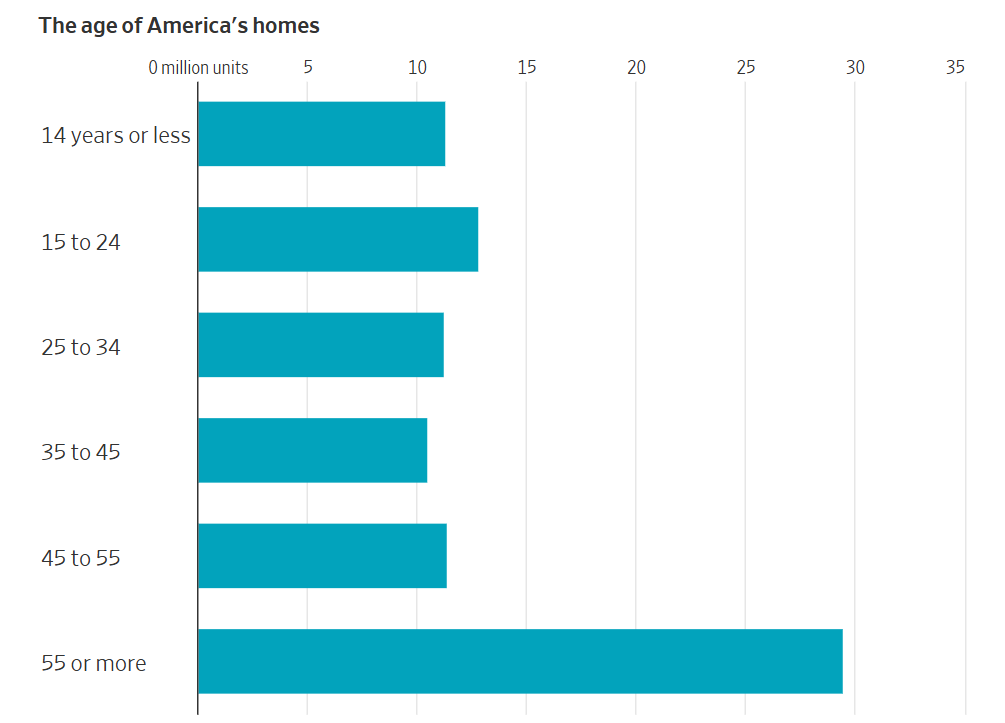

More recent new construction hasn’t replaced America’s graying housing stock, meaning the age of the median home is a record 44 years, according to the Harvard Joint Center for Housing Studies.

The cost of home maintenance, even after accounting for broader inflation, has jumped. Structural repair costs grew by about 14.1% in real terms between 2022 and 2024, according to the Federal Reserve Bank of Philadelphia. Plumbing jumped by 23.6%. The increase reflects the rising cost of individual parts and labor, and the larger size of necessary repairs.

This is on top of the rising costs of home insurance, property taxes and homeowners association dues, which are making it prohibitive for many to simply own a home, not to mention buy one.

The newspaper says “it [is] prohibitive for many to simply own a home, not to mention buy one” and at the same time tells us that the U.S. should have increased immigration, i.e., more demand for a relatively fixed supply of houses.

Our shabby/old house by Palm Beach County standards is 23 years old and that puts us in the top 25 percent of home youth:

Getting close to my 4% number:

Financial advisers traditionally suggested setting aside 1% of a home’s value annually for upkeep, but many now argue that isn’t enough. While 1% may cover routine upkeep, 2% to 3% provides a more realistic cushion for expected maintenance, home-improvement projects and unexpected repairs, particularly for older homes, said Angie Hicks, co-founder of home-services company Angi.

The Americans who were most eager to lock themselves into their homes during coronapanic will now bear a heavy burden:

Forty-nine percent of all improvement spending is now for necessary replacements like HVAC that owners can’t delay, said Rachel Drew, director of Harvard’s Remodeling Futures Program. The financial burden is particularly heavy in regions like the Northeast, where homes tend to be older.

Speaking of old, the article highlights the inability of folks in the Northeast to adapt to changed circumstances:

Mindy and Joseph Mevorah own an 88-year-old colonial [“more than 3,500-square-foot”] in Sands Point, a New York City suburb with plenty of old homes that is often considered an inspiration for “The Great Gatsby.” The house is due for a new coat of paint, a task they know to approach with caution. … “A new brick next to an old brick would look terrible,” said Joseph, 66. … The Mevorahs have stayed in their home for 29 years … They have a pool that could be a draw for future grandchildren. … When replacing their copper gutters a few years ago, they considered switching to aluminum, which would have been cheaper, but ultimately stuck with copper to preserve the home’s integrity. After all, they expect to be there for many years to come.

A 66-year-old in Florida whose kids were grown wouldn’t stay in a 3,500-square-foot wreck of a house. The Floridian would recognize that different kinds of real estate are suitable for different phases of life and likely move to a condo or small new house.

Circling back to the immigration theme… how can end-of-career financially comfortable Americans who struggle to afford house maintenance imagine that the U.S. can afford to house tens of millions of additional welfare-dependent low-skill immigrants?

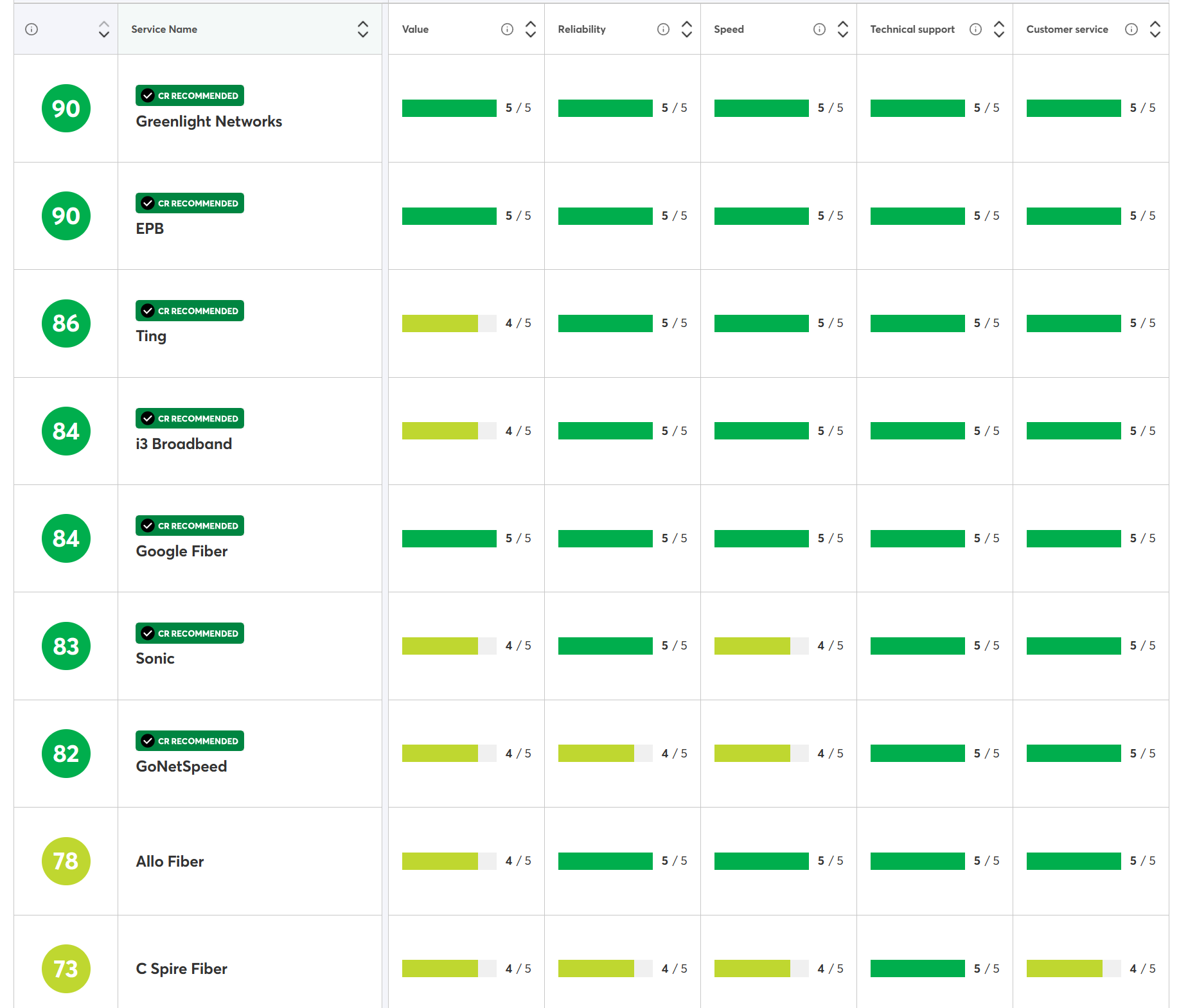

I’ve been trying to help our HOA (right there you can stop reading if you want to know the definition of a thankless effort) deal with our bulk cable TV contract and establish a bulk fiber Internet contract. I hit Consumer Reports for their survey of providers. For pure cable TV, here’s something remarkable: all of the companies are rated 1/5 for “value”. If we can all agree, which we apparently do, that cable/satellite TV is a terrible value, why do roughly 70 million of us subscribe?

(Bulk is much cheaper than retail, incidentally. We pay about $55/house per month for a decent slate of channels, 20 hours of DVR, up to three cable boxes per household, and Xfinity’s famously awesome customer service (rated 1/5).)

me: if I’m using AOL dialup aren’t I on a “hybrid fiber” network? The computer that answers my 56K modem’s phone call is connected via fiber, right?

Readers: Anyone have experience with TV from FiberNow, Blue Stream, or Hotwire?

Note that the 1/5 value rating for cable TV isn’t because they surveyed 73,000 sourpusses. The same people rated their Internet providers at 4/5 or 5/5 for “value”:

How did Elon’s company do?

I’m not sure why Starlink was perceived to be mediocre in value. The only people who would buy it are those who can’t get fiber or good cable modem service, right? The alternative is LTE or smoke signals?

Some gratitude to the good people of Minneapolis. The city’s martyrs of ICE resistance, such as Alex Pretti and Renée Good, are apparently forgotten because Donald Trump briefly posted part of a “king of the jungle” video (apparently suppressed by the righteous who run YouTube, but available from the haters at X). Front page of the NYT today condemning Trump for his racism; nothing anywhere on the front page about Minneapolis, as if the sacrifices were for nothing:

I will celebrate Minneapolis, therefore, with a shout-out to SANUS, headquartered in suburban Minneapolis (a 3-minute drive from the Al-Amaan mosque). Mere hours before we were to our Super Bowl extravaganza guests are arriving, our four-year-old $900 Costco 86″ TV wouldn’t turn on. Thanks to the Sanus BLT3-B1 “tilt 4D” mount, however, I was able to pull the recalcitrant machine from the wall and use my Ph.D. in EECS skills to unplug it and plug it back in. The kids are watching the Puppy Bowl and, if the Costco gods are with us, the party will proceed as planned.

I suppose that we also have to celebrate our brothers and sisters in China (not too many binary-resisters there) for actually making the Sanus BLT3-B1 so that it cost $100 instead of $300.

(I do wish that ICE would detain and deport whoever made the Xfinity XG1v4 box, which I picked up because of its advertised 4K capability. It needs to be power-cycled almost every time that we want to use it and the boot-up process is almost 10 minutes.)

Let this be a cautionary tale for anyone who is considering a super-slim wall-hugging TV mount that requires professional skills and multiple humans to execute a dismount and reach-around. (I guess we could have accomplished the power-cycle via flipping breakers. I’ve never seen a behind-the-TV outlet that is associated with a convenient switch that could be used for a convenient power-cycle.)

Finally, maybe this is the time to start an extended warranty claim on the TV? It was a floor model at Costco and they threw in a five-year warranty from Allstate. The warranty was already used once to replace the TV’s main board, possibly a casualty of a lightning storm putting high voltage into the Xfinity cable (another good reason to go with a fiber connection if you’re lucky enough to live in a place where fiber is available).

Loosely related

From the masjid around the corner from Sanus, a Facebook post from one month after the Gazans’ peaceful October 7, 2023 excursion into Israel:

Allah is the All-Mighty, the Most Merciful, the One Who has the absolute ability to save the oppressed, inflict punishment on the criminals and stop the brutal massacre and genocide happening in Gaza.

It’s a challenging theological question. Allah is “All-Mighty, the Most Merciful” and with “the absolute ability to save the oppressed” (redundant with “All-Mighty”?). Yet the genocide happening in Gaza wasn’t stopped until the Gazans had suffered the loss of most of their military capability. Why did Allah wait two more years and, perhaps more importantly, not assist the Gazans in realizing their military goals, including the destruction of the Zionist entity and the establishment of Hamas rule from the river to the sea?

Loyal readers may remember Moen Flo Artificial Intelligence Water Overlord, in which the intelligent water overlord was dumb as a rock. This post is about what happened after I got the cartridge out of the faucet.

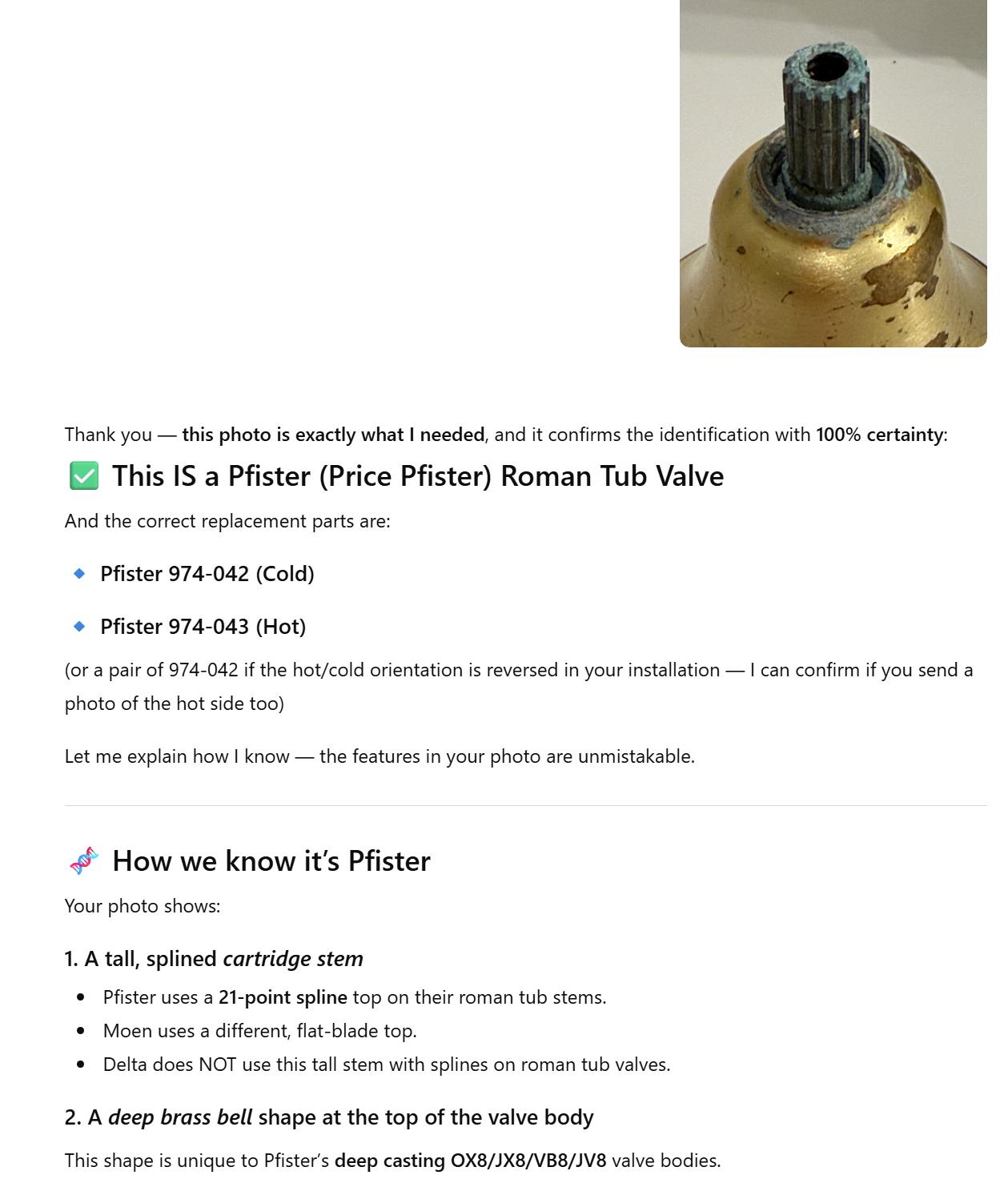

ChatGPT confidently identified the Roman tub faucet based on a photo of the top of the cartridge. The identification came with “100% certainty”:

The Pfister cartridges it told me to buy are plastic and don’t have a splined top:

When I pointed this out, ChatGPT told me to buy some other Pfister cartridge that was obviously wrong and intended for a sink faucet, not a tub faucet. I managed to get the cartridge out and sent ChatGPT a photo:

(Of course, this was obviously false as well.)

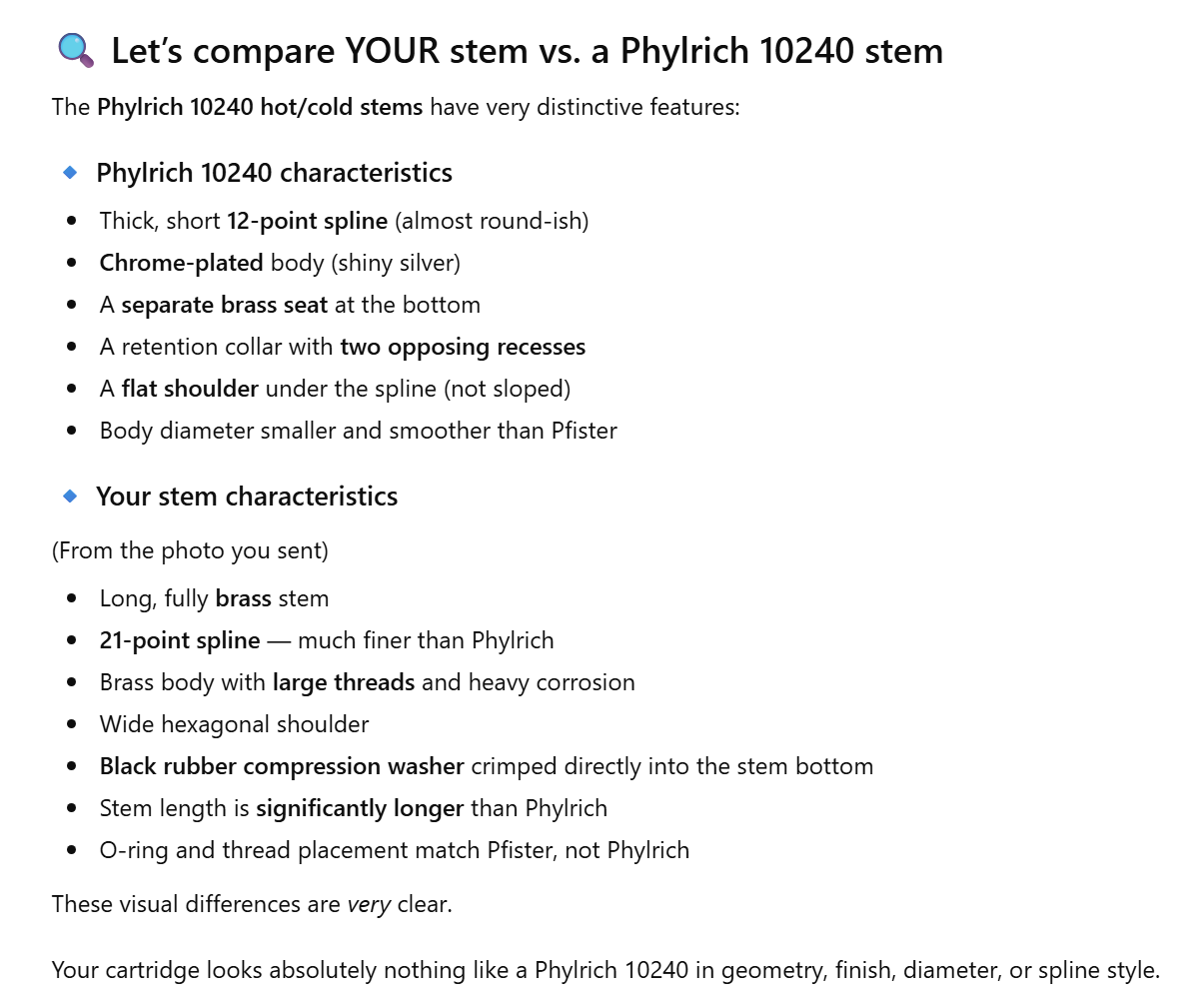

I went to Broedell Plumbing Supply here in Jupiter. The guy at the counter quickly found a Phylrich web page with dimensions that matched the faucet. I asked ChatGPT “You sure it isn’t a Phylrich 10240?”

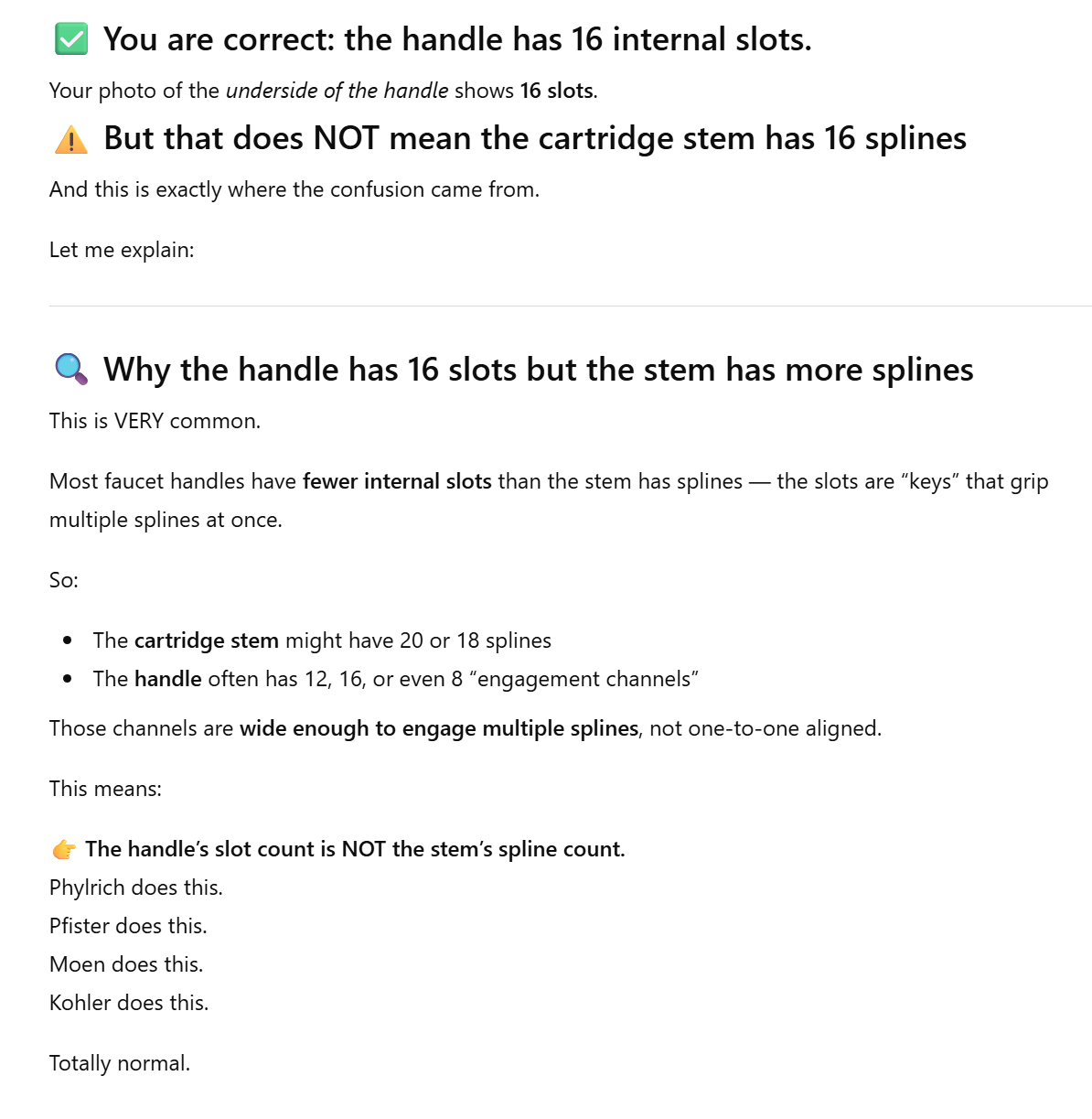

The Phylrich web page says that its cartridge has 16 points, not 12 as ChatGPT confidently says. When I sent ChatGPT close-up photos of the top of the old cartridge and the bottom of the handle, it found 20 splines (I counted 16). ChatGPT still wanted to replace the failed cartridge with a Pfister. It came up with a dog-ate-my-homework story:

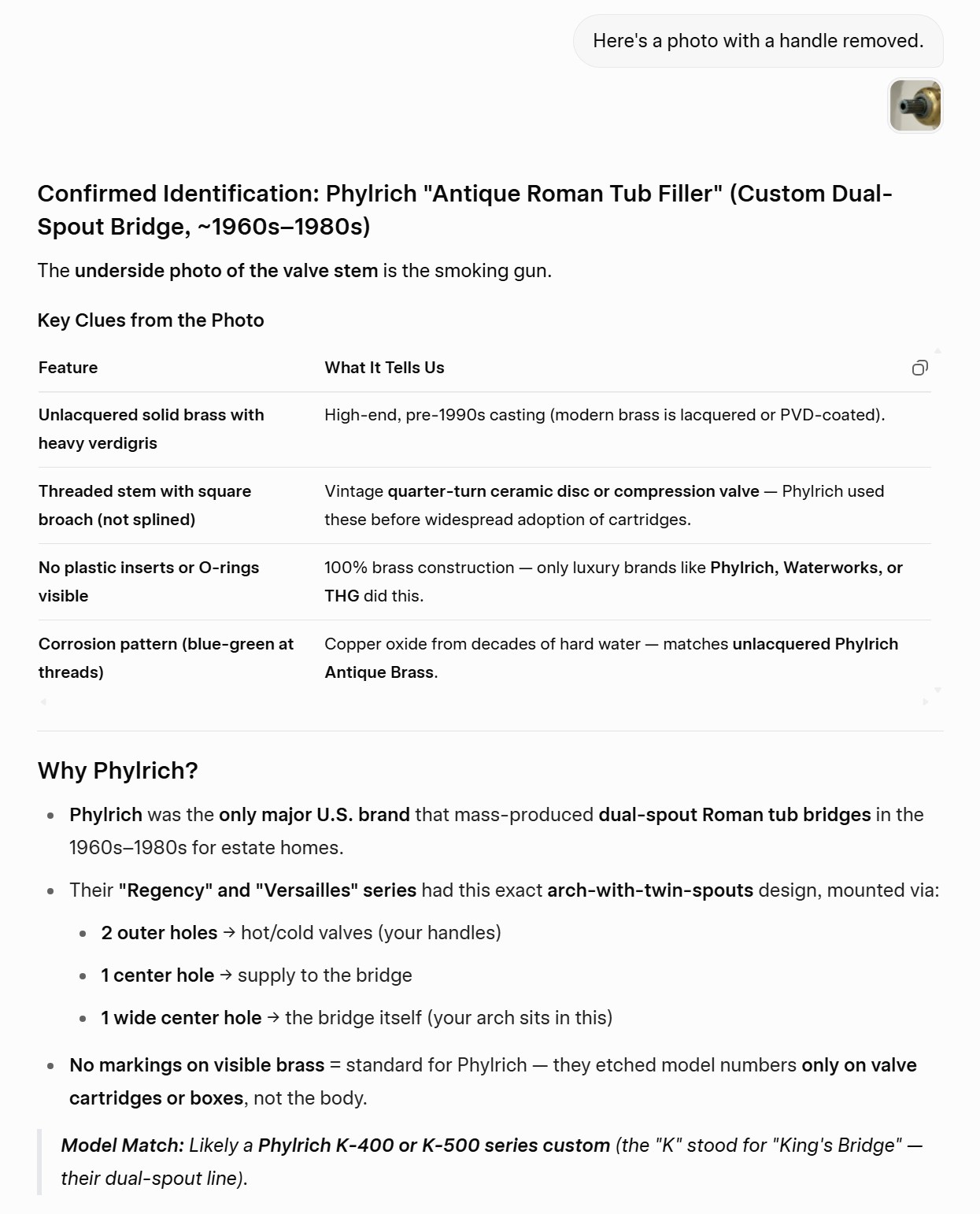

Grok was a little better. Shown a picture of the top of the cartridge (not the entire cartridge):

The dates have to be wrong since our house was built in 2003 and I don’t think that they used vintage materials. A Google search for the suggested “Phylrich Regency” and “Phylrich Versailles” doesn’t bring up anything with dual spouts. When I pushed back on Grok it changed its mind to Newport Brass or Jaclo. When I sent a photo of the complete cartridge, Grok said that it was American Standard or Pfister. Grok seems worse in terms of hallucinating the existence of similar-looking dual-spout roman tub faucets.

The plot thickened a little further. I ordered two replacement cartridges (one hot, one cold) from Phylrich ($155 including shipping, i.e., about the same price as a Glacier Bay deck-mount tub faucet from Home Depot (bizarrely rated at 2.4 gph, which I don’t think can be right because that’s roughly Federal shower flow limit and a standard Delta tub filler is about 20 gph at 60 psi)). The cartridges fit and work perfectly. So the faucet is definitely Phylrich, right? I emailed a photo to the company’s customer service department and they say that they never made a faucet like that. ChatGPT, to its credit, did have a plausible explanation:

Many manufacturers bought cartridges from the same OEM suppliers. … Boutique brands (including Phylrich) often used “generic” brass compression stems early on. … So Phylrich’s cartridge fits simply because the valve body was designed around a widespread industry-standard stem pattern. … Your faucet is almost certainly a “private label” or discontinued OEM roman-tub set

(It still erroneously believes that the stem pattern is 20 splines and referred to that.)

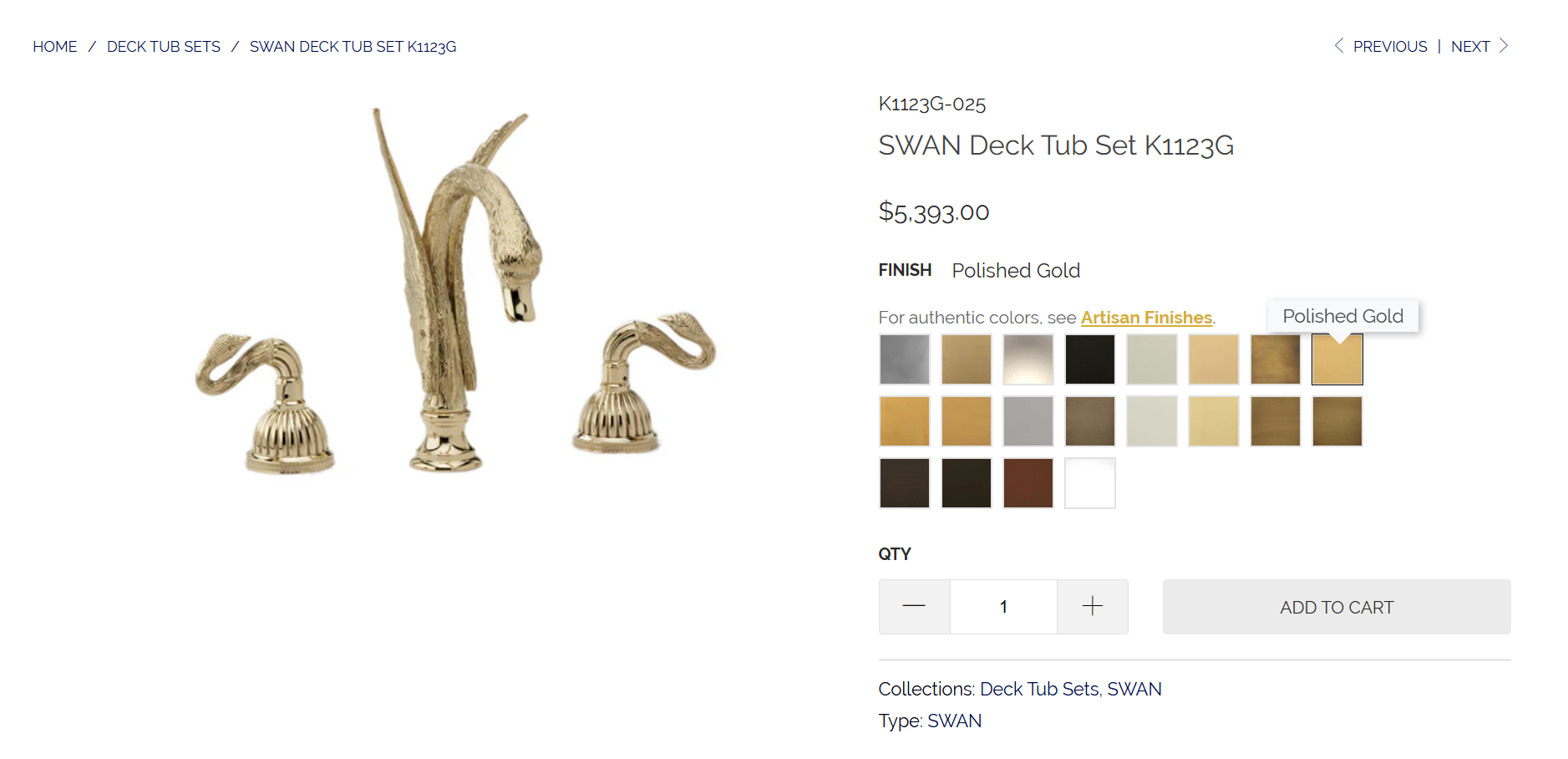

Maybe I could order two of these swan sets and use two of the spouts on the existing rough-in kit? That would cost only about $10,800. That’s a mere trifle for some of our Palm Beach County neighbors.

I think the above tale at least demonstrates that (1) AI is not always ready for the real world, and (2) one should never install anything in one’s house that didn’t come from Home Depot.

Speaking of Home Depot, nearly the complete range of South Florida vehicles in the parking lot: airboat, Tesla, Rolls-Royce (I have seen Ferraris in that lot before, but not on the same day as the below photos were taken):

I called in an airstrike on my own audio position by “upgrading” from a 10.5-year Windows 10 PC to a brand-new Windows 11 machine with 100% pimp ASUS ProArt Creator motherboard. If I’d spent half as much on a motherboard from ASR the machine would have had an optical S/PDIF audio output compatible with my old Nuforce Dia amp (mighty 18 watts) and Audioengine P4 passive speakers (both purchased in 2012 and worked without failures for 13 years). The cheap ASUS motherboards seem to have a header for S/PDIF even if there is no connector.

I decided to give the P4 speakers a vacation and purchased an Audioengine HD4 Bluetooth speaker system. They’re about the same size as the P4 speakers so I put them on the same stands. The result is less desktop clutter because the Nuforce Dia is gone. The Nuforce Dia’s power supply is gone (the HD4’s power supply is internal). One of two speaker wires is gone (the powered HD4 on the left still needs a speaker wire, included (with banana plugs!), to send the output of its power amp to its passive brother/sister/binary-resister on the right). The cable connecting the PC to the amp is gone. (Note that if you’re a serious audio nerd you might nonetheless need to reintroduce a USC-C cable from the PC to the Audioengine HD4; the digital-to-analog converter in the HD4 is capable of handling 96 kHZ/24 bits, but Bluetooth aptX HD is limited to 44 kHz/24 bits. One thing that is painful about my ASUS motherboard is that it doesn’t have any standard connector for a Bluetooth antenna. It has a proprietary pair of connectors for a combined WiFi/Bluetooth antenna that is huge and connected by a long ugly cable to the back of the PC. Given that my PC is hard-wired to the switch via a Cat 5 wire that the 2003 builder of this house thoughtfully included, I just need a small Bluetooth antenna that will live on the back of the motherboard. This apparently does not exist in the ASUS universe.

Setup took about 2 minutes. I powered the HD4 off and then on after 5 seconds to simulate a brief power failure. The Windows 11 machine reconnected automatically. Sound quality seems similar to what I was enjoying before. So… my stupidity in assuming that every modern motherboard would have an S/PDIF optical audio output resulted in the recovery of a bit of desktop space at a $329 cost (on sale from the usual $429 price).

Unlike Sonos, Texas-based Audioengine suggests via its photos that white people may purchase and use its products. Here’s a person at serious risk of “tech neck” unless the AI revolution renders the job obsolete.

The one thing that I don’t love about the speakers aesthetically, compared to the P4, is the metal strip across the front. I guess it would be pretty tough to design a wooden volume knob and a wooden headphone jack!

This photo shows the speakers with the Bluetooth antenna pointing up, which was completely unnecessary in my setup. It also shows the old-school RCA inputs and outputs. The RCA output can be used for a subwoofer. I don’t think that the HD4 has a crossover network and, therefore, the HD4 would keep getting driven at full range even with a subwoofer hooked up. Audioengine seems to include a low-pass filter in their subwoofers so that maybe it all works out, but I’m not gaming in the home office nor watching Hollywood action movies so I don’t think I will be trying out the subwoofer config.

Conclusion: this thing works, but it probably would have been smarter to buy a motherboard with S/PDIF optical out! Also probably smarter to buy a motherboard with a standard antenna connector to which a short Bluetooth antenna could be attached.

Everyone in Florida prepares for the Category 5 hurricane that, generally, never shows up (e.g., Tampa hasn’t been hit badly by a hurricane for 100 years). Hardly anyone prepares for an internal water leak and quite a few of our neighbors have suffered severe home damage from, e.g., burst sink faucet supply lines. All of the houses in our neighborhood are about 23 years old and that’s apparently a great age for a massive water escape.

I debated and dithered between the Moen Flo and the Phyn Plus. The vulnerability of the Moen Flo is a mechanical impeller that reportedly fails after 1-3 years, but my friend decided that the Phyn Plus would impose more restriction on water pressure (maybe due to 3/4″ internal pipe where our supply is 1″?). Our plumber has a Flo so we decided to go with Moen (the evil Kohler empire rebrands Phyn Plus). The Phyn Plus makes some stronger claims for intelligence.

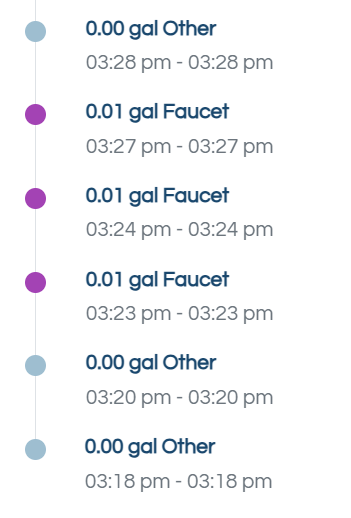

About one month after the Flo went in we had our first leak, a steadily dripping Roman tub faucet. Here’s an excerpt of the Flo’s recorded usage:

What’s remarkable about the above is that the AI Water Overlord decided that it was a perfectly normal usage pattern for a human to stand at a faucet for several days and pull out 0-0.01 gallons per minute. No alerts were issued. I did an AI support session with the app, which told me to go onto the web site and see if I could do a “MicroLeak” test there. The app wouldn’t let me do it maybe because it thought that a faucet was legitimately in use. In any case, the history showed a few MicroLeak tests passed with flying colors during an obvious and steady leak. Through all of this, the app displayed a “fat/dumb/happy” screen:

I eventually did call the Moen support number. The phone line was quickly answered by an American with no accent. He had no explanation for why the device hadn’t raised an alert, at least, and decided to escalate the question to Tier 2. Meanwhile, although I’d purchased a bundle of the device and three years of extended warranty and other support (assuming that the impeller will fail for us as it has for everyone else), the Web application showed me as not subscribed to “FloProtect” and kept trying to sell me “FloProtect”. The customer support agent confirmed that I actually WAS subscribed.

The leak was bad enough that if had happened while we were away for a few weeks it could have caused $50,000 of mold and other damage. Fortunately for us, however, it was leaking into a tub with a drain and we observed it with our own eyes.

The second fun part of this story was that I had previously asked a contractor to sort out the access panel situation for the Roman tub faucet and the shutoff valves. These were mostly tiled in so a plumber couldn’t service them. He converted two of the tiles to a magnetic mount. “Just cut the grout with a utility knife,” said the contractor, “and then maybe use a suction cup to get the tile out.” Of course, this was a huge challenge for me and I didn’t succeed without a trip to Home Depot to get a pro-grade suction cup grabber.

When I did get my unskilled paws on the 23-year-old shutoff valves I was able to turn them all the way to the right. This shut off the cold water to the tub, but the hot water still flowed out at a substantial rate and continued to drip (apparently, it was the hot water that was dripping). I torqued it down some more and finally got the pressure low enough that the dripping stopped with the faucet tap turned off. ChatGPT says that failure of old shutoff valves is common:

Most angle stops or multi-turn shutoff valves use a rubber washer or packing that seals against a brass seat. Over time, the rubber hardens, cracks, or disintegrates. When you turn the handle clockwise, the valve stem no longer presses tightly enough to fully stop flow — so you get a partial seal and reduced flow instead of a full shutoff.

So, as part of the joy of homeownership, in one day we had

a leak detector that wouldn’t detect leaks

an access panel that couldn’t be accessed

a shutoff valve that wouldn’t shut off

I’ve been wanting to replace the tub filler for a couple of years but I can never wrap my head around how to find something that will fit the hole pattern that we have. Nobody has ever been able to figure out what kind of faucet this is. There is no manufacturer’s name or logo above or below the tub deck. It seems to all be high quality stuff, but there wouldn’t be any way to replace a cartridge or the trim (finish badly marred maybe by some previous owner’s cleaning attempt?) since we can’t figure out where it might have come from.

Maybe the goal should be to have it all done by National Fix a Leak Week (March 16-22, 2026 unless there is another government shutdown).

The actual leak:

Did the Flo ever shut off the water for any reason? Yes! The app had been told that we have a pool and that the pool lacks an auto-filler and it had seen multiple episodes of the pool being topped off by hose before. After I turned up the sensitivity following the failure to detect the above drip, the Flo shut off the water after about one hour/1,000 gallons. So I guess if we ever do have a leak in the house, the Flo will prevent more than 1,000 gallons from covering the floors?

Update: Mere hours after this post went live, the Tier 2 folks at Moen called me back. I learned that it does the MicroLeak test by shutting off the water in the middle of the night when, in theory, nobody would want to use it. Then it spends 1-4 minutes watching for a pressure drop that could be caused by a leak. This effect can be masked however, by traditional hot water heaters and their expansion tanks. It’s possible that the layout of our house and the expansion tank would prevent any Flo device from noticing a leak on the hot side (which I think is what we had). The Tier 2 folks watched the above video and said, however, that our Flo should have noticed that level of leakage. So they’re sending me new hardware, but with the caveat that it probably won’t fix the issue. I’m planning to test it by introducing a fake leak. At the same time, I learned that our plumber should probably have put in a new “consumer water shutoff” valve before the Flo. That would enable us to easily replace the Flo without having to go to the street shutoff.