Meet in Holland or Ireland?

Folks: I’m heading over to mostly-peaceful Europe this week. I’ll be at the Delft University of Technology in Holland for a few days and then going to Ireland (Dublin, Sligo, and Belfast) for some aviation projects. If anyone would like to get together over there, please email philg@mit.edu.

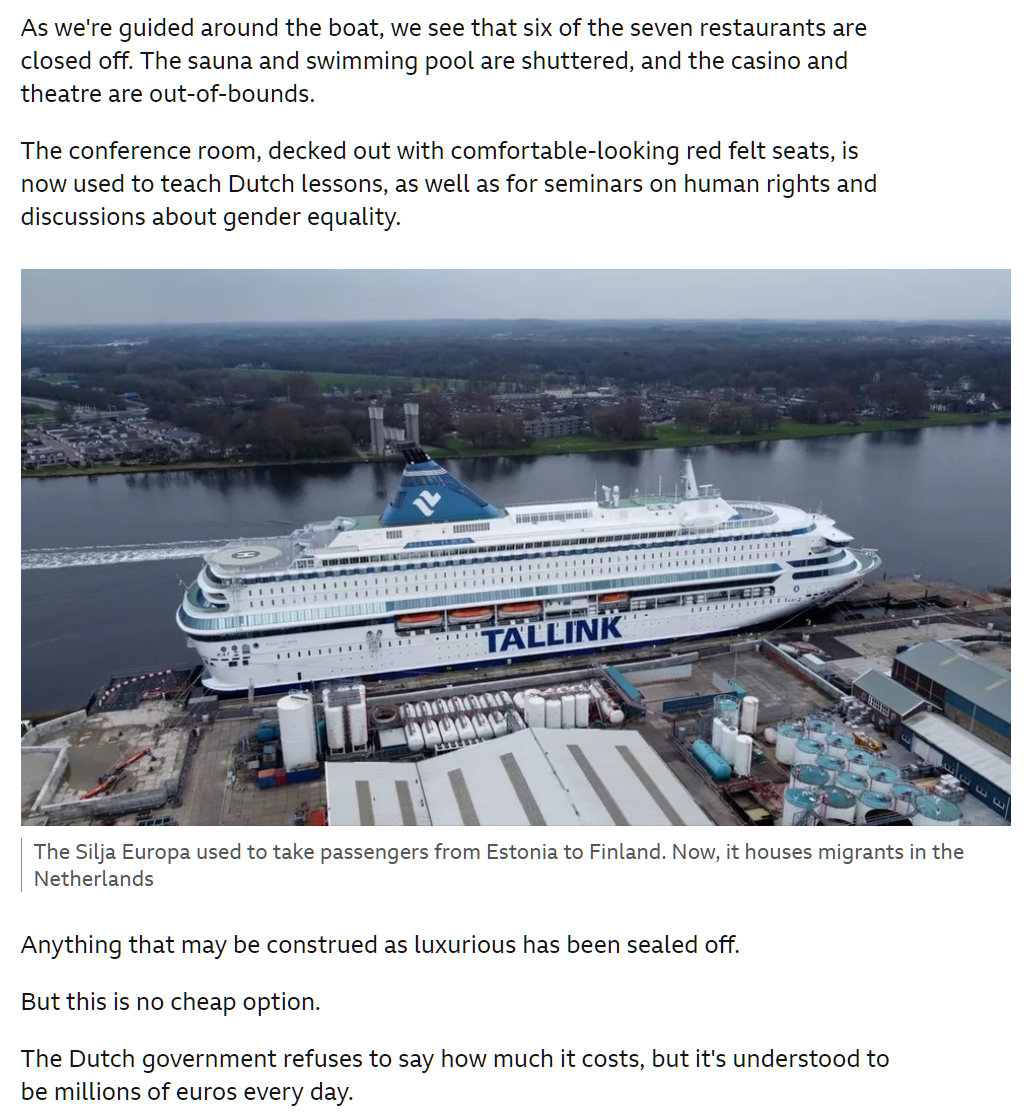

“The ferry in the Netherlands hosting refugees and migrants” (BBC, April 2023) shows one place where I’m not planning to stay:

The Irish voted to end birthrate citizenship by an overwhelming margin in 2004. Nonetheless, the haters aren’t satisfied. “‘There is no room’: anti-immigration protesters march in Dublin” (The Guardian, Jan 2023):

Pickets and blockades of roads are often held outside refugee centres in working-class neighbourhoods but on Saturday activists marched in the heart of the capital.

“It’s not about racism. There is no room for them,” said Gavin Pepper, 37, as he and about 350 others denounced the increasing number of asylum seekers. “Why should migrants skip Irish people on the housing list? I won’t accept it.”

An acute housing and homelessness crisis has collided with the state’s struggle to accommodate Ukrainians and asylum seekers, fuelling accusations that foreigners receive preferential treatment.

Protesters also say centres with “unvetted” young male refugees make them feel unsafe. “I have five girls and two boys and the girls are afraid to go out at night,” said one man, who declined to give his name.

I won’t be staying in a work-class neighborhood, so I may not meet the migrants.

In France, meanwhile, things are entirely peaceful not merely mostly peaceful, according to the New York Times… “Unrest in France Eases Nearly a Week After Fatal Police Shooting”.

In the alternate universe inhabited by the Deplorables at Fox, however, what the New York Times calls “protests” are “riots”… “French riots: New report details thousands of arrests, hundreds of attacks on police since violence broke out”:

A new report from France’s Ministry of Interior quantifies the damage done after nearly a week of protests in response to the police killing of a teen of North African heritage.

The report, obtained by the French newspaper Le Parisien, recorded 5,662 vehicle fires and more than 1,000 damaged buildings.

Since rioting first broke out on Tuesday, police have made 3,354 arrests – 1,282 of which were in the Paris metro area alone, according to the report.

Like Harvard and Democrats on the Supreme Court, the French are blaming Asians:

“Asian tourists, in particular, who are very concerned about security, may not hesitate to postpone or cancel their trip,” he warned. Didier Arino, managing director of the Protourisme firm said: “Tourists who know us well, like the Belgians or the British, who also have problems themselves in their suburbs, will be able to make sense of things”.

Maybe this summer it makes more sense to do Remy’s Ratatouille Adventure in EPCOT.

Full post, including comments