Art Basel Miami Beach 2025

Here’s my report from this year’s Art Basel. All photos from the iPhone 17 Pro Max.

Because paying $1,000 per night for a basic hotel room is just a rounding error for me… I stayed across the bay at the Marriott Biscayne Bay. This turned out to be a blessing in disguise because it was right next to Art Miami, which I hadn’t heard about and which I’ll cover in a later post, and also because it’s right next to a former Episcopal Church that has converted to Rainbow Flagism, consistent with Santiago de Compostela and End Stage Christianity.

If you don’t want to get stuck in traffic, the Miami Citibike system isn’t a bad way to get around. The bikes don’t seem to be in great shape and they don’t fit a 6′ rider that well, but the terrain isn’t hilly.

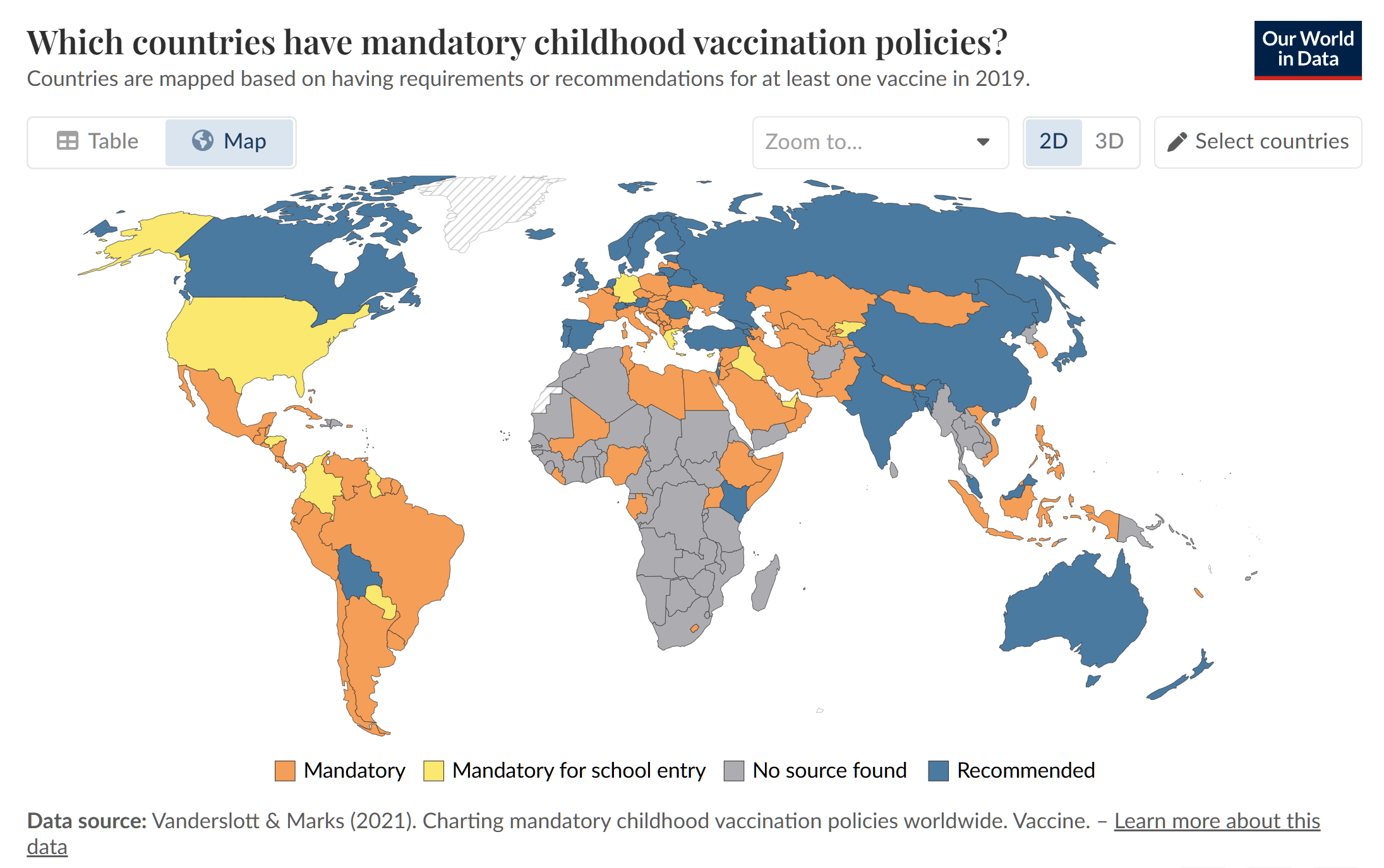

In Art Basel Miami Beach (2018) and Art Basel Miami 2021, UBS featured female victimhood and celebrated the handful of women who’d manage to overcome the “imbalance” and “make a difference”. The commitment to social justice seems to have evaporated and now UBS promotes getting richer:

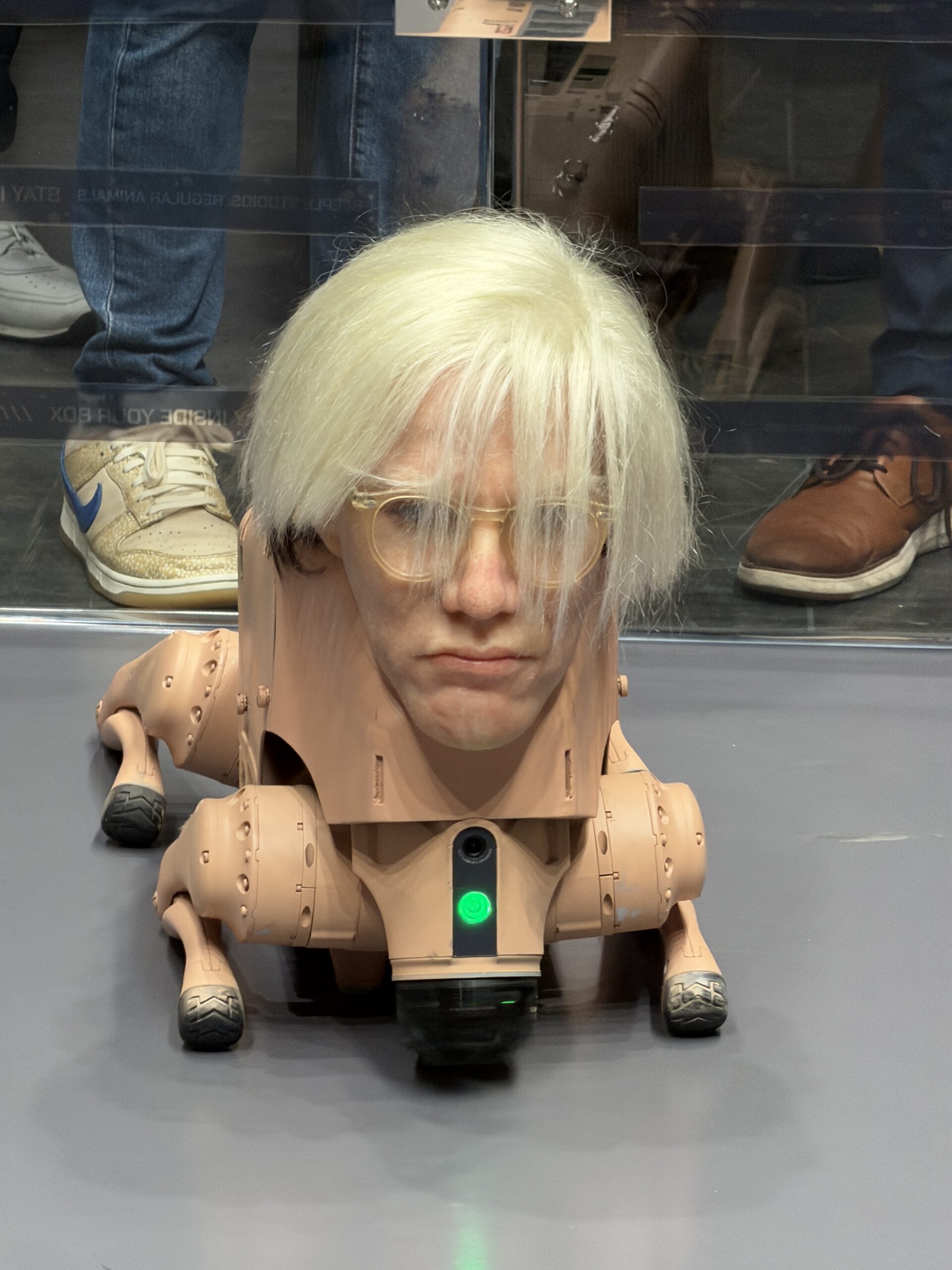

Speaking of rich, the most talked-about installation echoed the UBS theme of rich-meets-art. Busts of Jeff Bezos, Elon Musk, and Mark Zuckerberg on robot legs interacted with Andy Warhol, Picasso, and the creator of this work (Mike Winkelmann; a.k.a., “Beeple”). (Given Picasso’s fondness for teenage females, could he have survived today’s moral rectitude?)

Here’s Andy Warhol (the most famous gay person not famous for being gay?):

The Wall Street Journal says that $200 million is the new minimum for a decent house and there were quite a few pieces for sale that would have required a spare thousand square feet or two. Here’s an example from Anne Samat titled “The Unbreakable Love… Family Portrait.” It includes plastic swords, keys, wine corks, etc.

A work by Yinka Shonibare that inspired me to stop complaining for a few minutes:

I looked him up on Wikipedia: “At the age of 18, he contracted transverse myelitis, an inflammation of the spinal cord, which resulted in a long-term physical disability where one side of his body is paralysed.” If someone who is half-paralyzed can make it to Art Basel, what’s wrong with the rest of us?

Feel better about your middle-school dioramas (by Mondongo, a husband-and-wife team in Argentina):

Here’s a technique that I enjoyed, hand cut paper by Ariamna Contino (or maybe by her assistants?):

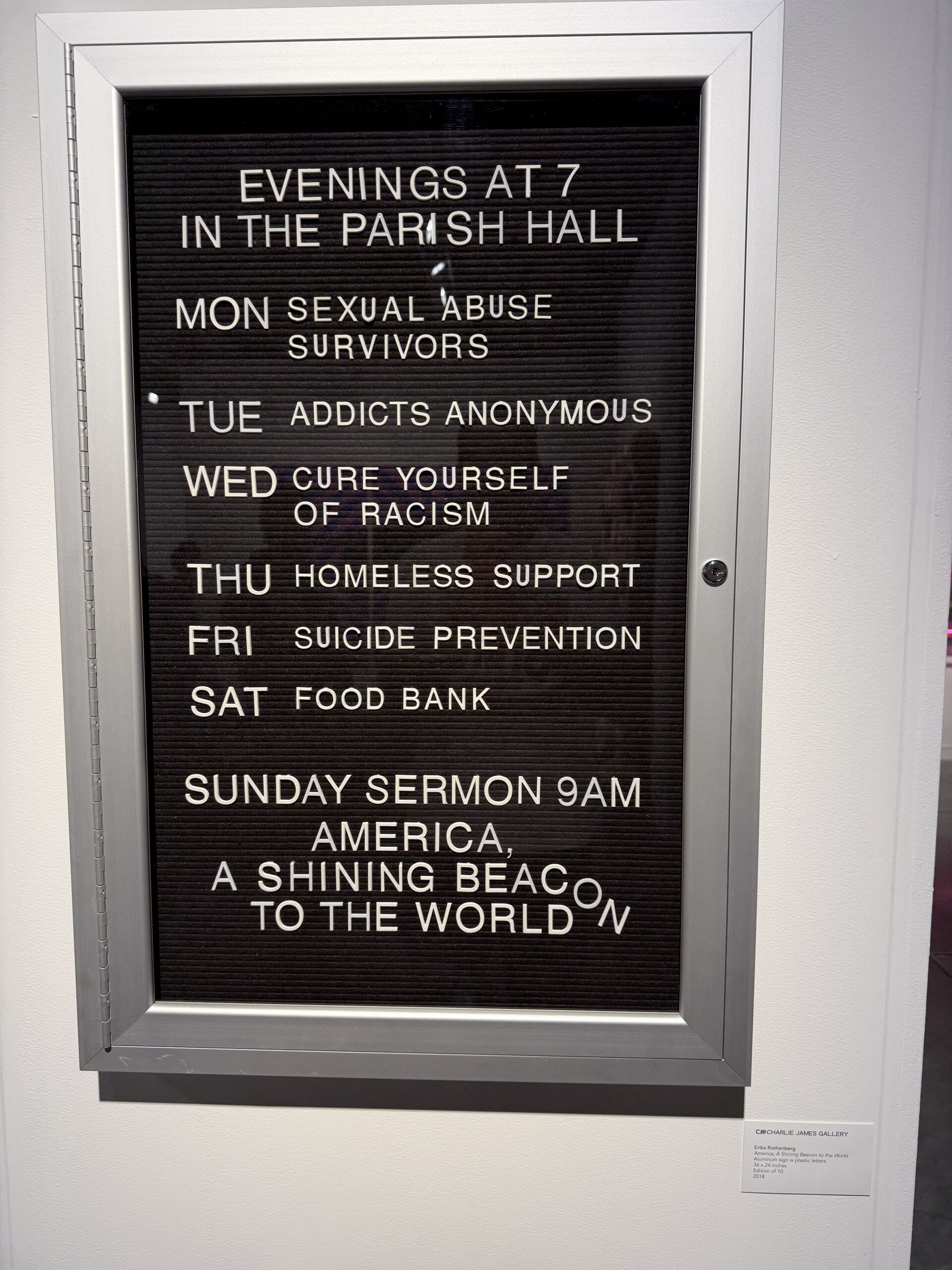

At the opposite end of the effort spectrum, Erika Rothenberg’s 2018 work America, A Shining Beacon to the World:

Only the Weinstein Gallery (they haven’t changed their name?) was crass enough to put prices on labels. Here’s a modest-sized $3.5 million Leonor Fini work from 1936 (imagine what it would cost to get an original oil painting by an artist that people have actually heard of!):

Some practical advice… pay a little extra for the 11 am entry tickets and go in right at 11 rather than at noon. The venue gets crowded by 1 or 2 pm. A 2:15 pm Friday image:

From 1:22 pm:

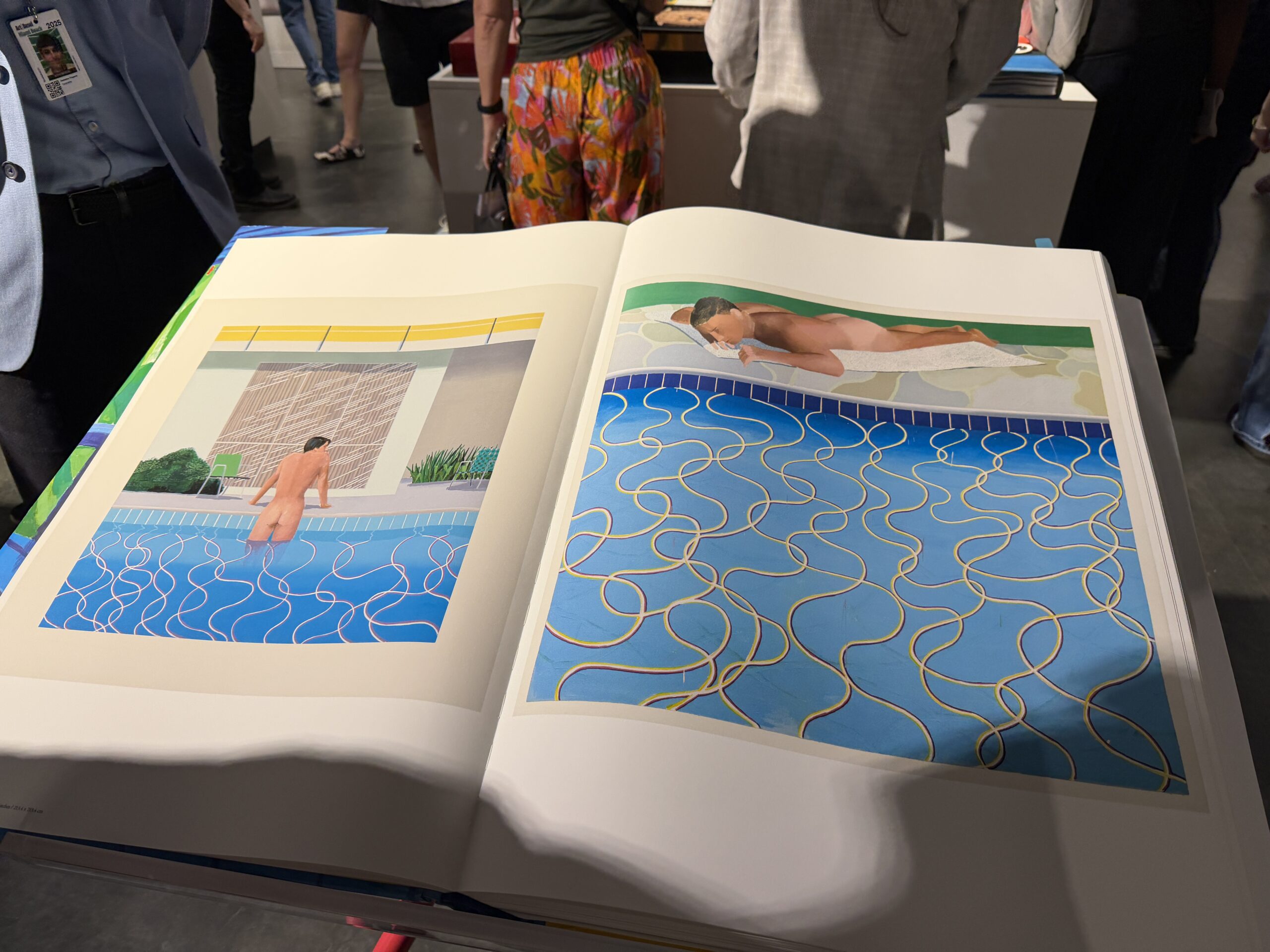

You don’t have to spend a lot to bring a souvenir home from the event. For only $5,500, for example, you can get a nice Taschen book of David Hockney pictures (printed in Italy):

Don’t worry about charging for your electric Rolls-Royce:

There are quite a few additional art events in Miami Beach and, covered in a later blog post, across the bay in Miami proper.

Here’s a Mayan pyramid made from Coleman coolers at SCOPE (Victor “Marka27” Quinonez of Mexico):

Finally, you can just walk around South Beach: