Happy Tax Day for those who celebrate (i.e., Americans who aren’t smart enough to have joined Mitt Romney’s Club 47).

David Brennan and Jackie Mustian, attorneys at Moffa, Sutton, & Donnini, gave a talk at Sun ‘n Fun about how people avoid owing a 6 percent sales tax when buying an aircraft that will ultimately be based in Florida. (Imagine the potential liability for an elite buying a $100 million Gulfstream!)

First, it seems unlikely that Florida is getting any real benefit from imposing this tax. The true beneficiaries are attorneys and accountants who set up schemes to avoid it. Perhaps because of that, there is no urgency among legislators to eliminate the tax, as Maskachusetts did back in 2001. Under the assumption that the tax, and the army of professionals whose job it is to avoid it, are with us forever, here’s what we learned…

A nonresident who owns a new-to-him/her/zir/them aircraft has to be careful about visiting Florida for reasons other than maintenance or flight training. If the aircraft is here for 21 days within the first six months of ownership, Florida sales tax is owed. A flight that lands at 11:55 pm and departs 10 minutes later at 12:05 am is considered to have spent two days in Florida out of the allowable 20.

A Florida resident cannot take advantage of the above exemption. If the Florida resident is the sole owner of a Maskachusetts, Delaware, or Montana LLC that owns the aircraft, the 20-day exemption might apply, but an auditor might also try to look through the LLC shell to the real owner. The Floridian ideally would keep the aircraft out of state entirely for six months and also not display an obvious intent to bring it into the state on Day 183 (maybe the Floridian is a super douche and also is looking at buying a house in Nantucket and has written to the airport there about getting on the hangar waitlist).

Where the tax advisors seem to make money is in setting up an LLC that is in the business of owning an aircraft and reselling it or its use to others. Prior to the aircraft purchase, the LLC is registered with the State of Florida to collect sales and use tax. The “real owner” then dry leases time with the aircraft from the LLC and the LLC collects and remits sales tax on the dry lease payments, e.g., $75/hour, but only for those hours flown within the State of Florida. In the speakers’ opinion, the State of Florida doesn’t have a legal basis for challenging the reasonableness of the lease rate. The state is entitled to collect tax only on the money that is actually changing hands. That said, a $10/hour dry lease rate for a $1 million aircraft could seem ridiculous. (Other states where this kind of scheme is employed have some rules about the minimum cost for the dry lease based on prevailing interest rates.)

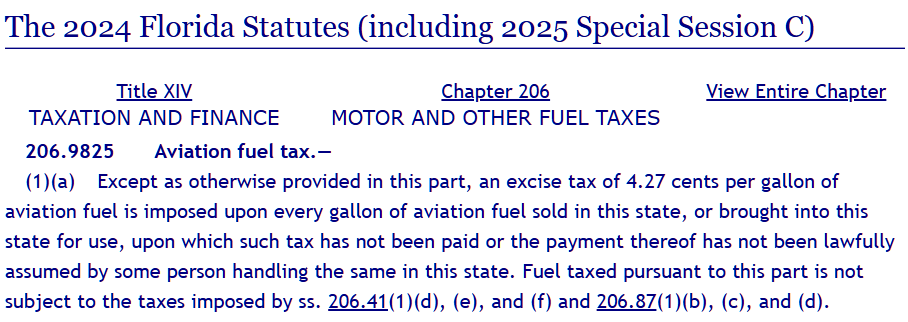

It’s too bad that DeSantis and the Legislature haven’t cleaned this up. In my opinion, the efficient way to tax aviation is a fuel tax and if the state wants more money from aircraft owners it should simply raise the existing aviation fuel tax (FL 206.9825):

Now that folks have had a chance to digest the Election Nakba… what are you all forecasting for tax policy? This is one of the few areas of federal policy where we could productively change our behavior given a change in the policy.

My guess is that the Trump Big Bang tax law that went into effect 2018 gets extended, more or less unchanged, thus revoking the expiration dates of 2025 and 2028 for various individual and business tax provisions. My basis for this prediction is that Congress hates cutting spending, but enjoys cutting taxes. That’s how we get the deficit spending that started in earnest when Congress refused to implement Ronald Reagan’s proposed spending cuts, but did oblige him on the tax rates that he suggested.

My first prediction for a change is that the limit on state/local (SALT) tax deductibility will be raised or eliminated in order to get some cooperation from the Party of the Economic Elite (i.e., the Democrats). My second prediction is that there will be some sort of enhancement of the current system for extracting money from the childless (the “drones”) and giving the cash to those with children, e.g., via tax deductions or tax credits or “refundable tax credits” for those who don’t bother to work and instead enjoy playing Xbox with their children for all after-school hours. There is nothing that American politicians love more than making the childless work another few hours every week so that parents can enjoy time with their kids.

What would I do about taxation if I could be dictator for a day?

no change to current tax rates (I assume these are already the revenue-maximizing rates and the federal government needs at least $36 trillion just to pay back debt)

no change to the mechanisms that Donald Trump put in place to keep multi-national companies from parking all of their profits offshore

the IRS prepares a draft tax return for every American income taxpayer (i.e., about half of us) with all of the information that it has received and enables us to edit it

eliminate the estate tax, which generates a huge amount of unproductive legal and accounting activity and hardly any revenue (about $20 billion/year against a federal budget of $7 trillion)

eliminate the Generation-Skipping Transfer Tax, which is a complicated add-on to the estate tax

eliminate the step-up in basis that assets get upon an owner’s death (so capital gains liability would increase on inherited assets once they’re sold)

index capital gains taxation to inflation so that fictitious (inflation-driven) “gains” aren’t taxed (see Uncle Joe’s capital gains tax (what could have been, unburdened by what was) for an example of what would happen to a long-term investor in GE stock who actually lost money in real dollars and then loses more to a tax on inflation)

eliminate charitable donation deductions (this prevents multi-billionaires from escaping taxation by giving money to the foundations that their kids control, etc.; Warren Buffett has already announced that the U.S. Treasury will get bupkis after he croaks because 99.5% of his money will go “to a charitable trust overseen by his daughter and two sons when he dies.” (USA Today))

Despite the elimination of the estate tax, note that the above changes would result in a huge increase in revenue from dead people and their heirs. Right now someone can inherit a $20 million house from two parents, completely tax free (estate tax exemption for a married couple is about $28 million), and the basis is $20 million, not the $1 million price that they paid in nominal dollars way back when or the $3 million price that is the $1 million adjusted for inflation. Thus, the heir could sell the $20 million house and pay no tax at all because the basis was stepped up to $20 million. If the above changes were implemented, an immediate sale of the inherited house would subject the heir to capital gains and Obamacare tax on a $17 million inflation-adjusted gain or 0.238 * $17e6 = $4 million. Same deal with a $2 million house (i.e., a Biden starter home!), but it would be perhaps $400,000 in revenue for the Federales rather than the current $0. (States that impose a capital gains tax (i.e., not Florida!) could be similarly fattened by these changes.)

Since my ideas are never popular with anyone else, I guess we can say for certain that none of the above changes will ever happen!

In 2012, Puerto Rico had passed two laws intended to make the island a “global investment destination.” Act 20 allows corporations that export services from the island to pay only 4 percent tax. Act 22 goes much further: It makes Puerto Rico the only place on U.S. soil where personal income from capital gains, interest, and dividends are untaxed.

The last big tweak to U.S. taxation was in 2018. Plainly, the rates were low enough that most rich Americans refrained from making the move to the Ritz-Carlton Dorado. But what if Kamala Harris and fellow Democrats are able to deliver on their promise to soak the rich? Wouldn’t there be a lot more rich people who would make the move for 183 days per year in order to avoid losing a big percentage of their wealth? If so, the only way to stop the erosion of expected tax base would be to eliminate Puerto Rico’s ability to offer Act 22 treatment and the only way that I know to strip Puerto Rico of its tax sovereignty is to make Puerto Rico a state.

The Democrats’ latest tax schemes, recently highlighted by Kamala Harris, include collecting tax on unrealized capital gains. To me, one of the strangest things about the US tax system is that losses are taxed as capital gains so long as there is even the slightest amount of inflation. For example, if you bought a stock in January 2021 for $100 and sold it today for $110 more you’d have about $10 in today’s dollars terms under official CPI and closer to $80 if adjusted for house purchasing power (Zillow). Despite the loss on what turned out to be an unsuccessful investment, you’d owe federal and, perhaps, state tax on the sale. The current not-adjusted-for-inflation capital gains tax regime is, thus, rather cruel when combined with Bidenflation but at least you can choose when to pay the tax on your fictitious profit/real loss.

IRC 877A imposes a mark-to-market regime, which generally means that all property of a covered expatriate is deemed sold for its fair market value on the day before the expatriation date. Any gain arising from the deemed sale is taken into account for the tax year of the deemed sale notwithstanding any other provisions of the Code. Any loss from the deemed sale is taken into account for the tax year of the deemed sale to the extent otherwise provided in the Code, except that the wash sale rules of IRC 1091 do not apply.

Section 877A(a) generally imposes a mark-to-market regime on expatriates who are covered by section 877A, providing that all property of a covered expatriate is treated as sold on the day before the expatriation date for its fair market value.

For purposes of the mark-to-market regime, the covered expatriate is deemed to have sold any interest in property that he or she is considered to own under the rules of this paragraph other than property described in section 877A(c). For purposes of computing the tax liability under the mark-to-market regime, a covered expatriate is considered to own any interest in property that would be taxable as part of his or her gross estate for Federal estate tax purposes under Chapter 11 of Subtitle B of the Code as if he or she had died on the day before the expatriation date as a citizen or resident of the United States.

In computing the tax liability under the mark-to-market regime, a covered expatriate must use the fair market value of each interest in property as of the day before the expatriation date in accordance with the valuation principles applicable for purposes of the Federal estate tax, except as otherwise provided in this paragraph.

The number of individuals who renounce their U.S. citizenship or terminate their green card status has increased significantly since the enactment of the current expatriation tax regime in 2008. Lists of these individuals published quarterly by the IRS in the Federal Register show that the number of individuals expatriating has increased from 312 in 2008 to 3,260 in 2023, with a peak of 6,705 in 2020.

My big question is how President Kamala Harris will collect long-term money from the targets of her extended (not exactly new, as noted above) unrealized capital gains tax. A person targeted by the tax has two choices:

pay President Harris for unrealized capital gains in 2026 (let’s assume it takes a while for this to be implemented), 2027, 2028, and every subsequent year until death

pay President Harris for unrealized capital gains at long-term rates in 2025 and then never pay income taxes to President Harris, the U.S. government, or any other government again (expatriation)

Why wouldn’t a rational target of the new tax choose Option 2? He/she/ze/they renounces U.S. citizenship, moves his/her/zir/their assets into an offshore Dutch trust (as U2 did) and moves to any country that doesn’t dig into offshore assets/income for computing income tax. Or establish a residence in Italy and pay a flat tax rate of €200,000 a year (recently bumped up from the €100,000/year rate established in 2017, which means it has kept roughly even after adjusting for inflation in the costs of things that rich people buy, but the bump doesn’t affect people who signed up for this prior to August 2024). Or simply move to a country that doesn’t impose any income tax (KMPG on relocation to Monaco). If the expat is nostalgic, he/she/ze/they can return to the US for 30-60 days per year, depending on the employment situation, without becoming subject to U.S. taxation.

There is a lot to like about living in the U.S. (especially here in Florida!), but is it worth paying 100X as much in taxes compared to living in some other part of the world? If there are friends you want to see buy them a first class ticket to Heathrow and push your way through the pro-Hamas rallies to a night of theater. Or, if you’re truly one of those who has taken more than he/she/ze/they needs, send the Gulfstream or Airbus Corporate Jet to pick up the friends.

Here’s a place in northern Italy that costs less than a tract house in Palm Beach County ($2.7 million for a modern house on 22 acres):

Given the tax savings, maybe there isn’t any need for maintenance. Just buy a new house every few years with a fraction of what would have been paid in unrealized capital gains tax and give the old house to a charity.

Separately, why didn’t the Democrats impose their new tax regime during the first two years of the Biden-Harris administration when they had control of both houses of Congress and the White House? How can Kamala Harris simultaneously say that she agrees with everything that Joe Biden did (or read from a teleprompter) and also that she will do completely different stuff starting January 2025?

Wikipedia page on Eduardo Saverin: “a Brazilian billionaire entrepreneur and angel investor based in Singapore. … With an estimated net worth of US$26.3 billion as of early August 2024, he is the 69th richest person in the world, and the richest Brazilian. Saverin renounced his U.S. citizenship in September 2011, thereby avoiding an estimated US$700 million in capital gains taxes.”

His plan to outflank Trump would scale up the calculated system of repression he designed in Florida. …To stifle dissent, in 2021 DeSantis signed a law that would ramp up penalties for rioting but that civil rights groups warned would ensnare peaceful protesters [what about mostly peaceful protesters?]; this spring he pushed legislation to unleash speech-chilling lawsuits against news outlets.

DeSantis, like other distrustful autocrats, keeps a tight circle of advisers, including his wife.

One way DeSantis has created space to operate is by hollowing out state government, filling key posts with donors and loyalists—the academic term is “autocratic capture”—perhaps most notably on the state Board of Medicine, which has supported his agenda to put new limits on gender-affirming care.

Nobody would live in Florida, in other words, unless he/she/ze/they has no other option, e.g., is incarcerated or established in public housing that would take 10 years of waiting to get into in another state. Anyone who cherishes freedom should have driven north on I-95 in fall 2020 when DeSantis ordered public schools to reopen and refused to permit county and local officials to order lockdowns, masks, and vaccine injections.

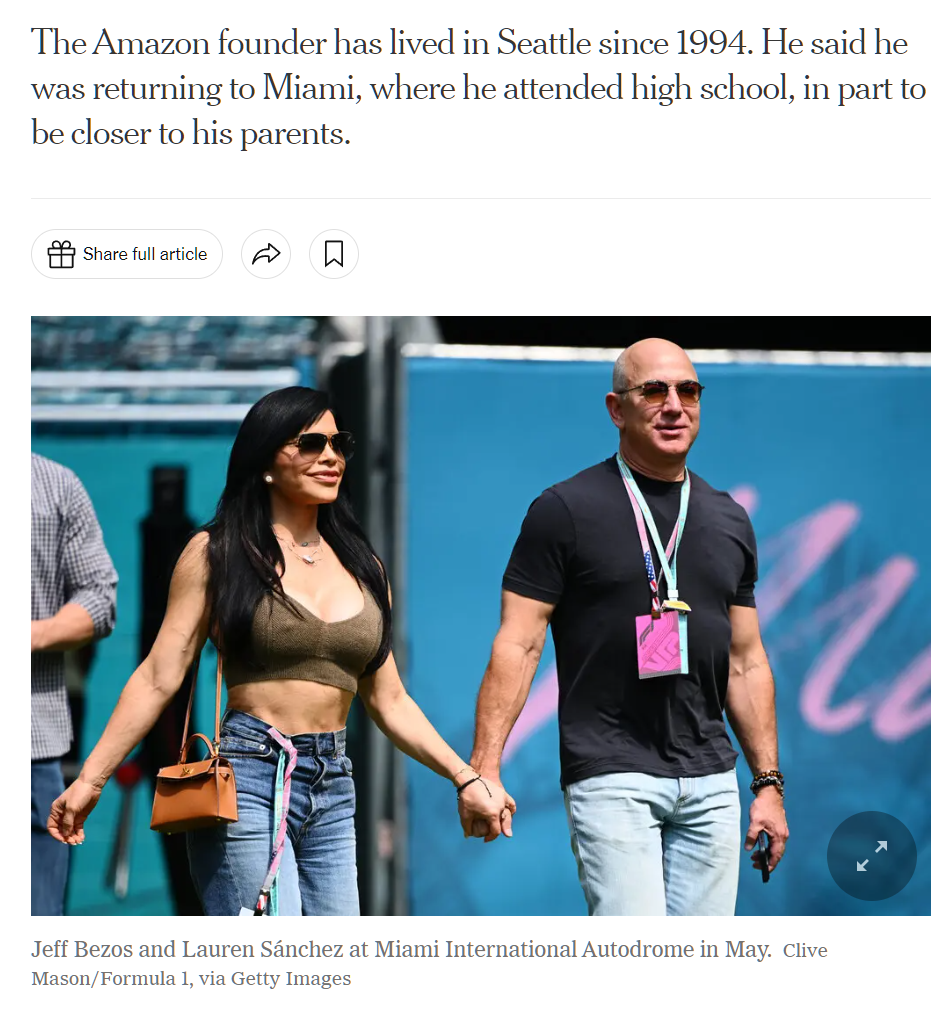

Mr. Bezos, 59, announced his move in an Instagram post on Thursday night. He said his parents had recently moved back to Miami, where he attended high school, and that he wanted to be closer to them and to his partner, Lauren Sánchez.

Another factor, he said, was that operations for his rocket company, Blue Origin, are increasingly shifting to Cape Canaveral, Fla., just over 200 miles by road north of Miami along the state’s Atlantic coast.

Bloomberg News reported last month that Mr. Bezos had purchased a mansion in South Florida for $79 million, a few months after buying a neighboring one for $68 million. Mr. Bezos is worth $161 billion, making him the world’s third-richest person, according to Bloomberg.

Mr. Bezos said in his Instagram post that he had “amazing memories” of Seattle and had lived there longer than anywhere else. “As exciting as the move is, it’s an emotional decision for me,” he wrote. “Seattle, you will always have a piece of my heart.”

The fearless journalists uncritically accepted the “emotional” explanation and did not include the word “tax” anywhere in the article. What’s new in Washington State, historically a state that was free from any personal income tax? A 7 percent income tax on long-term capital gains (wa.gov), starting in 2022:

The 2021 Washington State Legislature recently passed ESSB 5096 (RCW 82.87) which creates a 7% tax on the sale or exchange of long-term capital assets such as stocks, bonds, business interests, or other investments and tangible assets.

This tax only applies to individuals. However, individuals can be liable for the tax because of their ownership interest in a pass-through or disregarded entity that sells or exchanges long-term capital assets. The tax only applies to gains allocated to Washington state.

Washington State also imposes a death tax of 20 percent on residents who were successful in life. Florida’s constitution bars both income and estate taxes.

Even if the new tax was not a factor in Bezos’s decision to move to Miami, the move will have a big impact on how much revenue the Covidcrats of Washington State will collect from the new tax and, therefore, what they can spend on social justice initiatives (“The Democratic Party controls the offices of governor, secretary of state, attorney general, and both chambers of the state legislature” (source)). It seems like a failure of what we used to call journalism that the New York Times didn’t mention the dramatic changes in the Washington State taxation landscape (first the new tax and second the moving out of the biggest taxpayer).

Back in 2021, the state held a public hearing on House Bill 1406, which concerns a proposed Washington state wealth tax, Sen. Noel Frame, D-Seattle remarked at that hearing that there is a “really pessimistic view of the world to just assume someone would leave [Washington state].” “These are folks who have been deeply invested in our community,” (source)

The Myth of Millionaire Tax Flight, by Cornell sociologist Cristobal Young, pointing out that rich people won’t move in response to higher state taxes

“Lessons from Washington State’s New Capital Gains Tax” (by Kamau Chege; The Urbanist, June 2023): Taxing the rich works like a charm. … For decades, the wealthiest Washingtonians have gotten out of paying what they truly owe in state and local taxes. … One of the first lessons is that our state’s richest residents are much, much richer than we understood — and they are continuing to get richer at a faster rate than previously assumed. … working people know that private wealth is built on public infrastructure and public investments paid for by all of us — especially low-income folks who pay more than their share in taxes. … the richest people in our state, like Jeff Bezos and Bill Gates, have armies of accountants working to find tax loopholes and write-offs.

“Capital Gains and Tax ‘Fairness’” (Editorial Board; WSJ, 2021): “The Biden and Olympia tax increases on capital gains won’t matter to Bill Gates or Jeff Bezos, who are already rich and can hire lawyers to shelter their future gains.” [Maybe the WSJ envisioned that Bezos would switch to borrowing against his stock? But that doesn’t work in a high-interest-rate environment.]

New Hampshire has long been wrongly considered a “tax-free” state. There was no income tax on wages and, unlike other New England states, there was no death tax. But for successful people there was always a 5% tax interest and dividends to consider. The state’s web site, however, says that this tax is being phased out by 2027:

A 5% tax is assessed on interest and dividend income. The State of New Hampshire does not have an income tax on an individual’s reported W-2 wages.

Please note, recently enacted legislation phases out the Interest and Dividends (I&D) Tax starting at 4% for taxable periods ending on or after December 31, 2023, 3% for taxable periods ending on or after December 31, 2024, 2% for taxable periods ending on or after December 31, 2025 and 1% for taxable periods ending on or after December 31, 2026. The I&D Tax is then repealed for taxable periods beginning after December 31, 2026.

Tennessee did something similar recently. Note that New Hampshire does not have a sales tax and, therefore, I think it will join Alaska as the only state that is tax-free on both income and purchases. Maybe we’re getting closer to the glorious age of a land value tax!

How is everyone’s pre-Kwanzaa candle-lighting going this week? The Righteous are showing their commitment to stopping Jew-hatred by wishing everyone a Happy Hanukkah and, oftentimes, bringing out a menorah to sit in front of next week’s kinara. This is a little strange considering that the official Hanukkah narrative concerns some Jews whose policies were similar to those we decry in Afghanistan and Iran, i.e., forcing people to obey religious laws. Maybe the unofficial narrative is even more upsetting from the point of view of of a modern American holding correct views? From a professor of history at the University of Tel Aviv, “Religious Persecution or High Taxes? The Causes of the Maccabean Revolt against Antiochus IV”:

The issues of tax increases and royal appointments to the High Priesthood arise repeatedly throughout 2 Maccabees—always in conjunction with one another, and always decried by equating royal appointments with unworthy candidates. Because of the account’s emphasis on piety, these denunciations have been discounted by modern commentators, but if we read through 2 Maccabees’ culturally-conditioned narrative codes, the argument presented is perfectly rational—and plausible. The Seleucids’ attempt to control the appointment of the Jerusalem High Priests was indeed an innovation introduced by Antiochus IV, who exploited his appointees’ weakness—their lack of dynastic legitimacy—to extort sharp tax rises from them.

Like all popular revolts in ancient times, its principal cause was the newly-imposed high taxes.

Dying in a fight against high taxes struck no symbolic and no emotional chords in Judean culture—conversely, dying for the Law did. The account of the suppression was reshaped using a narrative pattern that is well documented in Babylonian literate culture: righteous kings enforced divine law, and wicked kings violated it.

Here’s an example of a politician who promises tax increases and also commemorating a tax revolt:

President Joe Biden is condemning growing antisemitism in remarks for a Hanukkah reception at the White House that will include a menorah lighting and blessing. https://t.co/j1Ph1dEVOa

In short, seemingly everyone who wants to increase the percentage of the U.S. economy devoted to taxation is lighting candles and partying during this pre-Kwanzaa holiday celebrating folks who fought against a tax increase.

Meanwhile, back in my home town of Bethesda, Maryland and actually at the high school from which I dropped out, some drama:

An example of what happens when a town is overwhelmingly dominated by supporters of Donald Trump.

Quite a few folks took issue with my statement that the consummate DC-insider suburb of Bethesda was primarily populated by Republicans…

Separately, who wants to bet that the author of “Jews Not Welcome” is, in fact, a Jew? The phrasing seems rather decorous for a Jew-hater. Would an actual Jew-hating Nazi (e.g., Donald Trump) say “Jews: Please don’t come to my cocktail party”? (See also “US-Israeli teen convicted of threats against Jewish centres” (BBC) for what happened when threats blamed on Trump supporters were investigated.)

Oh yes… to readers practicing Jewcraft… Happy Hanukkah!

I was chatting with a Dutch friend on WhatsApp on Thanksgiving Day, reminding him that we were celebrating our theft of an entire continent from the benevolent peace-loving Earth-preserving Native Americans. I shared a photo from the morning golden retriever walk:

For his part, he shared the European perspective: “There are two ways to live life. Short and violent or long and miserable.”

What else did I learn? “The left-wing parties control Dutch cities and say that they want immigrants to Holland, but don’t want the immigrants congregating in the cities that they rule. So they’ve been trying to force immigrants to settle in the conservative country towns. That hasn’t worked because the provincial towns have refused to provide free housing for migrants. So the Hague just passed a law forcing the country towns to take these immigrants.”

What are the Dutch with money doing? “Moving to Italy,” he responded. “The Italians let foreigners who move there pay 100,000 euro per year in tax. After that you can have 100 million euro in capital gains, dividends, etc. and they won’t even ask about it. It’s actually better than moving to a Caribbean tax haven because you get rebates on all of the withholding taxes on dividends because Italy has a tax treaty with the Netherlands.” (fact check: the scheme seems to have started in 2017) He said “You have to make sure that you don’t stay more than 182 days per year in the Netherlands or have kids in school here. Like New York State chasing after people who move to Florida, the Dutch government will try to find any excuse it can to continue collecting taxes. But it is really not a hardship to live in a Tuscan villa.”

Separately, the newspapers that warned us of the fascist takeover of Italy have gone silent regarding Giorgia Meloni’s dictatorship. Based on this Reuters article, it looks like the main program of fascism is stoking inflation via bigger government:

Italy’s new right-wing government signed off on its first budget in the early hours of Tuesday, a package focusing on curbing sky-high energy bills and cutting taxes…

Next year’s budget deficit is targeted to fall to 4.5% of gross domestic product from 5.6% this year. The package is still expansionary because under an unchanged policy scenario the deficit ratio was headed for 3.4%.

The budget contains almost 35 billion euros ($35.95 billion) of increased spending or tax cuts. Some 60% to be financed through increased borrowing.

Over 21 billion euros to help firms and households pay electricity and gas bills, mainly through subsidies for energy-intensive firms and low income families.

Next year Italians will be able to draw a pension from the age of 62 provided they have paid in at least 41 years of contributions.

That compares with the current rule, put in place for just this year by the previous government, allowing people to retire at 64 provided they have worked for 38 years.

The budget also extends to 2023, with adjustments, an early retirement scheme for women. Beneficiaries will be able to draw a pension at 58 if they have at least two children, at 59 with just one child, and otherwise at 60.

So, just like Americans under transferism, the Italians under fascism are going to work less and spend more!

Related:

The Italian program wouldn’t work for a U.S. citizen, who must continue to fund whatever Joe Biden dreams up even if he/she/ze/they no longer lives in the U.S. See “How Puerto Rico Became the Newest Tax Haven for the Super Rich” (GQ) for how the Manhattan rich go “Florida squared”.

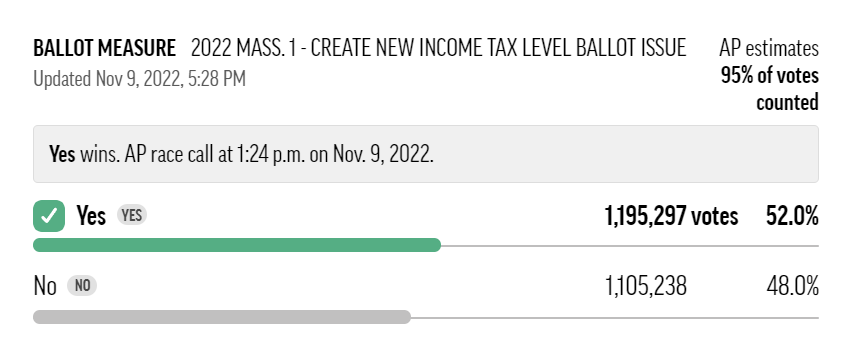

People in Maskachusetts say that they’re “progressive”. Very few earn more than $1 million per year. Why, then, did more than 1.1 million people vote “no” on a constitutional amendment that would allow the state to ding the rich (more than $1 million/year in income) at a 9% rate instead of the 5% flat rate that prevails for the peasantry?

“Massachusetts passes Ballot Question 1 (Millionaire’s tax), AP says” (MassLive):

We are informed that it is only Republicans and married white women who are so stupid that they vote against their own interests. There are hardly any Republicans in Maskachusetts and a lot of the married white women have taken advantage of the state’s no-fault divorce system to head for a profitable exit. This ballot measure should have passed by at least a 30-point margin, not a 4-point margin.

How can we explain the race being close? How could so many peasants be against rich people getting closer to paying their fair share? (which actually should be at least 13.3% because that’s what rich people in California pay for state income tax)

It can’t be because people were concerned that inflation would lift them from the old 5% bracket into the new 9% one. The text of the ballot question explains that there will be annual inflation adjustments.

Separately, this was a great outcome for the luxury real estate industry in Florida! Rich bastards will need to pull up stakes in MA before the end of December 2022 if they object to paying their fair share. (See Relocation to Florida for a family with school-age children )

Finally, the tax bump won’t be great for alimony defendants. “New Guidance on the Intersection of Alimony and Child Support” (Burns Levinson law firm, August 2022), quotes the law: “the amount of alimony should be determined with reference to the recipient spouse’s need for support to allow the spouse to maintain the lifestyle enjoyed prior to the termination of the parties’ marriage.” Alimony is now tax-free to the plaintiff and not deductible for the defendant. since most couples spend close to 100 percent of their income, the only way for a divorce plaintiff to enjoy the marital lifestyle is to collect close to 100 percent of the defendant’s income). So in setting the order, the judge has to make some assumptions about what tax rate the defendant will pay in order to figure out what the after-tax income is and make sure not to order the defendant to pay more than 100 percent of income. A high-income defendant in Massachusetts will have less after-tax income, but the court order to pay based on the old tax scheme can’t be changed without the defendant starting a “modification” lawsuit that could take years and cost $millions in fees to resolve.

Related:

Colorado FF, a proposition to hit those earning more than $300,000 per year with a stealth higher tax rate by reducing the deductions they can claim (it passed because lots of folks earning less than $300,000 per year voted for it!)