In the spirit of “Go To Statement Considered Harmful” by Edsger Dijkstra, renowned sourpuss…

“Hundreds of Billions in Loans Didn’t Make a Dent in Global Poverty” (Wall Street Journal):

Microfinance, loans issued in communities not served by traditional banks, would help poor people in developing countries start businesses and work their way toward prosperity. That was the goal of Muhammad Yunus, a U.S.-trained economist, who pioneered the practice in Bangladesh during the 1970s.

“In a poverty-free world, the only place you would be able to see poverty is in the poverty museums,” Yunus told his audience in Oslo in 2006 when he accepted the Nobel Peace Prize for his work.

Led by the adage of “doing good while doing well,” microfinance lenders have since advanced hundreds of billions of dollars to poor people in countries from Albania to Zimbabwe. Prominent voices including Hillary Clinton and Natalie Portman told inspiring tales of women entrepreneurs lifting the fortunes of their communities. Along with easing poverty, microfinance aimed to expand access to education and end gender inequality.

That was the dream, including for yours truly (I kicked in some money circa 2000 to a web-based microfinance portal). What has been the reality?

Academic studies, including randomized controlled trials, have found that microfinance doesn’t improve the economic conditions of most borrowers. Economists found excessive microfinance lending has set off repayment crises for borrowers in half a dozen countries, including Bosnia, India and Cambodia.

High interest rates, which can top 100% in some Latin American countries, and pressure tactics by loan officers have been tied to suicides, homelessness and children pulled from school to work. Rather than using the loans to invest in small businesses, many borrowers spend the money on medical expenses and other necessities.

Does failure to achieve stated goals have an effect on nonprofit organizations? No.

The hardening evidence of microfinance’s failure to alleviate poverty should have led to a rethinking of its use as a development tool, said Rafe Meager, an associate professor at the University of New South Wales in Australia, who has studied the academic research on microfinance.

“There still hasn’t been this kind of reckoning in a serious way,” Meager said.

The average microfinance borrower in Cambodia owes more than $3,900, nearly three times the median annual per capita income. Average debt per borrower is more than $6,000 when including small loans from microfinance lenders that are now commercial banks also providing other financial services.

Microfinance’s breakneck expansion in Cambodia in the early 2010s coincided with a government push to formalize land ownership. Contrary to Yunus’s vision that debts shouldn’t be collateralized, most of Cambodian microfinance loans greater than $3,000 are secured by a borrower’s land, which is the main hard asset for most poor families.

What happens when we throw AI into this mixture? Some people were already poor because their skill levels were too low to compete in a globalized economy. Do they get a boost in value for a while, at least, because the Optimus-style robots won’t be ready until well after the AI brains are perfected? Or do already-poor people in poor countries become further devalued by AI because they’re being partly paid for the use of their brains? Or, on the third hand, do they get a boost in income because they’ll use AI to become much more productive?

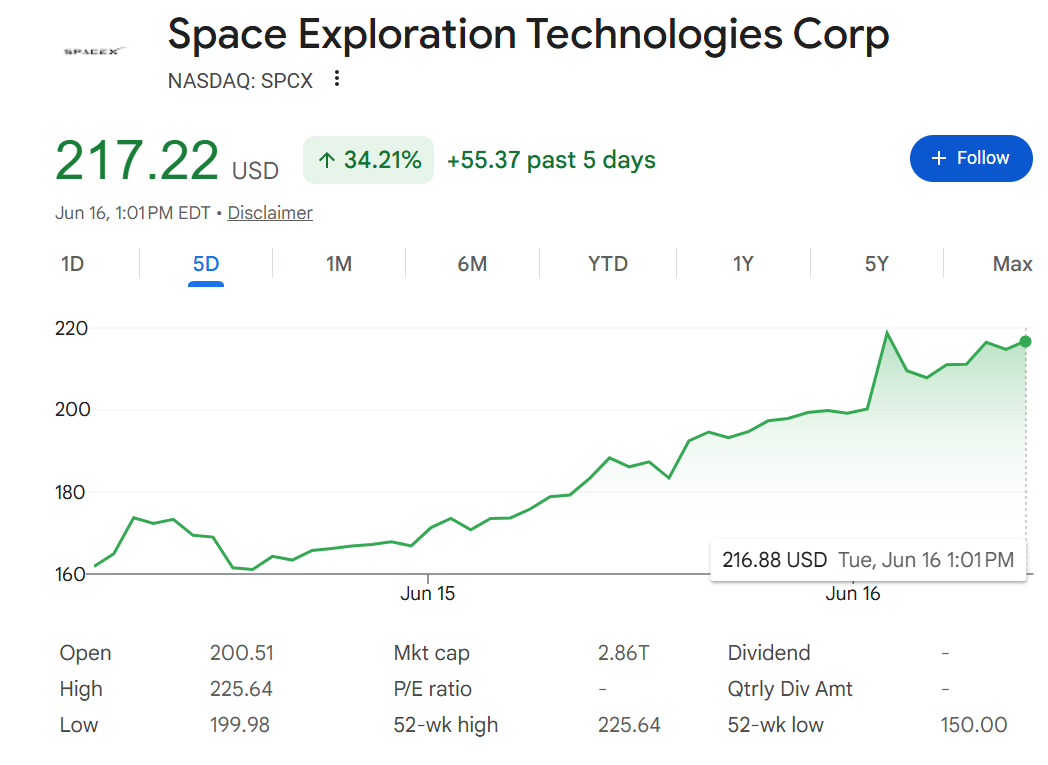

Separately, now that Elon is well on his way to a second $trillion, why isn’t he loaning Bosnians, Indians, and Cambodians however much money they want?

Poor people will continue to be exploited:

– As cheap recruits for armies

Eg https://www.reuters.com/world/africa/african-nations-tiptoe-around-recruitment-citizens-by-russian-networks-2026-03-15/

– As providers of surrogacy services

– As organ donors

– for prostitution

The American poor are lucky to have relatively benign overlords, the rest of the world, not so much.

Commercial surrogacy (illegal in nearly all of Europe) is a total scam against the people who do the actual work (not to say “mothers” since that would be hate speech. A 2014 NYT article reported that the paper shufflers get the majority of the money paid when someone buys a baby. See https://philip.greenspun.com/blog/2014/09/18/payment-for-surrogate-mothers/

SpaceX closed at $202, up only 5% for the day, so maybe Elon can’t afford to bail out all of the world’s unsuccessful humans.

Don’t feel too bad for poor Elon. Even at just $202, SpaceX’s market cap is higher than the combined value of CocaCola + McDonald’s + Disney + Nike + Starbucks ($0.9T).

So the microfinance loans are a lot like the Covid SBA loans and the “Great Recession” auto industry loans – none will be paid back.