The Florida Democratic primary for Senate is on August 18. One baffling aspect: Alex Vindman not only moved to Florida during the tyranny of Ron DeSantis (in 2023), but now the foreign-born carpetbagger is trying to take away a Black woman’s job in the Senate primary. Vindman says that he has a 15-year-old daughter:

I'm running for Senate to lower your costs.

So that young people like my 15-year-old daughter can afford to build a life in Florida. So that people on fixed incomes like my 94-year-old dad can afford to stay here. pic.twitter.com/HaQqU95FRG

Why would a noble liberal migrant move to Florida? He talks, above, about a 15-year-old daughter. The goal is for this girl to stay in tax-free Florida for the rest of her life, thus denying the virtuous Democratic-ruled states of much-needed tax revenue. Said daughter can’t be safe in Florida because life-saving abortion care isn’t available after 6 weeks of a pregnant person’s pregnancy (Vindman is on record as a passionate supporter of abortion care). Because she’s under 18, life-saving gender-affirming care isn’t available. Vindman is literally killing his/her/zir/their daughter. State law won’t change to became safe even if the carpetbagger wins the Senate seat.

Most confusing, for a member of a party that champions the advancement of Americans identifying as “women” and the advancement of Americans identifying as “Black”, the apparently white male carpetbagger is trying to take away the important Senate job from a Black woman:

The number of leadership jobs in the U.S. is more or less constant (absolutely constant with respect to the number of senators). The only way for members of victimhood groups to advance is for white heterosexual males to retreat into subordinate roles. How can there reasonably be even a single white heterosexual cisgender male running for any office as a Democrat? And how could a virtuous Democrat reasonably make the decision, in 2023, to move to any Red State? (Vindman even moved an elderly parent to Florida, thus avoiding paying state estate tax and preserving the “generational wealth” that Democrats oppose.)

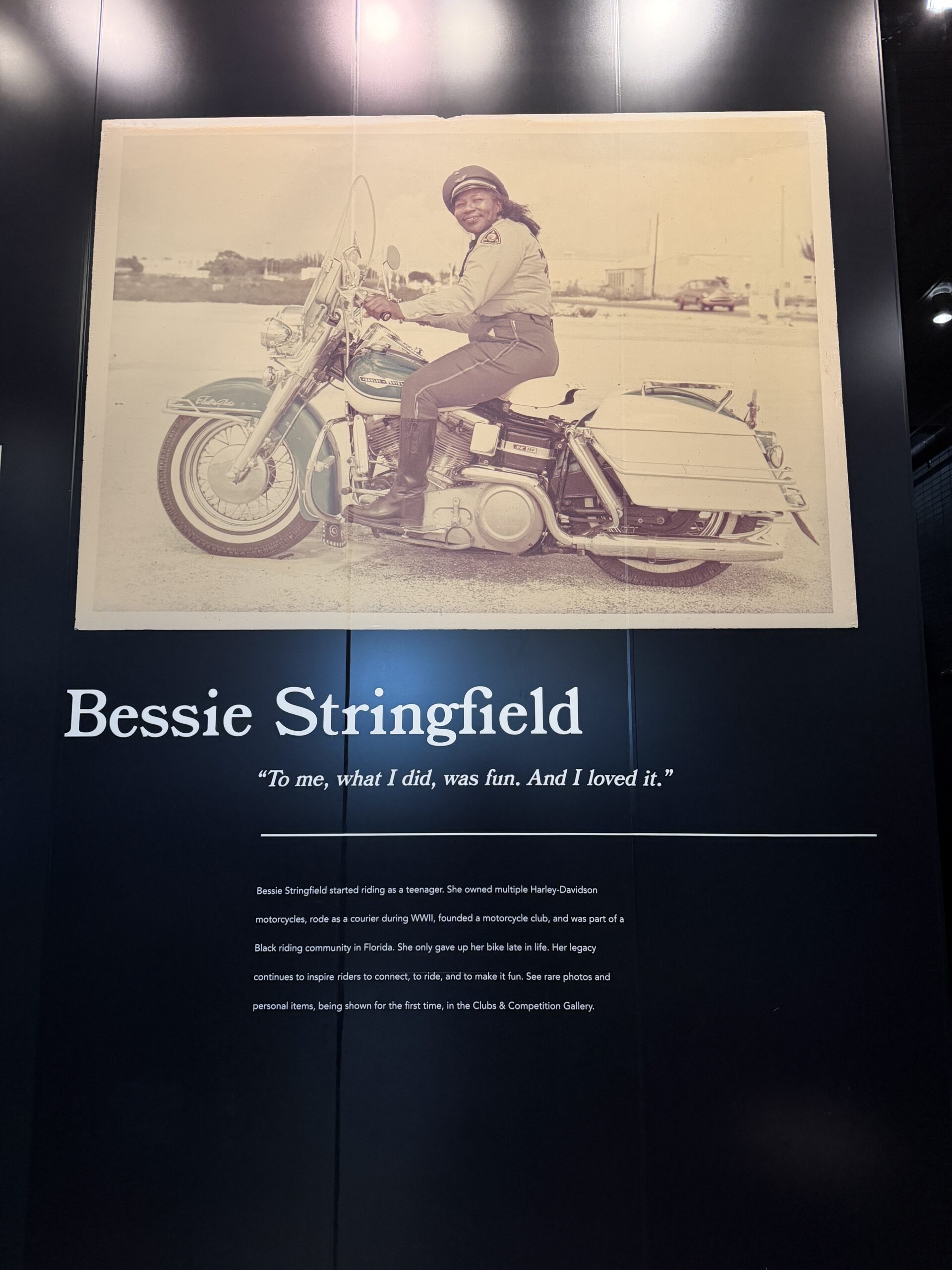

What was new for 2026? The entrance features just one person, “part of a Black riding community in Florida”:

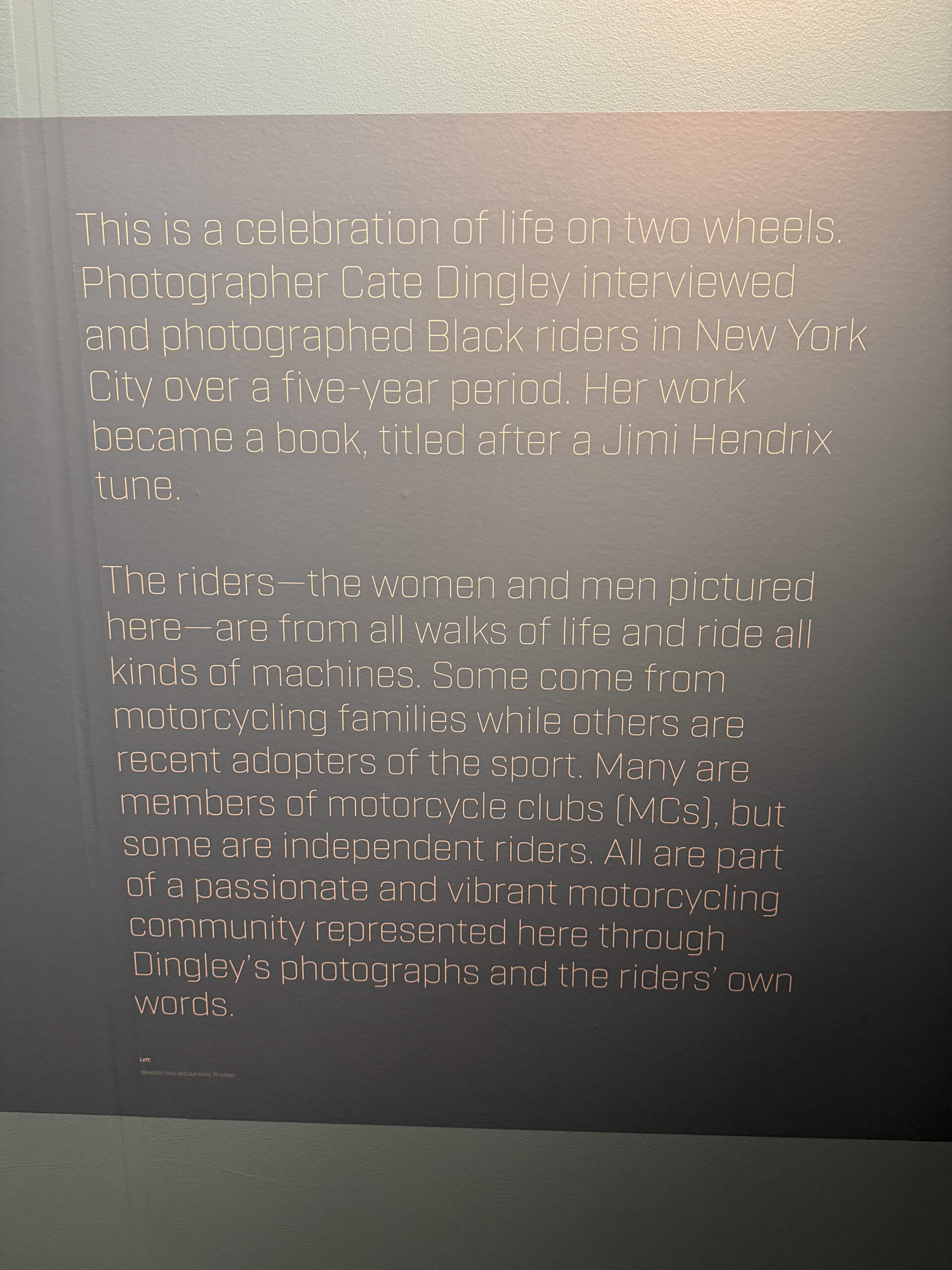

An upstairs gallery had an exhibit limited to photos of “Black riders in New York”:

What’s interesting about the above centering of the Black experience on Harleys? I don’t remember seeing any Black visitors inside the museum ($26/person; median income for a Black-headed household in Milwaukee is about $37,000/year), but we heard tons of conversations in Spanish.

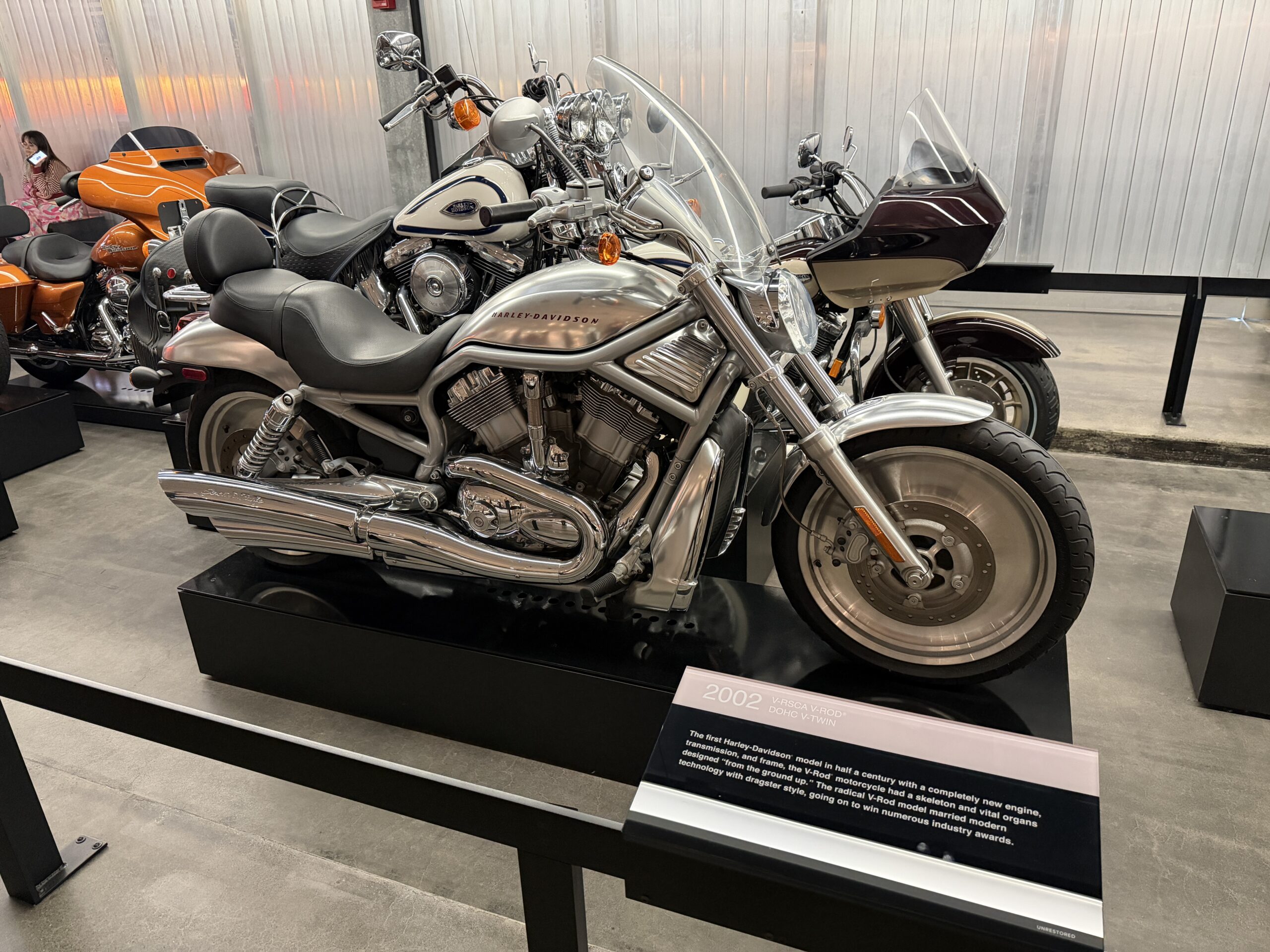

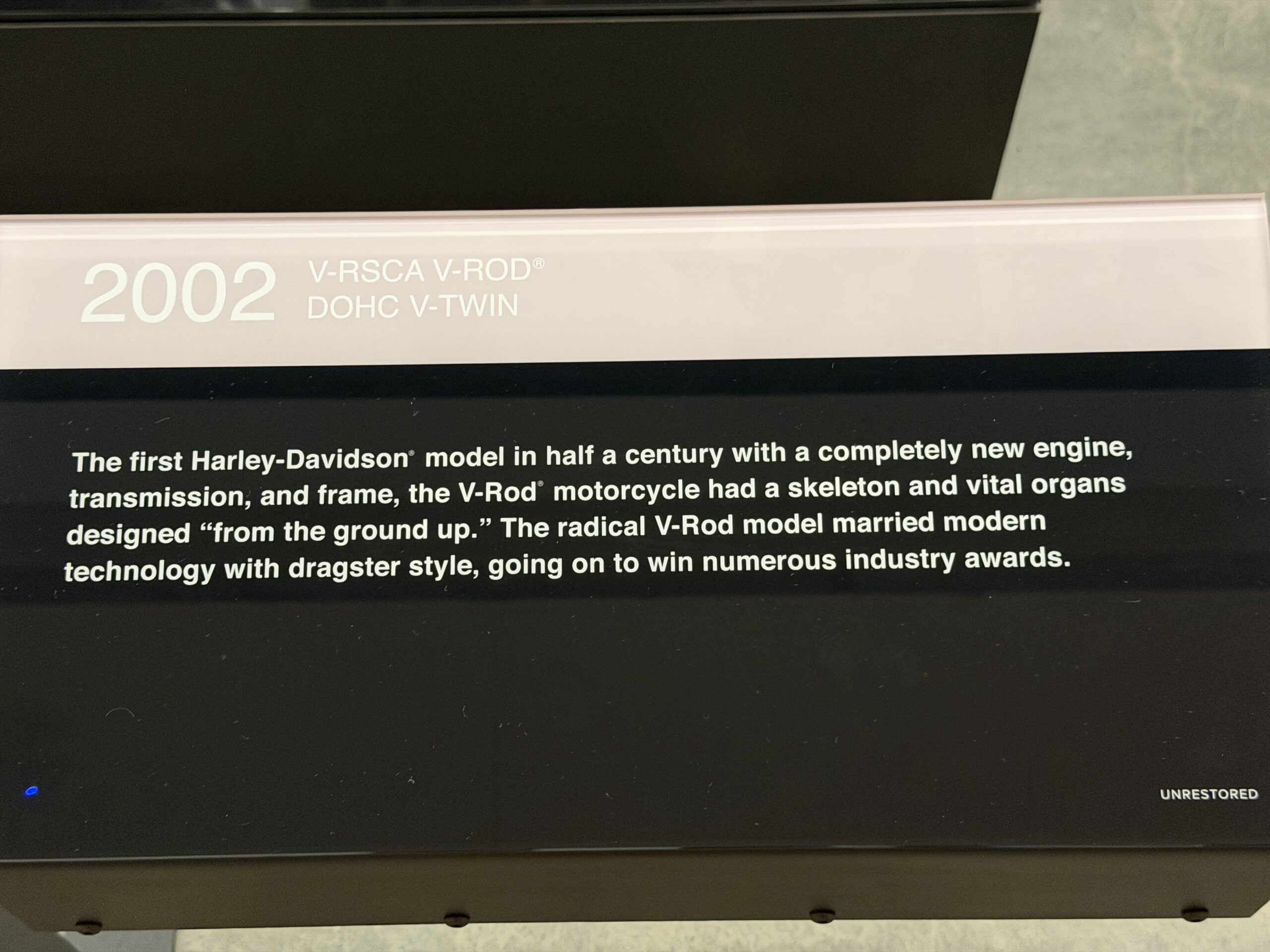

Photos of some parts of the museum not included in the 2024 post…

Biker chicks in the old days:

From roughly the same era:

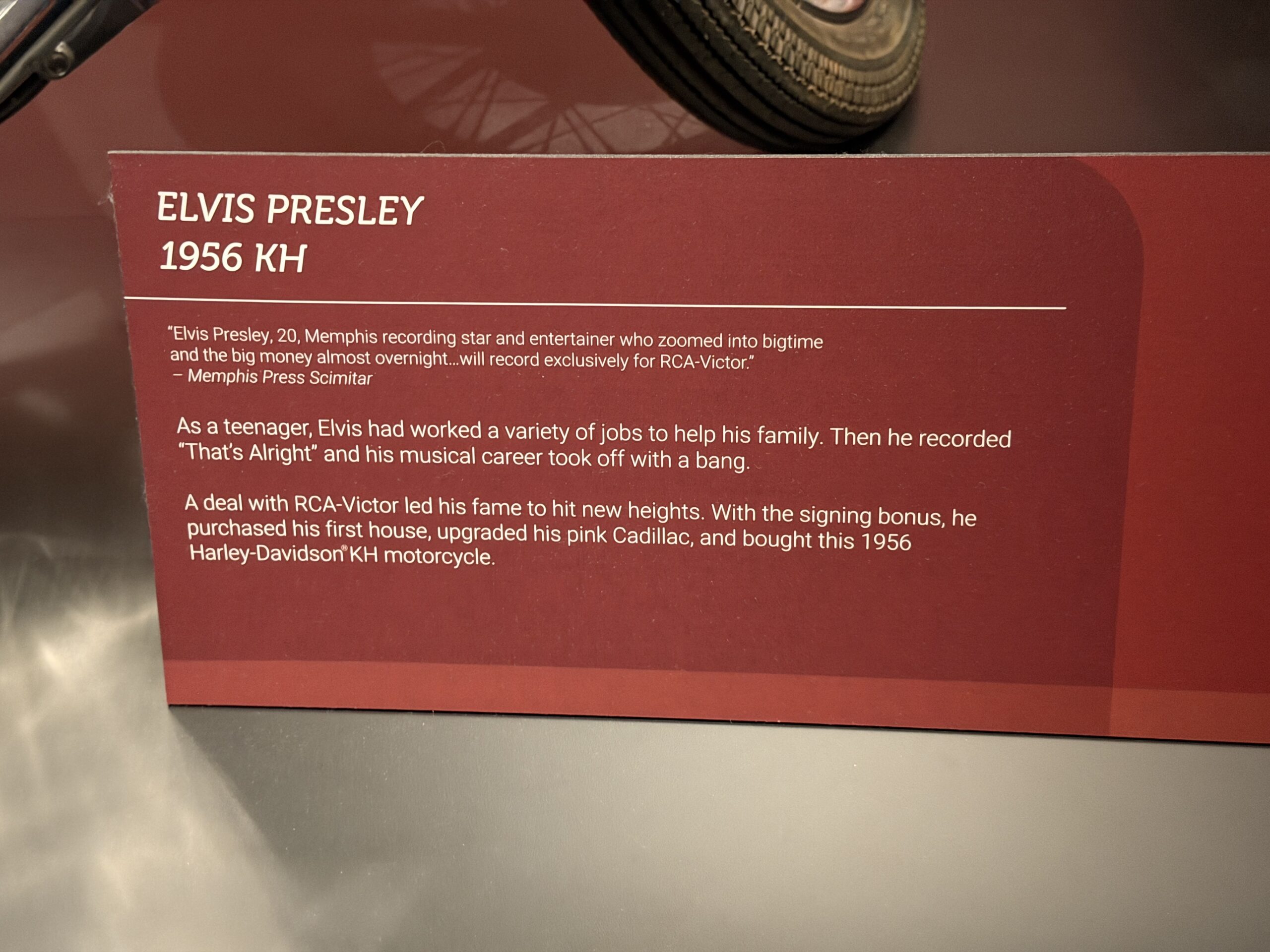

Elvis Presley, one of my candidates for Greatest American Ever, purchased a Harley with the income from some of his earliest success:

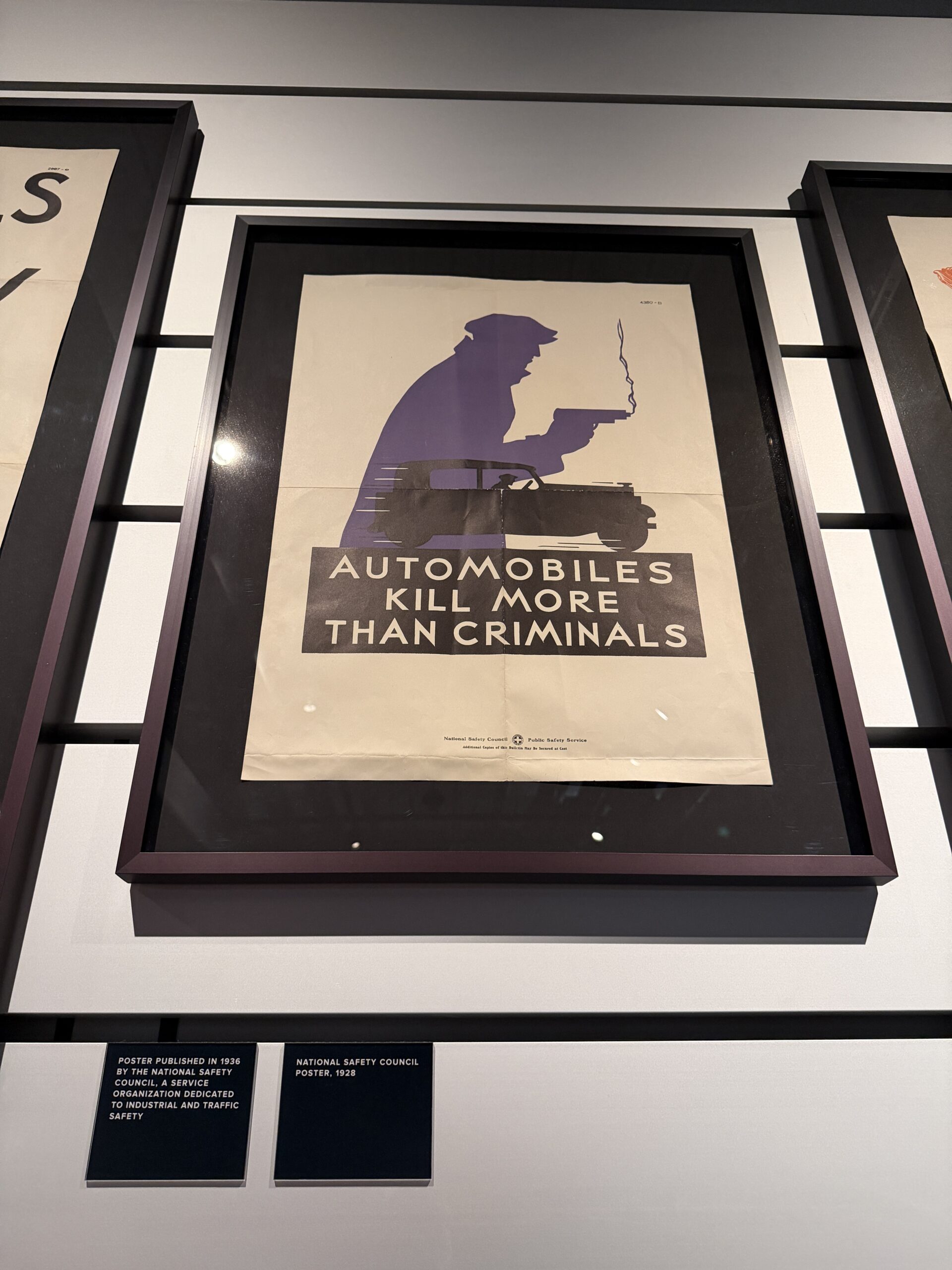

This might have been the inspiration for New York Times coverage of various European vehicle ramming events: it is the “automobiles” doing the killing.

Early voting has begun for the Florida primary election. I’m registered as a Republican (can’t go back to the Party of Fauci!) and the choices are a little unsettling.

Choosing a governor would be easy if Ron DeSantis had endorsed someone, but the GOAT has kept quiet.

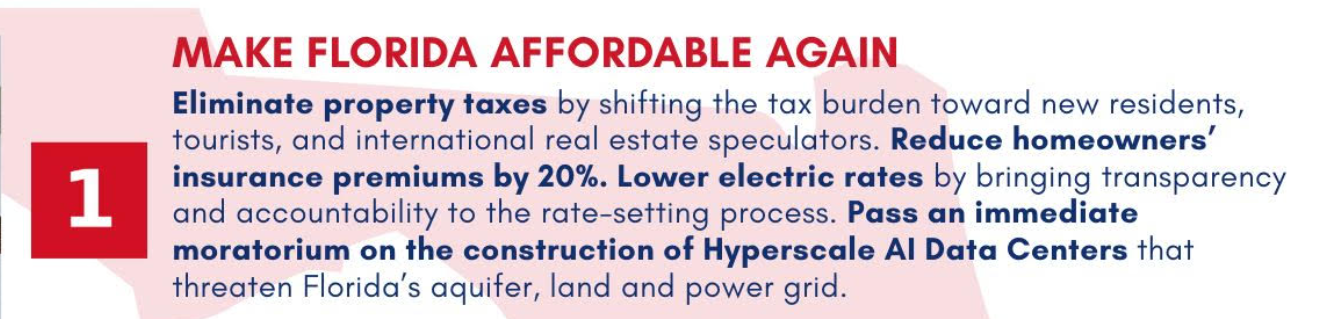

Let’s start with Paul Renner. He attended a liberal arts college, served in the Navy, and then went to University of Florida law school. He was Speaker of the House during part of the DeSantis administration. His campaign web site frankly is either the work of an insane person or, perhaps, a smart person who believes that everyone who reads it is stupid.

“Shift the tax burden to international real estate speculators”? How can that work in most of Florida’s 67 counties? International buyers are supposedly roughly 5% of the total dollar volume in Florida, but they’re heavily concentrated in a handful of counties.

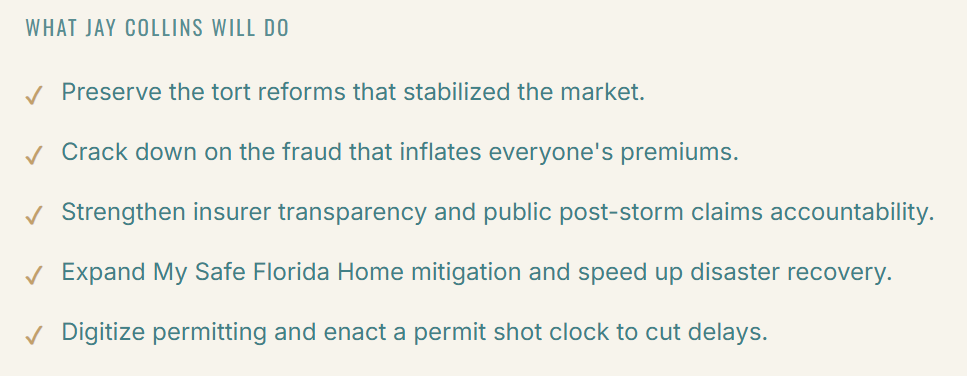

Jay Collins is the current Lieutenant Governor, appointed about a year ago by Ron DeSantis when Jeanette Nuñez left to become head of Florida International University. He has a distinguished military career, including serving as a Green Beret. His campaign site is a little less insane. He wants to exempt a larger amount of homestead residents’ home value from property tax, which I think is a terrible idea (there is already a huge discrepancy between what long-term residents pay and what new arrivals or second-home owners pay because homesteads are taxed at their purchase price plus a maximum of 3% per year appreciation or CPI, whichever is less; DeSantis is at risk of losing his GOAT title, in my view, for trying to further derange Florida’s property tax system via a ballot question in November.).

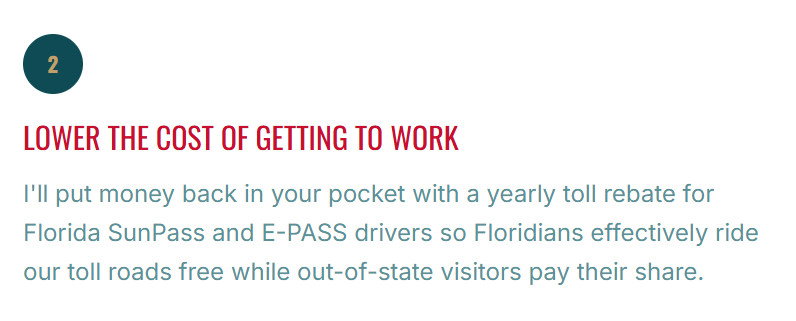

This seems like a terrible idea for anyone who hates traffic jams:

Collins promises to lower insurance costs, but not by a specific percentage and mostly via the “tort reforms” (making it tougher to sue insurers and get all legal fees paid) that were enacted in 2022 and actually did bring down premiums:

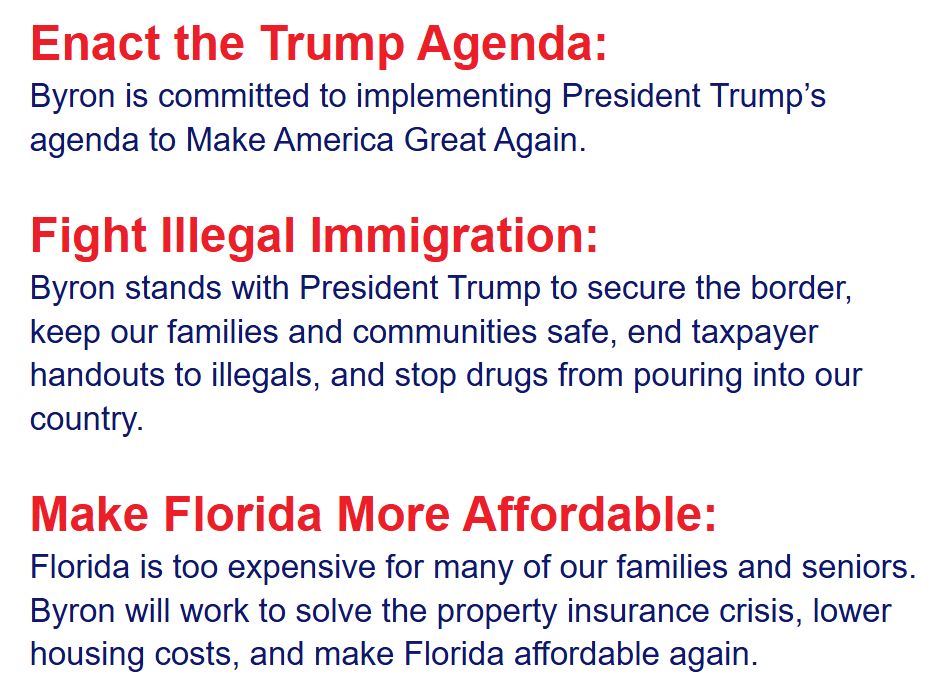

Next we turn to Byron Donalds, currently in Congress representing some of the world’s richest people (Naples, Sanibel), which is ironic because Wikipedia says that he grew up in Crown Heights, Brooklyn under the care of “his single mother.” His issues page:

“Enact the Trump Agenda”? How is the governor of Florida going to surrender to the Islamic Republic of Iran?

“Make America Great Again”? That actually works against Florida’s interests. What helps Florida is when New York City, Boston, Chicago, San Francisco, and Los Angeles fall apart and/or go into a Fauci-suggested lockdown. If the foregoing centers of American wealth were as nice as West Palm Beach and Sarasota, there would be no reason for rich people to move to Florida.

“taxpayer handouts to illegals”? Florida doesn’t do a lot in this area, I don’t think, other than pay for health care when the undocumented show up at emergency rooms (and how would we cut that off?). The real solution, though, would be to help the undocumented migrate onward to New York and Maskachusetts where they’re guaranteed a taxpayer-funded lifestyle. Donalds doesn’t seem to propose that.

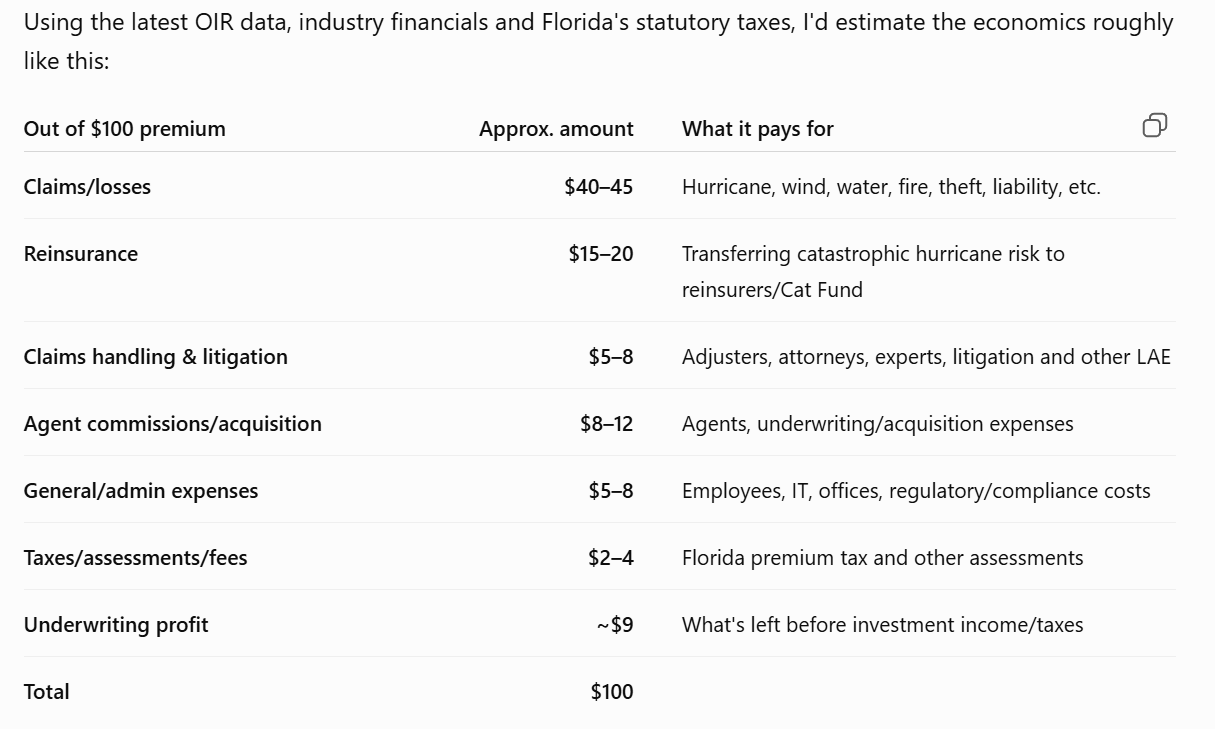

“property insurance crisis”? Maybe we could lose another 10% on premiums if all disputes between homeowners and insurers were moved into a specialized and streamlined resolution system staffed by arbitrators who actually knew something about home construction and repair. Beyond that, though, how is it a “crisis” if rates are higher than in some other states because of hurricane risk? ChatGPT’s estimates of available juice to squeeze from the insurance lemon:

(Look how expensive agents are! Maybe this is an argument for socialism. If there were just one insurance company, run by the state, rates could come down by about 20% because there would be no agents and no underwriting profit! What could go wrong?)

I hate to say that the candidate endorsed by Donald Trump is the least insane of the above, but perhaps he is! Mostly, I’m saddened that the only way to win an election in the U.S. seems to be promising people free stuff, absurd stuff, and impossible stuff. Average IQ in the U.S. is falling, but maybe this isn’t a new phenomenon. After all, when Lyndon Johnson and Congress in the 1960s decided to simultaneously expand the welfare state (Medicaid, Medicare, public housing, food stamps) open the borders (Hart-Celler), that was implicitly a promise that the U.S. would be infinitely rich forever. When FDR and Congress set up Social Security in the 1930s and paid the first beneficiary 1000X what she’d contributed via taxes that was tantamount to a “free lunch” promise.

The choice for Senate is much simpler. DeSantis-appointed fifth-generation Floridian Ashley Moody is the incumbent and everyone seems to like her. (Well, maybe the undocumented don’t like her because she’s in favor of border security and, when that fails, ICE. If she were in the Islamic Republic of Michigan running against Abdulrahman Mohamed El-Sayed she’d probably try to deport him to Egypt.)

Wilton Simpson is running to retain his job as Agriculture Commissioner. I won’t be voting for his opponent, Matt Taylor, because he styles himself “Matt the Welder” and that reminds me of “Graham Platner the Oyster Farmer.” Also, Matt the Welder is opposed to “government aerial mosquito spraying”, according to ChatGPT. One of the great things about our life in Florida has been that we’ve cut our DEET use by 90% compared to when we lived in the Boston suburbs (tick-infested 7 months per year and horrific mosquitos for 3-4 months per year). If Palm Beach County wants to use an Airbus A380 filled with whatever kills mosquitos I am all for it! (see Indigenous Peoples’ Day and the Mosquito for a recommendation of a great book on how horrible this insect is; see also Kill them all (mosquitoes) with genetic engineering and let God sort out the mutant survivors) Note that ChatGPT might be hallucinating/lying. Taylor seems to be hostile to herbicides and perhaps some of his supporters assume that he will also be hostile to insecticides. Regardless, “welder” is too close to “oyster farmer” for comfort, unless of course one is a progressive female looking for some action…

There’s also a race for a judge. Schnelle Tonge v. Jacob Noble. Ms. Tonge is endorsed by a lot of Palm Beach County officials while Mr. Noble is endorsed by the police. Noble seems to have a lot more litigation experience, e.g., he’s admitted to practice at the U.S. Supreme Court, a federal appeals court, and three federal district courts.

Update: I biked over to Florida Atlantic University’s Jupiter (Abacoa) campus and voted early. There was a substantial staff and nobody in line. I was offered the opportunity to use the voting machine, which ultimately prints a paper ballot, in English, Spanish, or Haitian Creole. It seems that, in our infinite political wisdom, we’ve created a huge class of eligible voters (U.S. citizens) who can’t understand the most basic English. ChatGPT explains that someone might be a birthright citizen and never learn English due to being taken back to Haiti or wherever as a baby. The anchor baby returns at age 18, let’s suppose, and decides to vote. We also hand out citizenship to people who are over 50 without requiring them to pass the English test that is normally required for naturalization. Finally, unlike Australia, which bars the entry of the disabled as likely to become a burden on their overstressed health care system, “a qualifying physical or developmental disability or mental impairment can exempt a naturalization applicant from the English requirement.”

Once we’ve filled the United States with citizens who don’t speak English, a federal law requires that we facilitate votes from those completely-disconnected-from-legacy-Americans-by-language citizens. The Voting Rights Act, Section 203:

… citizens of language minorities have been effectively excluded from participation in the electoral process. Among other factors, the denial of the right to vote of such minority group citizens is ordinarily directly related to the unequal educational opportunities afforded them resulting in high illiteracy and low voting participation.

The language minority provisions of the Voting Rights Act require that when a covered state or political subdivision provides registration or voting notices, forms, instructions, assistance, or other materials or information relating to the electoral process, including ballots, it shall provide them in the language of the applicable minority group as well as in the English language.

The requirements of the law are straightforward: all election information that is available in English must also be available in the minority language so that all citizens will have an effective opportunity to register, learn the details of the elections, and cast a free and effective ballot.

There is some discrimination, according to the Justice Department!

Covered language minorities are limited to American Indians, Asian Americans, Alaskan Natives, and Spanish-heritage citizens – the groups that Congress found to have faced barriers in the political process.

Why not Arabic for the noble enrichers of Dearborn, Michigan who’ve brought their parents over? “Chinese” is the second-largest non-English language spoken at home after Spanish (Census), but no provisions are made to facilitate voting by immigrants from China or Chinese anchor babies who’ve recently shown up as adults.

It surprises me that the U.S. hasn’t completely melted down. The lowest-earning 50 percent of eligible voters pay 3 percent of federal income tax (i.e., they receive a 97 percent discount on the federal government services that they can vote to receive; it would make sense for them to vote for a daily federal government delivery of popcorn even if they think they’ll eat it just once per month). We make huge efforts to gather votes from people who aren’t able to speak English, who have a “mental impairment” (I guess that’s consistent with the 100% disabled Graham Platner almost being elected Senator), and who may have lived in the U.S. for only a few months (the anchor-baby-returns-to-birthplace scenario)), and who aren’t interested enough in or informed enough about voting to zip over to the polls (sending out vote-by-mail packages to everyone).

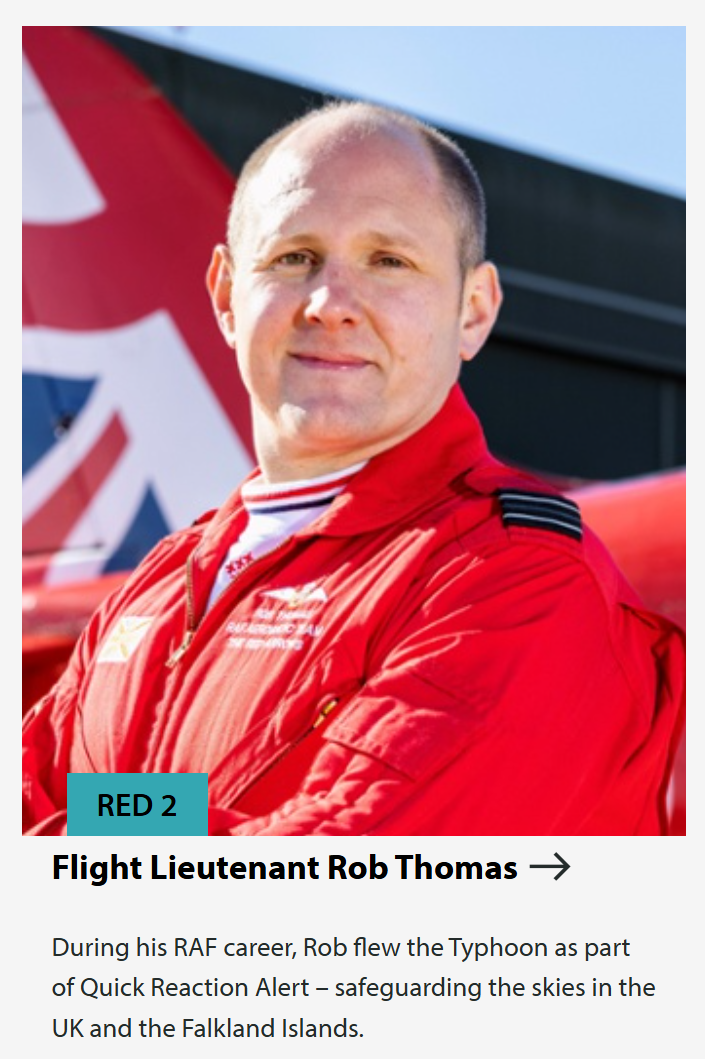

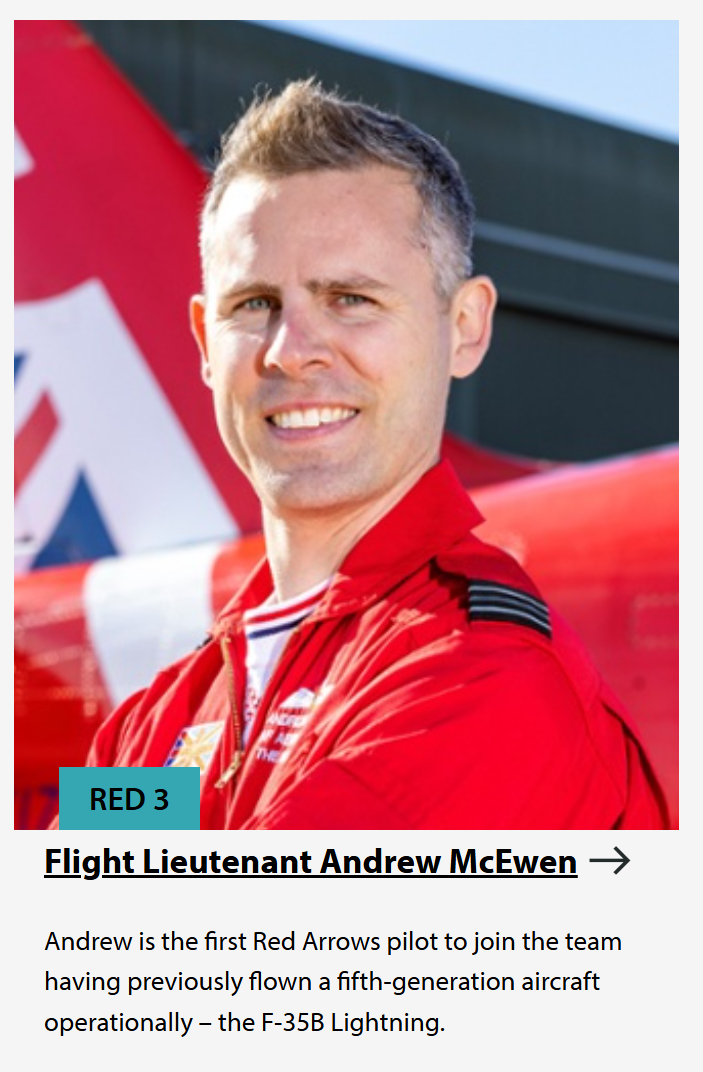

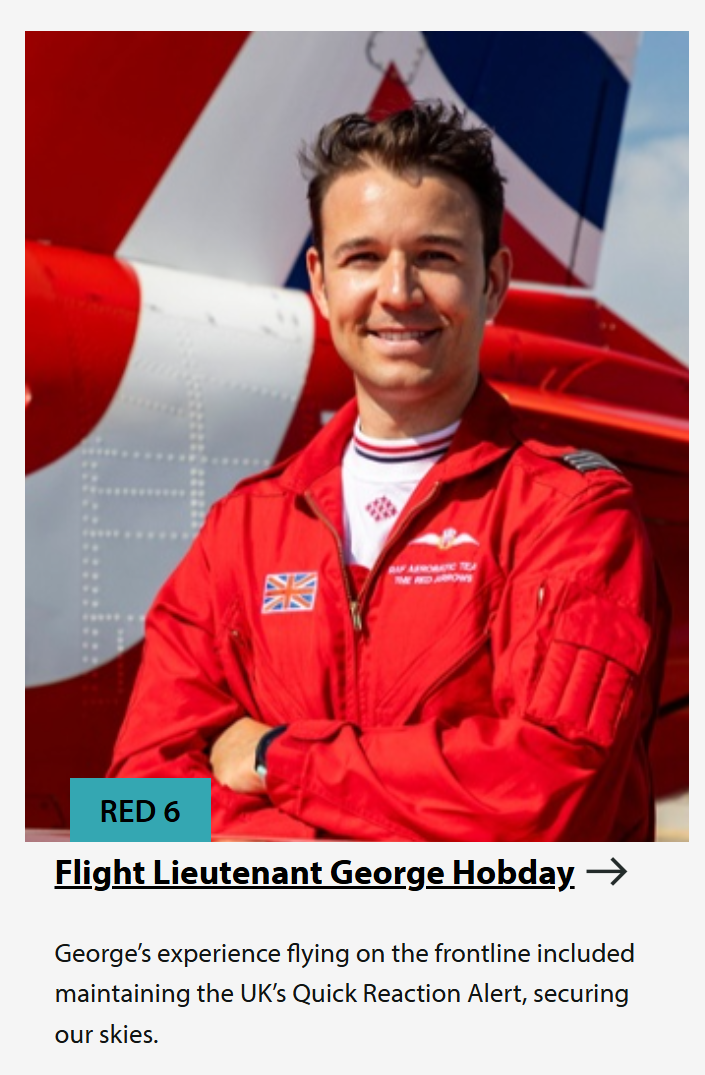

This was the first year that the UK’s Red Arrows appeared at EAA AirVenture (“Oshkosh”). It’s a quiet understated elegant display compared to what the Blue Angels and Thunderbirds put on and they fly the BAE Systems Hawk, a single-engine jet trainer from the 1970s. The Red Arrows have a “trademark Diamond Nine shape” but for whatever reason only 6 or 7 of them were able to fly at Oshkosh, depending on the day (during one show, a Hawk had to return to land due to a missing gas cap).

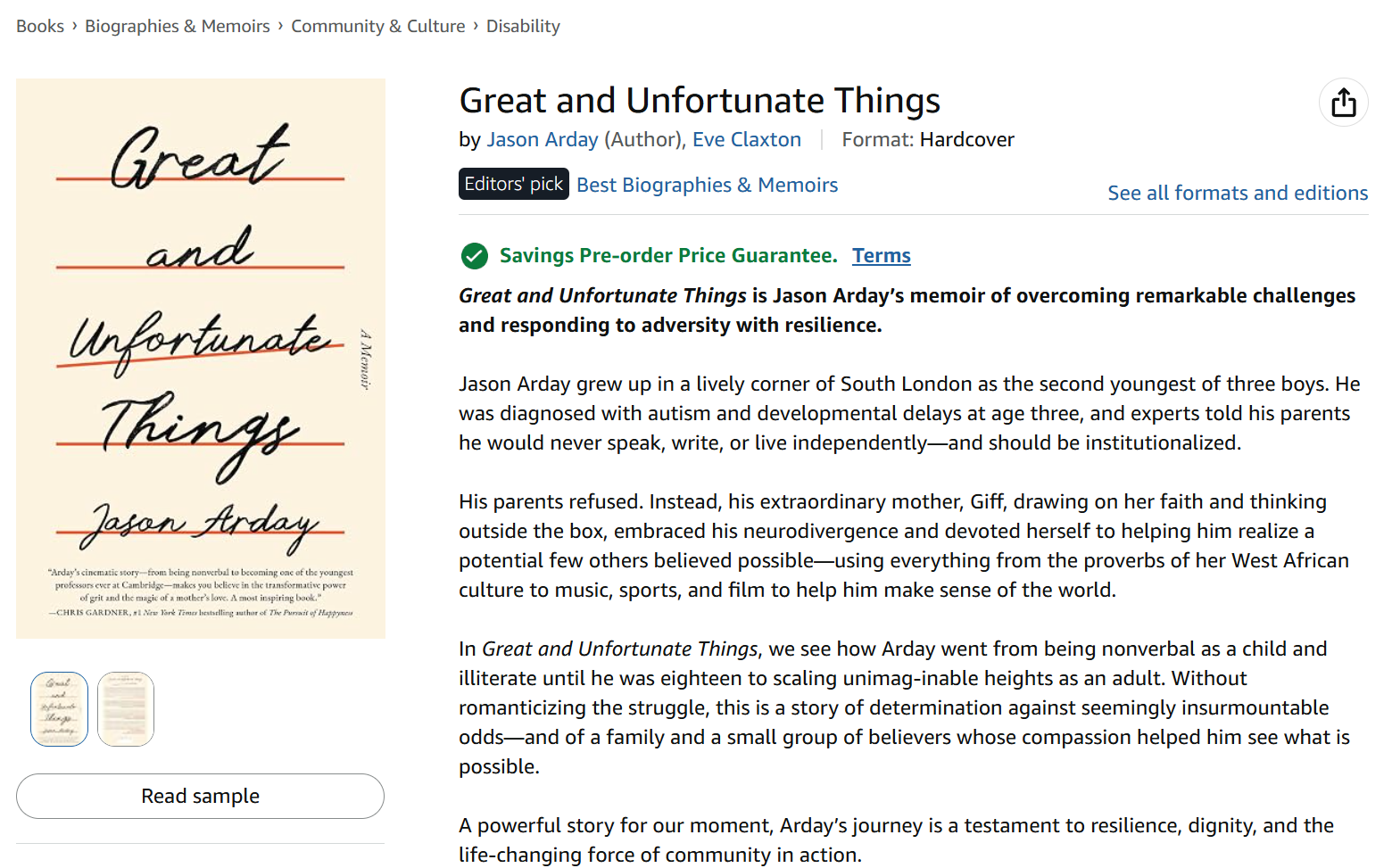

Who are the pilots? They appear to all be “legacy Britons” with names such as “Jon Bond” and “Rob Thomas”. As Keir Starmer pointed out (while wearing a mask, of course!), “Our nation’s diversity is one of its greatest strengths” (maybe when our copies of Jason Arday‘s autobiography show up we will learn that Prof. Dr. Arday, Ph.D. was at one time a Red Arrows pilot, which is certainly easier than running 30 marathons in 35 days):

Here’s the whole routine:

What else was interesting at the air shows? Jared Isaacman put the “Admin” in NASA Administrator by zooming around in his personal MiG-29:

In other “Don’t mess with NASA” news, the agency also brought one of its F/A-18s and also an F-15:

The Wisconsin National Guard was pathetic this year compared to 2025 in which they’d fire off a 155mm artillery round every 15 seconds. They also didn’t bring their tanker. Maybe the artillery rounds had to be shipped out to Ukraine and the tanker went to our surrender-slowly-to-Iran project? Fortunately, we haven’t had to turn over our Goodyear Blimps yet:

Check out the killer tail number:

Let’s definitely not give N1A to the Iranians!

Traffic after the evening air show wasn’t fun, so maybe stop at SOS Brothers for refreshments and music rather than being in the middle of a Ceuta-style wave of humans:

Legal filings from the 2019 dispute also give some of the history between EAA and the brothers:

In 1996, Winnebago County took 1.2 acres of land from the brothers through an eminent domain land acquisition. The move was part of the federally sanctioned Airport Improvement Program to increase the space between EAA crowds and air show flights.

The brothers sued after the county later turned the land over to EAA, which began using it for its own concessions. The county and state paid a combined $800,000 to settle the lawsuit.

Circling back (so to speak) to the Red Arrows, here are Jason Arday’s official portraits as a team member:

The smartest people in the Islamic Republic of the UK hired Jason A. K. Arday to hold a professorship at Cambridge University in 2023, which is a huge appointment (what we call “assistant professors” they call “mere lecturers”). He’s been in the news recently for Claudine Gay-style plagiarism combined with an unusual life story. From “Icarus in the Faculty Lounge” (The Atlantic):

According to a cover letter that his agent sent to publishers at the time [2023], Arday’s book, to be titled Great and Unfortunate Things, would be “an awe-inspiring tale of near mythic proportions.”

That now appears to be an understatement. Arday’s story was indeed astonishing: As a toddler, he was diagnosed with autism and developmental delays; he didn’t fully speak until the age of 11; he learned to read and write only as an adult. Arday’s parents are Ghanaian immigrants [enrichers!]

Arday’s grad-school alma mater, Liverpool John Moores University, which first received direct complaints about the dissertation last fall, did its own investigation and cleared Arday of wrongdoing. “A confidential procedure was conducted,” the university told me in a statement. “Professor Arday’s PhD still stands.” But some of Arday’s other academic papers had potential problems too—and they seemed much worse than the mere borrowing of language. Quotes from structured interviews that Arday claimed to have performed closely resembled those used by other researchers; parts of some interview responses also reappeared across different studies under Arday’s name, attributed to different people. This duplication, if deliberate, would be something other than plagiarism—it would be academic fraud.

Might this be Donald Trump’s fault?

Some of the people who were going after Arday had a political agenda. Cofnas, the philosopher who put Arday’s dissertation through a plagiarism checker last month, argues for a “hereditarian revolution” based on the idea that innate differences in intelligence and other traits exist across racial groups. (He also claims that “the humanities and much of the social sciences have been slain on the altar of DEI.”)

Everyone loves an abuse survivor:

The doctors who assessed him as a toddler told his mother that “there’s no one in there” and that he was “no better than a vegetable.” Even his speech therapist wasn’t optimistic that he’d ever learn to talk. (At one point, she also physically abused him, the memoir says.) As a boy, Arday rocked and hummed and banged his head until he bled; he slammed cupboard doors and smeared his feces on the walls. Yet still, eventually, he started to verbalize.

Arday is nearly deaf in one ear; he’s dyslexic; he finds simple math befuddling; he has “marked difficulties” with memory, reading, and processing skills. As a teen, he was beaten so severely by a group of kids his age that he became an epileptic. To make his way through secondary school while—by his own account—illiterate, he needed ample help: support assistants who sat beside him in class and took notes on his behalf.

(What good are “notes” if a person is “illiterate” (unable to read)?)

By the time Arday started on his master’s degree, he writes, he was reading at about the same level as his 3-year-old daughter.

Money was tight, so after each day of teaching, Arday writes, he had to work an overnight shift in a supermarket, from 11 p.m. to 5 a.m., and then a morning shift as a cleaner from 5:30 to 7:30. The only time he had left to write his dissertation was when he was commuting between London, where he lived, and Liverpool, where he taught. On those semiweekly five-hour rides, the book explains, he would open up his laptop on the plastic seat-back table and start typing out his thesis, hunt-and-peck style.

As his dissertation deadline approached, Arday started having blurry vision; medical scans revealed a brain tumor. After it was removed, he had a ministroke and lost his short-term memory. “I’d worked on my thesis for over thirty months, and now I was reading it as if for the first time,” he writes. As one might expect, his thesis defense did not go smoothly. One examiner was suspicious of his work: “I am struggling to see that there is any original contribution here,” she said, according to the book. But Arday, who often likens himself to Rocky Balboa, managed to fight back, and in the end, he passed. (The memoir brings up the fictional boxer in about a dozen different contexts.)

(Note that Rocky is now a Florida resident (Journal of Popular Studies) and stopped paying taxes to Gavin Newsom in 2024)

More troubles follow in the years ahead: Arday’s brain tumor returns; he splits up with his wife; he suffers autistic burnout during the coronavirus pandemic and can’t get out of bed. He decides to kill himself by jumping off a bridge, but at the very last minute, he listens to his favorite song, “Take It to the Limit”—delaying his attempt just long enough for a member of his family to rescue him. “In the end,” he writes, “my decision to listen to the Eagles likely saved my life.”

I reached out to the book’s fact-checker [at Simon & Schuster] to ask whether this and several other stories from the book had been verified, but she did not respond. … the book’s release is still on track and that it has even been designated as an “Editors’ Pick” on Amazon

This wasn’t part of the book proposal, but it seems that Prof. Dr. Arday, Ph.D. was also an RAF Red Arrows pilot:

The Professor’s PhD thesis is available online. I downloaded it and asked ChatGPT to “evaluate the quality of research and writing”. Some excerpts from the full interaction:

The biggest problem is the sample and selection mechanism. There are only four intervention participants, selected from 46, and selection expressly included whether the candidates demonstrated characteristics that the researcher thought “resonated with the study’s aims and objectives” and a desire/capacity to improve their teaching. … More seriously, the researcher was a lecturer at the university attended by the subjects and already had relationships with them.

There is also no convincing counterfactual. There is:

no control/comparison group, no random assignment, only four highly selected subjects, an intervention that the researcher helps facilitate, and outcomes that are overwhelmingly based upon the subjects’ own narratives and perceptions.

The thesis itself eventually admits a crucial point: it cannot determine with certainty whether improved reflective practice would have occurred naturally rather than because of the peer-mentoring intervention.

Contribution to knowledge: This is probably the weakest part of the intellectual case for a PhD.

Writing quality: This is much easier to judge: the prose is substantially below the standard I would expect in the final, examined copy of a PhD thesis from a British university. The problems aren’t occasional typos. They’re pervasive. Even the title contains an erroneous apostrophe… Throughout the thesis there is a characteristic tendency to take a simple proposition and turn it into an elaborate nominalized construction. … Most problematic is the repeated use of inflated pseudo-technical expressions that obscure ordinary ideas.

The prose also affects the scholarship: This is more important than cosmetic proofreading. The convoluted language sometimes makes it difficult to determine exactly what proposition is being asserted and how strongly.

Should Arday have been given the big job at Cambridge?

Cambridge’s published criteria for its highest professorial level say that a Professor at Grade 12 should demonstrate: “outstanding achievement in research and research leadership assessed by reference to international levels of excellence”… Against that benchmark, Arday’s 2023 record looks unusually thin.

Cambridge’s February 2023 announcement … emphasizes his work on race … and, very explicitly, the importance of his appointment to Cambridge’s efforts to increase representation of people from disadvantaged and ethnic-minority backgrounds.

Asked to place Arday in a percentile of people in the same field, ChatGPT grudgingly estimates “somewhere around the 30th–50th percentile overall” (i.e., quite a few people with PhDs in education/sociology are far dumber than Dr. Arday!).

Here’s the Amazon page showing that this is, according to their experts in Seattle, among the world’s “Best Biographies & Memoirs”:

Throw out your Life of Johnson. It’s not among the “Best Biographies”.

Related:

“Jason Arday taught me. Here’s what I learned” (Fiona Brown in Unherd): “Before Arday arrived at Roehampton, university leaders enthusiastically told us of his amazing backstory: how he only learned to speak at 11 and write at 18, and how excited they were to have him teaching us. … I can honestly describe Arday’s teaching as terrible. He rarely used the PowerPoint slides. Instead, he usually sat casually on a desk, giving his generalized views on racism … Roehampton is a very diverse university, both in terms of racial background and neurodiversity, and takes inclusion seriously. More than two-thirds of the class were either black or from other non-white backgrounds. Most were women… In the end, Arday gave me 70% for my essay. That sounds good — except that my average for the year was 75%, meaning my overall result was dragged down. … In our meeting, I explained that 70% was a low mark for me and asked him to provide feedback. Suddenly, his friendly, confident demeanor changed. I now saw a side of him I’d never seen before: angry, but also scared. Arday implied that I was racist, and said that the only reason I wasn’t happy with 70% was due to my “white privilege”.”

A post for those who are draining their 529 accounts to pay Harvard tuition, room, and board ($91,634/year total) and for friends who work at Harvard (A.K.A., the “dumb ones” who wrote their PhD theses from scratch)…

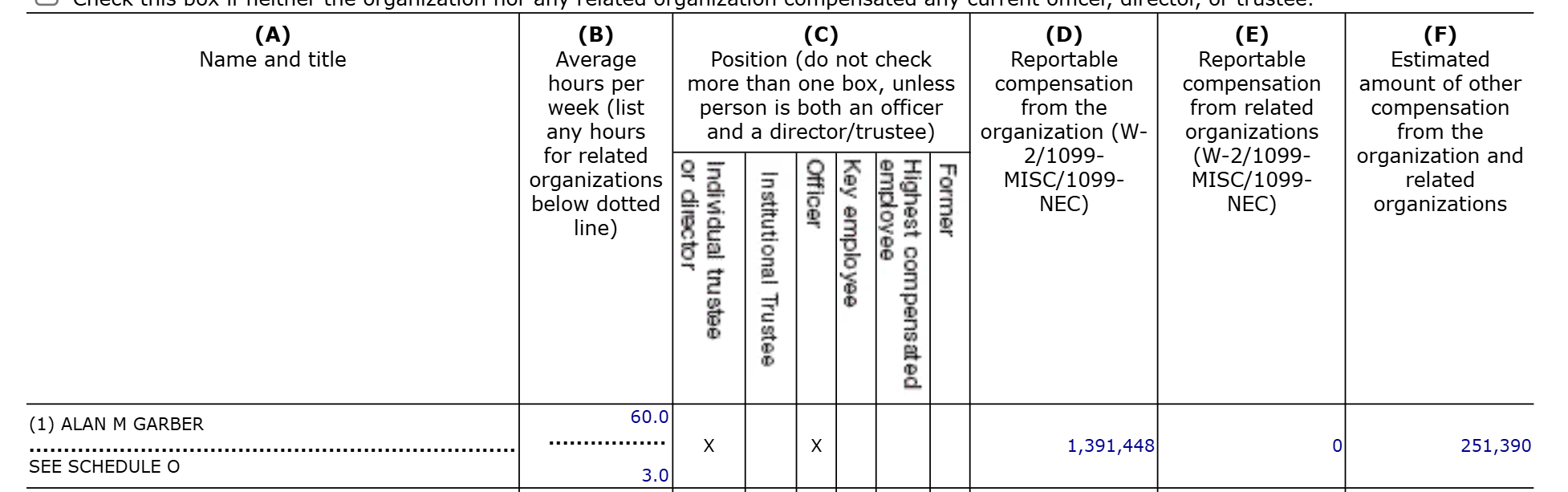

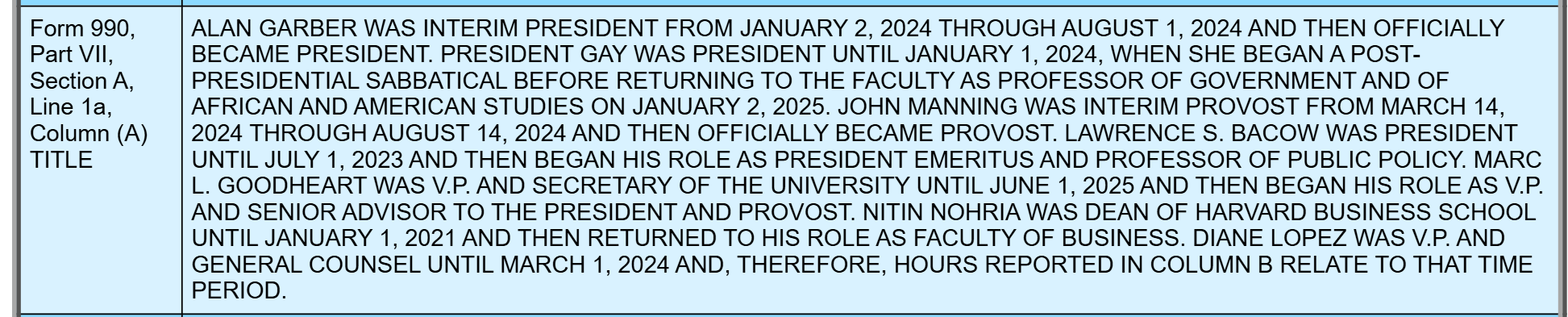

Being a plagiarist disqualified her from the President job, but not from continuing for the rest of her life as a professor, a possibility not mentioned anywhere in the above NYT article (“it has become clear that it is in the best interests of Harvard for me to resign” is the explicit quote), which somehow does find the space to point out that Gay is “the daughter of Haitian immigrants”. How much is the resigned-in-2024 Claudine Gay getting paid? Harvard’s latest Form 990 (Fiscal Year ended June 2025, so the period starts 6 months after her purported “resignation”):

Claudine Gay received $1.55 million, then, for one year of work as a lowly professor? No. Schedule O reveals that she worked for only half of FY2025:

The arithmetic is $1.4 million in W-2 earnings plus another $150k in “other compensation” and then, since she didn’t work for the first half of the year (“post-presidential sabbatical” (at home trying to figure out how to get ChatGPT to do the tedious plagiarism work on the next book?)), multiply by 2 = $3.1 million/year annualized.

Separately, Claudine Gay is the “Wilbur A. Cowett Professor of Government and of African and African-American Studies”. How much money would one have to give to Harvard to get her $3.1 million/year job retitled “the Jason A. K. Arday Professor of Government and of African and African-American Studies”?

(Finally, the page below says that she’s interested in “how the election of minority officeholders affects citizens’ perceptions of their government”. Wokipedia says that in at least nine states, and presumably a lot more cities, a “minority officeholder” would be a non-Hispanic white person: “As of 2024, nine states are majority-minority: Hawaii (20.7%), California (32.6%), New Mexico (35.1%), Texas (37.8%), Nevada (42.8%), Maryland (45.3%), Georgia (48.0%), Florida (49.1%), and New Jersey (49.5%).”)

How’s SpaceX stock doing today? Up 6% says the Google? Even if it had sagged to Morningstar’s number (see SpaceX is worth $63/share according to the most expert experts), there would still be a lot of newly minted rich people due to the expiration of employee lockups. It’s almost as though they won the lottery, which raises the question… Can one predict the effects of winning the lottery?

We estimate the effects of large, positive wealth shocks on marriage and fertility among Swedish lottery players. For male winners, wealth increases marriage formation and fertility and likely reduces divorce risk. For female winners, the only clear effect is a higher short-run (but not long-run) divorce risk. The gendered treatment effects are often similar to income gradients. Our findings align with models in which wives derive greater marginal utility from consumption when single than when married, whereas the opposite holds for husbands—but only if marital property is divided unequally upon divorce. We provide descriptive evidence consistent with such unequal division.

If the academics are correct, we should expect wedding bells for some of the male employees of SpaceX and that the female employees will be filing more divorce lawsuits than they otherwise would have.

(The “if marital property is divided unequally” phrase in the above, I think, refers to prenuptial agreements in which property is kept separate. Sweden’s divorce law allows for the possibility that a lottery prize could be joint property, in which case a female partner of a male winner could cash out via initiating a divorce and also the possibility that a man’s lottery prize could belong to him alone, in which case the female partner’s only way to spend some of it would be to stay married.)

Graham Platner was able to farm oysters, run for Senate, and have sex with every progressive female in Maine while receiving a disability pension from the Veterans Administration for 100% disability. What’s next for this noble fighter for river-to-the-sea liberation? How about airline pilot, a job that requires a First Class medical certificate from a Federal Aviation Administration medical examiner. Is it possible to be 100% disabled under the standards of one government agency, and receive a share of the $150+ billion that the VA pays out for disability, and 0% disabled under the standards of a sibling government agency? The answer, we learned at Oshkosh, is a resounding “Yes!”

Here’s a booth of specialists who help with the magic:

We also stopped by the Graham Platner Veterans Administration Service Center in Wisconsin (100% of parking spaces marked in blue):

What else was worth seeing among the vendors? I liked WingTent, despite the fact that it won’t work for us low-wingers:

“With standard wheels, the [16 lb.] WingTent can produce an enclosure that is approximately 220 sq ft. at the base”

On the back of a truck and sadly not for sale:

Here’s a bizarre one: Flare Bourbon. Covidcrats in all of the lockdown states deemed alcohol “essential”, but should a group of pilots get together and make booze?

My vote for best vendor ad:

For about $220, I was able to purchase a “women owned” banana (Aviator’s Club North):

I purchased a T-shirt from the NGPA:

And, of course, for fans of Christopher Nolan’s latest magnum opus, the best product of all on display at Oshkosh:

A Greek guy reviews the film that is named after the minivan:

A friend paid a ticked for me to watch Nolan's Odyssey. Despite all of my reservations about the way the movie was marketed, I really wanted to like it. But it was worse than I expected, much worse. The casting and the costumes were the least bad thing about it.

Here are some…

— Stelios Panagiotou (@Panagiotou90St) July 18, 2026

Abdulrahman Mohamed El-Sayed won the Michigan Senate primary yesterday. As he’s been complaining regularly about the “genocide” inflicted on the noble peaceful Gazans (a genocide whose suffering has been exacerbated by rapid population growth), presumably he’ll introduce a bill for the U.S. military to wage a jihad against Israel (the North American Ummah needs to try to stop the genocide, surely) and it will be interesting to see if any other Senators respond with “we had to surrender to Iran; isn’t Israel at least as tough?”

More interesting to me is the personal journey of Abdulrahman Mohamed El-Sayed’s defeated opponent, Haley Stevens. Wikipedia:

Stevens and Rob Gulley, a software engineer she met in high school, became engaged in June 2020. Due to the COVID-19 pandemic, they waited until September 3, 2021, to wed. Guests, who were required to have a negative COVID test, included Congresswoman Debbie Dingell and Michigan Attorney General Dana Nessel. Nessel officiated the wedding. On October 5, 2022, Stevens and Gulley announced their divorce.

The requisite pre-wedding coronapanic, in other words, lasted longer than the marriage. That’s a true 21st century American love story.

Abdulrahman Mohamed El-Sayed gets some assistance from state-sponsored NPR. Here’s an example from WBUR:

El-Sayed “opposes Israel’s war in Gaza“. As a matter of established fact (this is a news article, not opinion), it’s not the “Gaza-Israel war”, which would imply that the Gazans had perhaps done something aggressive to provoke fighting or, at least, were playing an active role in the fighting. It’s a war that Israel started, apparently, and is carrying out all by itself while the peaceful Gazans stand around peacefully in their UNRWA-provided housing.

What does Abdulrahman Mohamed El-Sayed want to do? His campaign site:

abolish ICE (“People don’t come here because they want to take away from America, they come here because they want to build in America”)

“Homelessness is an American crisis–and it’s a housing issue.” (but he doesn’t promise to do anything to address the “crisis” other than building more housing, which will presumably be immediately occupied by the humans streaming through the open borders (ICE is gone and, therefore, nobody can be deported))

surrender to Iran (“I oppose the illegal and unjustifiable war in Iran and demand an immediate end to the hostilities.”; but isn’t Trump already surrendering?)

“immediate arms embargo on Israel” (force the Israelis to use domestically-produced 155mm artillery against the peaceful Hezbollah, Hamas, UNRWA, and Palestinian Islamic Jihad fighters?)

keep paying Graham Platner’s 100% disability pension: “I believe in expanding and improving the VA, not cutting it.”

abolish the filibuster

oppose mandatory Voter ID laws

eliminate limits on abortion care (“government cannot and should not interfere with the right to pursue healthcare choices”)

I support raising the minimum salary for teachers to at least $60,000/year (starting total comp in Palm Beach County, Florida is already at $81,100 and this works pretty well… for teachers who live with their parents and/or a partner who has a decent job)

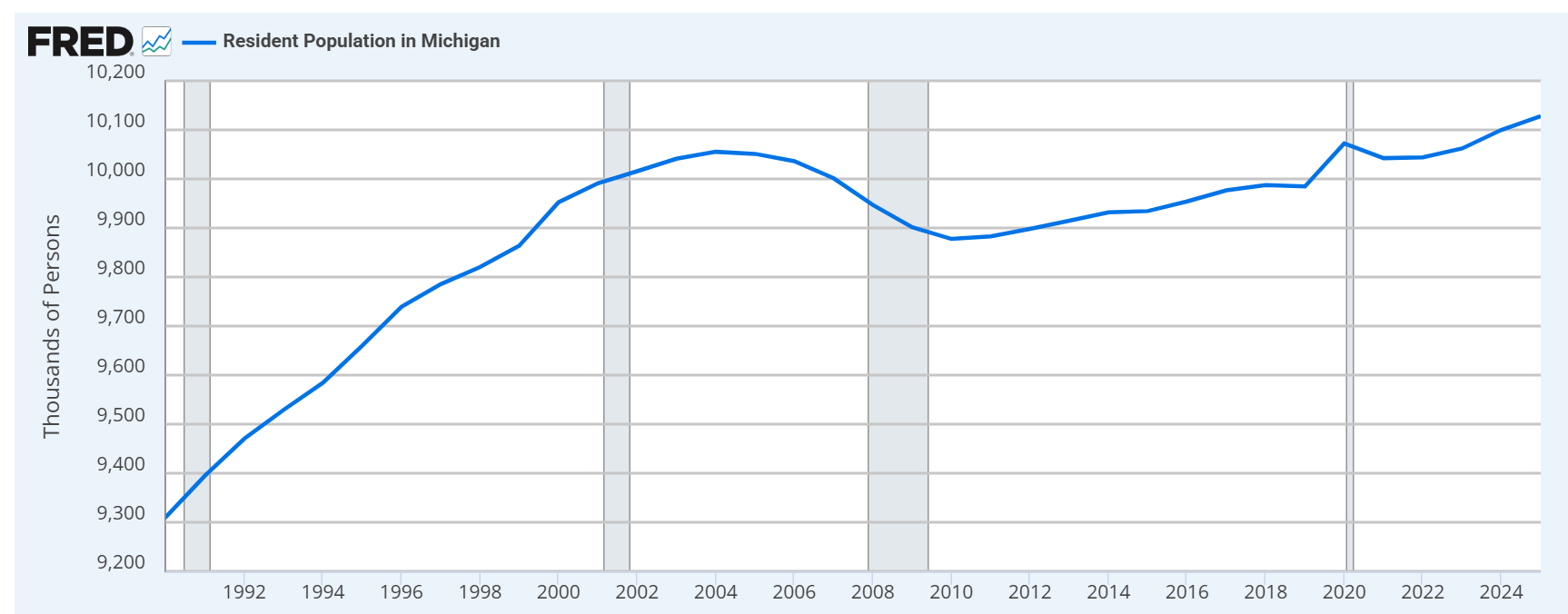

Separately, let’s see, from a biology perspective, how successful Michiganders are compared to Arabs who call themselves “Palestinian”. Since 1990, the population of Michigan has grown from 9.3 million to 10.1 million (“Immigration is the sole reason the state’s population is growing” (Detroit News); non-Hispanic white population percentage has fallen from 82% in 1990 to 72% in 2024 (Census). Note that the Census Bureau has classified Arabs as “non-Hispanic white”, though that will change post-2024 and for the 2030 Census with a “MENA” category. If there were a “legacy white” category that excluded Arab immigrants and their children, Michigan’s legacy white percentage is already below 70%.

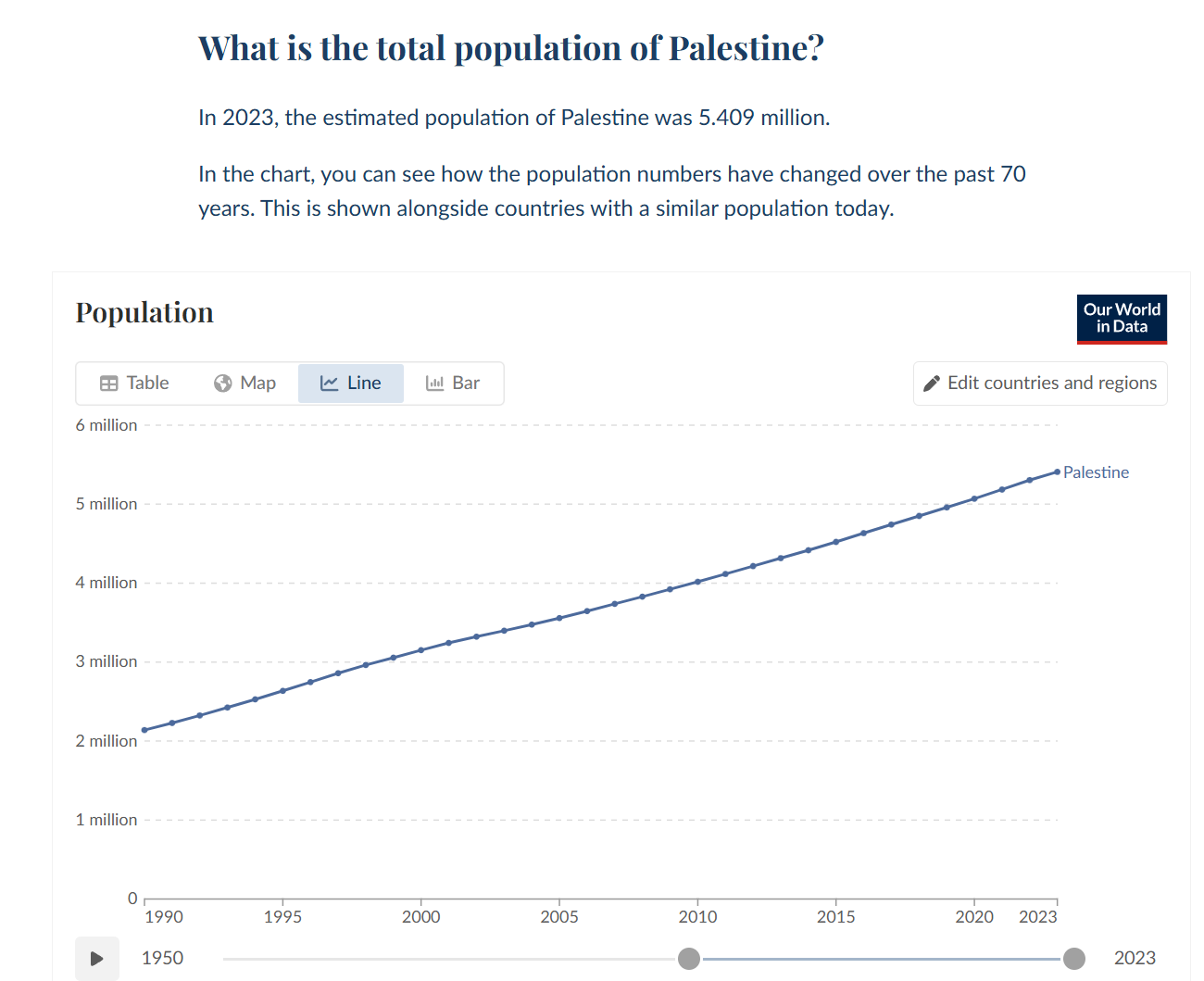

During the same time period, the population of “Palestine” has grown from 2 million to 5.5 million:

ChatGPT says that if these trends continue, including cramming Michigan full of additional migrants as the native-born escape and/or can’t afford to have kids (this is not a “replacement”, please keep in mind), “Palestine” will have a larger population than Michigan in less than 20 years.

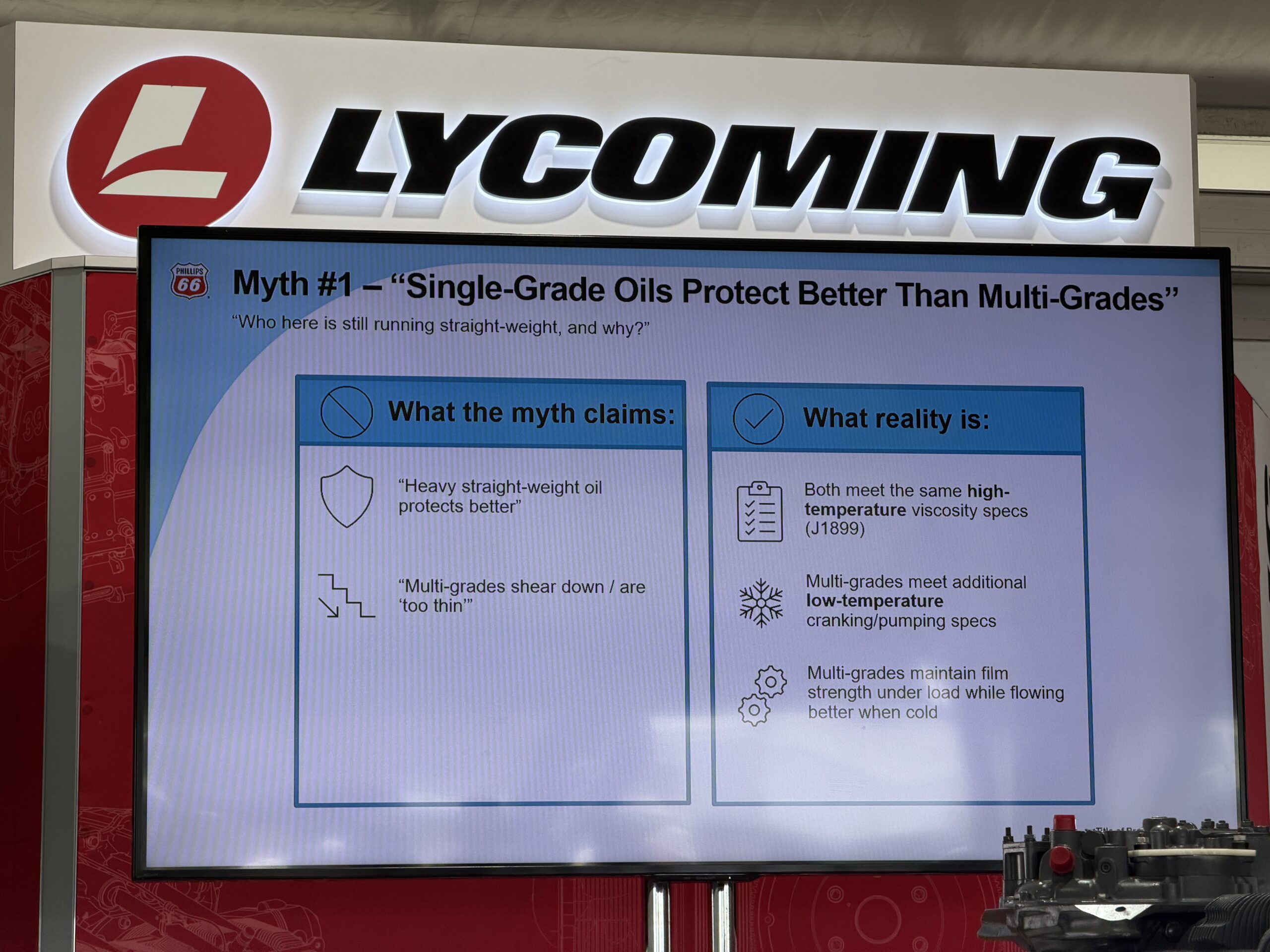

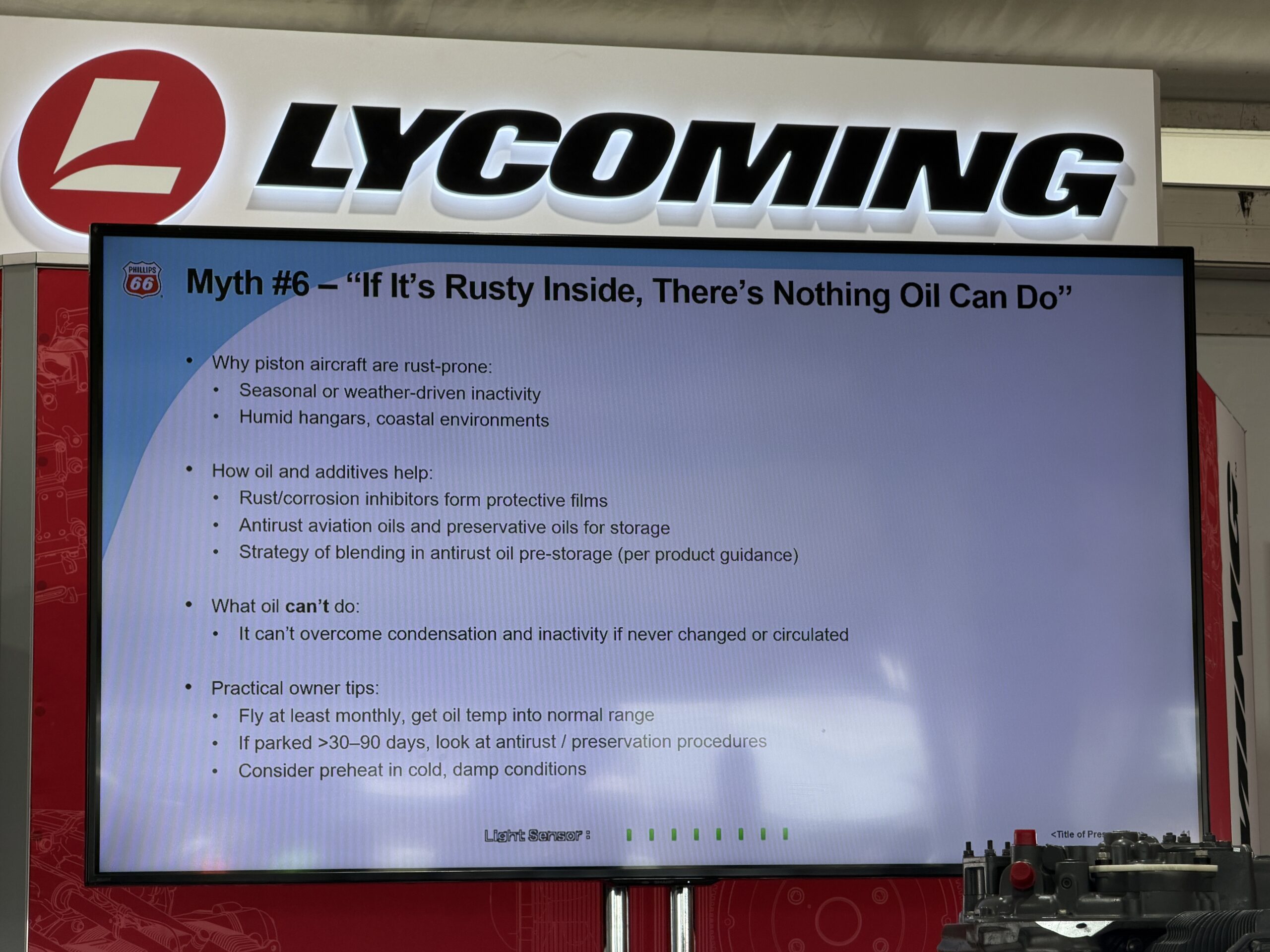

I dragged a friend to a Phillips 66 talk at the Lycoming pavilion and we found that Phillips 66 had dragged out a team of four experts, including the company’s top “scientist” in this domain, to answer questions from piston peasants.

What did we learn? A preference for straight weight 100W is purely superstitious and, even in a reliably warm climate such as Florida’s, it is smarter to use Phillips XC 20W-50 (bizarrely, the “50” in the multiweight and the “100” refer to the same “SAE 50” spec for viscosity at higher temperatures).

If you have a Lycoming engine, you should definitely use the “Victory” version of Phillips, which is preblended with a Lycoming-recommended anti-wear additive. For Continental owners, the representatives who were present leaned toward either the Victory version or XC plus CamGuard if the plane isn’t flown frequently.

Since every group needs at least one obnoxious person, I asked “You have a huge team of PhD scientists. All that CamGuard has is a snake. Why can’t you put something in the oil that will prevent corrosion for a plane that doesn’t fly regularly?” Unlike America’s Greatest Scientist, the chief scientist at Phillips 66’s oil division did not invoke the 5th Amendment. He answered that corrosion is an almost undefeatable enemy. There is always some water in the oil, even if a plane is based in the Arizona desert and even if the owner puts a Drybot in the filler tube (sadly, suitable only for T hangar royalty; those of us in shared hangars can’t expect the line guys to keep unplugging it and plugging it back in when the aircraft is moved). There is thus no substitute for flying regularly (“at least monthly”, but of course weekly is better).

What about the FAA-industry dream of unleaded gasoline in 1950s engines? So far, there isn’t a great one-fuel-fits-all solution. Patrick Ealy, a master’s student at University of North Dakota, gave a talk about capturing the lead out of the exhaust stream (about 40 minutes in; the first part of the talk is more about how aviation 100LL is falsely accused of being a significant contributor to America’s falling average IQ; he points out that even “unleaded” car gasoline has some naturally occurring lead in it and there are a lot more ground vehicles out there burning dinosaur blood than there are piston aircraft).

Related:

“Unleaded fuel takes center stage at AirVenture” (AOPA): “the FAA plans to release new versions of the transition plan after each phase. … The first phase includes authorizing fuels and doing comparison testing. … The third and fourth phases focus on the wide-scale transition—first in the Lower 48, with a goal of completing the work by 2030, followed by Alaska two years later.” (for the Cirrus SR20 with IO-360-ES engine… no unleaded fuel is approved by Cirrus, though GAMI G100UL is approved for this engine/airframe by the FAA)