Here’s a report on a recent business trip to Sherman Oaks (into LAX and out of BUR).

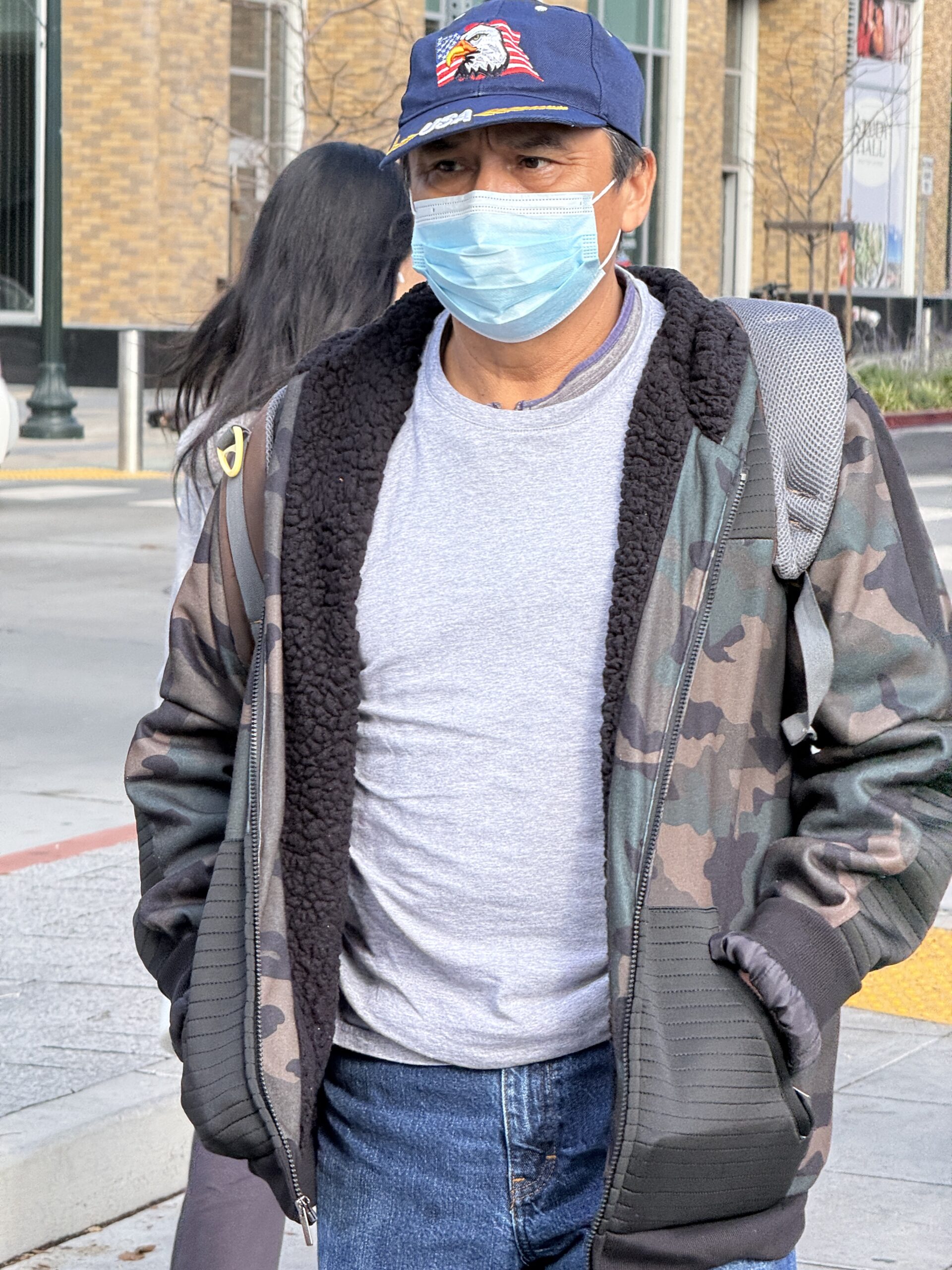

A heroic masked Californian is turned away from the gate at PBI for not being in a sufficiently high-priority boarding group (if there were any justice on this planet, Trump would have lost the recent election and masked passengers would enjoy top priority boarding along with military personnel):

The JetBlue Mint “studio” in their new-configuration planes. The seats are angled and that leaves a little bit of extra space in the first row. They actually put a second seat belt in the suite/studio for a guest (not during takeoff/landing) and the bed ends up being a little wider. My excuse for this luxury is that I needed to get some work done.

Departing east from PBI we flew over a 20-acre estate on Palm Beach that a Democrat judge in New York appraised, in an entirely nonpartisan manner, at $18 million. (A one-acre vacant lot nearby recently sold for $85 million.)

Bold #resistance can begin within moments of stepping off the plane in LAX via access to “Books Banned Elsewhere”:

The streetscape in front of my luxurious Courtyard hotel in Sherman Oaks included $5/gallon gasoline (currently about $3/gallon in Florida), outdoor maskers, and the unhoused:

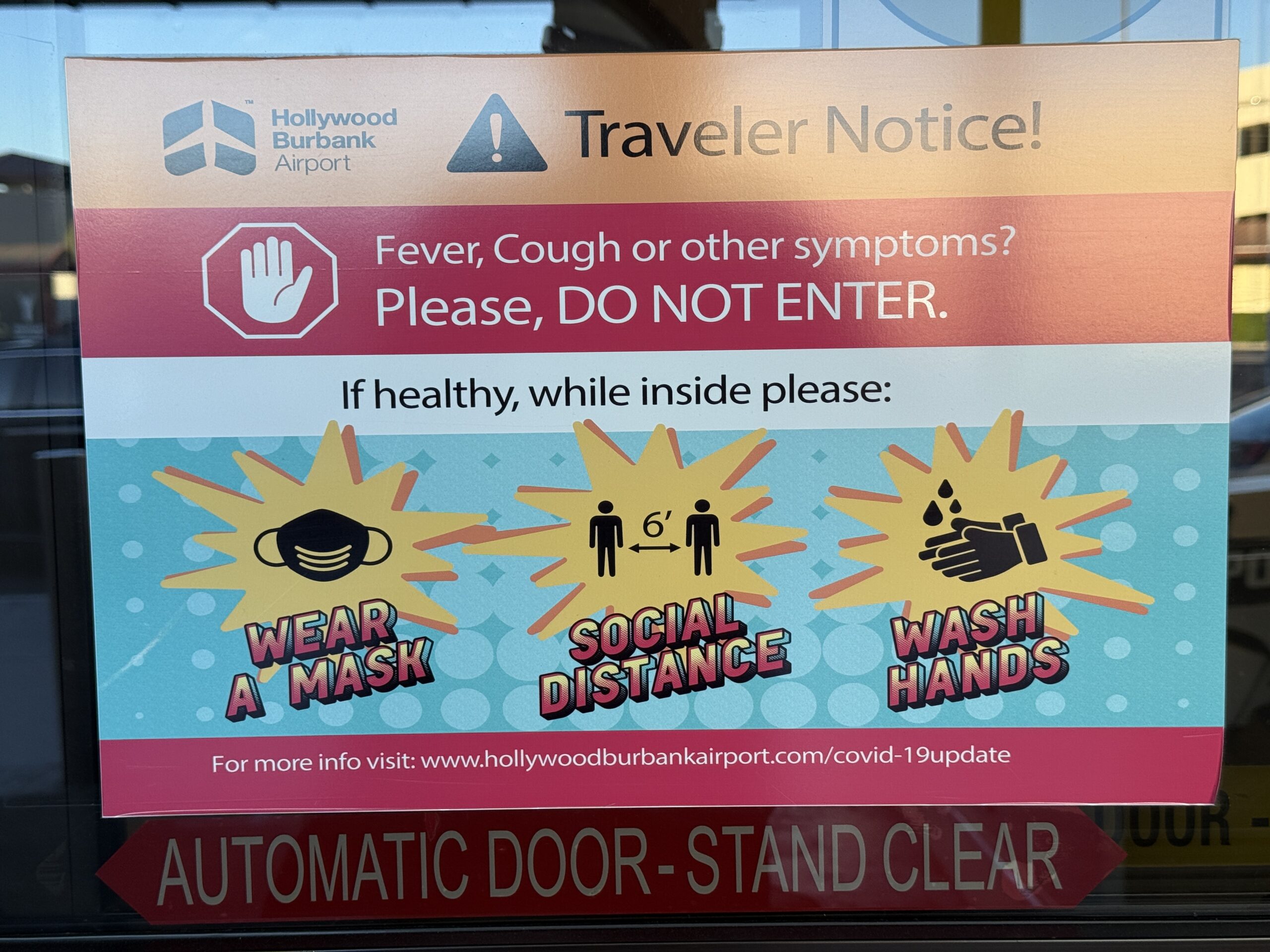

One is greeted at the Burbank airport by a sign reminding healthy travelers to “wear a mask”:

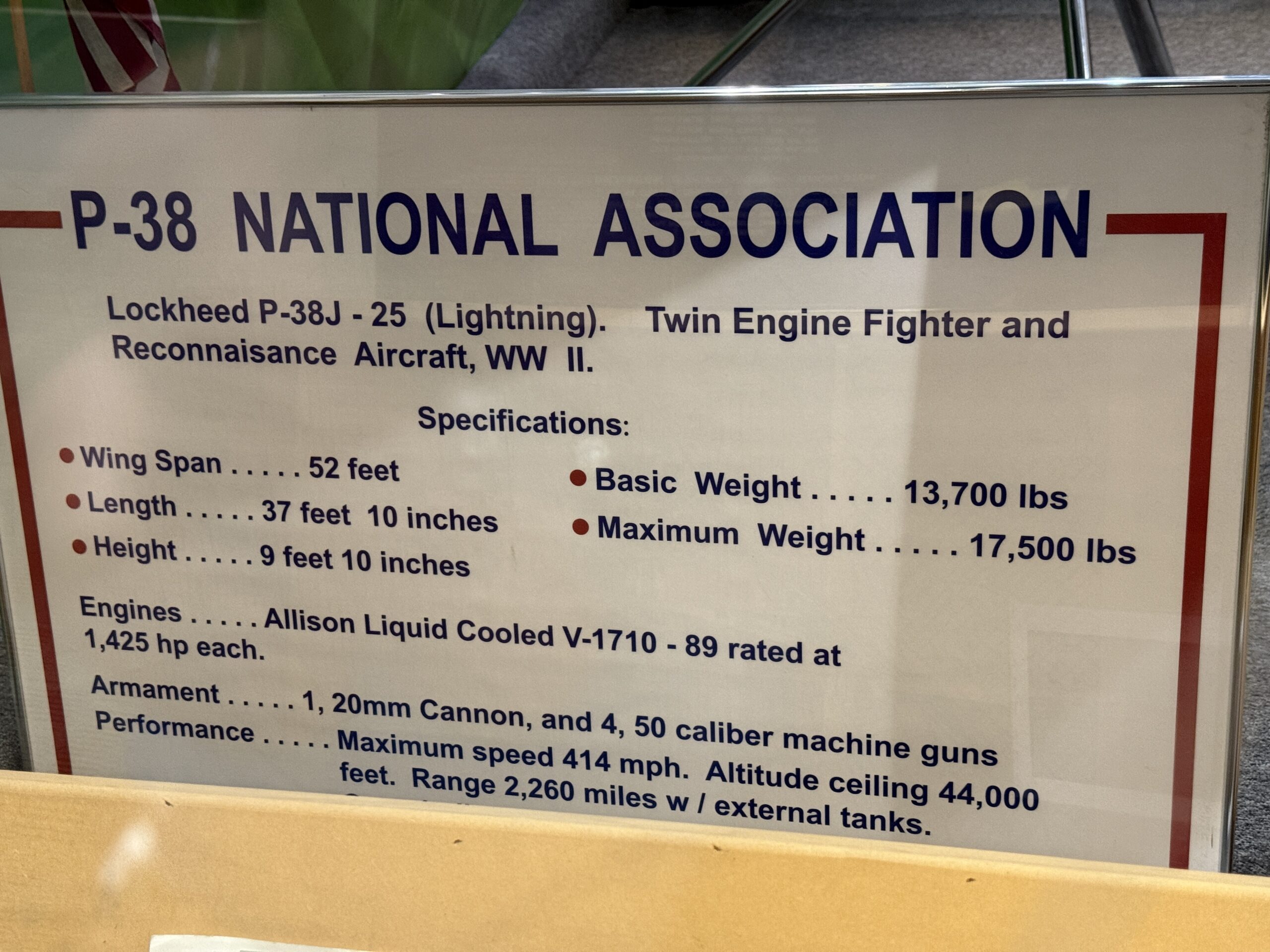

The airport also features an exhibit on the built-in-Burbank Lockheed P-38 Lightning, which helped the U.S. achieve “peace the old-fashioned way” (as B-17 and B-29 fans like to say) in World War II:

Thanks to United Airlines for getting us to SFO on time in a somewhat newer twin-engine plane.

The Election Nakba, in which Donald Trump was elected to a second dictatorship, occurred on November 5, 2024. This post is about a November 14, 2024 journey to Berkeley, California.

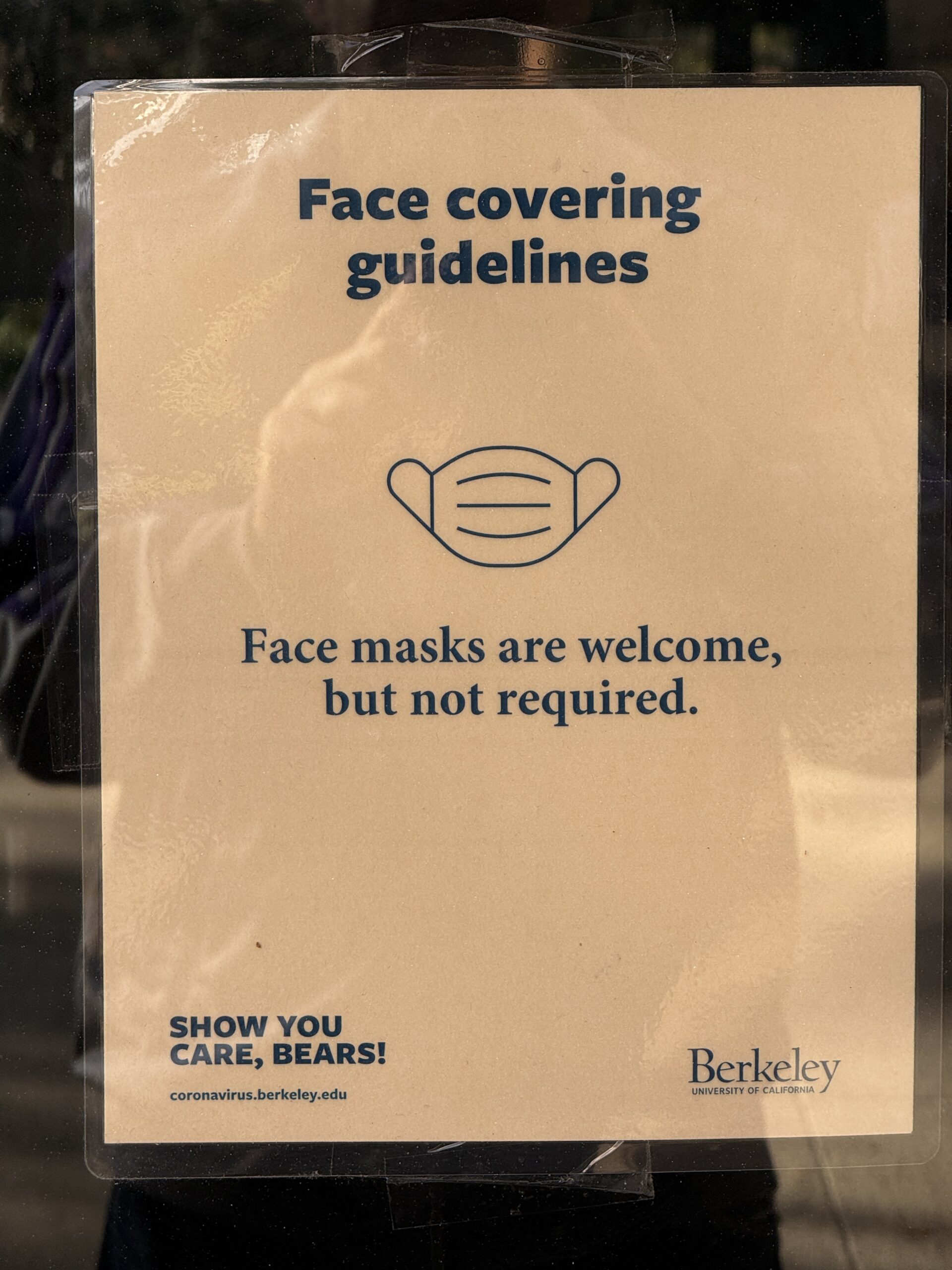

BART warns customers that “face coverings [are] required” and 10-20 percent seem to comply:

The gathering on the platform above includes about 16 people. Three are masked. One appeared to be unhoused (obscured behind the person in the gray jacket). One is Islamically covered, but not masked. Within a few steps of the Downtown Berkeley station there were unhoused Californians, outdoor maskers, and Halal food:

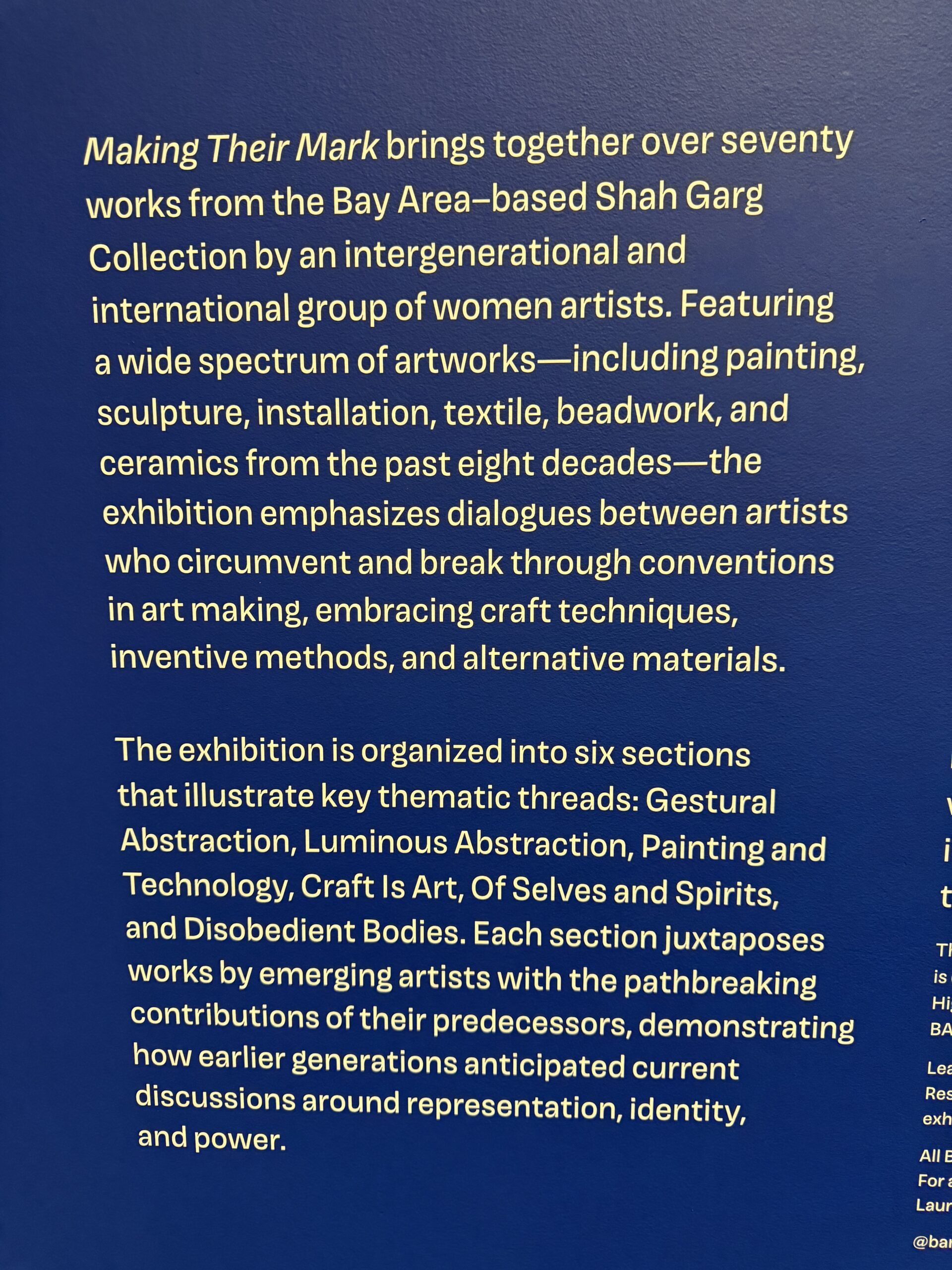

We entered the University of California’s art museum and found that most of the exhibit space was restricted to artists who identify as “women”:

Given that Democrats said that Americans would lose their freedoms and their democracy if Trump were elected (see Why do the non-Deplorables deplore the Trump shooting? for some examples), I had expected riots on campus or at least mostly peaceful protests. Surely, these brave souls who tweeted (before fleeing to Bluesky) about #resistance wouldn’t meekly surrender everything that was important to them. Not only did we not encounter any anti-Trump protests, it was difficult to find anti-Trump signs. A handful:

There were far more signs related to masks than to the horrors of a second Trump dictatorship:

The famous campanile has a statute of Abraham Lincoln, whose signature on the Morrill Land Grant Act was important for the founding of UC Berkeley (also a sign at the top regarding the gender ID of certain carillon players). My friend asked a sophomore majoring in environmental sciences what she knew about Abraham Lincoln. The graduate of California public schools knew that Lincoln had been a U.S. president, but not in which century this had occurred nor did she know of any wars or acts with which Lincoln was associated.

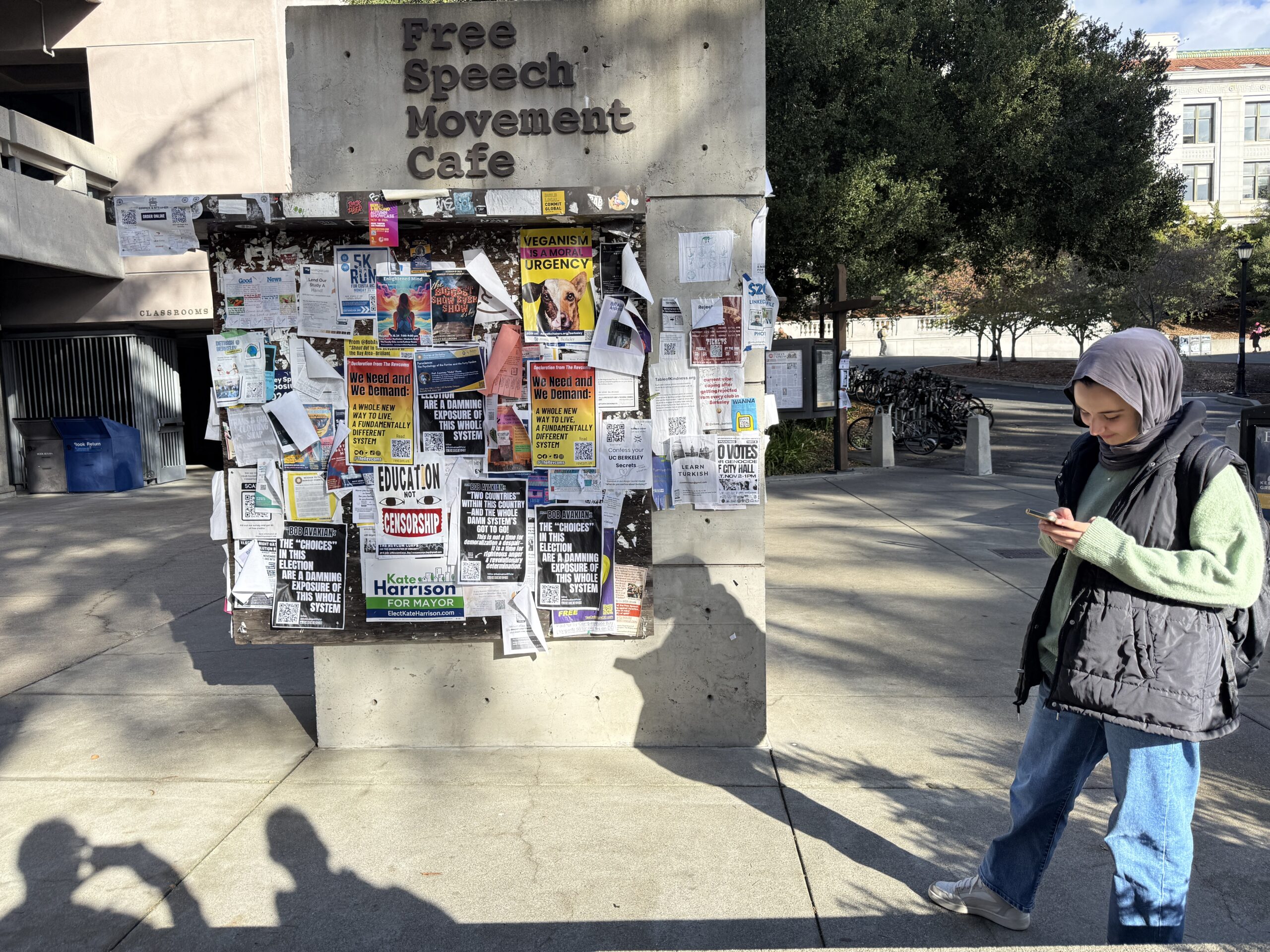

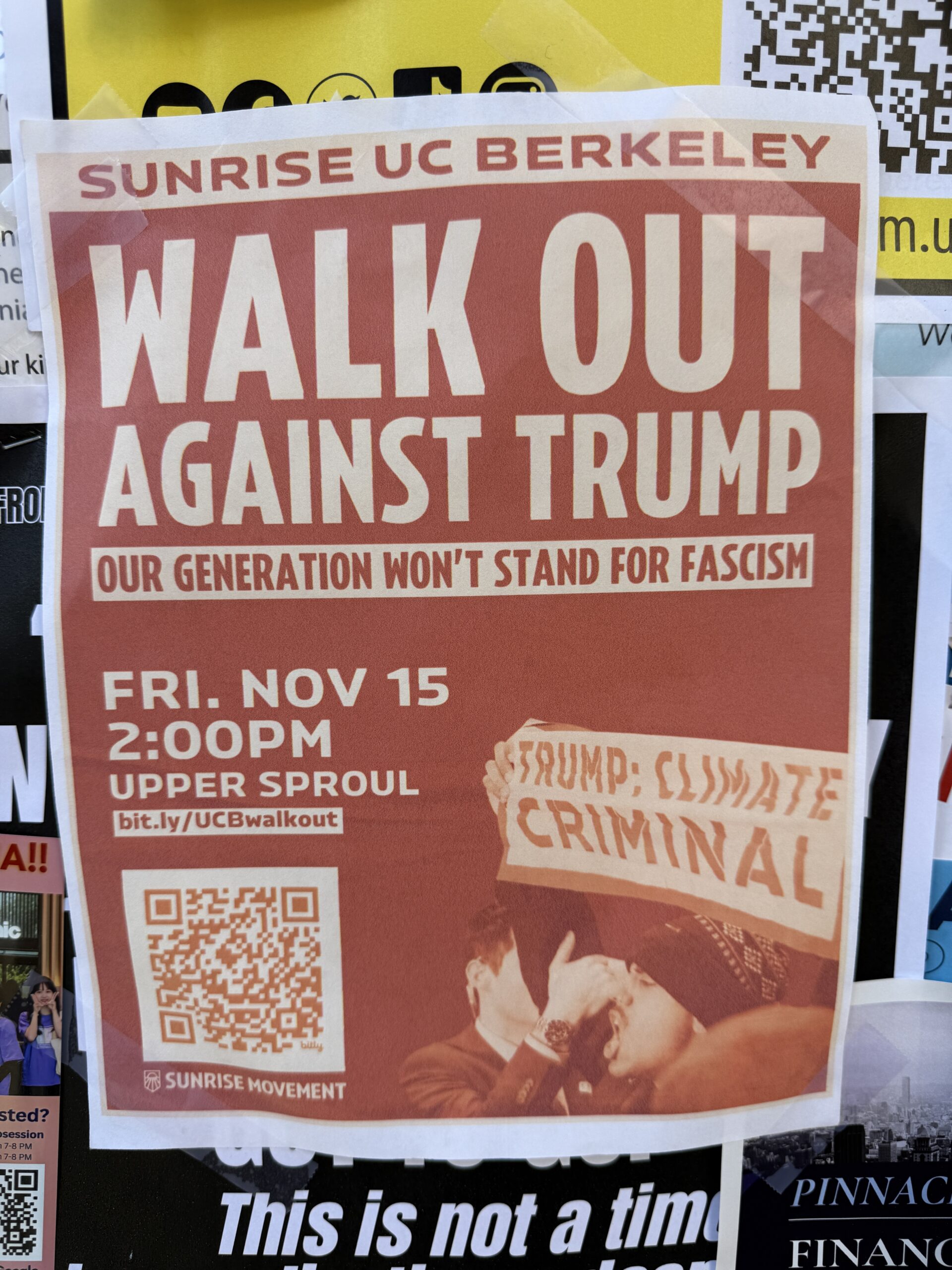

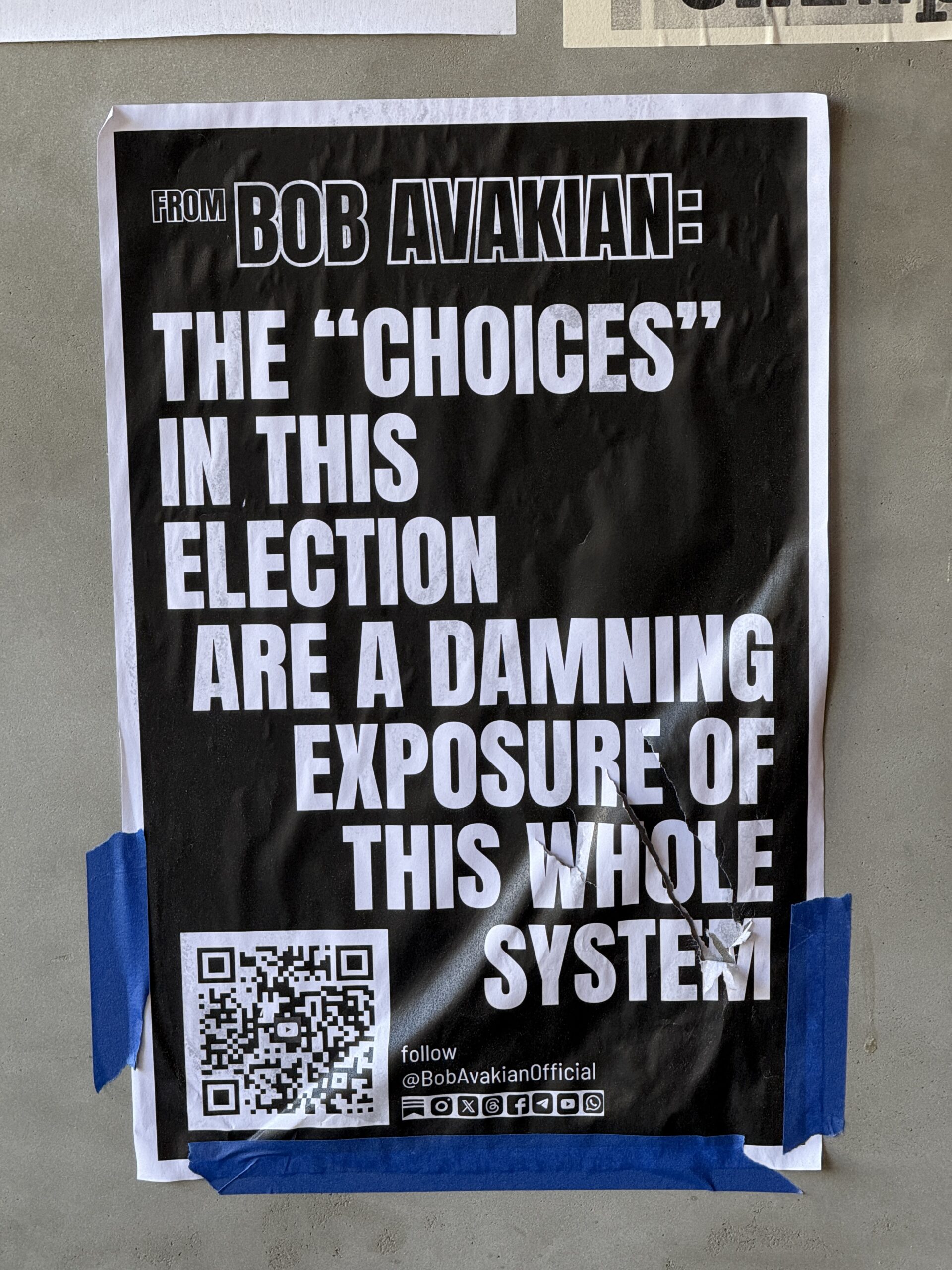

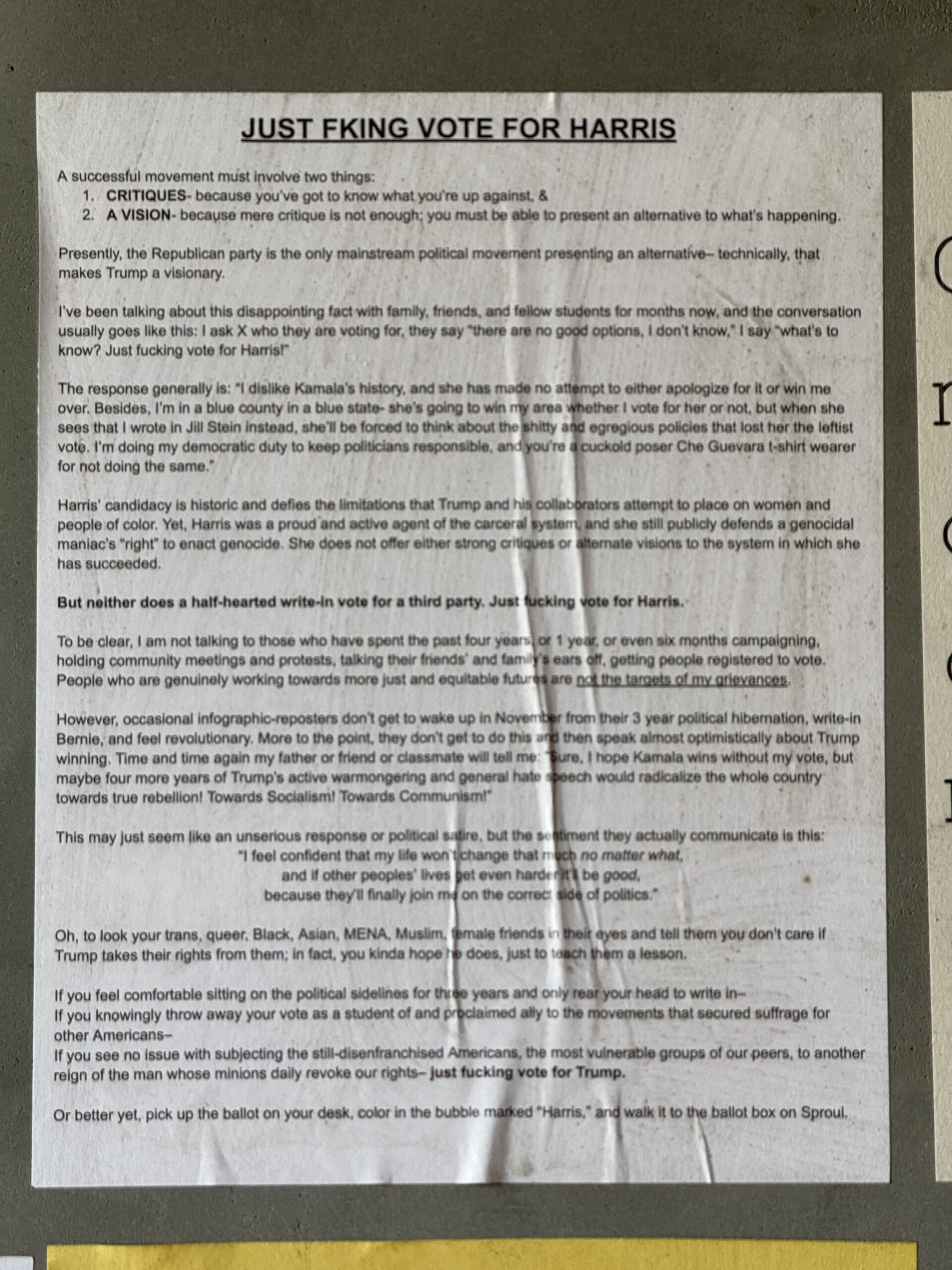

Our next stop in search of anti-fascism pro-democracy protests was Sproul Plaza, famous for student activism. We found a couple of Trump-related posters amidst of a sea of unrelated material:

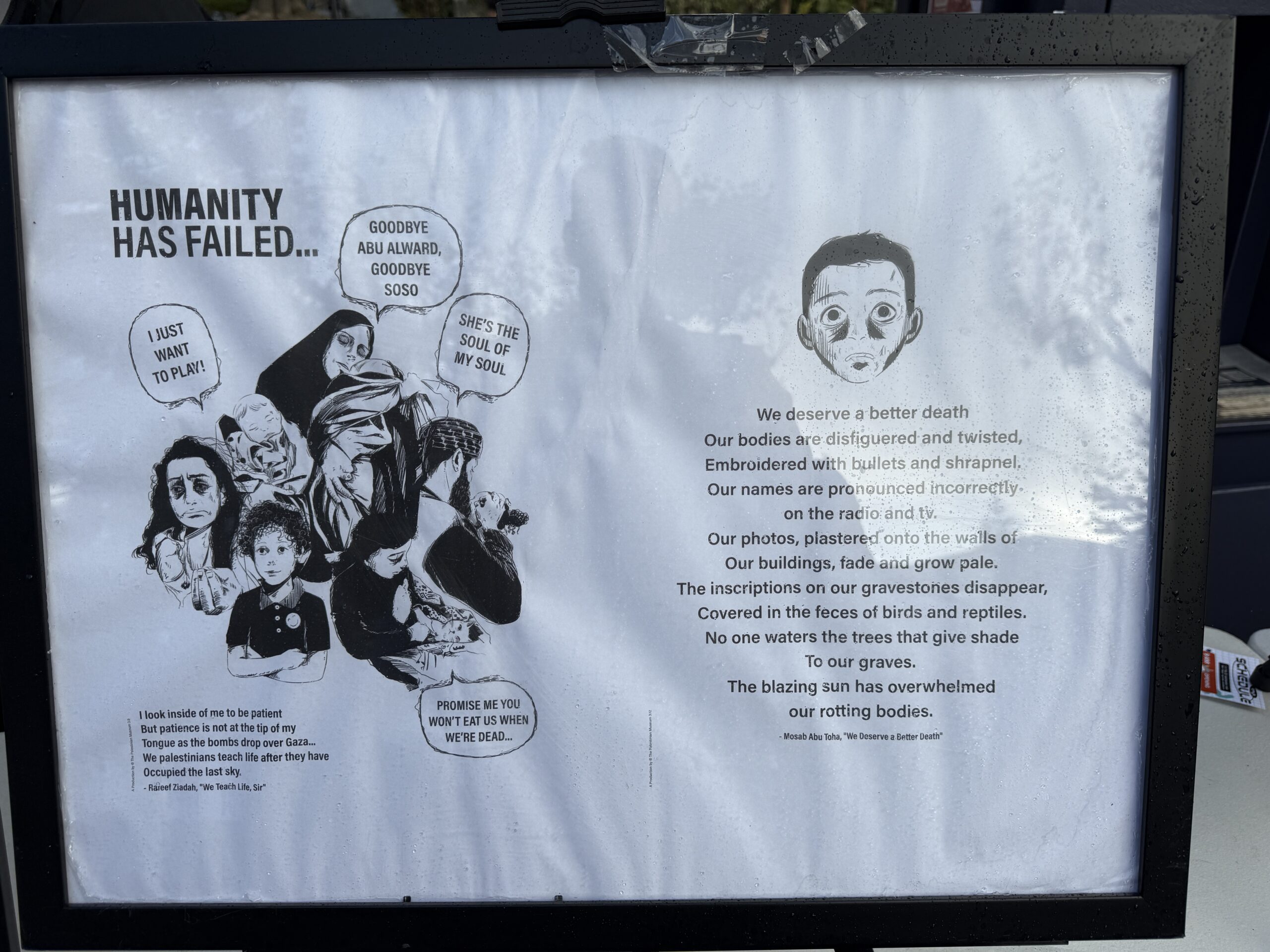

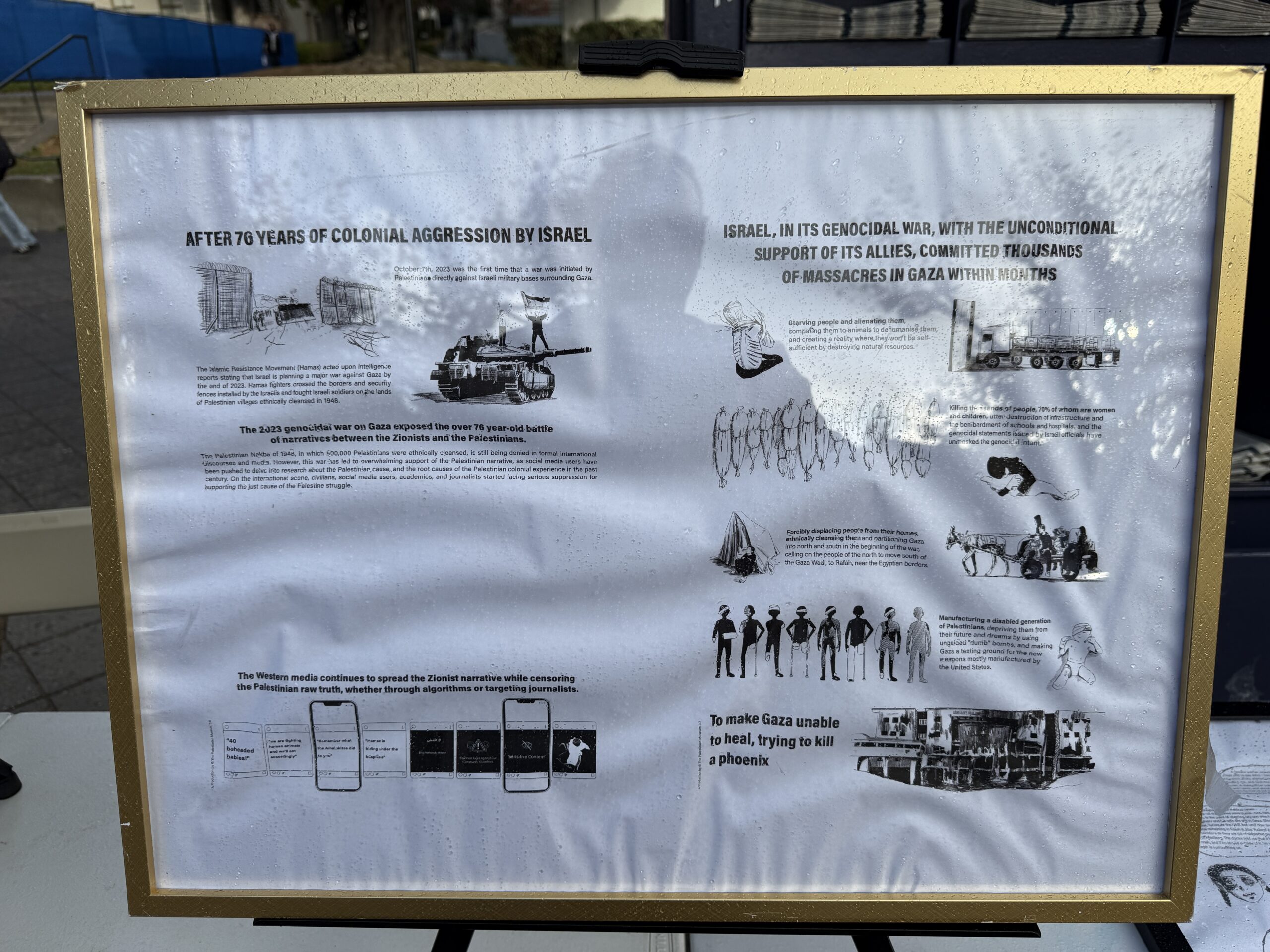

The anti-Israel protest that began just after October 7, 2023 was still in full operation.

End-stage Berkeley feminism is complete covering of the body, except for an eye slit, when in Sproul Plaza:

We wandered back into the commercial district and found that coronapanic level varied by shop.

We found that there was roughly one marijuana store on each block. Examples:

For those who get hungry after consuming a lot of healing cannabis, the good news is that L&L Hawaiian Barbecue is opening soon:

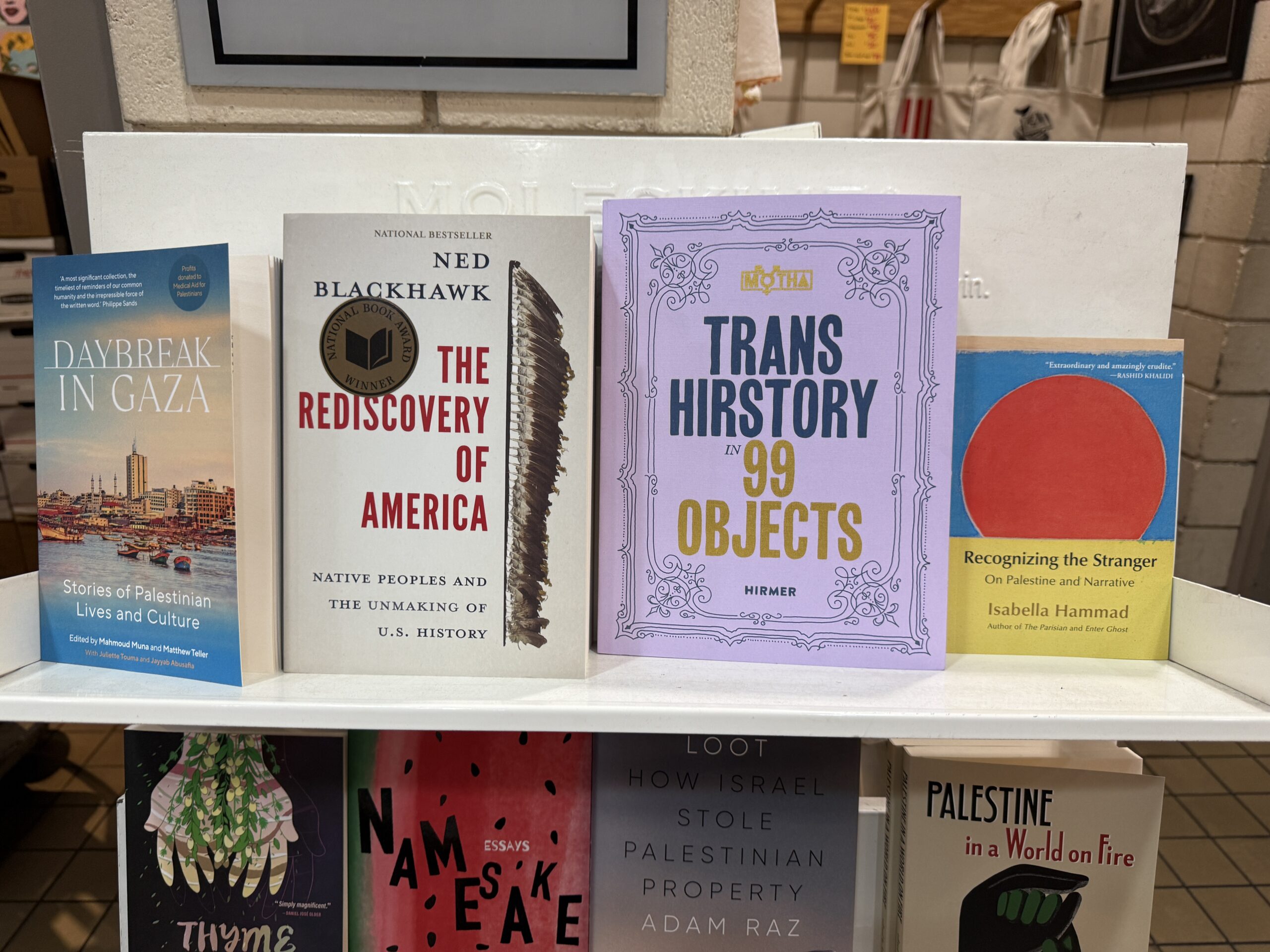

Moe’s Books is still at the center of Berkeley’s intellectual life. The area near the front door is primarily devoted to Queers for Palestine books, e.g., The Queer Arab Glossary (a bestseller in Gaza and the West Bank?):

(The secular Jews whom I know in Berkeley all say that they want Israel to be replaced by a river-to-the-sea country that would be ruled by Arabs and in which Jews, at the discretion of the Arab rulers, might continue to live as a minority group. These Jews-by-birth, none of whom have ever visited Israel, say that they’re “anti-Hamas” but also that Israel and Hamas are equally bad and that Israel should cease to exist as a nation. (Sometimes for fun I ask them “Suppose that you were pro-Hamas. What would Hamas want you to say that is different from what you currently say?”)

Going deeper into the store, we found a lingering commitment to coronapanic:

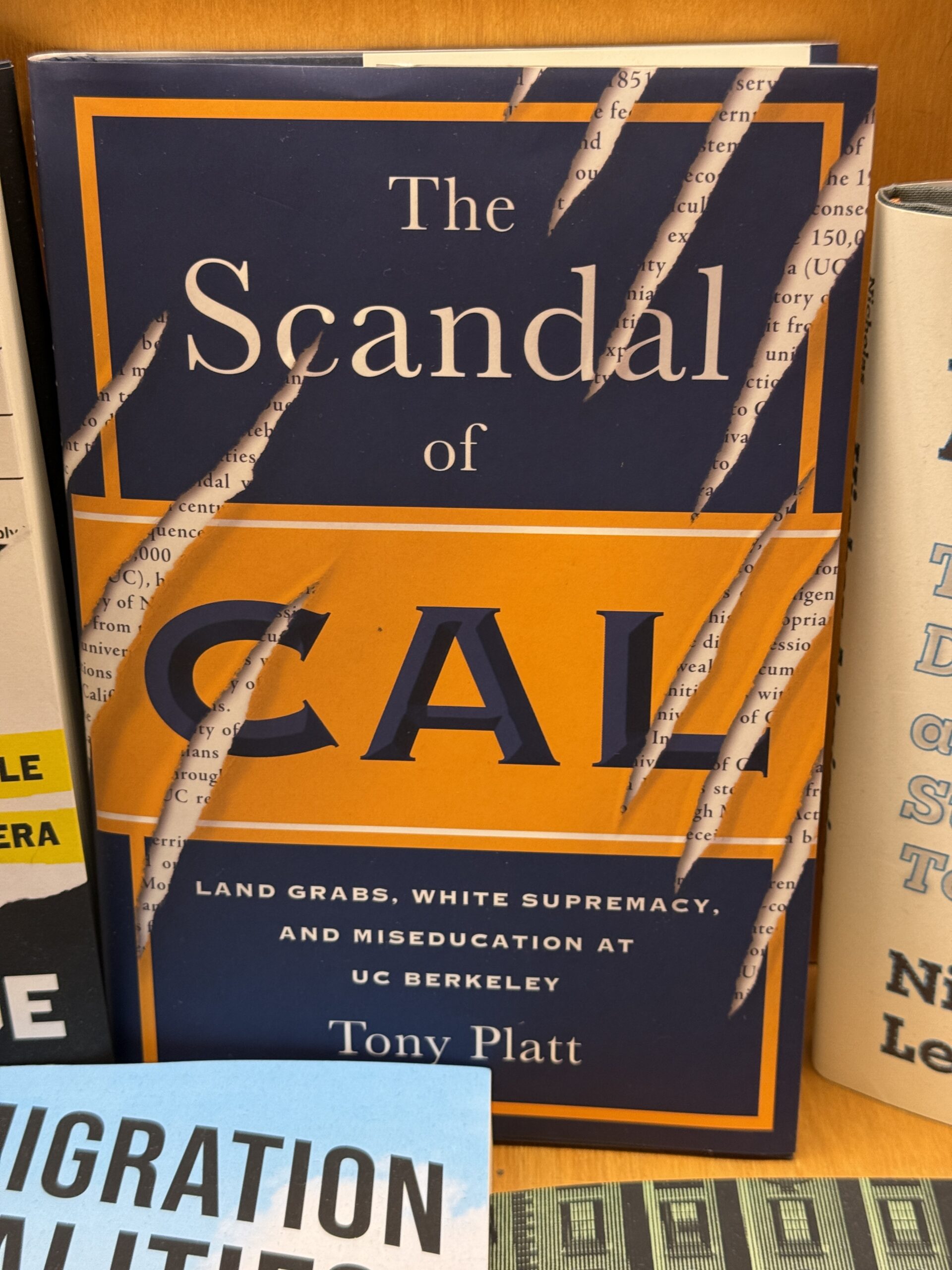

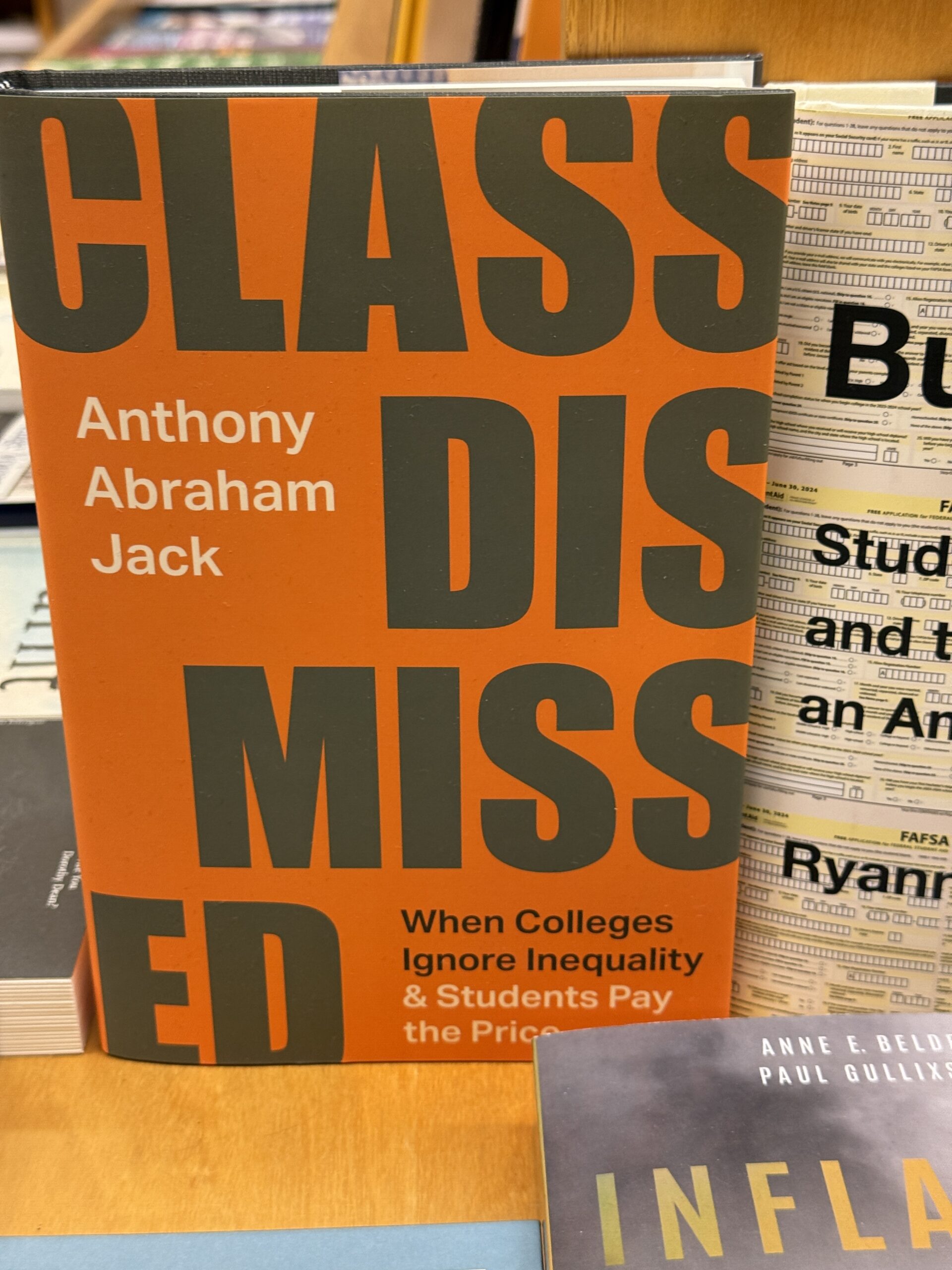

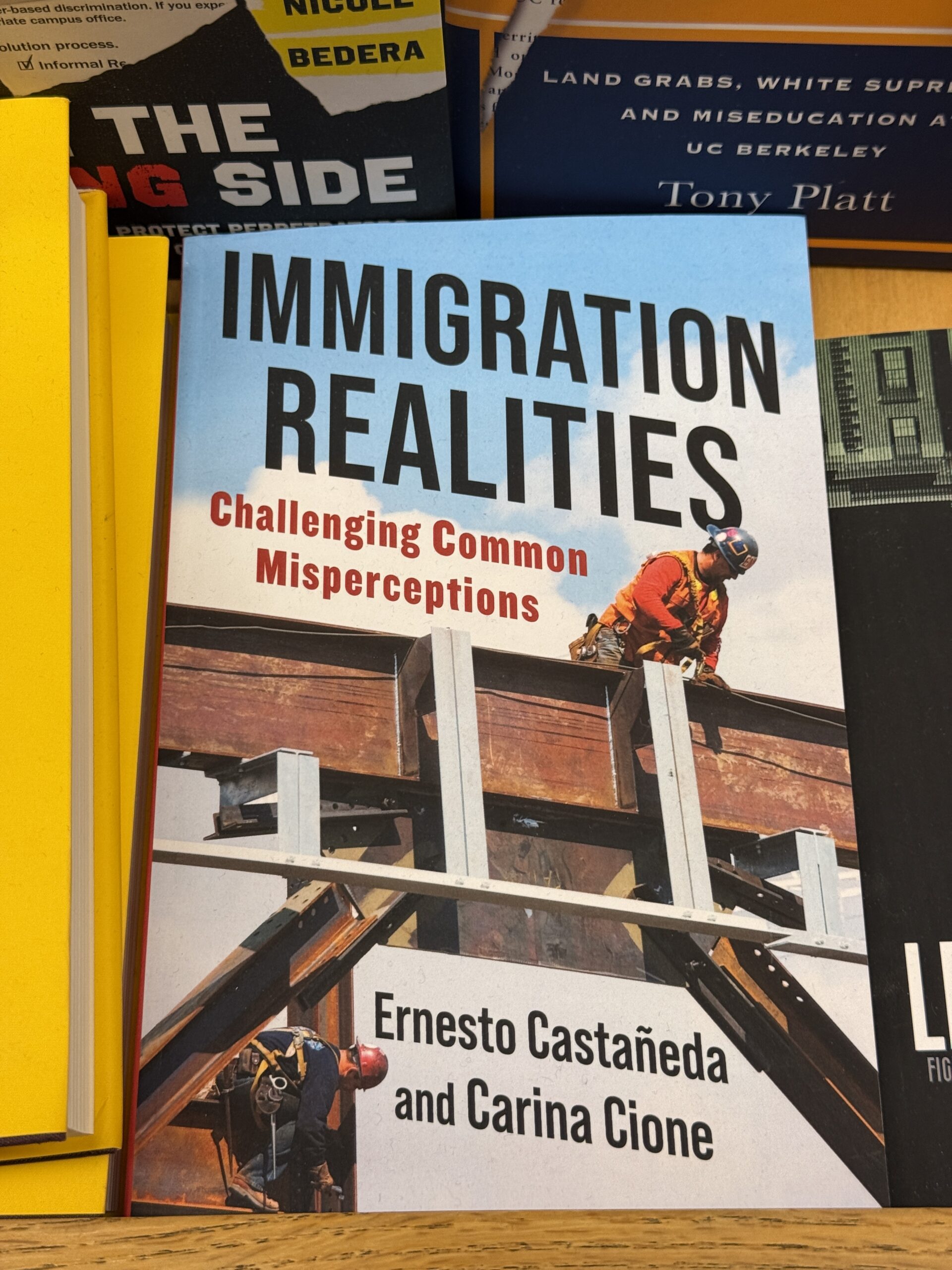

Some of the featured mid-store books:

Immigration Realities is from the giant brains of Columbia University Press, which starts its description of the book with “Immigrants are less likely to commit crimes. They are eager to learn local languages. Immigration is not a burden on social services. Border walls do not work.”

Right around the corner from this important work about how “border walls do not work”, we find the border wall that UC Berkeley installed around what used to be People’s Park:

On the way to a rich neighborhood south of downtown, I found that the Berkeley Playhouse has found one social justice cause to elevate above all others:

A clothing store:

A couple of miscellaneous houses:

A $3 million house features Black Lives Matter sign and alarm system signs on the front fence, plus a car sticker advertising the Black-free private school to which the kids are sent at a cost of $40,000 per year per child:

I Ubered back to San Francisco with a driver who lived in Oakland and said how happy he was that Sheng Thao, the mayor of Oakland, had recently been recalled.

Our stroll to the first morning of work in San Francisco included the usual sights, e.g., a homeless encampment in the same frame as a self-driving Waymo:

Also, a smashed office building glass door:

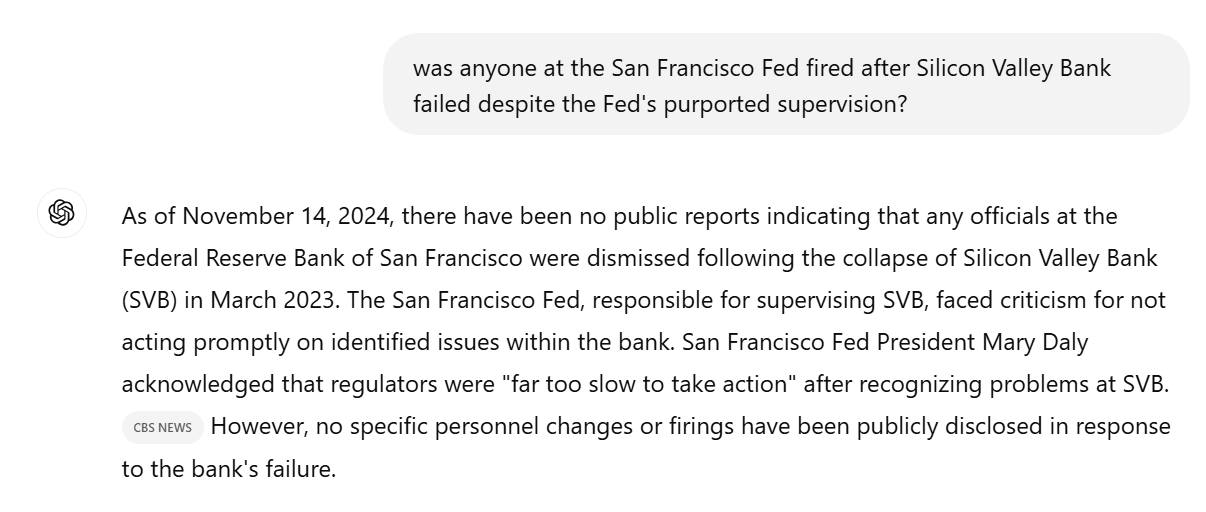

It also took us past a Silicon Valley Bank “Experience Center” and the San Francisco Federal Reserve Bank, notable for supervising SVB right until the bank was seized by regulators in March 2023.

According to ChatGPT, nobody at the San Francisco Fed was fired as a result of this spectacular immolation of taxpayer dollars (somewhere between $15 and $25 billion; the government pretends that didn’t do the bailout with peasant dollars because it made other banks pay, but of course the other banks are where peasants keep their money).

[Mary C.] Daly, who is openly gay, will become the third woman among the 12 presidents of the Fed’s regional banks. As a senior executive at the San Francisco Fed, she has been a leading voice for addressing what she has described as a “diversity crisis” in the economics profession and at the Federal Reserve. At the San Francisco Fed, she pushed successfully to balance the hiring of male and female research assistants.

Her online biography was updated June 2024 and makes no mention of her role in the SVB collapse.

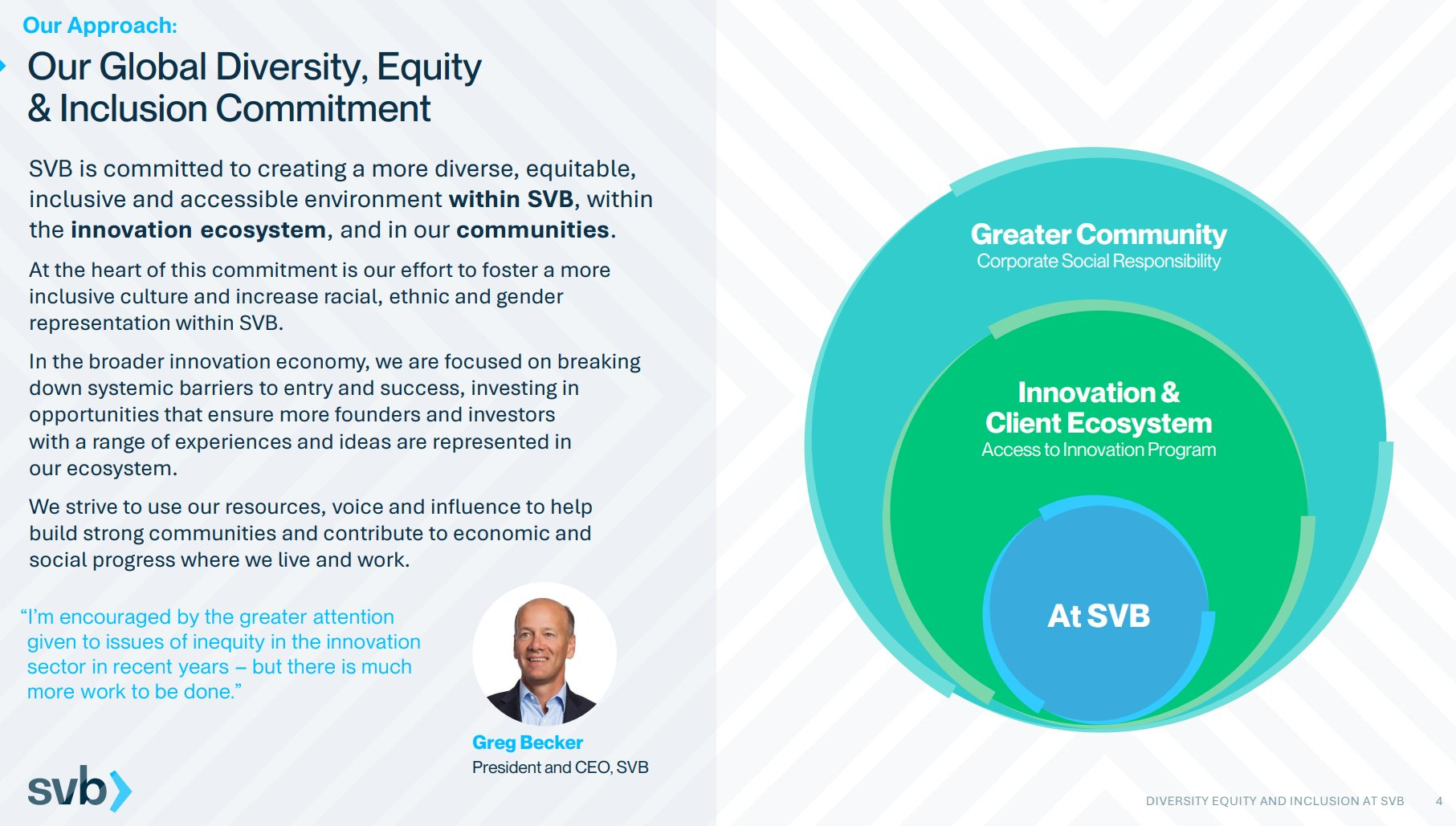

Incredibly, the bank still operates as SVB, though it is now a division of a North Carolina-based bank. SVB still has its DEI presentation online, updated a few months before the bank failed.

If not for the regulatory seizure they would have put 100 percent of employees through DEI training by now. The 5 percent quota for Black leaders didn’t go into effect until 2025:

Circling back to the life of an expert witness, here’s the view of the Ferry Building from the conference room where I was imprisoned:

In response to a reader question about whether ChatGPT can be trusted, Perplexity.ai’s answer:

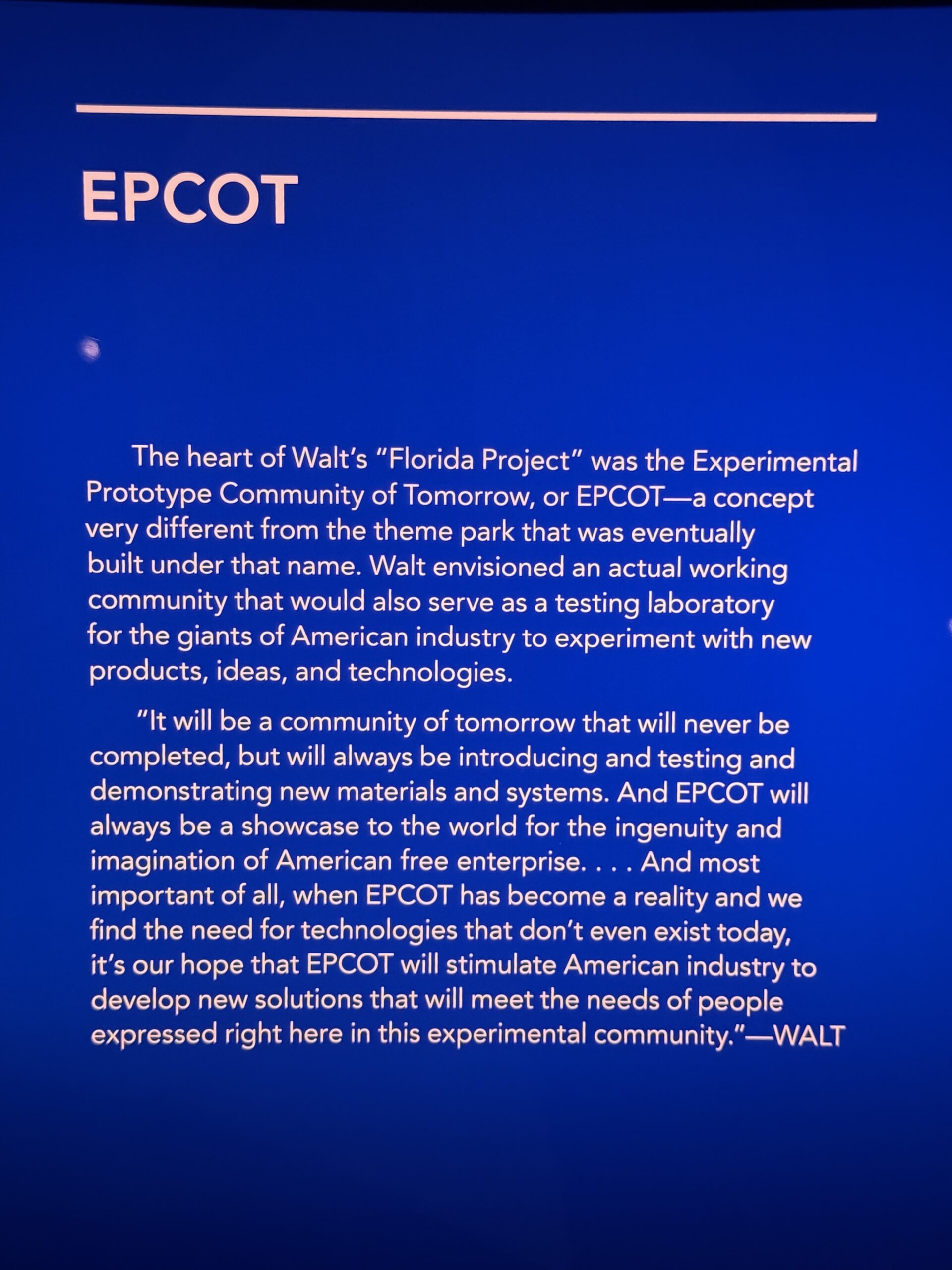

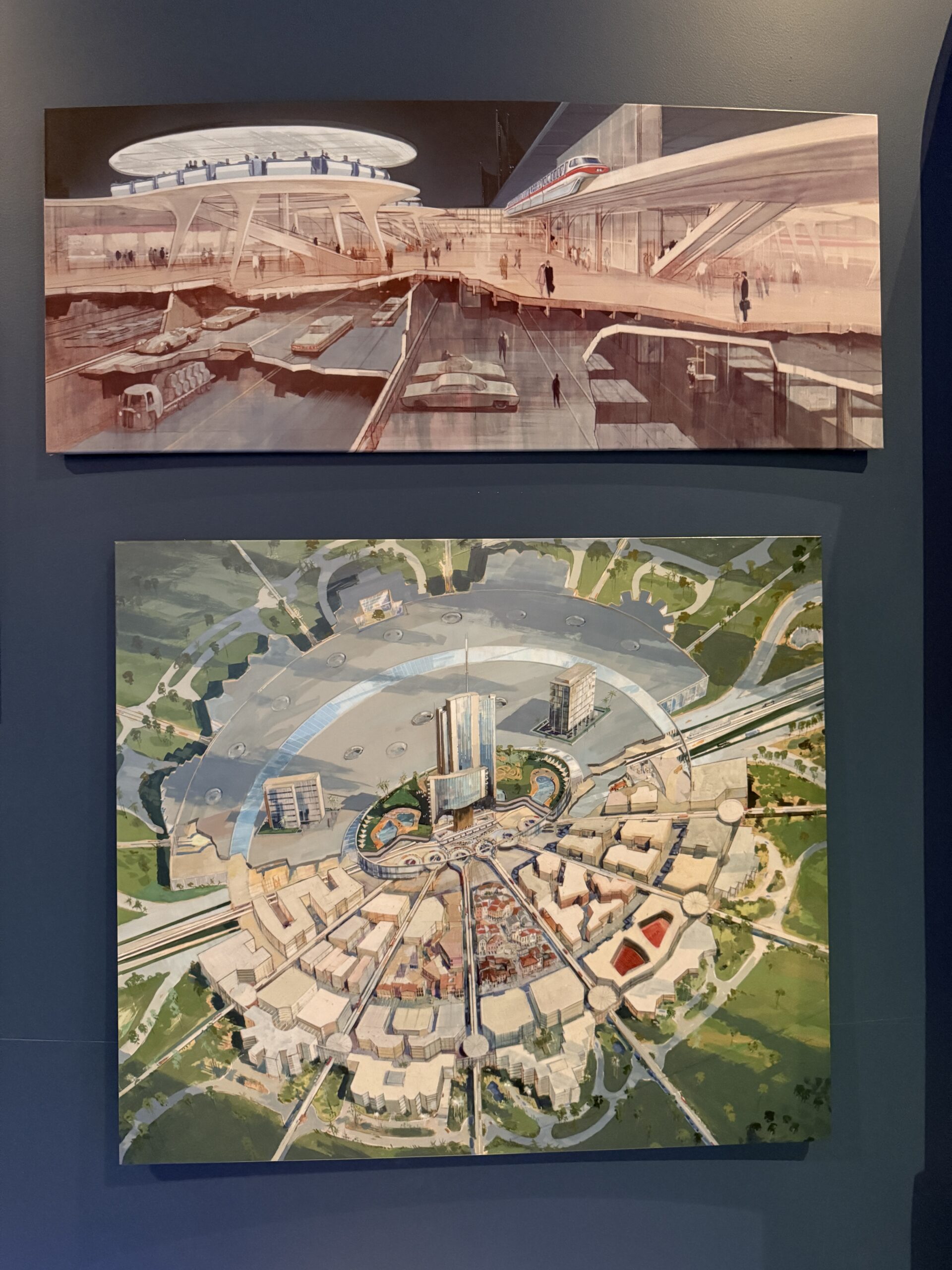

I finally made it to the Walt Disney Family Museum, smack in the center of San Francisco’s Presidio. Why is it in San Francisco when almost everything that Disney did was in Los Angeles or Orlando? Disney’s only child, Diane Disney Miller (mother of 7!), moved to the Bay Area in the 1980s.

I recommend that you have your Uber or Waymo drop you off at the top of Andy Goldsworthy’s Wood Line. You can then walk downhill through the Wood Line to the Yoda Fountain and from there it is an easy walk to the museum (arrive at the Wood Line about 40 minutes before your timed ticket to the museum).

Lucasfilm is headquartered in the Presidio and everyone is welcome to look at the Yoda fountain. Sadly, it is not inscribed “No, Try Not. Do or Do Not, There Is No Try.”

The museum is in the middle of the Parade Ground:

Getting into the museum costs $25 per adult or is free for those wise enough to refrain from work: an SF resident “receiving Medi-Cal and food assistance can redeem free general admission for themselves and up to three additional guests” (source). I got two free tickets via my Ringling Museum membership.

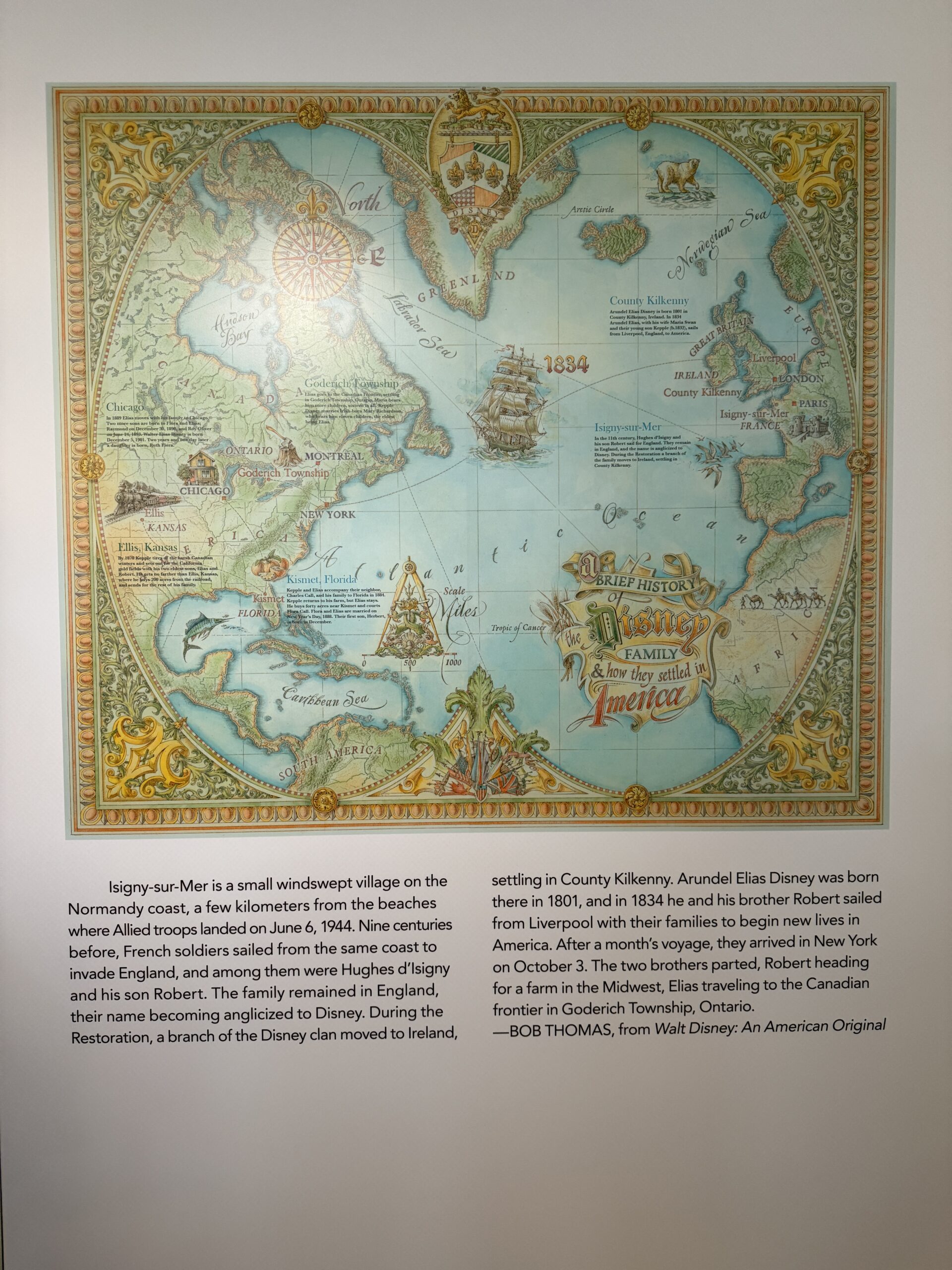

Back in the 11th century, it seems, Hughes d’Isigny and son Robert moved from France to England and that’s where d’Isigny was anglicized into Disney. The family moved to North America in 1834 (bouncing around Canada, Florida (Orange County, near today’s Walt Disney World), Chicago, and Missouri):

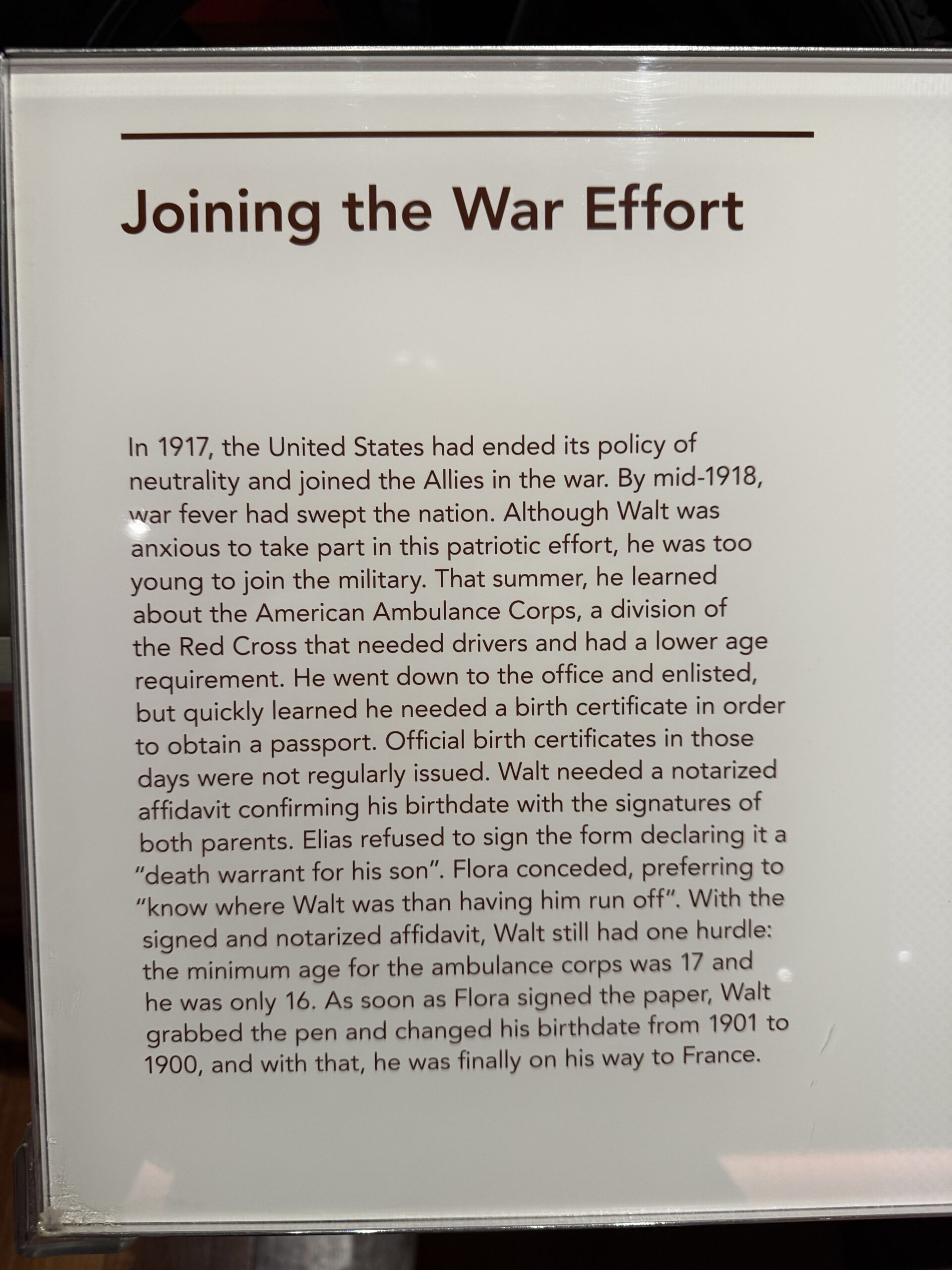

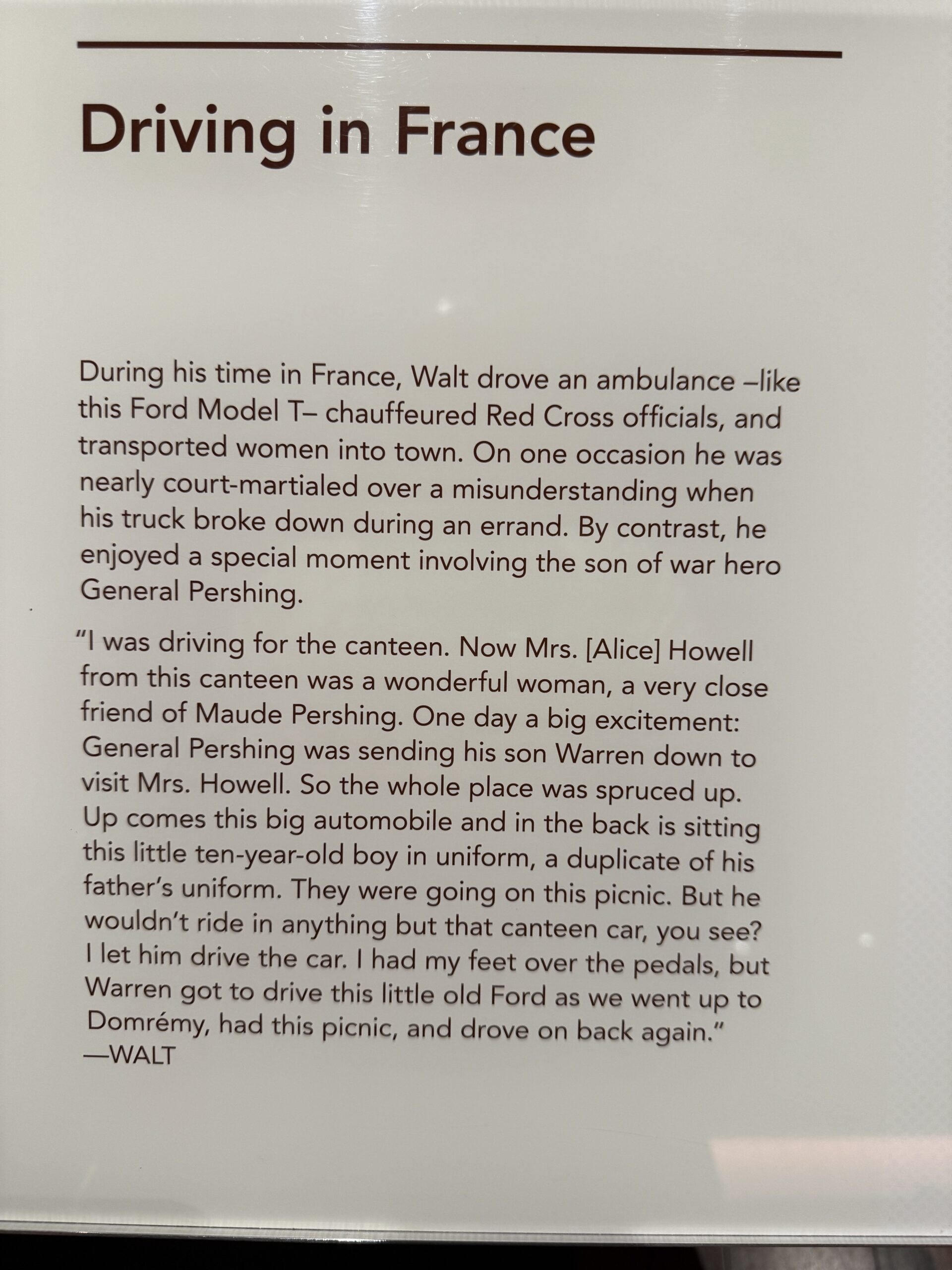

Disney was an ambulance driver in World War I and managed to refrain from writing a tedious novel about the experience:

Disney’s first animated movie company, whose techniques were informed by Animated Cartoons (E.G. Lutz) went bankrupt:

His second company, which featured Oswald the Lucky Rabbit, also essentially failed due to some badly drafted contracts with Universal Pictures, which took over the character. Walt Disney had to #persist through two business failures, essentially, before he could begin building the Mickey-based Disney that we know and love today. The museum does a great job of making it clear just how many false starts there were in what might seem like a steady inexorable rise to greatness.

Speaking of failures, both visitors and staff at the museum refused to accept the idea that simple masks had in any way failed to stop the spread of an aerosol respiratory virus (note also the spectacular autofocus failure of the iPhone 16 Pro Max just when I was relying on it to show that the young slender staffer chose to wear a mask while the older staffer did not):

Visitors are given a trigger warning, though it was unclear to me what the triggering content might be. Certainly, Song of the South clips were not played.

The trigger warning was repeated before a few signs that mentioned Squaw Valley Ski Resort, home of the 1960 Winter Olympics in which Disney provided some entertainment (in a victory for Native Americans, the resort was renamed Palisades Tahoe, thus removing all references to the existence of Native Americans other than the word “Tahoe” itself, which is a corruption of a Washo word for “lake”).

Nerds will appreciate the preserved multiplane camera, in which cels could be placed at different distances from the lens for more realistic perspective during camera motion.

What else is nearby? The Officers’ Club is now a free museum with a permanent exhibit devoted to the Native Americans who apparently won’t be getting any of their land back:

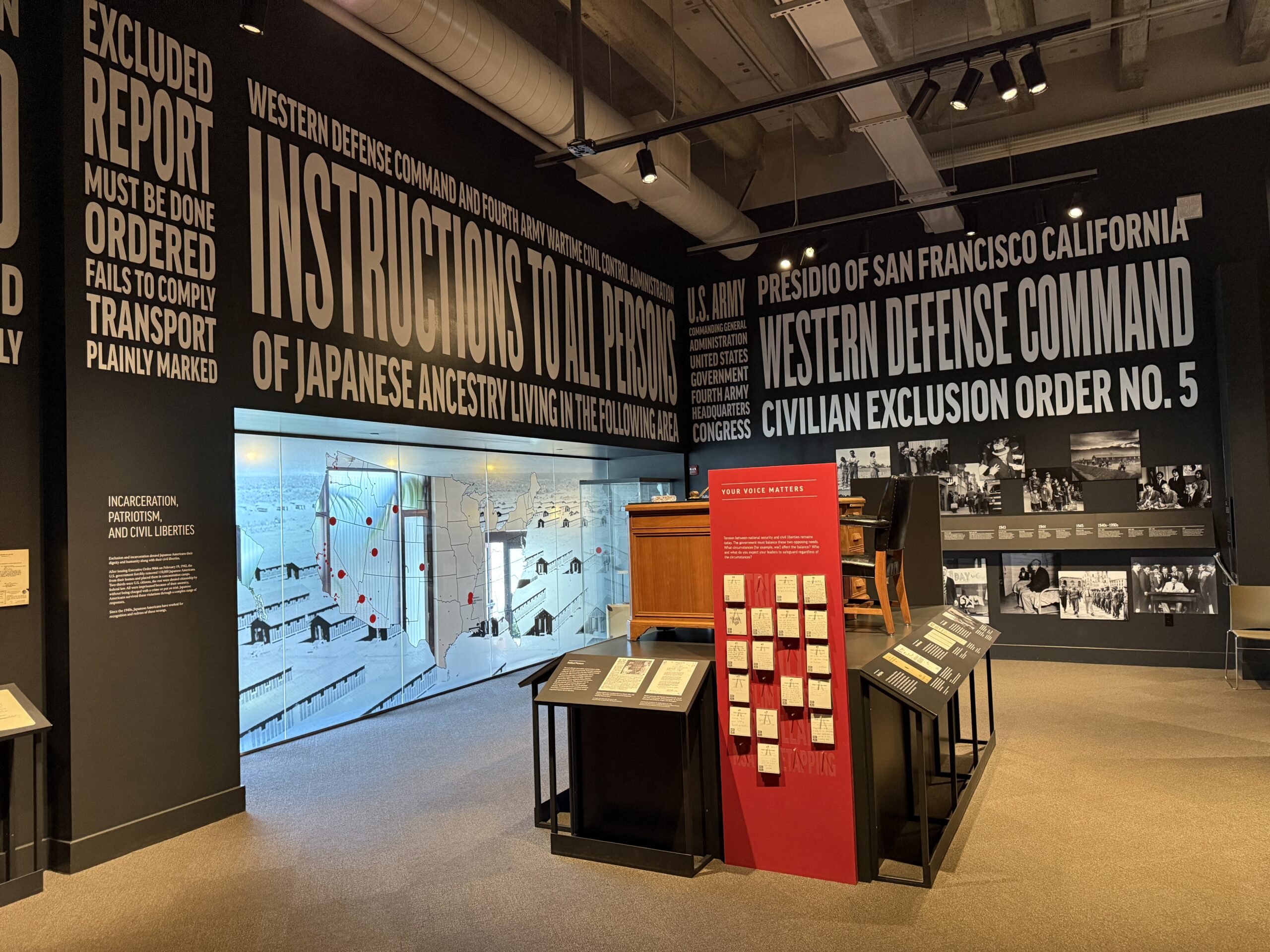

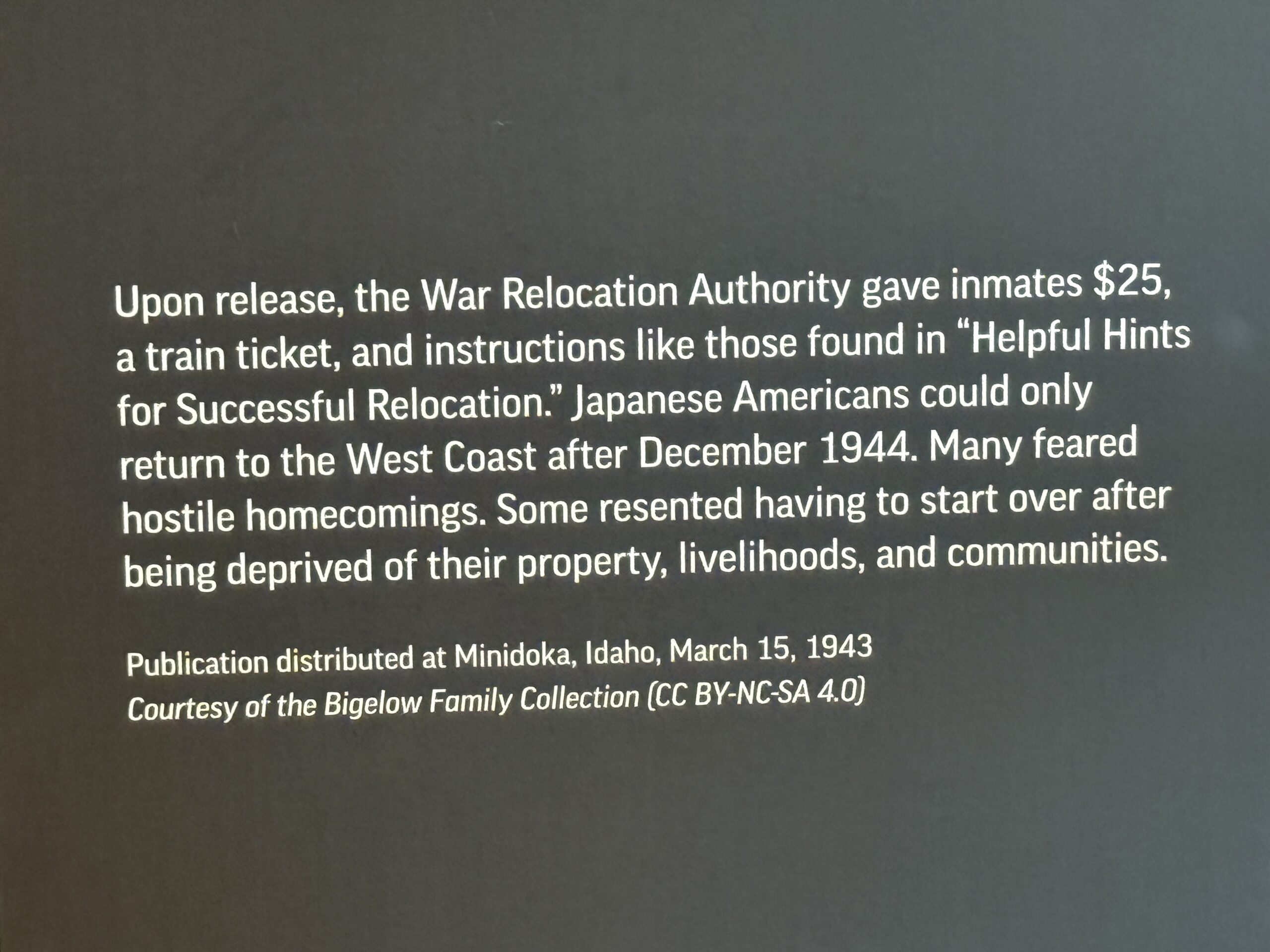

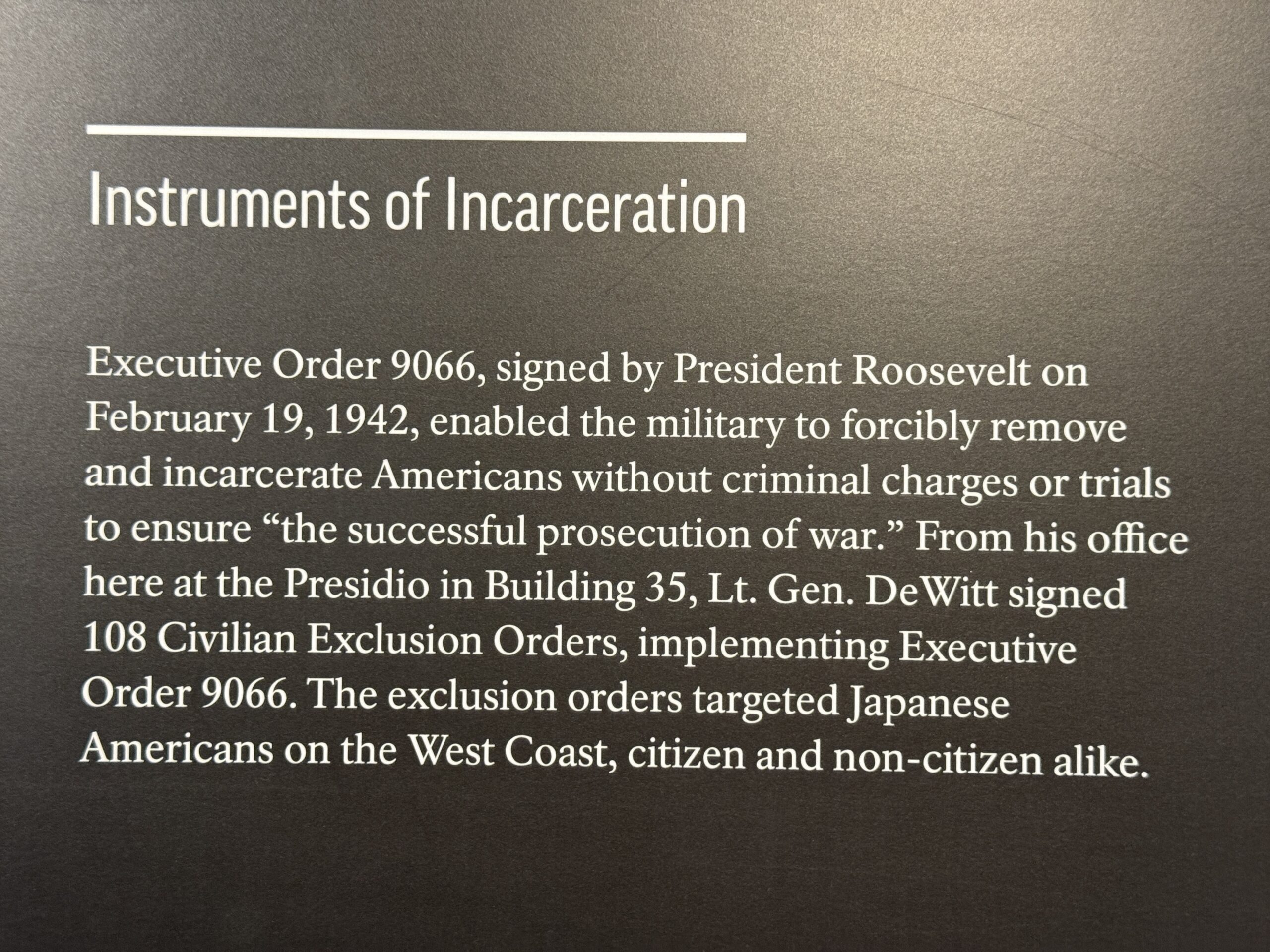

A temporary exhibit is up right now relating to the setting aside of the U.S. Constitution because politicians and bureaucrats declared an emergency and decided that it would be expedient to intern Japanese-Americans:

(Similar reasoning, of course, was applied in 2020 when the First Amendment right to assemble was tossed in favor of Science-dictated lockdowns.)

We didn’t leave by Waymo in an exciting rush of spinning LIDAR, but it would have been nice to!

Note Alcatraz in the background. If the U.S. government ever decides that it needs to reduce the amount of deficit spending/money printing that it does on the Cheat Our Way to Prosperity Plan maybe this island can be sold to a mid-level NVIDIA employee for $1 billion for use as a private home.

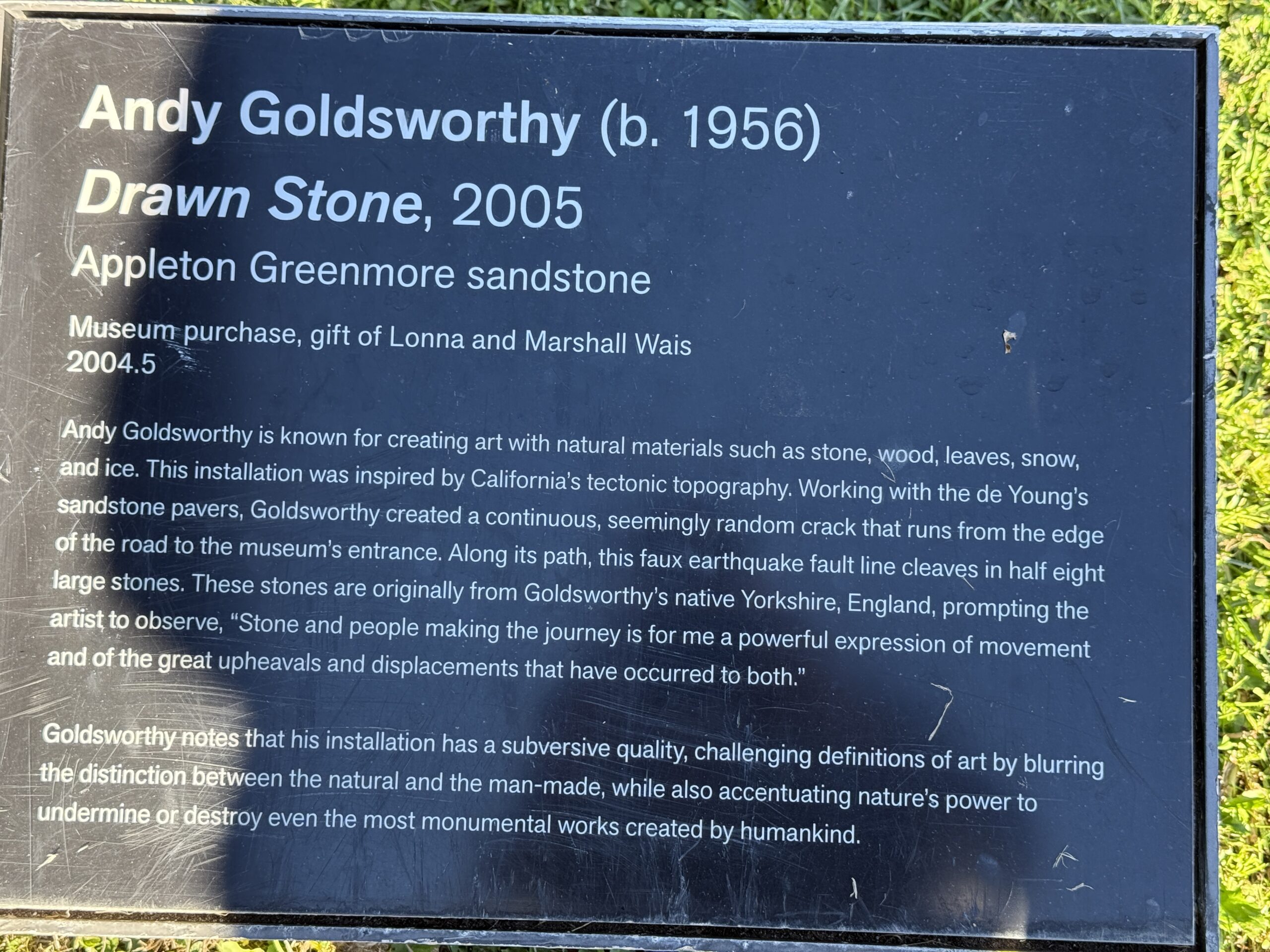

I hadn’t ever noticed this before, but on a recent visit to the de Young Museum in San Francisco, I noticed that they’d purchased Andy Goldsworthy’s crack for what was, no doubt, a significant sum:

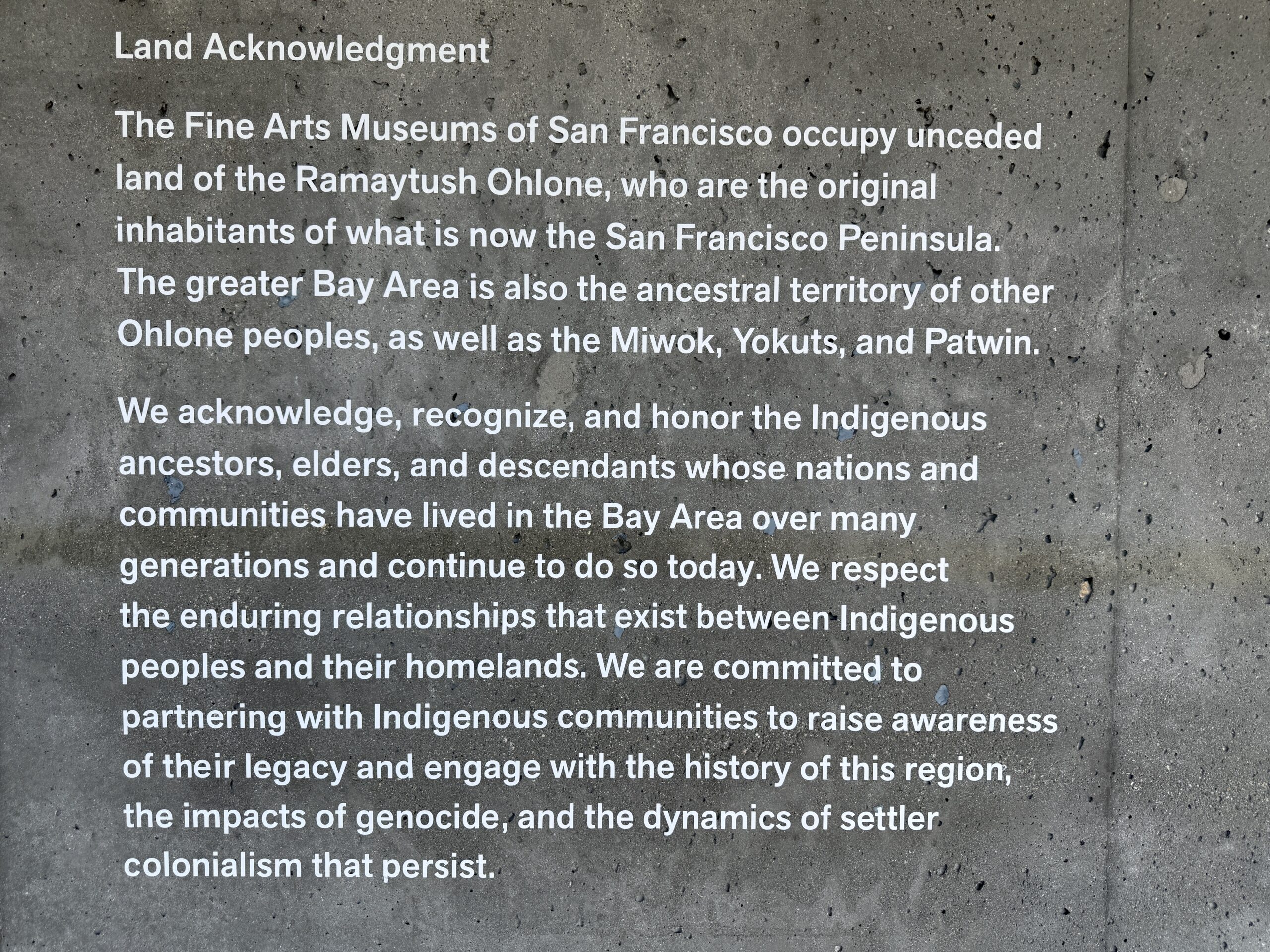

Speaking of the museum, they acknowledge that they’re on someone else’s land:

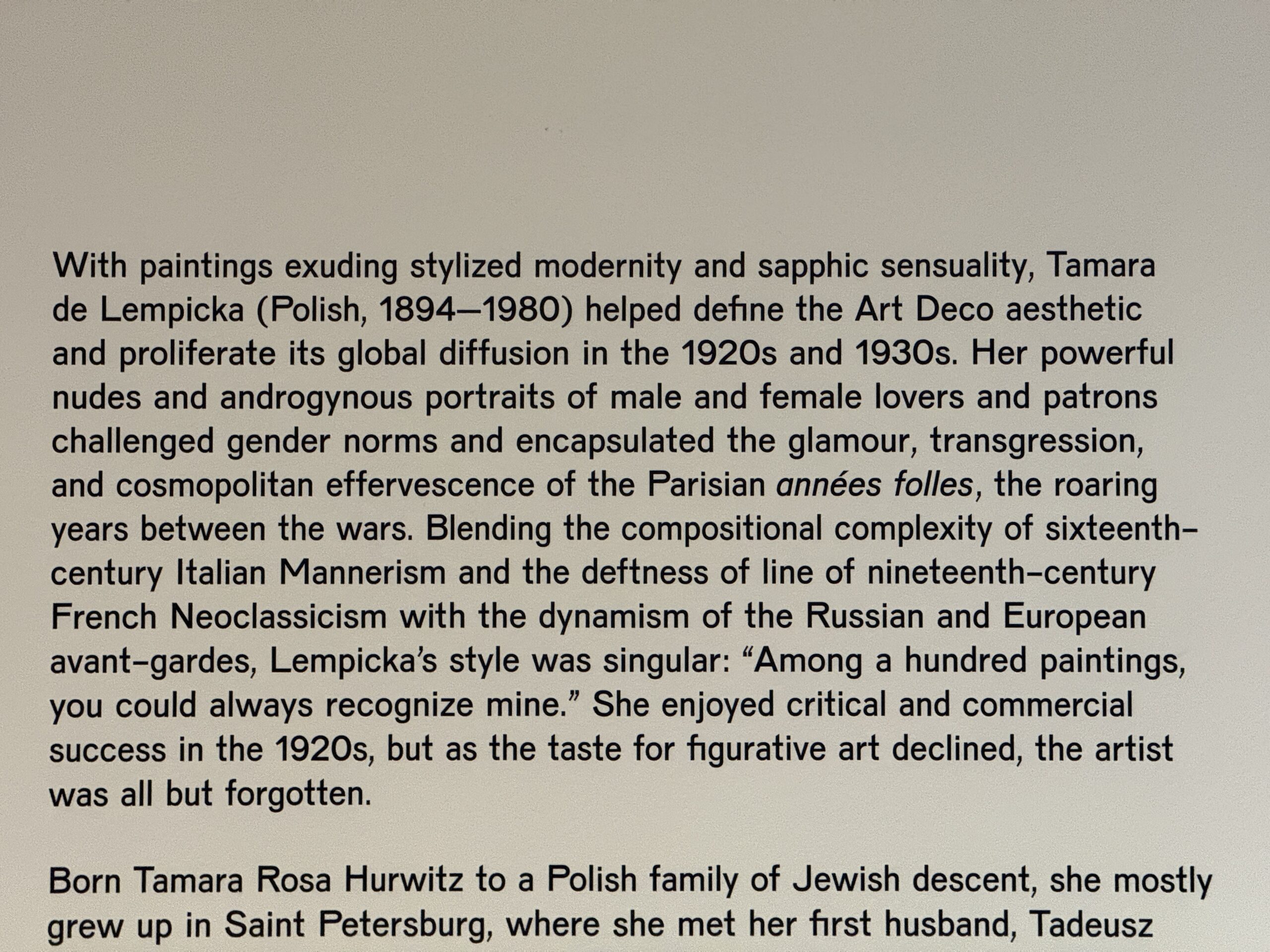

Native Americans are welcome to return to their land for $20 per person, $30 for parking, and $35 for the special exhibit of 100-year-old work that “challenged gender norms”:

It was great to see the Pavia tapestries again (see Could robots weave better tapestries than humans ever have?), especially with the added bonus of Californians wearing their 3-cent surgical masks against an aerosol virus (one of them with the mask over a beard):

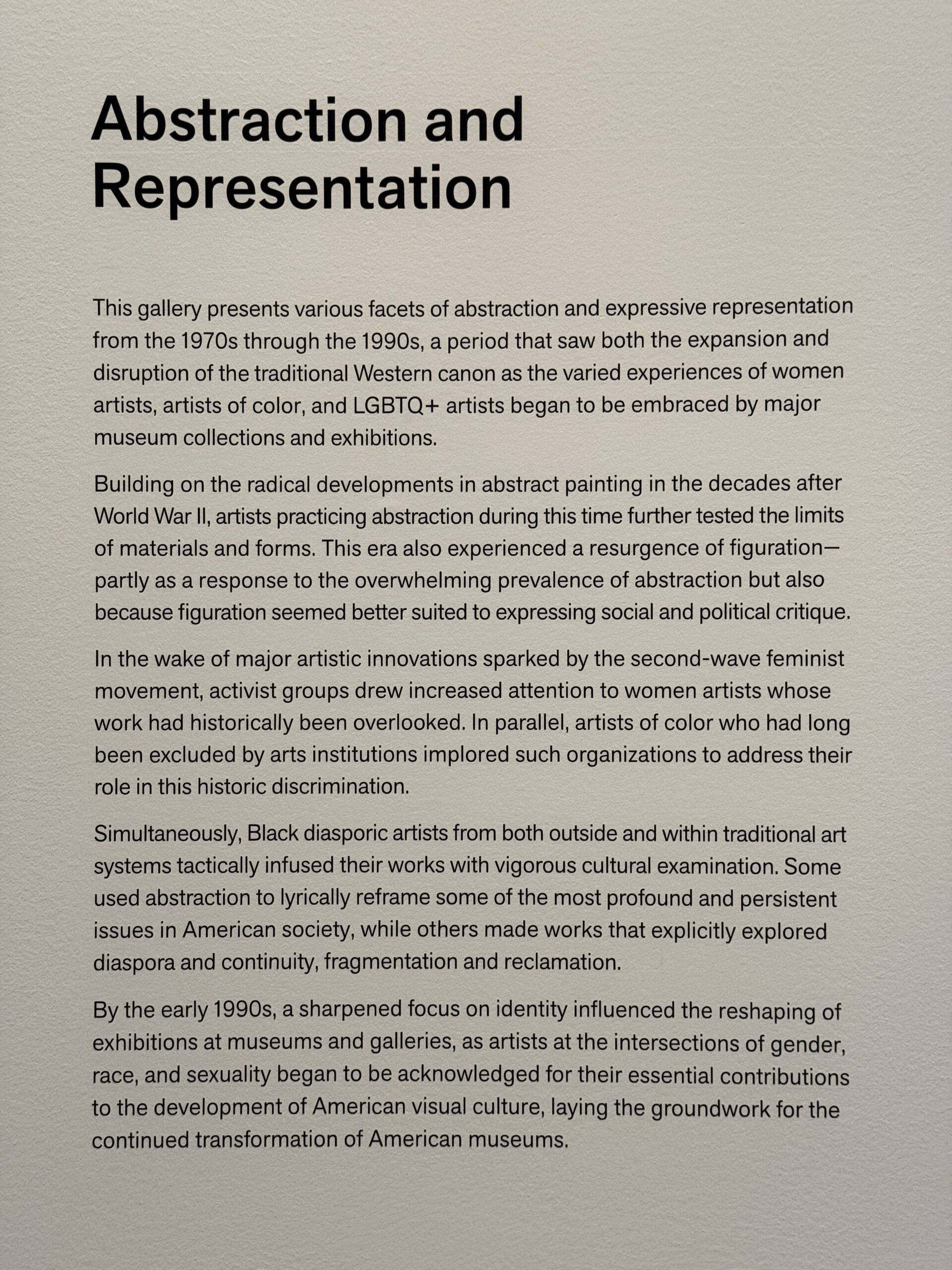

The museum reminds us that it is critical to consider the victimhood category of an artist (“women”, “of color”, and “LGBTQ+” are the choices):

Then they organize an activity centered around a sculpture by Louise Nevelson, who rejected and resisted being categorized as a “woman artist” (“I’m not a feminist. I’m an artist who happens to be a woman.”).

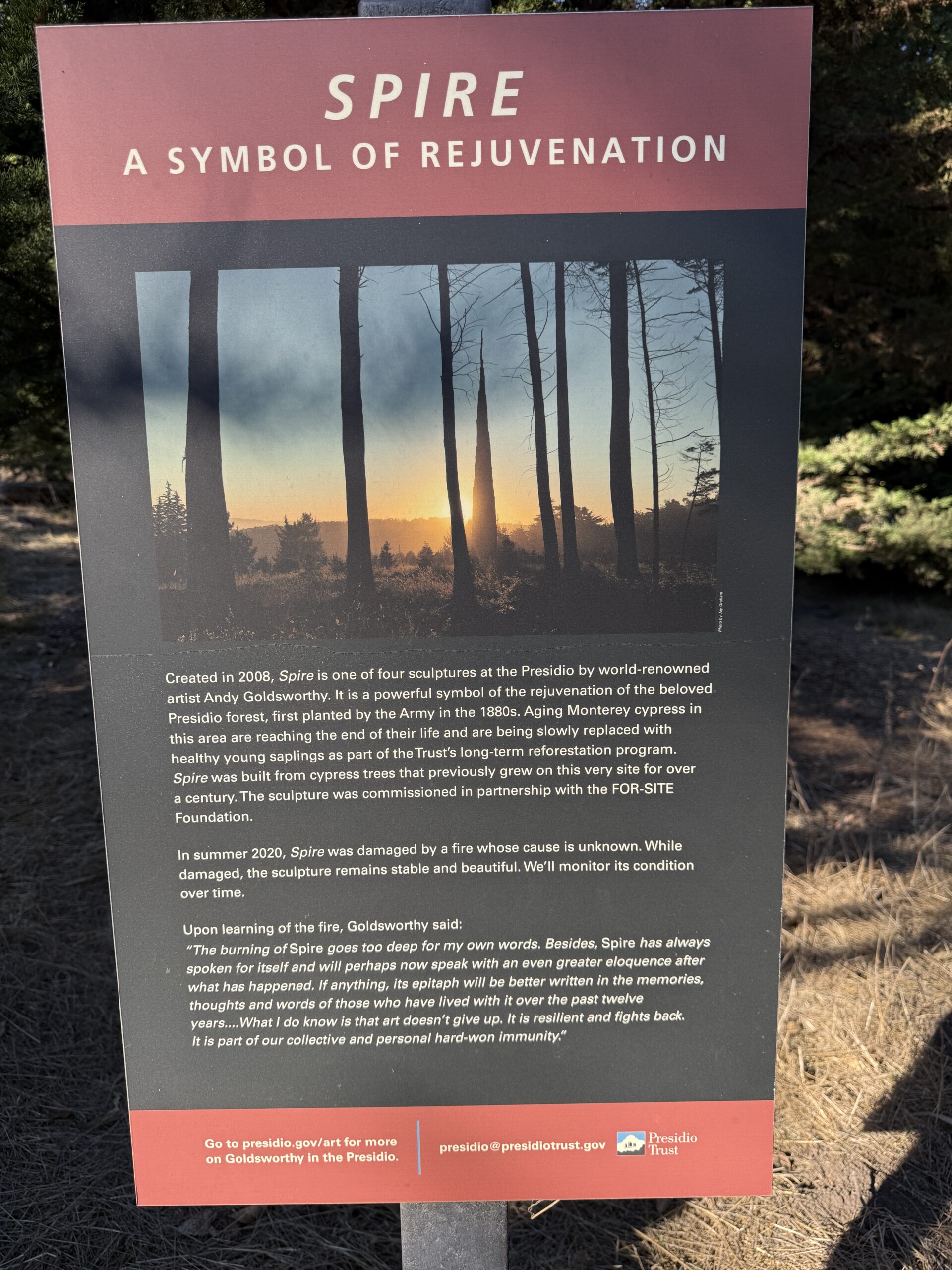

On a recent trip to San Francisco, a local friend took us to Andy Goldsworthy’s Spire in the Presidio:

We had just come from a parking lot where quite a few cars were virtuously marked:

Our friend said “What we need is a drone to paint the Spire sculpture in the Palestinian flag colors.”

Let’s suppose that residents of the U.S. with a lot of community spirit did build some drones that could paint the sides of building with huge messages such as “From the River to the Sea, Palestine will be Free”, “#Resist”, and “Trump is a Nazi.” It is much easier to build a spray-painting drone than a scrubbing drone, I think. How could cities and building owners defend against virtuous painting drone owners/operators?

(Though moderately rich by average American standards and blessed with a garage at home, our friend who lives in SF drives a 22-year-old car for fear that anything nicer will attract thieves.)

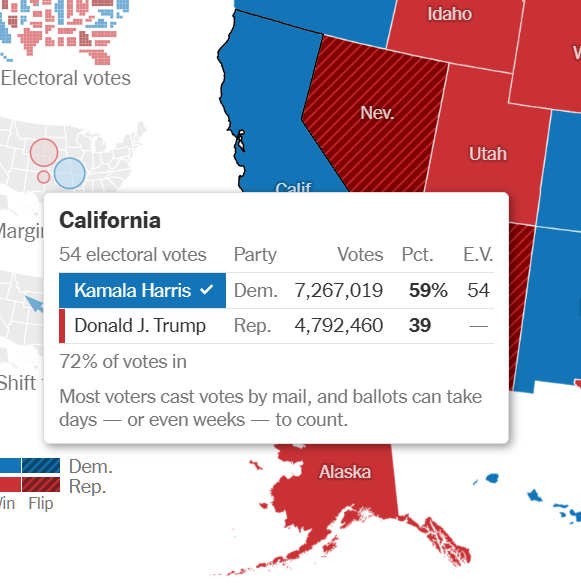

It’s five full days (about 120 hours) after the Election 2024 Nakba. The folks in California who say that they know how governments should operate have counted 72 percent of their presidential ballots (New York Times):

Let’s compare this to the numbers in Power restoration after Hurricane Milton. Recall that Milton was a Category 3 storm that hit Sarasota, St. Pete, and Tampa, knocking out power to 4 million “customers” (a household of 3 people would be just one customer). I didn’t stay organized to capture a number for how many were still out exactly five days after the hurricane made landfall, but four days afterward roughly 500,000 customers were still out, which means that more than 87 percent had been restored. Six days following landfall, roughly 190,000 customers were out from the original 4 million affected.

So.. Ron DeSantis-led Florida restored power after a Category 3 hurricane at a much faster pace than California has been able to count votes. (Florida also did count votes, but there aren’t any interesting statistics from that process because it took just a few hours.)

A few more photos of how the folks who say that they want to end economic inequality are living, from a Robinson R44 flight out of KSNA (Orange County Airport) up to Long Beach and then back down the coast to Dana Point before returning to refuel and then land (with a certain amount of fear and terror) on a rooftop adjacent to the airport.

I’d love to know what drugs the architect of the roof in the last photo was on!

If we ignore the water shortages, California does seem like a great place for golf. It doesn’t matter how cold the water is if the plan is to use the water only for decoration while trying to hit some balls:

Here are some folks who’ve probably figured out a way to avoid whatever new taxes Gavin Newsom might cook up (183 days/year in the Jackson, Wyoming house, for example?):

Unfortunate (termite treatment tent) and fortunate (personal oceanfront golf course?):

A lawn bowling court for communities of color?

Some hotels that could be turned into migrant shelters if Californians were willing to deliver on what they say are human rights:

Housing is a human right, but it’s also a human right to have a beach house and a yacht, which is why tax rates on California’s wealthy elites can’t be raised to pay for the housing that is supposedly a human right:

As in the previous post, the equipment used for the above photos is simple: Robinson R44, left front door removed, iPhone 14 Pro Max.

Let’s also have a look at some other photos from the trip. I saw three CyberTrucks in various parking lots in a 12-hour period:

For Californians to save the planet with these enormous vehicles will require the output of three continuously running steel mills.

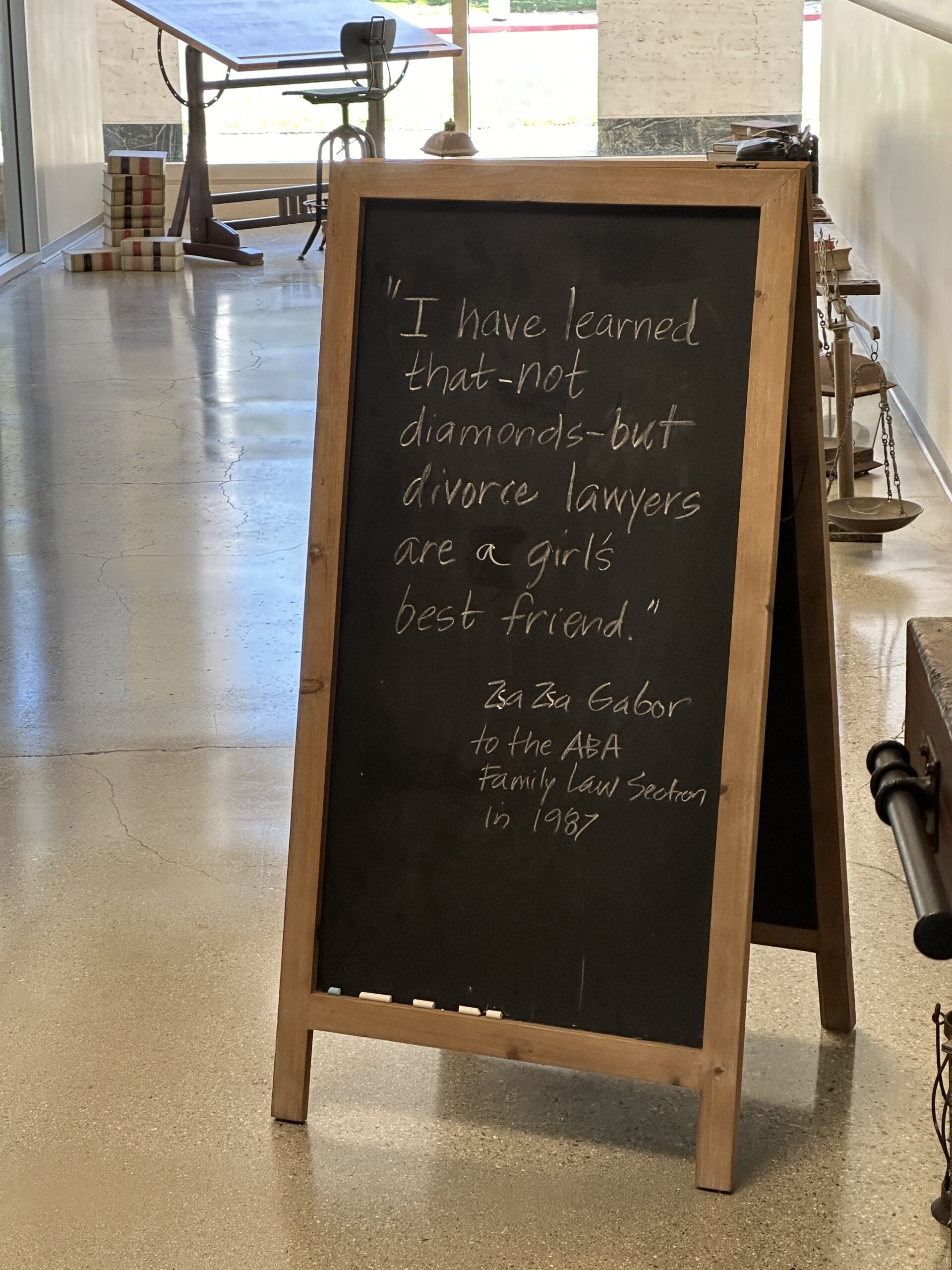

The most expensive space in the mostly-empty office building where I was working is rented by a divorce litigator:

CVS in Irvine has to keep the deodorant locked up:

At SNA on the way back to Florida, I found a Follower of Science wearing an N95 mask over a full beard, an always-delightful scene, albeit contrary to the 3M instructions:

What’s less than ideal about Vuichard, which results in recovery with remarkably little altitude loss? “Every other helicopter emergency procedure involves lowering collective,” responded my instructor, “so the Vuichard technique becomes an exception that is going to be tough to execute in a real-world emergency where you’re startled. Also, what if you’re settling with power because you don’t have enough power and you misidentify a vortex ring state? Then adding collective via Vuichard will immediately lead to blade stall.”

He explained that there have been at least a couple of fatal accidents during training in which the necessary counterintuitive heroism wasn’t summoned for the Vuichard technique. Thus, the new school is back to the old school.

(I have never personally gotten into vortex ring state (sometimes called “settling with power”) other than during my work as a flight instructor or while a student myself. It can be avoided by being careful during steep approaches, especially with respect to not doing a downwind steep approach.)

In addition to practicing emergencies, we managed to get in some flying up and down the coast. Here are a few snapshots.

An Nvidia branch office receptionist’s new weekend boat:

An oil platform off Long Beach cleverly disguised, when viewed from the water, as an island encircled by palm trees:

What your (3rd or 4th) house might look like if you and all of your friends and neighbors xpressed a passionate commitment to reducing economic inequality:

(All of the above photos were taken with an iPhone 14 Pro Max after removing the left front door of the helicopter.)

A portion of the closing ceremony is dedicated to the host city handover from Paris to Los Angeles, in which Paris Mayor Anne Hidalgo will give the Olympic flag to Los Angeles Mayor Karen Bass. … The [Olympics closing] ceremony will feature prominent performers representing California, a nod to the next host city. Rapper Snoop Dogg — who has become a fixture of this year’s Games — will play a role in the handover segment.

(Prejudice against women is so severe all over the world that the handover is from one mayor who identifies as a “woman” to another mayor who identifies as a “woman”?)

I’m a big fan of Snoop Dogg’s performance in Starsky & Hutch, but it seems that he has a colorful past.

From Rolling Stone, “Snoop Lion Opens Up About His Pimp Past”:

When Snoop Dogg called himself a “pimp” back in 2003, he wasn’t joking. “I put an organization together,” the rapper-turned Rasta artist Snoop Lion tells contributing editor Jonah Weiner in the new issue of Rolling Stone. “I did a Playboy tour, and I had a bus follow me with ten bitches on it. I could fire a bitch, fuck a bitch, get a new ho: It was my program. City to city, titty to titty, hotel room to hotel room, athlete to athlete, entertainer to entertainer.”

Unlike most pimps, Snoop says he let his women keep the money. “I’d act like I’d take the money from the bitch, but I’d let her have it,” he says. “It was never about the money; it was about the fascination of being a pimp . . . As a kid I dreamed of being a pimp, I dreamed of having cars and clothes and bitches to match. I said, ‘Fuck it – I’m finna do it.’”

The above statements get bowdlerized in OregonLive:

The rapper-turned-Rasta artist formerly known as Snoop Dogg tells Rolling Stone he fulfilled a life’s ambition by becoming a pimp — yes, literally — a decade ago.

“I’d act like I’d take the money from the (prostitute), but I’d let her have it,” he says. “It was never about the money; it was about the fascination of being a pimp. … As a kid I dreamed of being a pimp.”

It’s an interesting reflection of current American social mores that Snoop Dogg’s involvement in the world’s oldest profession didn’t motivated Los Angeles officials to find a somewhat less colorful representative.

Readers: What were your favorite Olympics sports/moments this year and what should we watch on Peacock Premium Plus before we cancel the subscription that we started a couple of weeks ago? Our kids so far have enjoyed rugby, equestrian eventing (running horses through the country), breaking, synchronized diving, BMX, volleyball, tennis (Djokovic!), table tennis, and the transition from swimming to biking in the triathlon.