Reason to love Legacy Media #479… we are informed that

Los Angeles is peaceful and therefore the (defunded?) LA police did not require any assistance

Los Angeles cannot be safely traversed by a group of soldiers clad in body armor and armed with M4 rifles (maybe they could be safe in this peaceful city if enclosed within an M1 Abrams tank or Bradley Fighting Vehicle?)

From the Financial Times:

A growing number of military veterans and serving officers have spoken out against President Trump’s decision to deploy marines and National Guard troops to LA, calling it a misuse of executive power that puts soldiers’ lives at risk

A growing number of military veterans and serving officers have spoken out against President Trump’s decision to deploy marines and National Guard troops to LA, calling it a misuse of executive power that puts soldiers’ lives at risk. https://t.co/flxk64rh8mpic.twitter.com/ku5DeYkUDY

Greta Thunberg is back in Europe after her heroic aid trip to Gaza. There are some open questions regarding this trip:

why does someone who says that the Earth is being destroyed by humans choose the Palestinians, close to world #1 in fertility and population growth, as her model society? Just imagine the CO2 output if every group of humans on this planet had 4-6 children per family, as is common among Palestinians entitled to UNRWA aid (i.e., free food, health care, education, etc., even if nobody ever works at any job other than Hamas or Palestinian Islamic Jihad soldier)

why was a female do-gooder visiting a group of Muslims (the noble Gazans) not wearing hijab and/or burqa?

I’m not holding my breath for answers to the above, but now that we apparently need not worry about climate change, perhaps the highest and best use for Greta Thunberg would be a diesel-fueled yacht trip to deliver aid to the Californians who are currently #resisting an occupying military.

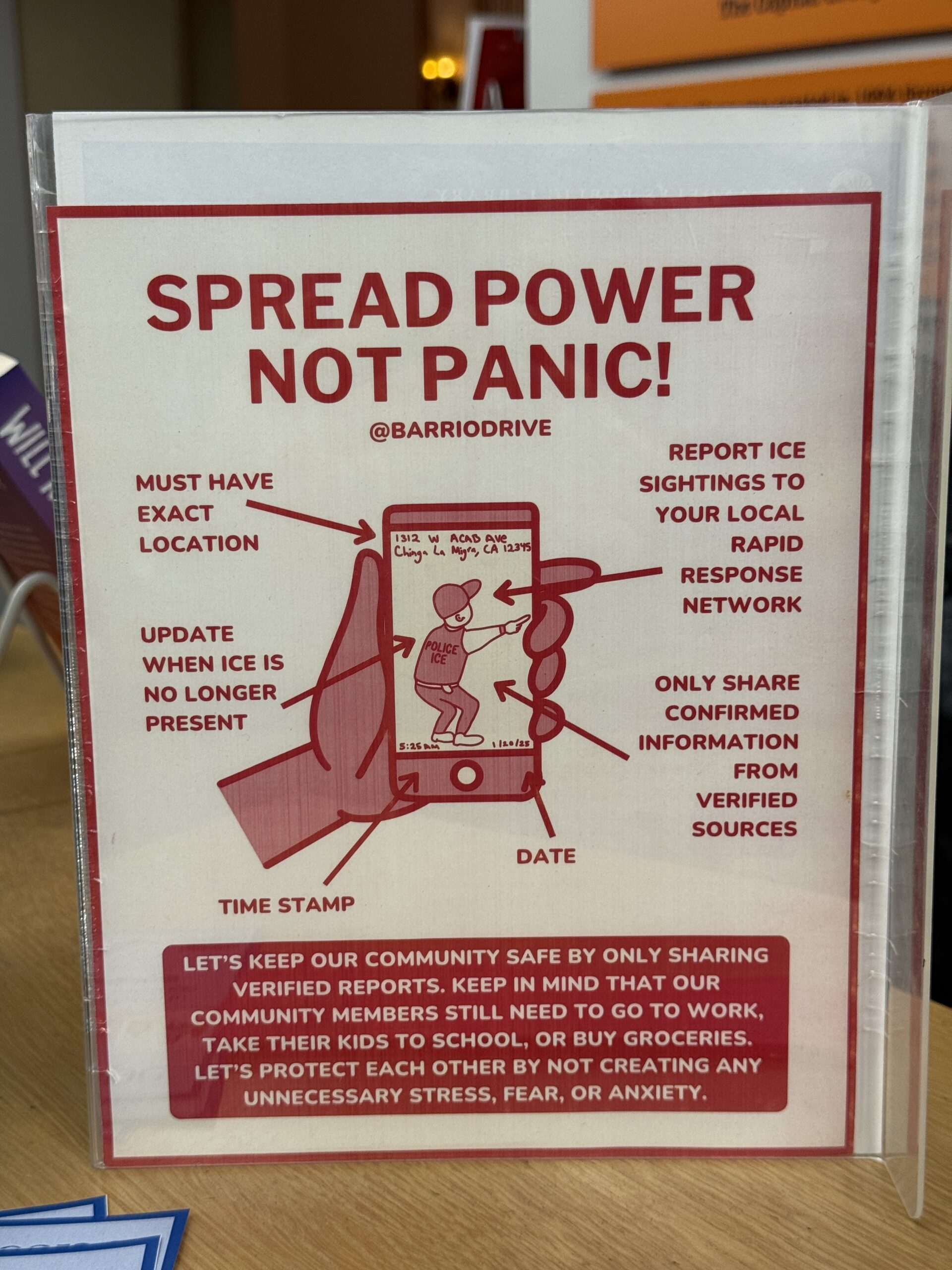

Let’s look at some photos from my recent visit to the teen section of the central Los Angeles Public Library, which officially teaches cooperation via smartphone to evade ICE. An important way to “keep our community safe” is to prevent federal government workers from doing their jobs:

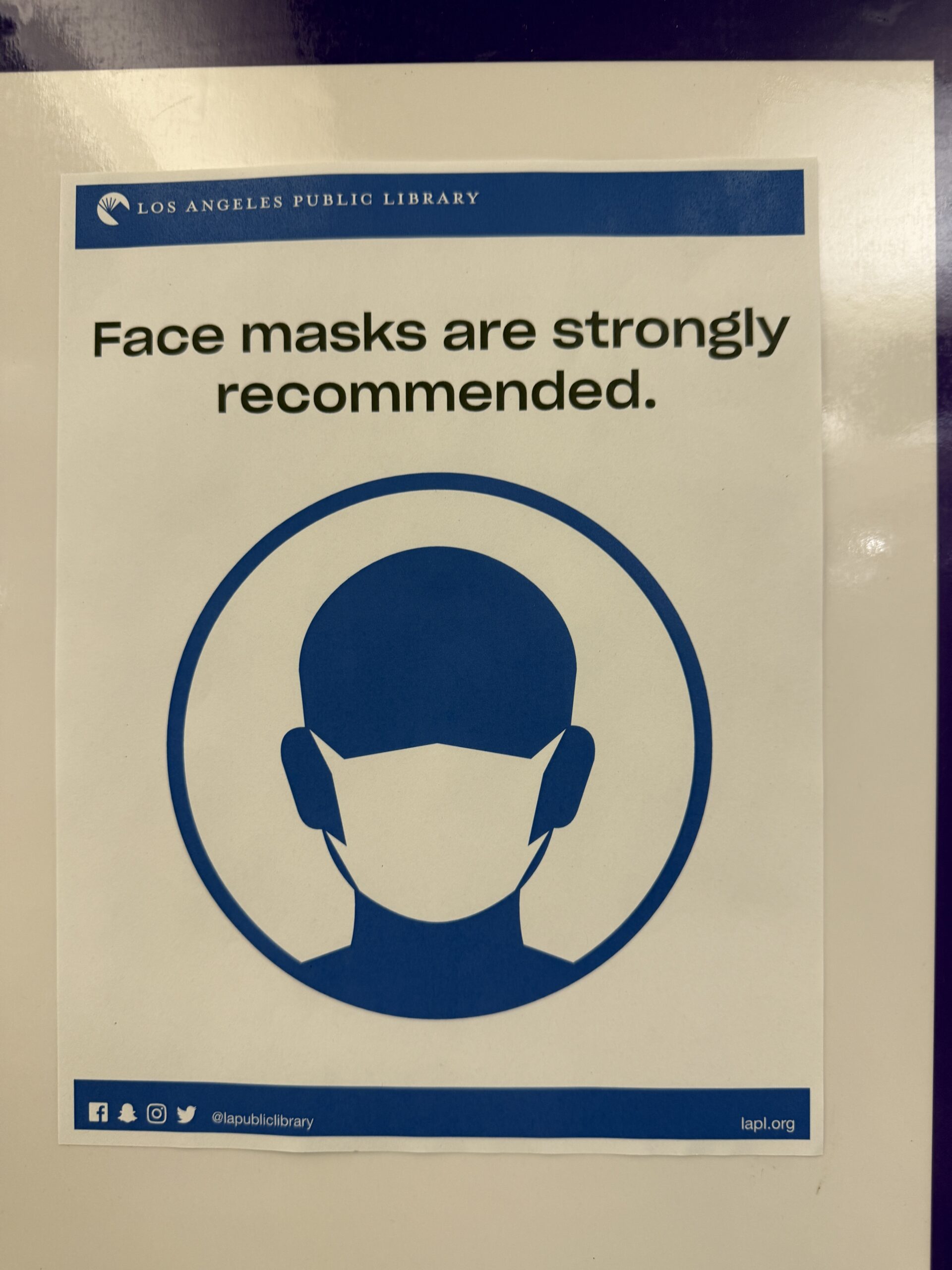

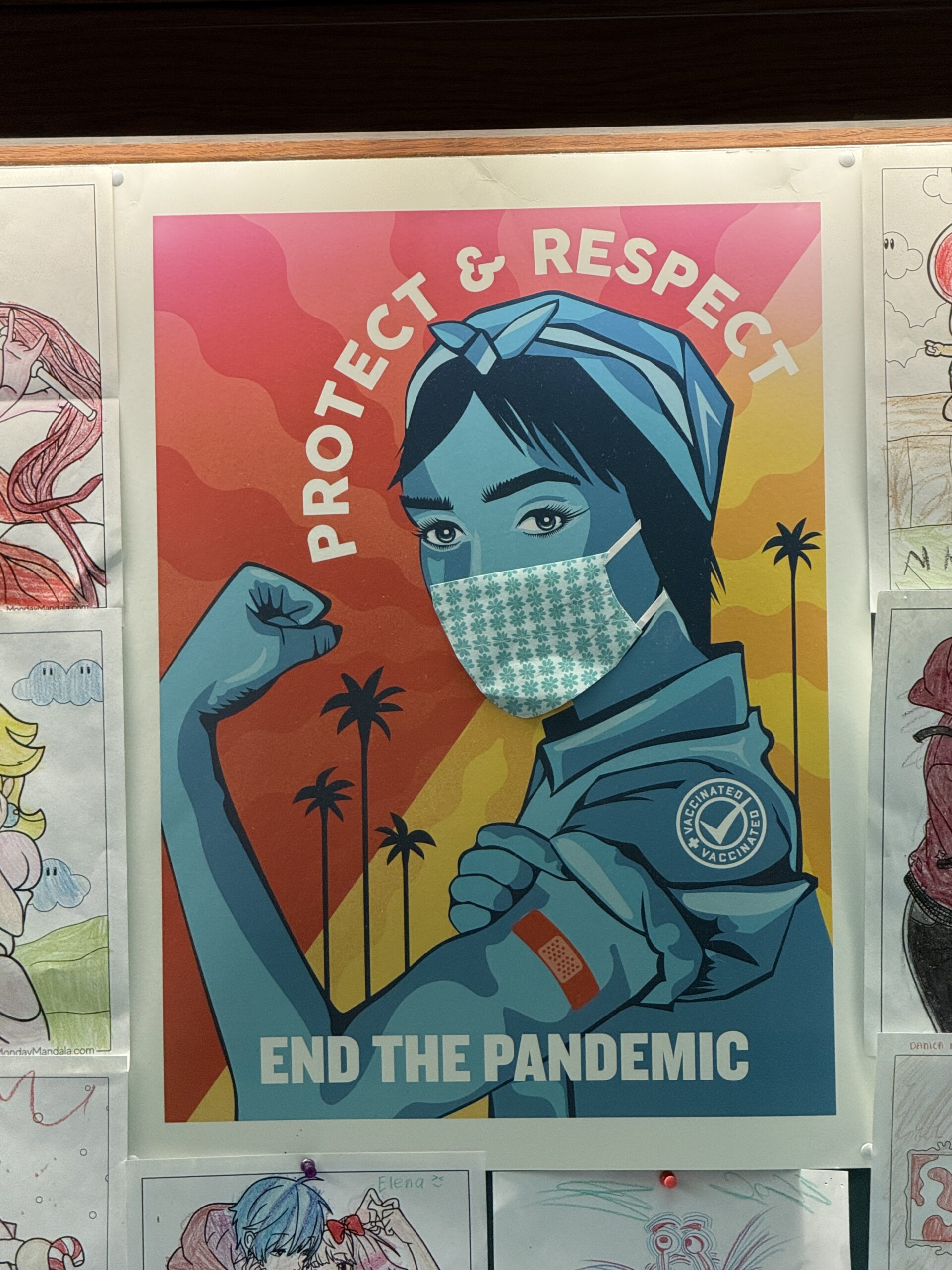

The #Science section in which we learn that SARS-CoV-2 is no match for teenagers wearing masks and voluntarily receiving an injection of an experimental vaccine that is reserved for those 75 years and older in the UK:

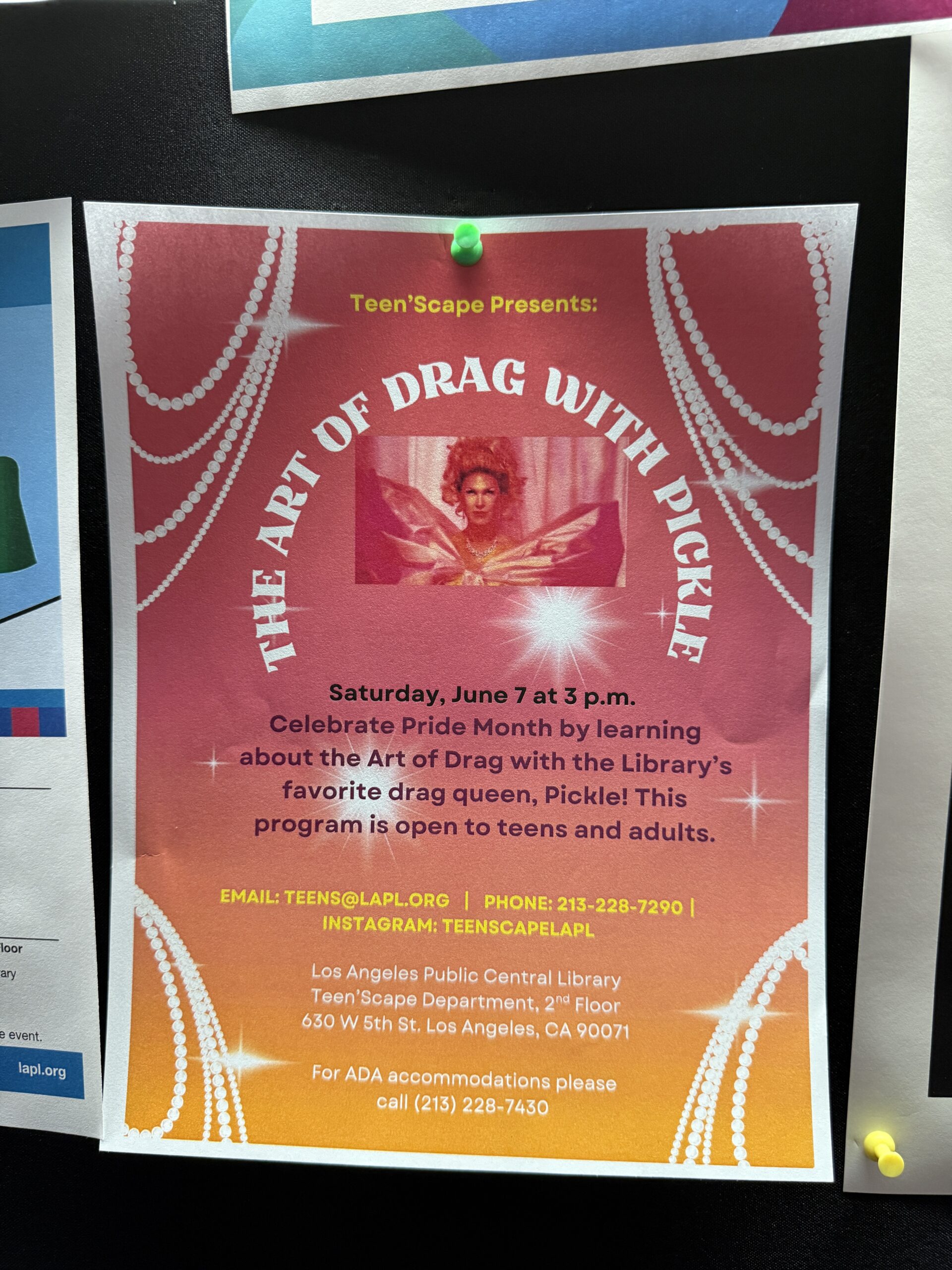

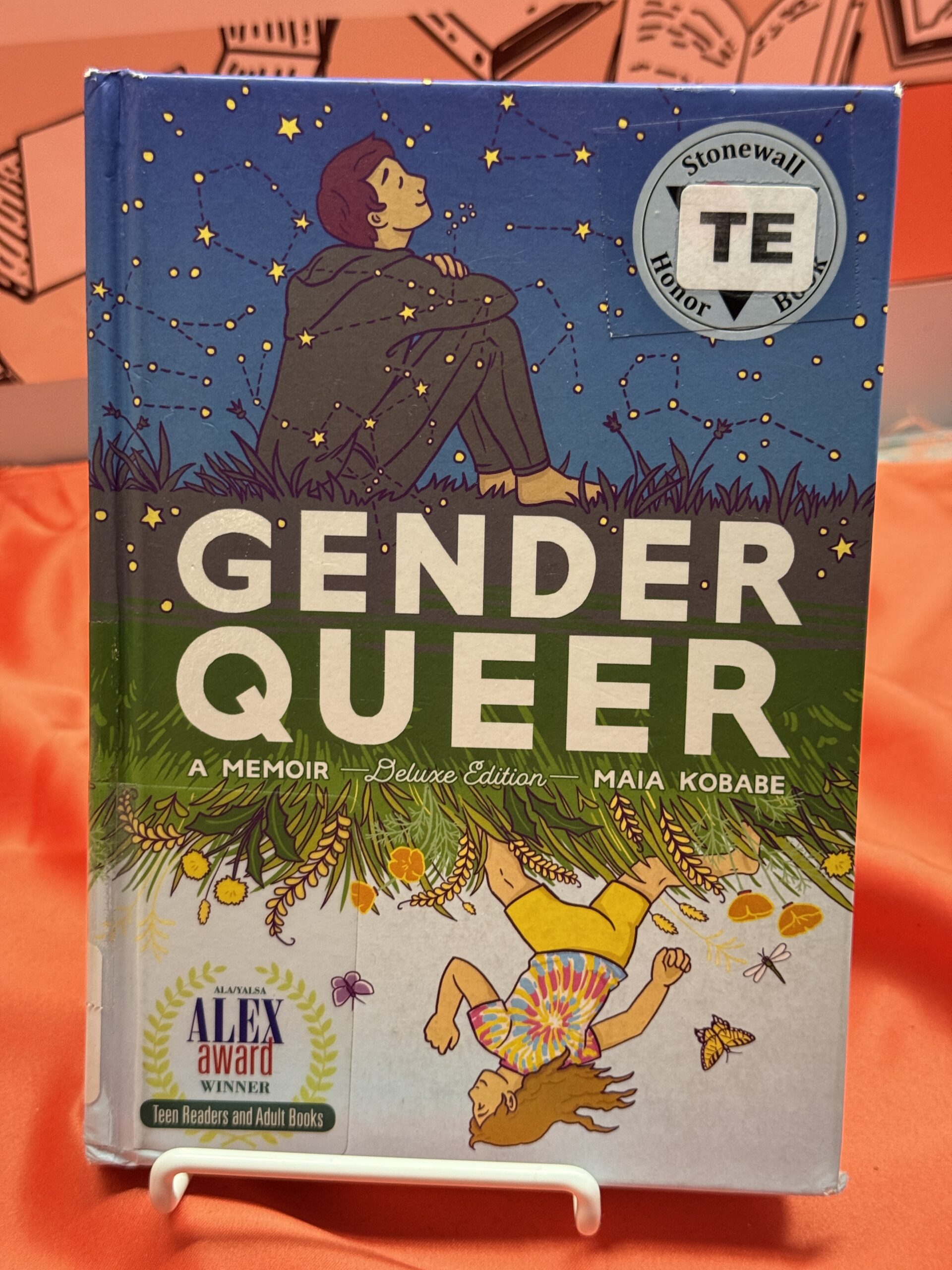

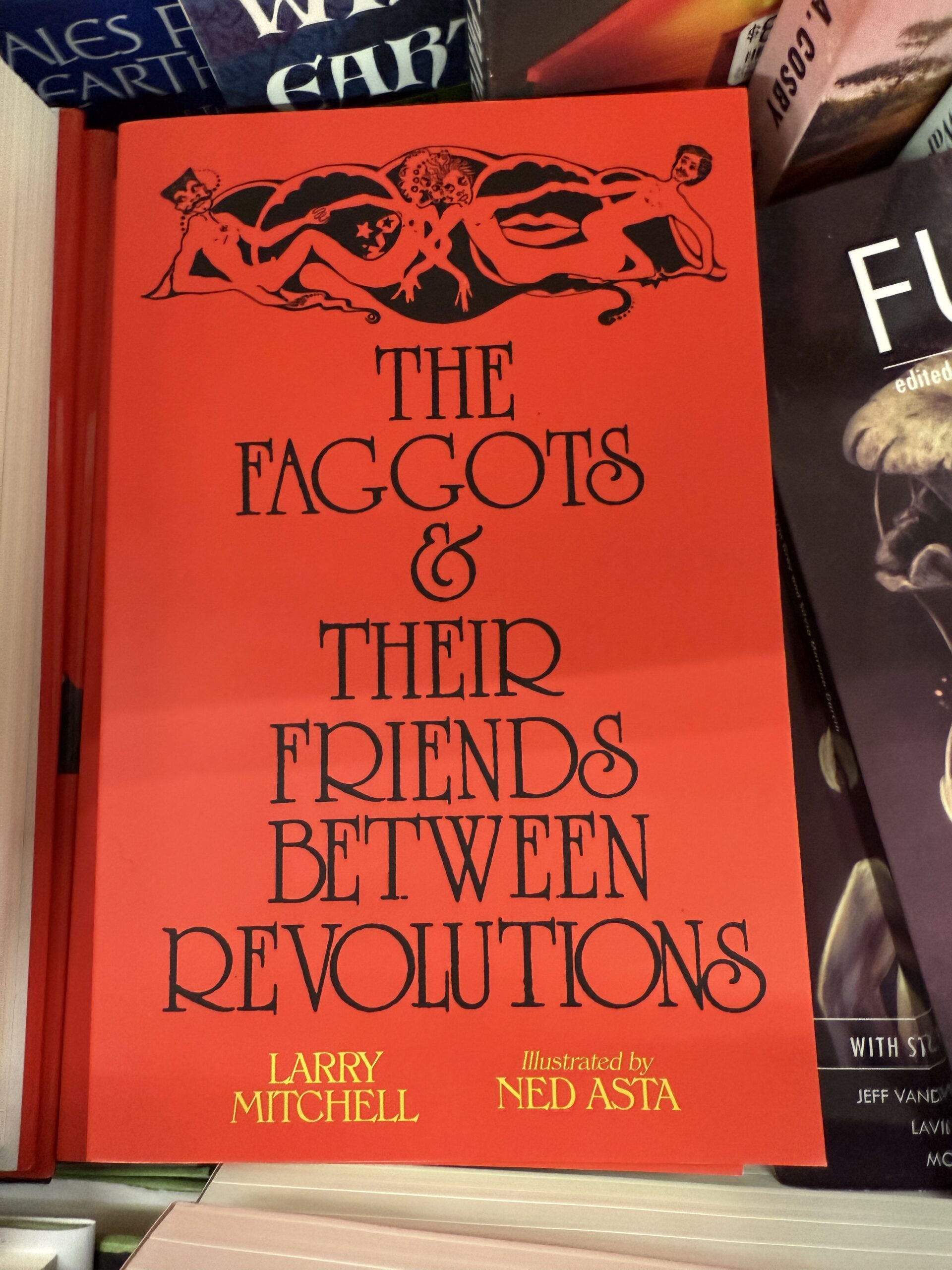

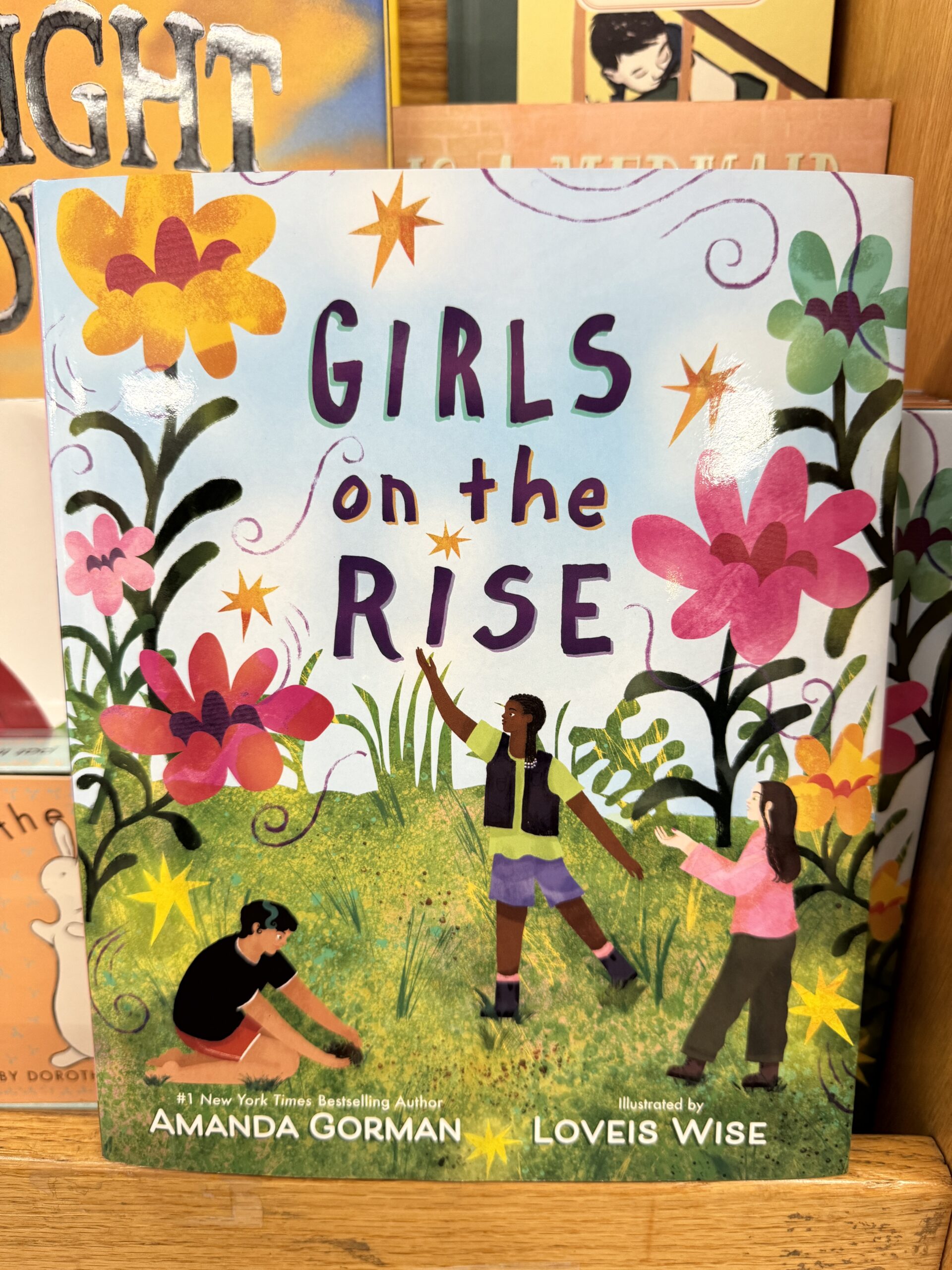

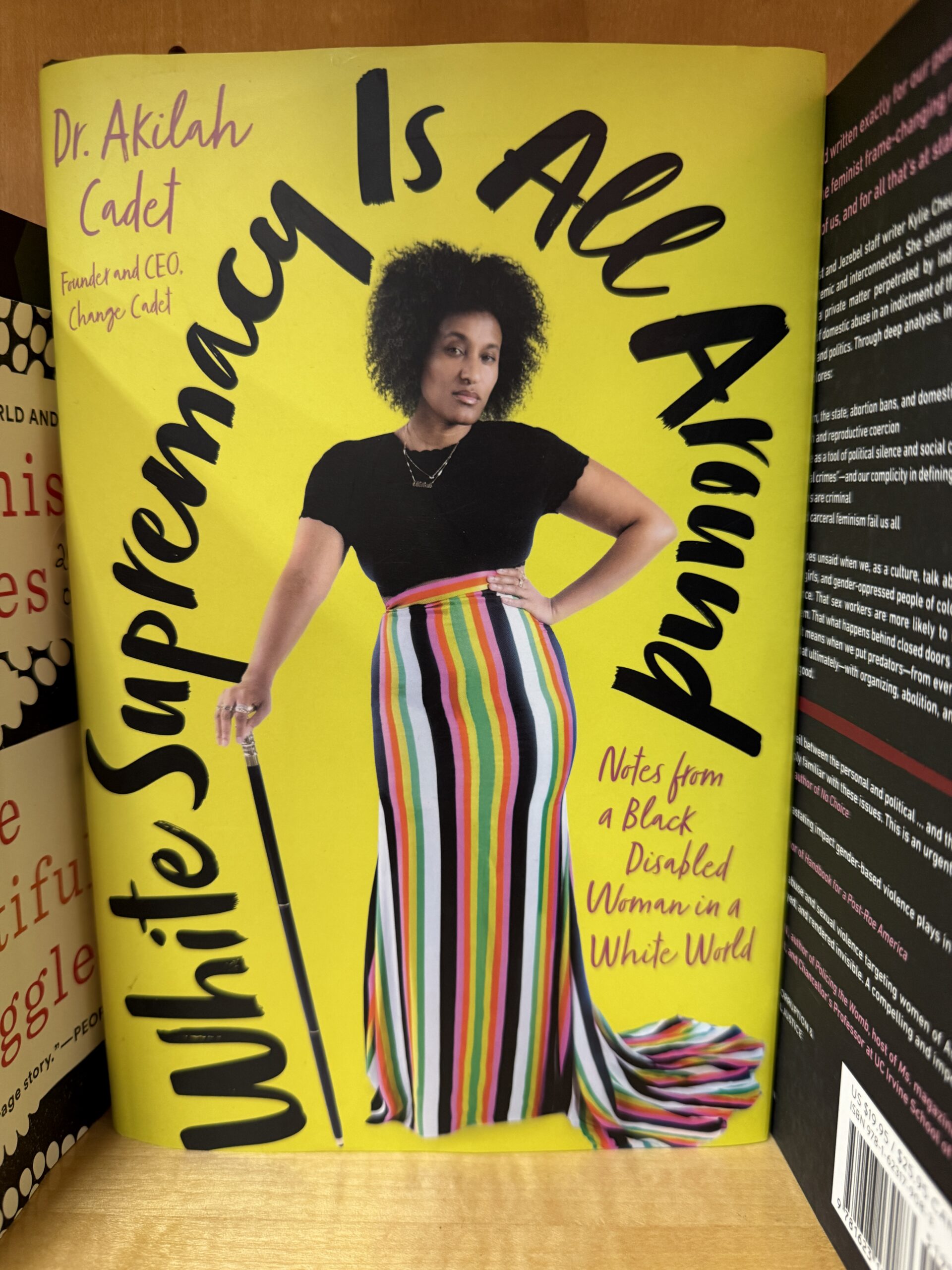

The library has an official “favorite drag queen” and he/she/ze/they recently performed for teenagers:

Any books for the teens to read after the drag show?

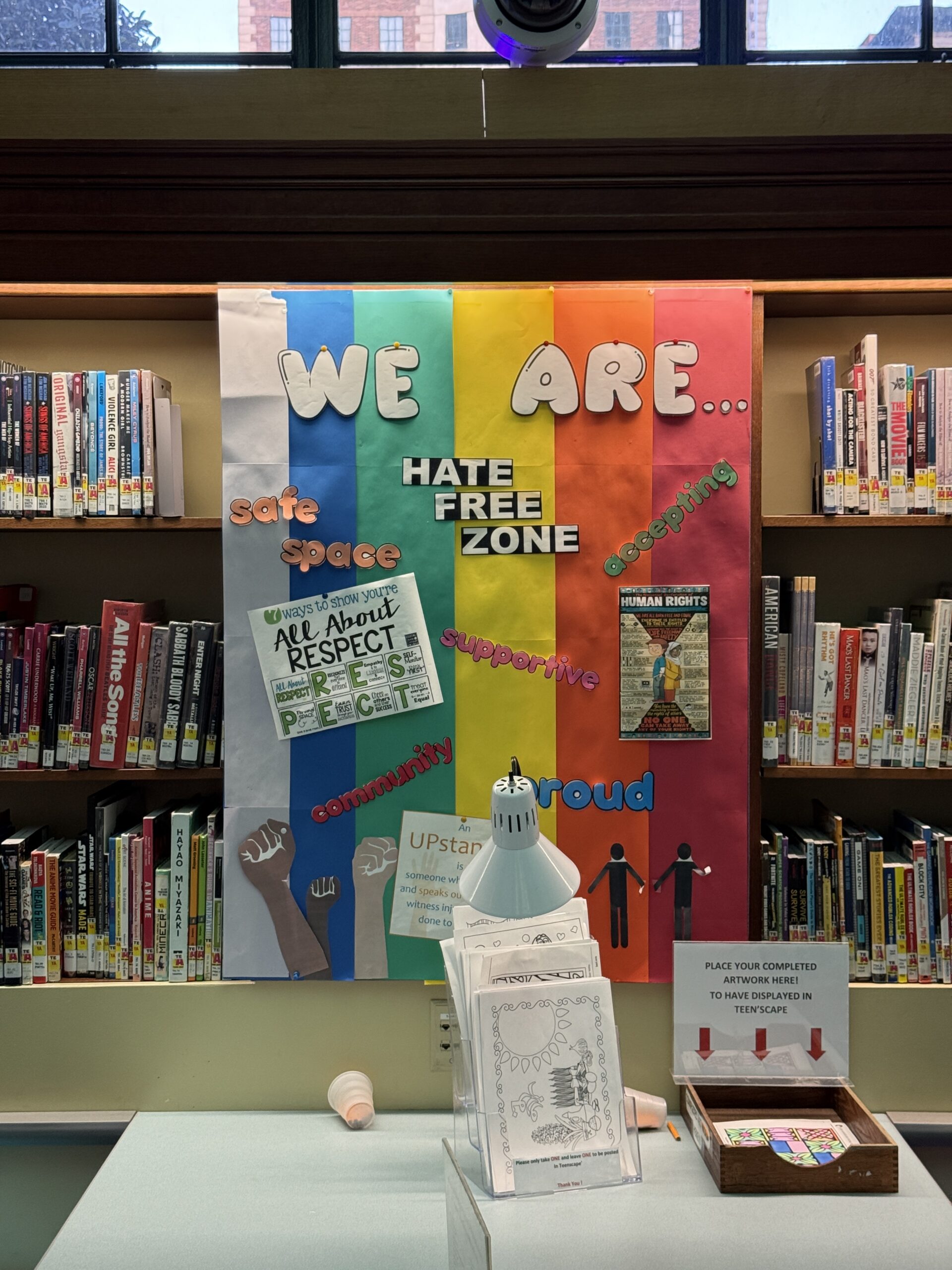

Finally, remember that Los Angeles is a hate-free zone (which is why Donald Trump and ICE are being welcomed with love?):

Readers: What should Greta T deliver to the besieged folks in Los Angeles?

We have tremendous inequality among U.S. states. Household income in California was $95,500 in 2023 dollars (Wokipedia) while Texas households enjoyed only $75,800 in income and in Mississippi the median household income was only $54,000. Who works to redress this inequality? Not the federal government, which keeps spending taxpayer money in the richest states, either directly (grants to universities, student loan subsidies, tuition subsidies) or indirectly (pharma and health care purchases).

But let’s consider Elon Musk. He has moved at least four companies from richer-than-average California to poorer-than-average Texas: Tesla, X, SpaceX, and The Boring Company. Is there anyone else alive who can be said to have done as much to reduce inequality among the states? If not, we must anoint Elon Musk as America’s Greatest Social Justice Warrior.

The company is also getting an injection of $17.3m (£13.4m) from the Texas government to develop the site, a grant that officials say is expected to create more than 400 jobs and $280m in capital investment in Bastrop.

Although I can’t blame Elon for taking the state’s money, that last bit is upsetting to me as a 14th Amendment Equal Protection purist. Why is it acceptable for a government (state, in this case) to favor one business with tax breaks while hitting smaller and less-connected businesses with the full force of taxation. I would like to see all of these state programs eliminated so that 2-person company is on a more level playing field with a 2,000-person company.

It’s the fifth anniversary of #Science in California filling skate parks with sand. The video of Venice Beach below, from ABC, is good because it also shows that the beach itself has been closed (part of the “Safer at Home” orders:

Same thing happened in San Clemented, California a few days earlier (Fox News).

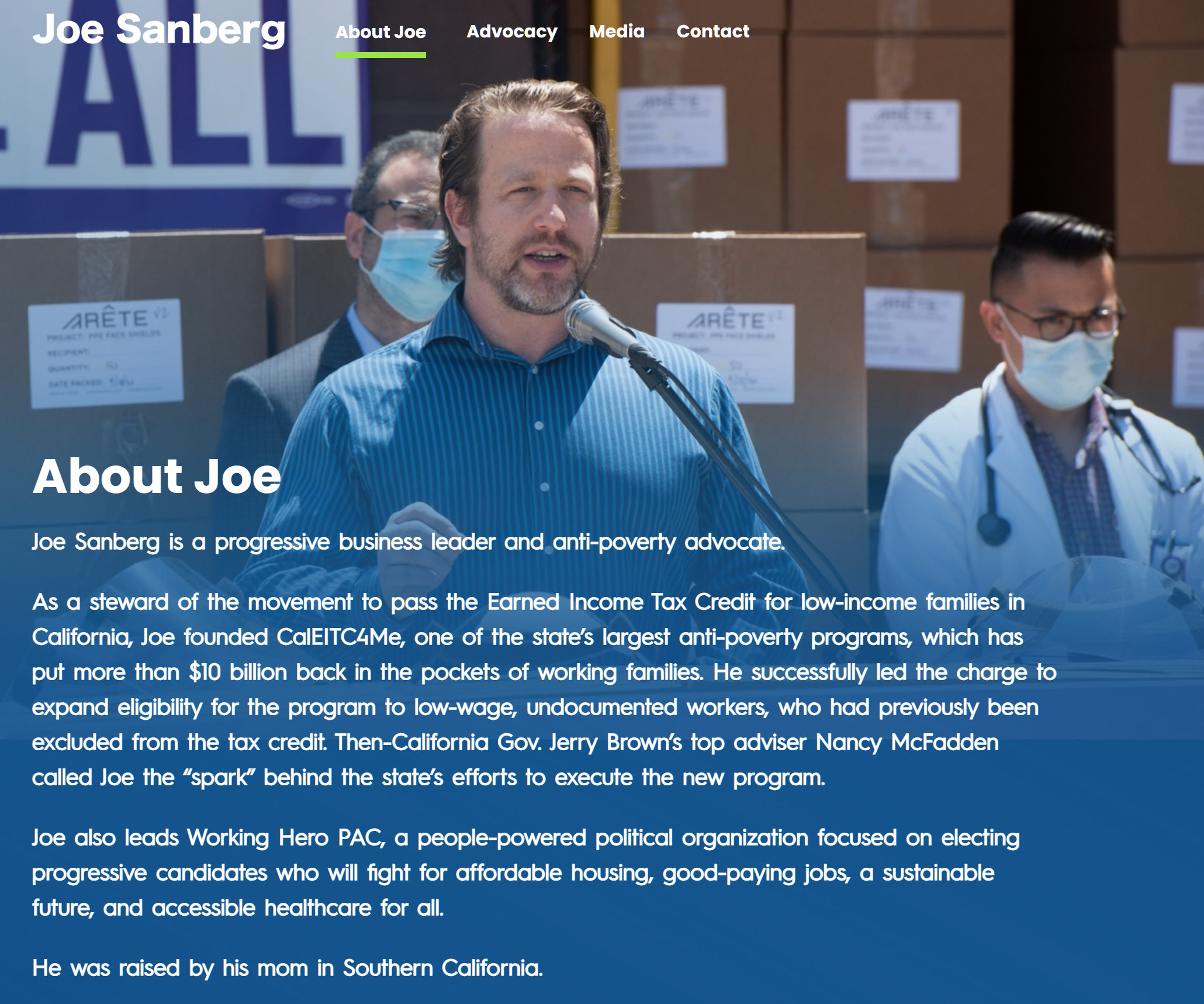

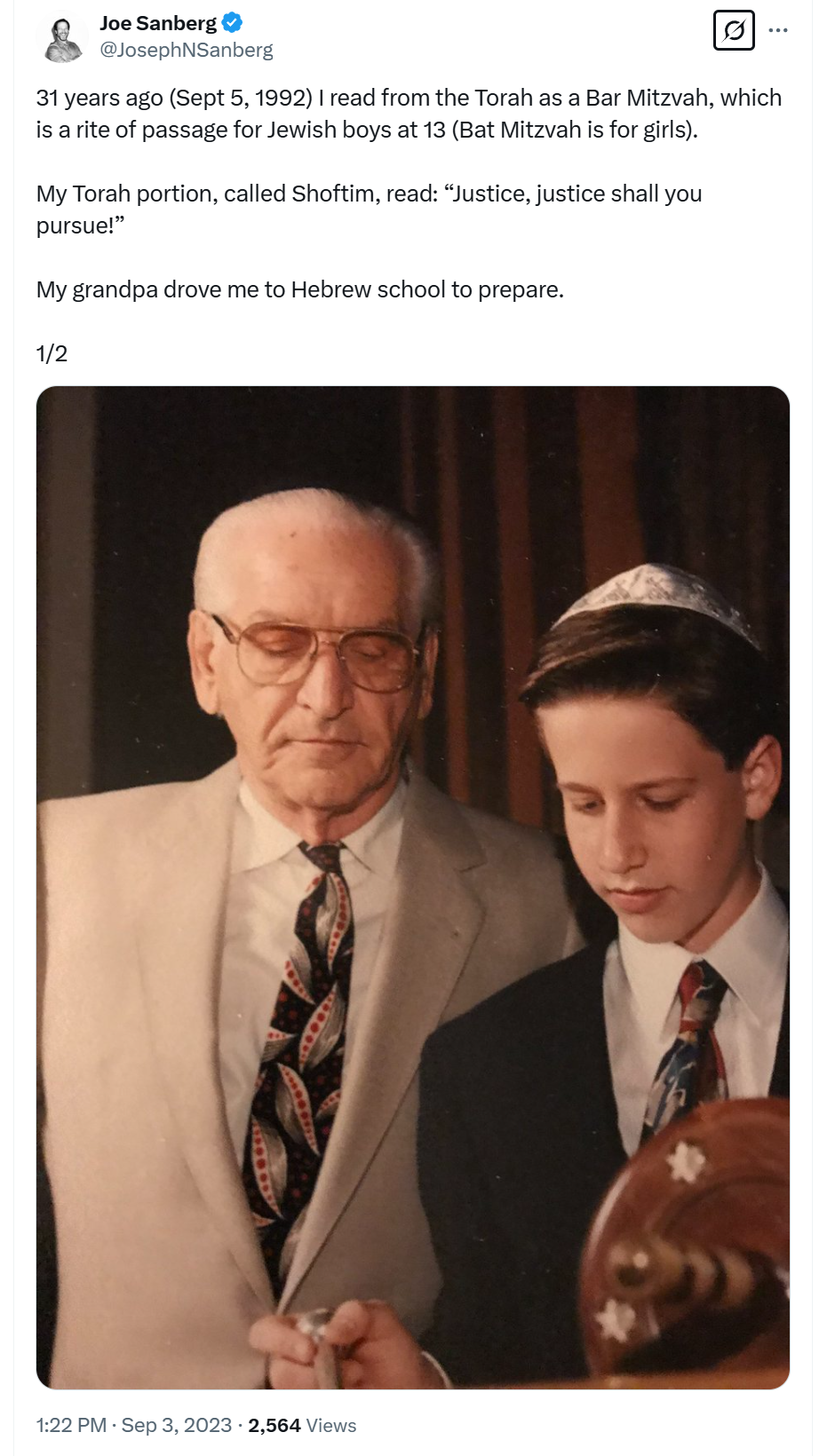

A few screen shots from joesanberg.com before it gets taken down…

His X profile consists of just a single quote from Dr. Martin Luther King, Jr. and shows no white people other than himself:

Here here says that he wants to give money extracted from native-born taxpayers to “low-wage, undocumented workers” (via a state EITC analogous to the federal cash hand-out program). He’s also proud that, if “single motherhood” occurred in the manner convention for white Jews, mom sued dad. I appreciate that every photo of Californians includes at least some Followers of Fauci:

A big donor to the Democrats, he was considering running for President in 2020 (Atlantic):

Ibrahim Ameen AlHusseini Pleads Guilty to Scheming with Sanberg

SANTA ANA, California – Joseph Neal Sanberg, 45, of Orange, the co-founder and largest shareholder of the financial and sustainability services company Aspiration Partners, Inc., was arrested today on a federal criminal complaint alleging that he conspired to defraud two investor funds of at least $145 million.

Sanberg’s coconspirator, Ibrahim Ameen AlHusseini, 51, of Venice, pleaded guilty today to an information charging him with wire fraud for falsifying documents and information to assist Sanberg. According to his plea agreement, signed on February 7, 2025, and unsealed today, AlHusseini personally received approximately $12.3 million in payments from the scheme. AlHusseini is scheduled for sentencing on September 29, 2025. … AlHusseini was arrested on a criminal complaint on October 7, 2024, and has been released on bond since November 13, 2024.

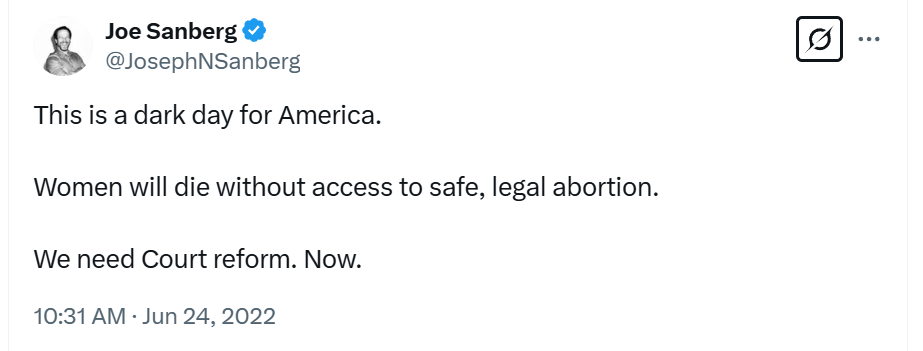

I can’t figure out what Mr. Sanberg allegedly did with the $145 million? Spent it on 8 Mar-a-Lago’s (using the New York judiciary’s estimated value of $18 million)? Used it in some business where he was the primary shareholder? I guess it is at least fair to say that Sanberg was telling the truth when he tweeted out “We need Court reform. Now.”

Flash back to 2023, when Mr. Sanberg tweeted “Justice, justice shall you pursue!”

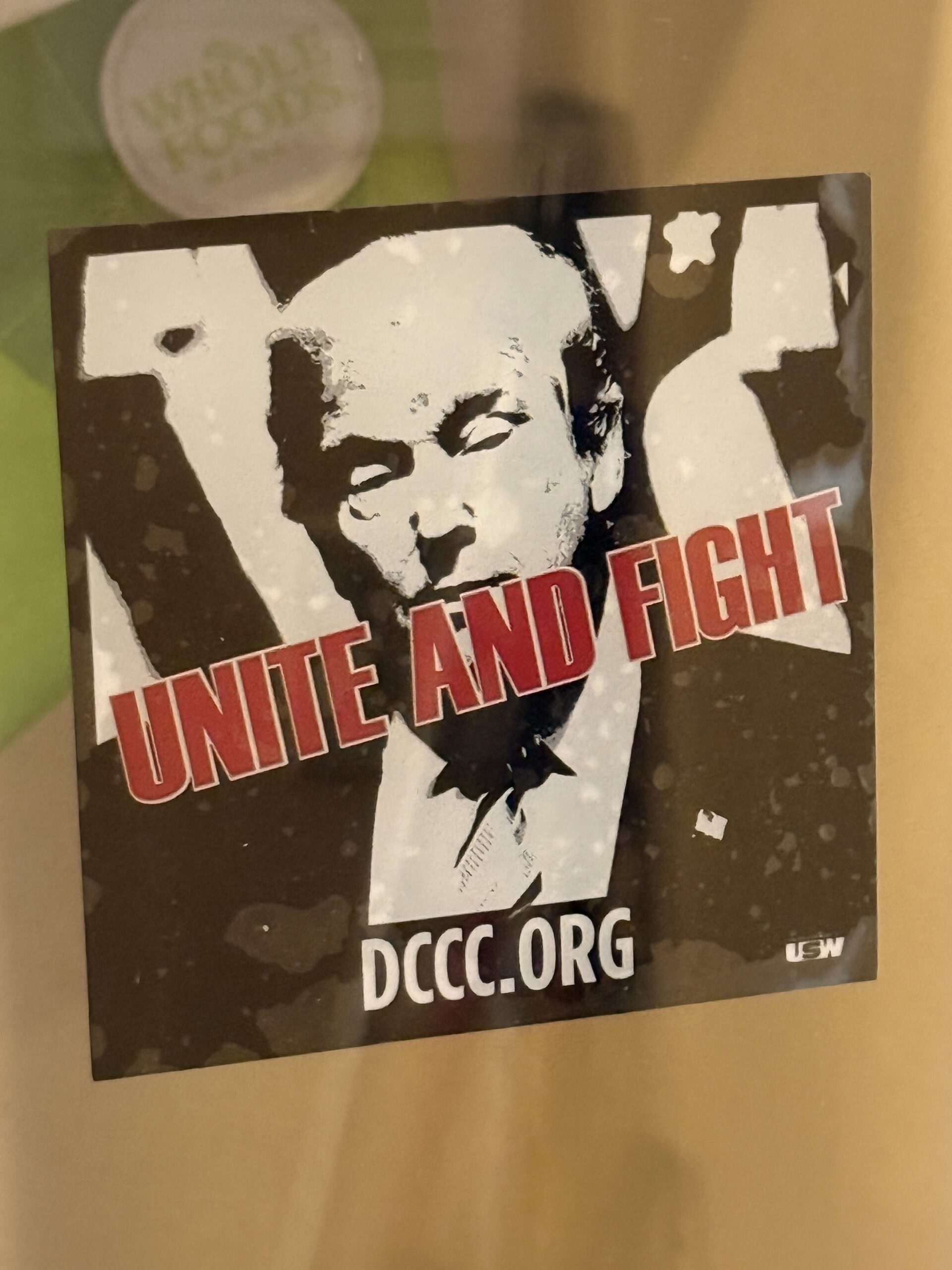

I recently visited friends who own 80 acres in Napa County, part of the San Francisco Bay Area. The wife describes herself as a “political moderate” and the husband as “apolitical”. Here’s a sticker on the front door:

Once inside, hanging on the wall:

The local gourmet establishment starts the unskilled at $23/hour:

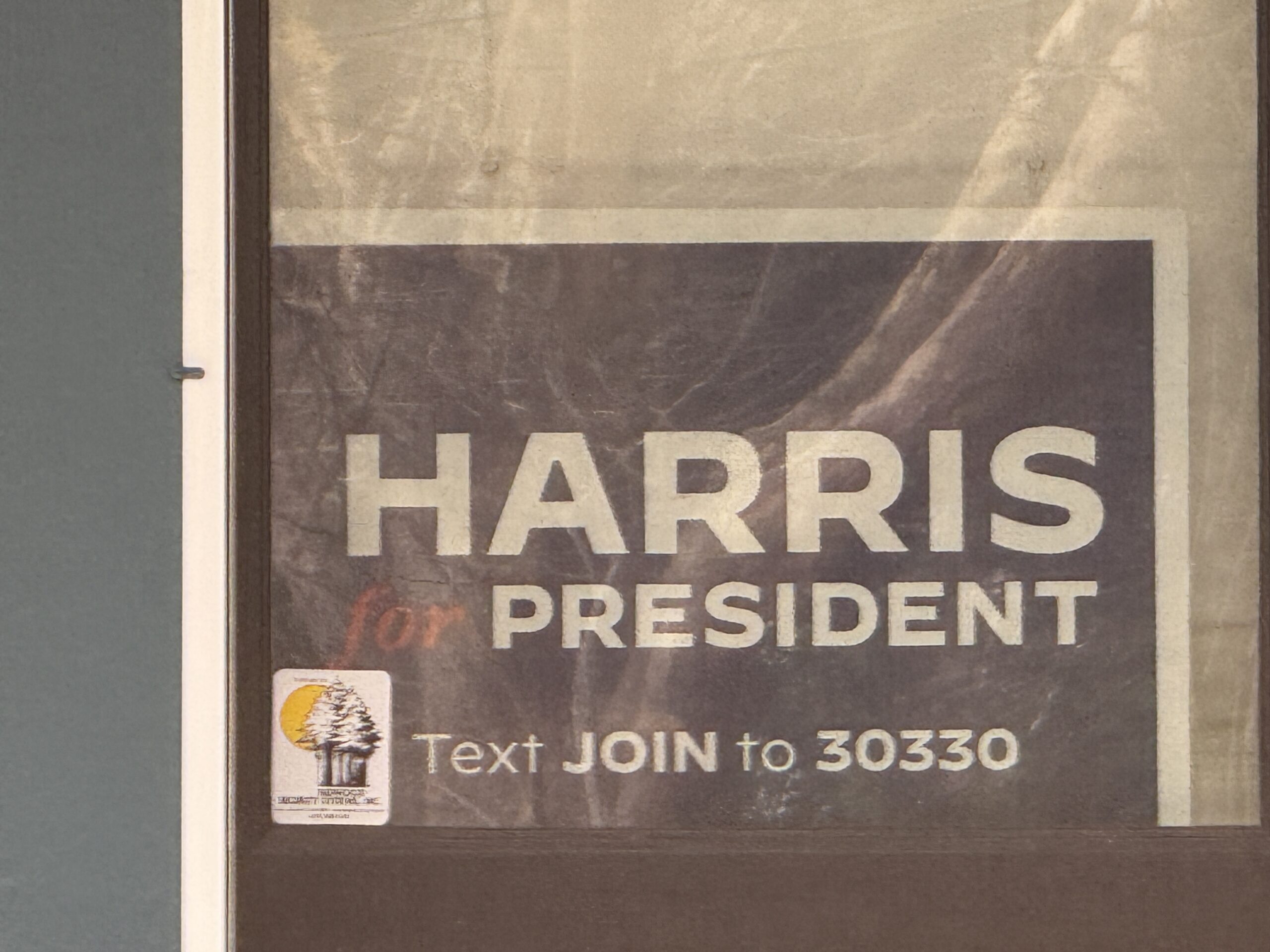

I also stopped to visit a friend in San Anselmo, part of Marin County and home to a ketamine injection clinic and a $3 million house still sporting its “Harris for President” sign:

$3 million (pre-Biden value?) P-51 Mustang and a 2700′ runway. Precision matters!

I stopped to take a quick walk around Berkeley with a friend. She assiduously locked her house and cautioned me to lock the rental car. I had observed at least one unhoused person at the entrance to her elite neighborhood. Here’s a sign at one of her neighbor’s houses:

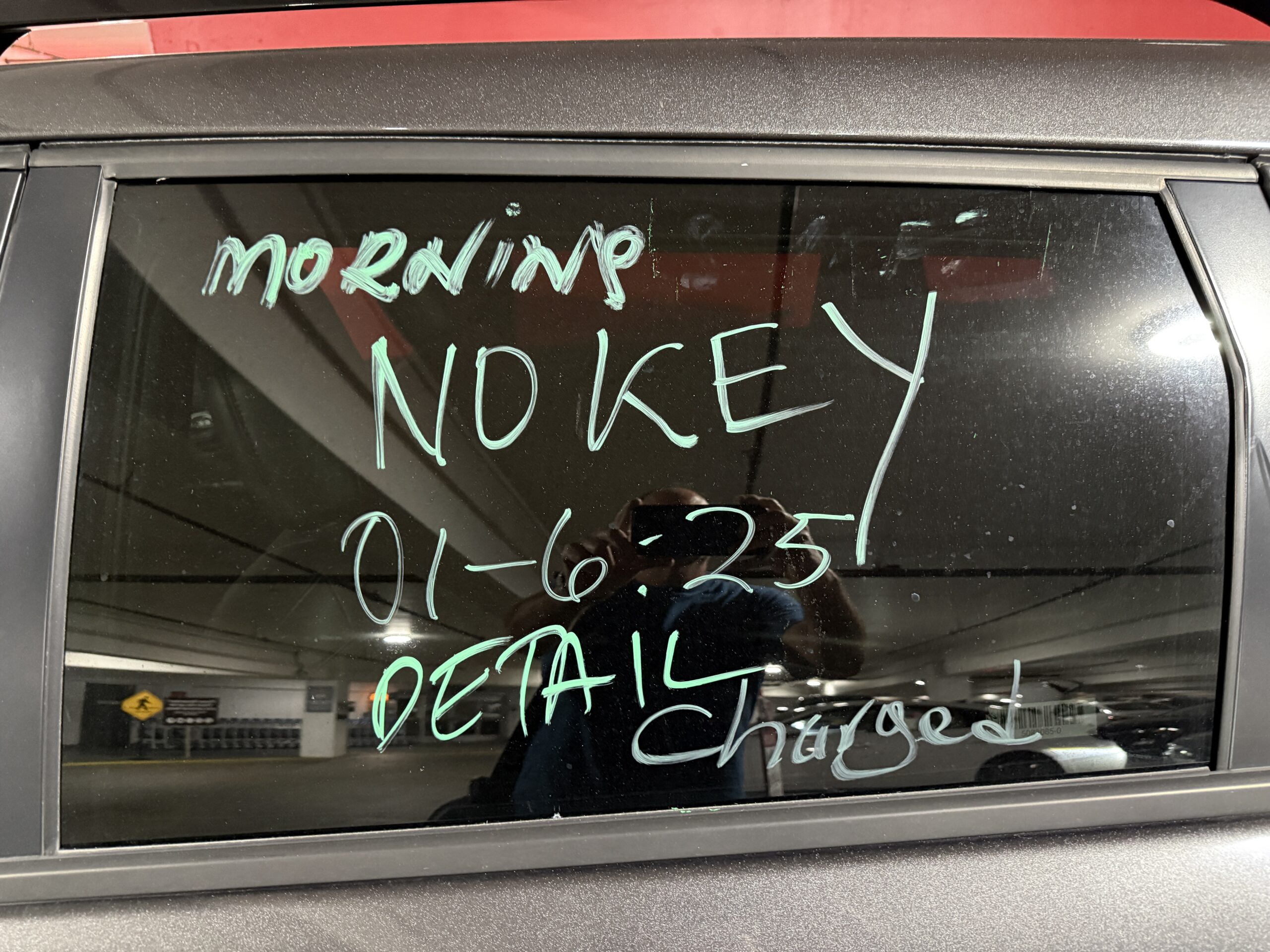

At SFO, I discovered that a #Resister had protested the J6 insurrection by returning a rental car to Avis/Budget on the 4th anniversary of this greatest event in American history, but without the key (photo from January 27):

And, of course, there were the usual outdoor bearded maskers (SARS-CoV-2 is a deadly enemy of humans, especially the young and healthy, but not so deadly that you’d want to invest 50 cents in a razor and shave your beard like it says in the 3M instructions to do; nor would you want to drive 6 hours in a COVID-free private car to Los Angeles (where they were heading)):

(Separately, I know a lot of male pilots who have discovered mountains of homosexuality within themselves and, after a period of reflection, realized that the terrain was a ridge of lesbian mountains.)

A recent trip to San Francisco’s Museum of Modern Art (SFMOMA)….

They’ve gone big into Yayoi Kusama, still productive and creative at age 95.

Both of these works are from 2023! (Perhaps she had some help with the physical construction.)

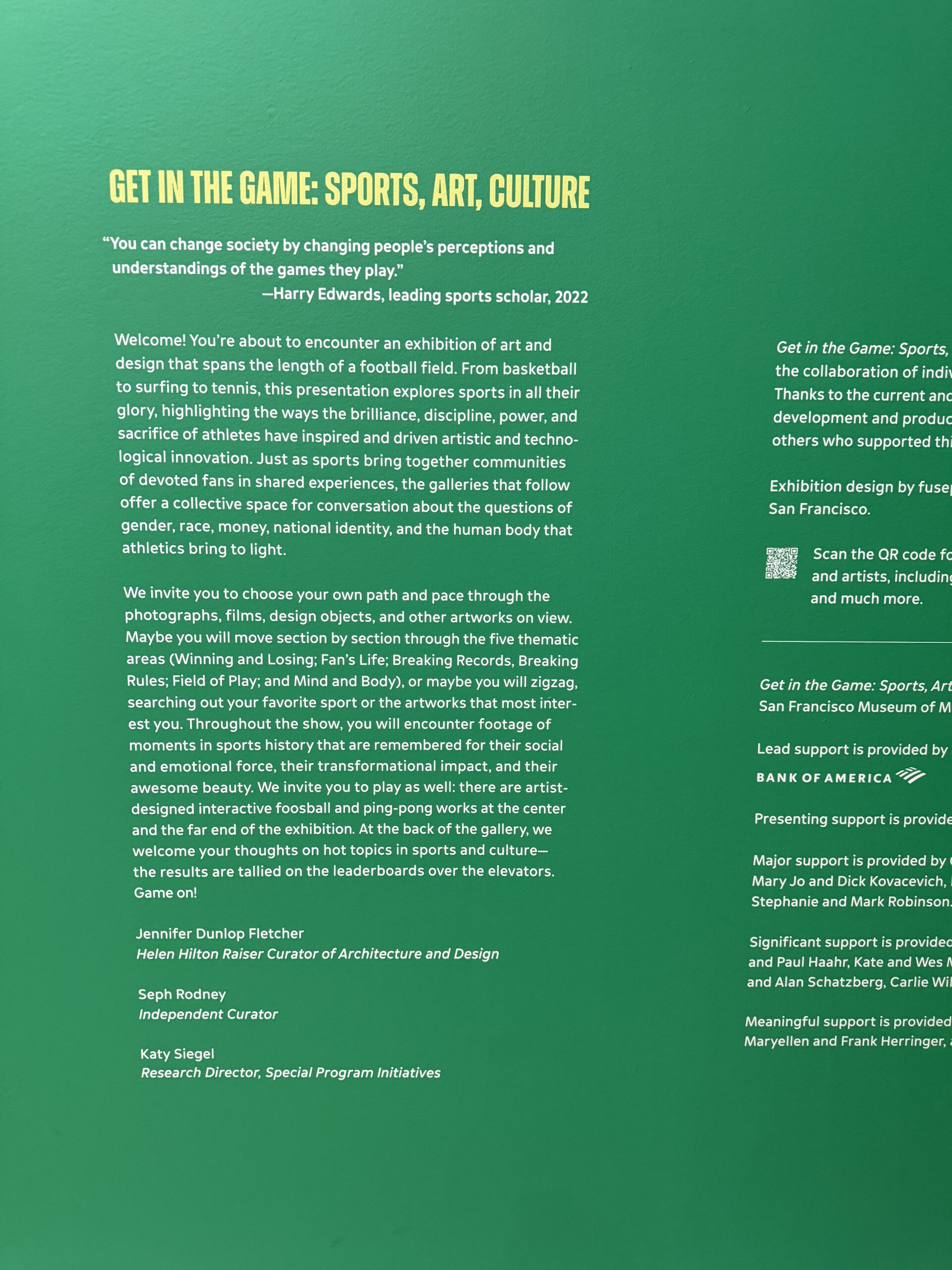

The “Get in the Game” exhibit appears to be about sports, but a sign explains that it is actually about “gender” and “race”:

Frontiers of aeronautical engineering… a lead airplane from Anselm Kiefer:

Old-school Dan Flavin, made with simple fluorescent lights of color (these could be updated, perhaps, with LED bulbs so that different color patterns can be offered at different times of day):

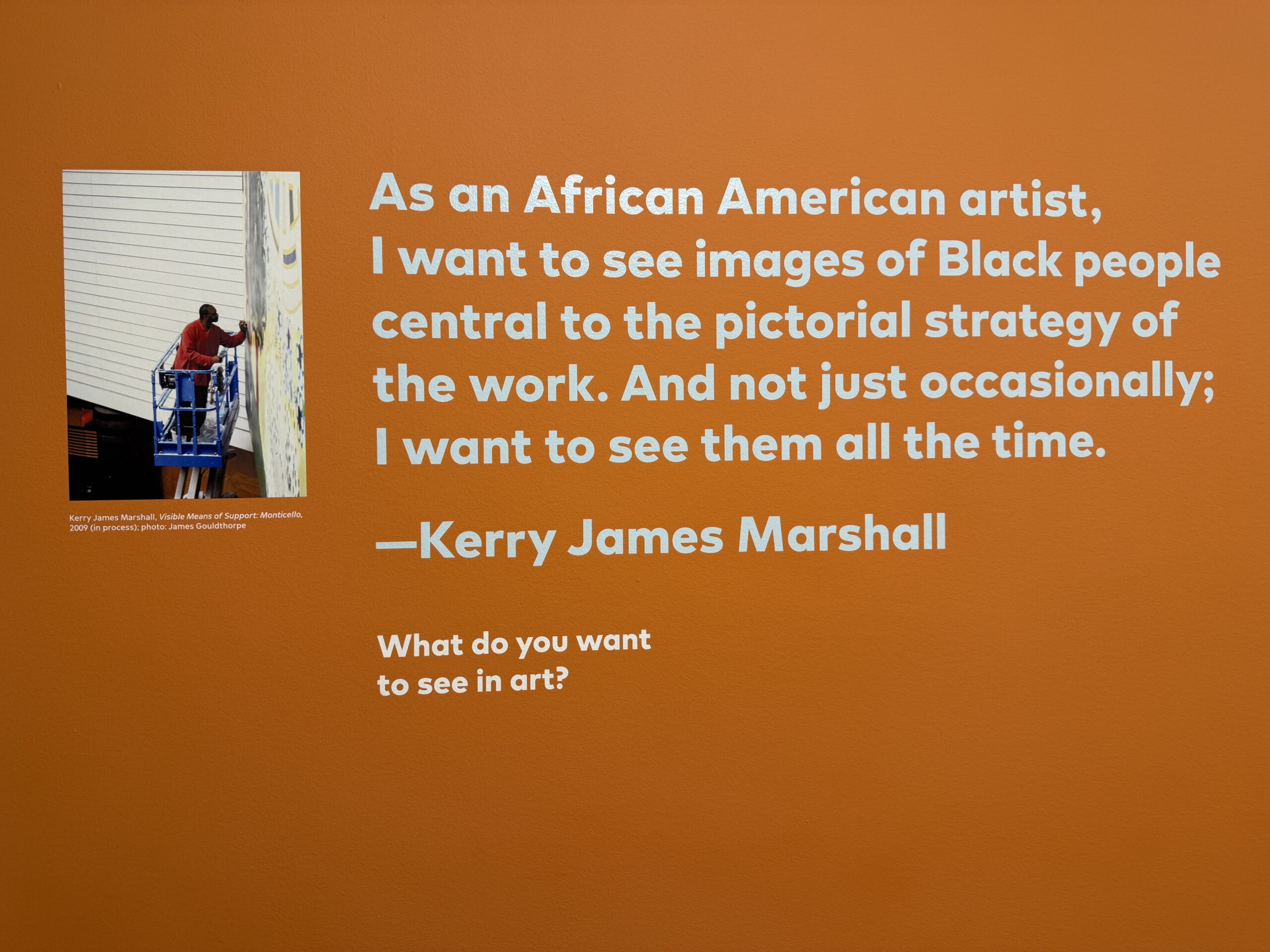

The museum quotes Kerry James Marshall as wanting to see only pictures of Black people and then obliges with a show of Amy Sherald’s work, in which only Black people are depicted (even in San Francisco, nobody wants to see paintings of Taiwanese people fabbing the chips that hold up the SF AI economy? A Black person standing around is more valuable to Humanity than a TSMC employee making an Nvidia H100?).

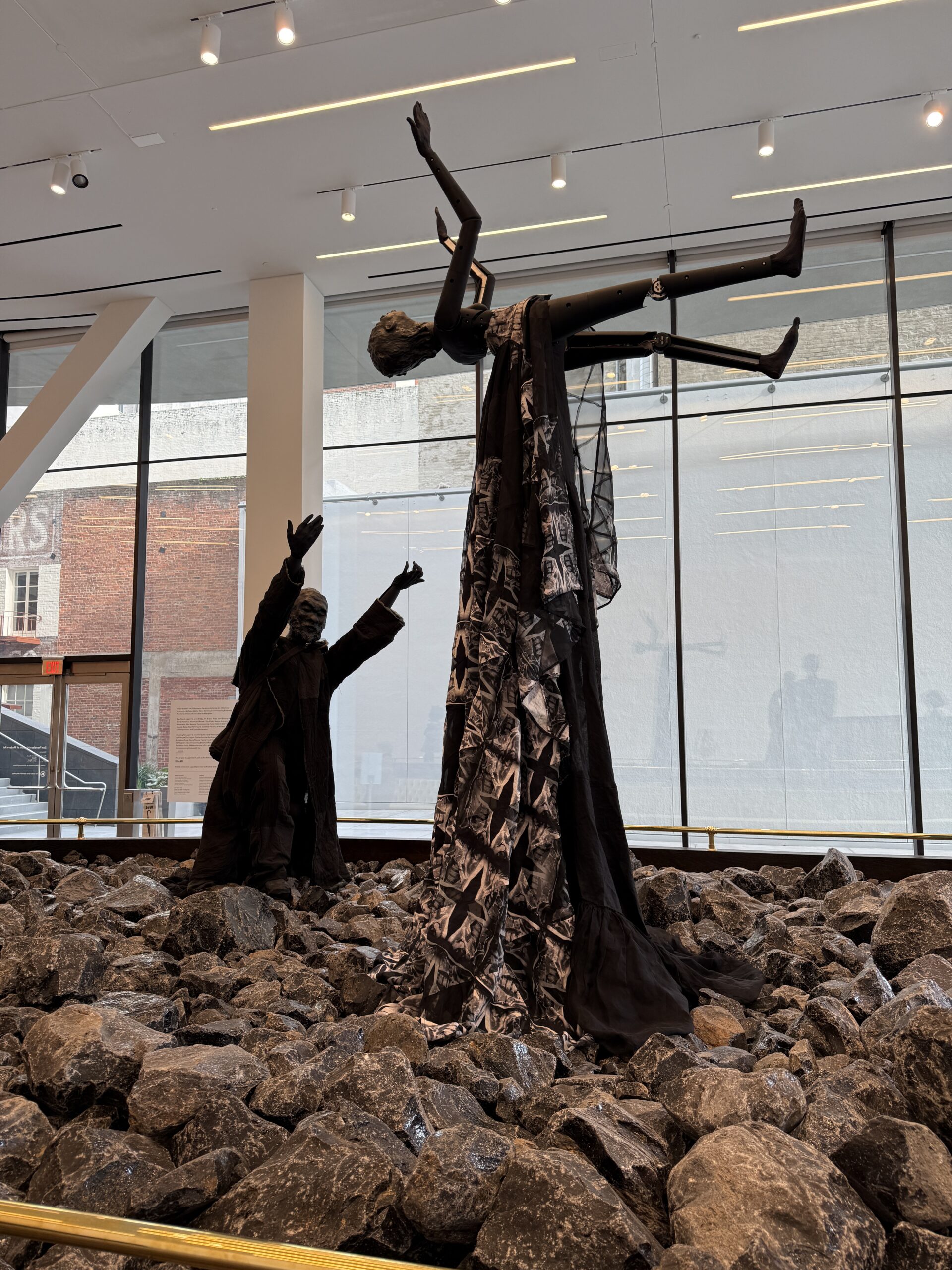

Speaking of Black people who aren’t fabbing H100s… there is a huge lobby area devoted to Kara Walker’s work:

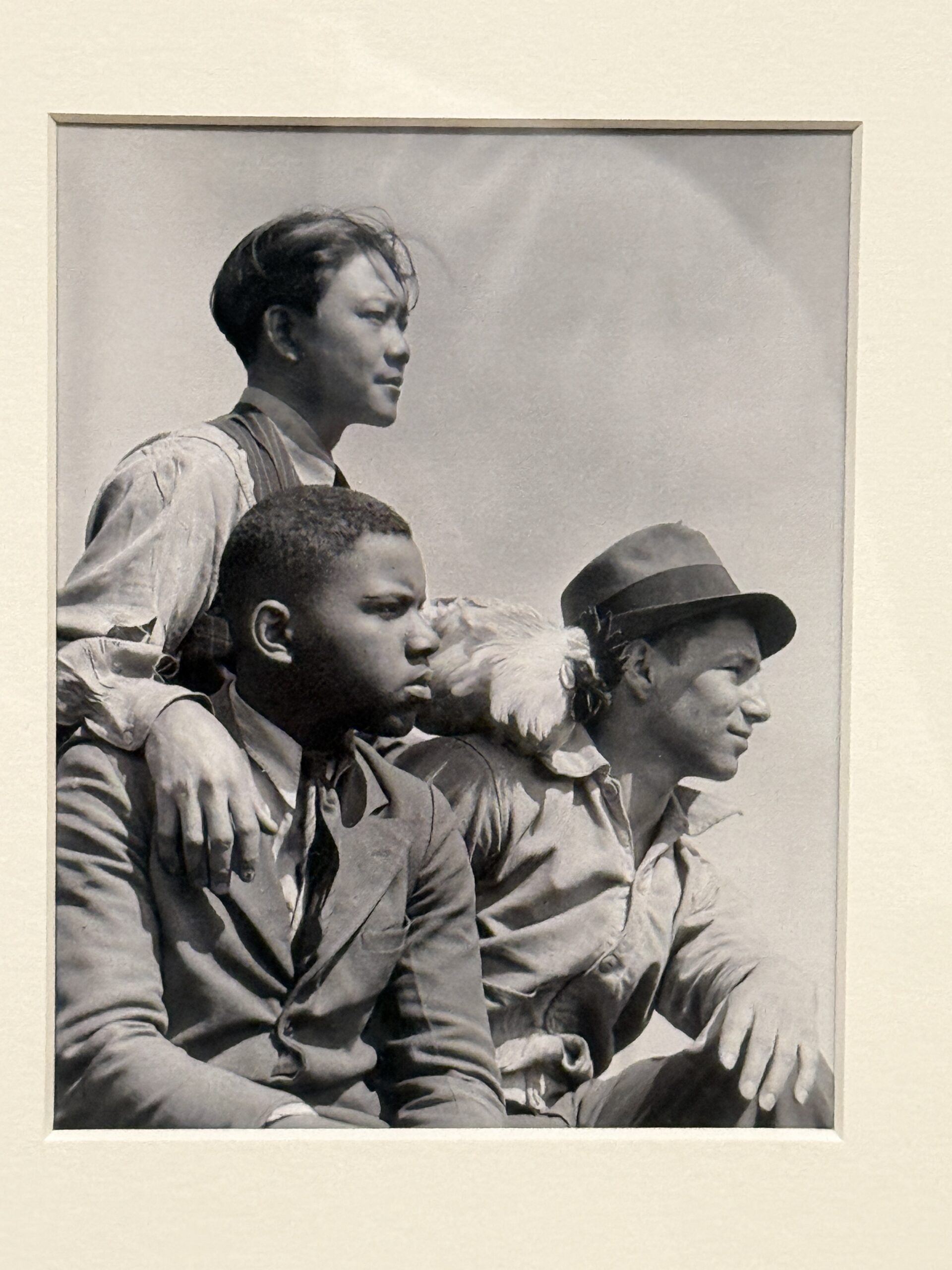

The major photograph show is devoted to pictures of Black people… by a white woman:

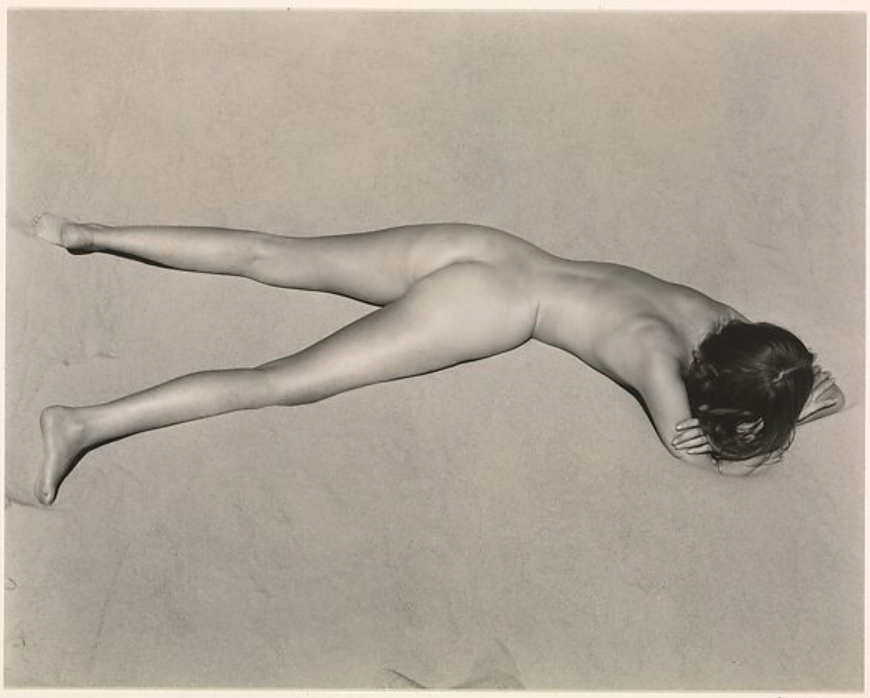

There’s a smaller show by a “woman of color” (from Peru) who “rewrites male-dominated history” by recreating Edward Weston’s photos using herself as a model:

Here is a Weston for comparison (Americans had better-defined waists back in 1936, apparently):

Exit through the gift shop, at which a complete home library may be purchased (or replace your worn copy of The Story of Art Without Men):

What do the streets outside look like after this $42 per person experience for Californians who say that they will pay any price and bear any burden to end homelessness?

More than 36 square miles of Pacific Palisades were burned, which is a tragedy, of course, but also an opportunity for California’s central planners. We are informed that California is suffering from a housing crisis, an affordable housing crisis, a crisis of unhoused people, and a crisis of housing for noble undocumented migrants. Also that housing is a human right. Californians, if they were sincere in their principles and commitment to solving these crises, could use eminent domain to buy the burned square miles (at whatever the raw land value was prior to the fire) and develop it as a cluster of fireproof (and earthquake-proof) concrete-and-steel high-rises. Built to the same density as Manhattan of 73,000 people per square mile, this would become home to 2.6 million people. If we assume 3 people per unit, the county and state would be building approximately 870,000 units. “Housing Underproduction in California: 2023” says “California must build 3.5 million housing units by 2025 to end the state’s housing shortage”. In other words, a project of this nature would solve about 1/4 of California’s housing problems.

Could Californians afford it? In City rebuilding costs from the Halifax explosion we learned that it cost roughly $555,000 per unit at pre-Biden prices to build in Boston (assuming free land). Adjusted for Bidenflation, California’s higher costs, and the need to pay for the land let’s assume $1.5 million per unit. The total cost would then be $1.3 trillion, but let’s assume that not all of the units are given away free to noble no-income and low-income residents. Perhaps half the cost is eventually recovered via rent or sales. Thus, the total cost is $650 billion. Divided by California’s 39 million people, this works out to less than $17,000 per Californian, which seems like a small price to pay to take a big chunk out of the housing shortage/crisis and also reduce fire risk going forward (concrete and steel won’t burn and homeless encampments have been a source of recent fires (NBC)).

For parents and students in the East Bay (of San Francisco, California), a reminder from a school bureaucrat, who has stayed entirely “neutral”, to “to follow the example set by Presidents Biden and Obama” (for better readability, not in quote style):

DUSD Community,

In the United States, we have always had a peaceful transition of power between presidents, except for January 6, 2021. President Biden and his administration have demonstrated a high level of professionalism during this transition, just as former President Obama did for President-Elect Donald Trump and each president prior.

The 2024 Presidential election was, for the second time, an extremely divisive election for our country. This election has itself become a point of protest for women, Muslim and Jewish communities, immigrants, and people who care about education, Social Security, Medicare, and a whole list of other issues. There has been a great deal of media coverage regarding the Presidential Inauguration that will take place Monday, January 20, in Washington, D.C.

As educators, we have the incredible opportunity to use the presidential election and the second Trump Inauguration as learning opportunities to help promote social justice [Ed: with taxpayer funds] in a way that actively engages our students. The activities, discussions, and student production that we choose to plan around the inauguration are opportunities to further develop the skills and competencies that we are developing in our Graduate Profile. We need to provide a safe environment for our students during the Presidential Inauguration. I encourage students and staff to reach out to each other and work together on shared, peaceful activities at our school sites. Listening to the Inauguration is an appropriate activity, along with providing the space for students to process Trump’s presidential address. Providing these types of activities is a critical responsibility and opportunity for our educational institutions.

Regardless of the activity, we will stay neutral, share the facts, allow for both sides of an issue to be shared, and create a safe place in our classrooms and at our school sites for discussion to take place. We need to follow the example set by Presidents Biden and Obama and engage in activities that support the peaceful transition of power between Presidents.

In addition, I want to reinforce the importance of maintaining the privacy rights of our students. Under FERPA laws and laws that govern the State of California, our schools will not provide any private student information to ICE (Immigrants and Customs Enforcement) without a formal arrest warrant. Our schools must remain safe and secure for all who attend and work in DUSD.

I thank you in advance for staying in school, remaining respectful, and engaging in meaningful dialogue around the upcoming Presidential Inauguration on Monday, January 20, 2025.

Sincerely,

Chris D. Funk Superintendent Dublin Unified School District

In other news, I was just in Berkeley, California, a simple 1.5-hour BART ride from Dublin! The laundry detergent is locked up at Target (along with almost everything you’d find at CVS):

Let’s stroll out of Target, past a few outdoor maskers, and into Pegasus Books, which features a permanent panhandler by the front door. Inside we find empty CD cases for fear that someone without a streaming account will steal the precious CDs themselves:

The Followers of Science (TM) are heavy readers of books about witchcraft:

What if a passion for Hamas rule and Socialism could be combined into a single book?

The news out of Los Angeles isn’t great lately. Here’s a photo of Pacific Palisades:

It looks as though some concrete structures are still standing.

My engineering/planning question for today: Why aren’t all houses in fire-prone parts of California made from concrete? In Florida, after wooden houses didn’t come through hurricanes in good shape people decided to pay an extra 10 percent during construction and build from concrete.

Maybe my assumption that a concrete house is mostly invulnerable to fire is wrong? It’s tough for me to imagine, though, a fire so intense that it would melt concrete and take out a roof supported by concrete or steel beams, especially if the houses themselves weren’t combustible what would be feeding a fire in a neighborhood like the one shown above?

Wooden houses are obviously easier to engineer to withstand earthquakes, but concrete structures can be made just as earthquake-proof, I thought.

As it happens, I’m in Berkeley, California right now. Here’s how the smartest Californians protect themselves against a risk even bigger than fire (University of California, Berkeley Faculty Club):