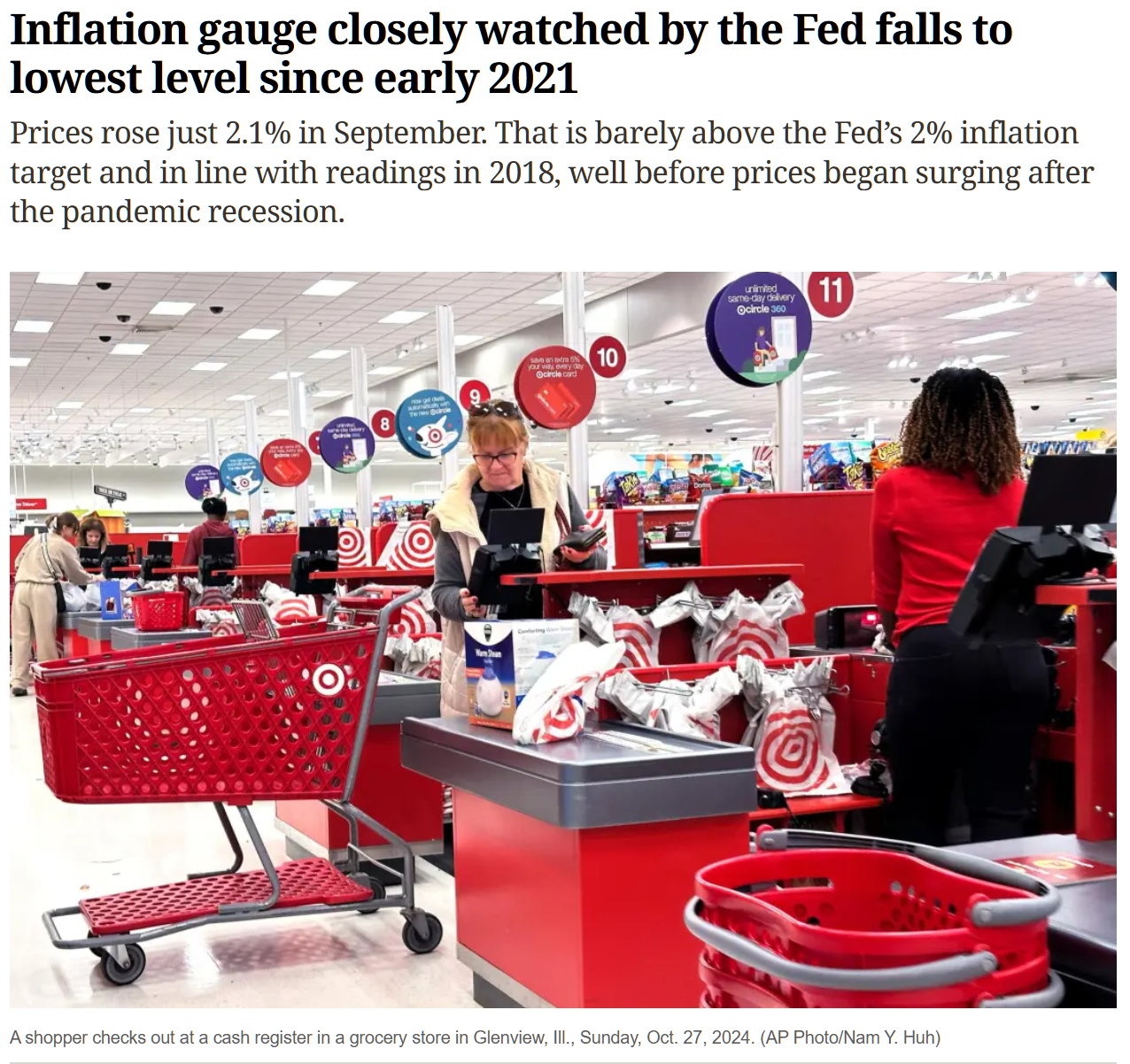

Consumer prices rose 3%, as fight against inflation continues to face headwinds

So prices are going up 0.247 percent per month, the rate that compounds to 3 percent after 12 cycles?

Consumer prices rose briskly in January, extending a recent pattern of price increases at the start of the year that likely derails the prospect for Federal Reserve rate cuts anytime soon.

The Labor Department said Wednesday that prices rose last month 0.5% from December on a seasonally adjusted basis.

0.5 percent per month works out to 6.17 percent annually.

So… the current inflation rate is 6 percent and we are told that it is 3 percent.

If you’re looking for a Valentine’s Day present that won’t break the bank, a piston-powered Cirrus SR22 for $1.2 million:

(Don’t forget state income tax on top of this unless you live in one of the states that sensibly doesn’t tax aircraft purchases (Maskachusetts being a surprising example!).)

If we specified pre-Biden delivery terms of 4 months, the price would be higher. Cirrus currently has 1.5-2-year waiting list.

As part of my mother’s moving from independent living to assisted living (February 2024) and then onward from assisted living into the next realm (January 2025) we have needed some assistance from a local moving company.

The February 2024 quote: “Charge is 2men $150 per hour 3h minimum, 1h travel time, $50 fuel plus materials (if we use any), $500 minimum.”

The January 2025 quote: “Hourly rate $185 2men 3h minimum 1h travel plus materials and fuel – starting $655 minimum.”

That’s a real-world annual inflation rate of 23 percent ($185/$150).

The latest official government inflation number from the Bureau of Labor Statistics was supposed to come out today. How does the BLS fantasy compare to our lived experience?

Inflation is whipped, except that the most significant cost for a typical person remains unaffordable (the “housing affordability crisis”), with government intervention required. The latest affordability crisis (i.e., Americans not being rich enough to afford what used to be considered American life) is for cars (San Jose Mercury News):

The good news is that expert assistance has arrived:

Bay Area residents wanting — or needing — to buy a car are steering this winter into what experts call an affordability crisis.

“The price of new cars, in general, has become alarming for a lot of people,” said Brian Moody, executive editor of Autotrader.com.

Nationwide, the average monthly payment for a new vehicle in November was $753, up more than 30% from just five years ago, said Jessica Caldwell, a head analyst at Edmunds, which tracks the auto industry.

Adding to buyers’ woes is the high price of most everything else. A recent Edmunds study found 54% of people surveyed who were planning to buy a new or used car in the next year said they would have to work extra hours or take a side job to afford it. “This wasn’t an issue 10 years ago,” Caldwell said.

Prior to the November 5, 2024 election, the same newspaper said that inflation was finished. October 31, 2024:

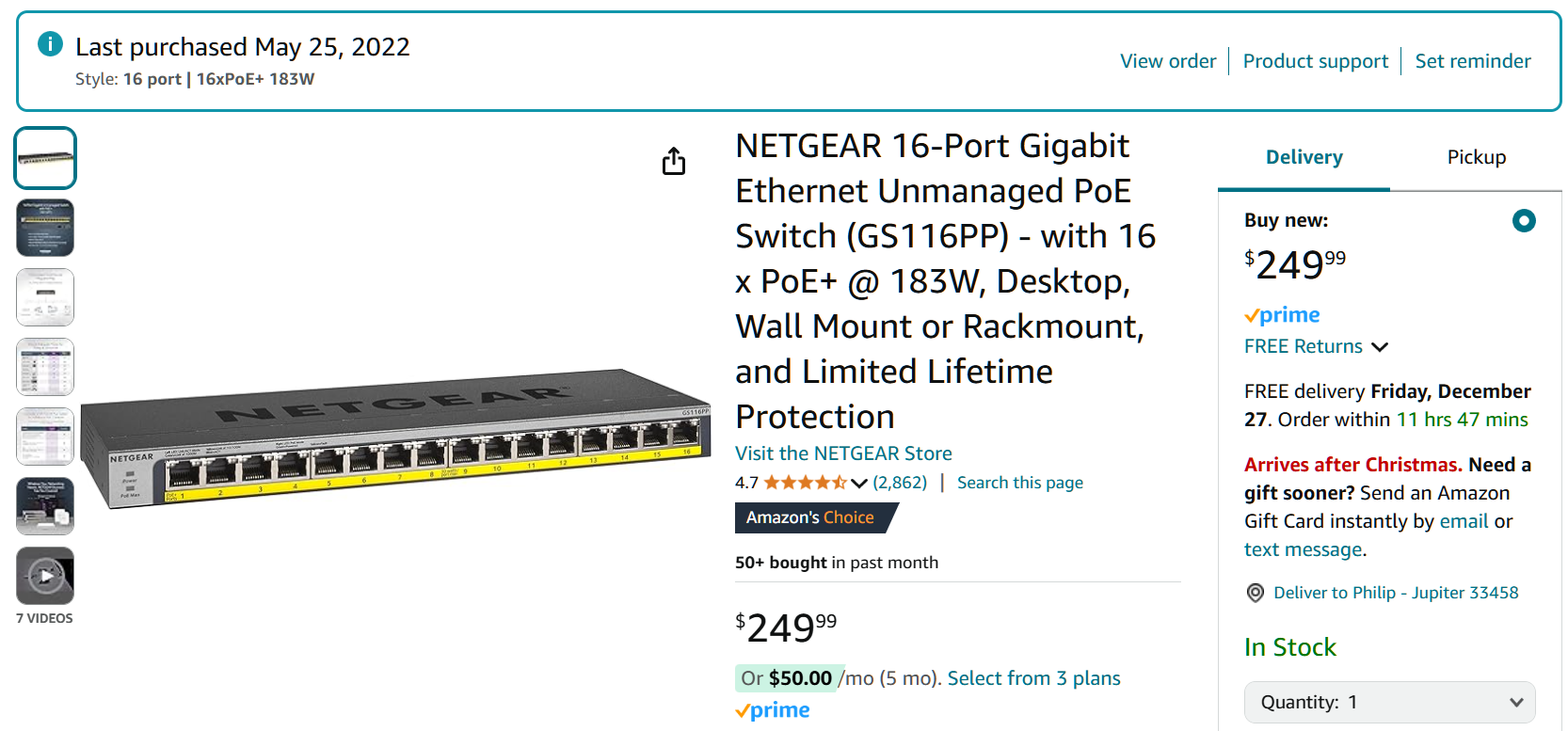

I was in a conversation with some friends, one of whom is a UniFi zealot, and wanted to check the power output compared to a feeble UniFi switch. I learned that the exact same Netgear switch was still available from the same retailer in December 2024… for $250:

That’s 39 percent inflation over 2.5 years in our otherwise inflation-free economy.

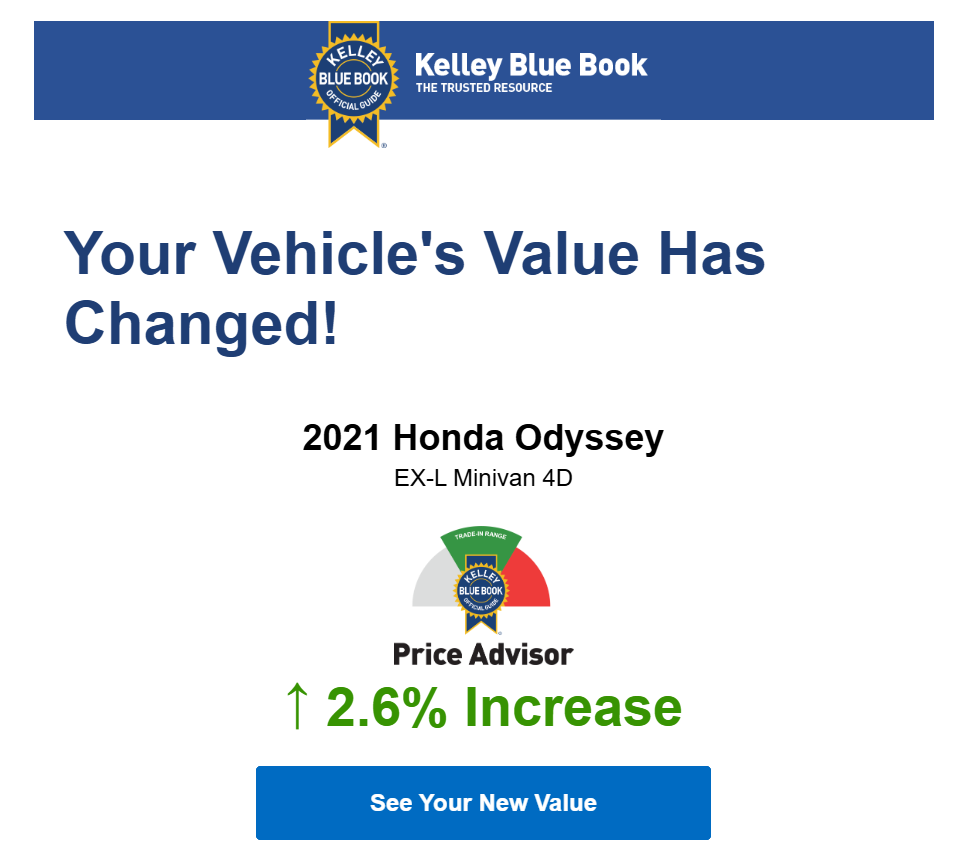

How’s our four-year-old minivan doing as a collector’s item? KBB emailed a week ago to say that it was still going up in value.

Happy New Year again! Let’s look at the new prices for the new year in our inflation-free economy or, at worst, our 2 percent inflation economy.

We have a United Healthcare policy for our family (two adults, two kids). The deductible/out-of-pocket limit for the family is $6,500/year, which means it would have been a skimpy policy back in the 1980s but now qualifies as luxurious. The premium is $48,312 per year, up 10 percent compared to 2024. Unlike Luigi Mangione, who wasn’t a customer of United Healthcare, we are grateful to have this small business policy because it is impossible to get Obamacare insurance that includes visits to the better providers here in Florida (e.g., Mayo, Cleveland Clinic, Tampa General, UHealth Miami). Every bill and “explanation of benefits” makes us yet more grateful for the United Healthcare policy because the document always starts with the provider trying to cheat us by charging 10-20X the fair price for a service (where “fair” = what United Healthcare has purportedly “negotiated” and what we often end up paying out of pocket because the $6,500/year limit (see above) hasn’t been hit).

Home health care aides in our corner of Palm Beach County? A 12-hour shift is now $264 ($22/hr), up 10 percent compared to 2024.

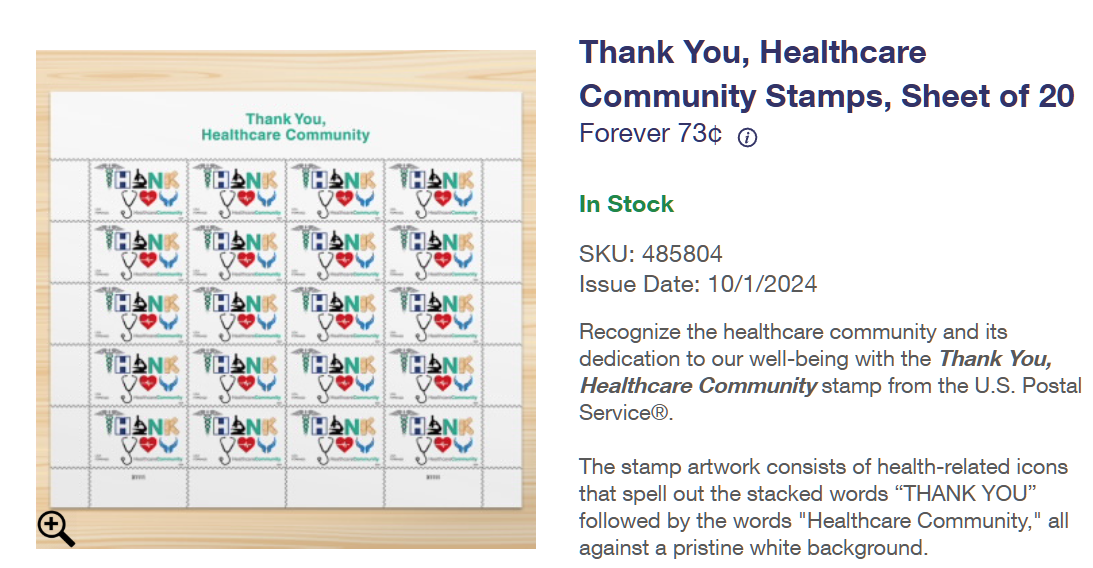

To be featured in a future blog post… a new USPS stamp thanking health care workers:

When will the USPS release a stamp honoring health insurers?

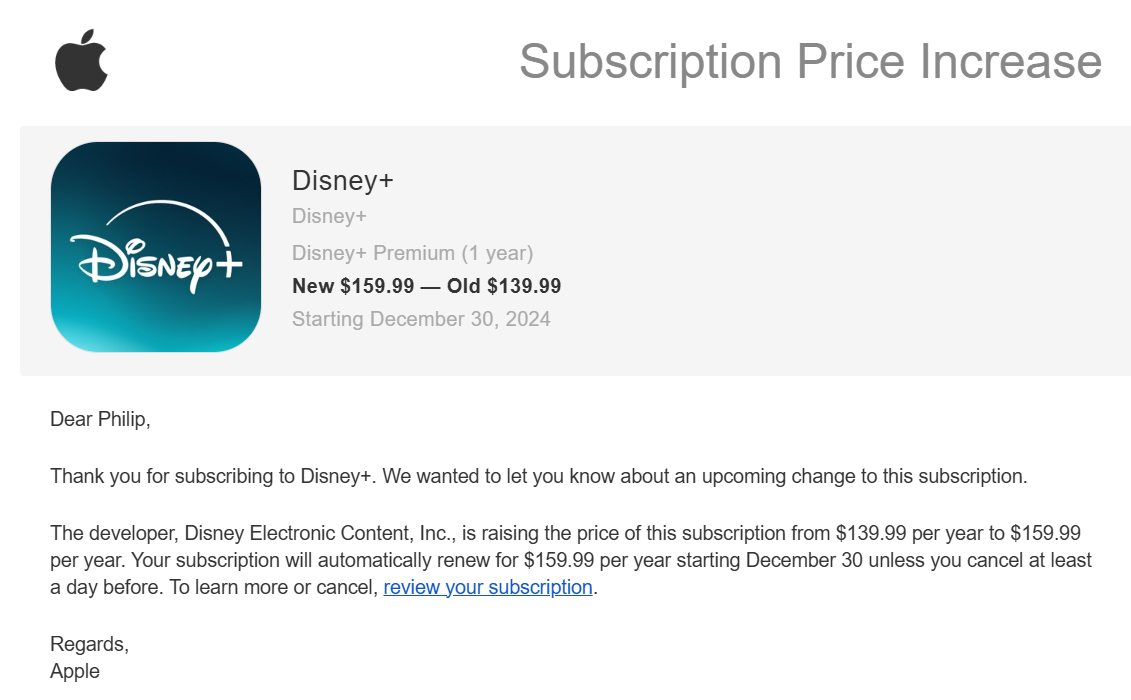

Email received earlier this month about a price increase that begins today:

We are informed that we live in an era of “disinflation” (see for example, Nobel Prize winner Paul Krugman in the NYT, 2023: “How (Many) Economists Missed the Big Disinflation”). I guess disinflation doesn’t preclude disflation (inflation in the cost of whatever Disney is selling).

Now that the election is behind us, the New York Times is writing that inflation and crime are both raging in New York City. “My Restaurant Was Named One of New York City’s Best. Here’s Why It Closed.” (NYT, Dec 28, 2024): “The combination of inflation, rising crime that required us to pay for security guards and declining profits simply proved insurmountable.”

“All the Good Economic News Vindicates Bidenomics” (New York Times, a month before the recent Election Nakba): A week earlier we learned that inflation has continued to decline and is now more or less at the Federal Reserve’s target of 2 percent. This success has defied the view, held by many economists just a couple of years ago, that disinflation would require years of high unemployment.

“Biden’s Chief Economist Processes the Election With ‘Confusion, Guilt’” (New York Times, November 2024): I understand that disinflation is less satisfying to people when they want their old prices back. I get that, and I’m going to have to deal with that, but at the same time, I do not regret talking about the sharp disinflation, or the strong G.D.P. growth or the historically low unemployment rate.

Today the Federal Reserve technocrats depressed investors by saying that interest rates won’t be lowered all that much in 2025 (unsaid: Congress won’t put down the deficit spending crack pipe and, thus, inflation is inevitable). Mary C. Daly, last seen addressing the diversity crisis at the San Francisco Fed and ensuring the stability and longevity of Silicon Valley Bank, voted with the rest of the governors to cut interest rates by 0.25%. The lone dissenter to the cut was from the Rust Belt: Beth M. Hammack, head of the Cleveland Fed (formerly at Goldman). Let’s follow Ms. Hammack going forward and see if she’s right about the inflation that the government and media assure us does not exist.

(A friend asked why the stock market was down today. She’s a physician and had interpreted the news from the Fed meeting as a prediction that the U.S. economy was going into a slump. My response: “Fed said it would have to keep interest rates high. Congress wont stop deficit spending. So the only way to tame inflation is high rates, which means stocks need high yields to compete w bonds. If a stock pays a fixed dividend it can only generate a higher yield by falling in price. Remember if you can buy a bond yielding 6% you need to buy a stock at a price where you’re sure you’ll get at least 8% return.” Curiously, the Wall Street Journal had a headline about the Dow Industrials (below) rather than the S&P 500.)

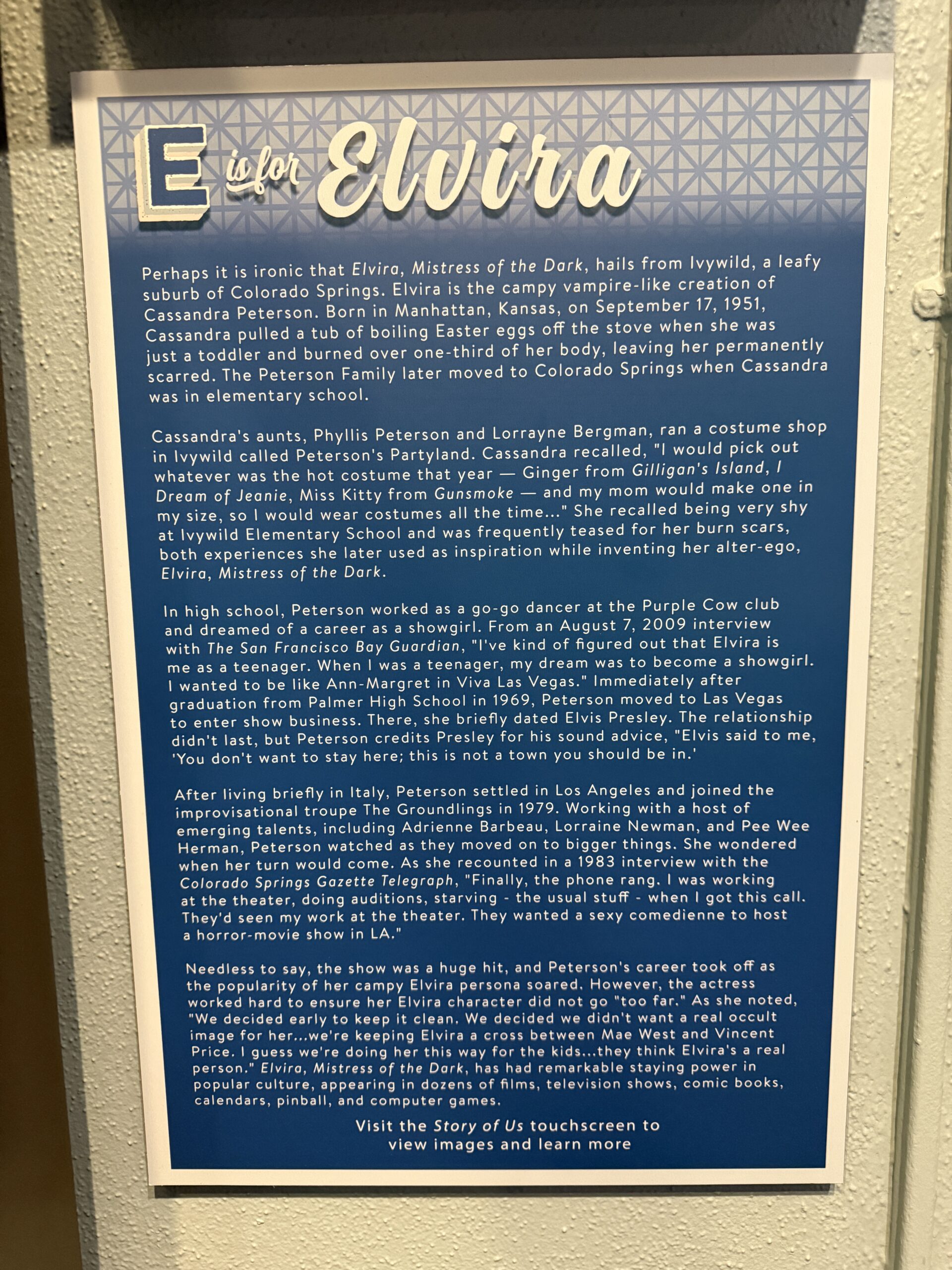

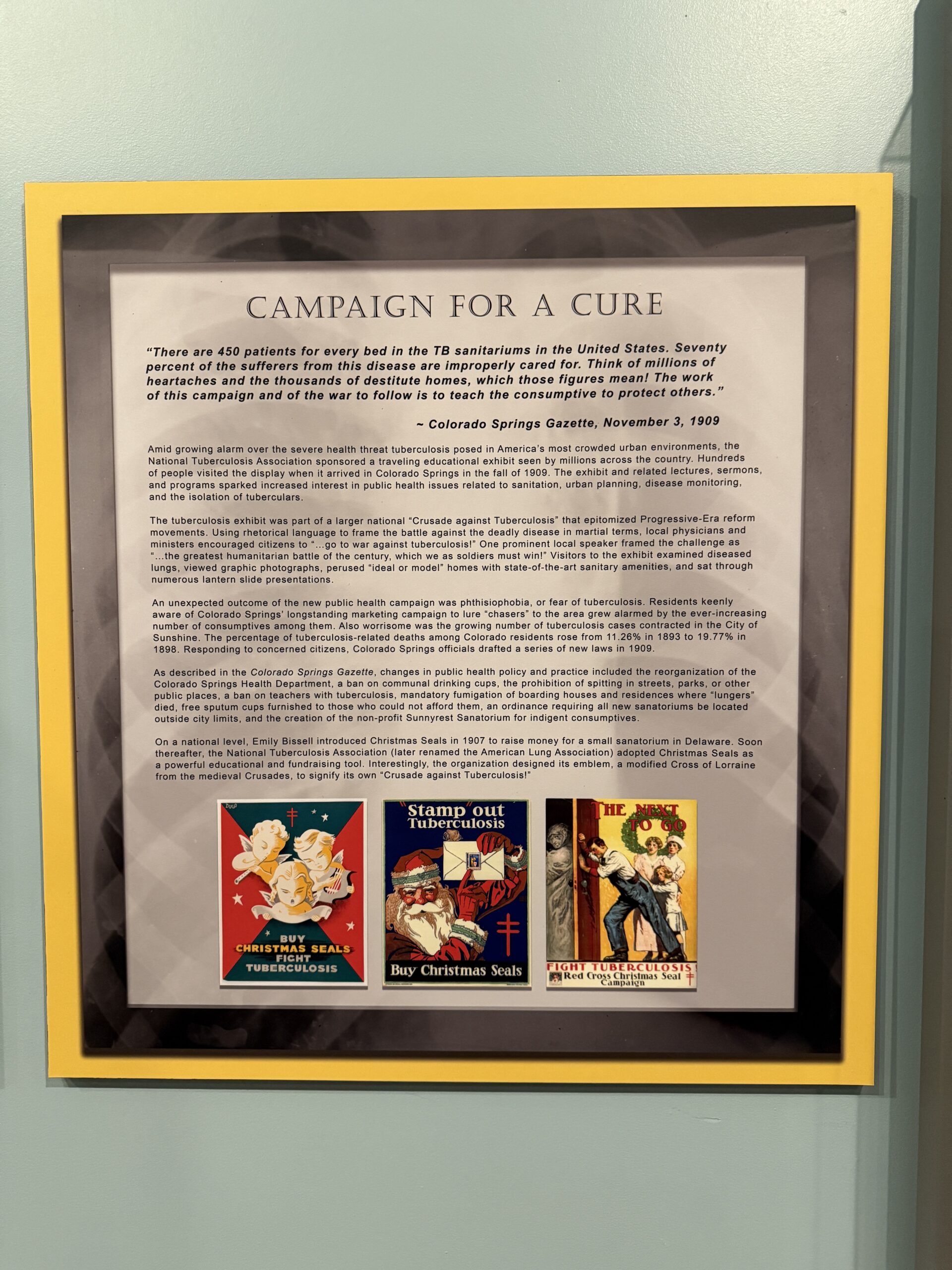

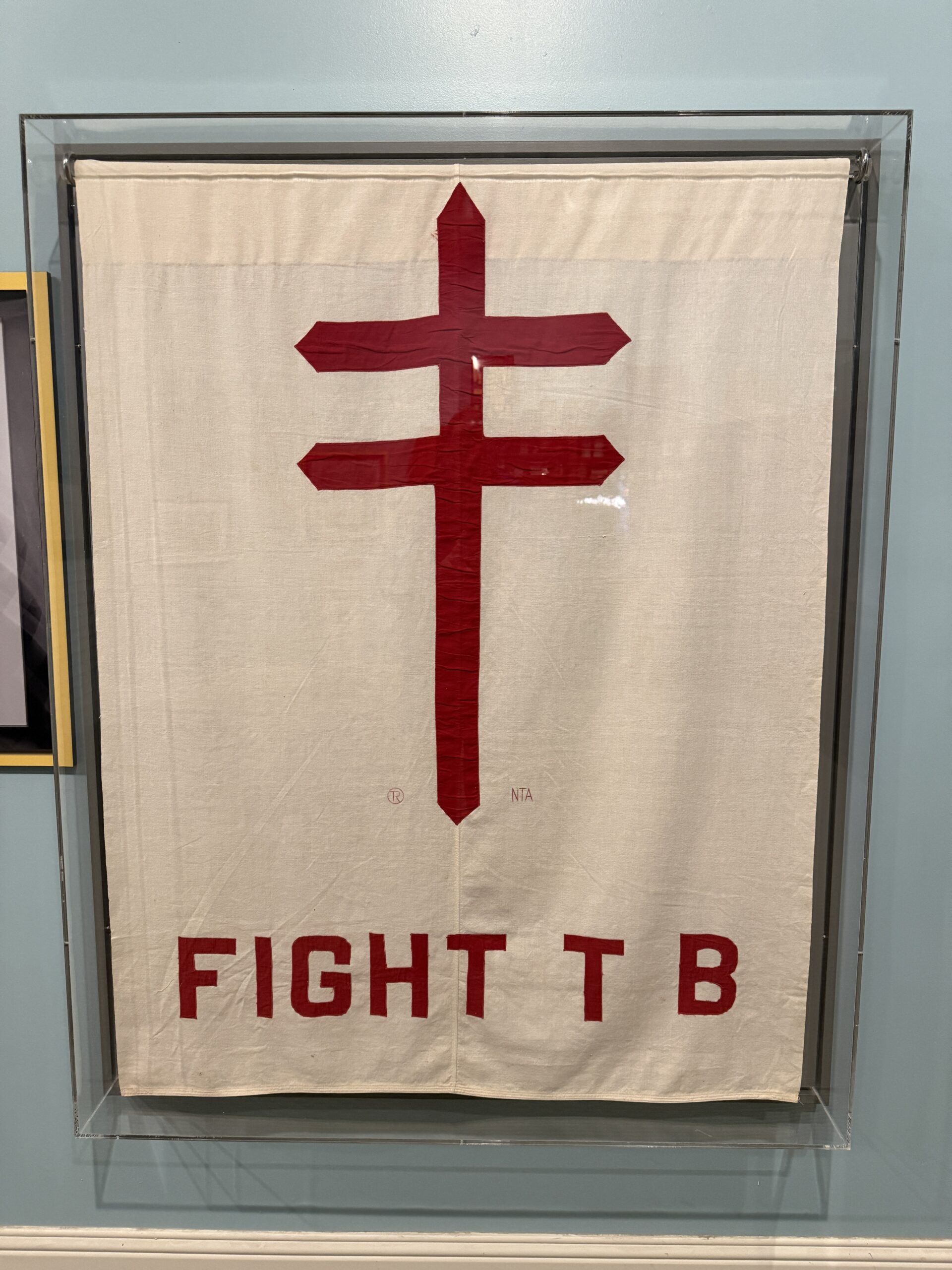

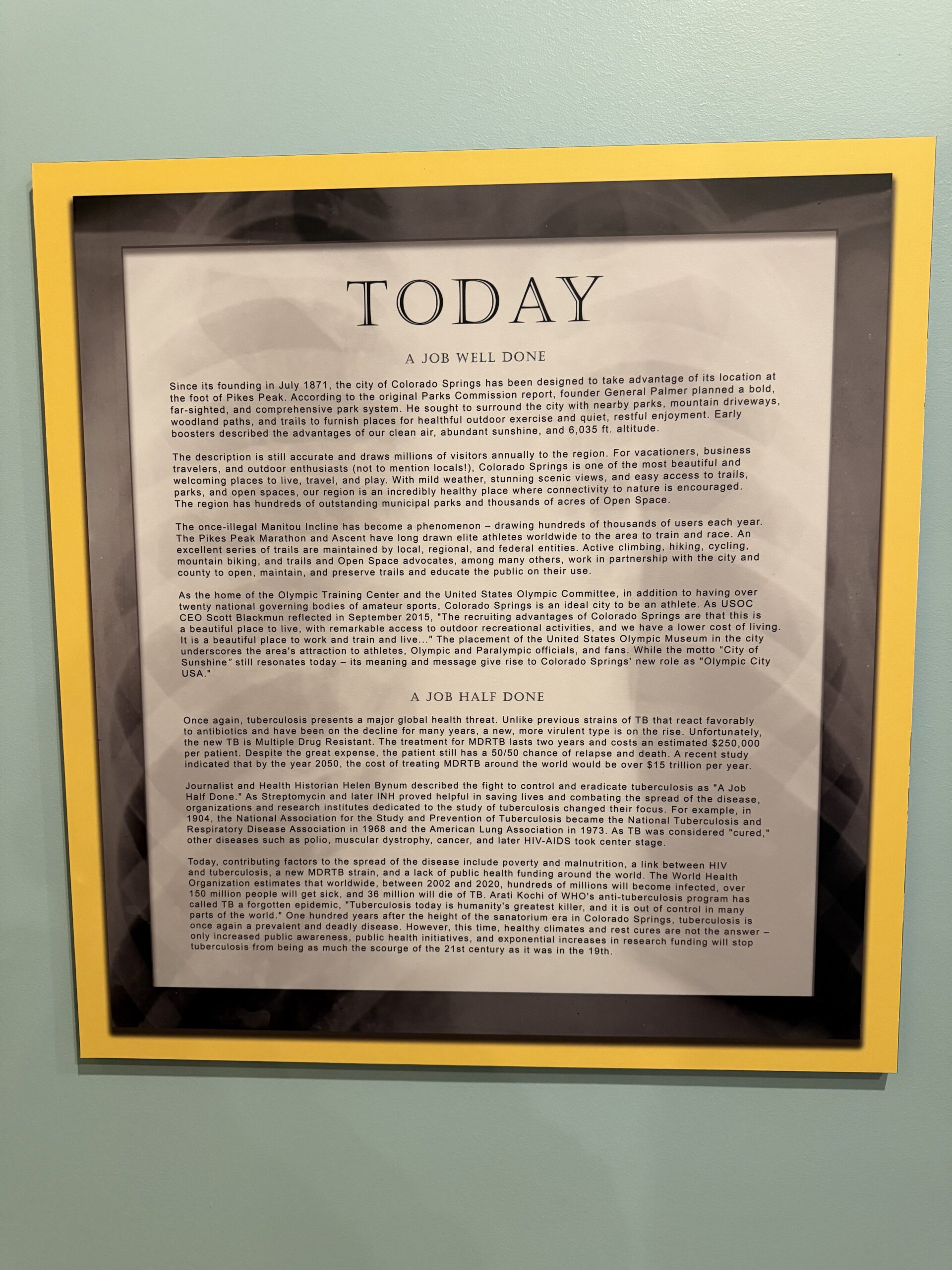

Speaking of non-existent inflation, I went to a museum today in Colorado Springs. It is inside a massive 1903 courthouse that is three stories high with a clock tower reaching skyward beyond. The volunteer at the front desk told me that it cost $420,000 to build.

It was replaced in the 1970s by a monster-sized concrete “judicial center” across the street:

What was inside the museum? An art exhibition in which paintings from any artist with a connection to the region were welcome… so long as the artist identified as “female”:

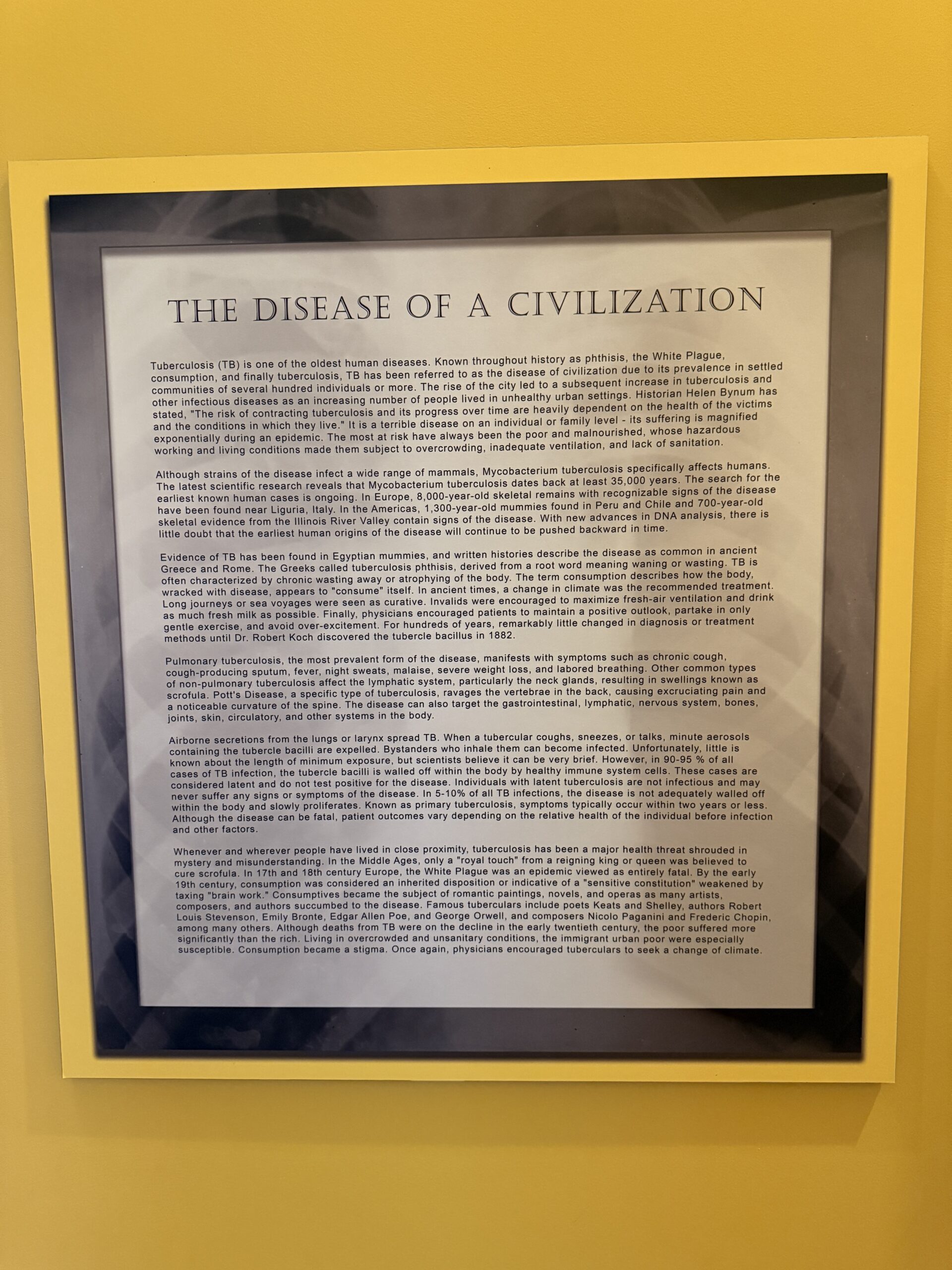

A reminder that SARS-CoV-2 was not the first pathogen to realize what fat targets humans living in cities presented…. (Colorado Springs was a cure destination for tuberculosis sufferers.)

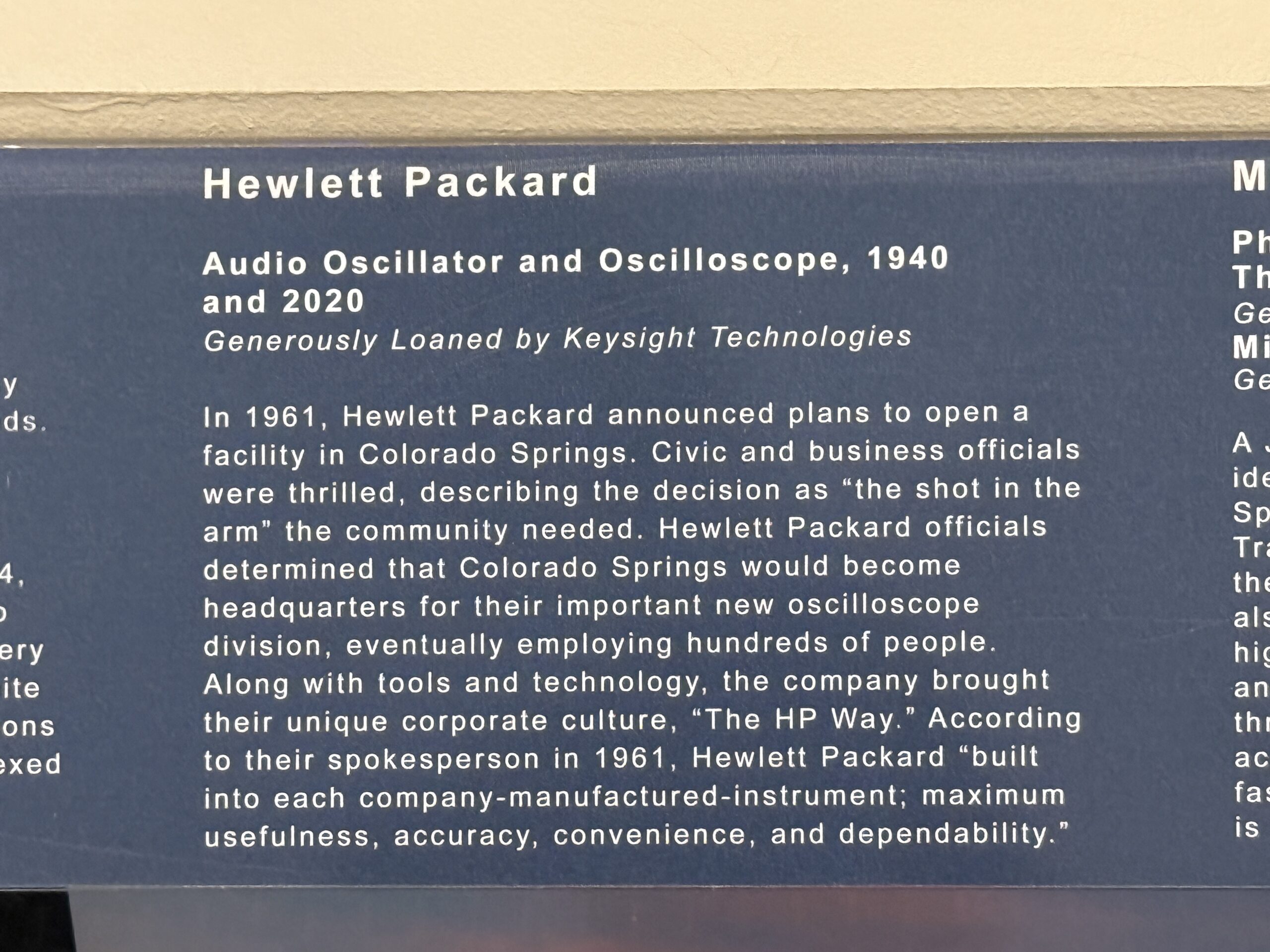

The glorious history of test equipment… (HP had a division here making oscilloscopes, spun off and spun off and now “Keysight”)

It seems as though taxpayers got a good return on their $420,000 investment.

We recently received a notice from my mother’s senior fortress. The basic “room and board” charge for her assisted living apartment (i.e., not the nursing care component) is going up from $8,100 per month to $8,750 per month, effective January 1, 2025. That’s an inflation rate of 8 percent.

Apparently, the average age of moving into any type of “senior dorm” is going up. From McKnights Senior Living, 2023:

the mean age of an older adult moving into assisted living is 85 (by comparison, it’s 82 for independent living and 83 for nursing homes), a finding that aligns with the results of other research.

It’s cheaper to stay in one’s existing house or apartment, even if some aides need to be hired, and there is more freedom, e.g., from coronapanic-style lockdowns. A middle-class American who did not purchase long-term care insurance (my mother has a John Hancock LTC policy and the company has been great about paying for most of what she has needed since transitioning from independent living to assisted) will have a lot of trouble accessing the necessary care. The standard path is for the old person to be wiped out financially and then Medicaid kicks in because the old person is now poor. In Florida, at least, the value of a homestead (primary residence) is excluded, but otherwise the only workaround is a Medicaid Asset Protection Trust and it must be done five years ahead of when it is needed (explained by a NY lawyer).

Our neighborhood HOA fee is going up 18 percent for 2025. The management fee (same firm) is going up 43 percent. Xfinity’s fee for cable TV to every household is going up 7 percent (each house must separately purchase Internet service). Xfinity’s fee for telephone/Internet service at the clubhouse is going up 70 percent to $7,000/year. Landscaping and irrigation services are going up substantially, but perhaps that reflects the landscape and systems getting older (22 years). “Janitorial” (cleaning our clubhouse/gym, mostly?) is going up 13 percent. Insurance is going up 10 percent.

This year let’s give thanks for not having been killed at any point during the preceding 12 months. And let’s also give thanks to the engineers behind the technologies that make it possible to survive a plane landing in the ocean or a boat sinking in the ocean. The PLB/EPIRB is critical, of course, but even ChatGPT can’t come up with the names of individual engineers whom we should thank. Same story with the latest smartphones, which are capable of sending distress calls to satellites. If rescue doesn’t arrive immediately, it is important to get out of the colder-than-body-temp, possibly-shark-infested water, and that’s where a life raft comes in. ChatGPT credits Horace H. Day for an 1846 “Portable India-rubber boat” (U.S. Patent No. 4356) and “Peter Halkett, a British Royal Navy officer who, in the early 1840s, designed an inflatable boat using Macintosh cloth.” So let’s give Messrs. Day and Halkett a thank-you today!

Aviation life rafts are supposed to be recertified every 1-5 years, depending on model and packaging. The raft gets unfolded, I think, and then a technician checks for leaks and condition before folding it all back up. The manufacturer of our 16-lb. 4-man raft charged $115 for this service in 2018, plus an additional $100 for an every-five-years cylinder overhaul. This month I got a quote for the same service on the same raft… 450 Bidies plus 200 additional Bidies for the cylinder. It’s mostly the same people at the same company in the same SE Florida location, yet the five-year cost for keeping the raft certified (this is an older model so it has a one-year interval) has gone from $675 to $2,450, inflation of over 260%. It will require some creativity to come up with a way to be grateful for this increase, though we are assured by the New York Times that our wages have gone up far more than 260 percent during the Biden-Harris administration.

Here’s what a modern minimum-size/weight raft looks like:

Here’s a video of the gold standard Winslow raft being inspected:

Why not use the gold standard, you might ask? A Winslow 4-man raft is 2X the weight and bulk. Every lb. counts in aviation! A Switlik is even heavier, but has a five-year service interval.

It looks easy in this video…

Update, April 2025: It took me a while to get the raft down to Sunrise, Florida (west of FLL). The cost was $659 plus $40 in tax to the hated dictator Ron DeSantis: almost $700 total (vs. $215 plus shipping in 2018). I think that the manufacturer made a mistake because aircraft equipment and repairs are free of sales tax in Florida so long as the tail number and max takeoff weight is written on the invoice. I asked David Brennan, a tax attorney at Moffa, Sutton, & Donnini who is an expert on aviation tax and Florida sales tax, and he didn’t think that the raft was sufficiently tied to the aircraft for maintenance on the raft to be considered maintenance on the aircraft. “Exemptions place the burden on the person claiming as much, with any doubts/ambiguities resulting in the tie or outcome being in favor of the state,” he noted. (In other words, my conjecture was wrong!)

Related:

Coronapanic Consequences: life rafts (2023; everyone was back-ordered): “Switlik is a supplier to the U.S. Coast Guard, which presumably knows water at least as well as Dr. Fauci knows SARS-CoV-2.”