Leftover Inflation?

We are informed by the Biden-Harris administration and media allies (“America’s fight with inflation has been won”, noted the Guardian a few days ago) that inflation has been vanquished. I wonder if there is a significant “leftover inflation” yet to come, though, from companies and people who neglected to raise prices or who were locked into long-term agreements during the core years of Bidenflation. The guys who push buttons at container ports recently won a 62 percent raise (ABC). Boeing workers recently won a 43 percent raise (NYT). A friend who owns an expensive-yet-crummy compound of wooden structures in Vermont (and a Grenadier INEOS that he loves) and rents a cottage out was just hit with a 100 percent increase by his long-time cleaner. I myself was recently hit by a 33 percent increase by the cleaner of the Harvard Square condo that I still own and rent out via AirBnB (cleaning cost up 60 percent compared to 2019). AT&T workers recently won what might be a 30 percent wage increase (wages boosted plus health insurance contributions lowered; the union).

The above-cited increases in costs must eventually be reflected in higher prices to consumers for (a) goods that come in via container ports, (b) airline tickets, (c) vacation rentals, (d) Internet and cable TV service. And the higher costs faced by consumers should lead to demands for higher wages in a classic Jimmy Carter-era wage-price spiral (I always predict this and, until the Biden-Harris-Whoever-Has-Actually-Been-Running-The-Country administration, was always proven wrong).

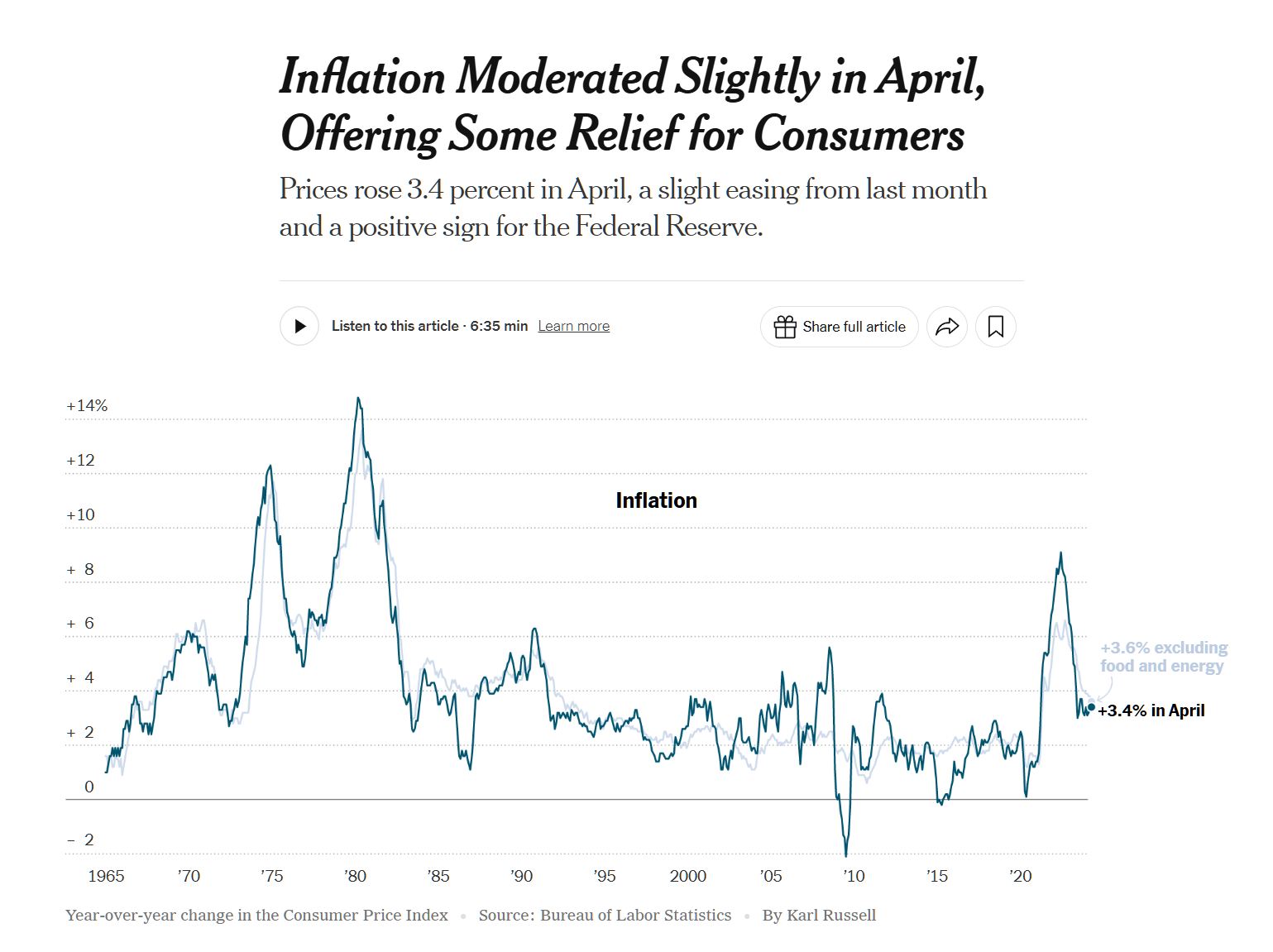

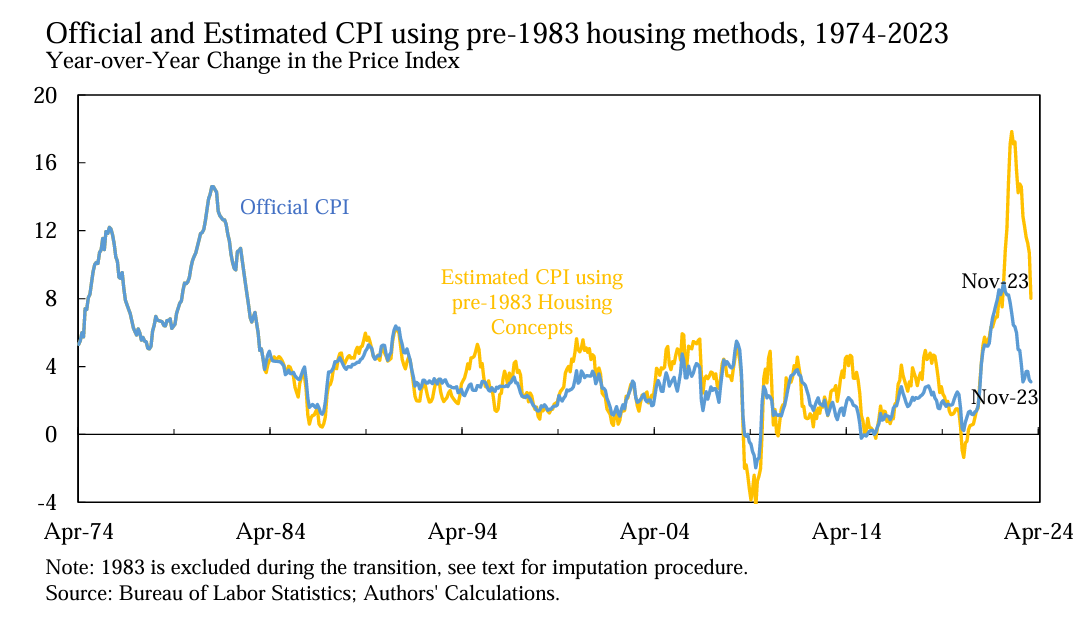

Today the wise minds of the Federal Reserve who at least partially authored Bidenflation will set interest rates. Readers: Who wants to predict what they announce and, more important, what official inflation (which doesn’t include most of the stuff that you’d spend money on, e.g., buying a house) will be on July 15, 2025, by which time the rate set today might have had some effect.

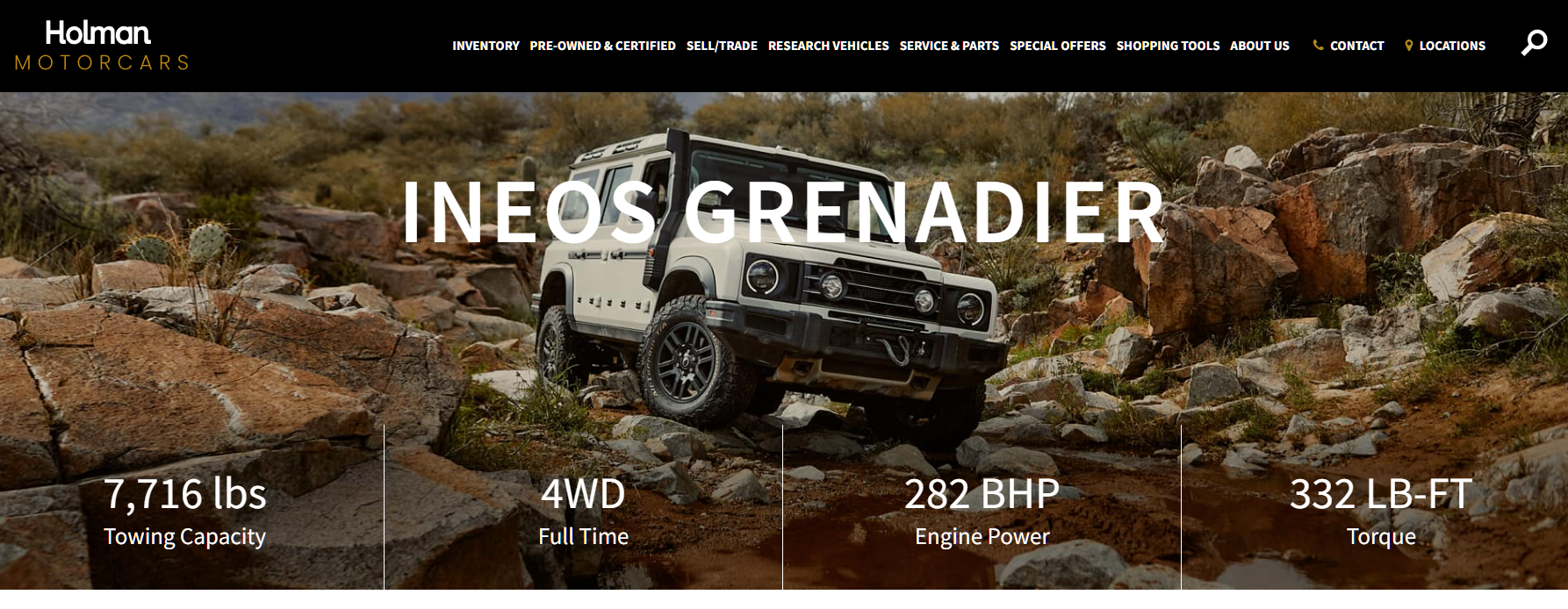

My prediction for the CPI released on July 15, 2025 is 3 percent. I’ll schedule a blog post to check this! Meanwhile, if you have 100,000 Bidies to spend on a 1970s tech Land Rover Series III-style vehicle made by a British billionaire who is a tax refugee living in Monaco… the Grenadier:

The above is the web site of the SE Florida dealer and features the rocky terrain that might be encountered on Ocean Drive in Miami Beach.

Update: The Fed did the expected thing and cut its rate by 0.25 percent.

Related:

Full post, including comments