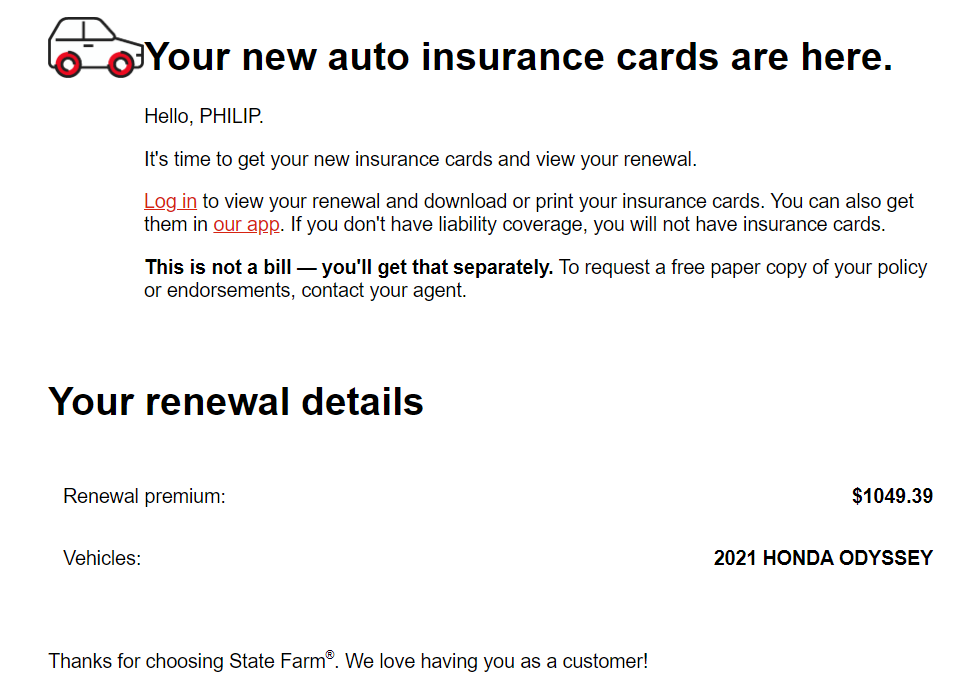

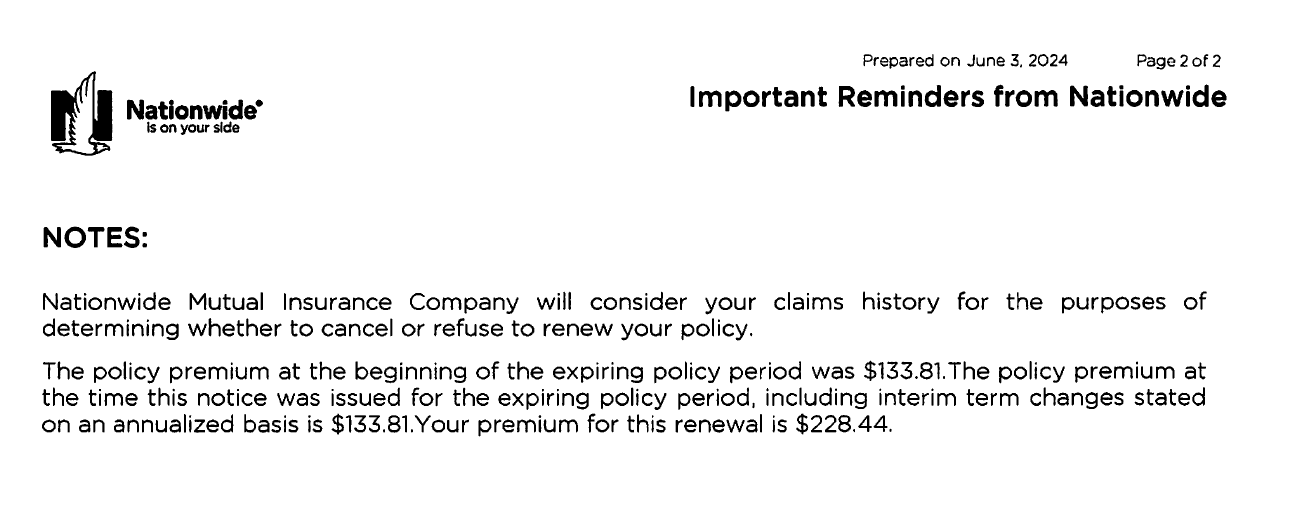

State Farm, January 19: $936 + $884 = $1820 for six months of car insurance.

State Farm, July 20: $1049 + $1001 = $2050 for six months of insurance.

That’s a 12.6 percent increase in half a year. If we weren’t assured that we live in an inflation-free economy, we would call that “25 percent/year inflation”.

(It’s the same two cars and, ordinarily, they would be worth less every six months. Thus, the rate of increase is actually higher than 25 percent (but it is not “inflation”).)

We are informed that the Biden-Harris team has whipped inflation, e.g., from state-sponsored PBS, February 2024: “Inflation is nearly back to 2 percent.” (“inflation nearly conquered”)

What’s happened to prices since February?

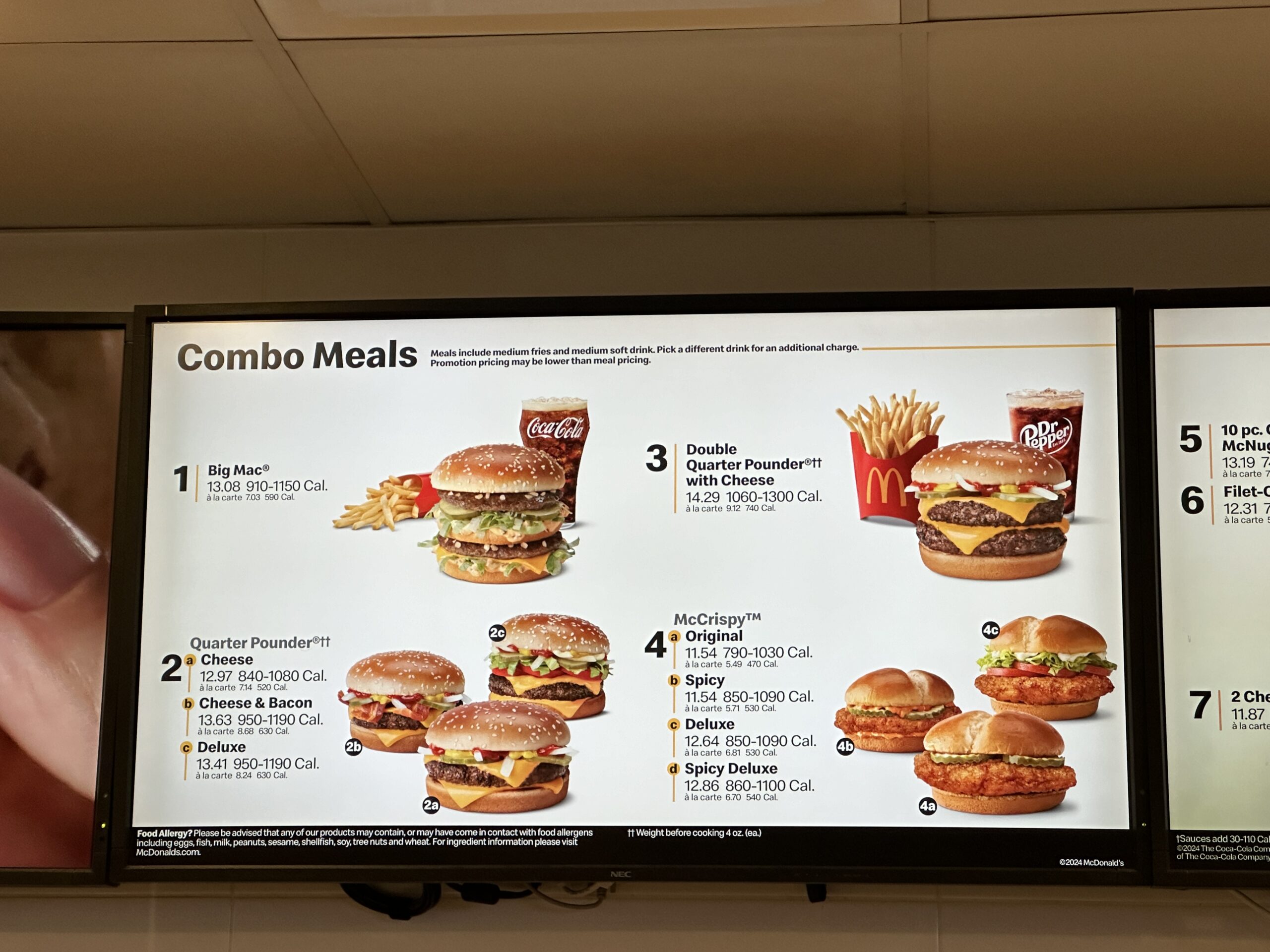

Here’s the menu at the Orange County airport McDonald’s, March 13, 2024:

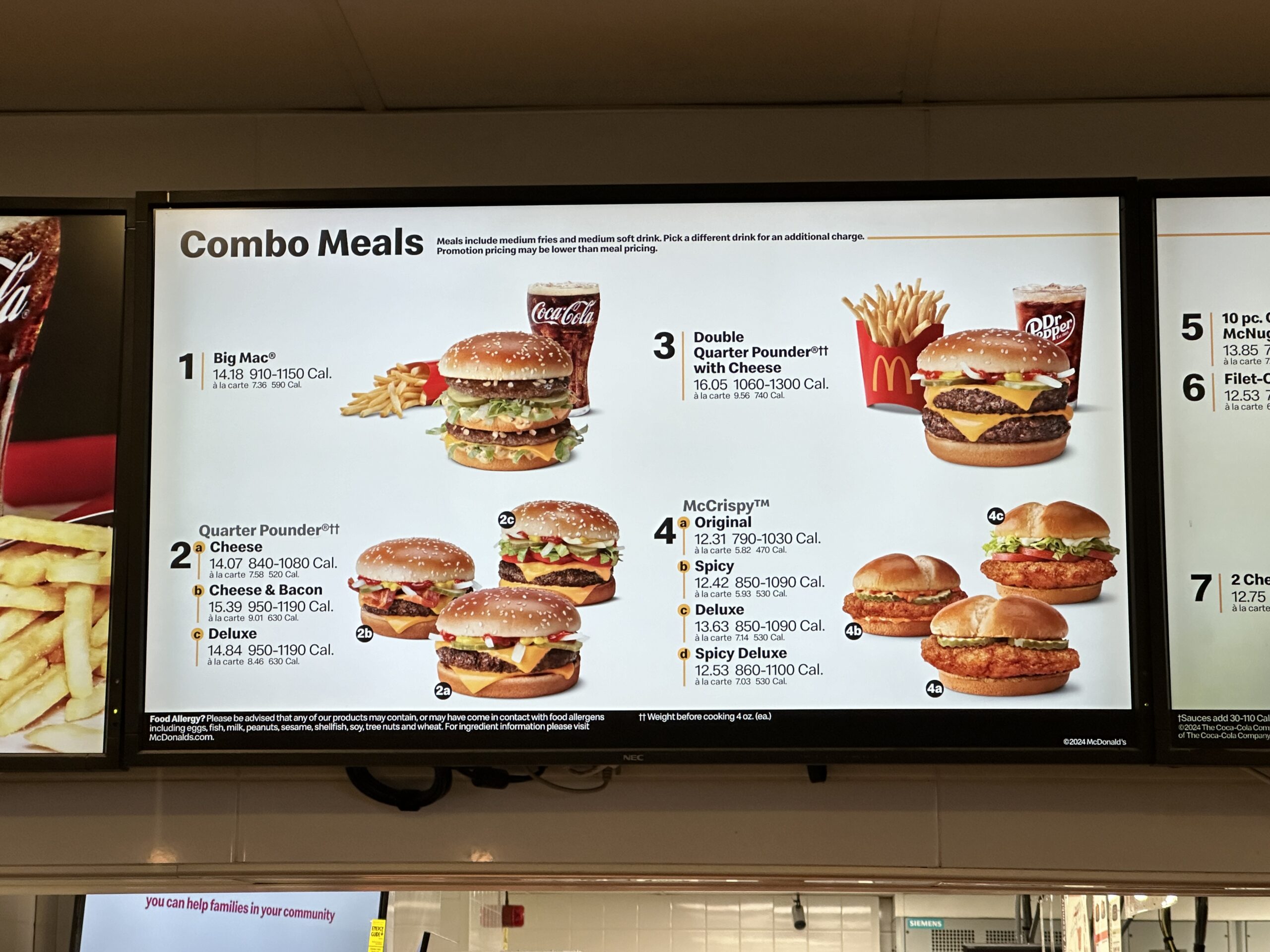

The same menu on July 31, 2024:

The pictures were taken 140 days apart, which is 0.38 years. In other words, to get an approximation of the annual price change we have to multiply the price change rate between the two photos by 365/140.

The Big Mac meal is $14.18, up from $13.08. That’s a rise of 8.4 percent, adjusted to an annual rate = 21.9 percent.

How about the Royale with Cheese (Deluxe, of course)? That’s up from $13.41 to $14.84, a lift of 10.6 percent. If we didn’t live in an inflation-free society, that would be an annual inflation rate of 27.8 percent.

Also on July 31, 2024, a friend who does some software consulting work decided to raise his hourly rate from $350 to $425 (a 21.4 percent increase).

I canceled the policy because (a) it isn’t valid if the policyholder lacks underlying insurance, (b) I don’t expect mom to do a lot of physical damage with her walker, and (c) $1 million isn’t enough to cover even a tiny fraction of the damages ladled out by juries when a non-physical injury is found (see E. Jean Carroll, for example, who suffered $83 million in damage to her reputation when her veracity was questioned).

Nationwide Pet, the country’s largest provider of pet insurance, says it is dropping about 100,000 policies between now and next summer to keep up with spiraling costs in vet care.

The move comes as other types of insurance, from homeowners to vehicles, are increasingly becoming harder to obtain for many Americans.

“Inflation in the cost of veterinary care and other factors have led to recent underwriting changes and the withdrawal of some products in some states — difficult actions that are necessary to ensure a financially sustainable future for our pet insurance line of business,” Nationwide said in an announcement last week.

I can’t figure out which 100,000 policies they’d choose to drop. If inflation in vet costs is a nationwide (so to speak) phenomenon, how does it help to pick certain policies to drop and others to keep? By breed? Age of dog?

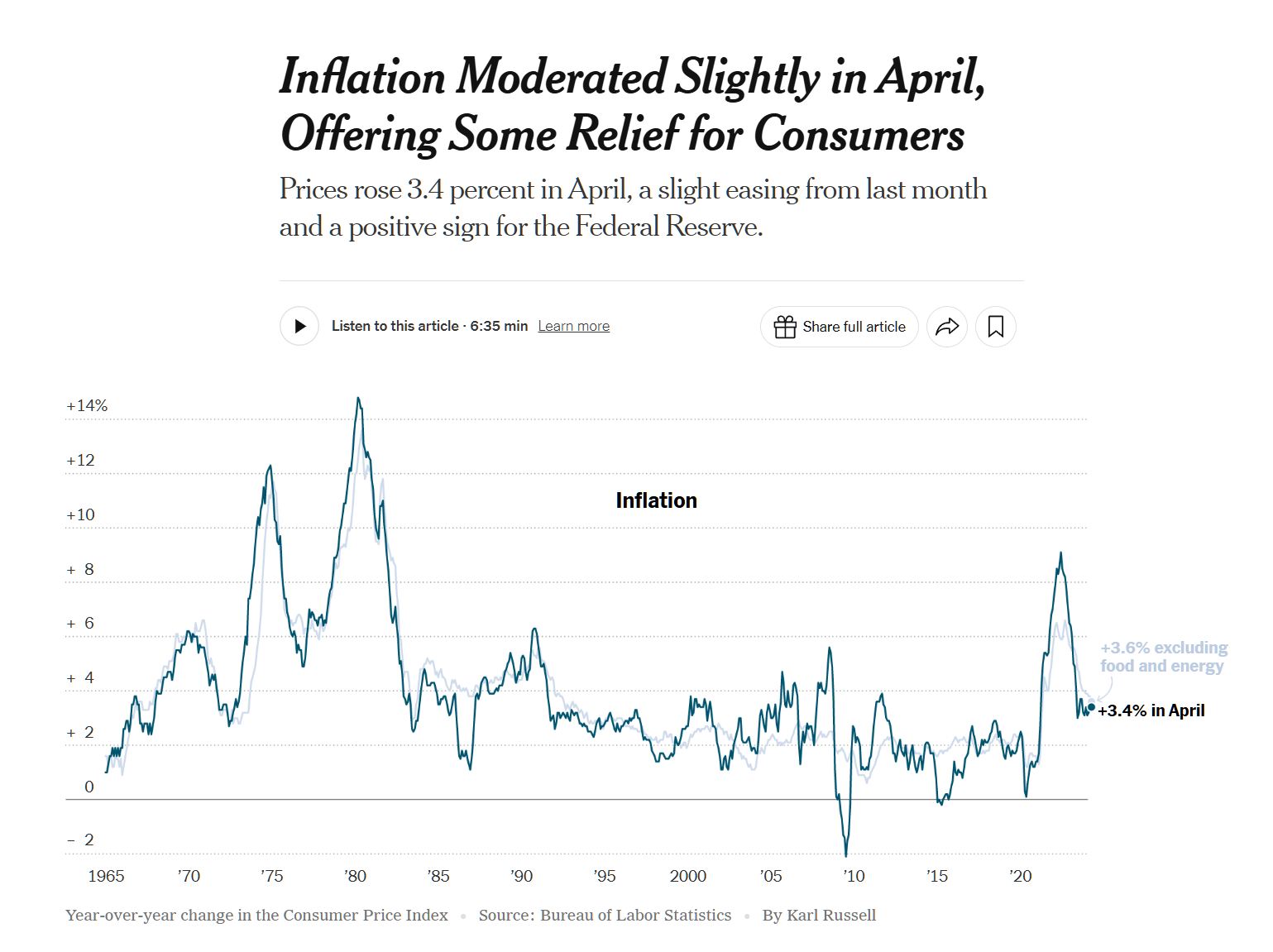

The Consumer Price Index climbed 3.4 percent in April from a year earlier, down from 3.5 percent in March, the Labor Department said on Wednesday. The “core” index — which strips out volatile food and fuel prices in order to give a sense of the underlying trend — rose 3.6 percent last month, down from 3.8 percent a month earlier. It was the lowest annual increase in core inflation since early 2021.

The report followed three straight months of uncomfortably rapid price increases that rattled investors and worried policymakers at the Federal Reserve. Economists cautioned that one month of encouraging data was far from enough to put those worries to rest. But they said that the data should ease concerns, at least for now, that inflation is re-accelerating.

If you couldn’t afford stuff previously, therefore, you’ll be “relieved” to learn that prices are yet higher.

Even more confidence-inspiring… an 81-year-old who never took an economics class is tackling what non-NYT readers might perceive as a problem:

“I know many families are struggling, and that even though we’ve made progress we have a lot more to do,” Mr. Biden said in a statement released by the White House. He called bringing down inflation his “top economic priority.”

If you don’t like higher prices, it’s “progress” when prices are higher every month. Maybe it doesn’t matter that the president hasn’t taken economics because he/she/ze/they is advised by expert economists? Let’s look at the chair of Joe Biden’s Council of Economic Advisors:

Bernstein stated he grew up in a “musical family” and aspired to be a professional musician as a young person. Bernstein graduated with a bachelor’s degree in music from the Manhattan School of Music where he studied double bass with Orin O’Brien. Throughout the ’80s, Bernstein was a mainstay on the jazz scene in NYC.

He also earned a Master of Social Work from Hunter College as well as a DSW in social welfare from Columbia University’s school of social work

(He’s so old that he could get to class at Columbia without pushing through a thicket of tents and Palestinian flags!)

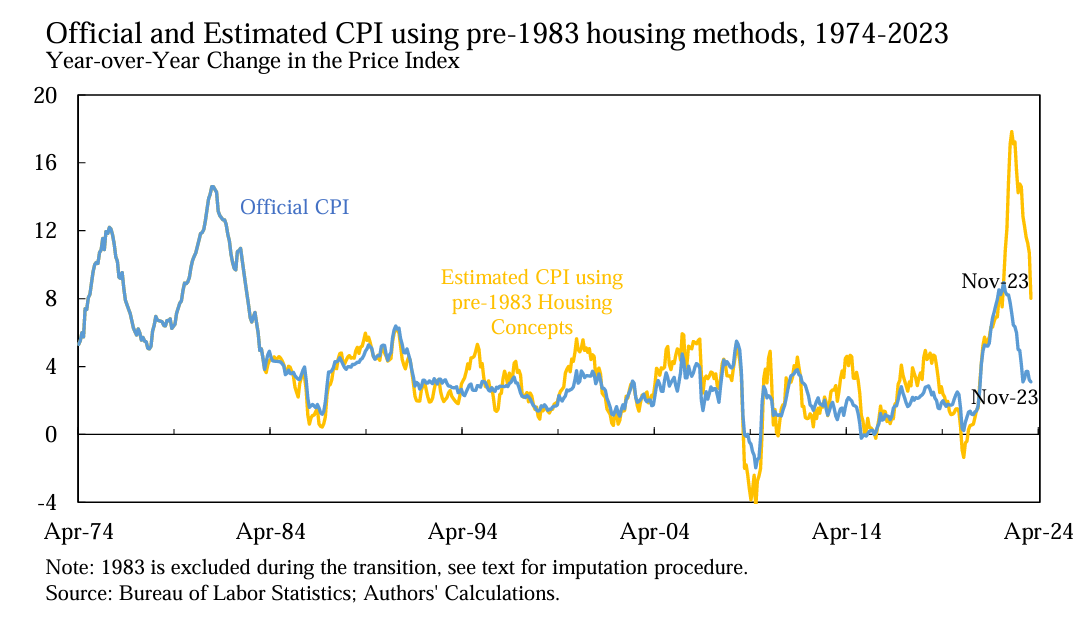

The NYT deceptively charts CPI since 1965 without noting that the definition has changed dramatically over this period. The reader is left with the impression that things were far worse during the Jimmy Carter “malaise years”:

Larry Summers and friends, though, show us what the chart would look if you simply undid the big change from 1983 to use a fictitious rent measure rather than actual housing costs. In fact, Bidenflation is roughly comparable in intensity to the inflation that Americans suffered as a consequence of the Kennedy/Johnson expansions of the welfare state and the Kennedy/Johnson decisions to enter the Vietnam War (Carter gets blamed for this, but the seeds were sown in the 1960s).

Mostly I find the above fascinating as an example of journalism that purports to be neutral and skeptical yet in fact is primarily propaganda about the great job that our rulers are doing.

Back in 2020, a former UK central banker predicted raging post-coronapanic inflation followed by 3-4 percent annual inflation rates starting at the end of 2022 and continuing for decades (see Inflation prediction to check in 2028). Here’s the official chart of CPI, mostly fraud because it doesn’t include the actual cost of housing:

What are you all seeing? A painting contractor in Cambridge did not start a project that he’d been hired to do last year. It had been scheduled for the fall of 2023. He demanded 20 percent more to do the same work starting in the spring of 2024, an inflation rate of 40 percent.

At the Flour bakery in Harvard Square, a $72 pie:

At a McDonald’s on the Mass Pike in western Maskachusetts, $15 for a standard meal including tax:

Although we did not pony up $72 for a pie, the Flour bakery experience was worth the $40 that my friend paid for our take-out lunch (two sandwiches, a drink, a brownie, tax, and tip). The line included not only an apparently young healthy female in an N95 mask but also a woman wearing a Palestinian keffiyeh-patterned sweater. As a bonus, this high-priced establishment sports a Black Lives Matter sign in the front window:

I’m not sure how retailers decide which social justice cause to support. Patagonia, which demanded eye-popping prices before Joe Biden made them popular, doesn’t care about Black Lives and instead proudly displays its allegiance to Rainbow Flagism:

Happy Tax Day for those in the U.S. and also U.S. citizens who live abroad and get no services from the U.S. but still must pay taxes (consider the U.S. citizens held hostage by Gazans, for example).

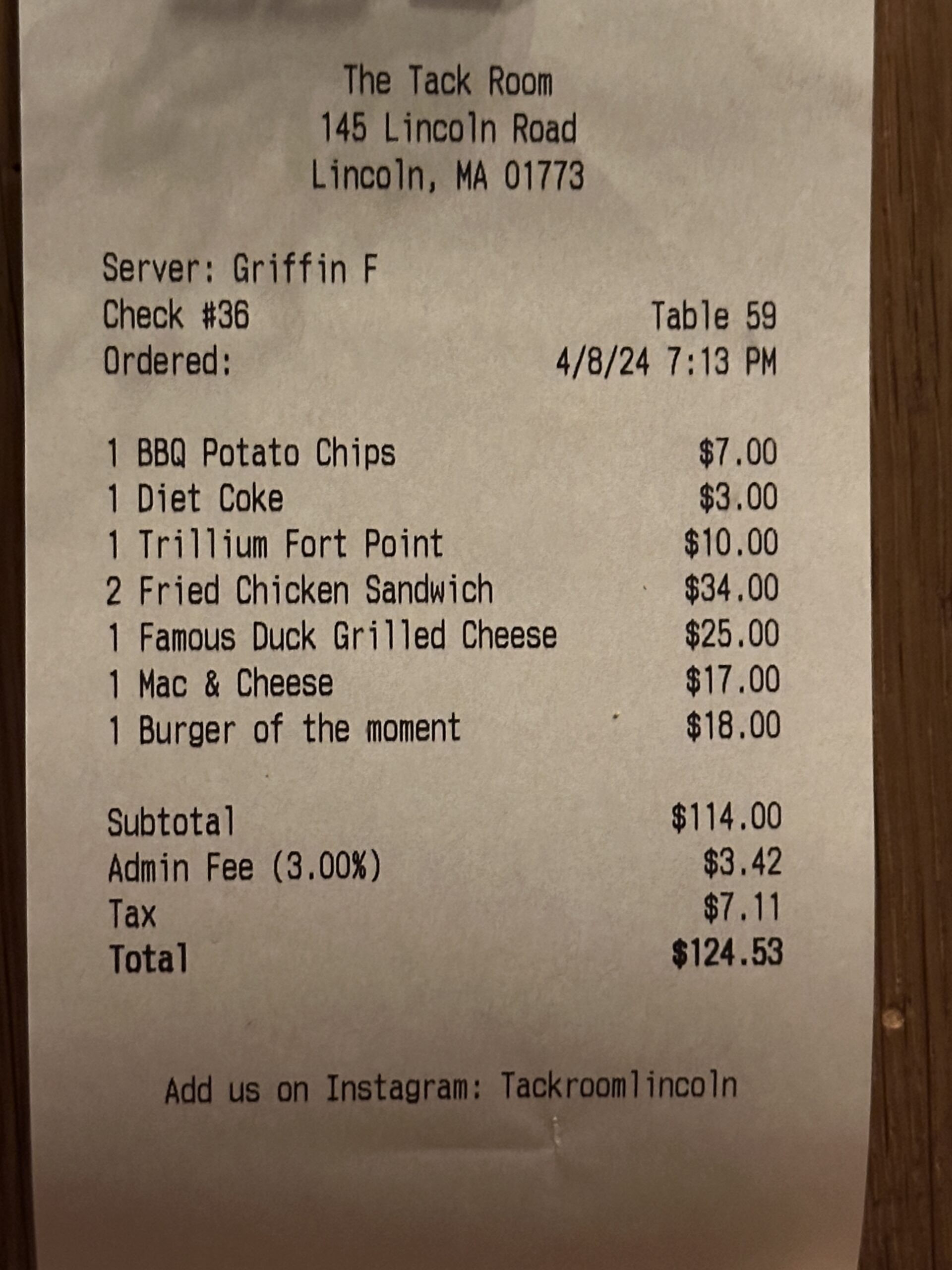

How about a new 3 percent tax from a restaurant on the restaurant and kept by the restaurant, couched as an “Admin Fee” on the receipt?

One of my companions asked what it was for. The waiter responded, “It’s a fee that we incur to keep our prices competitive.”

Note the solution to the inflation problem that the government tells us is entirely in our minds: tape over all of the prices and tell the customer what it’s going to cost only after he/she/ze/they orders.

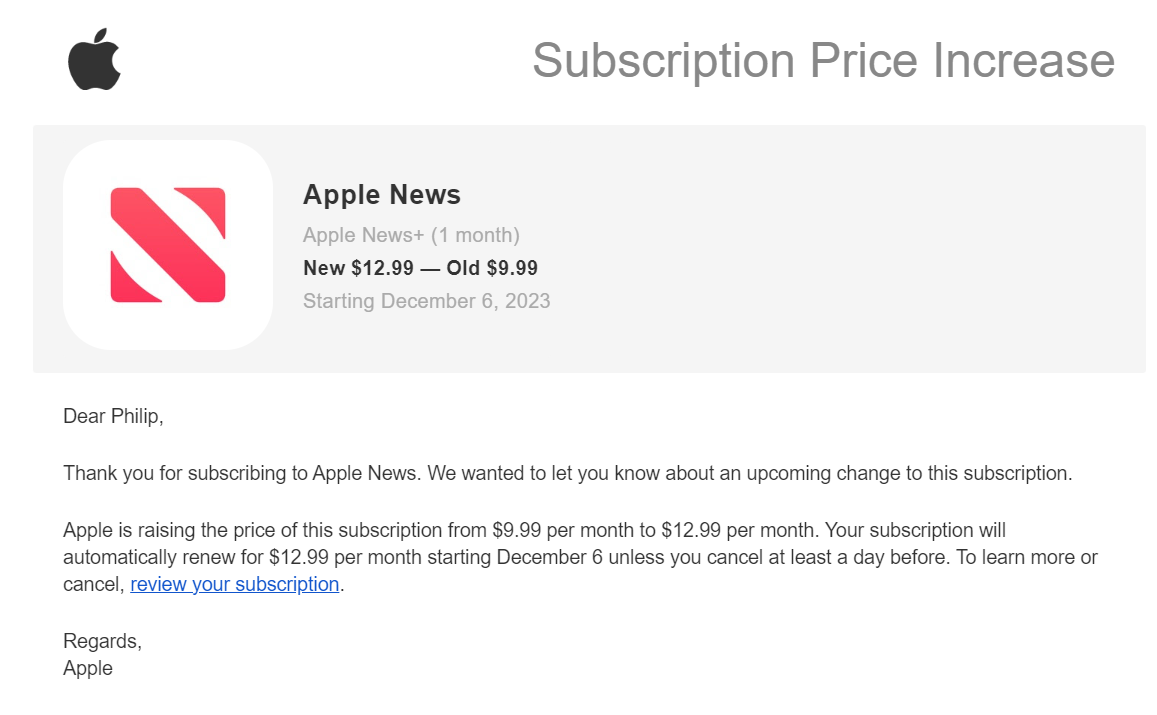

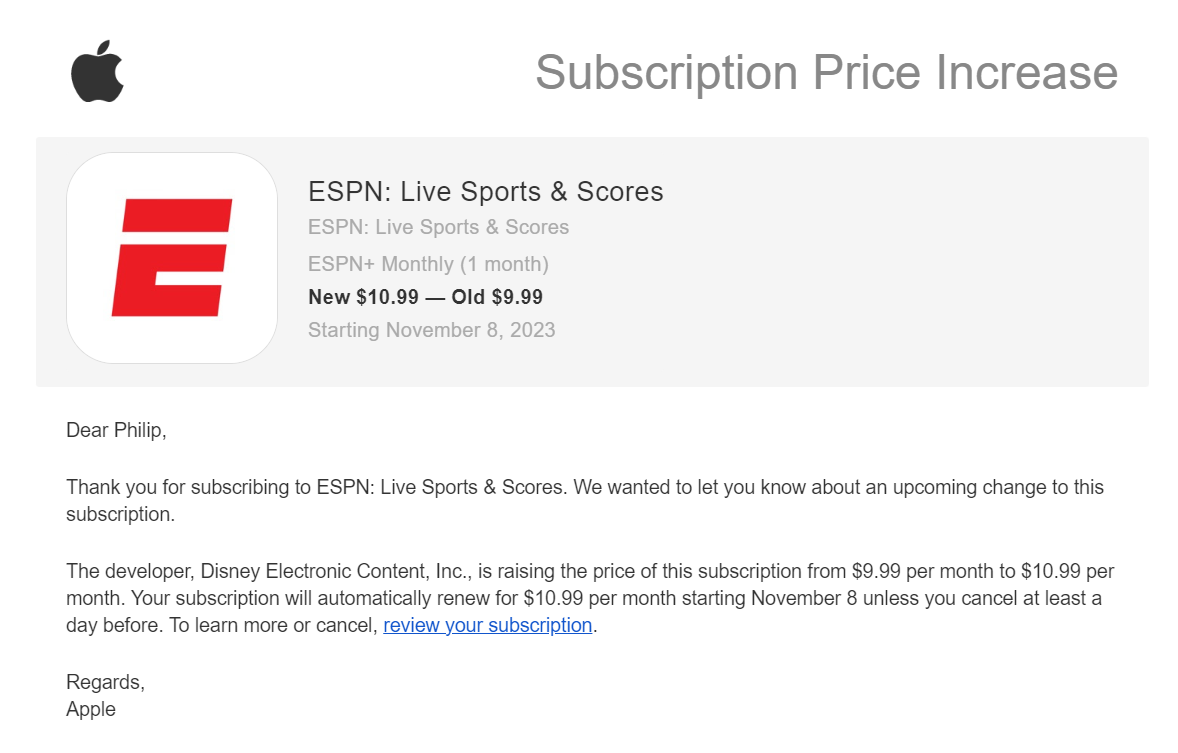

Today is my last day of Apple News+, the cost of which was recently raised by 30 percent:

I’m not sure what justifies this increase. The major news organizations have mostly been harvesting outrage from Twitter, reposting information straight from the Islamic Resistance Movement (“Hamas”), reporting on what other news outlets are saying, etc. Couldn’t ChatGPT do most of this? If so, news subscriptions should be getting cheaper, not more expensive. Maybe the 30 percent bump is consistent with media costs in what the media assures us is a mostly inflation-free environment? The latest union contract at the New York Times raised salaries by only 12.5 percent (NYT, May 23, 2023):

The New York Times reached a deal on Tuesday for a new contract with the union representing the majority of its newsroom employees, ending more than two years of contentious negotiations that included a 24-hour strike.

The agreement, if ratified, will give union members immediate salary increases of up to 12.5 percent to cover the last two years and 2023, and will raise the required minimum salary to $65,000, up from about $37,500. The previous contract expired in March 2021, and union members have not received contractual raises since 2020.

Under the contract, the median salary for reporters in the union would be about $160,000.

(The above raises a question: Why weren’t the progressive owners of the NYT willing to pay a fair wage? Why did it take two years of contention and a strike before the NYT agreed to what the union asked? Also, note that median full-time workers in the U.S. earn about $58,000 per year (BLS) and that includes government workers with their higher-than-private-sector wages. So even the lowliest journalist at the NYT is above the level of Americans identified as the principal financial losers from low-skill immigration (Harvard study) and, of course, being a native English speaker is a huge advantage in the journalism marketplace.)

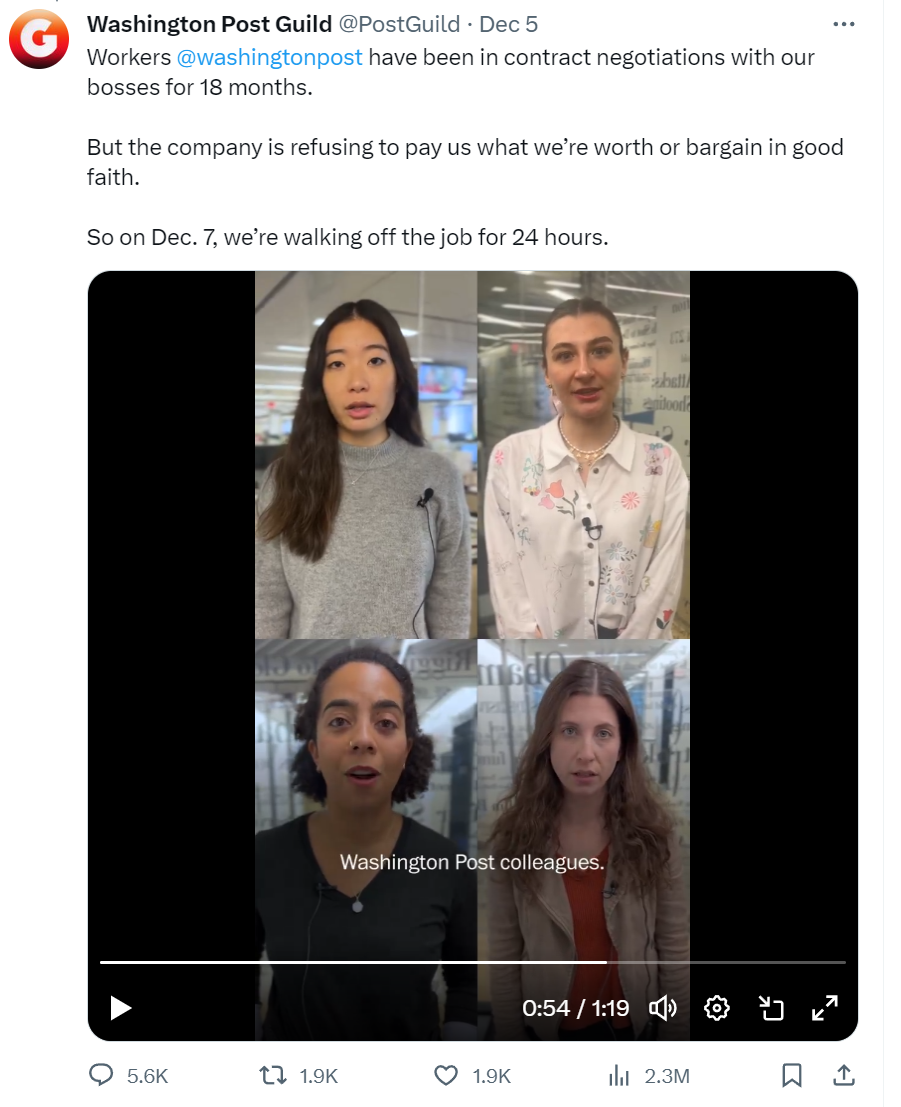

Speaking of labor unrest, the progressives who scribble for the Washington Post are striking tomorrow because the DC insiders who manage the paper won’t pay them what they’re worth:

Young Americans are the country’s most pro-union generation. Labor has poll ratings most politicians only dream about, and the Biden administration is making workers’ pay, benefits and rights its calling card.

Lest anyone doubt where the administration stands, the Treasury Department released what it proudly called a “First-of-Its-Kind Report” on the economic value of organized labor. It found that unions raise the wages of their members by 10 to 15 percent, have “spillover effects” that benefit nonunion workers, “reduce race and gender wage gaps” and “boost businesses’ productivity.”

All this adds up to a large cultural shift, said Heidi Shierholz, president of the pro-labor Economic Policy Institute. The fact that unions are in the news again means it’s more likely that those who feel they are being treated unfairly “see a possible path to help remedy what’s going on in their own job.” This contrasts with recent decades when “unions were not being talked about at all.”

On this Labor Day, from the president on down, that’s no longer a problem.

Why won’t the paper take its own advice and give the union what it asks for?

At the moment, wages are rising faster than inflation, which means that “real,” or inflation-adjusted wages, are rising.

“There is almost no evidence” that wage increases lead to inflation, Rosenberg wrote. His firm conducted a statistical test (called Granger causality) that found inflation causes wage increases, but not the other way around. He predicted that rather than passing along higher wage costs to customers, companies would be forced to swallow them and accept lower profits.

In other words, the Science of Rosenberg and Granger proves that cars and bicycles sell for the same amount because higher costs for producers don’t shift the supply curve and change the equilibrium price.

The School District of Palm Beach County reached an agreement with the Palm Beach County Classroom Teachers Association (CTA) that will give an average 7% pay increase and one-time 3% bonus to instructional employees. The agreement was approved by the School Board during its Special Meeting on October 4, 2023. The significant raise demonstrates the District’s commitment to fairly compensating teachers for their hard work and dedication to students.

There is no possibility of the price of property tax going up to pay for this, according to the New York Times.

September 2023: Hollywood agrees on a new, higher-paying, contract with writers; “an 18 percent pay bump and a 26 percent increase in the base rate with which residual payments are calculated” (Washington Post)

October 2023: “On the most popular days, though, Disneyland is raising prices by more than 8% to $194. For a five-day ticket, Disneyland raised prices by nearly 16% to $480. The park also raised the price of various add-ons. Disneyland’s Genie+ product, which gives customers access to shorter lines, will now cost $30 a person, up by $5. For five-day tickets, the price for Park Hopper, which lets customers go between Disneyland and Disney California Adventure Park on the same day, also rose by 25% to $75. Disneyland also raised the price for parking and other products, including its Magic Key annual passes.” (Wall Street Journal)

Readers: What else have you seen that could be considered evidence for my discredited theory that a wage-price spiral could occur?

The good news: if your own income isn’t keeping up with inflation, you can save money by shopping at Costco. On a September 25, 2023 visit, they were offering a bottle of Champagne for $4,500, including a free glass.

State Farm says “A rule of thumb is to set aside 1%-4% of your home’s value for a home maintenance fund”. Aside from the fact that this is a huge range, it seems questionable. If a house is brand new, for example, it will be worth more but shouldn’t cost as much to maintain. Does “home’s value” include the land? If we want to use a percentage of “value” should we start with what it would cost to rebuild the house at today’s prices?

Also, I’m not sure that these formulae are valid for keeping a house in like-new condition. People in our part of Florida will either bulldoze a house after 20-30 years or do a major renovation ($100-200/ft), often back to the studs.

State Farm considers costs for the roof, HVAC, water heater, garage door opener, windows, and appliances. But this list isn’t complete and if you had all-new items in all of those categories your house could still be extremely shabby.

Our sojourn thus far in a 20-year-old house has taught me a lot about life limits. I recently learned about the thermal expansion tank attached to the water heater. This prevents excessive pressure from developing in a house’s water lines if the system is sealed off from the municipal water supply via a backflow preventer (see Supreme Court saddens the guys working at our house today). As soon as our backflow preventer was rebuilt, we began to notice that sometimes water pressure was initially high when opening a faucet. Our next-door neighbor is a senior engineer for a Detroit automaker and my go-to source for everything related to the house. He said that he’d had the same problem when his thermal expansion tank had failed internally. We looked at our water heater (installed 2020) and there was no tank at all! (Due to the failed backflow preventer, any excess pressure was previously absorbed by the city water supply.) The plumber who put a tank in said they cost $300 and last 2-5 years (they have a one-year warranty). So that’s an extra $75/year in maintenance reserve, perhaps.

If we consider furniture to be part of the house, and we want a house to look good, we need to budget for replacement of all furniture every 10 years (usually not cost-effective to reupholster). Online estimates of furniture cost are 10-50 percent of the house value. If we take the bottom end of this range for cheap-ish furniture and assume that the furniture costs 10 percent of the house value, that’s 1 percent of the house value every year as a furniture renovation budget.

Backyard pools here in Florida have a life expectancy of about 20 years (leaks can develop; tiles start to come apart). They cost about $25,000 to rehab every 20 years and the pump and heater can die sooner, so that’s probably $1,500 per year amortized.

You’ll want to paint inside and out every 5-10 years if you want the place to look sharp. That won’t be cheap!

People in nicer houses seem to do complete kitchen and bathroom renovations every 15-20 years. Those are $100,000+, so at least $7,000 per year if you want to avoid a period of shabbiness and people walking in saying “this kitchen could use a renovation”. (Of course, hardly any cooking is done in these dream kitchens, but somehow the cabinets and appliances still manage to fall apart over time!)

In order to remain competitive, hotel owners are required to do complete renovations periodically. Every room is rebuilt, refurnished, etc. Every wall is painted and every floor gets a new carpet, tile, or other flooring. If you want to live in a house that isn’t shabby, you need to do the same thing and I suspect that will cost more than 4% of the house value per year. But how much more?

Or I wonder if we could take the cost of a complete rebuild of the house and multiply that by 4 percent. Building a mediocre house in South Florida will cost about $1 million (about $350/foot for 2,500′ plus another $100,000 for the pool). The maintenance budget for a 2,500′ house is thus $40,000 per year.

Here’s what I came up with…

Cost

Expected life

Cost/year

State Farm items

tile roof

$60,000

30

$2,000

hvac

$20,000

12

$1,667

water heater

$1,500

10

$150

windows

$60,000

20

$3,000

furniture

$100,000

10

$10,000

swimming pool rehab

$25,000

20

$1,250

pool filters/heaters

$5,000

10

$500

$150/ft renovation

$375,000

20

$18,750

Annual total

$37,317

Note that the $150/ft renovation is intended to include the kitchen, bathrooms, and all appliances. It would also include flooring and paint. The total comes out pretty close to $40,000/year and there is nothing in the budget for mid-cycle painting, unexpected repairs, or unknown unknowns.

In other words, if someone got a 2 percent mortgage a couple of years ago, his/her/zir/their annual maintenance budget could well be larger than the mortgage, an unexpected result for many.

The typical homeowner, of course, won’t do the renovation every 20 years, so he/she/ze/they will spend less and also live in an increasingly decrepit house (or move!).

For calculating inflation, the BLS uses the fictitious “owners’ equivalent rent” (OEI). Home maintenance costs rise with the price of labor, which in turns rises with the cost of health insurance and, thus, at a higher rate than overall CPI. I wonder if inflation is understated partly because it assumes that Americans will live in ever-shabbier houses. The shabbiness wouldn’t be compensated for in OEI because owners aren’t likely to notice how crummy their house has become compared to a new house (boiling frog syndrome, another false premise of Science).

In other words, our houses cost us way more than we think, either explicitly in money if we do keep them up or implicitly in shabbiness if we don’t, and that might lead to inflation being understated (since we would have to spend a lot more to maintain our lifestyle).