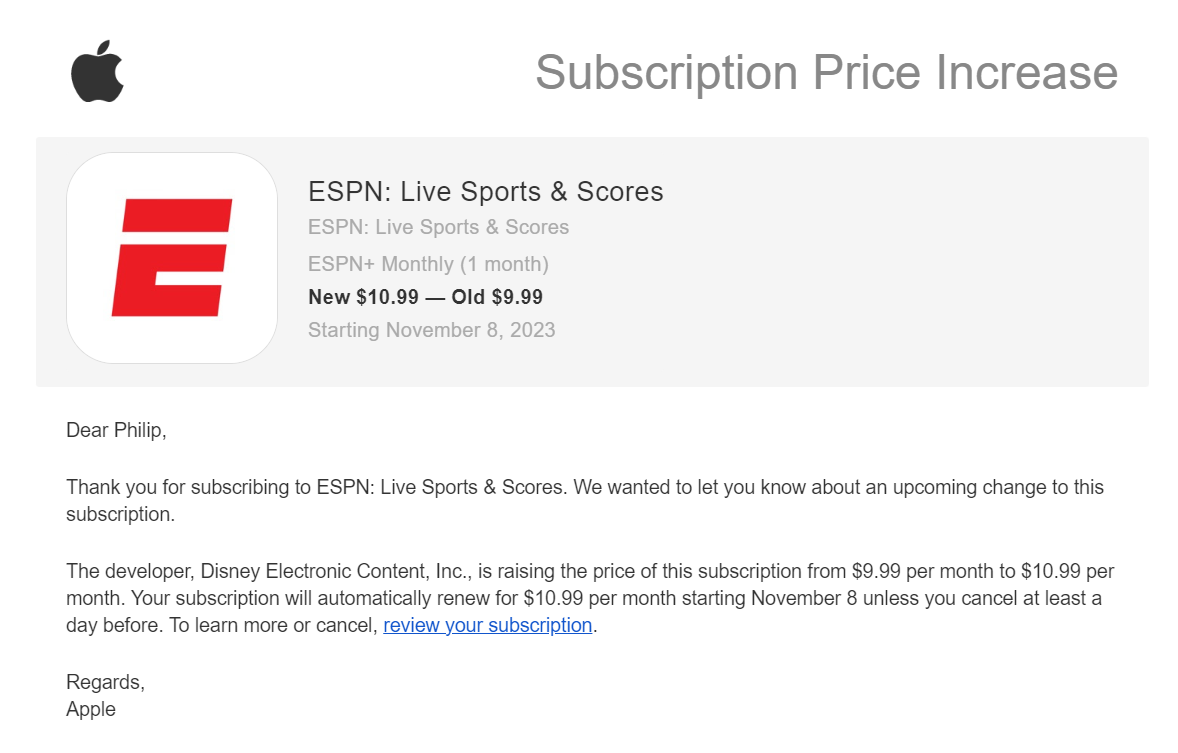

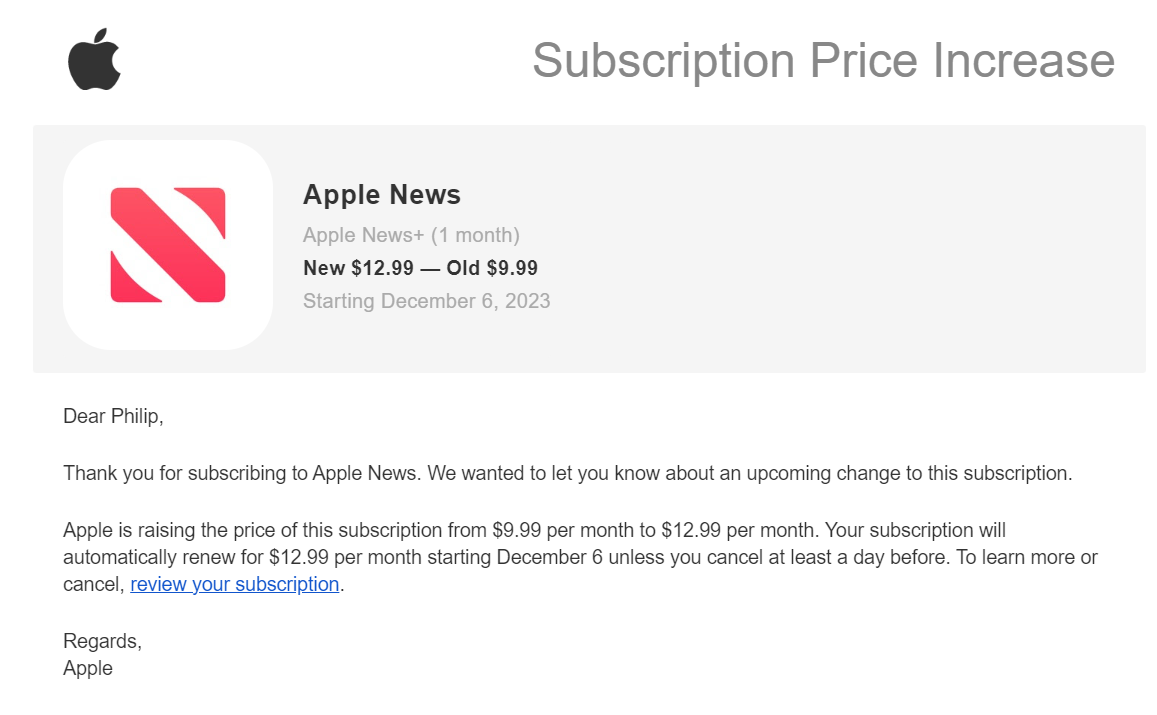

Apple News+ and 30 percent inflation

Today is my last day of Apple News+, the cost of which was recently raised by 30 percent:

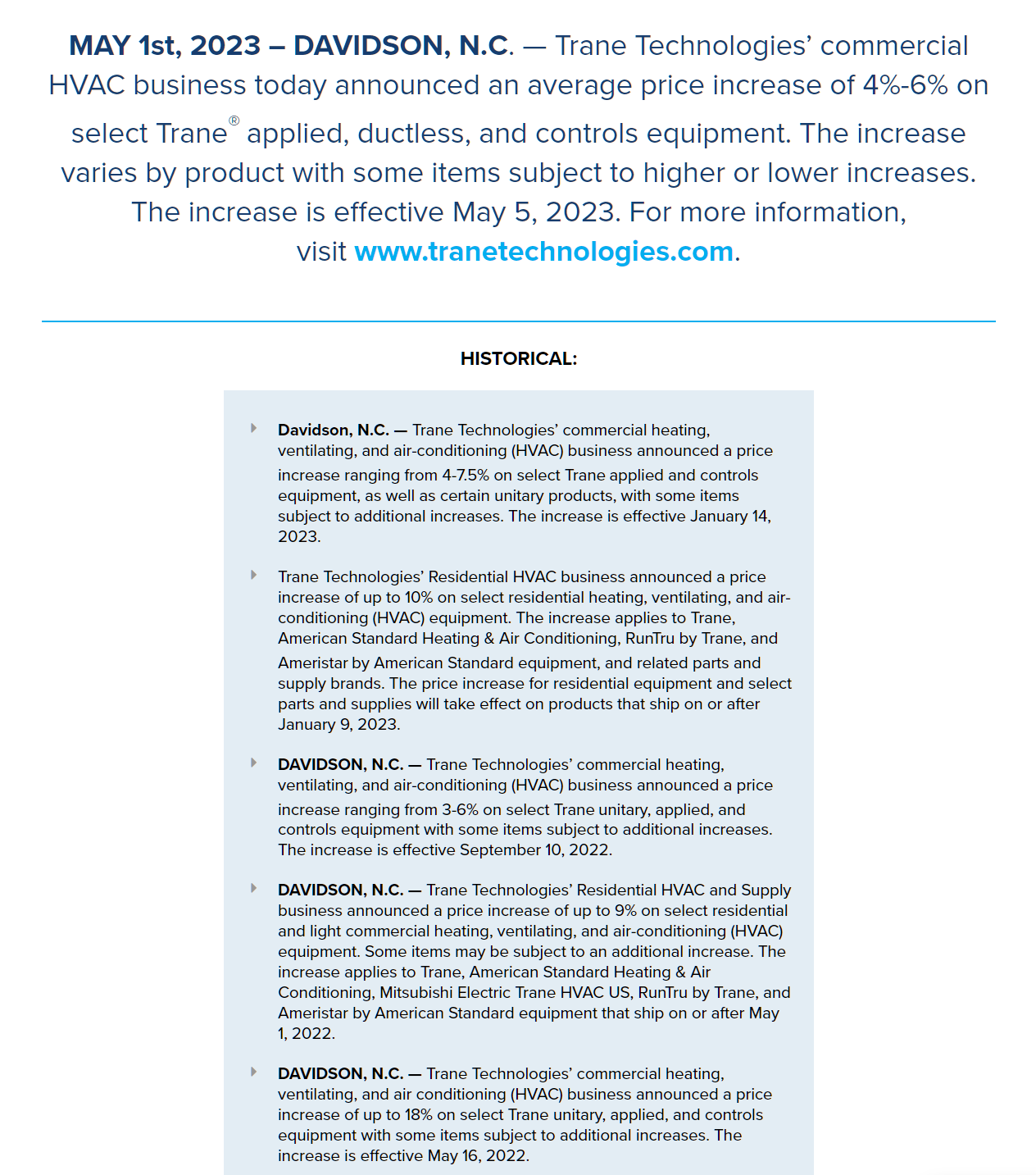

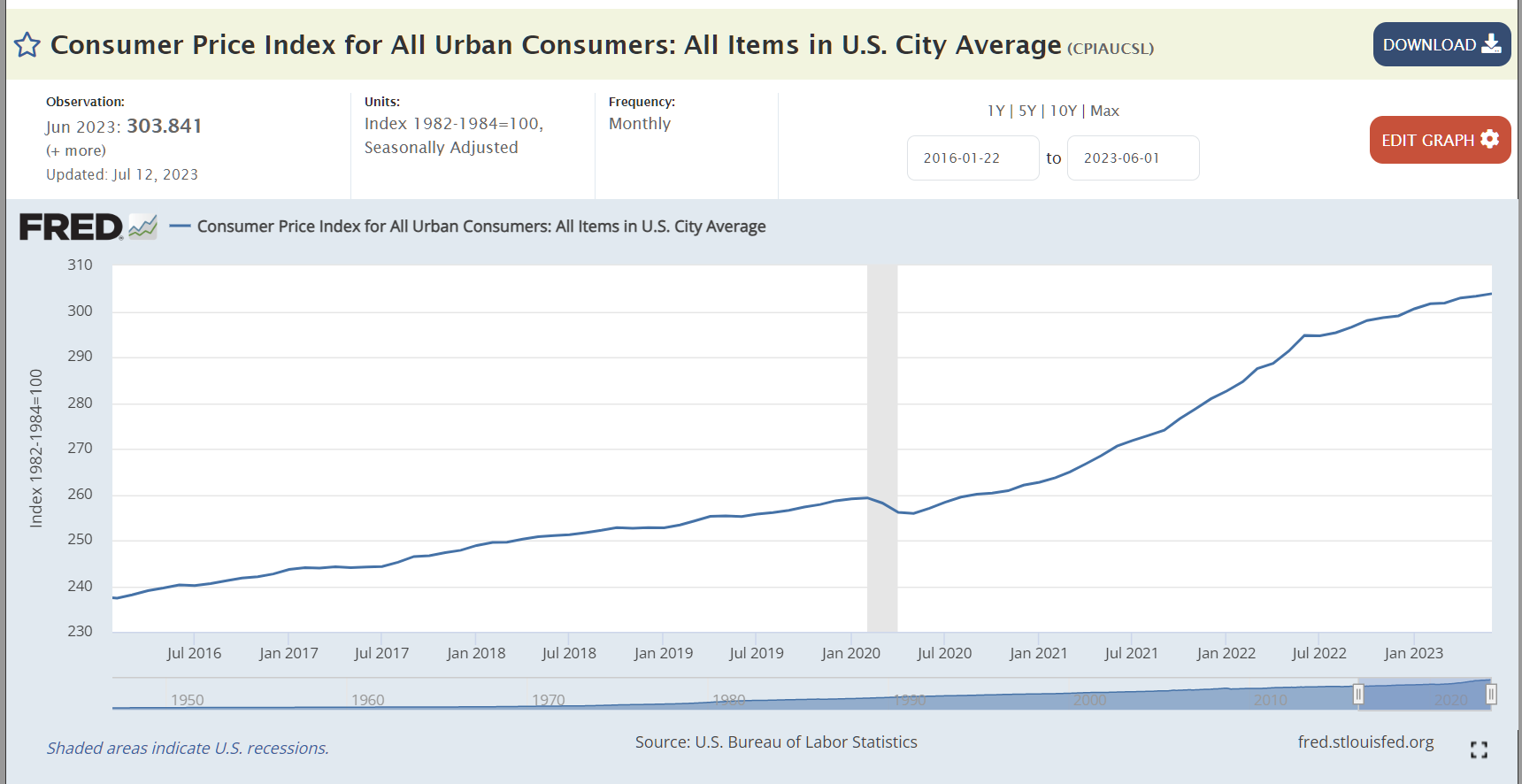

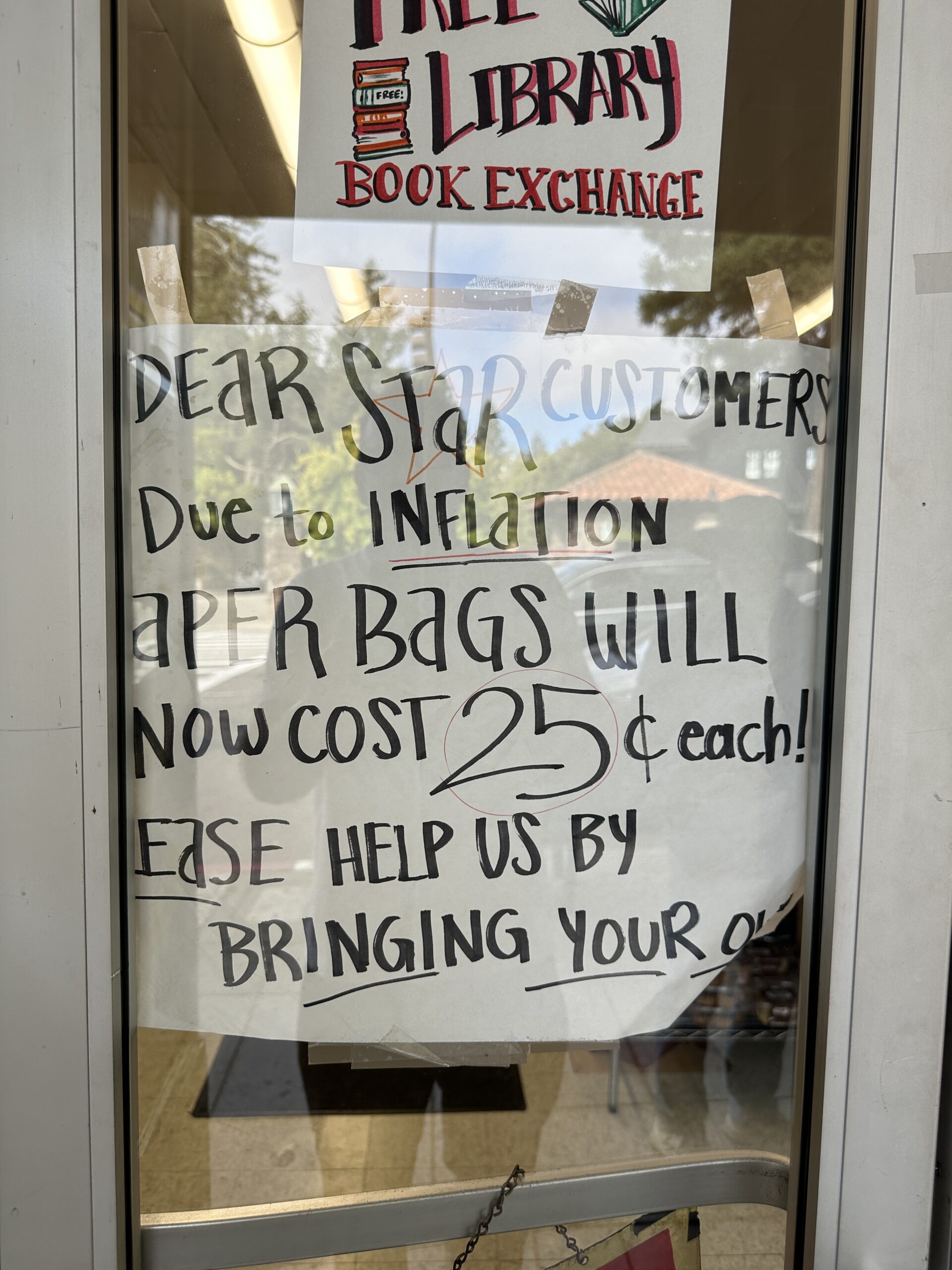

I’m not sure what justifies this increase. The major news organizations have mostly been harvesting outrage from Twitter, reposting information straight from the Islamic Resistance Movement (“Hamas”), reporting on what other news outlets are saying, etc. Couldn’t ChatGPT do most of this? If so, news subscriptions should be getting cheaper, not more expensive. Maybe the 30 percent bump is consistent with media costs in what the media assures us is a mostly inflation-free environment? The latest union contract at the New York Times raised salaries by only 12.5 percent (NYT, May 23, 2023):

The New York Times reached a deal on Tuesday for a new contract with the union representing the majority of its newsroom employees, ending more than two years of contentious negotiations that included a 24-hour strike.

The agreement, if ratified, will give union members immediate salary increases of up to 12.5 percent to cover the last two years and 2023, and will raise the required minimum salary to $65,000, up from about $37,500. The previous contract expired in March 2021, and union members have not received contractual raises since 2020.

Under the contract, the median salary for reporters in the union would be about $160,000.

(The above raises a question: Why weren’t the progressive owners of the NYT willing to pay a fair wage? Why did it take two years of contention and a strike before the NYT agreed to what the union asked? Also, note that median full-time workers in the U.S. earn about $58,000 per year (BLS) and that includes government workers with their higher-than-private-sector wages. So even the lowliest journalist at the NYT is above the level of Americans identified as the principal financial losers from low-skill immigration (Harvard study) and, of course, being a native English speaker is a huge advantage in the journalism marketplace.)

Speaking of labor unrest, the progressives who scribble for the Washington Post are striking tomorrow because the DC insiders who manage the paper won’t pay them what they’re worth:

The newspaper’s editorial section says that unions are the best thing that ever happened to a company or a country. Example from September 3, 2023, “At last, a Labor Day when workers can celebrate their power”:

Young Americans are the country’s most pro-union generation. Labor has poll ratings most politicians only dream about, and the Biden administration is making workers’ pay, benefits and rights its calling card.

Lest anyone doubt where the administration stands, the Treasury Department released what it proudly called a “First-of-Its-Kind Report” on the economic value of organized labor. It found that unions raise the wages of their members by 10 to 15 percent, have “spillover effects” that benefit nonunion workers, “reduce race and gender wage gaps” and “boost businesses’ productivity.”

All this adds up to a large cultural shift, said Heidi Shierholz, president of the pro-labor Economic Policy Institute. The fact that unions are in the news again means it’s more likely that those who feel they are being treated unfairly “see a possible path to help remedy what’s going on in their own job.” This contrasts with recent decades when “unions were not being talked about at all.”

On this Labor Day, from the president on down, that’s no longer a problem.

Why won’t the paper take its own advice and give the union what it asks for?

Full post, including comments