The wisdom of juries at the Elon Musk trial

A lot of folks, including journalists, love to concoct ex post facto explanations for why the stock market moved as it did on a particular day. The Elon Musk trial has introduced us to a guy who sounds a lot smarter than most pundits and financial reporters. “Jury Rules for Elon Musk and Tesla in Investor Lawsuit Over Tweets” (NYT):

The federal judge in the case, Edward M. Chen, had already ruled that “funding secured” and Mr. Musk’s second statement were untrue, and that Mr. Musk was reckless when posting them.

“I thought he was crazy to try his chances at trial, given the stakes involved,” said Adam C. Pritchard, a law professor at the University of Michigan, noting the judge’s pretrial rulings. “You’re fighting with one hand behind your back in that situation — and yet he won.”

If he had lost, Mr. Musk and Tesla might have had to pay billions of dollars in damages to investors who said they had lost money when the company’s stock surged after his statements on Twitter and then tumbled after his plan fizzled.

One male juror said their arguments were difficult to follow and sometimes seemed disorganized. “There was nothing there to give me an ‘aha’ moment,” he said, later adding, “Elon Musk is a guy who could sneeze and the stock market could react.”

Let’s check in with the superpundits to see how they did compared to this juror. Dow 36,000 was published in October 1999 when the DJIA was at 10,000. The D.C. insiders authors predicted that the DJIA would be at 36,000 no later than 2004. They were proved correct… in November 2021.

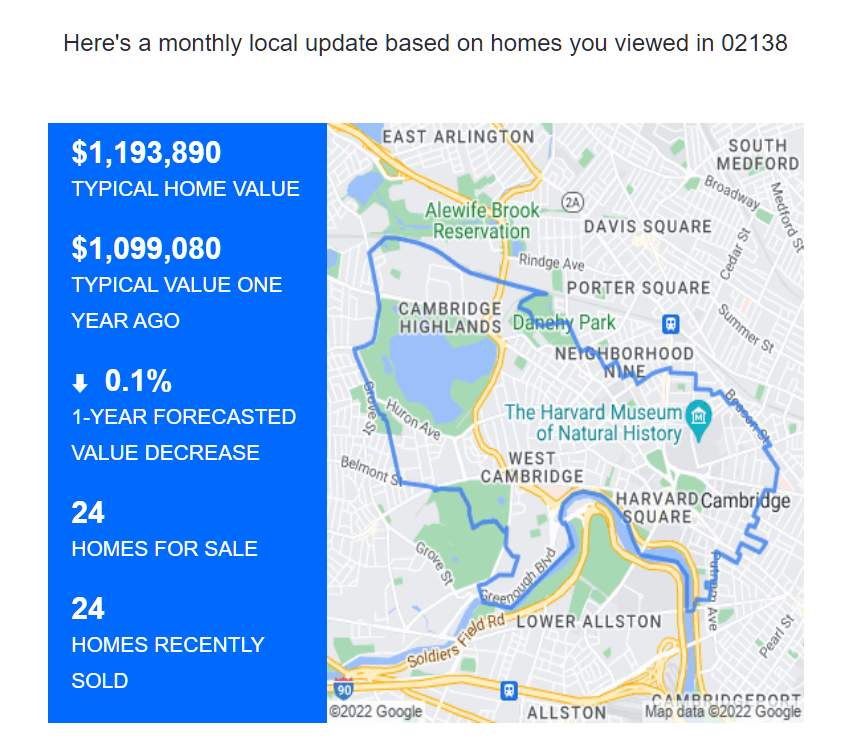

Of course, inflation makes every feel smarter. Despite the higher nominal value (3.4X what it was when Dow 36,000 was published), a basket of DJIA stocks has less purchasing power, in terms of real estate in any part of the U.S. where people actually want to live, than it did in 1999. Let’s check Zillow for some houses in our MacArthur Foundation-created development:

- overlooking a golf course: sold in February 2000 (before the dotcom crash) for $483,900 and now has an estimated value of $2.04 million (4.2X)

- a simple townhouse: sold in October 1999 for $192,900 and now estimated at $621,500 (3.2X)

Inflation has actually been far worse than the above examples suggest since, of course, these houses are now more 20 years old and aren’t in the pristine condition that they were when new.

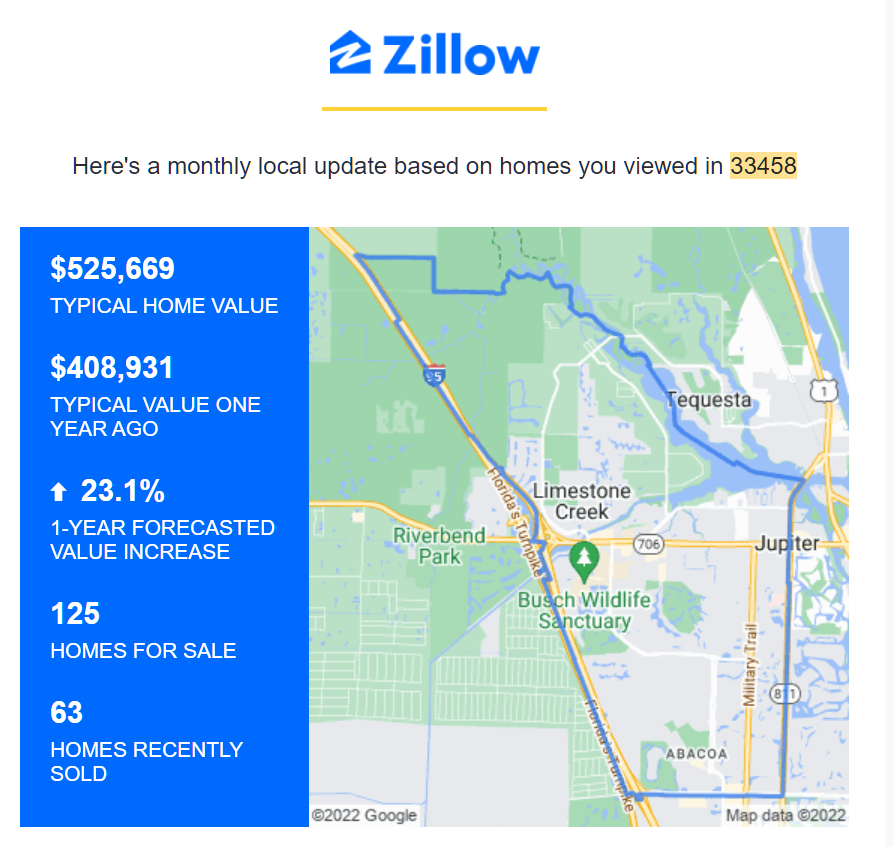

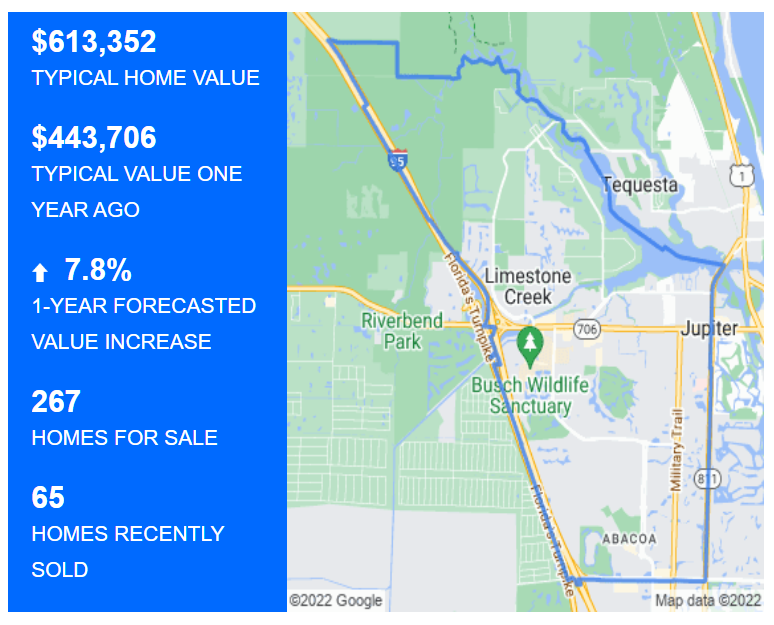

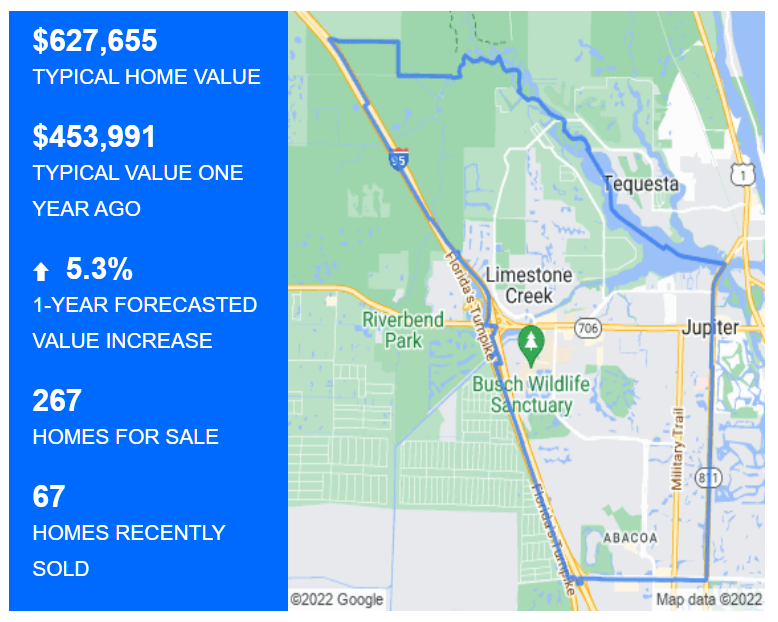

How about Jupiter Inlet Colony, where some migrants recently arrived?

- simple house from 1961: sold in 2005 for $850,000 and now estimated at $4.2 million (5X)

- house from 2000 with a dock: sold for $1.3 million in 2000 and now estimated at $9.6 million (7.4X)

(should be easy to find room for non-English-speaking migrants in the Jupiter Inlet Colony, described in this New York Post article!)

Let’s check in with the intersection of Efficient Market Hypothesis and coronapanic: