Who here has experienced Tesla Full Service Driving 13.2? A friend who is very tech-savvy and skeptical says that it was awesome on a couple of trips that he did in a sister’s car in Los Angeles. As a joke I asked a venture capitalist/Bitcoin bro friend in Miami when he’d be getting a Cybertruck and, of course, it turned out that he already had one. He says that FSD 13.2 does not work reliably in Miami and also that he isn’t surprised that it works great in Los Angeles: “The software works best in places where there are a lot of Teslas because it needs a huge amount of training data.”

If the goal of self-driving is to beat humans at their own incompetent game, what about a pole that can extend from the roof of the car up to a maximum of about 13′ in height as soon as the car is on the road? With cameras mounted at roof level and above, the self-driving car will be able to do what human drivers can’t, e.g., see over plants in the median (a Florida problem), over monster SUVs (a problem everywhere in the U.S.), etc. Waymo gets part of the way there with a non-extendable roof-mounted camera (photo from San Francisco with homeless encampment in background):

Why not take it up to 13′ when the situation calls for a bird’s eye view (“drone’s eye view”?)? (have a map of low-clearance areas, of course, and the pole won’t get stripped off the car by a bridge)

Aside from stupidity, what’s the problem with this idea? When the car is moving, the pole can’t be sufficiently stabilized to yield high-quality camera images? If so, the pole would still be useful when waiting to make a left turn and it is otherwise difficult to see oncoming traffic. NHTSA says that left turn accidents account for 22 percent of total accidents.

What to name this device? Tesla likes aviation analogies (“autopilot”) so how about “The Lindbergh”? Charles Lindbergh had a retractable periscope that enabled him to see forward during his famous NY-Paris flight in 1927. Or, if it is only practical to use when the car is stopped at an intersection… “The Selfie Stick”.

(Although often portrayed as an admirer of Nazi Germany, Lindbergh might have been pro-Israel, at least in concept (source). On the other hand, he lived until 1974 and even AI can’t find any statement by him regarding the modern state of Israel. Maybe he was too busy with his three secret girlfriends and seven secret European children? (Wikipedia) These additional kids should make Elon/Tesla like Lindbergh even more!)

Trey Parker and Matt Stone, the creators of South Park, grew up in Denver. When Casa Bonita, their favorite childhood restaurant, went bankrupt during the coronapanic lockdowns, they bought it and spent a rumored $40 million restoring it to its former glory. It’s tough to get a reservation so book as soon as you think you might be going to Denver!

Your visit to Mexico begins in a downscale strip mall (Dollar Tree) in Lakewood, a downscale part of the Denver metro area:

There are a variety of theme park-style environments that have been created inside. Here’s a village that houses the restaurant’s museum, for example:

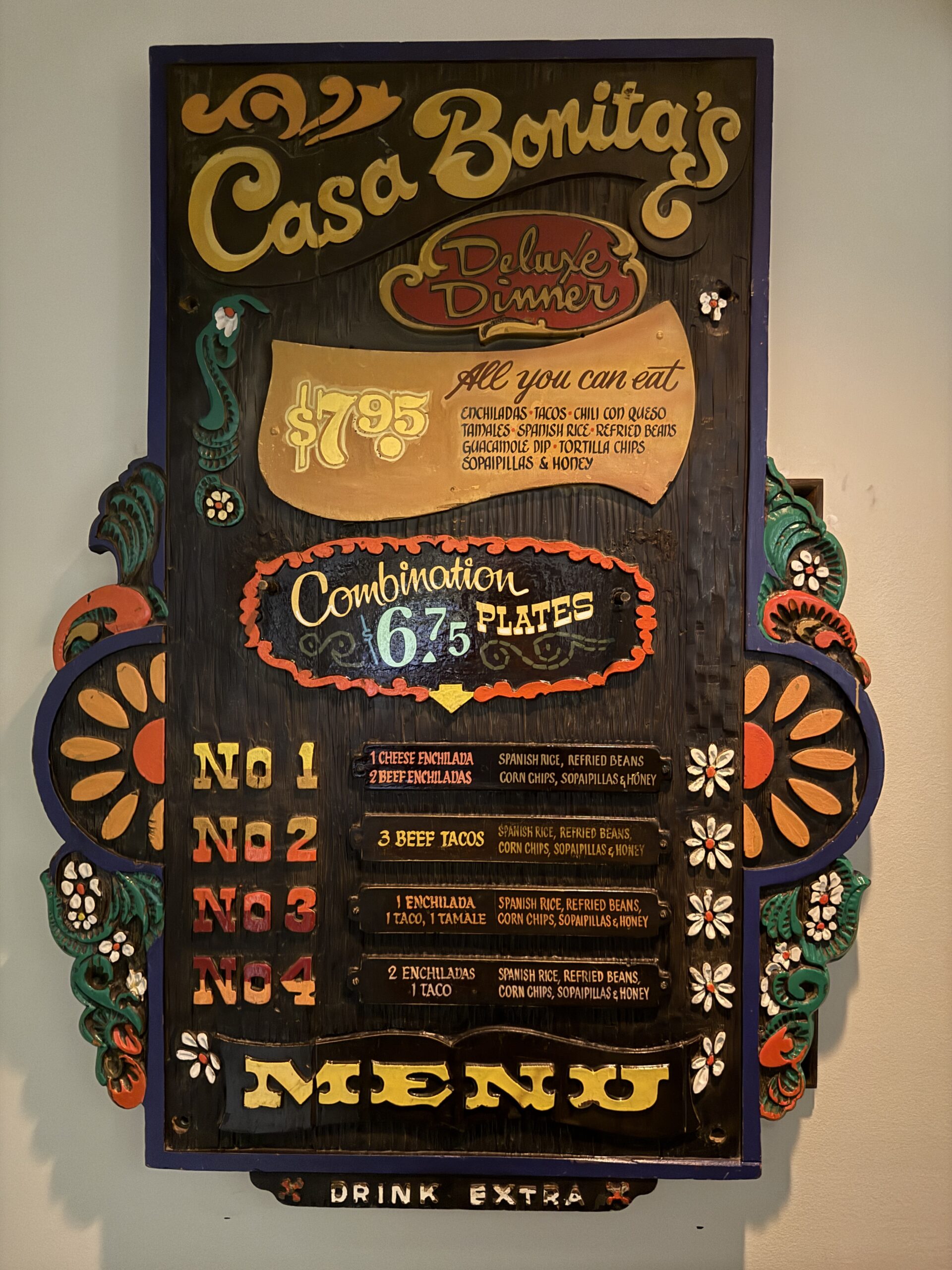

You eat first and then wander. The $6.75 combination plate offered below is a pre-Biden price. Today it is $30 at lunch or $40 at dinner for one of about 9 choices. You won’t be introduced to the subtleties of regional Mexican cuisine, which has resulted in some people complaining about the price, but it does include soft drinks, dessert, and a 15 percent tip. It wouldn’t be easy to get out of Five Guys for much less.

After the meal, one can take in the Acapulco diving show:

They also have live musicians in various locations, a puppet show, a magic show, free face painting, balloon sculptures, etc. It would be easy to spend another 1.5 hours after the meal here. My one complain is that the arcade doesn’t include a South Park pinball machine (2,200 were made; Sega is a predecessor to Stern so the South Park guys could probably persuade Stern to do an updated version).

A few photos:

There are cave and mine sections for dining, but the premium seats are around the cliff diving lagoon:

Inside the cave…

It’s an experience, for sure, and I’m grateful to the South Park guys for preserving and revitalizing it. I wish that more restaurants were like this, but the cost of paying live performers is just going to go higher as health care costs inflate.

I wonder if anyone told the happy couples in the article that “have children” is a process that, with the best current technology, can be rushed only to a certain extent.

Here’s a choice portion of the article:

They are one of many gay couples in recent weeks who are rushing to get married, start fertility treatments and take other measures out of fear that some of their rights might be rescinded during a second Trump administration.

The Party of Science believes that there is an effective “fertility treatment” for when Ben and Adam are trying to have a baby together?

The news out of Los Angeles isn’t great lately. Here’s a photo of Pacific Palisades:

It looks as though some concrete structures are still standing.

My engineering/planning question for today: Why aren’t all houses in fire-prone parts of California made from concrete? In Florida, after wooden houses didn’t come through hurricanes in good shape people decided to pay an extra 10 percent during construction and build from concrete.

Maybe my assumption that a concrete house is mostly invulnerable to fire is wrong? It’s tough for me to imagine, though, a fire so intense that it would melt concrete and take out a roof supported by concrete or steel beams, especially if the houses themselves weren’t combustible what would be feeding a fire in a neighborhood like the one shown above?

Wooden houses are obviously easier to engineer to withstand earthquakes, but concrete structures can be made just as earthquake-proof, I thought.

As it happens, I’m in Berkeley, California right now. Here’s how the smartest Californians protect themselves against a risk even bigger than fire (University of California, Berkeley Faculty Club):

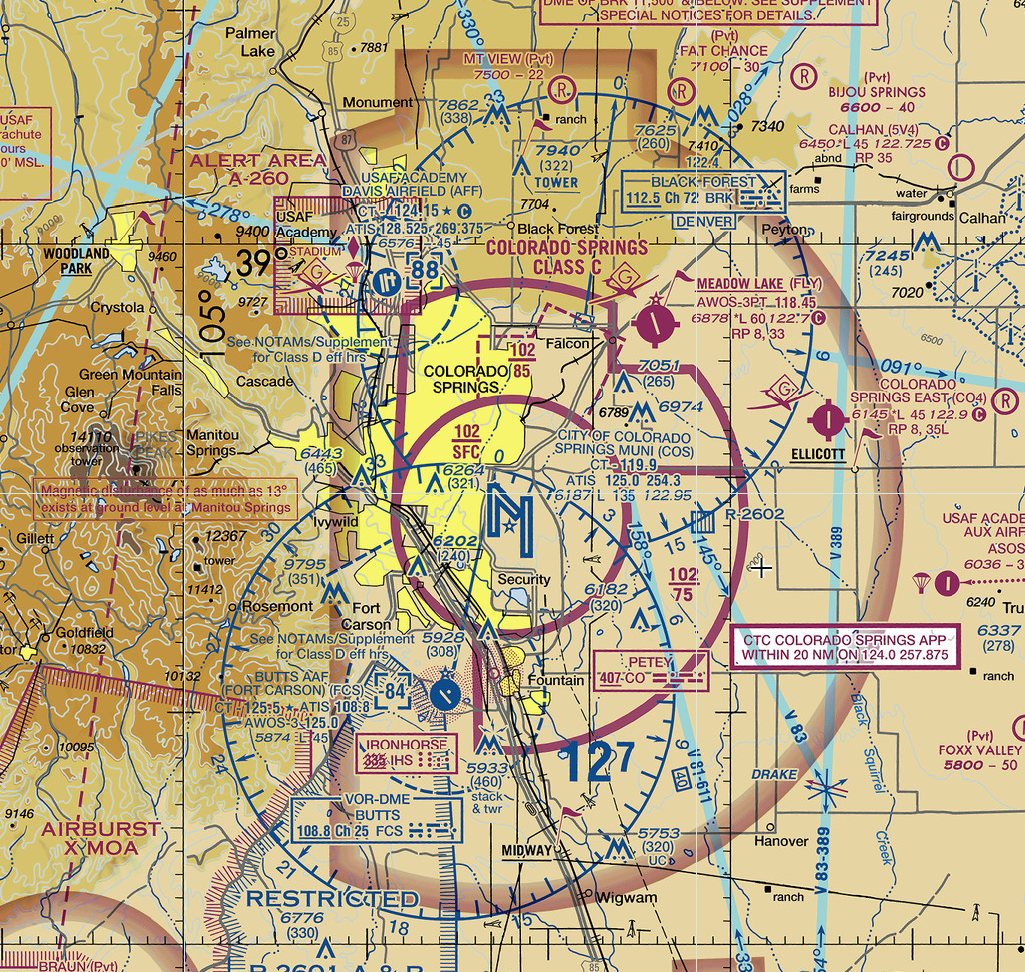

I made it to the USAF Academy in Colorado Springs last month. It’s home to just over 4,000 students, hardly any of whom learn to fly while there. The school has about 20 Cirrus SR2x piston-powered aircraft and some gliders. This fleet enables the typical cadet to take between 4 and 14 flights during the four-year program. The good news is that the academy has its own airport: KAFF. The bad news from the chart is a 4500′ runway 6576′ above sea level. A Cirrus SR20 with two average American guys on board and two hours of fuel would be lucky to clear a crush-proof cigarette package after a 4500′ ground roll in the summer (note that the big airport there has a 13,500′ lighted runway (“L 135”).

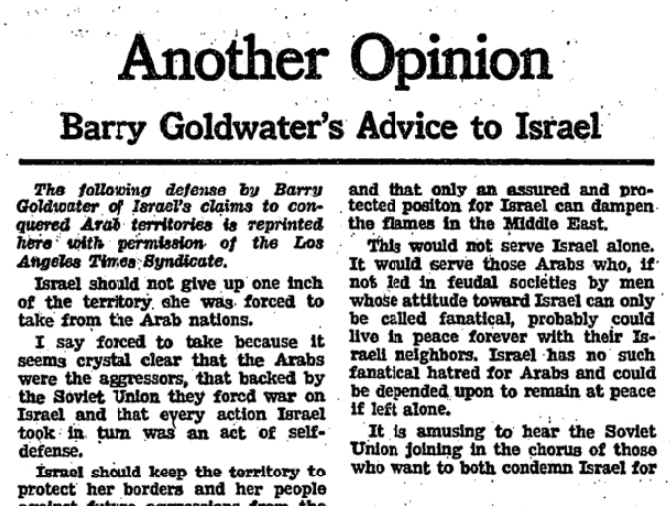

They’re building a new visitor center, but it isn’t ready yet. The old visitor center is named for Barry Goldwater, best known for losing the 1964 Presidential election to Lyndon Johnson. Goldwater was also, however, a pilot for the U.S. in World War II and, as a senator, promoted the idea of the Air Force Academy for the then-new standalone branch of the military, from which he retired as a Reserves Major General. (af.mil bio)

(Just for fun, let’s compare Goldwater’s politics to today’s United States. Goldwater wanted people of different skin colors to be treated equally; today’s Air Force Academy, like the U.S. Naval Academy, has a race-based admissions system (NYT). Goldwater objected to Eisenhower’s $72 billion budget for being too large; today’s federal budget is approximately $7 trillion per year, 100X that objectionable number. Goldwater suggested, in a July 2, 1967 NYT opinion piece (below), that Israel keep all of the land it had conquered in the six days of fighting in June 1967; half of Americans today are marching with the Queers for Palestine. Goldwater’s name will be expunged from the new visitor center in favor of a former academy director’s.)

The visitor center contains a somber reminder that sometimes the enemy wins or training flights don’t go as planned. Each white rectangle below represents a graduate whose life was lost while serving in the Air Force:

Bizarrely, in a world where my friends’ kids can’t get in anywhere, only about half of the cadets were in the top 10 percent of their high school class:

The Academy discriminates against those who are married and those who are over 23 (both would be illegal for a private college? certainly for an employer, right?):

Cadets are protected from streaming and other distractions by not being able to own any distractions:

In the gift shop, Nike’s logo appears right next to one of America’s most savage weapons, the AC-130. Nike is fully committed to diversity, equity, and inclusion (nike.com) and also happy when diverse people are equitable massacred by 105mm shells and 25mm Gatling gun rounds from an unseen aerial foe.

The cadets had all gone home for the winter break (at least 3 weeks) and the famous chapel was being renovated, but the Academy offers a planetarium show to visitors and one can walk around statutes of various USAF greats.

Here’s Hap Arnold, who commanded the WWII predecessor to the USAF. He was a huge enthusiast for strategic bombing of Germany and Japan and is quoted in The Man from the Future: The Visionary Ideas of John von Neumann as saying that he wished he had vastly more destructive bombs to drop on the Germans and Japanese (which, of course, he eventually did get, partially thanks to von Neumann).

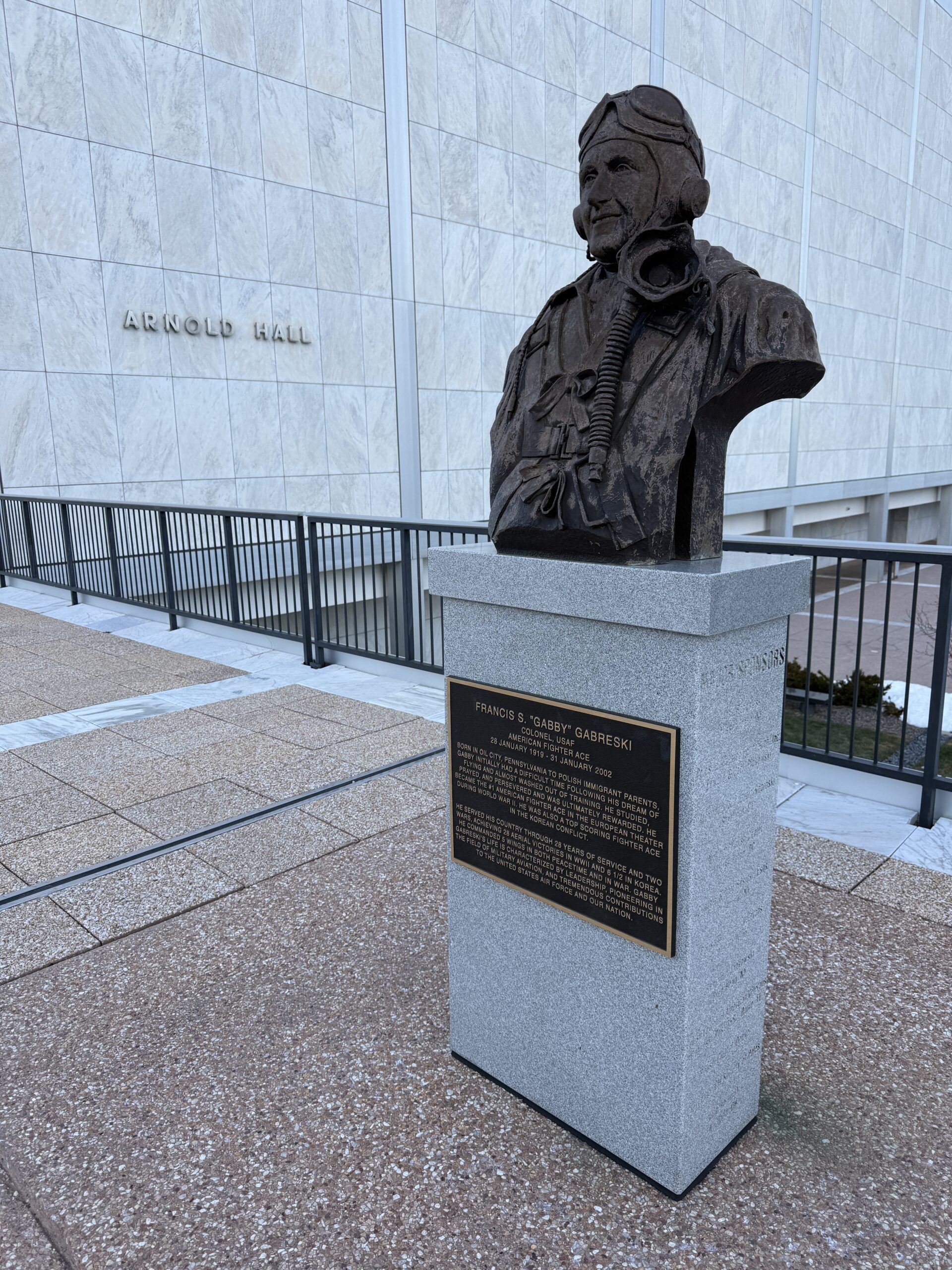

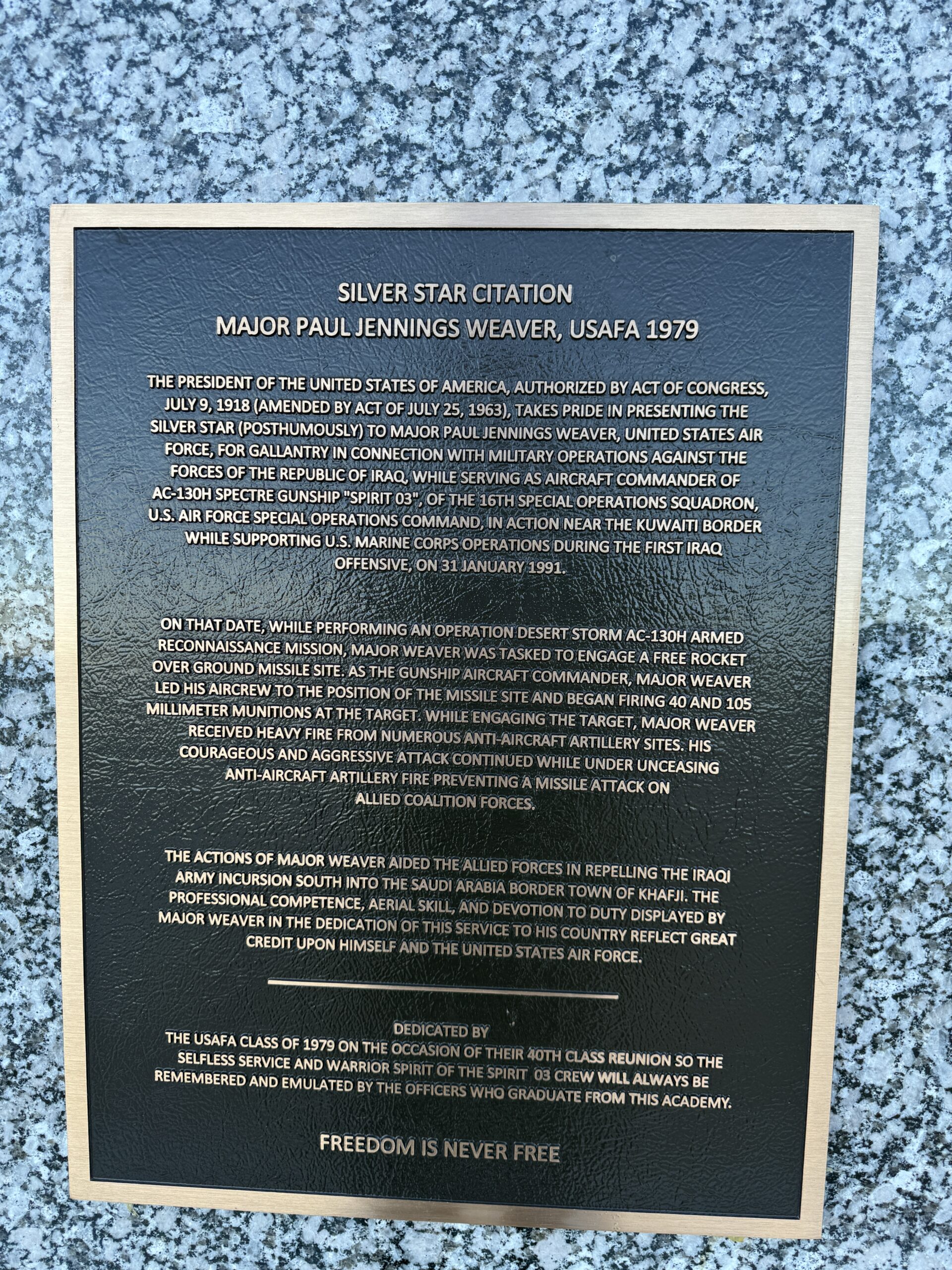

Gabby Gabreski, who fought in combat during both WWII and the Korean War, and Paul Jennings Weaver, who was killed in Iraq War I while flying an AC-130, are examples of commemorated men:

Women get an award for showing up and ferrying aircraft around the Continental U.S.

On the drive back toward Colorado Springs there is an overlook for the the Academy’s airport with some signs explaining the flying and parachuting programs:

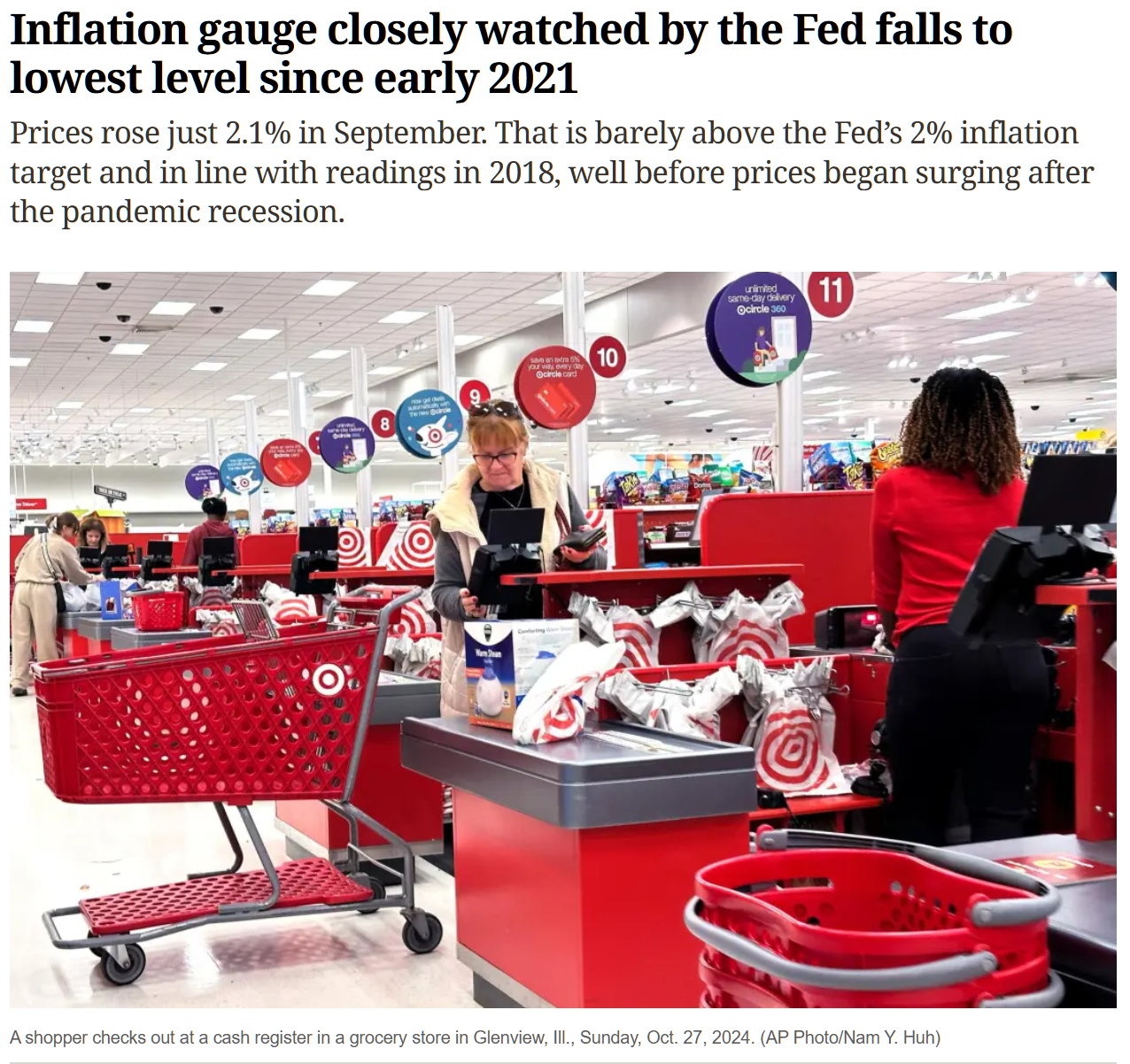

Inflation is whipped, except that the most significant cost for a typical person remains unaffordable (the “housing affordability crisis”), with government intervention required. The latest affordability crisis (i.e., Americans not being rich enough to afford what used to be considered American life) is for cars (San Jose Mercury News):

The good news is that expert assistance has arrived:

Bay Area residents wanting — or needing — to buy a car are steering this winter into what experts call an affordability crisis.

“The price of new cars, in general, has become alarming for a lot of people,” said Brian Moody, executive editor of Autotrader.com.

Nationwide, the average monthly payment for a new vehicle in November was $753, up more than 30% from just five years ago, said Jessica Caldwell, a head analyst at Edmunds, which tracks the auto industry.

Adding to buyers’ woes is the high price of most everything else. A recent Edmunds study found 54% of people surveyed who were planning to buy a new or used car in the next year said they would have to work extra hours or take a side job to afford it. “This wasn’t an issue 10 years ago,” Caldwell said.

Prior to the November 5, 2024 election, the same newspaper said that inflation was finished. October 31, 2024:

After shrinking during the pandemic and then stagnating for several years, California’s population is finally growing — thanks to immigration from abroad.

Native-born Californians are moving out (“Net domestic migration”) and foreign-born immigrants are moving in, which is further evidence that the Great Replacement conspiracy theory is false.

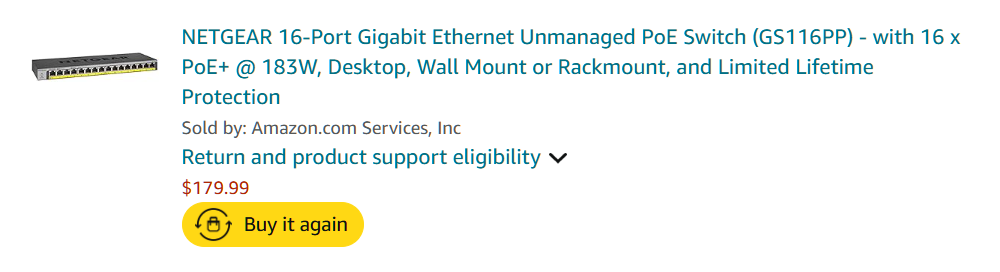

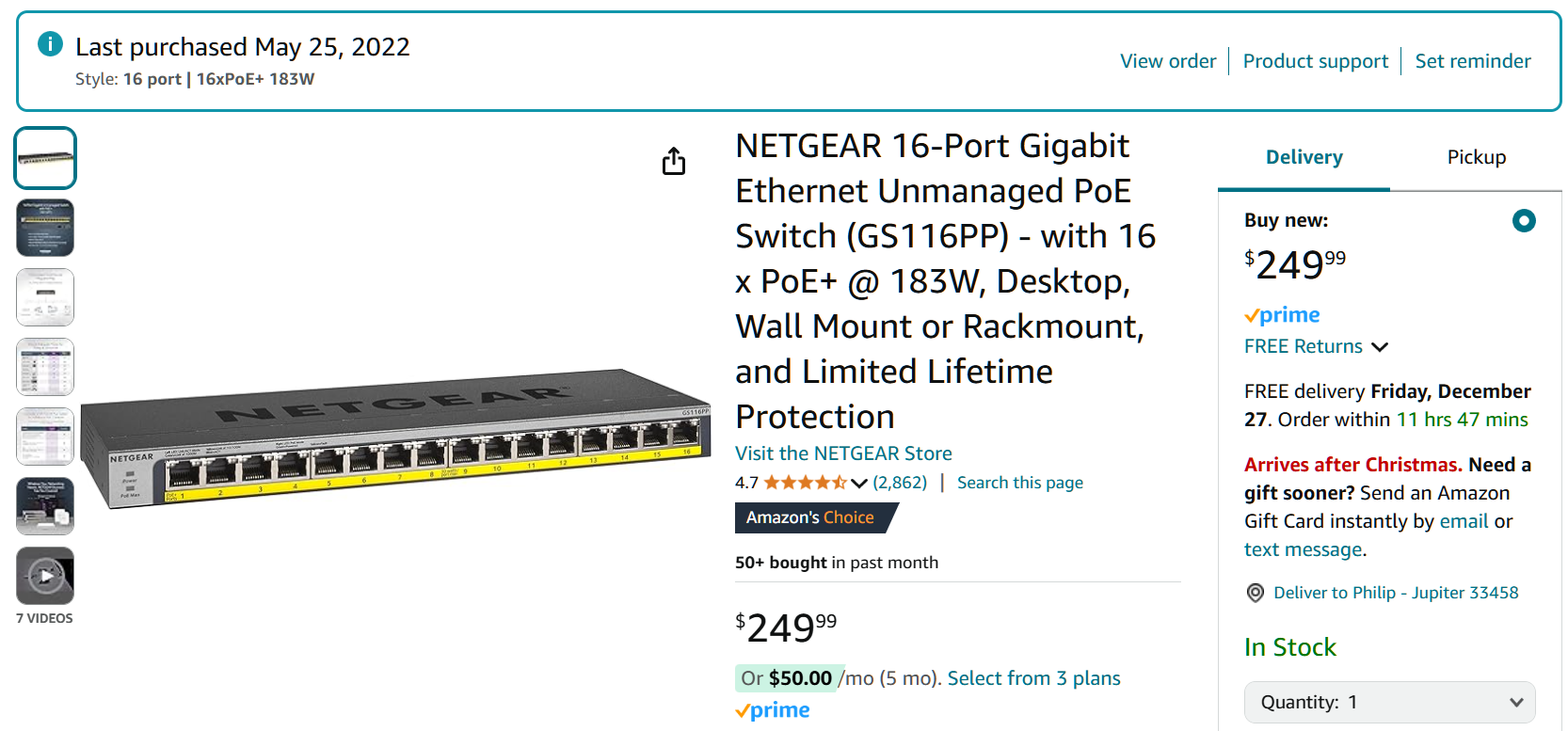

I was in a conversation with some friends, one of whom is a UniFi zealot, and wanted to check the power output compared to a feeble UniFi switch. I learned that the exact same Netgear switch was still available from the same retailer in December 2024… for $250:

That’s 39 percent inflation over 2.5 years in our otherwise inflation-free economy.

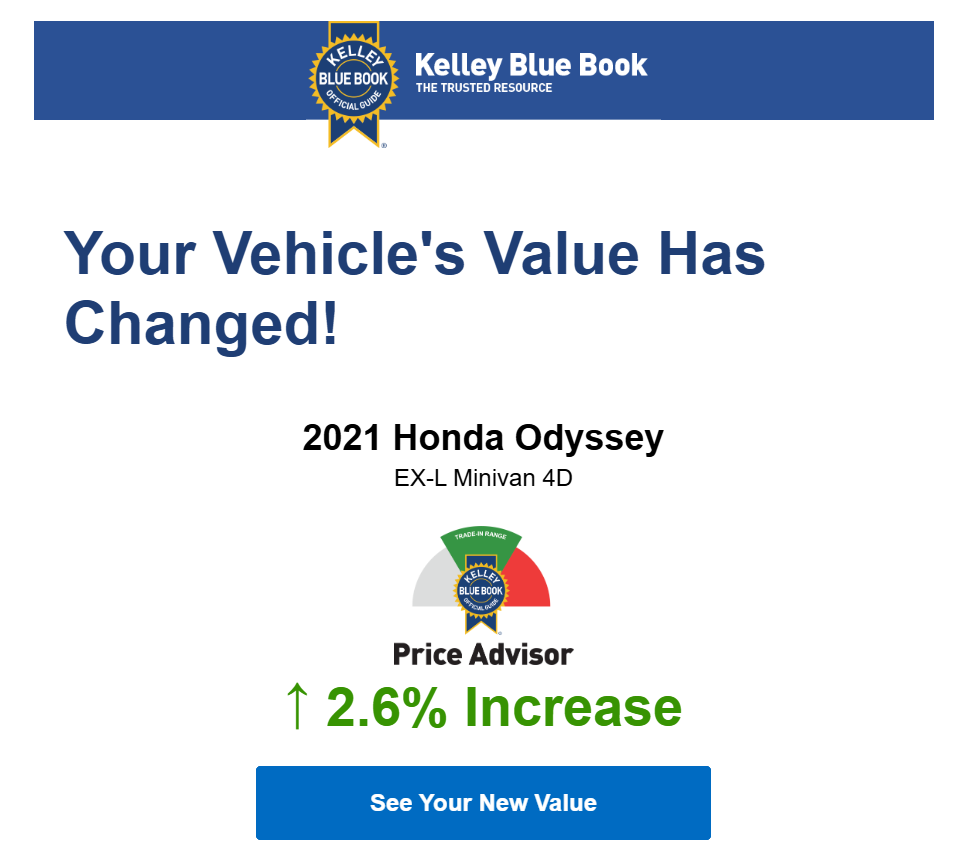

How’s our four-year-old minivan doing as a collector’s item? KBB emailed a week ago to say that it was still going up in value.

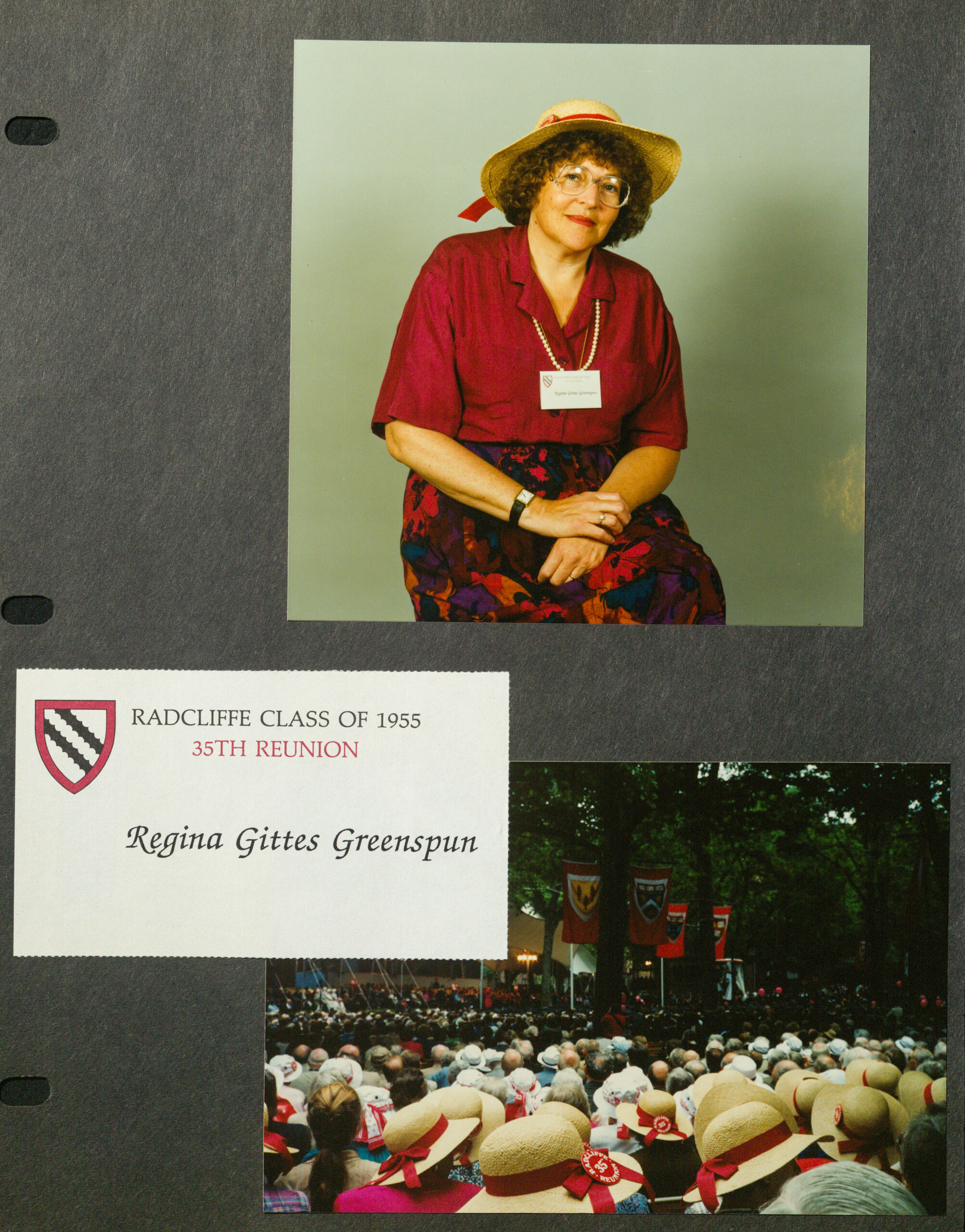

Regina Greenspun died at age 90 on January 6, 2025 at her home in Abacoa, Jupiter, Florida. My father wrote most of his own obituary, but my mother didn’t leave any guidance so this post should be considered as one person’s memory of Regina augmented by what was found in some recently scanned photo albums and other documents…

Regina moved to Florida in February 2024 and enjoyed spending at least 4 afternoons and dinners per week with her grandchildren until Thanksgiving 2024, at which point she developed pneumonia and began a steep decline from an already fragile state that included lymphedema and stage 4 chronic kidney disease.

Regina was born in Melrose, Massachusetts. Her father Nick, who owned a hardware store with his brothers that had been started by his father, liked to say that Marjorie (younger sister) was the prettiest girl in Melrose High School and Regina was the smartest. She was Class of 1955 at Radcliffe College, became a leader of Harvard Hillel, and remained involved for the rest of her life with Harvard and Radcliffe alumni events and the friendships she had formed at Harvard. In fact, she had a five-hour meeting with Harriett Eckstein (widow of Otto) on November 8, 2024 where the two of them reminisced about people they’d known at Radcliffe, shared their fears of the bad things that would happen after Donald Trump returned to the White House, and kept remarkably silent on their respective health challenges (stoicism was one of Regina’s core characteristics; she almost never described any medical issue or plan to see a doctor). She was also regularly in touch by phone with friends from her old neighborhood in Bethesda, Maryland.

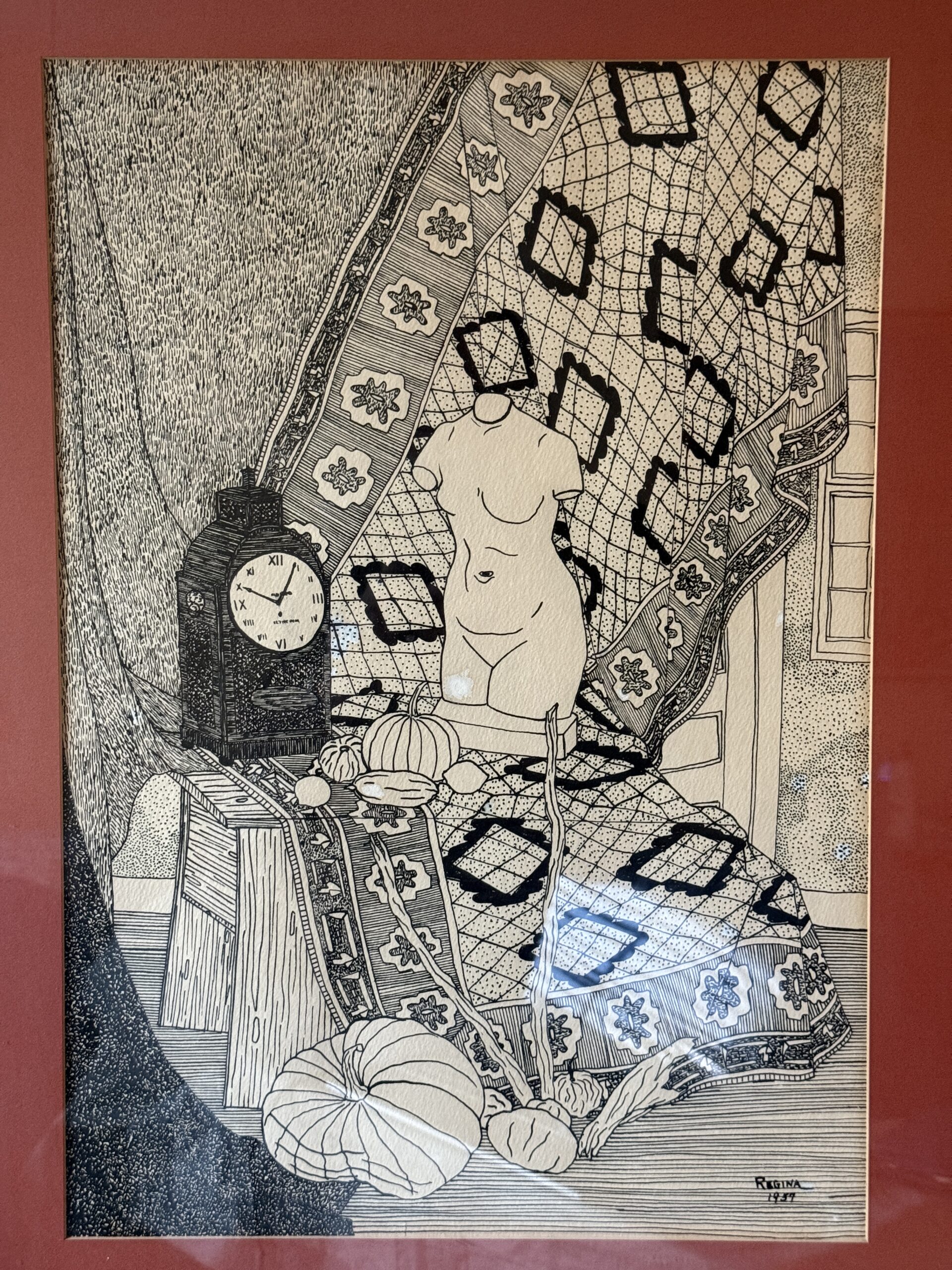

Regina earned both bachelor’s and master’s degrees from Harvard/Radcliffe in Art History (bachelor’s thesis from 1955: The Synagogue and Its Architecture) and was an accomplished artist herself, well-trained in the fundamentals of classical drawing. One of her teachers was Lux Feininger and she kept in contact with him for decades after she graduated Harvard. Here’s an example of Regina’s student work (1957):

When her husband Nathaniel (married 1956; Nathaniel died in 2021) got a job in Washington, D.C., Regina moved there with him and became an art teacher in the D.C. Public School system. She suspended her career while we three kids (born 1961-65) were young, except for teaching on weekends at Washington Hebrew Congregation (a Reform temple), then resumed part-time work as an art consultant. She might, for example, help a law firm acquire 200 paintings and lithographs to decorate a new office. She also trained to become a tutor to dyslexic teenagers.

Regina patiently tried to teach us art skills and organized projects in various media, including baking enamel in the toaster oven and building sculpture from telephone wire (at least 50 different color combinations available in those glorious analog days). My standard line: “We were denied coloring books because they would stunt our creativity and were jealous of our cousin Doug who got as many coloring books as he wanted. Because of this training, discipline, and emphasis on creativity, I became a computer programmer while Doug became a Disney animator.”

Unlike today’s helicopter/snowplow moms, most of Regina’s hours were spent pursuing her own interests. We organized our own breakfast (unsweetened cereals, unlike the delicious commercial concoctions our lucky cousins got), got on the school bus, and grabbed our own after-school snack. Regina read 3-5 library books per week, got together with friends, and went to some weekday theater matinees with neighborhood moms. She’d cook dinner most nights and then our dad or a kid would do the cleanup. This was a transitional time for feminism in which upper-middle-class women did not work, had domestic help, could buy whatever they wanted on then-newish credit cards, and used some of their 100+ hours/week of leisure time to note as an uncontestable fact that they were oppressed by men. Despite the loss of certainty regarding gender roles that evolved during their marriage, my parents seldom argued. Nathaniel loved and treasured Regina until his death in 2021 and used to say that the happiest period of his life was after we three kids had moved out of the house because then he was able to have Regina to himself.

Our parents had an active social life. We tortured babysitters on at least 2 nights per week while our parents attended theater, concerts, and dinner parties at friends’ houses. They hosted dinner parties themselves at least once or twice a month. This was the 1970s so we were allowed to drink as much alcohol as we wanted at these events, usually preparing a weak bourbon and ginger ale. (Despite the unlimited booze available to us as kids, none of us turned into regular drinkers as adults.)

“I canceled out your father’s vote,” Regina would tell us proudly after every election. Our dad, who worked as a federal government economist, was a “Gerald Ford Republican” who cheered the deregulation efforts, such as for the airlines, initiated by President Ford and agreed about the importance of a balanced budget. Regina was more interested in local politics, especially the school board, and generally supported any proposal put forward by mainstream Democrats. She had no concerns about enlarging the size and role of government because she believed that Americans were uniquely positioned to innovate and produce, much as we had been in circa 1950 when she came of age. Productive Americans could never sink under the weight of the welfare state created by FDR and Lyndon Johnson because the next innovative world-dominating U.S. company would come along to pay for it. Given the recent decades of runaway growth in the U.S. stock market compared to foreign stocks, I think we have to rate her #MostlyRight as an international trade and macroeconomist.

(One of the school board issues in my day was around “Man: A Course of Study” in which we were taught that Eskimos leave behind old people who can’t keep up with migrations among hunting grounds. Some conservatives wanted Montgomery County (Maryland) to remove these materials, which they said taught children to abandon elderly parents. Regina was one of the progressives who wanted it, and similar classes, retained. If memory serves, the progressives won. Of course, the adults talked about this material far more than we 6th graders ever did!)

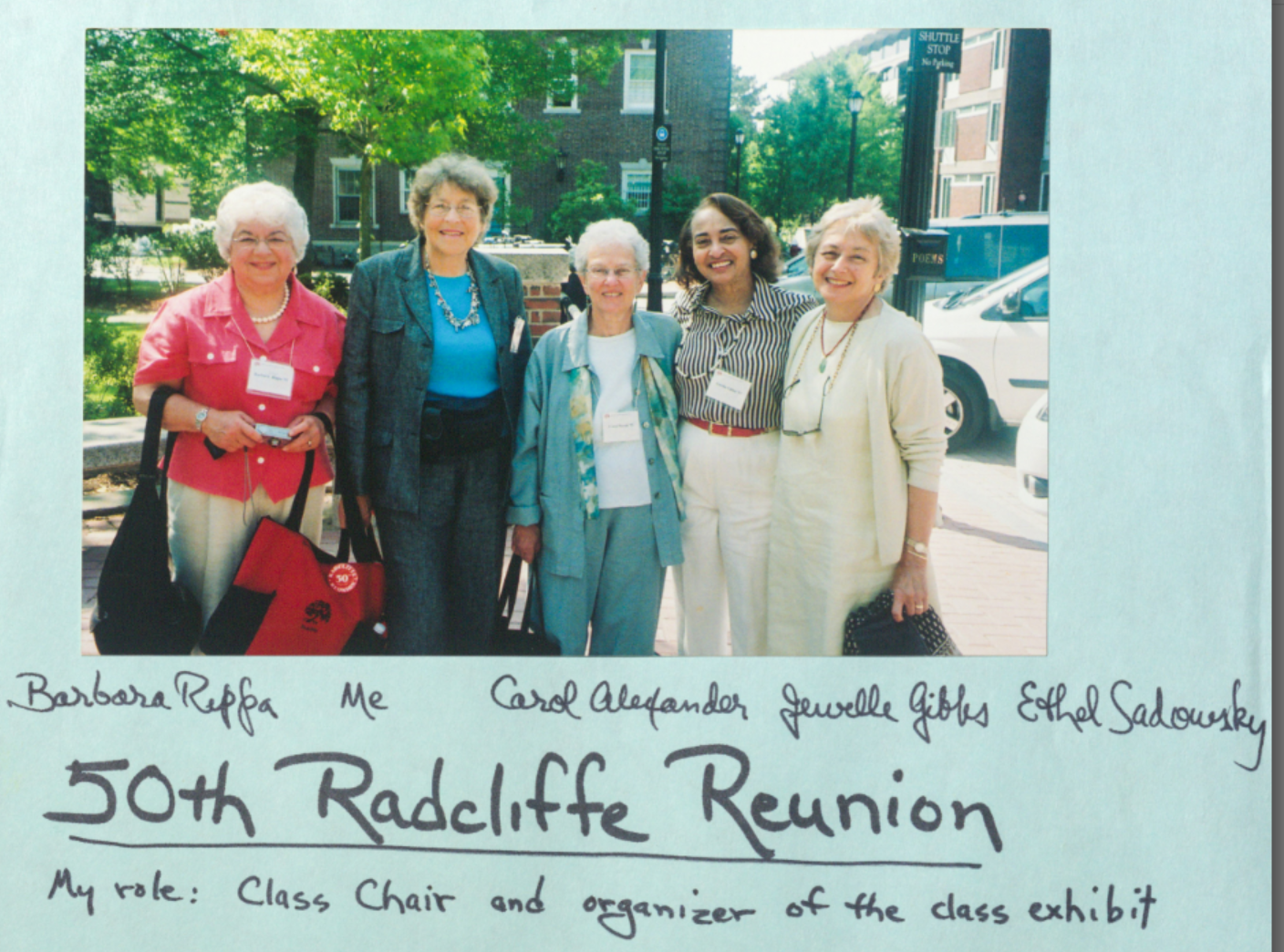

Regina traveled extensively around the U.S. and to Europe with her husband. With friends and relatives, she also went on organized tours to Asia and Africa that Nathaniel considered too adventurous. Regina loved to socialize and organized a move to the Maplewood Park Place senior community in Bethesda, Maryland in 2012 where she was a tireless organizer of committees and events, especially those having to do with art. There were some health scares beginning in 2018 that led us to fear the worst was at hand, but each scare was followed by a remarkable reboot, e.g., via pacemaker (thanks to Dr. Helen Barold for these extra years). Unfortunately, she began to experience episodes of confusion that worsened in January 2024, which resulted in the staff at Maplewood concluding that she could no longer stay in her “independent living” apartment. She lived briefly with us here in Abacoa, but decided that she preferred the “senior dorm” experience and moved to assisted living at Addington Place of Jupiter, a 15-minute walk away. She was delighted to be surrounded by her art collection and old furniture, but never got used to the 70-inch TV that I picked up for her at Costco (“why does the TV have to be so big?”). She eagerly participated in all of the organized activities, including trips to art galleries, museums, and even the Hard Rock Casino down in Hollywood, Florida.

Regina put a lot of energy into the grandmother role. She was fortunate to have my sister and brother, with their respective children, living close by for several decades, and loved family get-togethers. She and Nathaniel also took several grandchildren on individual trips, e.g., to National Parks out West or down to Florida. Despite my late start on having children (“if you think teenage parenting is bad it’s only because you haven’t seen old people with kids”), Regina made the effort to travel up to Boston while she was still able.

Regina is survived by 3 children, 11 grandchildren, and 3 great-grandchildren. A memorial service will be held at a future date at the Garden of Remembrance in Clarksburg, Maryland.

This is from the 1963 book, which means the baby might be me:

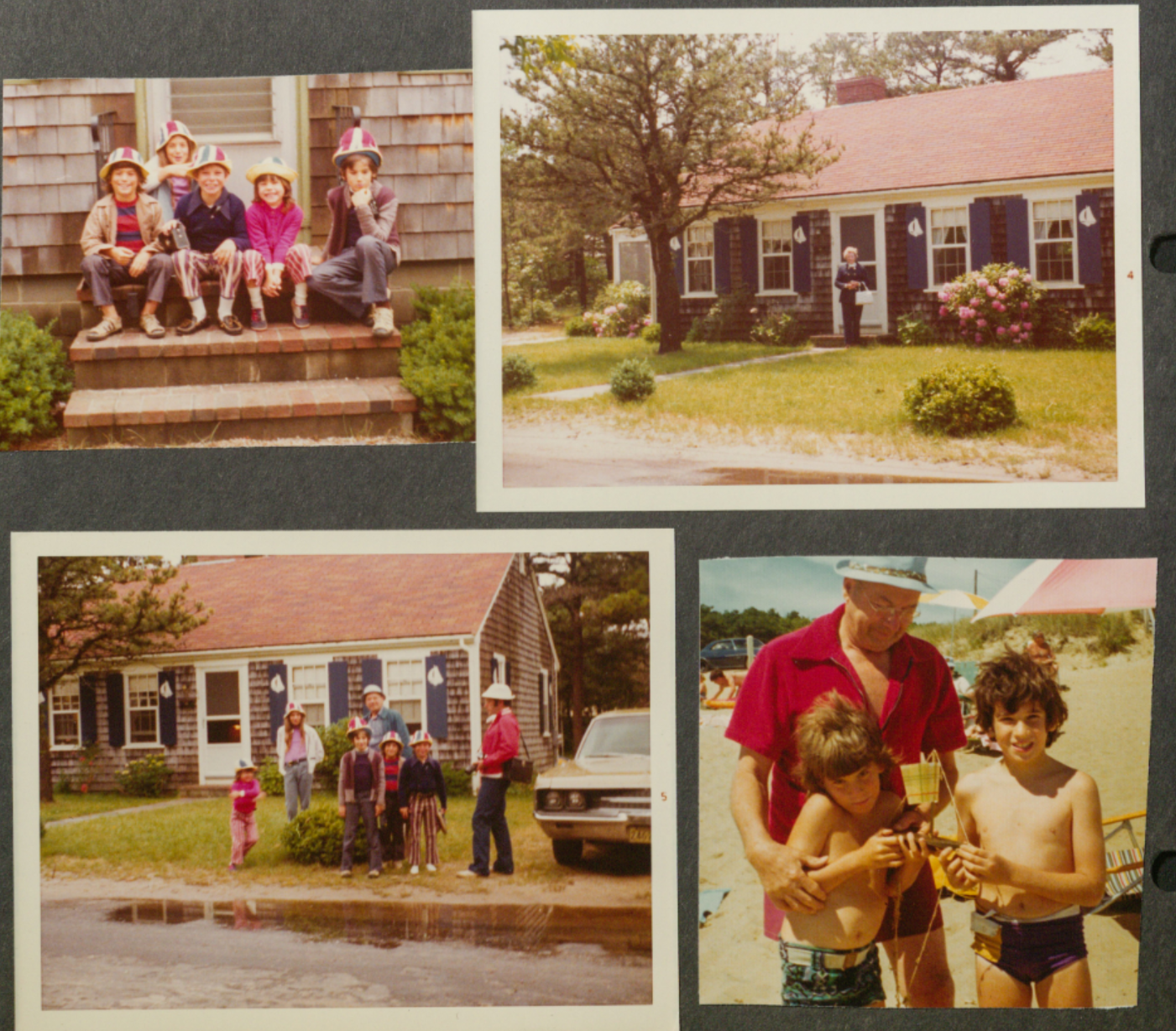

Regina’s parents, Nick and Cecile, rented houses across the street from each other (5 Ginger Plum Lane, Harwich, Cape Cod) every summer and we would spend two weeks there with our cousins (Marge’s kids):

Regina circa 1980 with our family’s miniature poodle:

Regina in 1982 with the artist who is the subject of Herman Perlman, his life and art, a book that she wrote (amazingly, available on Amazon 40+ years later!).

Here’s me and Regina at the Avebury stone circle in 1983 (my parents were in Britain and I had a business trip to Europe):

She traveled to Cambridge for the big college reunion years (1990):

Also from 1990, a portrait that my friend Henry and I made of Regina:

At the Great Wall of China in 1999, a trip with five neighbors (Lois, Ginny, Carolyn, Lorraine, and Regina):

A 2005 album page featuring Barbara Rippa, a Vermont-based college classmate (and roommate) with whom Regina would be in touch by phone every week or two here in Florida.

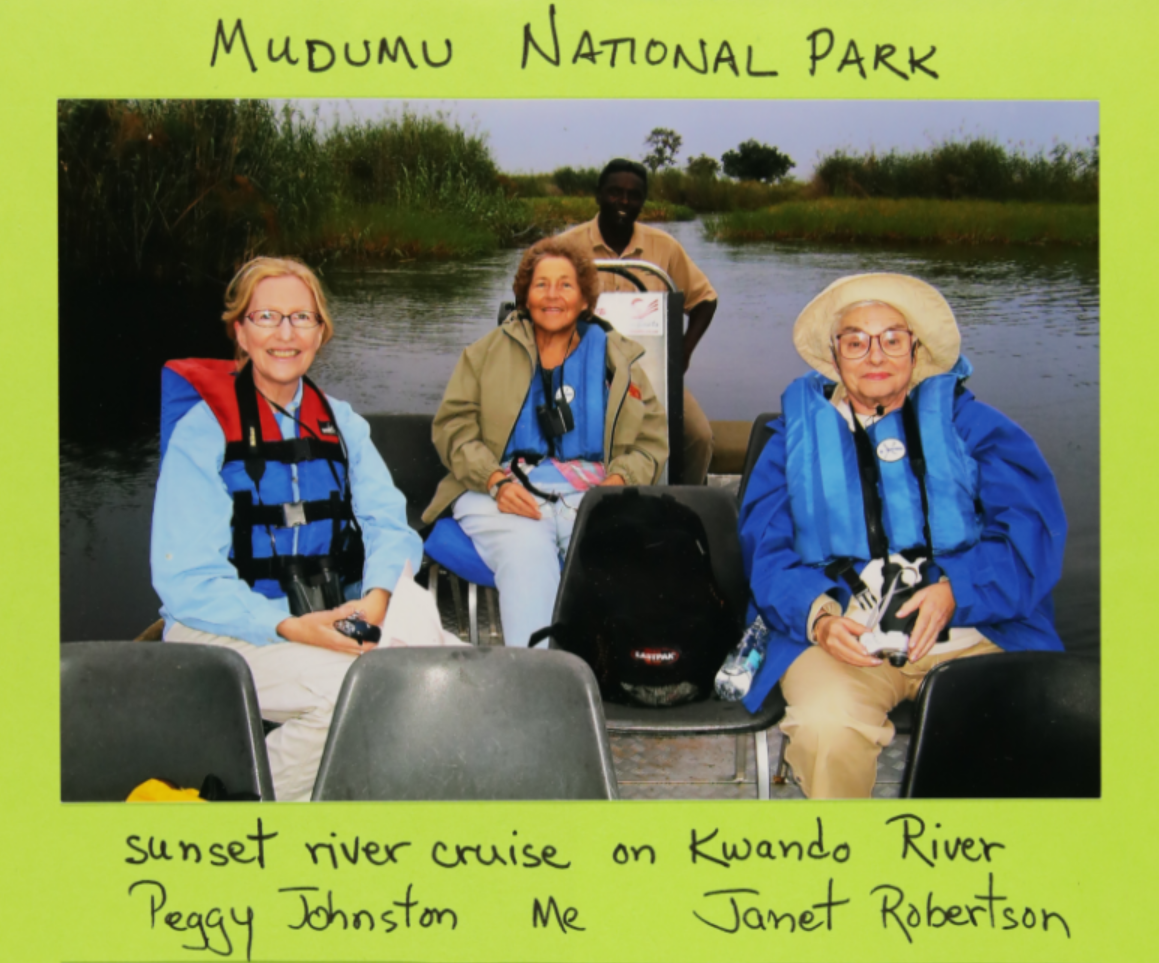

Here’s Regina in 2007 (age 73) in Africa (I think that Janet Robertson was a classmate at Radcliffe):

Another one from 2007, taken by a grandchild:

In 2009, holding a new grandchild:

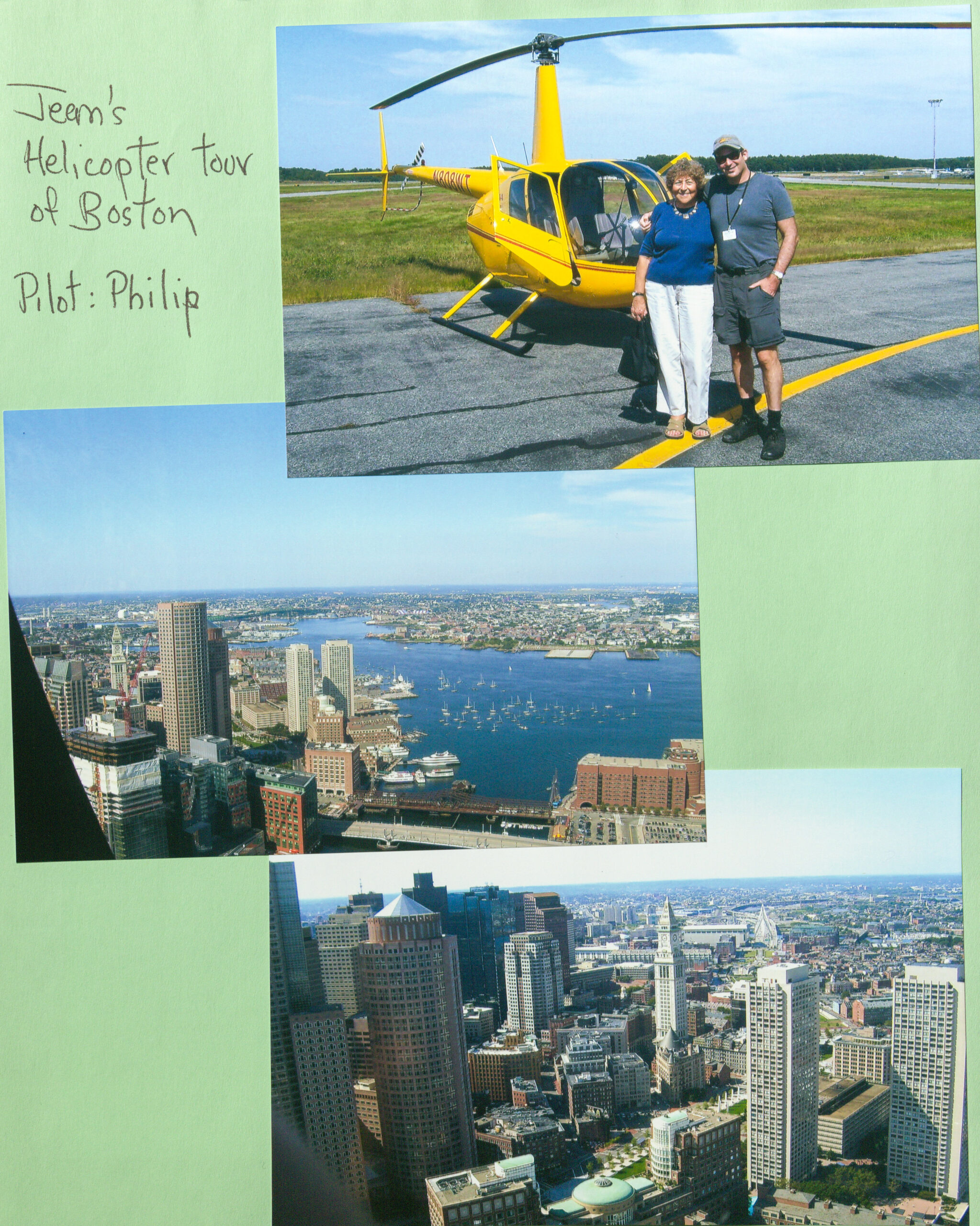

I made it into Regina’s 2009 photo album with a little help from the Robinson R44.

Headed to Paris with me in 2016 (wedding of a former student at MIT then Baltic cruise, the first of two cruises that we did together (tip: become a hero among seniors on a cruise ship by paying for a parent’s ticket (word spreads quickly about this reversal of the apparently conventional arrangement)):

2018, in the independent living apartment she shared with Nathaniel (she loved what she called “ethnic food” and she’s holding some bread that I picked up on the way in from the Gaithersburg, Maryland airport):

Regina was passionate about family connections and wanted to push through her increasing infirmity to a grand-niece’s wedding in New Jersey in July 2022. Despite my awareness of the absurdity of listening to people vow permanent attachment in a society that offers profitable no-fault (“unilateral”) divorce, I flew up from Florida, rented a car, and drove her to the event. Here she is at a diner and then at a stop in her beloved Longwood Gardens, which was usually a stop for us during family trips to New York or Cape Cod (cue the unairconditioned 1970 Chevrolet Chevelle station wagon with dark green exterior (to match the hedges) and black vinyl seats (ouch!)):

In February 2024, her first day in Florida (after being pushed out of independent living in Maryland and a couple of weeks before moving into assisted living), with Mindy the Crippler who was to become her almost-daily companion:

Regina’s passion for fine art never dimmed and she enjoyed revisiting the Norton Museum in West Palm Beach (March 3, 2024):

As with the pundits who said that television would be great because Americans would watch Harvard lectures and Shakespeare plays at home, we imagined that Regina would teach our kids fine art. Instead, they taught her to play pinball, pool, and table shuffleboard.

Mindy the Crippler liked to be Regina’s lap dog during thunderstorms:

Kamala Harris told us that Donald Trump would end our (beloved) democracy and rule as a (hated) dictator. Today she tells us that it will be her “sacred obligation” to certify the end of democracy and the beginning of the hated dictator’s rule:

Today, I will perform my constitutional duty as Vice President to certify the results of the 2024 election. This duty is a sacred obligation — one I will uphold guided by love of country, loyalty to our Constitution, and unwavering faith in the American people. pic.twitter.com/w21HzdNxGs