A total of 219 people have been injured in clashes between football fans and police across France after Paris St-Germain (PSG) won the Champions League final against Arsenal.

It might have been the police who started the violence, in other words, and the only thing that we know about the non-police combatants is that they were “football fans”.

X perspective: the rioters were Muslims and/or “North African”.

The Muslim gang riots continue in Paris.

A huge fire was started at the foot of the Eiffel Tower.

Notice how they chant “Allahu Akbar.” This is a religious war, and this is their way of saying “we own the place now.” pic.twitter.com/MLXSc3IEXi

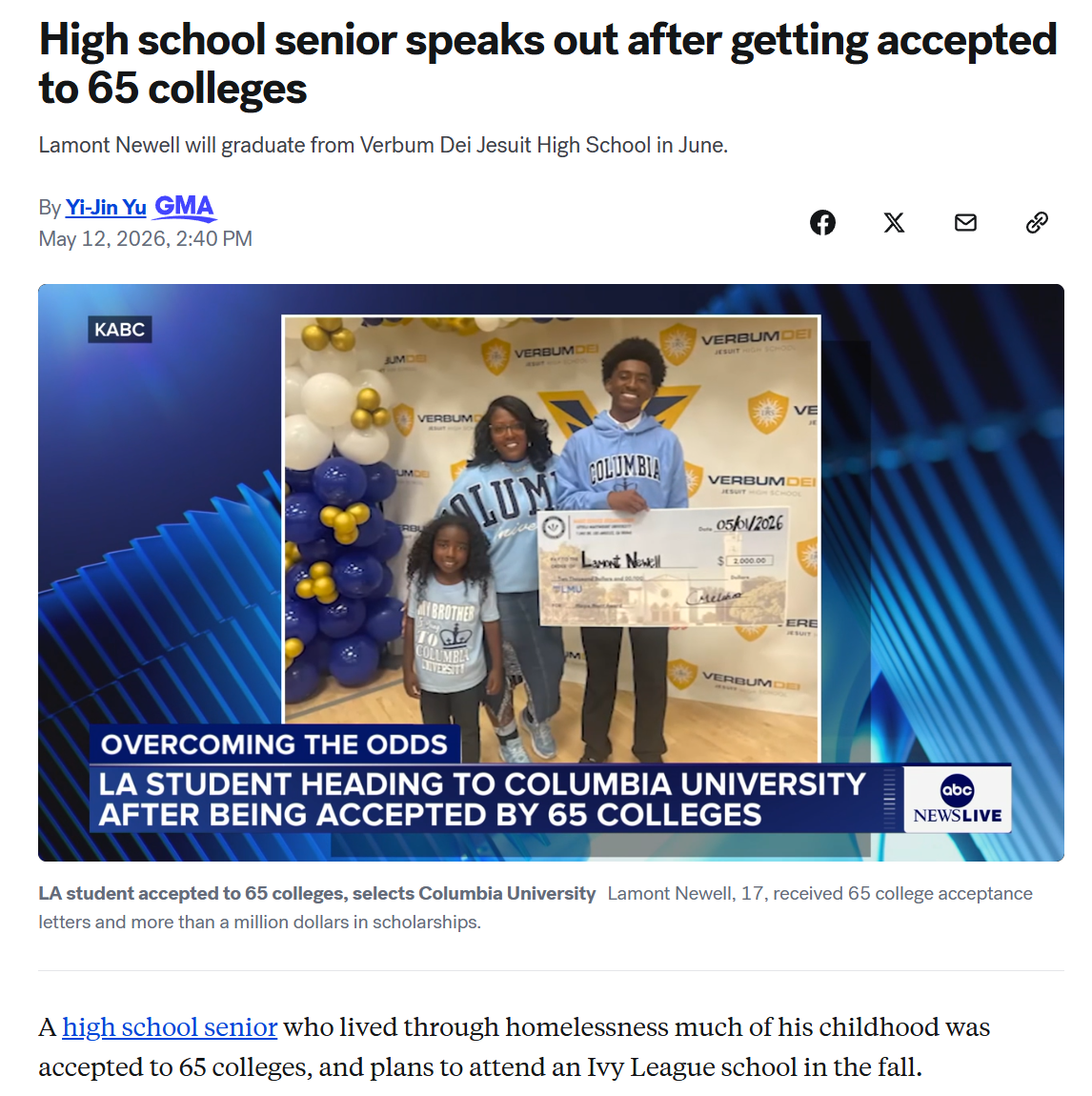

As we complete our celebration of Asian American and Pacific Islander Heritage Month, celebrating the common culture, language, and religion of Samoans, Koreans, Burmese, and Rajasthanis, here’s an ABC story that will warm the hearts of Asian American and Pacific Islander parents:

A high school senior who lived through homelessness much of his childhood was accepted to 65 colleges, and plans to attend an Ivy League school in the fall.

Note that if we believe The Son Also Rises: economics history with everyday applications we wouldn’t expect Lamont Newell to do as well as a 17-year-old with the same grades and same test scores (assuming that he took any tests; Columbia is permanently test-optional) who came from a successful (not homeless) family. Our society has chosen to invest in Mr. Newell, who won’t be paying or borrowing a dime for his education (“California teen who grew up homeless earns full ride to Ivy League school after 65 college acceptances”), rather than invest in an Asian 17-year-old whose parents worked like slaves to avoid homelessness and/or reliance on “public assistance” (i.e., taxpayers). If University of California economist Gregory Clark is correct, in other words, by lower admissions standards for those whose families are poor, the U.S. is doing the opposite of what investors in higher education would do if the goal were a return on investment.

(Why is it “society” rather than “Columbia” investing in Mr. Newell? At least half of Columbia’s money comes from taxpayers thanks to (1) Columbia’s tax-exempt nonprofit org status (investment returns aren’t taxed; half of every donation comes from taxpayers rather than the donor because the donor’s tax bill is reduced), (2) Columbia’s federal grants that yield massive overhead profits.)

The second (or 11th) part of a report on my April/May 2026 pack-up-patch-up-and-sell-the-condo sojourn among the world’s most intelligent humans. (Part I)

Cambridge is populated by Scientists who closed kids’ schools for 18 months and locked themselves in their crummy apartments for 2-3 years so as to deny a respiratory virus the opportunity to spread and mutate. These same people now voluntarily cram themselves, without masks, into coffee shops that are (1) more crowded than my 100%-full JetBlue flight, and (2) entirely lacking in modern ventilation.

All is not lost, however, because the Scientists do wear their masks at Whole Foods (the employees were about 50% masked):

Having Instacart deliver, thus sidestepping the respiratory virus risk entirely, is apparently not an option. CVS carefully protects precious Dawn and Windex from respiratory viruses by putting them behind locked glass cabinets:

Various retail businesses also protect their workers, and by extension all of us, from ICE and Donald Trump:

The walk home from shopping, with winds gusting over 20 knots, is made safer via outdoor masking:

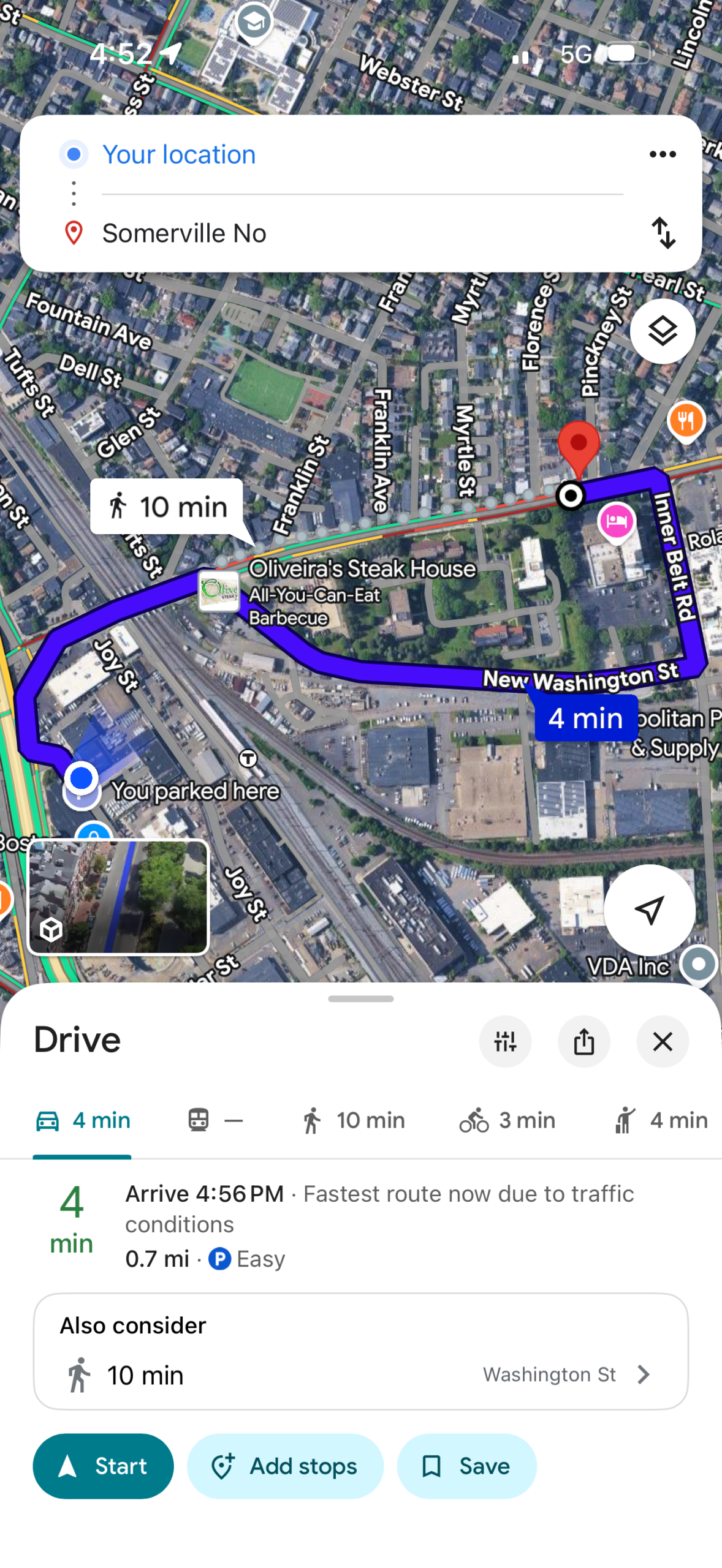

The brilliance of our AI overlords was on display. I borrowed the neighbor’s ancient Mini and asked Google Maps for directions from U-Haul in Somerville to a car wash. The Tensor Processing Units decided that it would be smarter to instead walk to the car wash rather than bringing the car to the car wash:

Here’s the passenger footwell of a car owner who has lectured me for decades regarding my inadequate level of passion for protecting our environment:

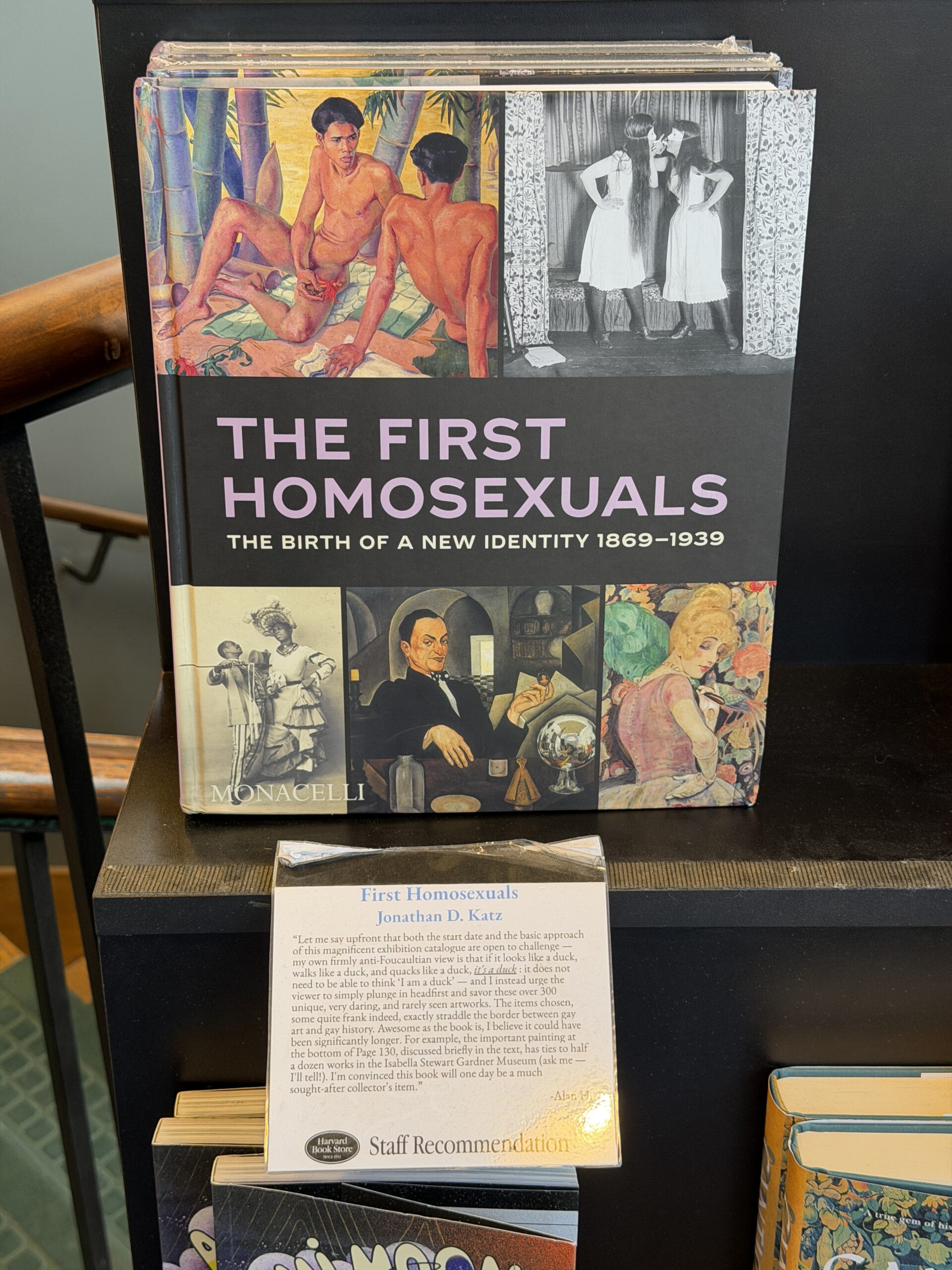

Environmentalist/Hater isn’t the only useful way to categorize people. At Harvard Book Store, one learns that Americans can be neatly divided into racist/anti-racist and fascist/anti-fascist:

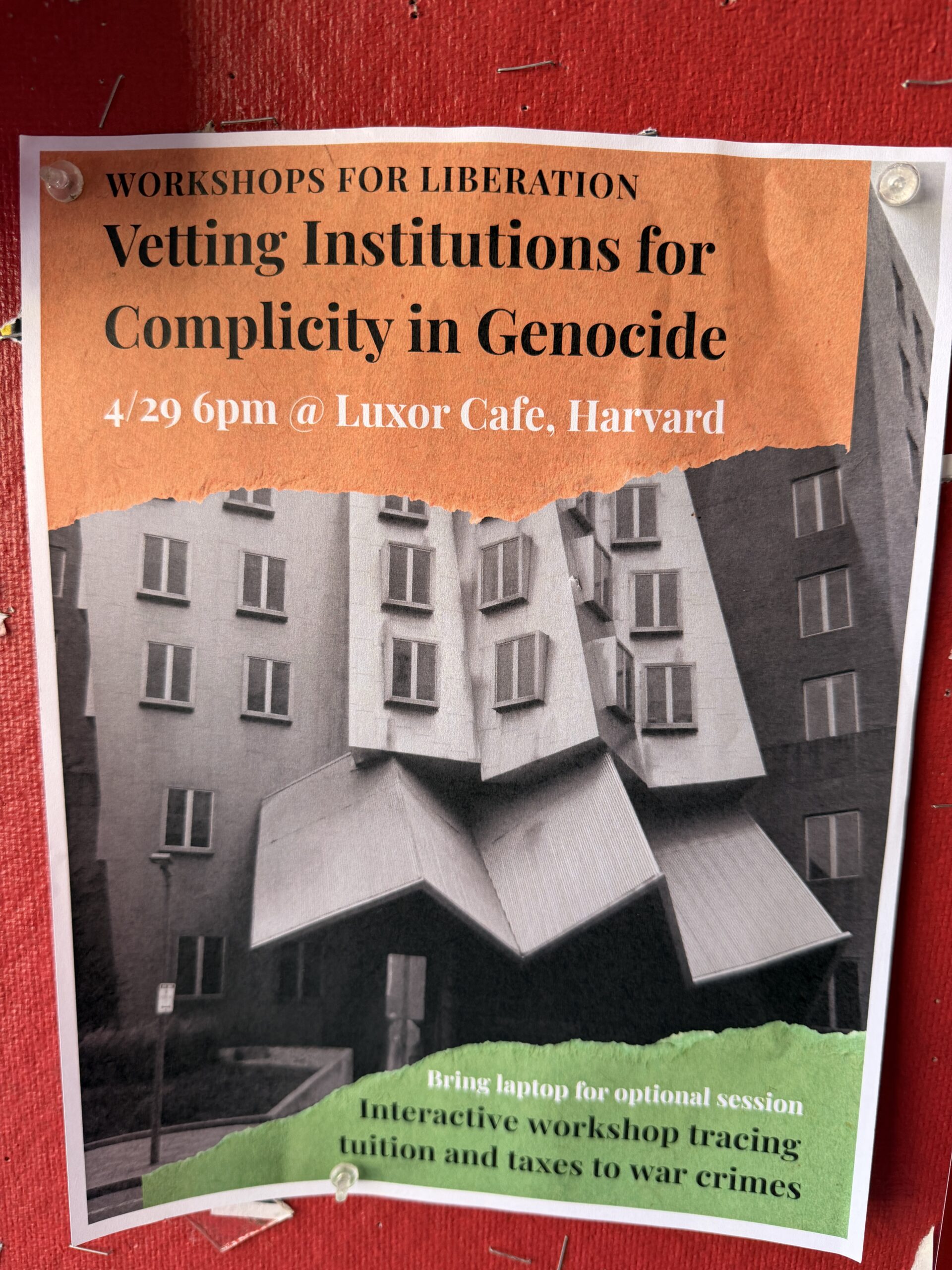

At Harvard, we learn that there is also a useful division into Genocidal/Not-Genocidal:

(The advocates for Arabs who call themselves “Palestinians” meet at a cafe named for Luxor, Egypt, thus reminding people that many of the Arabs who were living in the modern state of Israel in 1948 were themselves recent economic migrants from Egypt. For example, Layla Almasri is an athlete who represents the purported country of “Palestine” in the Olympics. She calls herself “Palestinian” despite having been born in Colorado. Her last name, according to ChatGPT: “Almasri / Al-Masri in Arabic is usually المصري (al-Maṣrī), meaning “the Egyptian” or “from Egypt.””)

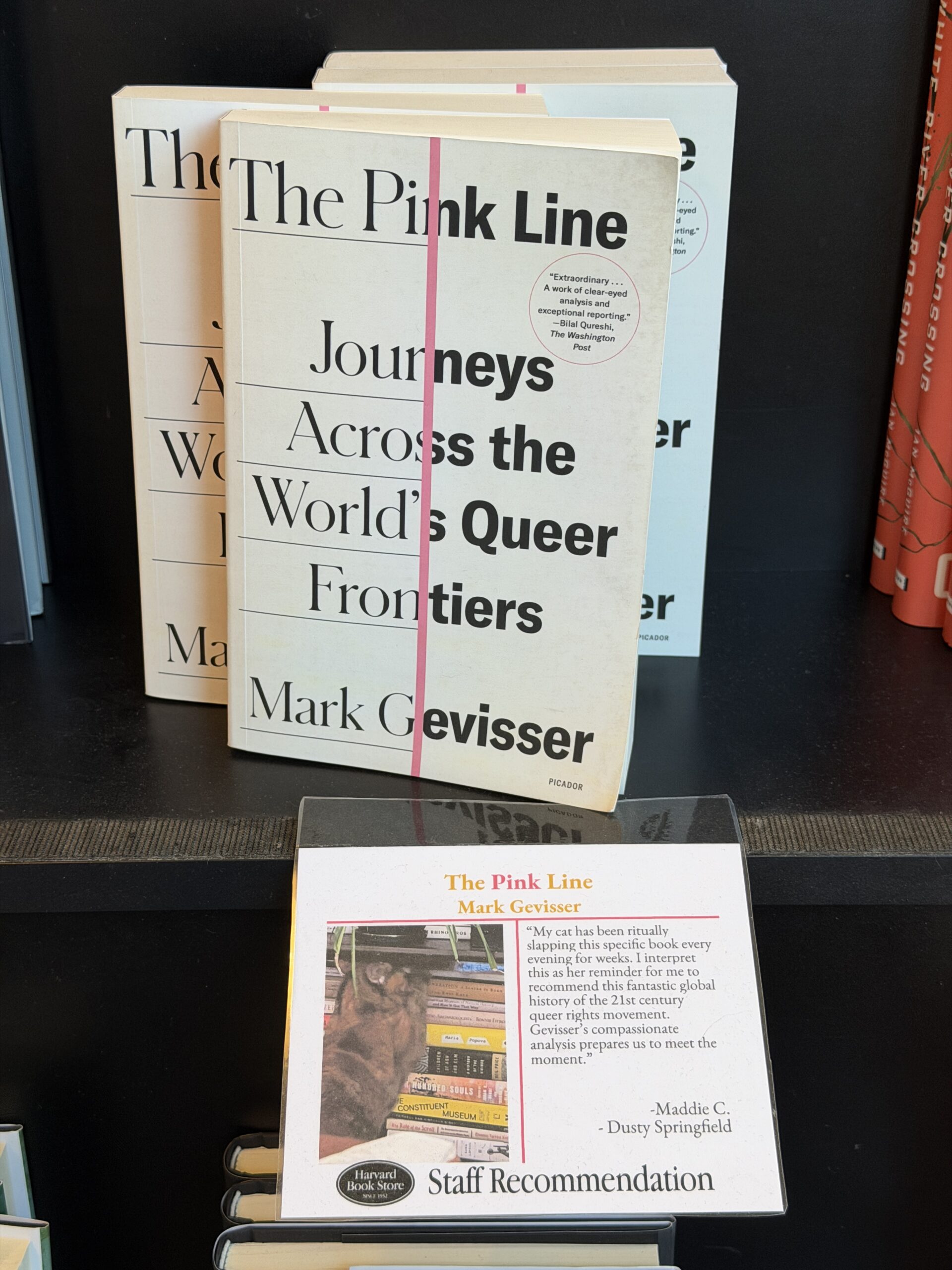

Related, from the Harvard Book Store’s featured book table in the front:

(Americans won’t read poetry in English, but there is a market for poetry translated from Arabic?)

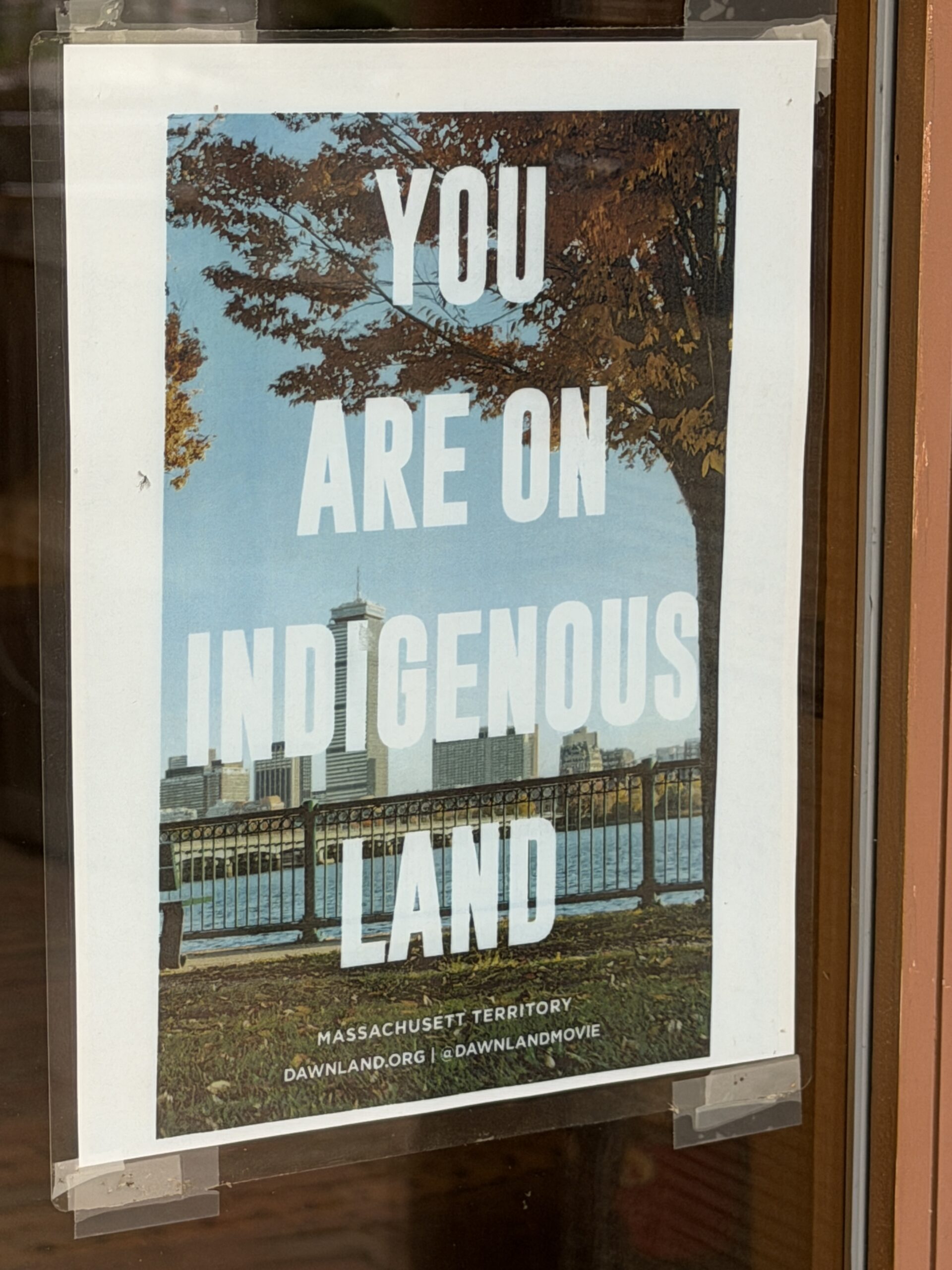

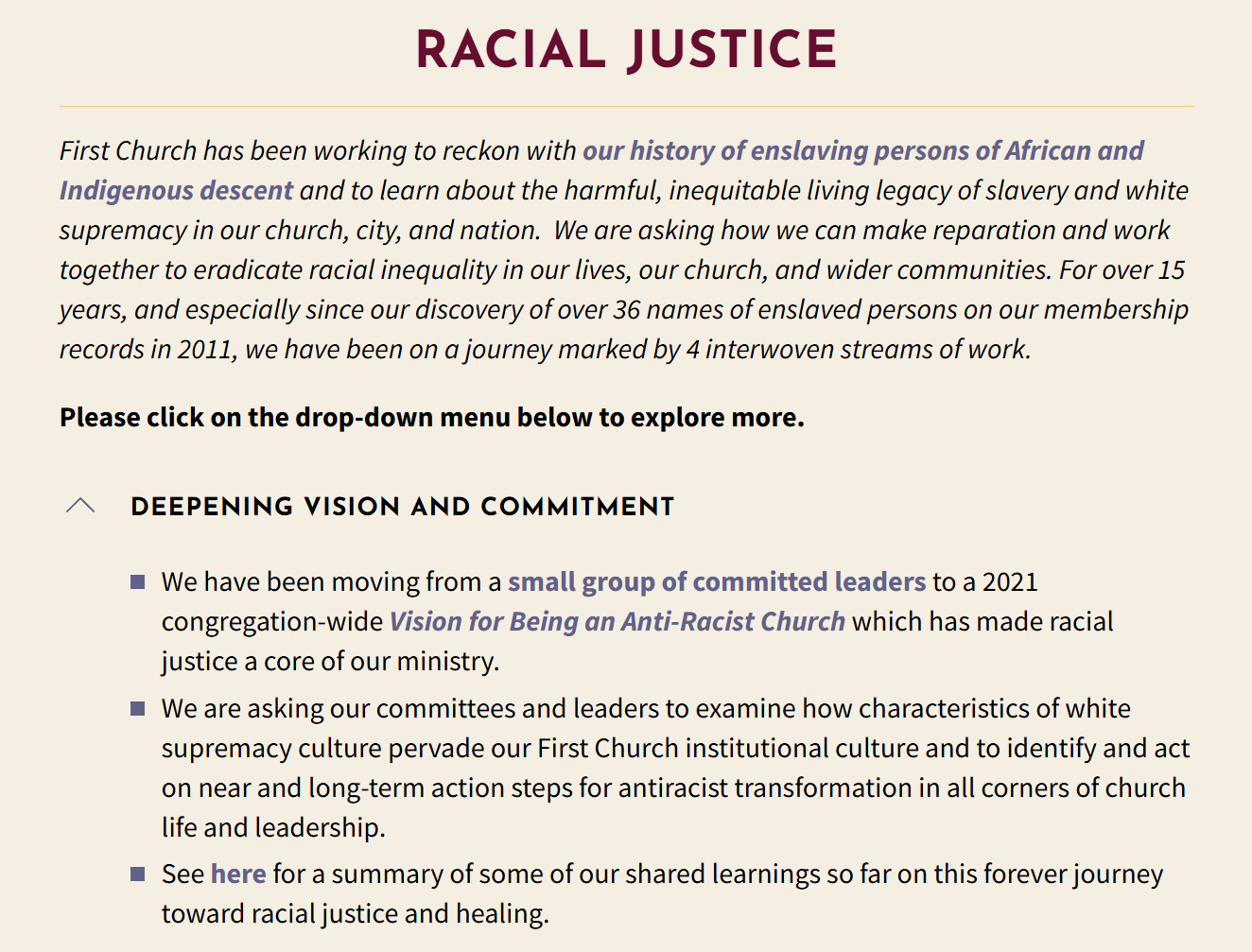

Aside from observing Islam, what’s going on with spiritual life in Cambridge? The First Church reminds visitors that the church has stolen some land and refuses to either give it back or pay rent to the rightful owners:

What have they placed on this stolen land? Signs that say Jesus is their “center” just above the sacred Trans-enhanced Rainbow Flag that, presumably, Jesus designed.

Kids in the day care that runs on church property learn about the importance of the Rainbow:

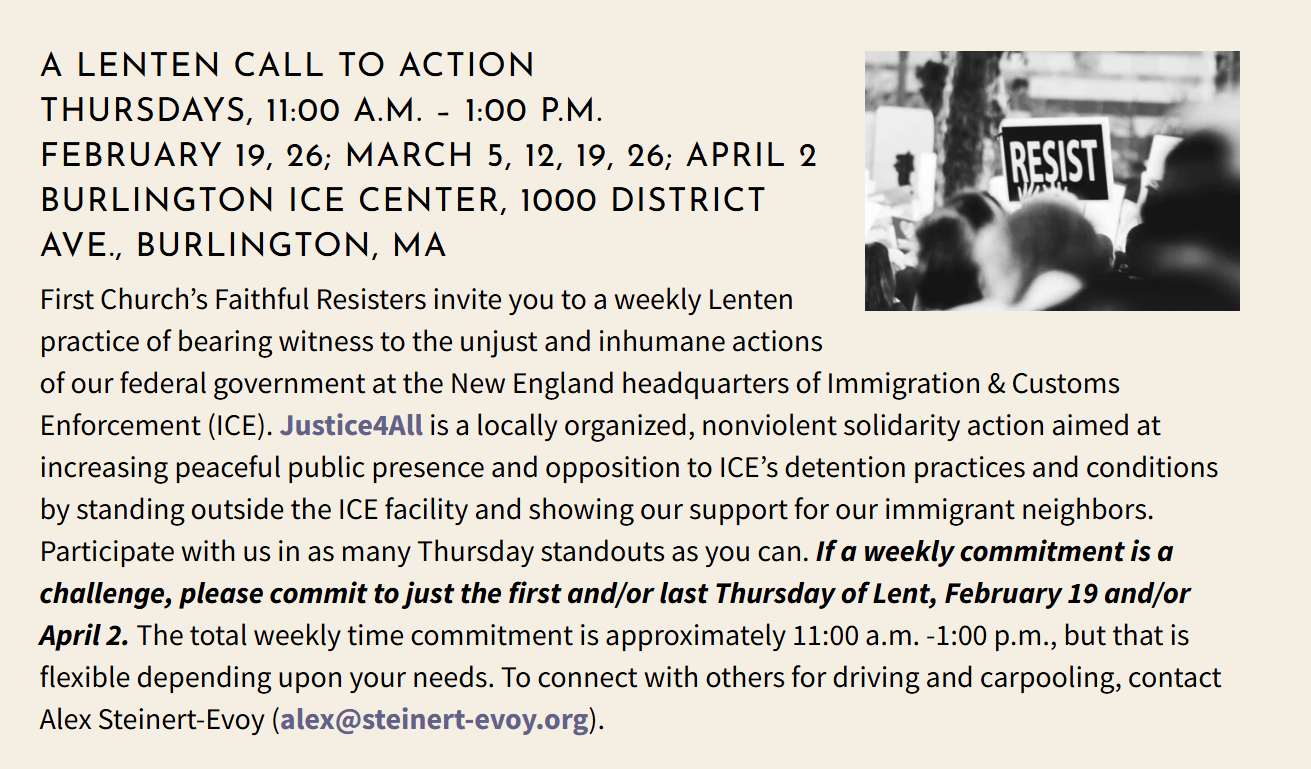

The Church says that they want to maximize the number of low-skill immigrants to the U.S. and obstruct ICE’s deportations. Example:

Black Americans who are descendants of slaves will receive a lot of kind words from this church and will also receive lower wages because of competition from low-skill immigrants whom the church brings to Maskachusetts (though maybe the immigrants will figure out that being on welfare in Massachusetts provides a higher spending power than working at the median wage (Table 4) and, thus, won’t compete for jobs).

A couple of the books left behind by AirBnBers (there was also plenty of masks stuffed into various corners):

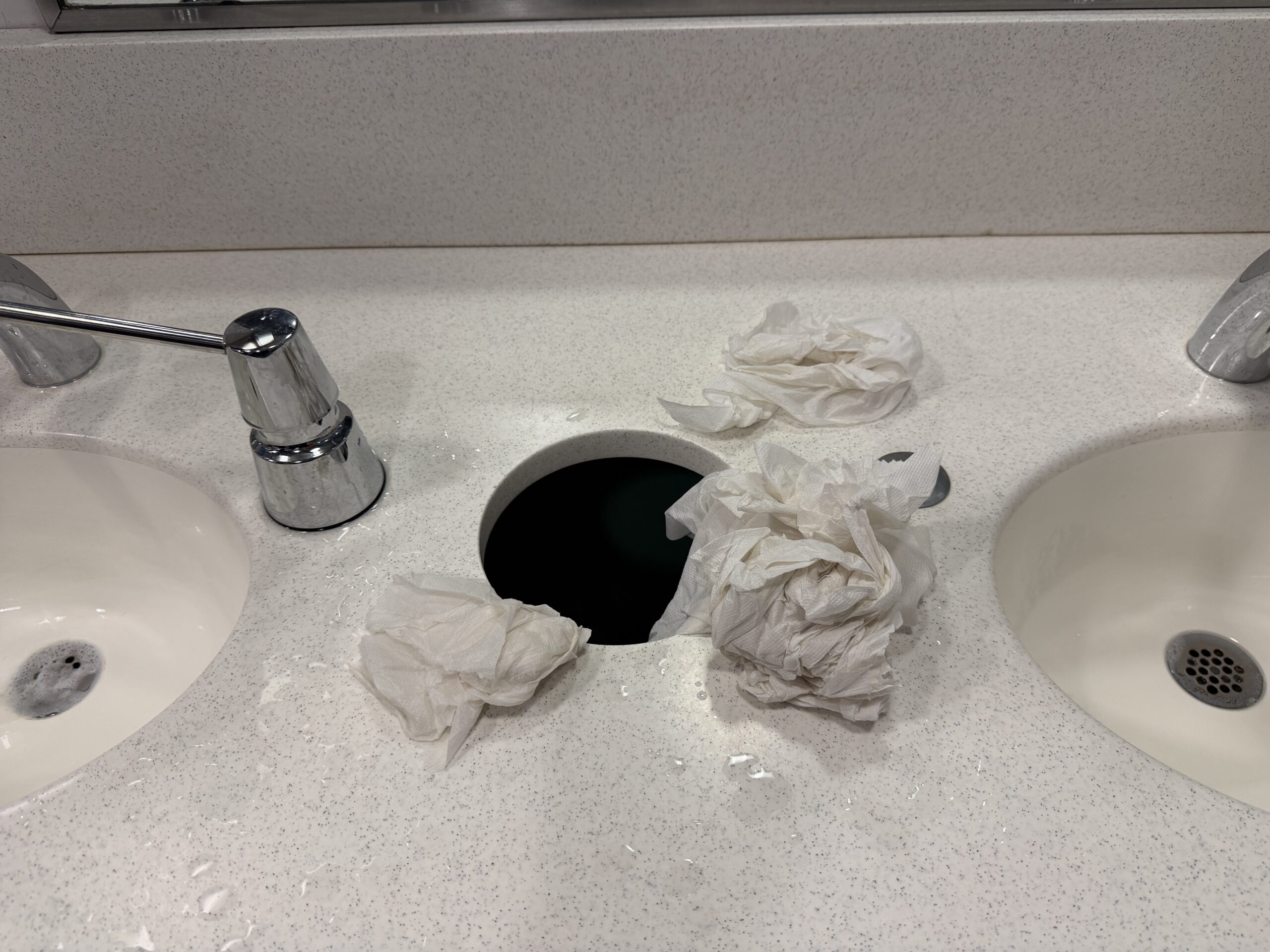

At Logan Airport, the world’s smartest humans couldn’t handle the challenge of getting paper towels into the trash:

Floridians, despite being afflicted with low intelligence (according to the smart/full-masked-in-2026 residents of Maskachusetts), are consistently able to master this skill, as evidenced by the cleaner bathrooms at PBI, FLL, and MCO. Speaking of PBI (soon to be “DJT”?), here’s the view during the approach (Singer Island in the foreground, famously home to the MacArthur Foundation’s donor (the MacArthur Foundation set up our development).

Once inside the airport, we see the masked Bostonians waiting for the jet’s return to the Land of Science:

A few photos from my April pack-up-patch-up-and-sell-the-old-condo trip to Cambridge….

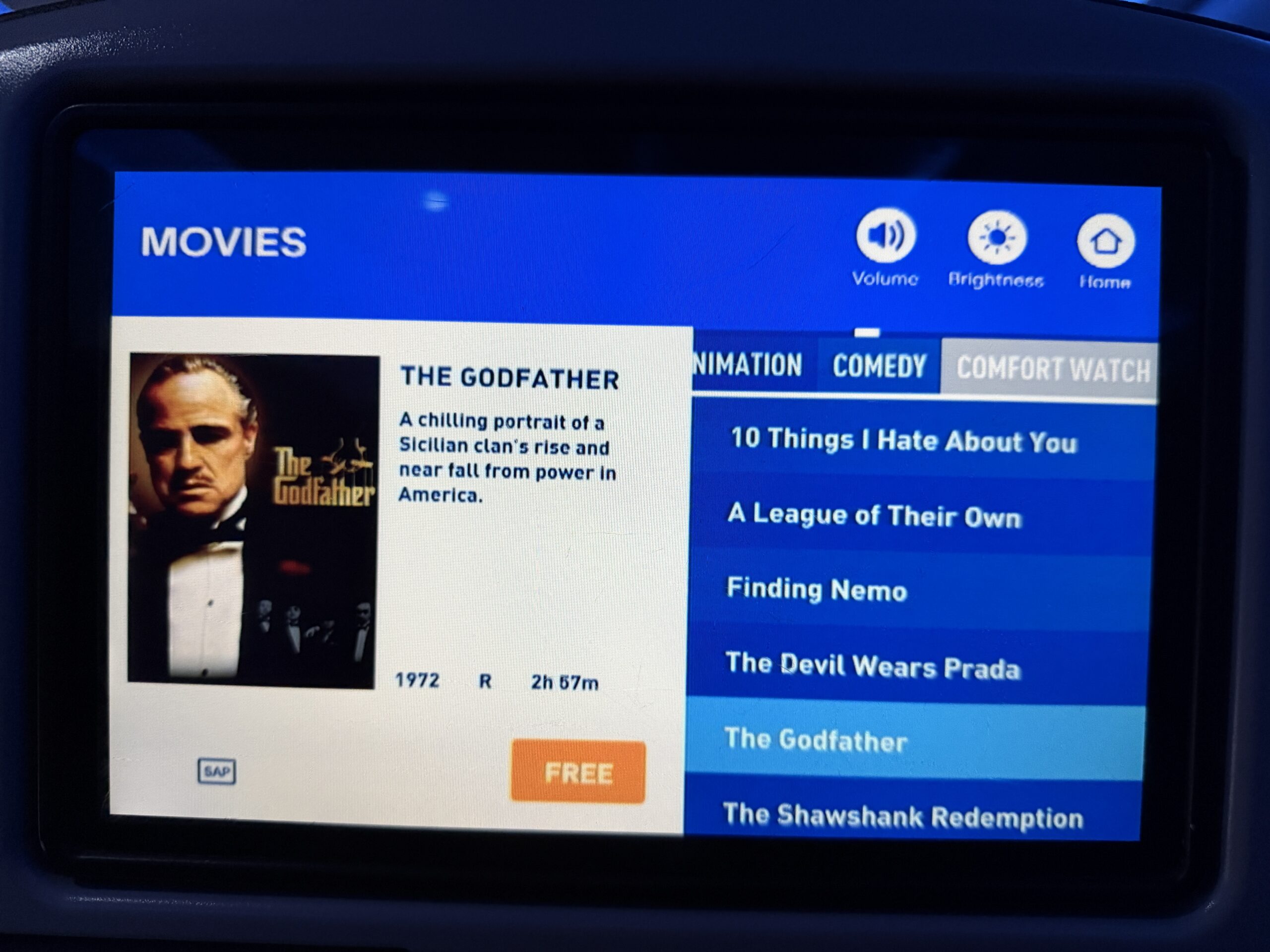

JetBlue classifies The Godfather as a “comfort watch”. Nobody at JetBlue loves horses?

Note that this movie doesn’t contain the best line in the series: “‘A lawyer with his briefcase can steal more than a hundred men with guns.”

A Prius drives over the sacred trans flag crosswalk (Central Square):

Compared to Palm Beach County, where apartment buildings and HOA generally ban pit bulls, seeing these loving animals (“A dog owner was hospitalized Saturday afternoon after being attacked by his own pit bull on River Street.”) is a common sight (front of Cambridge Public Library):

A few steps away, observant Muslims are forced to live in a decidedly un-Islamic society. Not only were they exposed to pet dogs (haram), but there is a shameless hussy in the background who isn’t covering her hair:

Had they wanted to sit in front of a bench by City Hall, they would have been forced to sit on the sacred trans-enhanced Rainbow Flag:

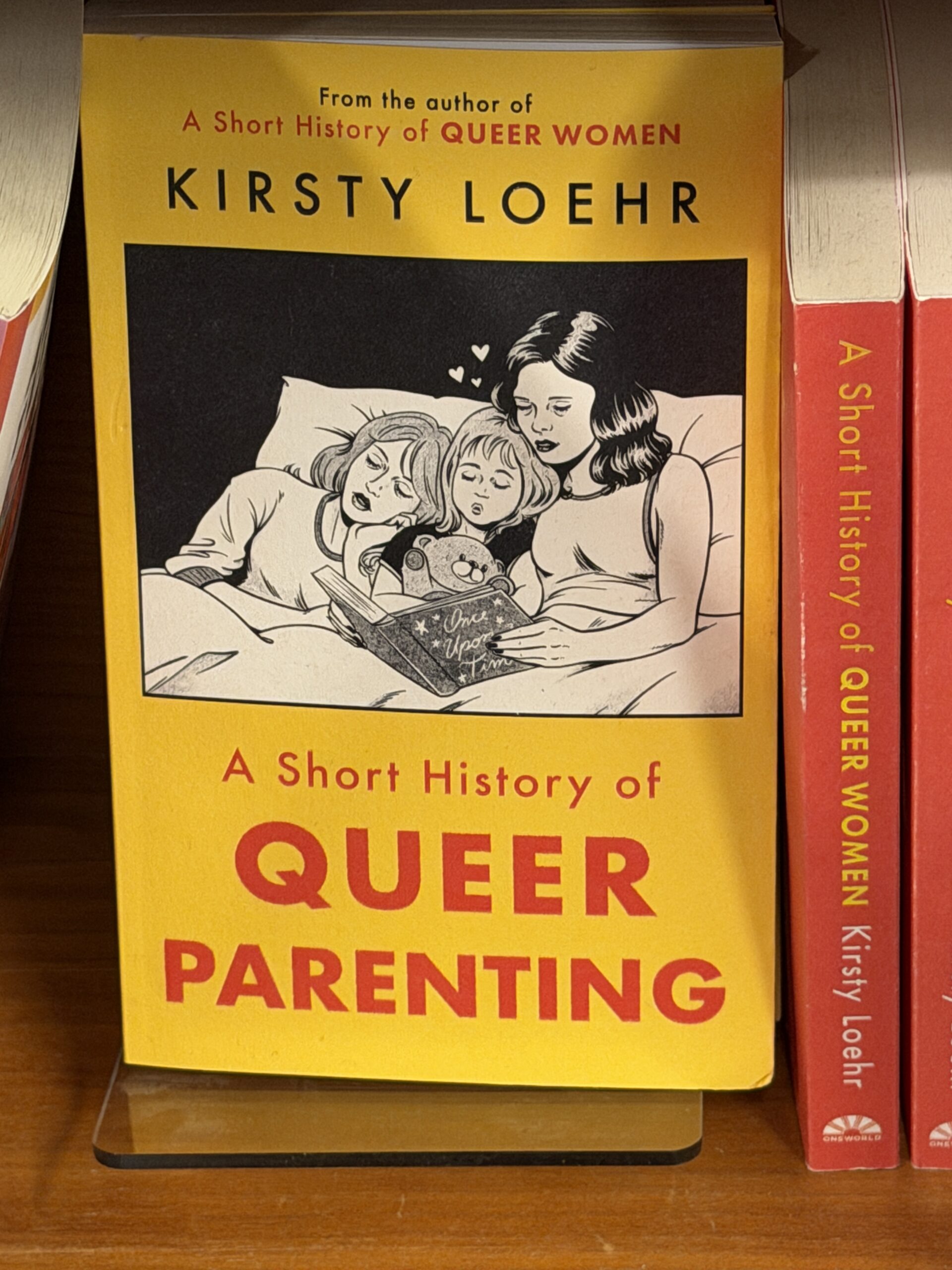

Had they gone to Harvard Book Store, they would have been assaulted by a wide variety of books on the subject of a haram lifestyle:

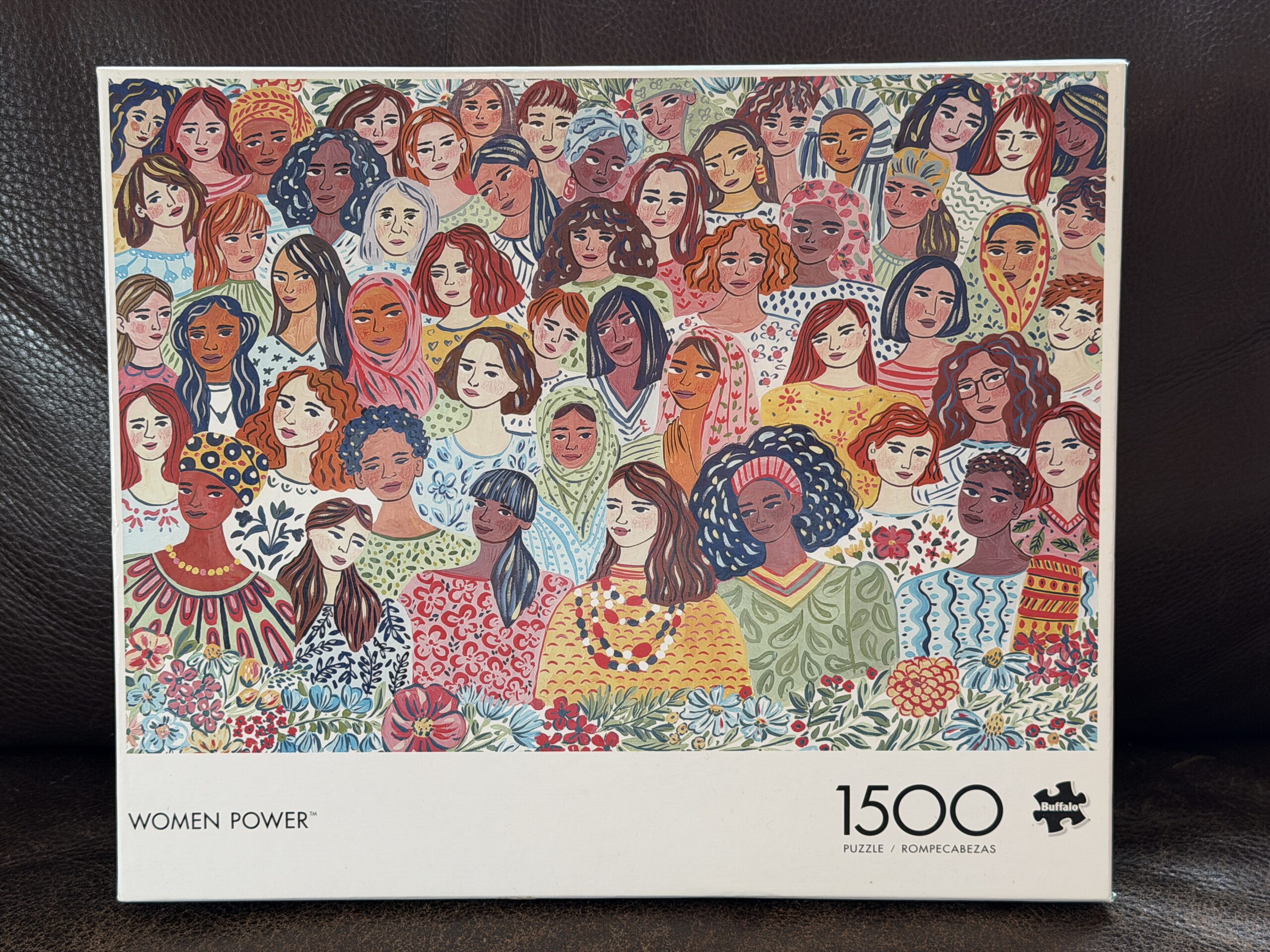

Had they wanted to spent a couple of weeks putting together a 1500-piece puzzle on “Women Power” they would found only a handful of hijabis (this was left in my old condo by an AirBnBer):

If they had done the “Women Power” puzzle they would have been saving our planet:

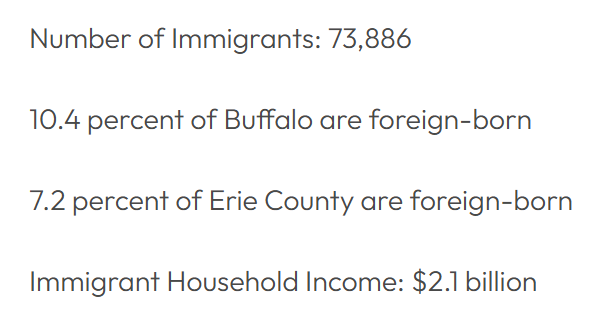

Perhaps the puzzle was made by migrants? Rust Belt cities such as Buffalo seem to be growing their economy primarily by importing people who will be entitled to taxpayer-funded housing, health care, food, and smartphone. “Know the Value of Immigrants and Refugees” (International Institute of Buffalo):

These 73,886 noble enrichers earned a total of $2.1 billion in 2025. That works out to an average per-capita personal income of $28,422 per year. According to the BEA, overall US per-capita personal income was $76,375 per year. So the majority of immigrants who live in and around Buffalo should be entitled to every form of what used to be called “welfare” (now “means-tested benefits”).

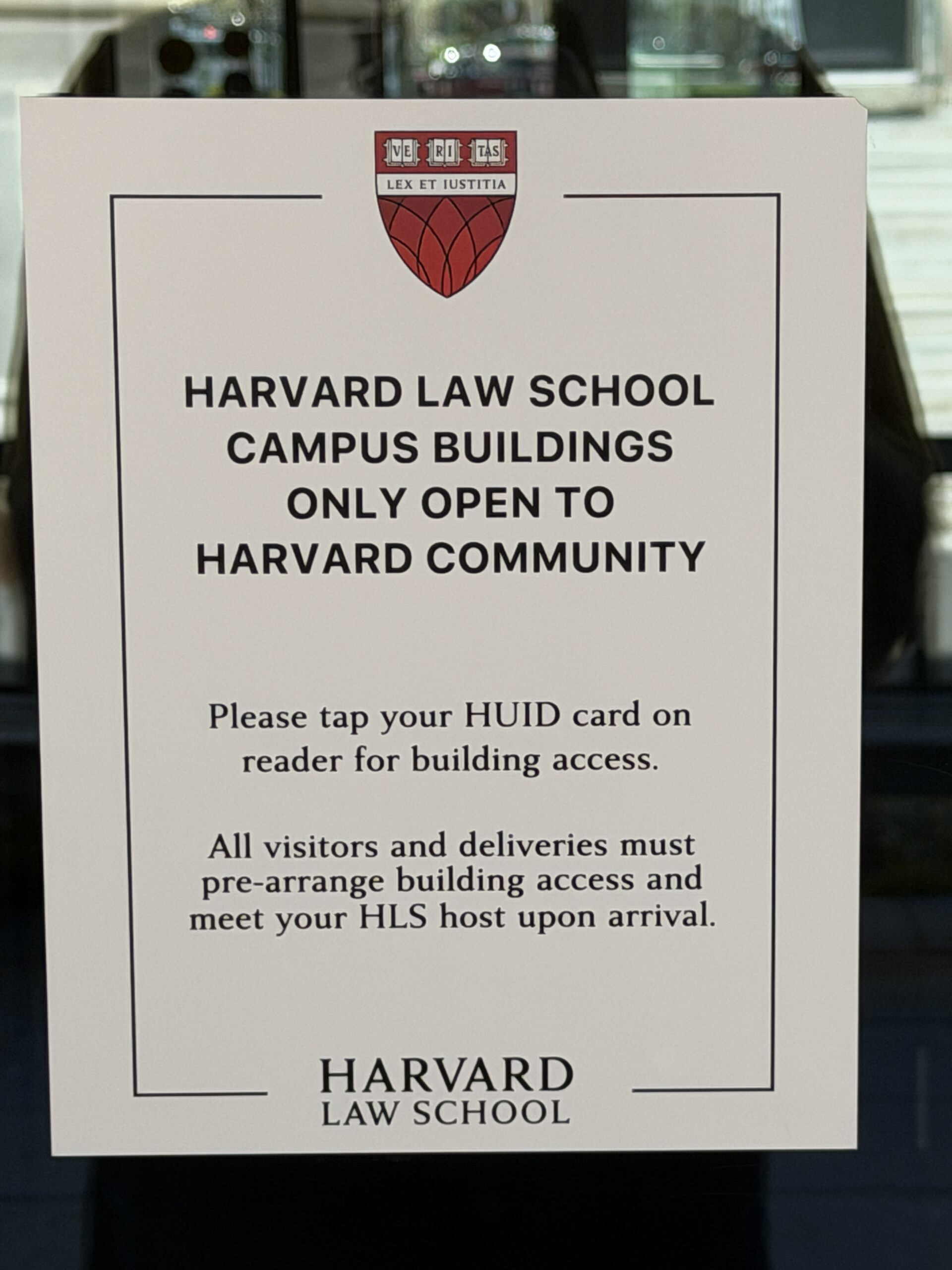

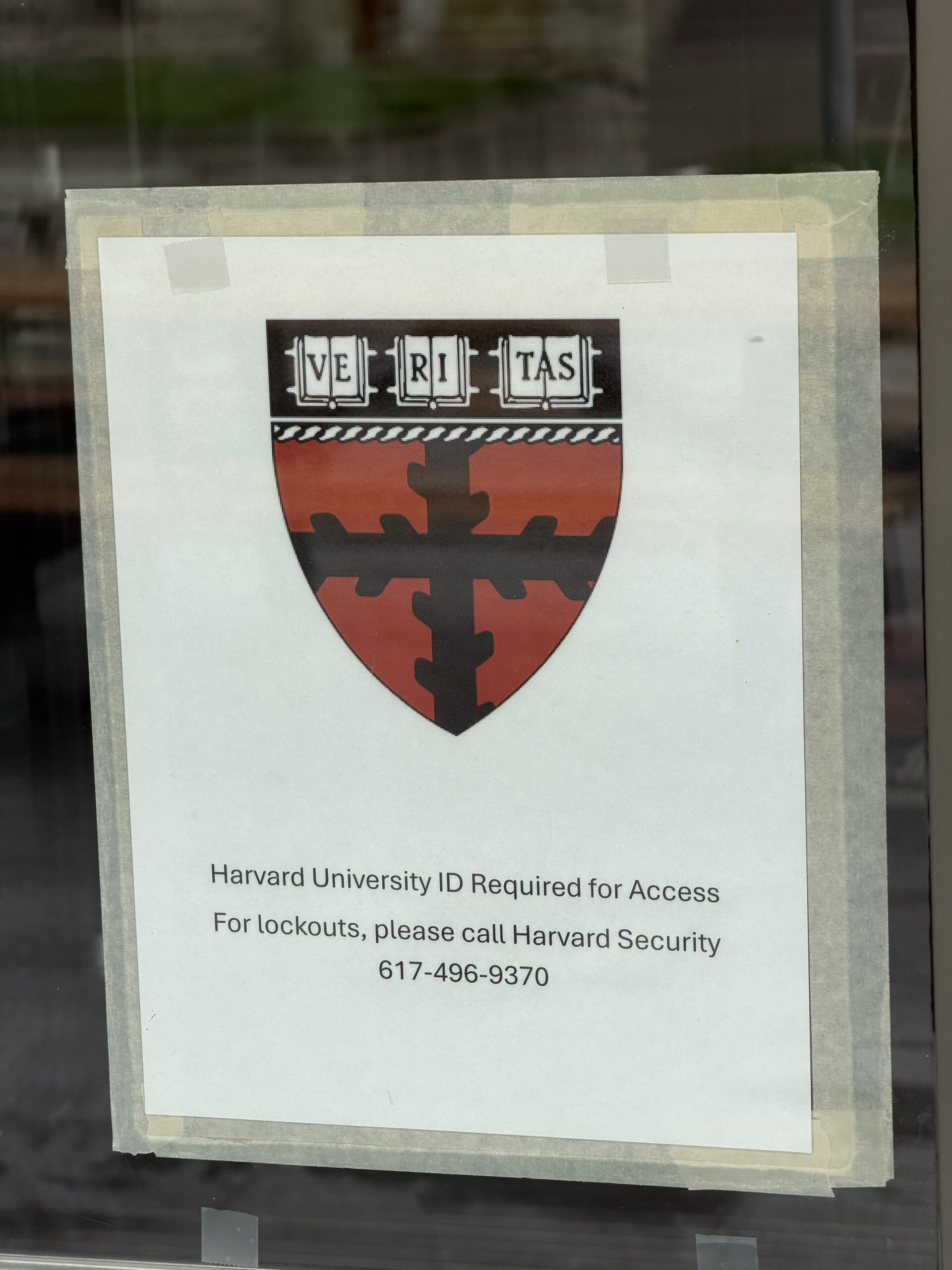

Had the above ladies, presumably migrants, wanted to enter a Harvard building and meet with one of the many virtuous people who say that no human is illegal and that the U.S. should be doing more to welcome migrants, they would have discovered the doors locked against them. According to the best minds of Harvard, the U.S. should allow any of world’s 10 billion humans (revised estimate) to come here and receive four generations of taxpayer-funded housing, health care, food, and smartphone. Requiring an ID to vote is Hate of the First Magnitude. At the same time, there are strict border walls around every Harvard building, with strict computer-enforced ID checks, and nobody can immigrate even for 15 minutes. Trying to visit a friend who teaches at Harvard Law School and also the computer science building:

Speaking of Harvard, the elite Democrats who control the institution and who say that all workers should be unionized apparently won’t pay their own union workers a fair/living wage:

According to the Crimson:

The offer, announced in an email to faculty, would raise salaried student worker compensation by 11 percent over four years — up from Harvard’s previous 10 percent proposal.

In other words, at the current rate of inflation, the workers now on strike would be paid less, in real dollars, four years from now!

Here’s a disturbing proposal from a politician whose policies I generally agree with:

Today in Tampa, I outlined the Save Our Homes from Excessive Property Taxes plan that will eliminate taxes on homesteads.

Property tax revenue collected by local governments has nearly doubled in the past seven years (from $32 billion to $60 billion) and is expected to reach an… pic.twitter.com/3ZcexD9L7X

While I don’t enjoy paying property tax, the idea that the majority of Floridians eligible to vote will soon pay nothing seems like a recipe for much faster growth in county/local government spending. (Many Florida voters already pay next to nothing because they’re taxed on the original purchase price and perhaps that is what accounts for the rapid rise in county spending that Gov. DeSantis decries.)

If the majority of Floridians aren’t paying property tax, won’t they vote for every blue sky spending dream that counties and cities put forward? That’s how it works at the federal level. The majority pay either nothing or next to nothing and have voted the U.S. into the world’s largest or second largest welfare state, as a percentage of GDP (we vie with France for the title). Even if a homeowner who isn’t taxed receives only 1 penny of benefit for every additional $1 million spent it would still be rational for him or her to vote for increased spending.

Is there a method to Ron DeSantis’s apparent madness? I’m sure that he understands politics much better than I do, but I am struggling to find merit in narrowing the tax base and feel that the experiment has already been run on the American people. If the goal is limiting county spending, why not a state-imposed limit on county/local government spending? Take the 75th percentile of per-capita spending in 2025 and impose that as a limit, adjusted annually for inflation, on all Florida counties. A county that is already over the limit would have five years to come down into alignment with the law. This might force counties to eliminate affordable housing subsidies, for example, which have the potential to be infinitely expensive as well as certainly unequal (some people get below-market-rate housing; others, equally virtuous and equally situated, are forced to pay market rates).

Maybe the method in the apparent madness is that homesteaded property isn’t that important to county budgets, e.g., for Miami-Dade just 7 percent of the total budget. ChatGPT says it is 9 percent of the total Palm Beach County budget. Both of these counties have a lot of commercial real estate, but property tax as a whole isn’t the lion’s share of the budget as I would have expected.

Miami-Dade: Residential homesteaded property tax is about ~$0.88 billion — just 6.9% of the $12.9 billion FY 2025‑26 budge. Removing it entirely leaves 12BB to spend: Miami-Dade last operated at less than 12BB in FY ‘23‑24. So you could eliminate completely and still operate at… https://t.co/dbwU06Hs8J

Republicans in general seem to be competing with Democrats in the “make the rich pay for everything” department. As noted above, I don’t see how this can work in a democracy where the people paying nothing have the right to vote for unlimited enhancements to whatever they’re receiving from a government funded by a minority that can be trivially out-voted. Maybe it can work in California and New York City where AI and Wall Street actually do generate infinite wealth on a recurring basis, but Florida isn’t home to NVIDIA and the AI companies that use NVIDIA chips.

Happy Harvard graduation day for those who celebrate.

As part of unloading the Harvard Square condo that I bought in 1996, I hired the realtor’s favorite handyman to fix some recessed lights, shim an old Lightolier track so that the heads could be removed (an aluminum frame installed around them was interfering), replace some ancient smoke detectors in common areas, and secure a front door jamb into the rotted frame (over 100 years old?). He charged $1800 for his labor and worked from 9a-3p, including a trip in the middle to Home Depot. When I asked if that was really the going rate, he said that he makes this much every day. If he works 250 days per year, that’s $450,000 per year for the immigrant from Brazil with no college degree.

Gemini: “Harvard graduates earn a median salary of approximately $85,000 to $95,000 ten years after enrolling.”

I previously hired a different handyman whose rates were, I think, a little lower (but that was before Bidenflation). He eventually just started saying “no” to all jobs, however, because he was too booked out. Update: I searched Gmail and found that he was charging $90/hr in 2020.

If you’re going to criticize me for financial irrationality, the situation is even worse than overpaying a noble migrant. The buyer already accepted the condition of the property and I wasn’t obligated to fix anything, do anything, or pay anything. The buyer hired a professional inspector whose job it was to uncover anything substandard. Why did I hire and pay various tradespeople, invest some of my own time in doing stuff such as changing electronic lock batteries with new 9V lithiums, etc.? I just didn’t like the idea of handing over known-broken stuff.

(The $1800 doesn’t include the $20 sandwich that I got for him at the bakery around the corner.)

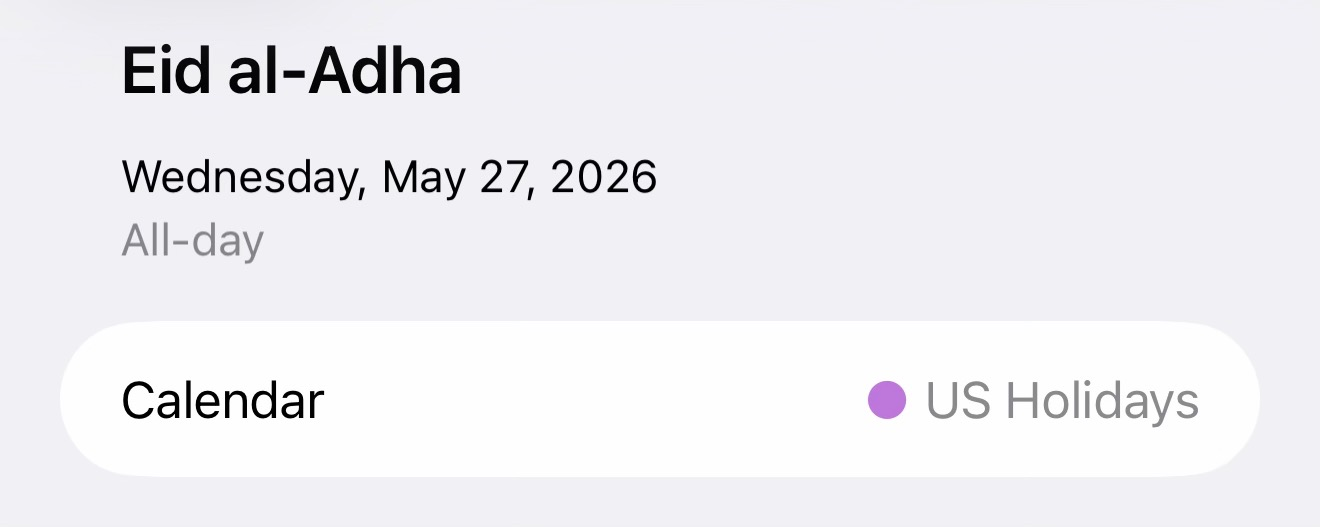

Today is Eid al-Adha, a “U.S. Holiday” according to Apple:

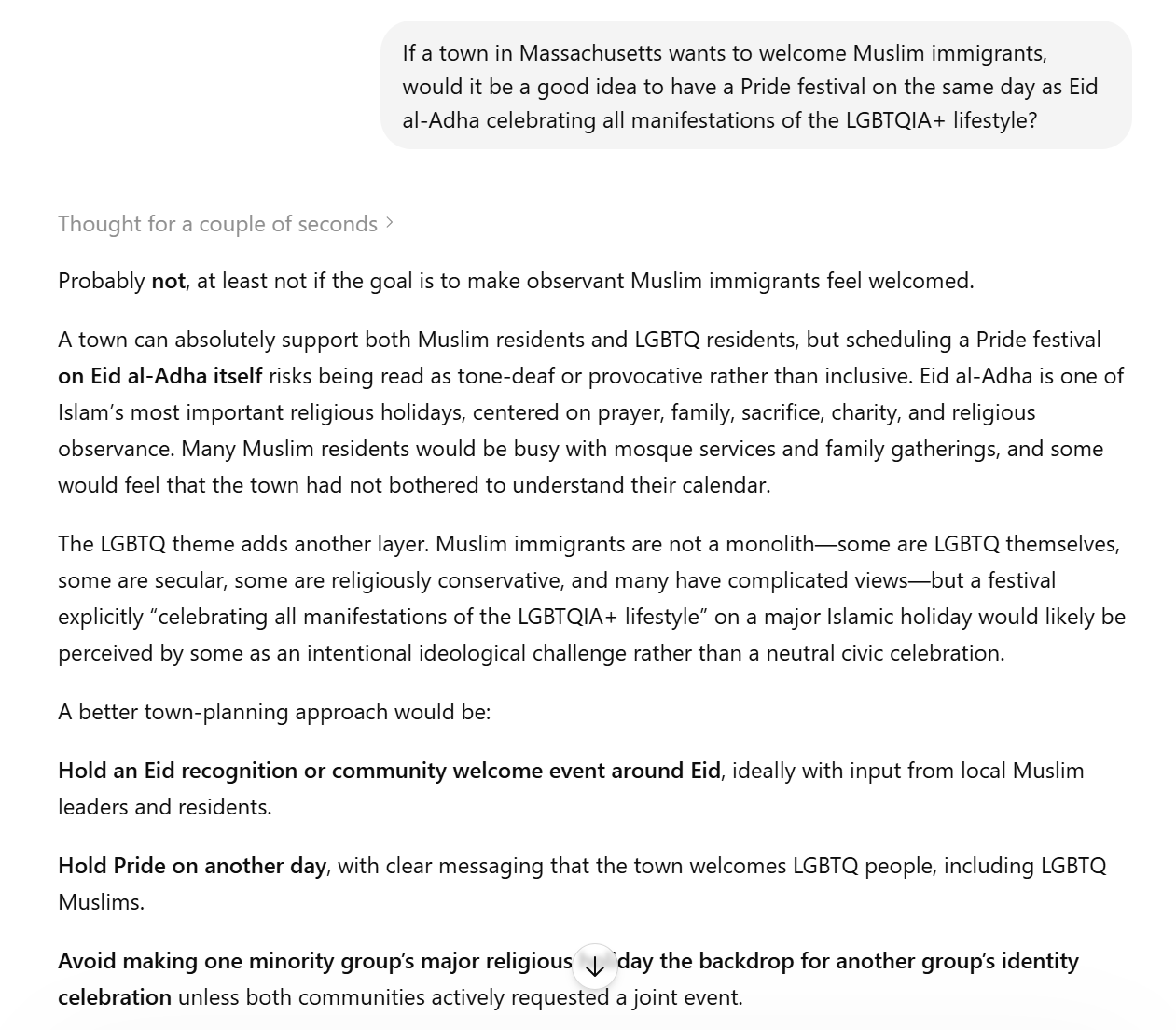

How do progressive Democrats choose to celebrate what Google AI says is “the second and holiest of the two main Islamic festivals”? They’ll be getting an early start on Pride because #OneFullMonthIsNotEnough (friend’s photo; he moved to Florida a year ago and is putting the finishing touches on unloading his house in Maskachusetts):

Note also that irrigation is limited to one day per week because, in what should be the wettest time of year, they’re already running out of water. (What do people with postgraduate credentials do in response to running out of a resource such as water? Promote accelerated population growth via low-skill immigration.)

What does ChatGPT say about this scheduling?

I asked for a clarification and received “my earlier “some are LGBTQ themselves” was about identity and lived reality, not a claim that orthodox Islamic law permits male-male sex.”

Asked if there is an “Islamic law” that isn’t orthodox and that does permit male-male sex, ChatGPT responds by citing a handful of individual writers who offered personal opinions on the subject, not proposed or adopted “laws” in any jurisdiction.

N.P. “Narv” Narvekar, the head of Harvard University’s nearly $57 billion endowment, recently told the endowment’s board he plans to retire, according to people familiar with the discussions. He has served nearly a decade in the post.

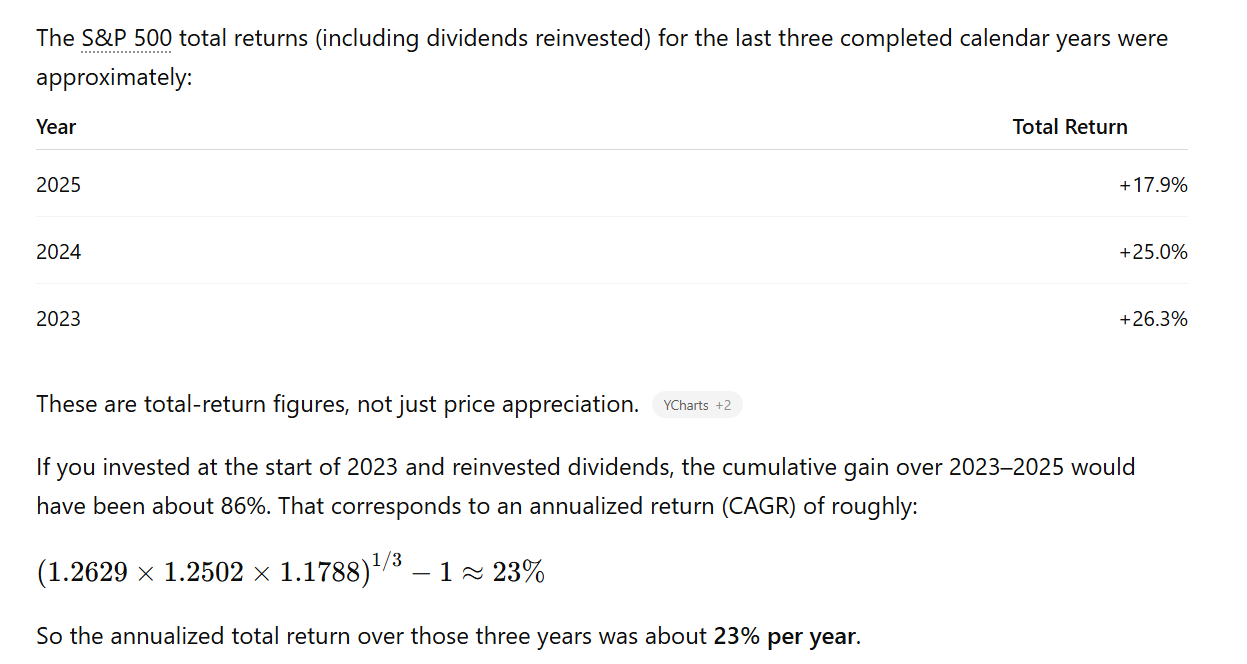

In the past three years, Harvard earned an annualized return of 8.1%, a rate that topped that of Ivy League rivals Yale and Princeton and which placed it in a tie for fourth among a group of 12 top schools, according to financial technology company Markov Processes International.

The Wall Street Journal doesn’t bother to ask Edward Tufte’s question, “Compared to What?” But ChatGPT can come to the rescue:

In other words, one can get paid $6 million per year for dramatic underperformance relative to the simplest imaginable investment strategy, dumping everything into the S&P 500 (a 23% annual return vs. the 8% achieved by Mr. Narvekar and subordinates). That’s a career almost as good as “receptionist in NVIDIA branch office”!

Reading to remember the sacrifices that some U.S. military personnel made during World War II: 81 Days Below Zero: The Incredible Survival Story of a World War II Pilot in Alaska’s Frozen Wilderness. When Seward bought the territory in 1867, nobody could have imagined that the interior would end up being useful for the yet-to-be-invented heavier-than-air military airplane, including the B-24 that Leon Crane was co-piloting in the crash that led to his fellow airmens’ deaths and his own remarkable survival.

Of course, most of the military deaths in Alaska occurred in the Aleutian Islands battles (see Justifying our total war against Japan for some Fairbanks museum exhibits on this subjectd). It’s tough from today’s perspective to see the military value of these fights, but we can still reflect on the memory of those who were willing to sacrifice their lives in the cold for the perceived value at the time.

I was in Juneau yesterday. Seward doesn’t look too happy about the future state that he purchased:

The Righteous of New York City love to talk about how they’re protecting our precious planet. Here’s their police department proudly displaying a video of perfectly functional mopeds being crushed rather than being sold and/or exported to a lower-income country:

The NYPD is crushing it when it comes to taking illegal mopeds and scooters off our streets.

So far this year, the NYPD has seized over 5,700 of these dangerous, illegal vehicles — and we are not letting up. pic.twitter.com/AJNnBCGsyq

Mayor Zohran Mamdani unveiled a whopping $124.7 billion executive budget for New York City on Tuesday – built on the back of $4 billion in funny money from Gov. Kathy Hochul.

The governor’s bailout – announced hours before the city budget’s reveal – was quickly criticized as a fiction used to help out her reluctant ally Mamdani as she faces re-election and pressure to appease the lefty mayor’s comrades.

If inequality haters in NYC actually do hate inequality, they shouldn’t want to receive any money from the state. (Same deal with Harvard University, which says officially that inequality is bad and then takes federal money that could have been spent at University of Michigan instead (U. Mich. is a poorer university than Harvard and located in a poorer state than Maskachusetts).)

Finally, let’s reflect that Mamdanism (steal from the rich; give to everyone else) is going to end up working beautifully because the rich won’t move out of NY and stop paying for whatever Ayatollah Mamdani and his sidekick Gov. Hochul dream up. The rest of the U.S. can reasonably vote for Mamdanism on a federal level after watching what a success it has been in NYC due to these elite tax cattle staying in place and paying.