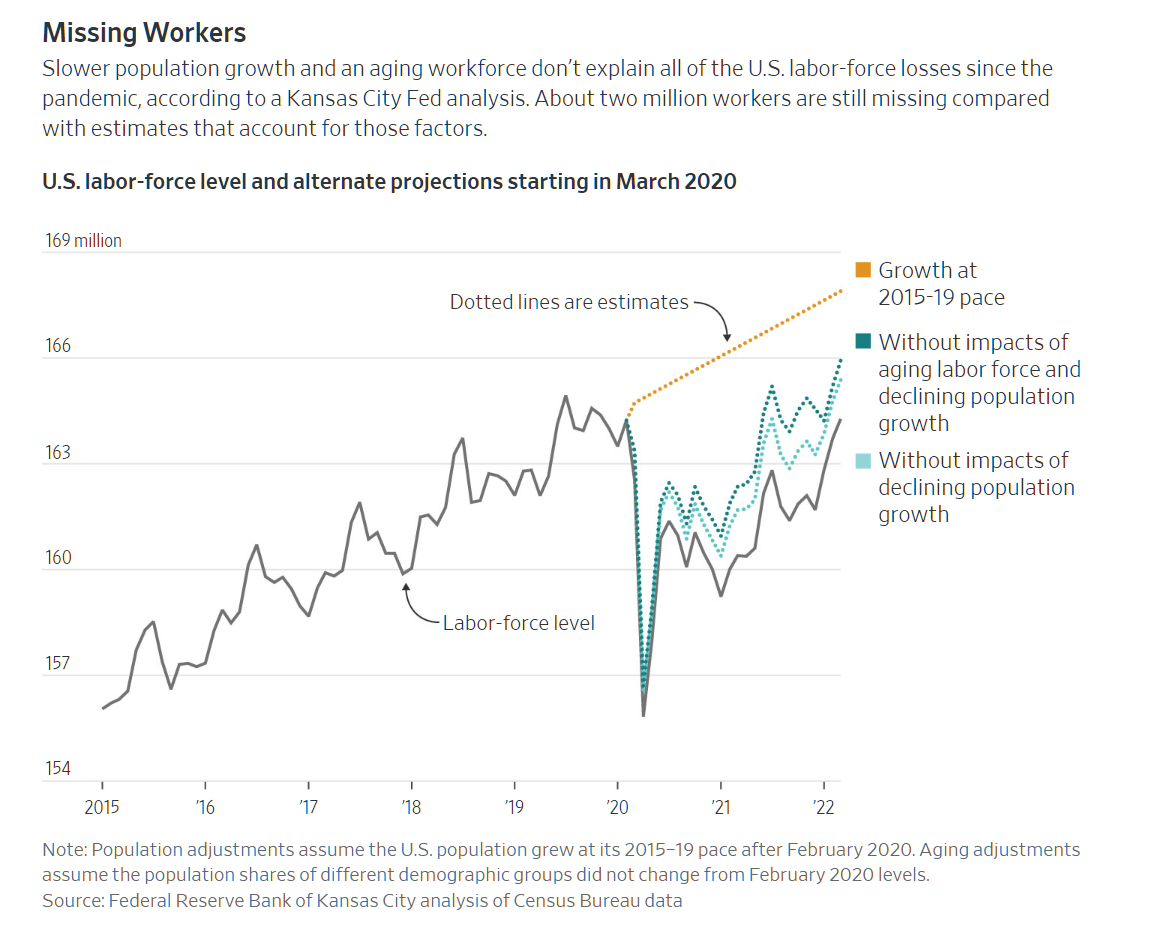

Pent-up inflation from low labor force participation rate?

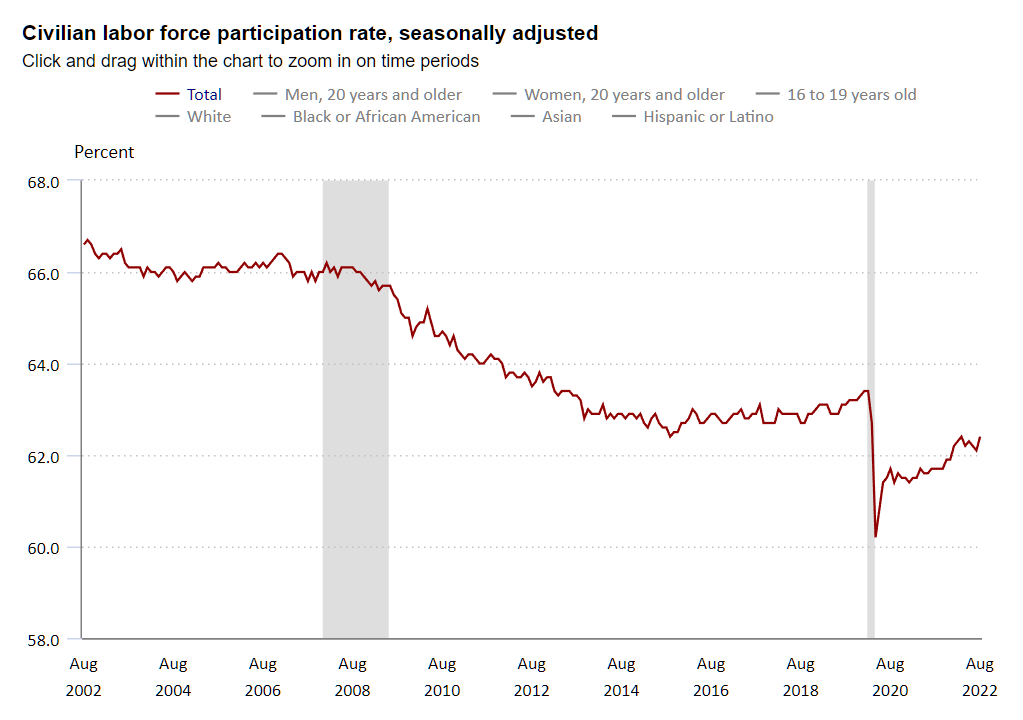

In the spring of 2020, the typical state governor ordered his/her/zir/their subjects to stay home and watch TV or play Xbox. A lot of us are still following the habits that we developed in 2020. The U.S. labor force participation rate:

A business executive with whom I talked in Oslo said “it takes three months to create a new habit,” which was his explanation for why a fair number of Norwegians haven’t returned to their pre-coronapanic work habits. (World Bank stats show that Norwegians are much more likely to work than Americans, with participation rates of 66 percent versus 61 percent. Part of this may be a difference in family law. It is not straightforward in Norway to live comfortably off a prior sexual relationship, either by alimony or child support. The country offers no-fault (“unilateral”) divorce, but anecdotally, profits are limited to about 10 percent of the defendant’s pre-tax income. Having sex with a high-income defendant and harvesting child support is even less lucrative.)

I’m wondering if there is some pent-up inflation that we’ve built into the U.S. economy by teaching people how great life at home with a plethora of screens can be. Getting Americans back to work at previous levels plainly will require paying them more than what employers are currently paying.

We saw evidence of this in every state that we visited this summer between Florida and Oshkosh, Wisconsin. A coffee shop near Great Smoky Mountain National Park:

Indianapolis:

A hotel manager in Oshkosh explained that he had to fly people in from Florida and Georgia to work during the peak EAA AirVenture week.

An airport manager retired in May 2021 and, as of July 2022, the city of Prairie du Chien had not been able to find a replacement at the wages offered (about $63,000 per year, plus benefits worth another $40,000 per year?):

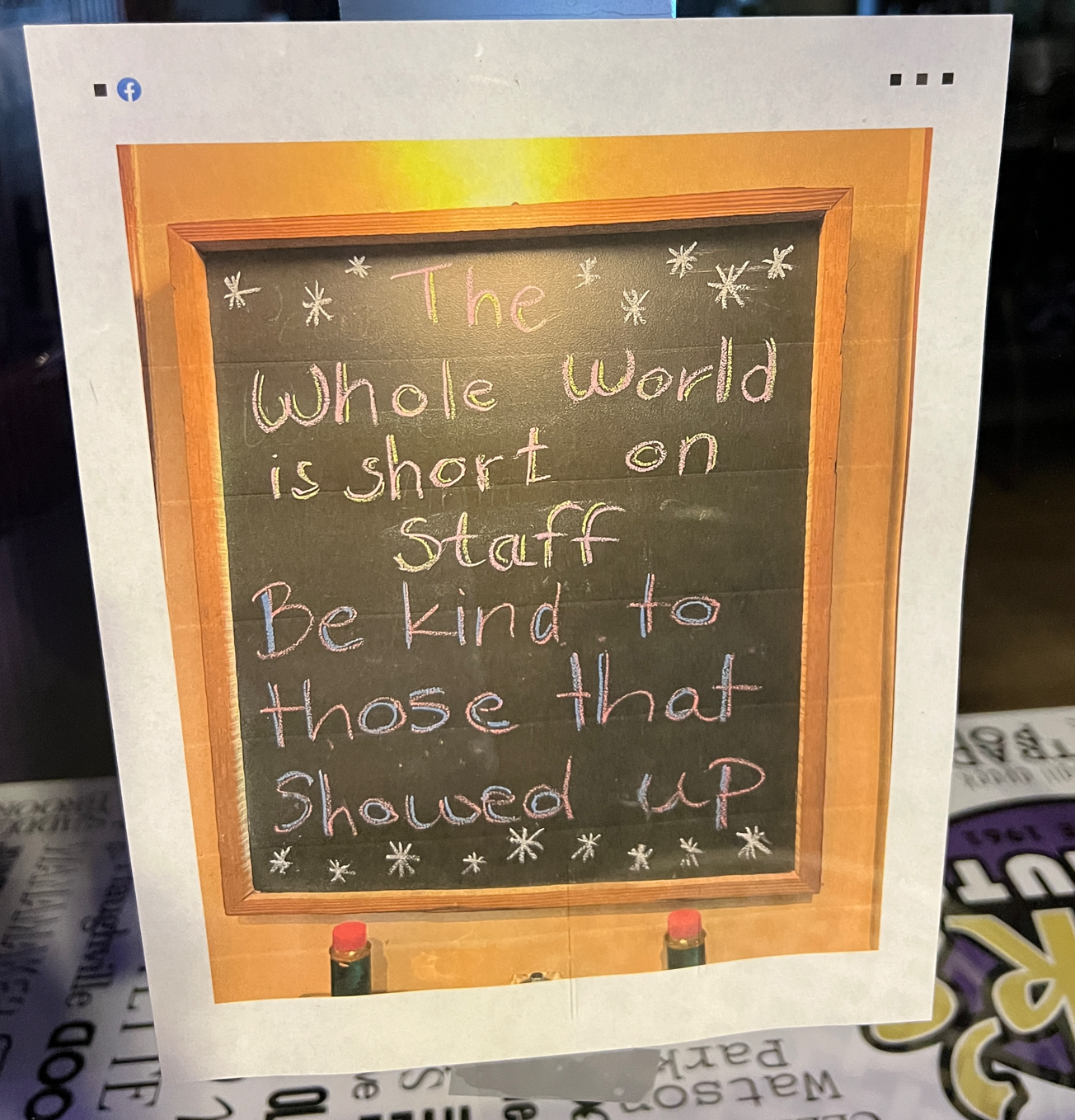

The saddest photo of all… a homemade donut shop with shortened hours in Chattanooga:

What do we think? Is there a round of inflation built into our society that is yet to hit us? Either employers will have to raise wages to get Americans off our couches or money will need to be borrowed/printed by the government to fund all of the means-tested benefits to which the couch-dwellers are entitled (raising tax rates is not an option, I don’t think, for increasing revenue because rates are already set to the level that maximizes taxes actually collected). Both of these changes would be inflationary.

(Norway, incidentally, has no help-wanted signs nor, as far as I could tell given my illiteracy, any apology signs. The locals say that service businesses are short-staffed and that quality has suffered, but that all recruiting is done online so customers won’t see signs encouraging job applications.)

Related:

- “Who Are America’s Missing Workers?” (NYT, 9/12/2022): “I could jump back in, but then I got used to being retired,” said Thomas Strait, who chose early retirement at the beginning of the pandemic. [moving from California to Florida] … men in their prime working years, from 25 to 54, have retreated from the work force relative to February 2020, while women have bounced back. [Is it men or women who love Xbox more?] … “A lot of workers are still disconnected, and we’re just not seeing them come on,” said Jesse Wheeler, an economic analyst with the polling and analysis firm Morning Consult. “It’s unclear how all of them are making ends meet, but I think it has a lot to do with consolidation of households and cutting costs. It would’ve been difficult to change if they weren’t forced into it.”

- Help-wanted ad from the University of California, Santa Cruz: The Critical Race and Ethnic Studies Department (https://cres.ucsc.edu/) at the University of California, Santa Cruz (UCSC) invites applications for a an Assistant/Associate Professor of Critical Race Science and Technology Studies (STS). … A demonstrated record of research that de-centers Western scientific ways of knowing and challenges extractivist capitalist practices is especially welcome as are commitments to queer and indigenous ecologies, trans-species studies, and race-radical approaches to STEM. … Ideal applicants will demonstrate an approach to science and technology grounded in histories of and innovative methods of analyzing anticolonial, decolonizing, liberationist political thought and praxis, … Document requirements … Statement of Contributions to Diversity, Equity, and Inclusion** – Statement on your contributions to diversity, equity, and inclusion, including information about your understanding of these topics, your record of activities to date, and your specific plans and goals for advancing equity and inclusion if hired at UC Santa Cruz. Candidates are urged to review guidelines on statements (see https://apo.ucsc.edu/diversity.html) before preparing their application.