My old neighborhood in Harvard Square was home to a 30-year-old sandwich shop whose workers took advantage of the coronapanic labor market to unionize in the fall of 2021. After 9 months of union bliss, they responded to Bidenflation by demanding higher wages. The employer’s counter-offer was to shut down entirely:

The popular Boston-area coffee chain Darwin’s Ltd. announced plans to close the store’s original Harvard Square location at the end of the month, prompting some workers to stage a protest at Cambridge City Hall on Sunday denouncing the move.

Darwin’s United — a union representing the chain’s employees — responded by organizing a protest at City Hall, where workers rallied on Sunday before gathering outside the Darwins’ Cambridge home.

“We have been offered no guarantees of jobs for those who want to stay, no guarantee that workers will have an income going into winter,” the union wrote in a Twitter statement. “We will not back down, we will not take this.”

At the rally, union members called on the Darwins to keep workers at the Harvard Square store employed if they wished to stay on and reiterated past demands for $24 per hour wages, three weeks paid time off, and zero-deductible healthcare for employees.

“We know that Steve has long been considering selling the business, but the timing really couldn’t be worse,” said Sam White, a Darwin’s United representative. “We’re telling him to come back to the bargaining table and respond to our proposals.”

A majority of workers at the four Darwin’s locations voted to unionize in September 2021 and began negotiations with management for a new contract for workers. Since then, talks have stalled, according to White. In March, workers at all four locations staged a mid-morning walkout to raise pressure on the owners.

Maybe things are more harmonious on the West Coast? The academics at UC Berkeley claim that they know what workers are entitled to and how to redress inequality in the United States. Yet their own workers had to go on strike to try to force the university to pay a fair wage. “University of California workers continue strike amid threat of arrests” (Guardian, December 10, 20220):

Tens of thousands of academic workers throughout the University of California are currently on their fourth week of striking for a new union contract and the situation is intensifying amid the threat of arrests after direct actions by some strikers.

The strike of 48,000 academic workers, including graduate workers, academic researchers, postdoctoral scholars and teaching assistants, began on 14 November and is the largest in the history of higher education in the US.

About 12,000 postdoctoral researchers and academic researchers reached a tentative agreement with the University of California on 29 November, which included pay increases up to 29%, but have continued striking in solidarity with other academic workers still pushing for a deal and while the agreement is put to the membership for a vote.

Graduate workers at UC have reported issues in affording rent, food and basic necessities in the cities they work and live in on salaries averaging about $23,000 annually.

If the politicians and academics in California are experts on fairness, why did their workers need to strike? University of California professor Robert Reich, for example, is fond of scolding America’s evil capitalists for underpaying workers. Why didn’t he pay his own slaves fairly?

Oil companies have already posted $127 billion in profit this year versus $42 billion over the same period last year.

Folks, inflation isn’t being driven by workers asking for better wages or government spending. It’s being driven by corporate greed.

Side Effects forces us to face up to – rather than ignore or deny – the realities of balancing the vast sums that can be spent on a single, seriously ill patient against the “distressing conditions in which many frail and elderly people live out their final years, often as a result of lack of adequate funding”. It is all too tempting, Haslam recognises, to dismiss as abhorrent the act of attaching a price tag to a person – as though their worth can be measured in pounds and pence. A human life, surely, is priceless? No amount of mere money or stuff comes close? But anyone who is actually involved in the real, messy world of healthcare knows full well this is nothing but rhetorical posturing.

Later that afternoon I was talking to a guy who is married to an emergency medicine doc in London. With the cost of living adjustment, she can expect to earn 80,000 pounds per year (i.e., $80,000!) after 15 years of slavery for the NHS (age 40). “A train driver will earn more,” he noted, “because their union is actually effective.”

Who is smarter than the Brits for running a universal health care system that doesn’t bankrupt everyone? Africans! “Middle class Nigerians who need any kind of advanced medical treatment will come here on a tourist visa,” my friend explained, and go straight from Heathrow to an NHS hospital. Once they’re in the system they get treated just like anyone else. After consuming what might be hundreds of thousands of pounds in services and recovering, they go back to Nigeria.”

What else did they have in the bookstore? It’s “smart thinking” to fight structural racism:

An American hero who inspires Biden voters can also inspire the British:

Although the age of consent in the UK is 16 (e.g., a 16-year-old could consent to have sex with a rich guy after a Gulfstream flight to somewhere luxurious) and prostitution is a legal career for an 18-year-old, the British are apparently shocked about what Jeffrey Epstein was allegedly up to:

Anyone who isn’t a cisgender heterosexual white male is in trouble:

England was saved from German invasion by women of color who were willing to risk their lives in combat while white men relaxed in the safety of their country homes:

Despite the fact that some heroines exist, the entire Earth is, literally, toast because of those who Deny the Science (i.e., unlike World War II, this is not a war that can be won by women alone):

An entire section of the front of the bookstore was devoted to a personage who by right should have been King of England and was denied this position purely on account of her gender ID:

Circling back to the British health care system… if we aren’t willing to use death panels or at least a quality-adjusted life year calculation the way that the Brits do, how are we going to keep health care from growing to consume 25 percent of American GDP (a shrinking quantity in the aggregate and, since the population continues to grow via immigration, an even more dramatically shrinking quantity on a per-capita basis)?

There’s a sports car dealer next to our favorite taco place here in Jupiter. Their lot was jammed with cars, seemingly twice as full as in the summer. From their perspective, the car market turned about 30 days ago. They’re now paying only MSRP for nearly-new (500-mile) C8 Corvettes. What do they turn around and sell them for? It’s a little unclear because they say “We haven’t had a call for a Corvette in 3-4 weeks. The interest rates have killed demand.” (Note that this is contrary to my theory that we have enough deficit spending and inflation-indexed spending to have inflation even if nobody does any borrowing; see Can our government generate its own inflation spiral? and Economist answers my question about high interest rates and high deficits.)

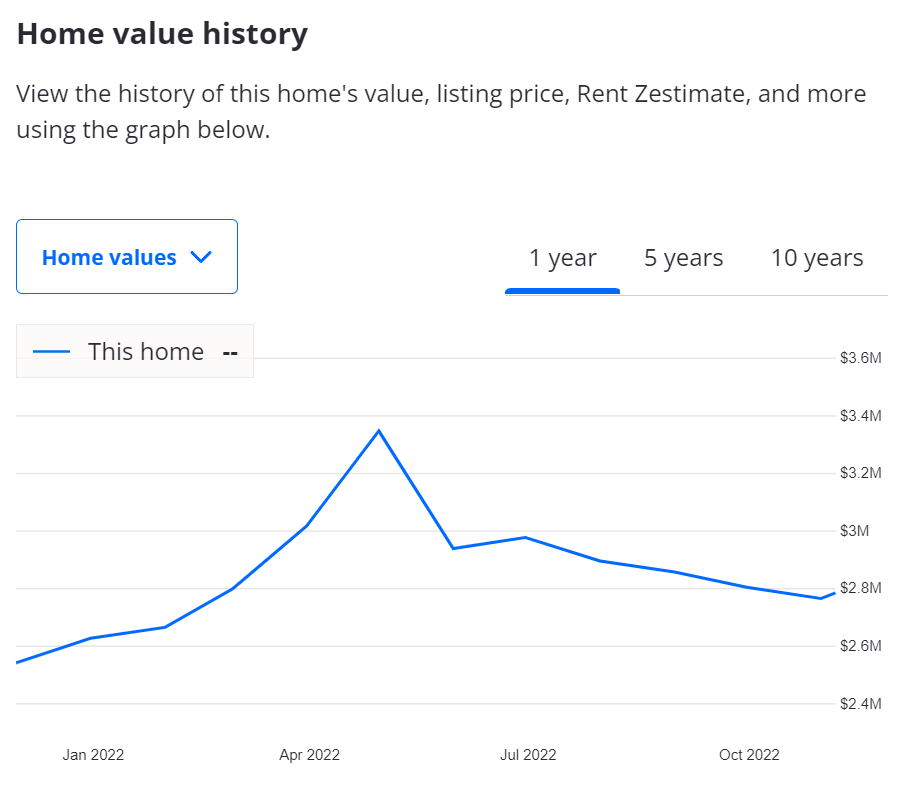

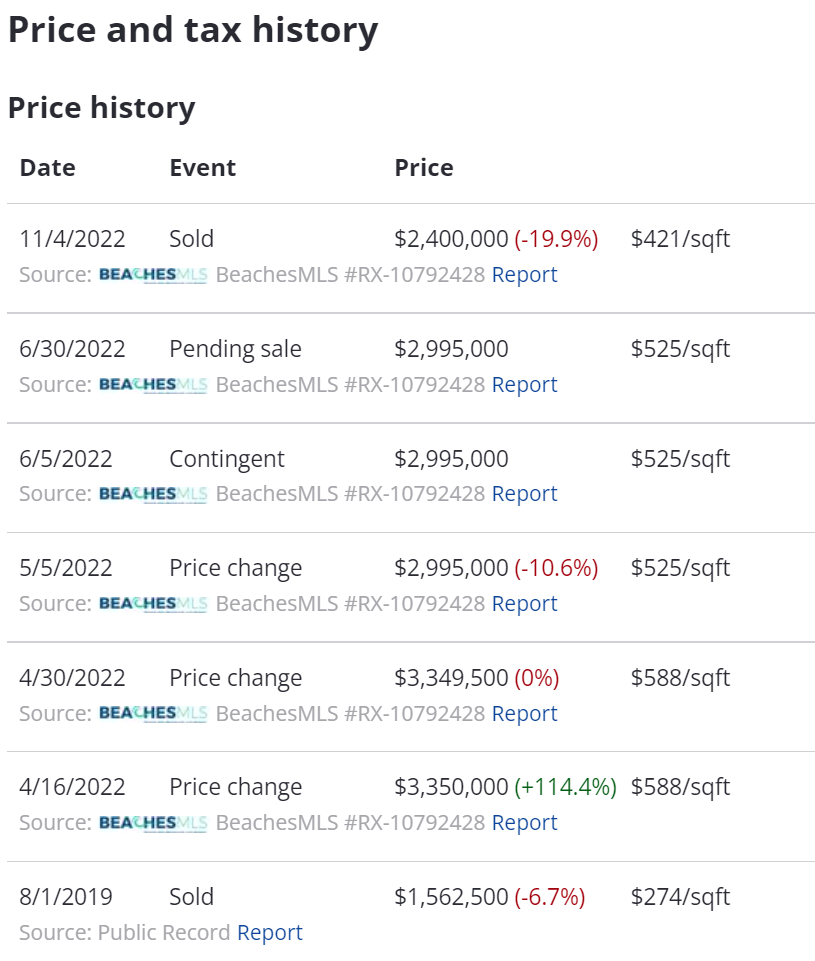

How about real estate? There’s a house in our neighborhood (built by the MacArthur Foundation for middle-class and upper-middle-class people!) whose $3.35 million asking price in April 2022 seemed aggressive, particularly since there was no pool and the new owner would have to lease it back to the sellers until October when the sellers expected their new-built house to be ready.

Here’s the “value history”:

In June 2022, there actually was a greater fool who agreed to pay $3 million for this albatross. But then it seems that this person disappeared or wised up and the closing price was $2.4 million (last week):

If you’re depressed because you forgot to sell all of your assets in March 2022, this message from the taco place might be useful:

If you’re depressed because you were dumb enough to buy a house early in 2022 at early-2022 prices (looking in the mirror is painful!), you can be comforted that you don’t live in San Francisco, which MSNBC uses as shorthand for a truly crummy and crime-plagued urban environment (the MSNBC interviewer says, regarding a higher-crime Manhattan, “We’re worried this could be San Francisco”):

Even MSNBC is calling out Democrat Kathy Hochul.

"Here's the problem: We don't feel safe…I walk into my pharmacy, and everything is on lockdown because of shoplifters. I'm not going in the subway. People don't feel safe in this town." pic.twitter.com/JUKhxXCk4c

Joe Biden’s economic policy seems to follow the same logic as that used by my 88-year-old mom’s circle of friends. These women are generally innumerate, despite having enjoyed elite educations, because they took their last math class in high school and, as stay-at-home wives, could enjoy afternoons at the theater rather than reviewing accounting reports or doing the other tedious stuff with numbers that is required to earn money. They believe that the U.S. has an infinite supply of wealth, partly because Asians are inferior to Americans in creativity and, therefore, cannot truly compete with us. Due to the fact that our wealth is infinite, there shouldn’t be any limit to what the government can spend. Any spending program that might help at least one American, therefore, should be approved.

Joe Biden seems to hold similar beliefs, but what about the professional economists who have been advising him on his Inflationary Journey? Jerome Powell, chair of the Federal Reserve, must be one of the world’s leading experts on macroeconomics, right? Wikipedia says that his/her/zir/their degrees are in “politics” and law. I.e., there was no formal training in economics behind “Fed’s Powell says high inflation temporary, will ‘wane’” (AP, June 2021).

The Chair of Biden’s Council of Economic Advisors is Cecilia Rouse. In May 2021, she characterized inflation as “transitory” and “temporary” (Reuters). Here she is in June 2021 doubling down:

“As supply chains ease, as people get back to work, as we normalize our economy, the price pressures will start to ease,” said Rouse, who’s on leave from her post as a Princeton University economics and education professor.

Rouse called the coronavirus the biggest, ongoing threat to the U.S. economy — one that could upend Americans’ willingness to take jobs, travel and spend money on activities like dining out. It’s still too early to know the ways in which the new variant called omicron could affect the U.S. economy, she said.

(It is not politicians ordering lockdowns and school closures that are threats to the economy, but SARS-CoV-2 itself.)

She’s 58 years old so at least has the potential to not be senile. On the other hand, Cecilia Rouse seems to be a specialist in labor economics, a potentially irrelevant specialty given a country where the long-term trend is people preferring not to work:

Google Scholar shows this top advisor’s papers. A sampling:

“Orchestrating impartiality: The impact of blind auditions on female musicians” (possibly flawed; see also this critique)

“Diversity in the economics profession: A new attack on an old problem”

“Constrained after college: Student loans and early-career occupational choices”

“The Costs and Benefits of an Excellent Education for All of America’s Children” (Science says that the obvious answer is to close schools entirely for 12-18 months, particularly anywhere that Children of Color are to be found)

The Fed has raised its primary credit rate by 3 percent compared to the spring of 2022 (this chart doesn’t show today’s bump):

If the Fed recognized back in the spring of 2022 that low interest rates plus wild deficit spending was a toxic combination, thus leading to the 0.75 percent bump in June with forecast additional bumps, why didn’t it increase the rate to today’s level immediately? If you want to stop inflation, and convince markets that you’re serious about the effort, why keep lending money at an interest rate dramatically lower than the inflation rate?

The obvious answer is “Philip, you’re an idiot who took a few graduate level econ courses; Fed chair Jerome Powell is a brilliant macroeconomist who knows what he/she/ze/they is doing.” The problem with that answer is Wikipedia says that Mx. Powell has no formal training in economics. He/she/ze/they studied politics and then law. While it is still a safe bet that I don’t know anything about economics, it is also possible that Jerome Powell has no better insight into what will happen with inflation.”

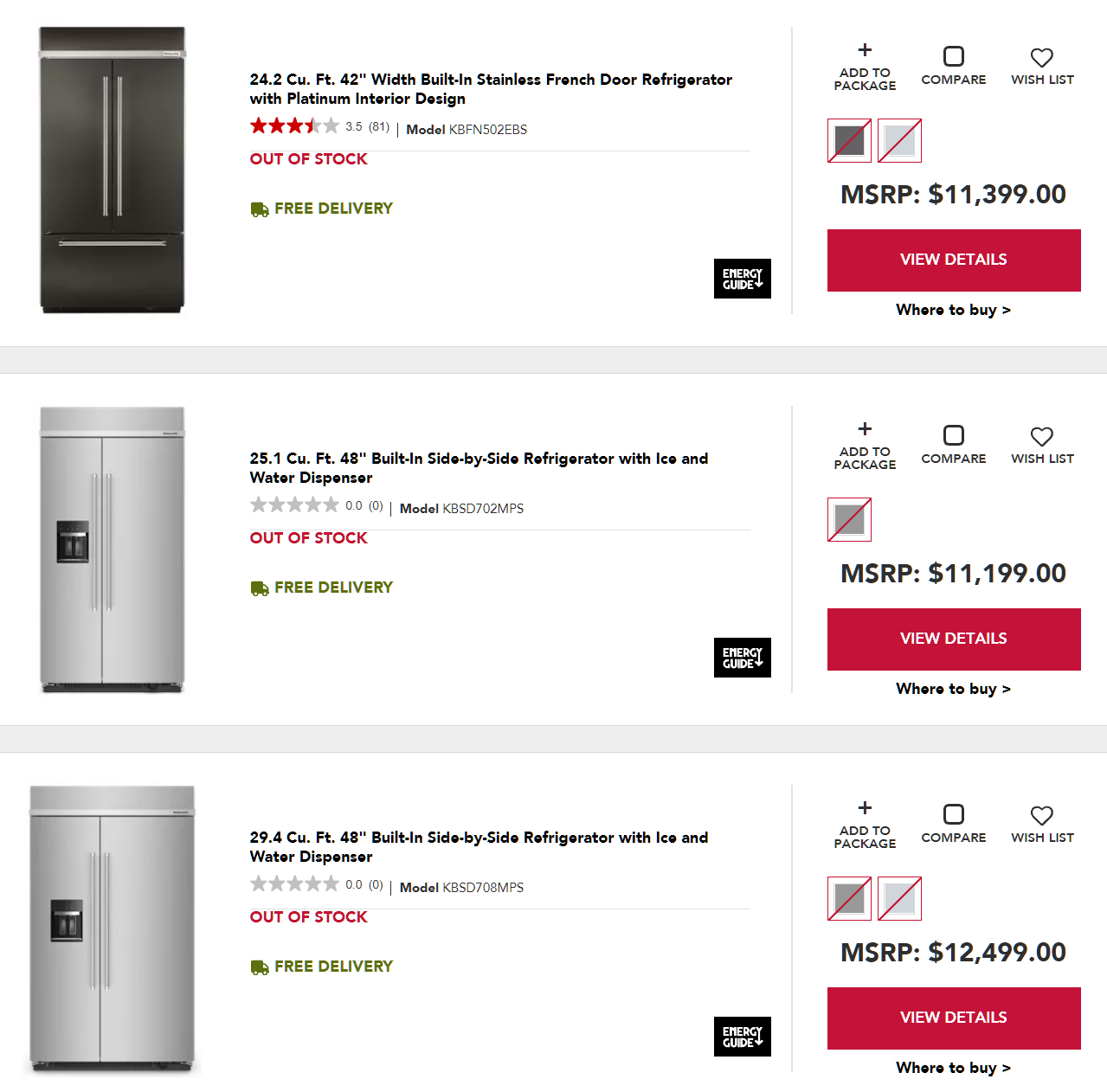

I think that there is plenty of room for continued inflation in the U.S. economy. Now that higher mortgage rates make buying a house more expensive, landlords shouldn’t feel dramatic pressure to cut rental rates (though, presumably, they did get a little ahead of the market in the spring). There should still be steady demand driven by immigration and the resulting higher rents will ensure the continued misery of the working class that was forecast back in 2016 by a Harvard economist. After rent, cars are a big expense for Americans. A neighbor shopping for a Honda was told that it would be $6,000 over dealer cost and that he might have to wait a month. Those aren’t better terms that what I learned about in the spring of 2022 when getting an oil change for our beloved Odyssey. Let’s look at appliances. We recently priced a Sub-Zero refrigerator to replace our dying 42″-wide KitchenAid. The Sub-Z is plainly underpriced at $14,000+ (including sales tax and installation) because there is a one-year wait (in 2019 it was a 7-10-day wait). Why not buy another 42″-wide KitchenAid and then wait for that one to die? The cost would be closer to $12,000, but they are also out of stock, which means the correct price is higher.

Maybe the downturn in real estate occasioned by these higher interest rates actually will do enough damage to the economy to stop hyperinflation for 2023. But that leads us right back to the question above: Why didn’t the Fed do a full 3 percent raise back in June and stop hyperinflation perhaps 6 months earlier? (Presumably we’ll still have inflation of at least 2 percent, just not hyperinflation!)

Related:

Can our government generate its own inflation spiral? (since everyone in the government half of the economy gets an inflation-indexed paycheck, folks in the non-government half will need to be nearly ruined before inflation is whipped)

“Why the Federal Reserve has made a historic mistake on inflation” (Economist, April 23, 2022): “America’s Federal Reserve has suffered a hair-raising loss of control. … the worst overheating in a big and rich economy in the 30-year era of inflation-targeting central banks.”

There has been a lot of drama in the currency and bond markets regarding the new UK government’s economic policy, which sounds like it is along the lines of what the U.S. did in the 1980s. President Ronald Reagan proposed shrinking government with spending cuts so that tax cuts could be implemented; Congress agreed to the tax cuts, but refused to cut spending and the result was massive deficits, which eventually faded due to economic growth.

The UK government is already somewhat leaner than what we have in the U.S. Heritage says that the UK government consumes 42 percent of GDP, which is a touch higher than the US government (39 percent), but the UK figure includes nearly all health care spending. If we add government-mandated-and-regulated “private” health care to the US number, we get closer to 50 percent of GDP.

The business folks and investors with whom I spoke in the UK were generally positive regarding Prime Minister Truss‘s plan, which they felt would deliver a substantial amount of growth. They attributed much of the hatred and hysteria to an anti-Conservative press. On the other hand, hatred and hysteria in currency and bond markets isn’t usually driven by whatever the Guardian has to say.

One part of Truss’s plan seemed insane to me, i.e., preventing consumers from seeing that prices for energy have gone up. But the French are also doing it. Wholesale electricity prices are up 5X and consumers are paying… 1X. Party On with printed money.

Britain is the only Group of Seven country with a smaller economy today than in the fourth quarter of 2019, before the coronavirus pandemic. In the 40 quarters preceding the pandemic, its economy grew at an annual rate of less than 2 percent more than half the time.

Maybe a country where all of the young people get stumbling drunk every night at the pub isn’t ideally situated for growth?

The government’s tax plan would cancel a scheduled increase in the corporate tax rate to 25 percent from 19 percent and would make permanent a temporary increase in the annual investment allowance, letting businesses deduct the full cost of qualifying plants and machinery up to 1 million pounds in the first year.

This sounds reasonable to me! With a 25 percent rate, a company would have to be crazy to refrain from pushing all of the profits into Ireland (12.5 percent rate and full membership in the EU if frictionless trade with Europe is required). The depreciation simplification should front-load investment and activity and shouldn’t change the tax owed in the long run (spending one million pounds will yield one million pounds of deductions against revenue).

The most questionable parts of the plan are the income tax cuts. Reducing the basic rate of income tax by one percentage point, to 19 percent, will fuel consumption at a time when the Bank of England is attempting to curb inflation.

The prime minister’s proposal to eliminate the 45 percent tax bracket on incomes above 150,000 pounds per year — the top 1.1 percent — was also unwise in the current fiscal and economic environment, …

I’m not sure that a 45 percent rate is revenue-maximizing. At that rate, a Brit would get a great return on pushing activities offshore or structuring activities to get the 10 percent entrepreneur’s rate. The U.S. government is greedy for money and the top personal income tax rate is 37 percent (which works out to 37 percent in Florida or 50.3 percent in California).

It looks like the markets are locking Britain into the same policies that put it on the slow bus to economic mediocrity. Given some reasonable value placed on leisure and drunkenness, the decision to forgo the second job or language study and spend the evening in the pub with friends will be a rational one. For those who are ambitious, the decision to emigrate will likely be a rational one (one of our neighbors in Florida recently arrived from the UK, having accepted a transfer within a multinational industrial products company (held up for more than a year due to coronapanic restrictions on non-walk-across-the-border-and-claim-asylum immigration); he will do the same thing that he did in the UK, but for a much larger market).

What am I missing? My default assumption is that markets are right, but I can’t figure out what is so terrible wrong with the latest British government’s plans. Is part of the explanation that the pound isn’t the world’s reserve currency and therefore the consequences of deficit spending are more severe than they are for the U.S.?

Separately, how can a country full of midgets and randoms fail to thrive?

If you tried to put out a fire with water, and the fire got no smaller even after 3 attempts, you’d hopefully realize this is no normal water and/or this is no normal fire. And if you were able to come to this conclusion, you would not be the Fed.

My response was “I think the government may itself be the inflation spiral. Government is nearly half the economy and everything the government pays money for is indexed to inflation. Medicare, military and similar contracts, Social Security, pensions, employee salaries, etc.”

If everything that is part of the local/state/federal government sector is indexed to inflation, doesn’t that mean that inflation goes down only if horrific pain is being inflicted on those dumb enough to be in the private sector? If government workers are getting cost-of-living adjustments (COLA), their spending power by definition cannot change (assuming that the BLS is calculating the CPI correctly). If the CPI says prices went up by 10 percent, the government workers will have 10 percent more in salary to go chasing after a mostly fixed supply of goods. This is the classic wage-price spiral.

Government is not 100 percent of the U.S. economy, so maybe the wage-price spiral can be broken if significant spending power reductions are imposed on non-union non-government workers. But at some level of government control of the economy, the spiral should be unbreakable regardless of interest rates and regardless of how poor the private sector chumps become.

(Why “non-union”? Union workers typically would have an automatic COLA increase and we could also consider union workers part of the government sector because they depend on the government to sustain their union power.)

Loosely related… prices and government worker wages go around in the Bois de Boulogne:

Related:

“Inflation Is Unrelenting, Bad News for the Fed and White House” (New York Times, today): “This is a self-inflicted wound that will impact the most vulnerable members of our society the most,[” said Mohamed El-Erian] (I think that El-Erian is saying what I say above, but more succinctly; everyone involved with the government will be 100 percent protected from inflation, which means that the peasants are going to be destroyed to keep those affiliated with the government from feeling any pain)

“Retirees Catch a Break With the Social Security COLA” (WSJ): On Thursday, the Social Security Administration said recipients will get an 8.7% increase in their payments next year and, for the second year in a row, that actually exceeds estimates of how much their costs increased. That is according to a 35-year-old initiative to measure the true rate of inflation facing those over 62, via an experimental consumer-price index produced by the Labor Department’s Bureau of Labor Statistics, known as the CPI-E; the E stands for “elderly.” … This year, the COLA was 8.7%, more than the 8% rise in the CPI-E.

Here in Paris, I met a guy who works in real estate development in Los Angeles. Assuming that you’ve already got the land, what does it cost to build a McMansion-grade house? “$500 per square foot,” he responded. How about an apartment building for the middle class? “Closer to $400 per square foot,” was the answer (same as levelset.com). So the 2,500-square-foot house costs $1.25 million to build and the 1000-square-foot apartment will cost $400,000 to build… assuming that land is free.

“Rents have a long way to go up before they cover these kinds of costs for new construction, plus the land and all of the permitting,” he said.

I am not sure how California is going to house all of the migrants that it says it wants to welcome. How many folks who show up in the U.S. not speaking English will earn enough to pay $2 million for a house (construction plus land costs) or $600,000 for a condo (construction plus land costs)? At current interest rates, the nerdwallet calculator says that a Californian earning $200,000 per year can afford a $675,000 house (Census.gov says that median household income in California is less than $80,000 per year).

From these same folks, I learned that the cost of a suite in one of Paris’s nicer hotels is normally $2,800 per night, but they were paying $2,100.

the venue where the conversation happened, a house that would cost a lot more than $500/sf to replicate. Note the visitor using a cloth mask to protect him/her/zir/theirself against an aerosol virus in one of the world’s most crowded indoor environments whose ventilation system was put in by Louis XIV and got its last significant upgrade in 1698. Was the trip to Versailles actually necessary or could he/she/ze/they have stayed home and saved lives?

cloth masks again… outside in the bright French sunshine:

and, because I know Mike will want to see this, one last Warrior for Science in a hall depicting heroes in various French battles (note failure to shave beard while attempting to seal out aerosols with a mask):

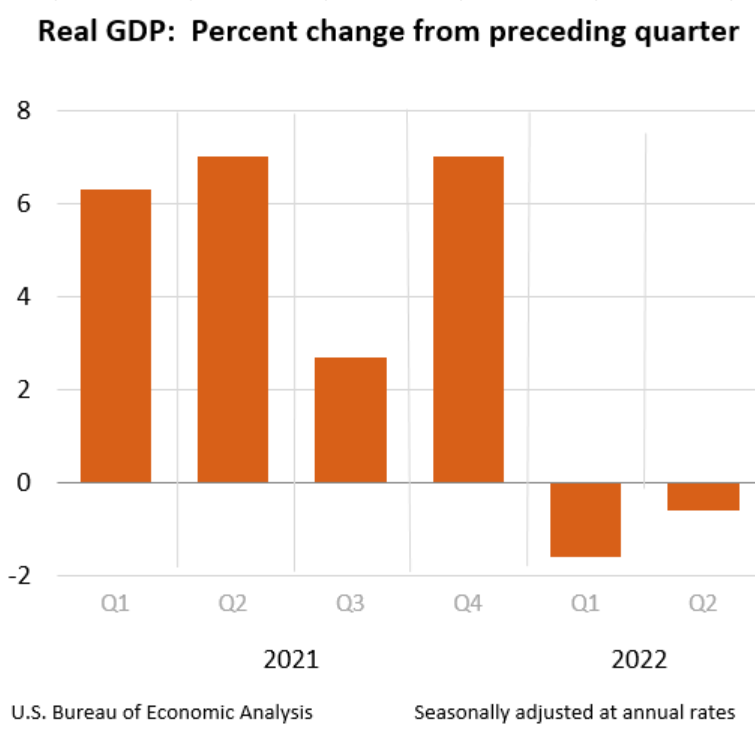

At the end of September, BEA will update five years of U.S. gross domestic product and related statistics, as well as GDP statistics for industries and for each state.

Maybe we’ll get some insight into how badly we fooled ourselves in imagining that people sitting at home scrolling Facebook and playing Xbox were as productive as if they’d continued to go to the office. The latest from the BEA:

Speaking of fooling ourselves, let me recommend The Lost Bank: The Story of Washington Mutual – The Biggest Bank Failure in American History by Kirsten Grind, a Wall Street Journal reporter. The Collapse of 2008 has been covered at a high level in a lot of books, but this one manages to touch on all of the big issues in the context of a single enterprise and group of people. As with “A single death is a tragedy; a million deaths is a statistic,” a narrative about one company is more compelling and easier to follow than a story about the entire U.S. economy.

The book explains how our modern world of a handful of enormous banks came to be. When there are no limits on how big a bank can get, small variations in bank health lead to enormous concentration. Due to being slightly larger, WaMu might have slightly lower costs per customer than a smaller bank, e.g., with information systems being spread across a larger base, thus making an acquisition sensible on both sides. WaMu would buy banks after the CEO got sued for divorce, leaving the target without effective leadership while the CEO was defending the lawsuit. WaMu would ultimately buy banks to feed its own executives’ egos, particularly Kerry Killinger’s, regarding its size rank among U.S. banks (when you’re #4, the desire to become #2 or #1 becomes tough to resist).

The book explains the roots of the Collapse of 2008. At a high level, the book identifies the following culprits:

the federal government, starting with Bill Clinton, pressuring banks into lending big money to Americans with low income and bad credit history to serve a social justice goal of achieving a desire mix of skin colors among borrowers (regulators could simply shut down a bank that didn’t lend enough money to the groups of interest to the government)

Fannie Mae, which abandoned its insistence on high quality mortgages and, partly due to pressure from the government, started buying low quality mortgages issued to home buyers/flippers who could not be expected to pay back loans if house prices flattened

New York City, whose investment banks sold mortgage-backed bonds to investors worldwide and, also, those investors. The book describes people on the ground at subprime lenders, e.g., Long Beach Mortgage (acquired by WaMu in 1999), recognizing that the borrowers would never pay but assuming that if Wall Street kept buying the mortgages the investors must know something that they didn’t.

California, where most of the fraudulent practices originated.

the issuance of complex variable rate mortgages, such as Option ARM, to consumers who lacked the sophisticated or, in many cases the English language skills, to understand them (it didn’t help that these folks had the financial capacity only to pay the initial teaser monthly payments and were guaranteed to default if a house price didn’t go up enough to enable a refinance; Federal regulators at the Office of Thrift Supervision approved the practice of issuing a $4000/month mortgage to a consumer who could afford only the $1000/month teaser rate)

As in Bubble in the Sun book: even those with the best information can’t predict a crash, those on the inside did not always see crash coming. In early 2007, for example, as investors were fleeing from high-risk mortgages and as some of his junior executives warned of impending doom, Kerry Killinger tried to buy a huge California-based subprime lender, Ameriquest, which went bankrupt shortly afterwards. Questioned regarding why he would want to pay for Ameriquest while the crash appeared to be underway, Killinger responded “They don’t ring a bell at the bottom.”

The book is a great lesson in what we might call “success disease.” Executives who take risks when everything is going up imagine that they have some special talents. Like individual investors in high-beta stocks, they don’t risk-adjust their high historical returns for the fact that they took a lot of risk and that it could easily have gone in the other direction.

The book answers the question Why did banks work so hard to lend money to people who obviously weren’t going to pay? Due to the higher interest rates on subprime, and the assumption that almost all of the low-income folks who took out subprime loans would actually pay, it was 5-10X more profitable to lend money to someone with no job than it was to lend money to a person with a job and a history of paying his/her/zir/their bills. The book doesn’t say so explicitly, but this also explains why banks couldn’t easily abandon their subprime practices in 2005 when the problems were already obvious. If they had done so, they would have needed to fire half of their employees (since the revenue from being a mortgage lender to those who could actually afford houses was such a small fraction of the subprime revenue stream).

Those passionate about social justice will be pleased to learn that the one voice of praise from a shareholder at the April 2008 meeting was from a Ph.D. economist who was also and employee. She expressed confidence in the Board and executive team, thanking them for their focus on diversity in hiring and lending to minorities (“community”). WaMu had recently rejected an $8/share buyout offer from J.P. Morgan Chase and also recently obtained $7 billion in smart money from the private equity geniuses (WSJ, Sept 2008 describes all $7 billion being lost). The private equity investors got half the company and let the Board and executives keep their jobs.

The book is also a cautionary reminder that it can take a while for bad decisions to work their way through the system. The California-style lending practices first reached the rest of the U.S. perhaps in 2003. It wasn’t until four years later that the subprime lenders began to go bankrupt, in mid-2007. And it was more than a year later before the broader U.S. markets and economy collapsed. If you think that U.S. economic policy has been misguided since March 2020 (as I do, because the rewards have been tilted in favor of those who don’t work or who engage in counterproductive activities), it could be a few years before the consequences of this policy become apparent.

Don’t forget that a disaster for ordinary folks, investors, etc. may be only a minor problem for the executives who caused the disaster. Kerry Killinger took so much money out of WaMu on the way up that he could pay off Wife #1 while also building and enjoying a dream lifestyle with Wife #2 that apparently persists to this day. The Latinx subprime borrowers lost everything, but Killinger still had his collection of $6 million houses (worth $20 million each today?). Killinger’s epic risk-taking would have been rational, even with full advance knowledge that it would render the bank’s shares worthless. If he had managed the bank conservatively, nothing dramatic would have happened either to the shares or to his own net worth.

Nationalizations. Subsidies. Cash handouts. Price caps. Profit taxes. It’s back to 20th-century economics in Europe.

Governments are resorting to old-school solutions, long dismissed as bad policy, throwing vast amounts of money at the energy crisis engulfing the region, in a bid to avert a political, social and economic meltdown.

In response [to rising energy prices], E.U. governments have already earmarked more than $350 billion to subsidize consumers, industry and utility companies; ministers are to meet on Friday to finalize the bloc’s direct intervention in markets to grab excess profits, cap electricity prices and subsidize utilities companies.

The huge public spending is in addition to a nearly trillion-dollar stimulus package adopted over the past year to deal with the economic fallout from the pandemic, mostly through borrowing. The ballooning debt load would have normally caused an uproar in the bloc, where fiscal conservatism has dominated policy and politics for years.

“This is clearly an exceptional and one-off situation,” said Daniel Gros, a German economist and director of the Centre for European Policy Studies, a Brussels-based think tank, who normally takes fiscally conservative positions. “It’s different from increasing unemployment or social benefits structurally forever, and it’s a special situation that won’t last forever.”

The last paragraph is my favorite. Coronapanic was exceptional, so borrowing/printing and spending $1 trillion (amateurs! the U.S. spent $10 trillion) in 2020/2021 was okay. The rise in energy prices is 2022’s exceptional event, so borrowing/printing and spending another $1 trillion will also be okay. The end of the paragraph is also interesting. The U.S. actually did make “structurally forever” changes to the American welfare state, already the world’s 2nd largest (percent of GDP), the free-forever broadband benefit for those who choose not to work and King Biden’s forgiveness of student loans previously owed to the Crown. According to the Germans, therefore, we are headed for disaster.

Eurocrats seem to think that voters won’t notice the subtle inflation tax caused by these programs and/or future standard tax increases. They’re paying subjects with their own money:

The Belgian government has handed out $100 to every household irrespective of income.

This is a fascinating example of human psychology. Europeans will eventually have to pay for all of the energy that they’re consuming in 2022 and they’ll have to pay the 2022 price. But they’re going to be happier paying starting in 2023 if the government gives them a Three-card Monte game to watch in 2022. And they’ll be happier getting a pay cut via inflation than getting a pay cut in nominal euros.

What’s non-EU-member Norway doing, other than getting insanely rich from the war in Ukraine? The nation’s hydroelectric power is being sold at record prices to the rest of Europe. The oil and gas wells are producing unprecedented gushers of money. Consumers have to pay higher prices for natural gas, but the government steps in and pays, using the record revenues coming in for oil and gas, 90 percent of the amount over a set price. Cruise ships that formerly stopped in St. Petersburg now come to Oslo for two days per sailing, paying enormous port fees and buoying the local tour operators.

“The problem with socialism is that you eventually run out of other people’s money,” said Margaret Thatcher. Norway has amended this to “The beauty of socialism is that you never run out of the dinosaurs’ money”.

Here are some of Oslo’s gleaming new waterfront neighborhoods next to the gleaming new Munch Museum: