Climate change has had a dramatic effect on EAA AirVenture (“Oshkosh”). High temperature today was 90 degrees, 12.5% higher (using God’s preferred temperature units) than last year’s 80 degrees.

How about prices? We parked a car at the seaplane base this morning. It’s $25 to park for the day, 67% more than the $15 charged a year ago (the Biden administration says that inflation is 3%).

Speaking of the seaplane base, here’s a Cessna that was previously parked in a tow-away zone:

…and some general photos…

Finally, three cheers for AirCam. With two people on board, the twin came off the water after about 100′ with no apparent transition from plowing to step!

“Inflation has moderated somewhat since the middle of last year,” Mr. Powell said. “Nonetheless, inflation pressures continue to run high, and the process of getting inflation back down to 2 percent has a long way to go.”

“Inflation has consistently surprised us, and essentially all other forecasters, by being more persistent than expected,” Mr. Powell said. “And I think we’ve come to expect that — expect it to be more persistent.”

He added that there’s a “common factor” that has driven price increases higher. “It’s the pandemic, and it’s everything about the pandemic: The closing of the economy, the reopening of the economy, the fiscal support, the monetary support. All the things that happened went into high inflation.”

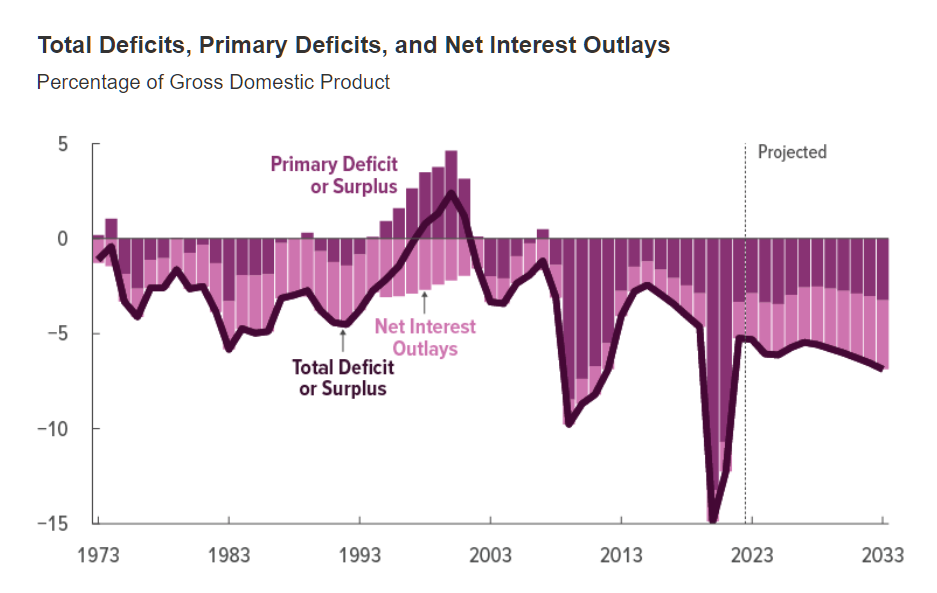

Of course, it is the virus that is to blame, not the human response (panic everywhere other than in Sweden) to the virus! But if the wild government spending on coronapanic is now the official cause of inflation, how can the Fed stop inflation? Congress continues to spend wildly with annual budget deficits that were, prior to 2008, seen mostly during wars. From the CBO:

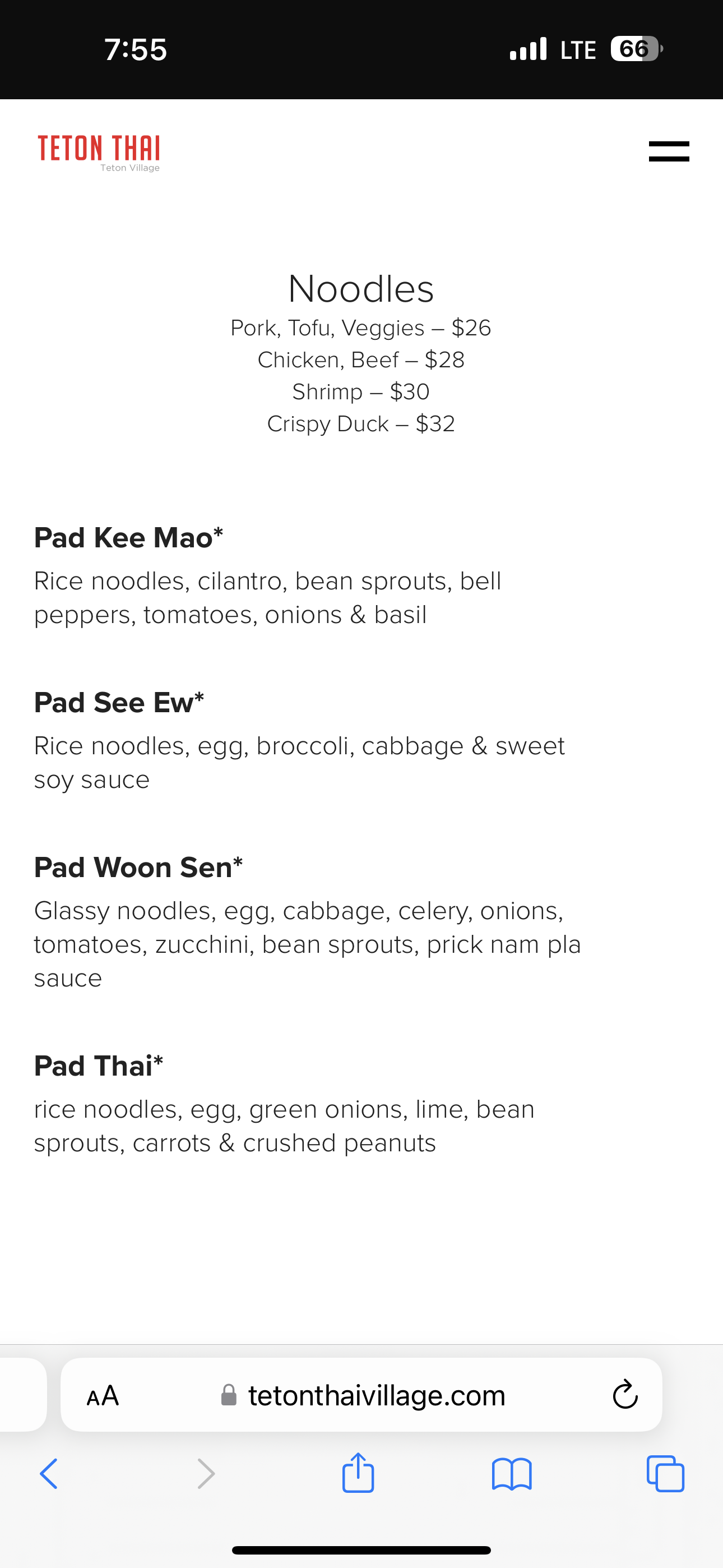

Separately, here’s my latest inflation achievement… paying $30 for Pad Thai (Jackson, Wyoming):

That was one week after getting a haircut in a barber shop… for $55 plus tip (Big Sky, Montana).

I hope that all white readers who are members of the laptop class and/or government employees are enjoying their paid holiday for Juneteenth. For readers (like me!) who suffer from reduced income as a consequence of reduced working hours, let’s have a look to see whether we can afford to take it easy…

“You have to look at year-over-three-years replacement costs, and they’re high,” [Triple-I CEO Sean] Kevelighan said. “Personal homeowners replacement costs are up 55 percent. We’ve got personal auto replacement costs up 45 percent.

The three-year inflation rate, as perceived by insurers paying claims, is around 50 percent. Maybe the problem is behind us thanks to the muscular efforts of Joe Biden to whip inflation? “State Farm Halts Home-Insurance Sales in California” (Wall Street Journal, May 26):

State Farm is stopping the sale of new home-insurance policies in California effective Saturday, because of wildfire risk and rapid inflation in construction costs.

State Farm is the nation’s biggest car and home insurer by premium volume. It said it “made this decision due to historic increases in construction costs outpacing inflation, rapidly growing catastrophe exposure, and a challenging reinsurance market.” It posted the statement on its website and referred questions to trade groups.

I think that we can ignore the wildfire risk as the primary business reason here. The wildfires of 2023 aren’t dramatically riskier than the wildfires of 2022. Maybe State Farm is just being greedy so that they can enrich their fatcat shareholders? They’re not truly losing money on new policies, but are trying to pressure California regulators into giving them yet more profits:

State Farm is a mutual company, meaning it is owned by its policyholders, and it has deep pockets. It ended 2022 with net worth of $131.2 billion.

Why does it matter if construction costs are outpacing inflation, as State Farm says? Our grow-the-population-to-450-million-via-immigration plan will result in skyrocketing rents and miserable living conditions for most Americans unless new housing can be built at some price that is affordable to low-skill migrants (who earn below-median wages).

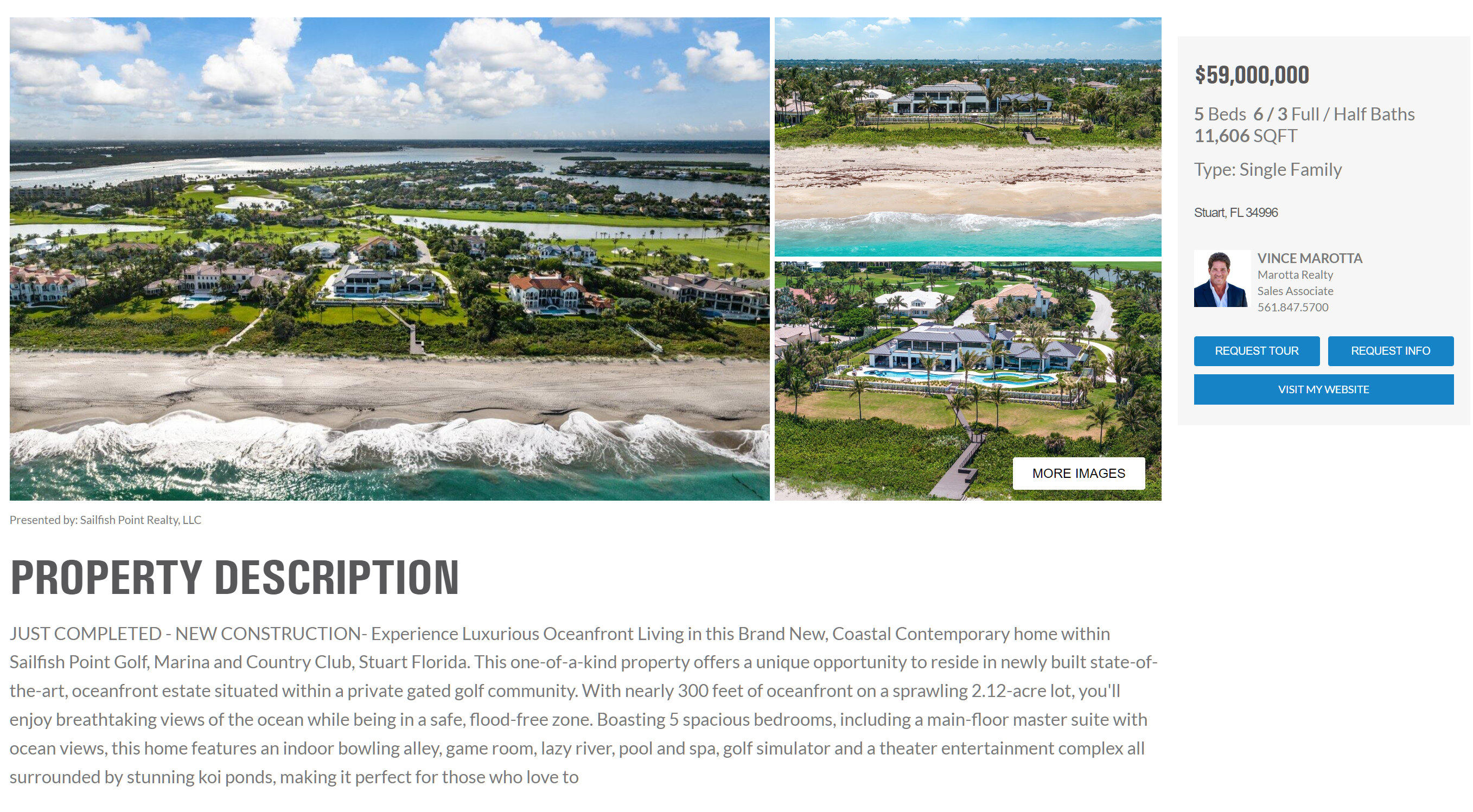

Let’s have a look at a newly built house just north of us in Martin County, Florida, far away from the high prices of Miami and Palm Beach. It’s only about $5,000 per square foot and comes with 2 acres of land:

Related:

City rebuilding costs from the Halifax explosion (in which we look at the numbers for a Boston housing development where a two-income couple working full-time at the median wage couldn’t afford the bare construction cost of an apartment, much less the land or any profit for the builder)

I took our 2.5-year-old Honda Odyssey in for a B127 service, for which I’d made an appointment. Due to the dealer being short-staffed and, apparently, not completely organized, they couldn’t do “7” (brake fluid change) without adding a multi-hour wait on top of the promised 1.5-2-hours.

The parts stock situation has improved compared to 1.5 years ago in that they had all three wiper blades available for the minivan compared to just one back in 2021. The car stock situation is also slightly improved, with a handful of new cars in stock and available at $2,000 over retail. It was $5,000 over in 2022, but of course the total price in nominal dollars is similar because Honda has raised the list price. The identical minivan that we leased in 2021 for $400/month is available… for $800/month. Here’s a 2008 jalopy that, pre-coronapanic, the dealer would have sent to auction (the venerable Ford Taurus sits amidst the parking spaces that in 2019 were jammed with new cars):

Fresh from a checkup with one of America’s 190 board-certified veterinary dentists, Mindy the Crippler was my companion for the two-hour wait and made a lot of new friends inside the dealership. I left her with another customer while I went to get coffee and returned to find that the invasive species had invaded the vinyl seats:

My question for today is how consumers are able to keep spending like drug dealers and/or alimony plaintiffs. A lease quote is the best indication of the true cost of car ownership because it factors in the time value of money and the market’s expectation of depreciation. The cost of car ownership gone up dramatically doubled for anyone who needed to buy a car in the past two years or so, especially when you factor in higher gasoline prices. Therefore, these car owners should have less money to spend on rent, TV/phone subscriptions, entertainment, dining out, trinkets, etc.

What’s new in the Honda minivan world, aside from nothing? Honda seems to have dropped their basic trim level. For Corvette enthusiasts, there is a new “Sport” trim level that has black wheels:

What do readers think? To me, it looks like an old Dodge Caravan whose wheel covers were boosted in the Bronx.

Wikipedia says that pre-coronapanic production of this car was 100,000-130,000 per year between 2009 and 2019. For 2020, however, production fell to 83,000. In 2021, production was down to 76,000. In 2022, it fewer than 48,000 Odysseys were made. Half as many cars at 10X the total profit for manufacturer and dealer? Do we suspect a continued chip shortage or quiet collusion among the handful of major car manufacturers?

If integrated circuits were primarily made in the U.S., it wouldn’t be surprising to find them still in short supply. After all, quite a few Americans were introduced to the advantages of sitting at home playing Xbox all day and habits, once formed, are tough to break. But the Japanese, Koreans, and Chinese continued to work during coronapanic. Why aren’t these hard-working nations making as many chips as car companies need/want?

Against the collusion hypothesis: if the legacy car companies won’t supply a mass market anymore, that opens the door to infiltration by Tesla, Lucid, and Hyundai/Kia (sort of a legacy car company, but also not exactly mainstream until recently).

Related:

“Car Dealer Markups Helped Drive Inflation, Study Finds” (WSJ, April 23): “extra dealer profits contributed between 0.3 and 0.5 percentage point of the nearly 16% rise in the consumer-price index between the end of 2019 and the end of 2022, a study published in a U.S. Bureau of Labor Statistics journal found.”

Pravda says “The U.S. is now two years into abnormally high inflation“:

The U.S. is now two years into abnormally high inflation. But 2023 inflation is drastically different from the price increases that first appeared in 2021. Here’s why.https://t.co/2ksnZPLkWv

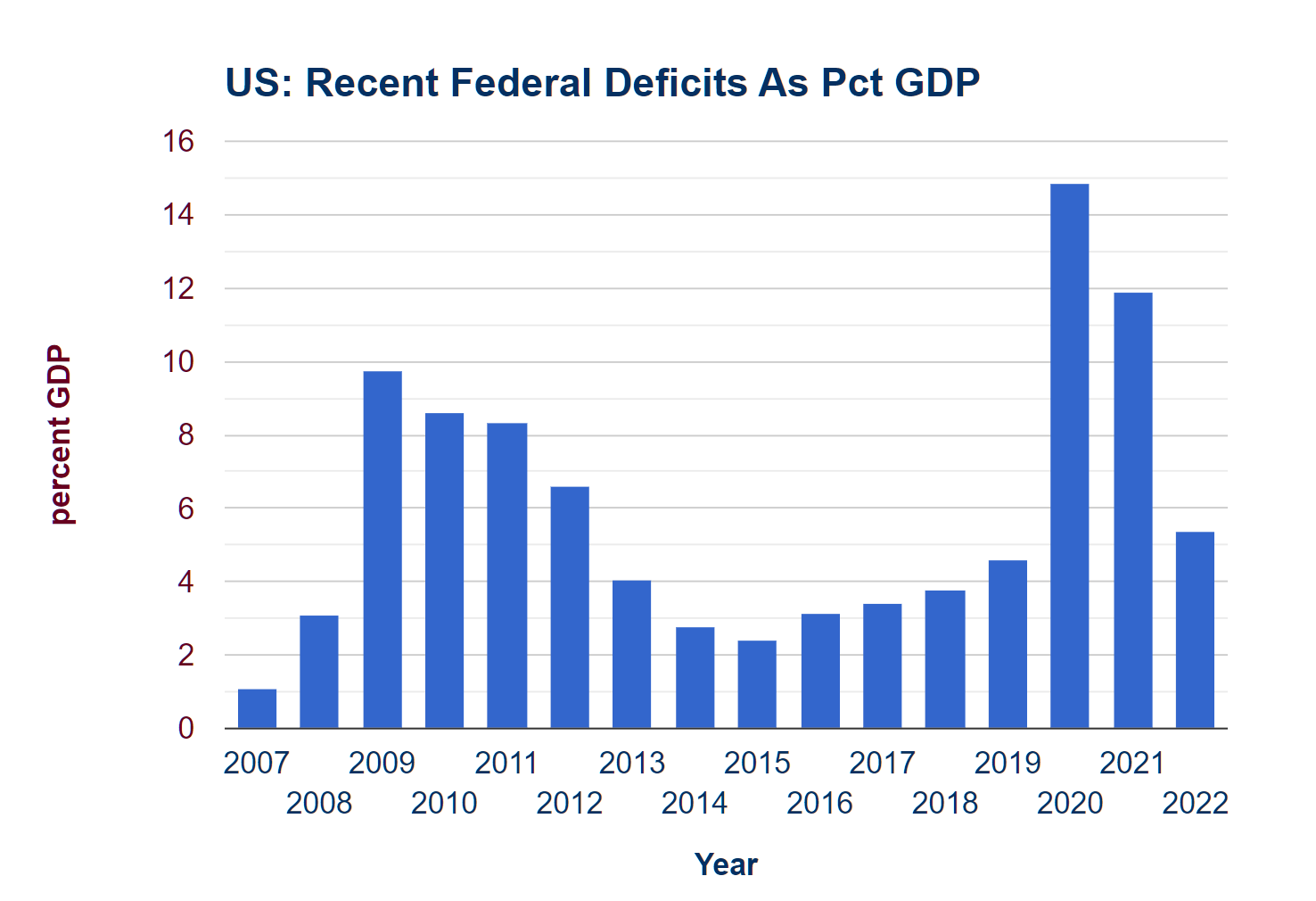

But wouldn’t it be more accurate to say that we have roughly the inflation that we should expect given the level of deficit spending that we voted for? To prevent runaway inflation, the EU established a deficit limit of 3% of GDP for member countries and a debt-to-GDP ratio of 60%. The US deficit has been 5-15% since 2020 and was higher than 3% before that:

U.S. inflation today is drastically different from the price increases that first appeared in 2021, driven by stubborn price increases for services like airfare and child care instead of by the cost of goods.

We can buy as many DVD players as we want, in other words. It is only services that are going to be unaffordable to the non-elite. What percent of the economy is subject to a wage-price spiral, then? 77.6 percent.

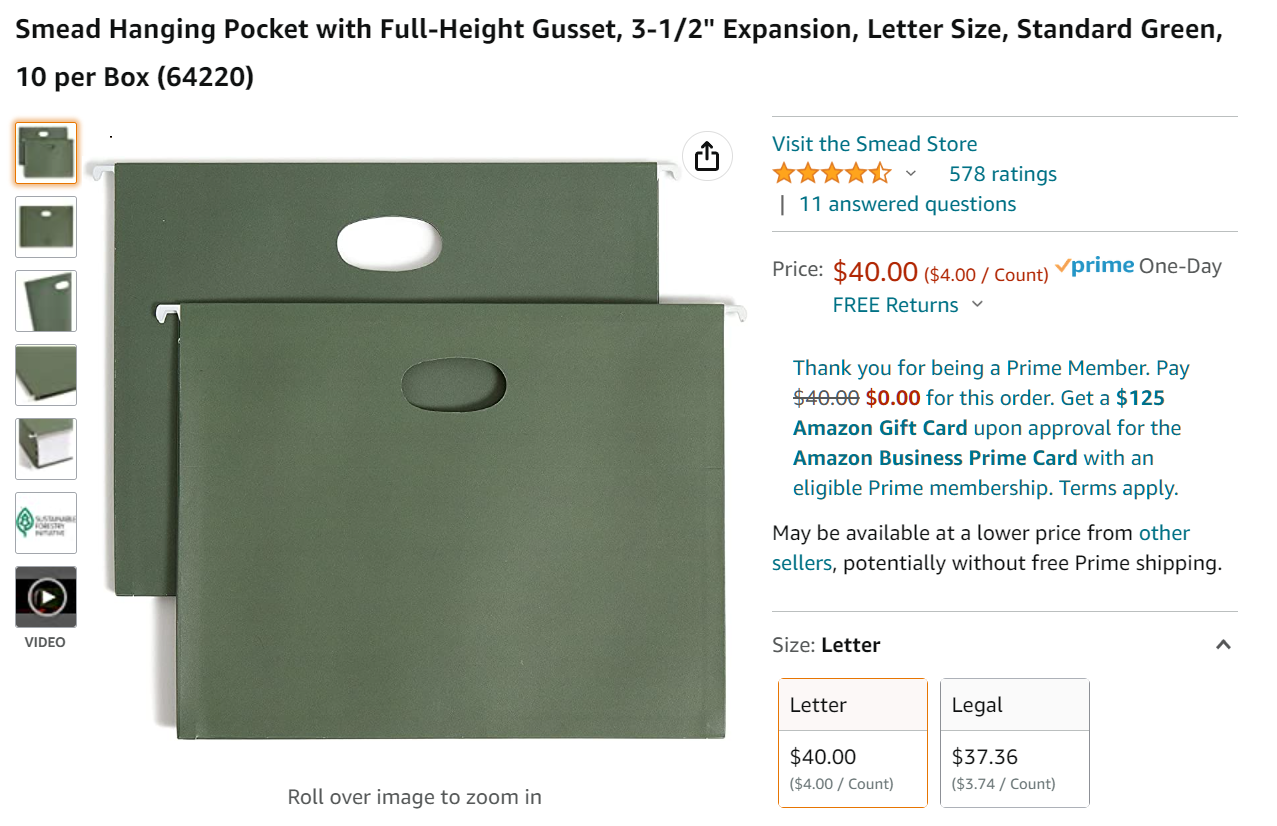

One way to stay organized is to place cables and other miscellanies in hanging folders within a lateral filing cabinet. So that small items don’t fall out, pocketed folders are ideal. I bought 10 in July 2022 for $34.97:

That’s an inflation rate of more than 15 percent annually. The government, however, assures us that these folders have inflated to only $35.63 (BLS calculator).

How are folks feeling after today’s inflation report? The Wall Street Journal:

Core prices, a measure of underlying inflation that excludes volatile energy and food categories, increased 5.6% in March from a year earlier, accelerating slightly from 5.5% the prior month. Core inflation, which economists see as a better predictor of future inflation, has stayed stubbornly high in part because of inflationary pressures from shelter costs.

(The journalists don’t speculate on what might be causing shelter costs to rise. It couldn’t be a shift in the demand curve from 175 million post-1965 immigrants and their descendants (half of these folks are already in the U.S. housing market and the other half are forecast to arrive soon), could it?)

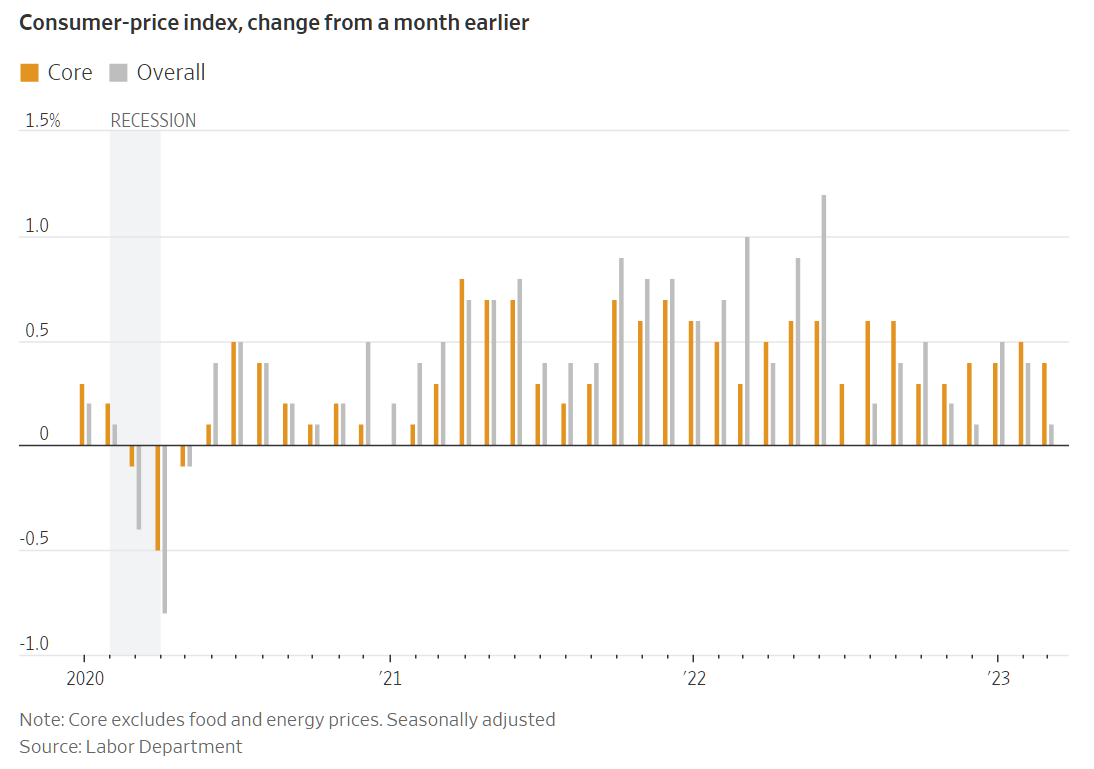

The month-to-month chart shows reasonably stable core price inflation of close to 0.5 percent per month.

We, via Congress and the Fed, can’t resist trying to cheat our way to economic prosperity. The deficit spending and quantitative easing aren’t going to stop, in other words, and therefore the steady erosion of the dollar’s purchasing power won’t stop. But maybe we can adapt in a small way….

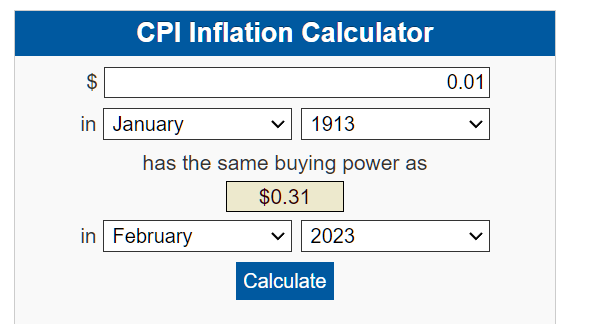

As the price of a crummy apartment trends toward $2000/month, can we let go of the pennies that litter our floors and clog our vacuum cleaners? The BLS CPI calculator goes back only to 1913, but it shows that the economy functioned just fine back then with the smallest coin being worth more than today’s quarter:

Given that most transactions are via credit card anyway and that we expect continued Bidenflation, why not declare that the smallest coin going forward will be the quarter? While we’re at it, we can decree that all quarters must be from the American Women Quarters Program, e.g.,

The next step up from quarters would be a $1 coin with a picture of (cloth-masked) Dr. Fauci on one side and Pfizer CEO Albert Bourla holding a positive COVID-19 test result.

Today’s $5 bill is worth less than a quarter was in 1913 so we’d get rid of it in favor of a $5 coin showing the legitimate government’s victory over the January 6 insurrection (Jacob Angeli, the QAnon shaman; obverse) and Joe Biden’s victory over Corn Pop (reverse).

Paper money would start with the $10 bill, which is worth a little more than the 1913 quarter.

Any better ideas for streamlining the use of cash?

Inflation anecdote: Chewy shipped Mindy the Crippler’s food recently. It was $2.97 per pound in September 2019. The same brand/variety food is $5.13/lb. today. That’s 73 percent inflation over a 42-month period…. roughly 17 percent compounded annual inflation. We are informed by the BLS that the price should have gone up to $3.48/lb. I.e., the government says that inflation is 17 percent and Chewy says it is 73 percent.

“Men and nations behave wisely,” the Israeli statesman Abba Eban observed, “when they have exhausted all other resources.”

In an interview for these pages in 2011, he warned about the broad discretion the then-new Dodd-Frank law gave government officials to deal with what they deem systemic risks. The “atmosphere of unpredictability” doesn’t “make the system any safer,” he said. “This is nuts to be identifying systemically important institutions.”

A dozen years later, he still thinks it’s nuts: “As we’ve seen with SVB and Signature, virtually any institution can be deemed systemically important overnight and seized, with the government then completely empowered to determine what happens to various classes of creditors.”

The result is to destroy market discipline and encourage bankers to behave recklessly. He recounts a conversation on the trading desk at his firm following the recent weekend of bank bailouts. “If they hadn’t guaranteed all the deposits,” a colleague said, “things would’ve gotten very ugly in the markets on Monday.”

Mr. Singer replied: “That is entirely true. Things would’ve been ugly. But is that what regulation is supposed to be? Wrapping all market movements in security blankets?”

What about the most significant economic phenomenon of the moment?

Mr. Singer saw inflation coming at the start of the Covid pandemic. “We think it is very unlikely that central bankers will move to normalize monetary policy after the current emergency is over,” he wrote in an April 2020 letter to investors. “They did not normalize last time”—meaning after the 2008 crisis—“and the world has moved demonstrably closer to a tipping point after which money printing, prices and the growth of debt are in an upward spiral that the monetary authorities realize cannot be broken except at the cost of a deep recession and credit collapse.”

Mindful of the history of the 1970s, when inflation retreated several times only to come roaring back, Mr. Singer figures short-term declines will convince policy makers that they’ve slain the beast. They’ll “probably go back to their playbook,” resuming the policy of easy money.

The guy’s remedy is one that will never fly with the American voter:

How do we chart a course back toward sound money and long-term prosperity? “The optimistic scenario,” Mr. Singer replies, “would entail pro-growth reforms across the board, including tax reductions, entitlement reforms, regulatory streamlining, encouraging energy development including hydrocarbons . . . cutting federal spending, selling the asset holdings on central bank balance sheets.”

(see quote from Abba Eban, above)

Let’s assume that Congress and the Fed are never going to change. How does an individual investor protect him/her/zir/theirself from the doom that Singer predicts? That’s where it gets tough! The guy is bearish on nearly all assets, especially crypto. His $55 billion Elliott Management fund can do things that none of us can do, e.g., buy a big stake in Salesforce and get the company to fire 10 percent of its employees to boost profits (and therefore stock value).

A friend who has done some co-investing with Paul Singer’s fund points out that “talk is cheap” and he won’t accept Singer as a prophet without evidence that he made huge money in inflation swaps after that April 2020 newsletter to his clients. Wikipedia points out that Singer was predicting doom in 2014:

In short, if this smart and experienced fund manager is right, U.S. and European assets will be eroded by inflation for the next few years and returns to investors will be minimal.

In a November 2014 investment letter, Elliott described optimism about U.S. growth as unwarranted. “Nobody can predict how long governments can get away with fake growth, fake money, fake jobs, fake financial stability, fake inflation numbers and fake income growth,” Elliott wrote. “When confidence is lost, that loss can be severe, sudden and simultaneous across a number of markets and sectors.”

Anyone who acted on that advice would have done quite poorly until 2022!

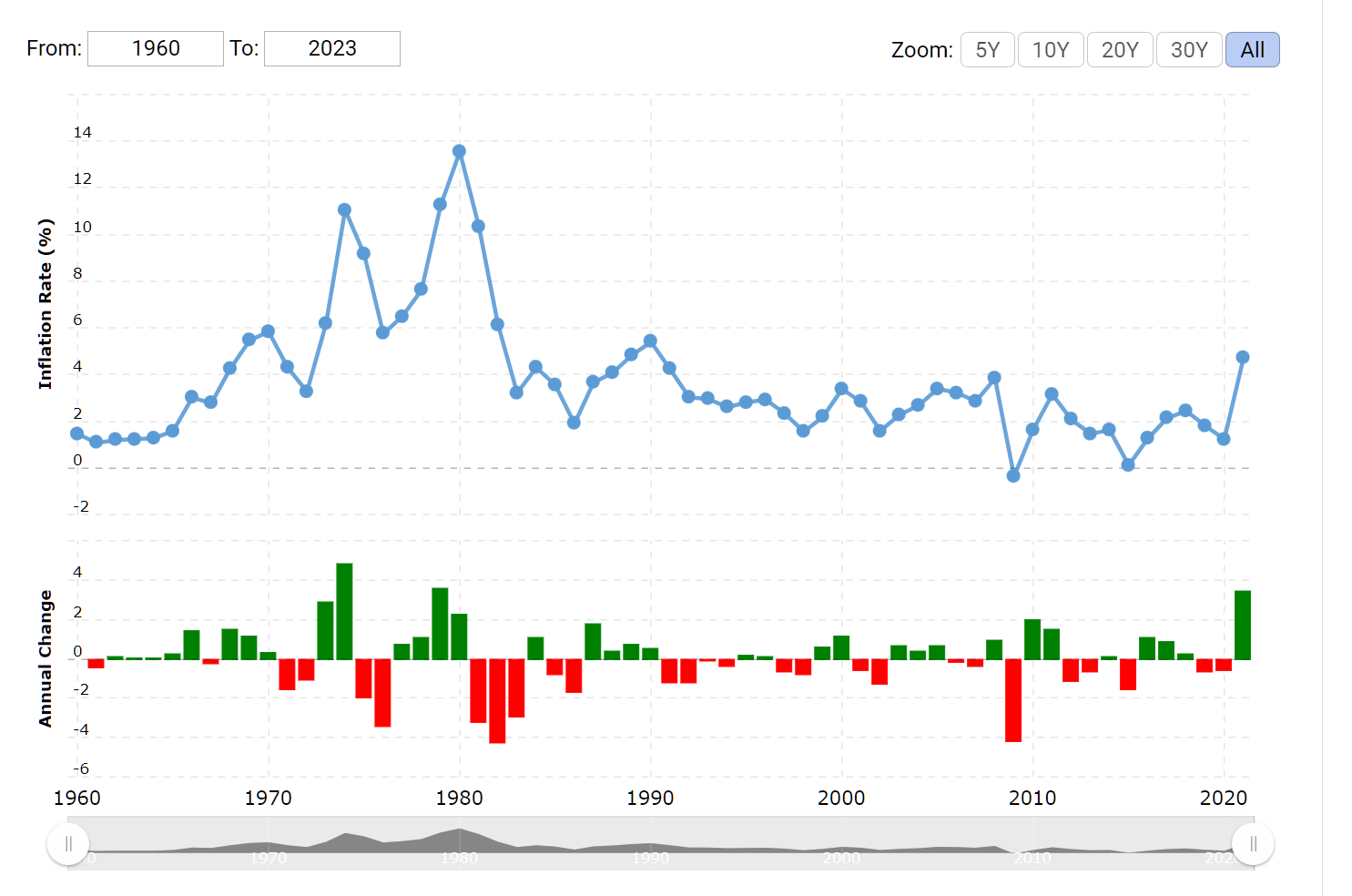

Maybe the take-away should be that Americans today aren’t smarter than Americans were in the 1960s and 1970s. Inflation jumped dramatically in 1966 as Lyndon Johnson and Congress spent like alimony plaintiffs on (1) the Great Society programs of Medicare, Medicaid, etc., and (2) the Vietnam War. The inflation rate did not come down to the pre-1966 level until 1998. Maybe we could argue that inflation was finally whipped by 1992 (chart):

If we’re expecting at least 26 years of elevated inflation, what do we do? For a person who doesn’t already have a house, one reasonable response is for him/her/zir/them to try to get a 100 percent mortgage at today’s 6.5-7 percent 30-year rates. Put some stocks in as collateral as necessary to hit the 100 percent number. If Paul Singer is right that the D.C. technocrats won’t be able to resist inflation-as-usual policies, inflation will render the real cost of borrowing almost $0. If Paul Singer is wrong, there is no prepayment penalty so just refinance if rates fall dramatically.

We have two cars. They’re older than they were a year ago and presumably less valuable. We have had no tickets, accidents, or claims. Progressive is bumping the rate by 30 percent. I talked to a friend in Austin, Texas. His rate is also going up 30 percent.

Readers: What are you seeing for car insurance rate increases? What’s the explanation for this in what we are informed is a market economy? Most of the premium is for collision, right? Have body shop rates gone up 30 percent now that Americans realize it is more pleasant to relax on the sofa than to work in a body shop?

Separately, the news is not all bad. When one goes to the Progressive web site, the first and most prominent link is to learn about the company’s “commitment to diversity and inclusion” (not their actual diversity and inclusion, but their commitment to the religion).

What if we follow the link?

For years, we’ve been saying there’s a very real and important business case for DEI. It’s been proven time and time again that a more diverse, equitable, and inclusive organization drives profit and productivity by creating brands, products, and services that are more relevant and desirable in our competitive and multicultural marketplace.

It was almost impossible for a DEI champion such as Silicon Valley Bank to fail, in other words.

How about over at State Farm? Instead of being at the very top of the homepage, Diversity & Inclusion is relegated to the footer, under Careers:

The question for today is whether we’re in a wage-price spiral. If everyone’s monthly bills are being bumped 5-15% annually because of the inflation that happened over the past year, shouldn’t we expect continued inflation because workers will need salary bumps of 5-15% and then the monthly fees will go up 5-15% in 2024?

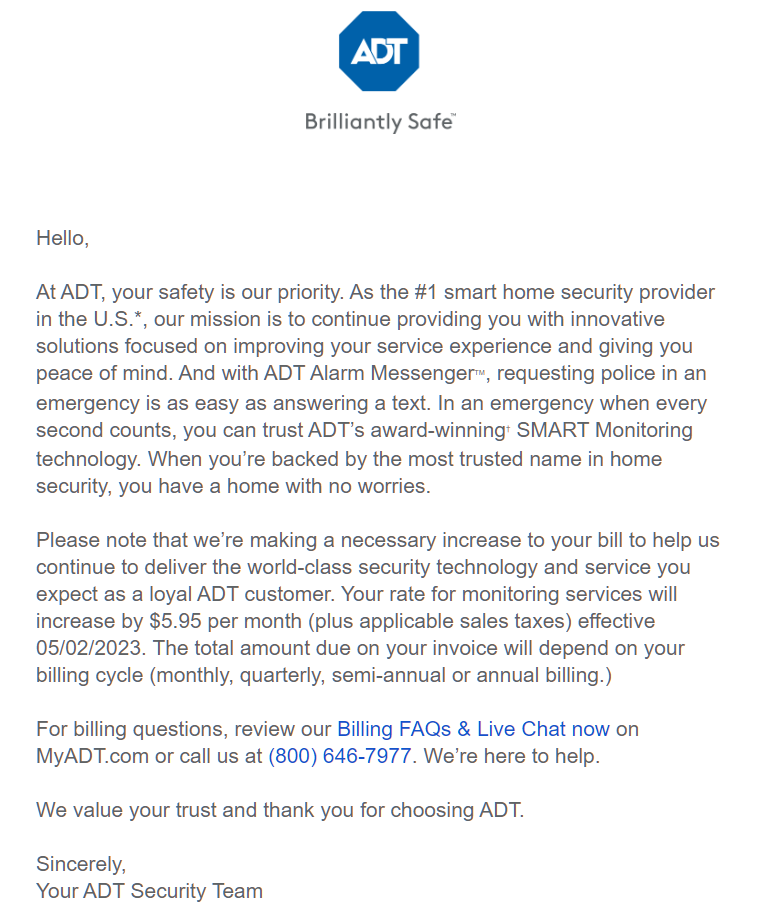

Anecdote: When we moved in a year ago, ADT bamboozled me into signing up for a three-year monitoring contract for the alarm system that was already installed in the house. Apparently buried in the fine print is a clause that allows them to raise the rate as much as they want. It is going up 11 percent. Here’s the email:

For the percentage calculation:

ADT did not get the memo from Joe Biden, Janet Yellen, and Jerome Powell that inflation has been whipped?

On the bright side, our lawn care monthly fee recently was bumped up by only 5 percent. The letter from the owner explains that his break-even rate is $30 per hour per person. Where are the low labor costs for laptop class members that open borders was supposed to deliver? (Harvard study)

Readers: Are we in a fully-established wage-price spiral?