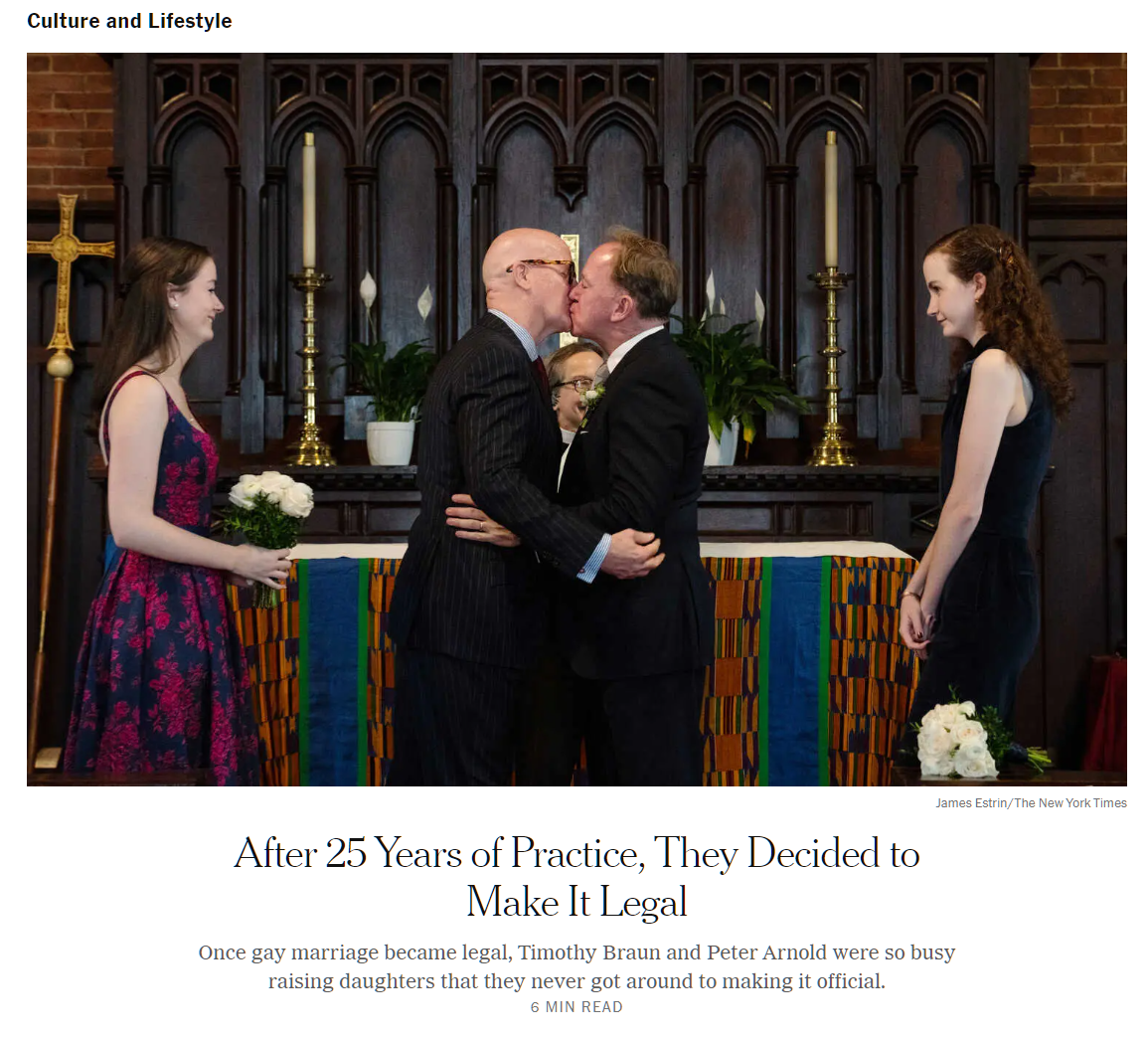

I went to Costco to set up my mom’s new life as a Floridian. As part of the sales process, Costco customers are informed that some of the profits from the towels for sale flow into the pockets of people who identify as “women”. The “Women Owned” logo certifying that this is where the money goes has a rainbow embedded within. What does it mean? Are they saying that a heterosexual cisgender woman, for example, is somehow part of Rainbow Flagism?

I ended up buying towels from Land’s End. Maybe other shoppers are persuaded by the magic of this logo or the idea that their money is going to business owners of a particular gender ID? Wirecutter says buy Frontgate Resort Collection towels.

For $500 of miscellaneous household items, I had a choice between the Heroes of Rainbow Flagism at Target or the more prosaic Walmart, which is a little closer to our house. I chose Walmart.

An window into what’s on the minds of progressives! (But how is it consistent with their love for the Islamic Resistance Movement (“Hamas”) and Palestinian Islamic Jihad? Neither of those groups is renowned for celebrating the 2SLGBTQQIA+ lifestyle.)

If you love the ideas of two young English gentlemen getting naked together, massaging each other, and taking a shared bath, this is the novel for you. I downloaded the text from Project Gutenberg, however, and it seems that Dickens did not write these scenes of gay male passion. It should perhaps be retitled “Rainbow Copperfield” so that readers don’t get confused.

Helena Bonham Carter is fantastic as you might expect. Six stars for her.

It’s an interesting window into how the past can be quietly reconfigured to align with contemporary religion. A young follower of Rainbow Flagism, for example, might never realize that Charles Dickens was not a coreligionist.

Disney did the same thing with Dear Evan Hansen, but on a much faster clock. I attended the show in 2019, back when it was still legal to enter a theater in New York City. Part of my review:

One group that might not love the show is LGBTQIA. “This must be the only new Broadway show without an LGBTQIA theme or character,” I remarked. My companion, a regular at the theater, agreed, but that might be because her LGBTQIA teacher typically chooses LGBTQIA-themed shows for the public middle school crowd. The only reference to LGBTQIA issues is when teenage boys are anxious to avoid being perceived as gay (“that’s how it is in my school, too,” said the 12-year-old next to me).

When the play was turned into a purportedly faithful movie, the doctrinal error was corrected. The character who mocked gay male sexual activity in the play was turned into one who engaged in gay male sexual activity in the movie.

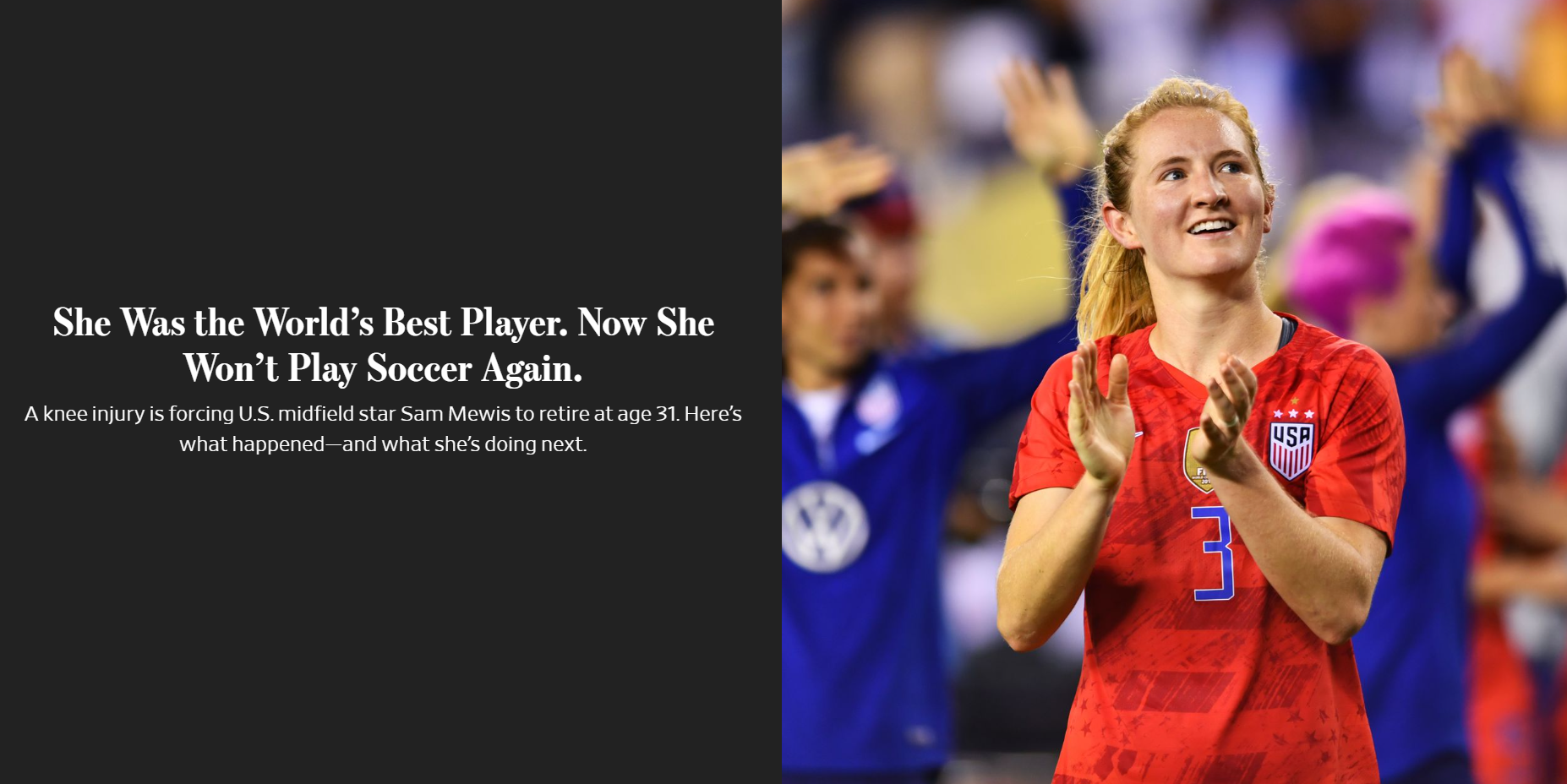

The Wall Street Journal reporter and editors determined that this player was, prior to the unfortunate injury, a better player than Lionel Messi or Cristiano Ronaldo. Here’s the reporter’s biography:

Related:

ChatGPT bets on soccer (seeing what AI makes of the world’s best players being beaten by 14-year-olds on a city team)

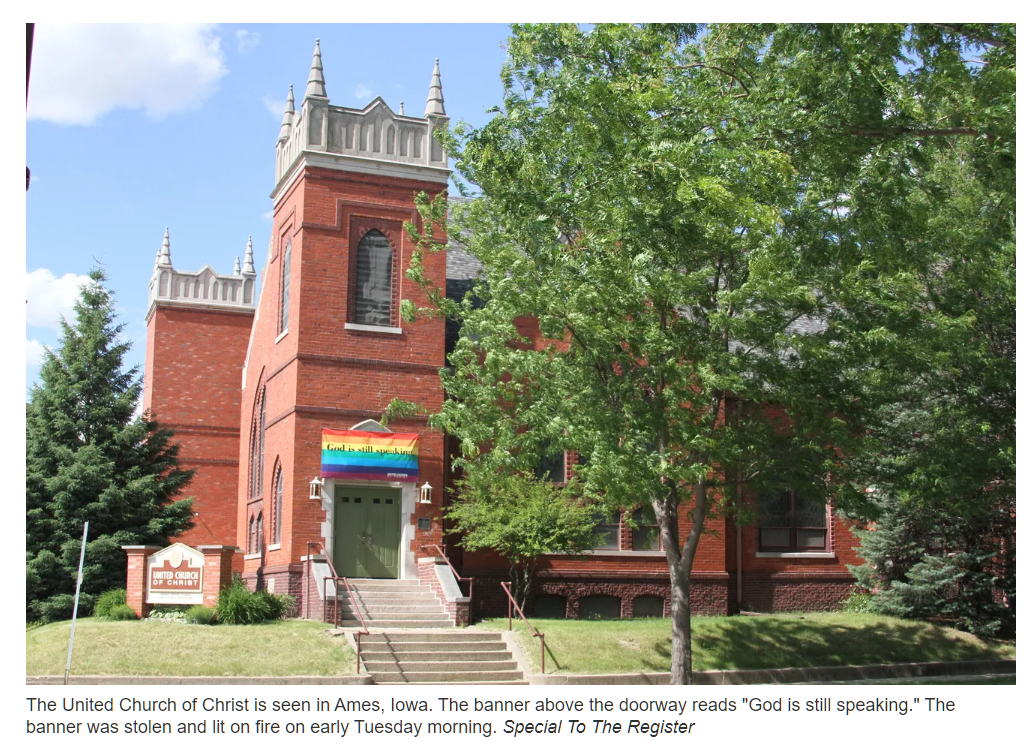

Here’s the church web site as of September 25, 2023:

Who can decode the symbols on the “Community Pride Worship” banner above?

I can’t find any post-imprisonment media stories about Adolfo Martinez. He has been erased, it seems. He was 30 years old when he was imprisoned and will be 46, almost ready to retire on SSDI, when he gets out.

Tara Tarawneh — a 2020 graduate of King’s Academy in Madaba, Jordan — was arrested Nov. 4 for allegedly stealing an Israeli flag from the front of a Campus Apartments house near the Ivy League campus, The Daily Pennsylvanian reported last week.

Tarawneh gave a hate-filled speech at a Philadelphia rally last month, with video of her addressing the pro-Palestinian crowd going viral, … “I remember feelings so empowered and happy, so confident that victory was near and so tangible,” she tells a crowd of the monstrous Oct. 7 attack. “I want all of you to hold that feeling in your hearts. Never let go of it. Channel it through every action you take. Bring it to the streets.”

Mx. Tarawneh could reasonably have expected an award for his/her/zir/their actions (the current gender ID of a college student today can never be assumed). A 2019 tale from NYU:

As soon as the [Israel Independence Day celebration] started, an anti-Zionist student rushed to the front of the protest line, held up the Israeli flag, lit it on fire, and threw it to the ground where it continued to burn. Adela [the Jewess] told her friends to ignore him, sing “Hatikvah” and move on.

Suddenly, a student protestor grabbed a microphone from a Jewish student, yelled “Free Palestine!” and waved his hands in the air. More protestors took the 10-foot Israeli flag, shredded it, and hung it from lamp posts and trees. Two protestors were arrested by NYPD and charged with assault, reckless endangerment, and property theft and damage.

Soon after, Adela, who was also a senator for the NYU student government, met with the administration to tell them that a line had been crossed and it was time to act.

What did NYU instead? They gave the anti-Israel hate group the President’s Service Award – the highest honor a student group can receive.

Related:

“Man gets 10 years for fatally stabbing Sioux City roommate” (Des Moines Register, also in the fall of 2019): 39-year-old Elmi Said was sentenced Friday. He’d been charged with second-degree murder for the Oct. 28, 2018, slaying of 40-year-old Guled Nur. … Said is also known as Abdiqadar Sharif.

“Iowa man in face-mask fight sentenced to 10 years in prison” (2021): Police and court records indicate Shane Michael, 42, went to the Vision 4 Less eyewear store on Merle Hay Road in Des Moines on Nov. 11 of last year. While there, Michael was wearing his face mask pulled down slightly, leaving his nose exposed.

“Driver sentenced to 2 years probation in April crash that killed East High School student” (2022): The driver involved in a crash that killed a 14-year-old East High School student has been sentenced to two years probation. Des Moines police said Terra Flipping struck 14-year-old Ema Cardenas with her car on April 28, 2022. She drove away following the crash before and was arrested that same day.

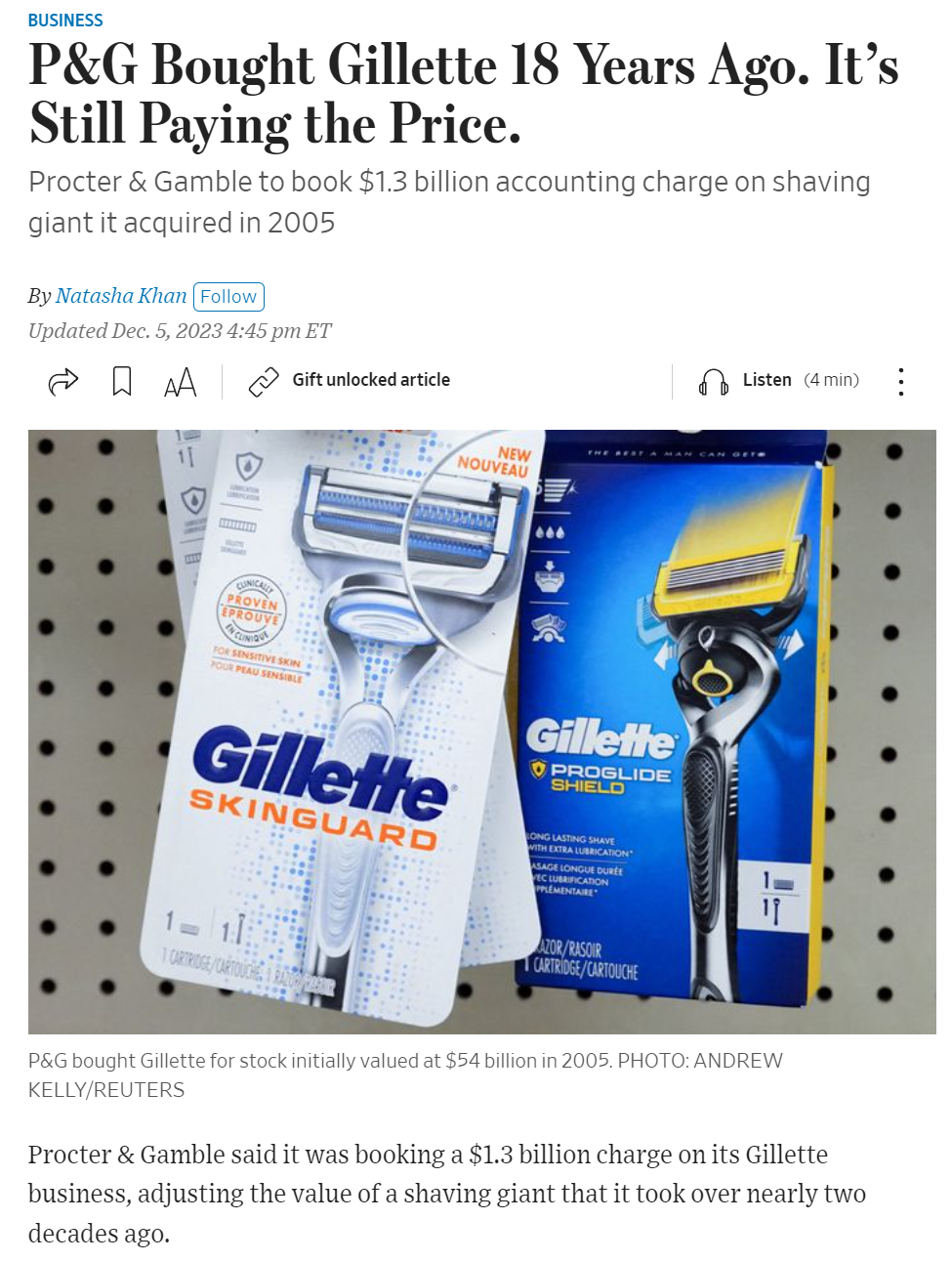

Loyal readers may recall A/B tests here in which the Dorco Pace 7 proved slightly superior to anything that Gillette offers. Other brands of razors were found to be grossly inferior. Background:

P&G wrote down the value of their $54 billion Gillette purchase by $8 billion after the Toxic Masculinity and transgender ads. The Wall Street Journal recently reported a $1.3 billion additional charge:

It looks as though Gillette is still stuck on the same 5-blade system that I tested in 2019, though it has been renamed.

I was chatting with an executive from Grameen America, the U.S. division of Grameen Bank, winner of the Nobel Peace Prize. I learned that, out of the rainbow of 74 gender IDs recognized by Science, Grameen American will lend to those who identify with just one gender: “women” (at an 18 percent interest rate).

Everything financial in the U.S. seems to be tightly regulated, so I’m wondering how this is legal. If a bank seems not to be lending with alacrity to Black and Latinx borrowers, the federal government is right there to sue them (recent example). How is it legal for Grameen to say “No men need apply”?

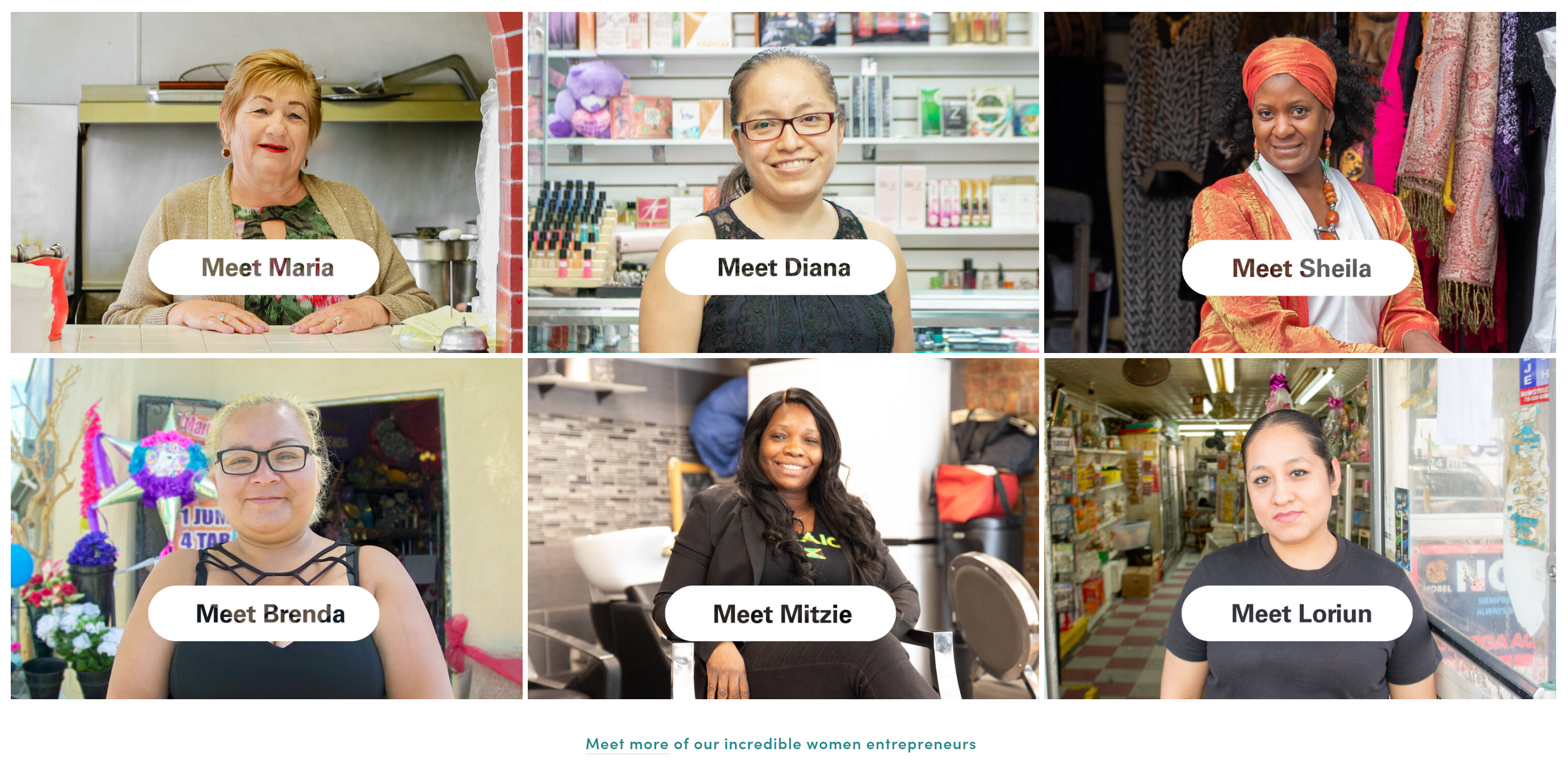

Note the “Meet more of our incredible women entrepreneurs” at the bottom. Why is “incredible women” a common phrase (3.3 million Google results) while “incredible men” is only about 1/8th as frequently used and “incredible nonbinary” occurs just 1,020 times on the Web? Are women 8X more incredible (“less credible”?) than men and vastly more incredible than the nonbinary?

“I think that she’s paid her dues. There are going to be no surprises, and she has earned the right to be president and the head of the country at this point. It’s that simple. And she’s a woman, which is very important because her take on things may be what we need right now.”

I.e., hiring for the President of the U.S. job should be done based on gender.

A federal jury in Manhattan on Thursday found Robert De Niro’s company liable for gender discrimination against a former employee who claimed that the actor assigned her “stereotypically female” job responsibilities such as washing his sheets and attending to his home even as she climbed the ranks of his company, awarding her $1.3 million in damages.

In more than six hours of sometimes colorful and explosive testimony, Mr. De Niro fiercely denied any wrongdoing and dismissed Ms. Robinson’s claims as “nonsense,” though he acknowledged that he could have called Ms. Robinson a “bitch” and a “brat” when she was his employee. He also addressed Ms. Robinson’s claim that Mr. De Niro asked her to scratch his back on occasion, saying that it may have happened one or twice, but that there was never any “disrespect” or “lewdness” attached to it.

Lawyers for Mr. De Niro, 80, portrayed Ms. Robinson, 41, as someone who exploited the trust and generosity of her boss, who had already given her significant perks and gifts — including a Rolex watch and part of a vacation in Hawaii — while also agreeing to pay her a salary of $300,000 per year in 2019, far more than other Canal office workers were paid. They argued that even though she received title changes, per her own request, her job responsibilities remained that of a personal assistant throughout her 11-year employment, and they repeatedly underscored the fact that she had not made any formal complaint over gender discrimination until she had been accused of financial improprieties.

Related:

“Years after presidency, Donald Trump is still living rent-free in Robert De Niro’s head” (Los Angeles Times, October 17, 2023): The actor has welcomed his seventh child, which he mentioned in passing earlier this year. The mother is his girlfriend Tiffany Chen, whom he credited with doing the “heavy lifting” with the newborn — De Niro may be an octogenarian, but she is a martial arts instructor. He told the Guardian: “[S]he does the work. And we have help.” … He’s also a grandpa several times over.

In an urgent plea, federal health officials are asking that any American who is pregnant, planning to become pregnant or currently breastfeeding get vaccinated against the coronavirus as soon as possible.

Covid-19 poses a severe risk during pregnancy, when a person’s immune system is tamped down, and raises the risk of stillbirth or another poor outcome, according to the Centers for Disease Control and Prevention. Twenty-two pregnant people in the United States died of Covid in August, the highest number in a single month since the pandemic started.

About 125,000 pregnant people have tested positive for the virus; 22,000 have been hospitalized, and 161 have died. Hospital data indicates that 97 percent of those who were infected with the virus when they were hospitalized — for illness, or for labor and delivery — were not vaccinated.

Vaccination rates among pregnant people are lower than among the general population. Fewer than one-third were vaccinated before or during their pregnancy, the agency said.

Some data also suggest that pregnant people with Covid-19 are more likely to experience conditions that complicate pregnancy … Clinical trials have a long history of excluding pregnant people from participation, and pregnant people were not included in the coronavirus vaccine trials.

The phrase “pregnant people” occurs 10 times in the article.

… increased options and assistance for women who traveled …

The response by abortion providers and activists to the end of Roe v. Wade, it seems, has resulted in more access to abortion in states where it’s still legal — not just for women traveling from states with bans but also for women living there.

Many women, especially in the South, have turned to methods outside the U.S. medical system or carried their pregnancies to term, researchers said. These women are likely to be poor, teenagers or immigrants, and to have young children or jobs that don’t give them time off.

Planned Parenthood Northern California, which operates 17 clinics, began hiring and expanding appointments and telehealth months before Dobbs. It was in part to prepare for an overturn of Roe, and in part a realization that demand for women’s health care had built up during the pandemic, said Dr. Sara Kennedy, its chief operating and medical officer.

More recently, women in states with bans have also been able to order the pills because of shield laws that protect providers that prescribe and mail pills to such patients.

Not a single use of the phrase “pregnant people” to describe those who receive abortion care.

It’s been more than a month since Governor French Laundry signed a new California bill that revoked the state’s ban on taxpayer-funded travel to the Lands of the Deplorables (26 horrible states).

Hate is now okay, in other words? Not exactly. The new bill says that California taxpayers’ money will be used to eliminate hate in the 26 bad states via advertising: “creates a new public awareness project that will consult with community leaders to promote California’s values of acceptance and inclusion of the LGBTQ+ community across the country” (press release)

The marketing geniuses behind Target and Bud Light famously failed this summer at their stated goals of getting more Americans to embrace the 2SLGBTQQIA+ lifestyle or, at least, celebrate the 2SLGBTQQIA+ lifestyle. The bureaucrats in Sacramento imagined that they will be more successful than the world’s highest-paid advertising experts.

Readers who live in formerly banned states: have you been reached by California’s public awareness project? If you were a hater, were you persuaded to stop hating?

Separately, I’m wondering if the ban revocation was timed to allow California elites to travel (on the taxpayers’ dime) to Austin, Texas for today’s Formula One race. Who’s watching the race on TV or in person? It might be fun to be a Formula One fan here in Florida if the organizers would schedule the Miami race for February or March rather than May (a time when a person should be paid to sit outdoors all afternoon, not pay $2,000 for the experience).

Separately, a Facebook friend in Maskachusetts is an attorney with a passion for Constitutional rights (which is why he continues to reside in a lockdown state?). He recently represented a woman who was attacked and ultimately sued by her wealthy suburban Boston neighbors for thoughtcrime. An excerpt from her lawsuit defense:

[one lawn sign displayed by the defendant] shows the words “PRIDEMONTH” and then the letters on each side of “PRIDEMONTH” fade out, to “PRIDEMONTH” to finally “DEMON” and on the last line, it says “Makes sense now.”

The judge was hostile to the Deplorable lady, and she told the defendant to stop sharing her political views, but ultimately couldn’t find a basis to rule in favor of the plaintiffs.