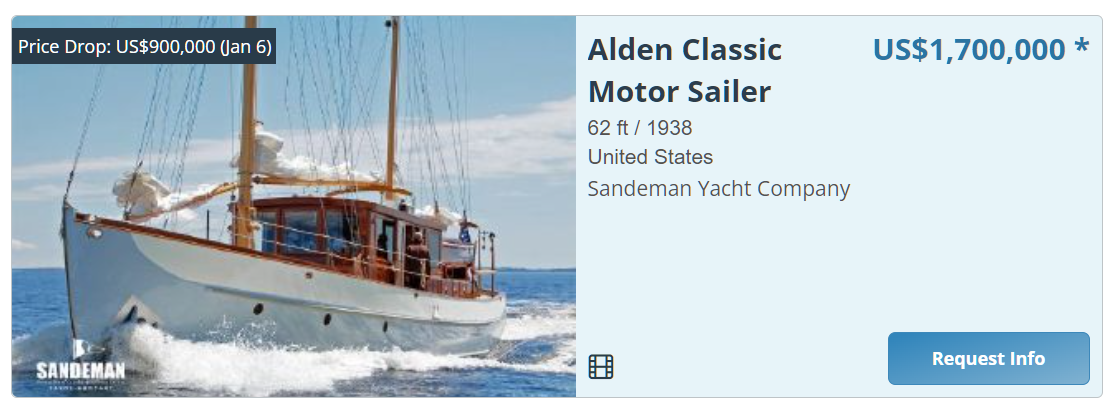

One of our neighbors refused to go to medical school and be like everyone else in the neighborhood. He needs to earn money without practicing medicine, so he sells yachts. I found him putting his new Porsche 911 GTS ($200,000 and 1.5-year wait) away in his garage and asked if the wind had gone out of the yacht world’s sails. “Yachts that cost under $2 million have taken a big hit from rising interest rates,” he responded. “They’re down about 25 percent from their peak a year ago. Anything over $5 million is steady. Those are cash buyers and prices haven’t moved.”

Representative Kevin McCarthy of California finally secured the House speakership in a dramatic vote ending around 12:30 a.m. Saturday, but the dysfunction in his party and the deal he struck to win over holdout Republicans also raised the risks of persistent political gridlock that could destabilize the American financial system.

Economists, Wall Street analysts and political observers are warning that the concessions he made to fiscal conservatives could make it very difficult for Mr. McCarthy to muster the votes to raise the debt limit — or even put such a measure to a vote. That could prevent Congress from doing the basic tasks of keeping the government open, paying the country’s bills and avoiding default on America’s trillions of dollars in debt.

The only way to stabilize our economy and currency is to borrow and spend more!

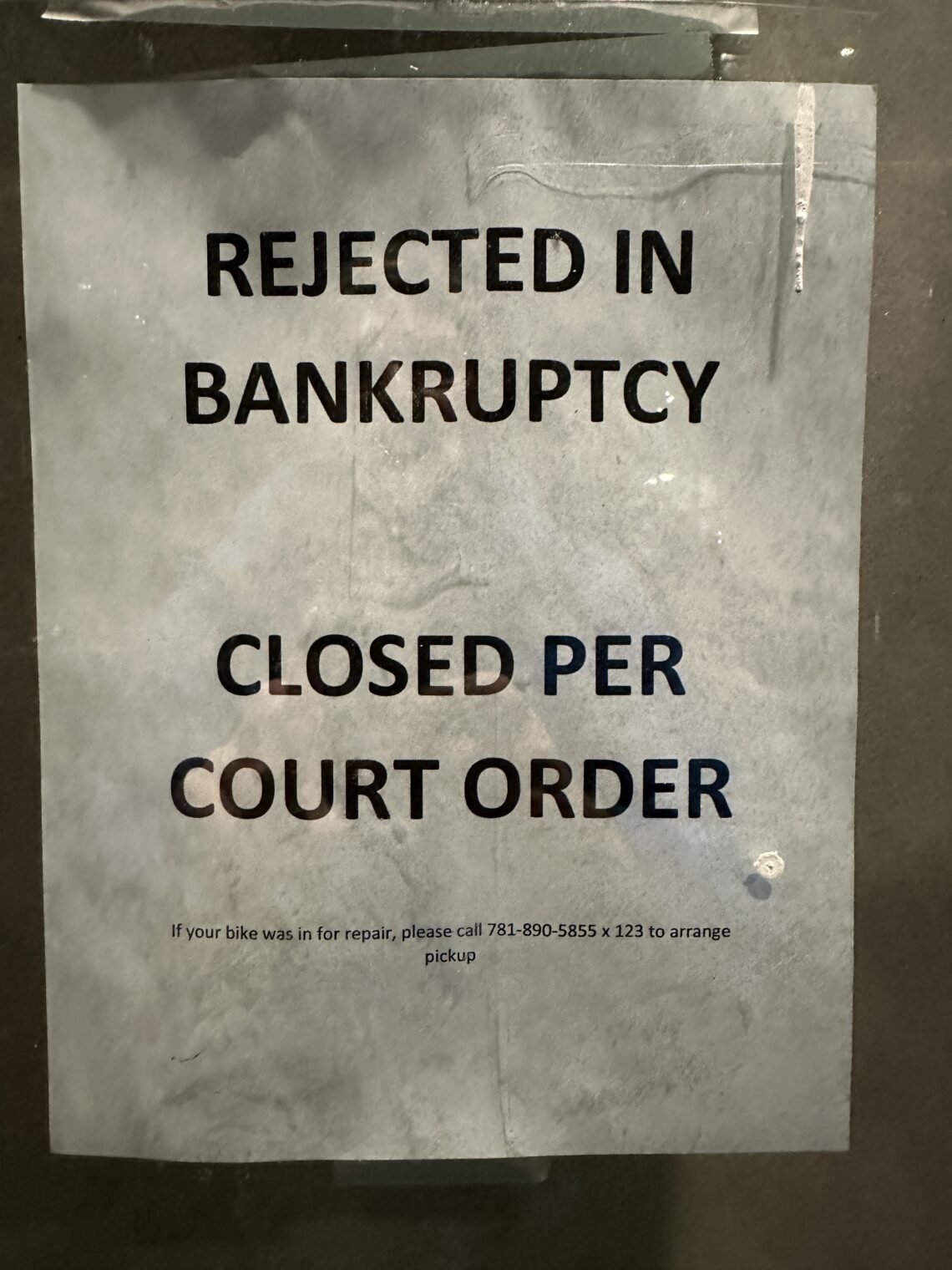

Speaking of the economy, here are a few photos from my old neighborhood in Cambridge, Maskachusetts. The marijuana stores are thriving while the bicycle shop went bankrupt:

Some photos from a recent trip to Costco where we stocked up for holiday entertaining. A roast feeds a lot of (masked-for-safety) people inexpensively:

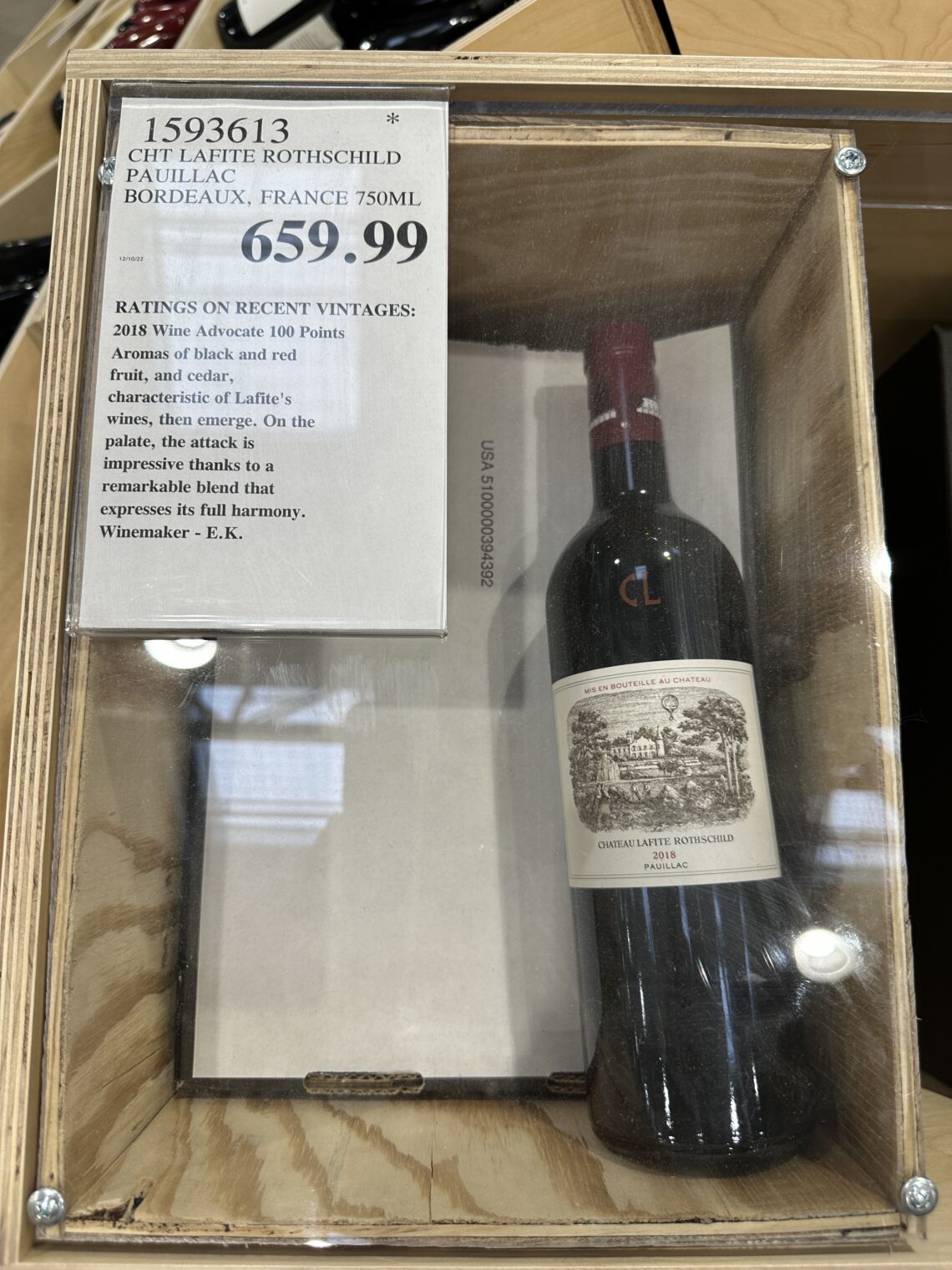

Wash it down with some red wine, reduced in price thanks to a glut in Australia:

Costco in Florida offers fun family fireworks for after dinner:

And the local Publix agrees that explosives and incendiaries are safe for the whole family:

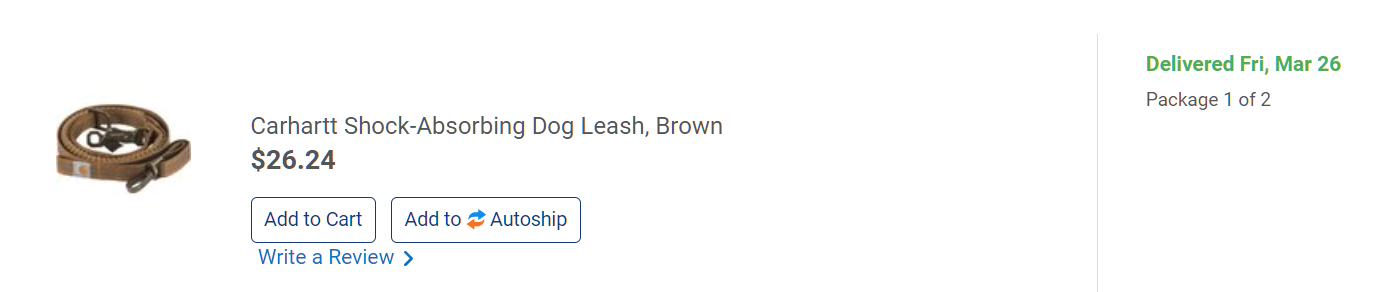

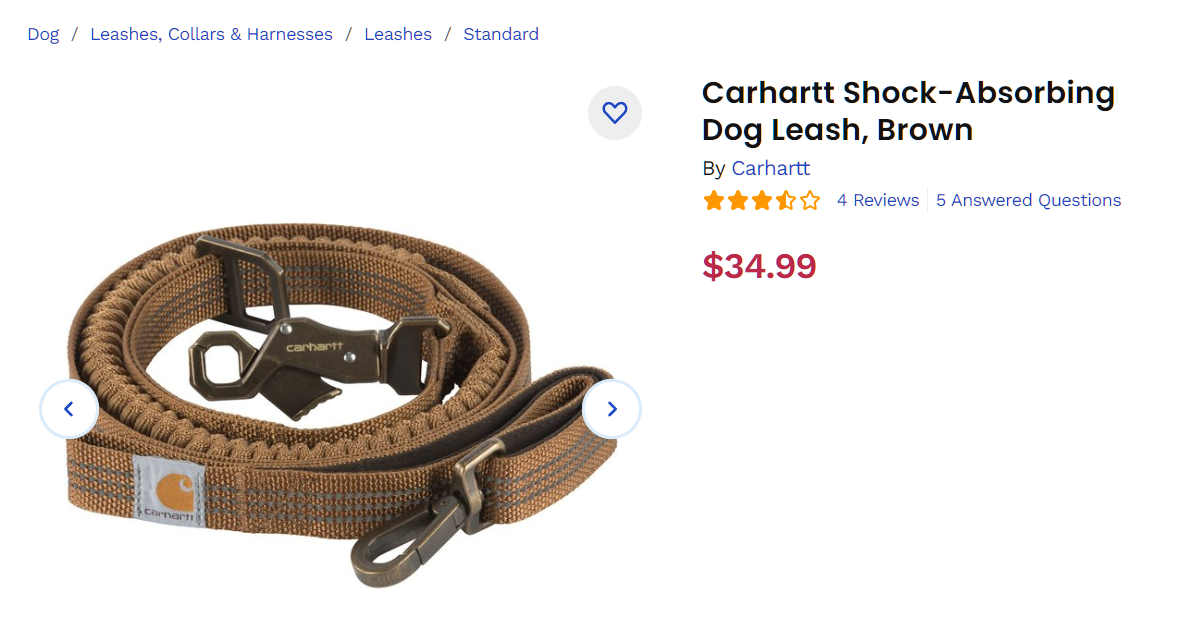

That’s a 33 percent price increase in what the human and AI minds at Chewy.com think that a consumer will be willing to pay. The leash is actually available at $30 from Zappos so maybe this proves our Native American elders correct. Consumers are now so accustomed to Bidenflation that they won’t question dramatically higher prices. This leads to price gouging ($5 worth, in this case) and massive profits.

Large corporations are using inflation as cover to jack up prices and expand their profit margins. We must promote market competition, enforce our antitrust laws, and crack down on corporate price gouging.

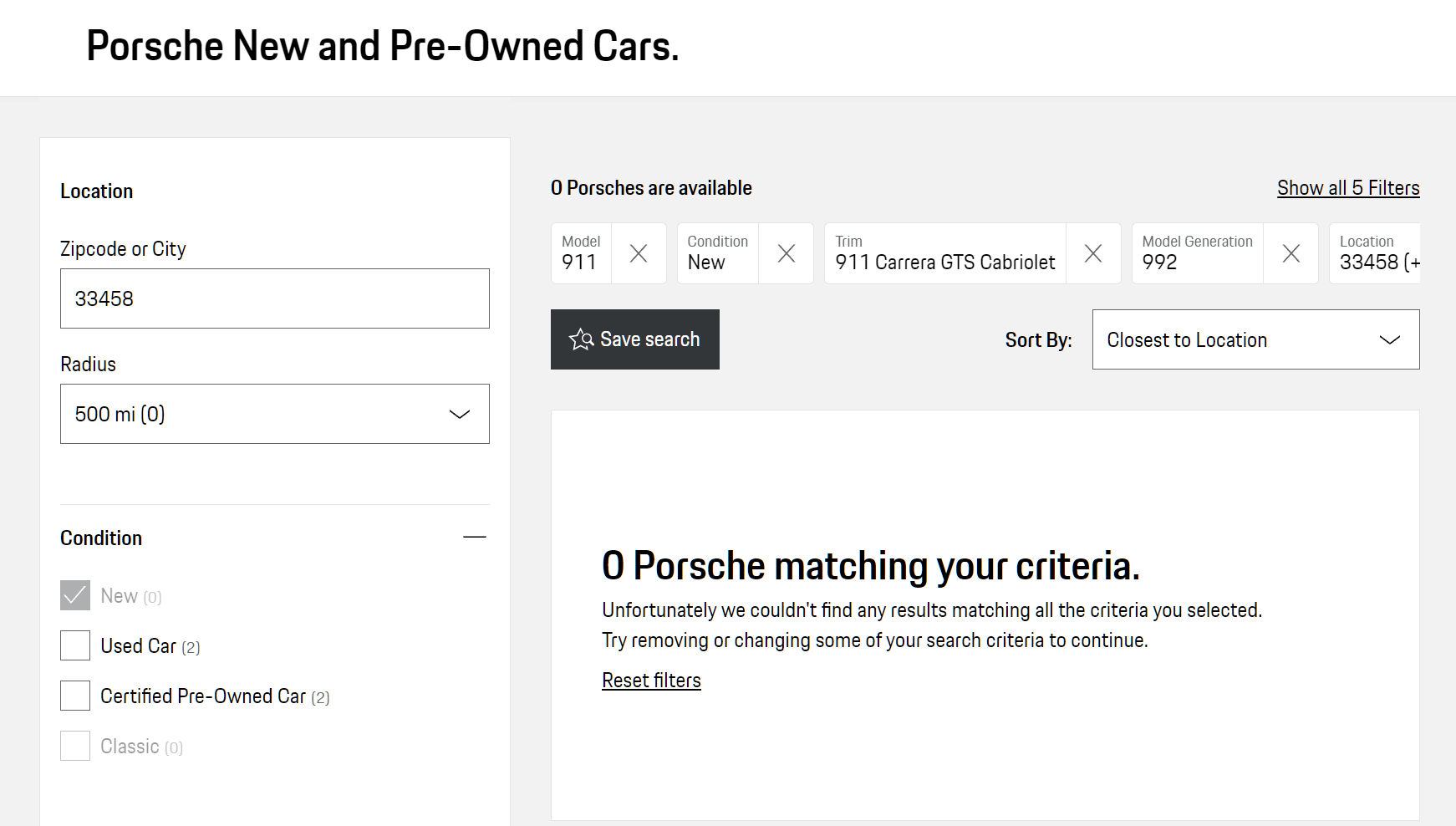

There’s a sports car dealer next to our favorite taco place here in Jupiter. Their lot was jammed with cars, seemingly twice as full as in the summer. From their perspective, the car market turned about 30 days ago. They’re now paying only MSRP for nearly-new (500-mile) C8 Corvettes. What do they turn around and sell them for? It’s a little unclear because they say “We haven’t had a call for a Corvette in 3-4 weeks. The interest rates have killed demand.” (Note that this is contrary to my theory that we have enough deficit spending and inflation-indexed spending to have inflation even if nobody does any borrowing; see Can our government generate its own inflation spiral? and Economist answers my question about high interest rates and high deficits.)

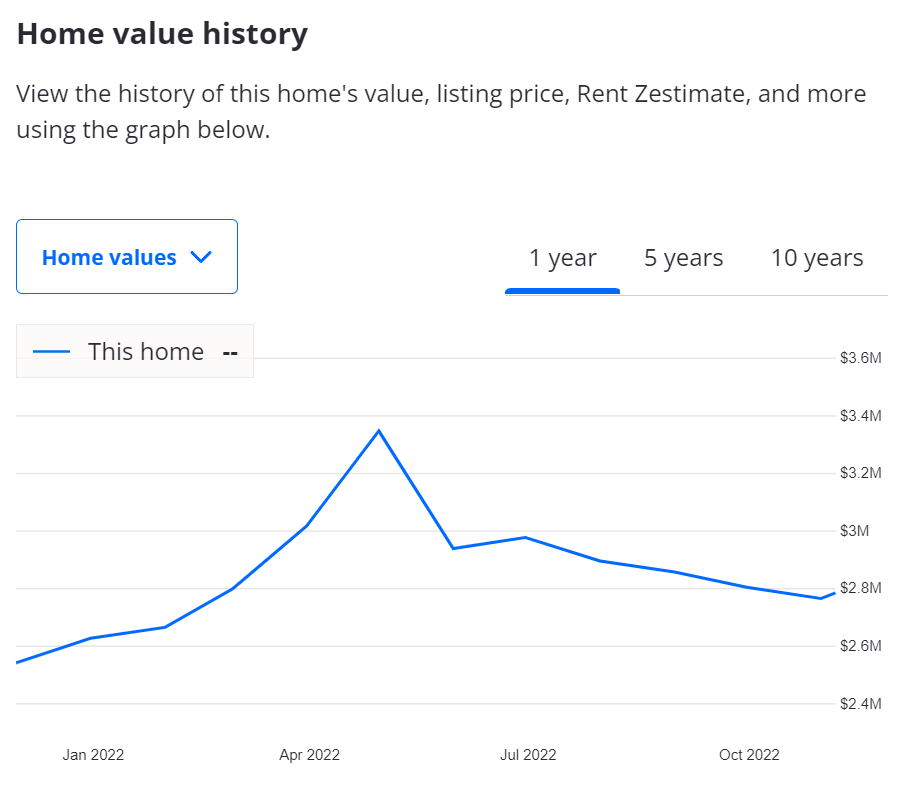

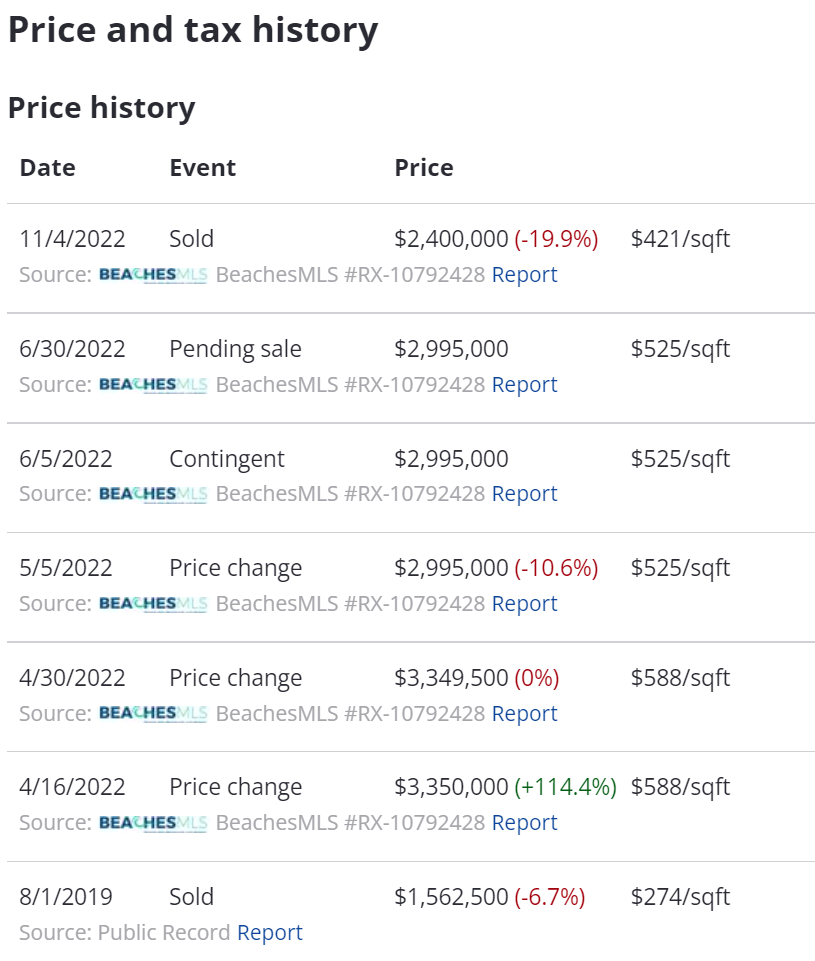

How about real estate? There’s a house in our neighborhood (built by the MacArthur Foundation for middle-class and upper-middle-class people!) whose $3.35 million asking price in April 2022 seemed aggressive, particularly since there was no pool and the new owner would have to lease it back to the sellers until October when the sellers expected their new-built house to be ready.

Here’s the “value history”:

In June 2022, there actually was a greater fool who agreed to pay $3 million for this albatross. But then it seems that this person disappeared or wised up and the closing price was $2.4 million (last week):

If you’re depressed because you forgot to sell all of your assets in March 2022, this message from the taco place might be useful:

If you’re depressed because you were dumb enough to buy a house early in 2022 at early-2022 prices (looking in the mirror is painful!), you can be comforted that you don’t live in San Francisco, which MSNBC uses as shorthand for a truly crummy and crime-plagued urban environment (the MSNBC interviewer says, regarding a higher-crime Manhattan, “We’re worried this could be San Francisco”):

Even MSNBC is calling out Democrat Kathy Hochul.

"Here's the problem: We don't feel safe…I walk into my pharmacy, and everything is on lockdown because of shoplifters. I'm not going in the subway. People don't feel safe in this town." pic.twitter.com/JUKhxXCk4c

Late-night political thought… If prices are guaranteed to keep spiraling upward due to everything the government spends being indexed (see Can our government generate its own inflation spiral?), might Republicans be better off losing all of the Senate and House races on Tuesday? Even if the Republicans earned majorities in both sides of Congress, Joe Biden would likely veto any legislation that cut spending or removed inflation indexing from spending. So the Republicans have no realistic chance of reducing inflation, any more than the Inflation Reduction Act. If they’re totally out of government, only the Democrats will be blamed for the next two years of inflation and maybe that would help Republicans win the White House as well as Congress in 2024.

If we ignore the government inflation spiral-from-indexing effect, how much pent-up inflation is there? I remarked on the price increase for frozen peas (Peaflation at Publix). On a more recent trip, the supermarket shelves were entirely bare for all brands of frozen peas. The market-clearing price for peas is obviously higher than even the new high-ish prices. Similarly, canned pumpkin was sold out. Our 42-inch-wide built-in fridge is dying. Is a Sub-Zero a ripoff at $14,000? Actually, it is underpriced and should go up further according to Econ 101 because it will take a year (a year!) for them to build and deliver one. The company is giving away fridges right now for way less than the market-clearing price.

Isn’t there a good chance that Americans will become disenchanted with whoever wins in 2022? And some might remember Republicans’ absurd campaign promises. Here’s a medical doctor promising to “fix” inflation, which is as plausible as a Scientologist being significantly helpful at a car accident scene (Tom Cruise video; go about 1 minute in).

Inflation is an economic and health crisis – a doctor can help fix it. As PA's next Senator, I'll keep us safe, cut your taxes, and protect our jobs.

Even if Dr. Oz was in possession of an economic policy that would Whip Inflation Now, Joe Biden would surely veto it. Sprinkling a few Republicans into Congress isn’t going to turn around the policies that got the U.S. into this inflationary mess. Will Republicans truly gain by promising to stop inflation and then not stopping it?

Here are the House Republicans implying that voting for them will somehow stop “the highest inflation in 40 years”:

WATCH 📺@GOPLeader slams the Biden administration and House Democrats for their Far Left agenda that has created the highest inflation in 40 years:

Here’s a promise from the Republican House leader to “lead the way” on inflation:

Democrats: —> Defunded the police and made our cities less safe. —> Spent $9 trillion dollars and increased inflation. —> Cut our energy production, and made you pay more at the pump.

It’s time to chart a better course. Republicans are ready to lead the way.

The big story of the year is the worst inflation in almost 40yrs. It is a tax on Americans. Families have had to spend $3,500 more than they did last year just to tread water. It is directly attributable to Democrats' multi-trillion-dollar inflationary spending earlier this year. pic.twitter.com/NgwT9Q70qB

But Congress has never been able to cut spending (which spirals upward with inflation automatically). And the Republicans won’t support tax increases. So the deficit spending will continue even if Mitch McConnell and fellow Republicans can win a majority.

What’s different this year? Inflation means that ordinary schlubs can pay tax rates that were sold as applying only to the elite. The Obamacare “Net Investment Income Tax” of 3.8 percent on top of ordinary income and capital gains taxes, for example, wasn’t supposed to hit Joe Average. But what if Joe Average tried to escape the lockdowns and school closures in California by selling a house and moving to Texas? Adjusted for inflation in the real estate market, his house might not have gone up in value at all. In other words, his purchasing power from selling the house to buy a different house wouldn’t have changed (probably reduced, actually, in terms of how big a house in Austin can be purchased with the proceeds from selling a house in California). But almost surely he will have more than $250,000 in nominal gains. This is all an illusory inflation-driven “gain” and the tax code recognizes that to a small extent by excluding the first $250,000 of house price inflation. But on the rest of it, Joe will have to pay California capital gains tax, Federal capital gains tax, and an additional 3.8 percent for Obamacare. From the IRS:

The Net Investment Income Tax does not apply to any amount of gain that is excluded from gross income for regular income tax purposes. The pre-existing statutory exclusion in section 121 exempts the first $250,000 ($500,000 in the case of a married couple) of gain recognized on the sale of a principal residence from gross income for regular income tax purposes and, thus, from the NIIT.

How about a wage slave? If he/she/ze/they was earning $170,000 in 2019 and got bumped to $210,000 in 2021, his/her/zir/their spending power is actually lower due to raging inflation. Yet now he/she/ze/they is subject to the 0.9 percent Obamacare “Additional Medicare Tax” due to having income over a fixed threshold of $200,000 (soon to be the price of a Diet Coke?).

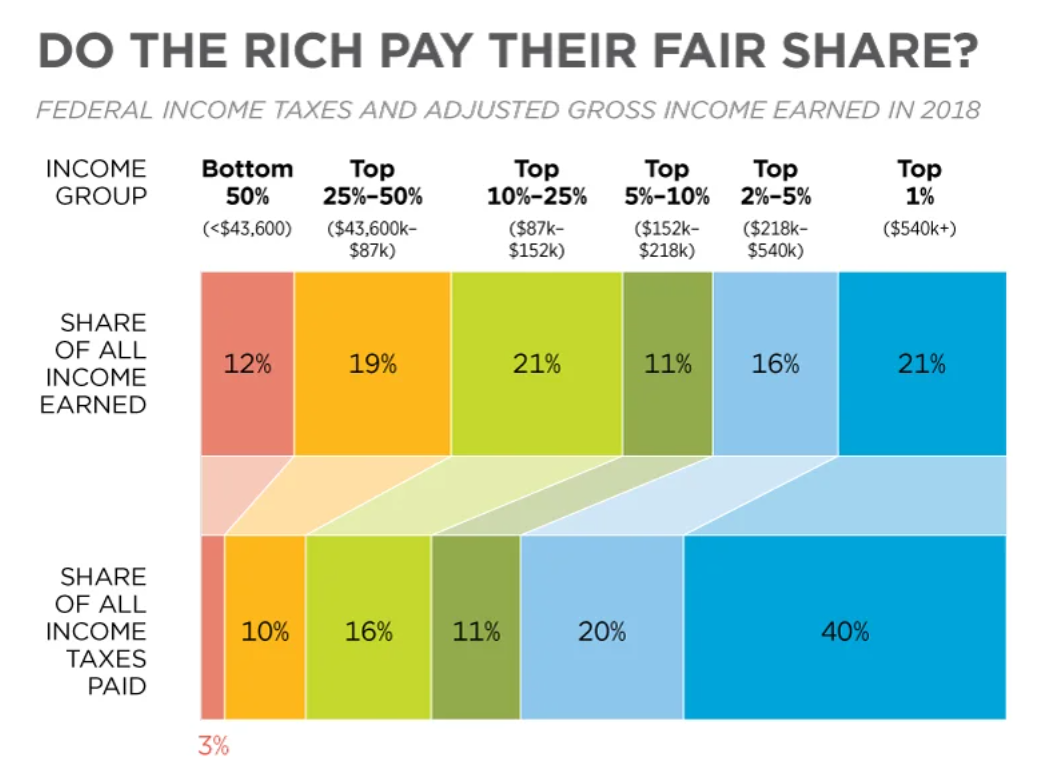

What kind of people are paying the bill for all of the great work done by Congress and Joe Biden? From the haters at Heritage Foundation:

In 2018, due to the cruel policies of the dictator Donald Trump, the rich Americans who earned 21 percent of all income paid only 40 percent of income taxes. Separately, keep in mind that the above chart relates to cash income. A person could be in the “Bottom 50%” with $0 in W-2 income and still have a spending power and lifestyle better than someone earning $50,000 per year (in the “25%-50%” column) due to means-tested public housing, health care, SNAP/EBT, smartphone, and broadband. See “The Work versus Welfare Trade‐Off: 2013” (CATO) for the states where being on welfare leads to a larger spending power than working at the median wage. Maskachusetts is #3 in Table 4, with welfare being worth 118% of median salary.

This machine has brewed its last cup. How much is the new one?

The $42.39 price is 42 percent inflation relative to the $29.88 price paid in 2017. What does the official government site say? It should cost $35.88 (20 percent inflation).

Separately, if you don’t like the weak Keurig coffee, you might enjoy this one though it is slightly more effort. Keurig is trying to be French press coffee, but with minimal contact time between water and grounds. A standard drip machine like this yields a more intense drink.

The government has been shoveling out cash to people who don’t do anything to earn it while at the same time trying to stanch the inflation bleeding with high interest rates charged to those who might have a productive purchase for money. Our best and brightest can’t figure out why inflation persists.

Until a few months ago, we paid $1.99 for 16 oz. of frozen peas. Now it is $2.29 for 15 oz. That’s 23 percent inflation.

Related:

“Frozen food category surges amid inflation: ‘It’s a dramatic shift,’ says food exec” (Yahoo! Finance, May 2022): Saffron Road’s Durrani added that “frozen is now considered an ESG value,” as well— representing yet another benefit to the overall category. …”Consumers are making a discerning choice to pay up for ‘better-for-you’ brands,” he continued, adding that the brand upped its pricing twice since the start of the pandemic — once last year (+5%) and again this year (+5%). “We haven’t seen any backlash when it comes to those price increases,” he revealed.