In a recent phone call regarding correct Christmas Card mailing addresses, a nurse friend in Boston told me that she’s moonlighting providing anesthesia at an abortion care clinic. Anesthesia is required starting at about 10 weeks of gestation and the clinic provides abortion care to pregnant people who are up to 24 weeks pregnant. She said that they are especially passionate about providing abortion care to pregnant people who’ve come from states where abortion care is illegal or unavailable in practice at the 24-week mark.

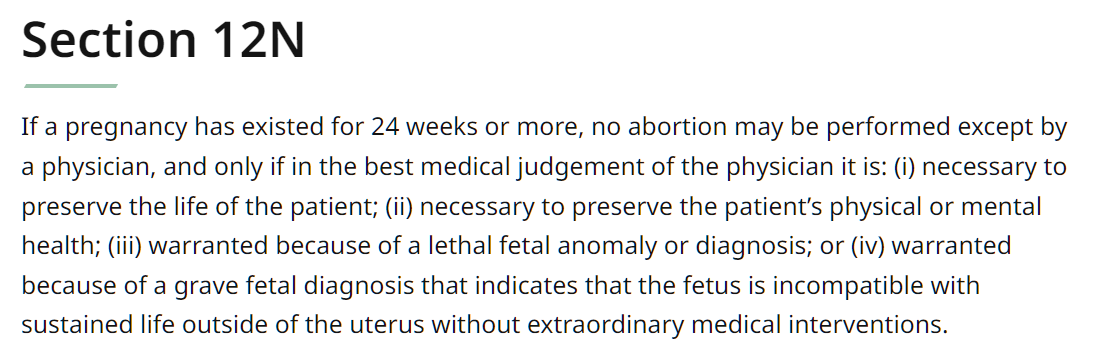

Who decides how long the pregnant person has been a pregnant person? “That’s done with a combination of ultrasound looking at bone sizes and also asking the patient about the date of the last period.” In other words, depending on what the ultrasound shows, the clinic might refuse to provide abortion care to a pregnant person who has been pregnant for only 23 weeks or, if the customer gives a later-than-reality last-period date, to a pregnant person who has been pregnant for more than 24 weeks, which is still perfectly legal in Maskachusetts:

(Note the “mental health” judgment item.)

What’s the revenue picture for the clinic? “Prices start at $600,” she replied. What about for abortion care at 23.99 weeks? “I think it is about $3,500.”

What’s her daughter up to? I learned about various biomedical internships for the college undergrad. “She wants to go to medical school and become an ob-gyn.” I told my nurse friend about our neighbor who does IVF and who tells people if their insurance won’t cover the astronomical cost to get a job at Starbucks where they’ll be immediate covered. “Oh, my daughter wants to work on the other side of O.B. She wants to work in an abortion clinic where women [hateful term quoted; her language, not mine] come from out of state if they can’t get abortions in their own state.”

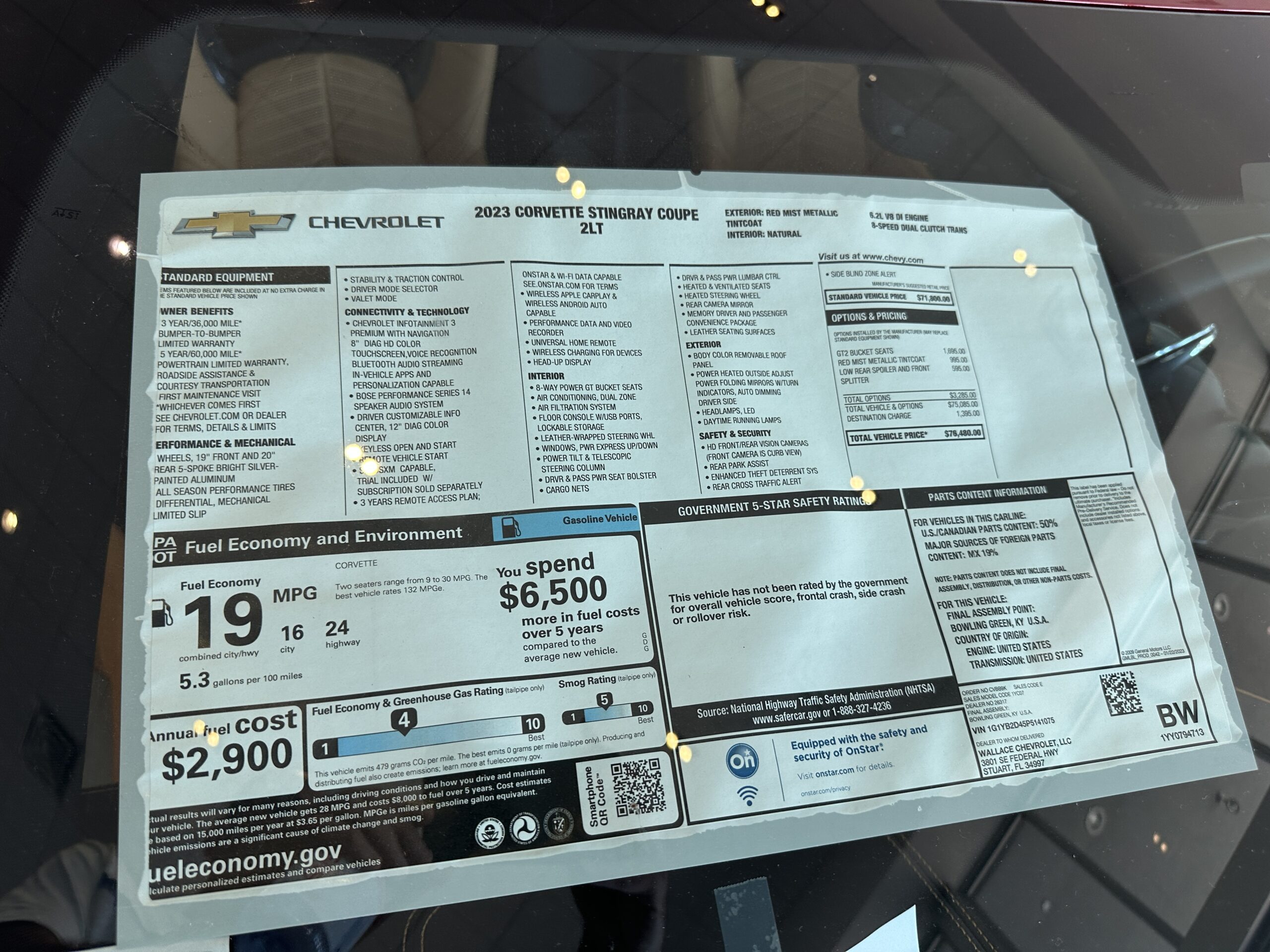

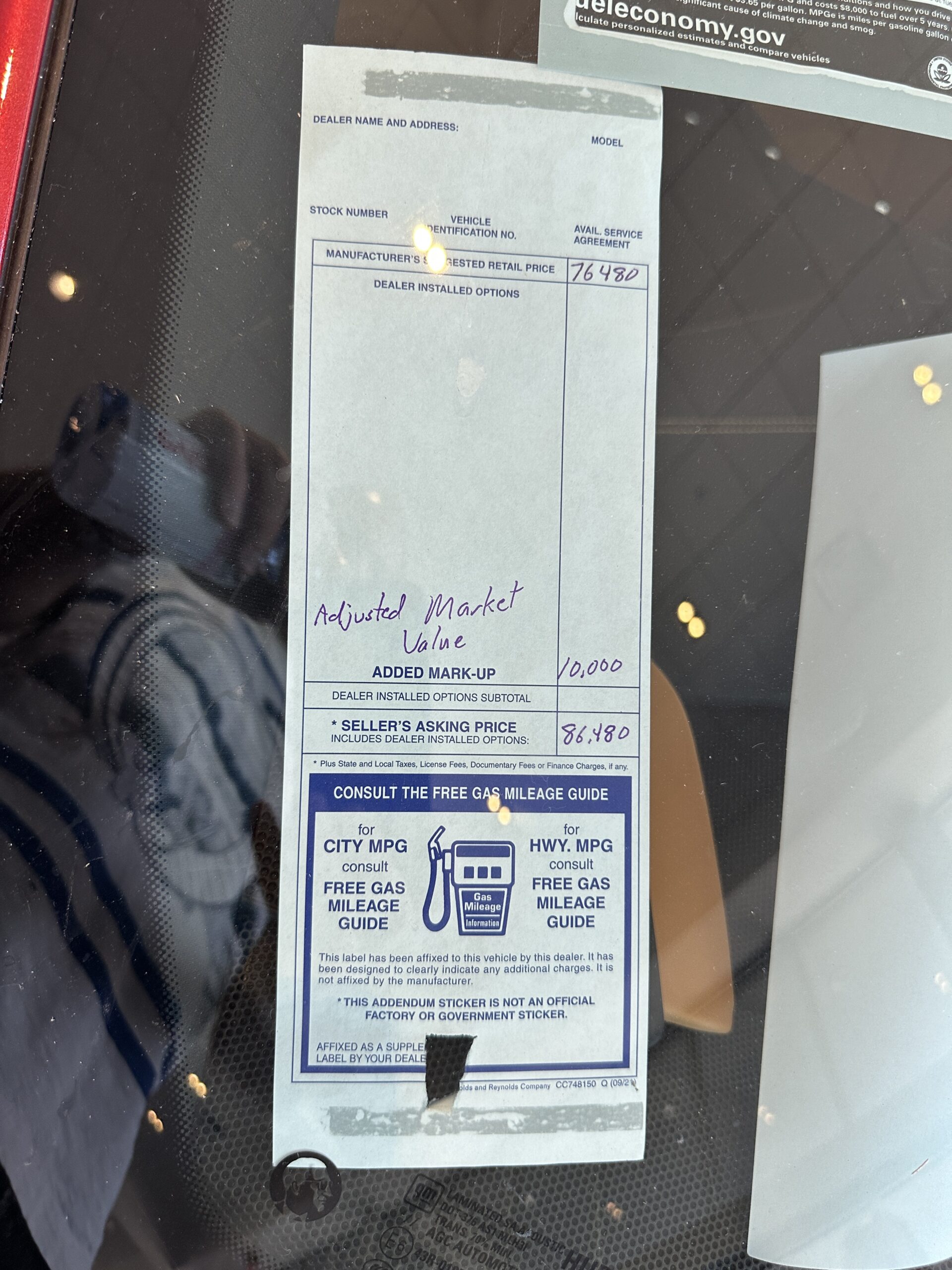

At a Chevrolet dealer in Stuart, Florida on September 15, I learned that not-in-demand cars are selling at MSRP sticker price, leaving the dealer with $4000 more in profit than in the old days when the cars sold at invoice. In-demand cars continue to carry an additional markup. For example, an electric Chevy is $10,000 over sticker, as is a regular Corvette. A Z06 Corvette is $75,000 over sticker on those rare occasions when the dealer can get one.

Can you save some $$ by buying used? A three-year-old 2020 Corvette 3LT (the premium trim) is available for $95,800, which I’m sure is more than its original sticker price.

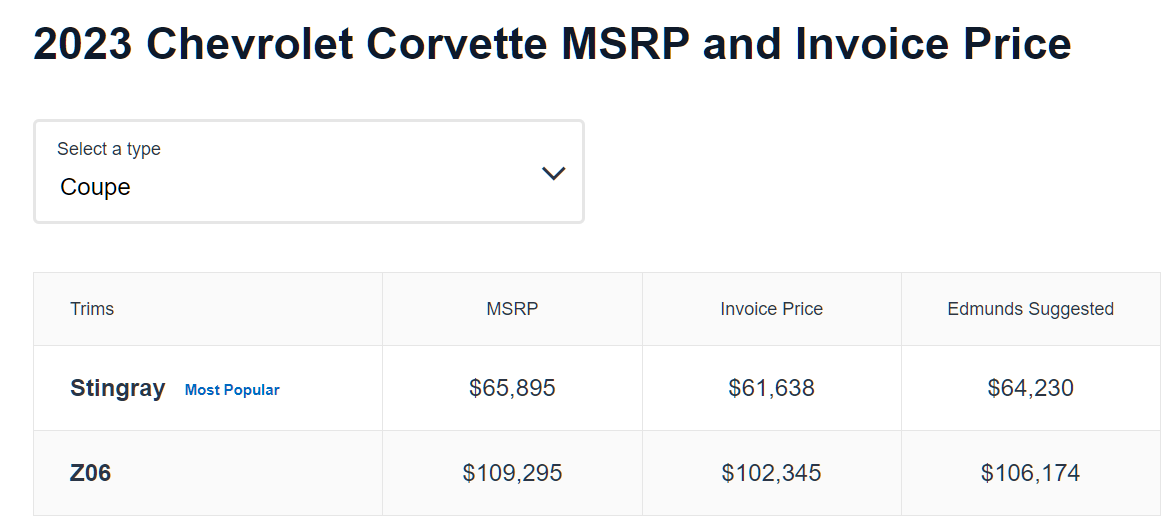

Let’s look at the Z06 Corvette. Here’s what Edmunds says about the simplest model:

According to the official prices, GM thought that the dealer would get about $7,000 in profit from selling this car. In the post-coronapanic world, however, the dealer will get $82,000 for taking an order (the difference between MRSP+$75,000 and invoice).

I’m wondering if this is why the car shortage has continued for so long. Ordinarily, if something goes up in price the producers get paid a lot more and begin working hard to increase production. If gasoline becomes more expensive, for example, gas stations don’t become insanely rich while oil producers keep getting the same old price. The gas station gets its usual small markup and the extra money for petroleum products goes to the oil company, precisely the signal that the market is supposed to give to producers in Econ 101. The legacy automakers, however, never got any financial signal that cars were in demand. Nearly all of extra money paid by consumers went to dealers, who responded by buying new beach houses, new business jets, new jet-powered helicopters for their kids, new yachts, European vacations, etc. The boost in auto prices, thus, spurred production of business jets more than production of cars.

I wrote about this back in 2022: Why aren’t cars (and pinball machines) auctioned as they come out of the factory?. The dealer agreement that I found did not prevent the manufacturer from abandoning a fixed retail/invoice price structure and instead simply auctioning cars to dealers or at least establishing a new market-based price every week. Nothing in the agreement required a manufacturer to keep the price to the dealer fixed for 6-12 months, as has been conventional for legacy automakers even during coronapanic.

Tesla, of course, has been a notable exception. The company has made frequent price adjustments throughout this period of lockdown-induced economic disruption. Thus, Tesla has had a financial incentive to maximize production, e.g., paying chip suppliers extra money if necessary to keep the lines going.

Let’s also consider the recent strike by the United Auto Workers, of whom roughly 146,000 work for the Detroit Three. They want a 40 percent pay increase to compensate for the inflation that the government says does not exist. Could the legacy car companies easily afford to pay this if they hadn’t been selling cars for far less than they were worth for nearly three years?

I think that the Detroit 3 have U.S. revenue of about $300 billion per year, combined. Let’s say that they could have gotten 10 percent more money by selling cars for what they were worth instead of selling them for whatever invoice price they’d established. That would have worked out to approximately $90 billion in additional revenue over three years. In other words, they could have given each UAW member a $600,000 coronapanic bonus and still had money left over to give to shareholders.

Should all of the executives at the Detroit 3 be fired? Every day they produced assets owned by shareholders, i.e., the cars coming off the assembly lines. Every day they sold those shareholder-owned assets for far less than they were worth. They enriched the dealers to whom they owed no fiduciary duty. They starved their own production facilities of the extra cash that could have been used to motivate suppliers, workers, etc. to maximize production and ease the supply shortage that has cost consumers so dearly (and helped to generate ugly inflation numbers). They failed to capture the cash that the UAW is now on strike to obtain.

Related:

One thing that keeps the Detroit 3 afloat is a 25 percent tariff on light truck imports imposed by Lyndon Johnson (Reason), though Wikipedia says that a Mexico-built truck wouldn’t be subject to the tariff

According to the economic logic used by enthusiasts for low-skill immigration, even the lowest skill migrant makes Americans richer because he/she/ze/they causes some sort of bump in economic activity, thus increasing the aggregate GDP.

I wonder if Danilo/Danelo Cavalcante should win Migrant of the Year 2023. By escaping from a Pennsylvania Prison, he is responsible for at least 500 police officers receiving two weeks of overtime pay (timeline). He’s 34 and has been sentenced to life in prison, so that will boost the U.S. economy by at least $50,000 per year for the next 50 years or so (see “Pa. spends over $40k a year per inmate.” but remember that the $42,727 per year number is in pre-Biden dollars).

The dramatic encounter with Cavalcante, involving a helicopter, a lightning storm, a police dog and more than 20 tactical officers, led to his capture around 8 a.m. Wednesday morning, authorities said.

So the migrant can also take credit for some Jet A sales and the overhaul reserve for what was very likely a $3-6 million Eurocopter (helping the French and German economies too!).

Why is the U.S. criminal justice system so interested in this Migrant of the Year?

According to prosecutors, he stabbed Brandão 38 times in front of her two young children in Pennsylvania in April 2021. He was arrested several hours later in Virginia, and authorities said he was attempting to flee to Mexico and intended to later head to Brazil, his native country.

In addition, Cavalcante is also wanted in a 2017 homicide case in Brazil, a US Marshals Service official has said.

Like the New York Times, the Wall Street Journal has worked tirelessly to spread the Good News about the Miracle of Low-Skill Migration. An example from 2015… “Migrants Offer Hope for Aging German Workforce”:

By some estimates, Britain is on course to eclipse Germany as Europe’s biggest economy by 2030, thanks in part to its large numbers of young, energetic immigrants.

Germany “is going to be severely challenged” by demographics, said Peter Sutherland, the United Nations special representative for international migration. Managing the trends “requires a great deal of proactive thinking” and openness to immigration, he said.

About 20% of asylum seekers were from war-torn Syria—more than from any other country—and four out of five arriving Syrians are believed to be from “average or even well-off economic circumstances and have a good education,” the agency said.

In the 1950s, Italians and other Southern Europeans flooded in to help rebuild the country, contributing significantly to its fast postwar economic recovery. In the following decades, millions of Turks arrived and many ended up working in German industrial companies, helping its economy more.

Europe’s current predicament has been long in the making. An aging population with a preference for free time and job security over earnings ushered in years of lackluster economic and productivity growth.

Adjusted for inflation and purchasing power, wages have declined by about 3% since 2019 in Germany, by 3.5% in Italy and Spain and by 6% in Greece.

Karim Bouazza, a 33-year-old nurse [in Brussels] who was stocking up on half-price meat and fish for his wife and two children, complained that inflation means “you almost need to work a second job to pay for everything.”

The eurozone economy grew about 6% over the past 15 years, measured in dollars, compared with 82% for the U.S., according to International Monetary Fund data. That has left the average EU country poorer per head than every U.S. state except Idaho and Mississippi, according to a report this month by the European Centre for International Political Economy, a Brussels-based independent think tank. If the current trend continues, by 2035 the gap between economic output per capita in the U.S. and EU will be as large as that between Japan and Ecuador today, the report said.

Apparently, expert consensus is that there is no longer a connection between low-skill migration and economic vibrancy. The 2023 WSJ article does not contain any of the following words or phrases: “migrant”; “immigrant”; “refugee”; “asylum-seeker”.

Separately, here’s a luxury car in one of Europe’s richest countries, the Netherlands (photographed in Delft, July 6, 2023):

The Netherlands now contains 27 percent migrants and children of migrants and thus should be insanely rich if we believe the Wall Street Journal’s 2015 Science.

How is the Omada system working, you might ask? Quite well, but there are occasional failures of the upstream connectivity between the Arris cable modem that I purchased and Xfinity and these require power cycling the Arris device to restore. The software being run by the Arris device is controlled by Xfinity and it looks as though there hasn’t been an update for two years (see this post regarding the same issue from December 2020; the software image name is the same as what our Arris reports running).

Anyone else noticed that long-scarce items are available once more?

The scale rates every applicant from zero to 99, taking into account their life circumstances, such as family income and parental education. Admissions decisions are based on that score, combined with the usual portfolio of grades, test scores, recommendations, essays and interviews.

In other words, if your parents were unsuccessful, UC Davis wants you as a medical student!

The NYT article actually confirms the UC Davis economists’ conclusions:

There is also a family dynamic. Children of doctors are 24 times more likely to become doctors than their peers, according to the American Medical Association. It’s hard to know why the profession passes down from generation to generation, but the statistic drove the association to adopt a policy opposing legacy preferences in admissions.

The tendencies to enjoy sitting in biology lectures, studying for tests, and slicing up cadavers are “passed down from generation to generation” but the Followers of Science at the New York Times can’t come up with an explanatory mechanism.

Separately, let’s have a look at UC Davis’s most famous recent pre-med major, Carlos Dominguez. KCRA:

Dominguez came to the U.S. near Galveston, Texas in 2009 from El Salvador.

A U.S. and Immigration and Customs Enforcement official confirmed to KCRA 3 that ICE has placed a detainer with the Yolo County Sheriff’s Office, which means the agency would take custody of Dominguez should he be released from local custody.

Detainers are requests to state or local law enforcement agencies to remove non-citizens arrested for criminal activity once they have been released from their custody.

The ICE official referred to Dominguez as Carlos Alejandro Reales-Dominguez and said his immigration case had been closed in April 2012. He had come to the U.S. as an unaccompanied minor from El Salvador in 2009 near Galveston, Texas, and was transferred to a family member at the time.

Mr. Dominguez thus will qualify for preferential admission to UC Davis Medical School due to the adversities of (1) being an undocumented immigrant, and (2) having an encounter with our racist criminal justice system.

The good news for folks who actually live in Davis, California, is that their health is guaranteed to be excellent because the town is rich in (“essential”) marijuana:

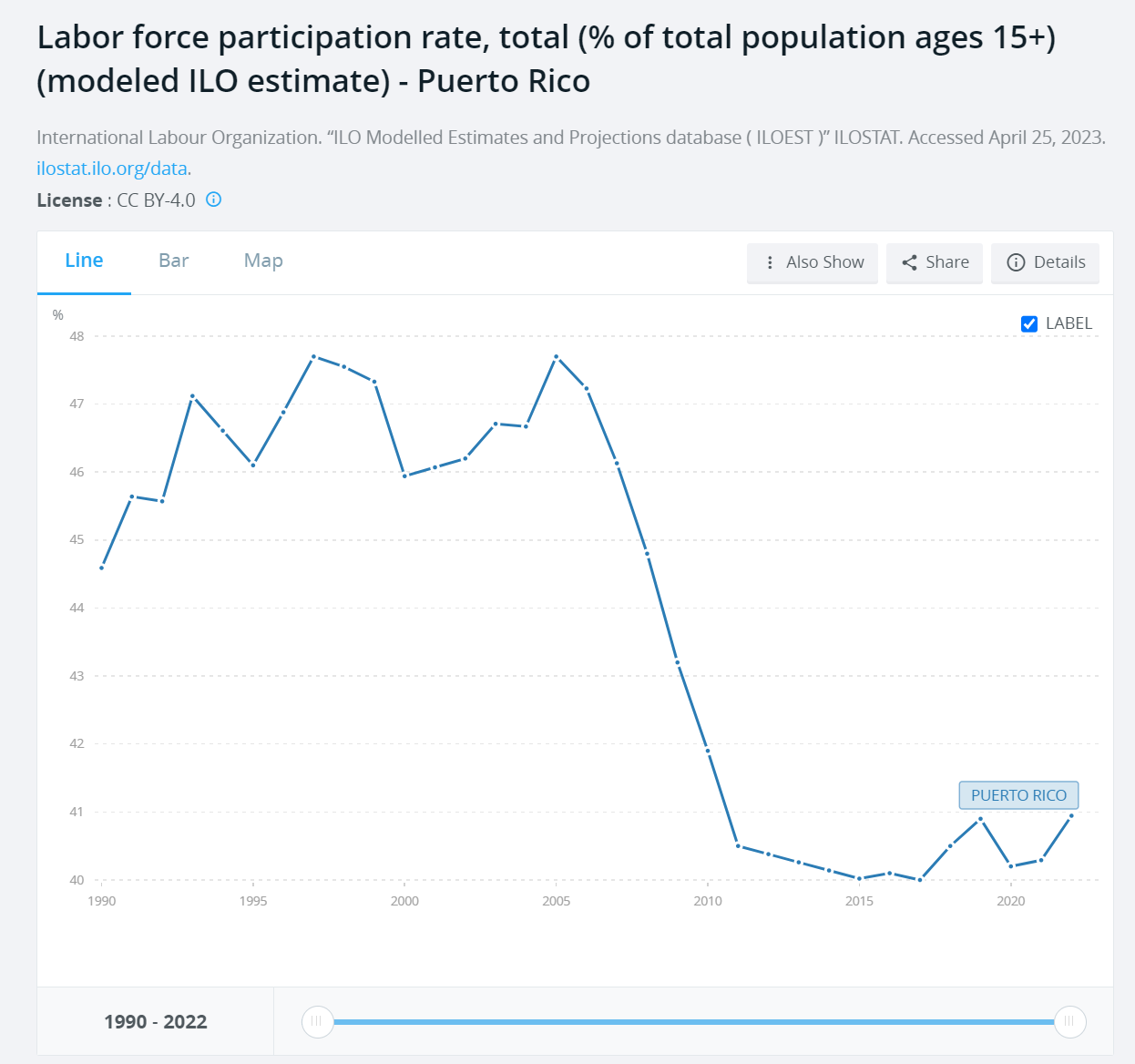

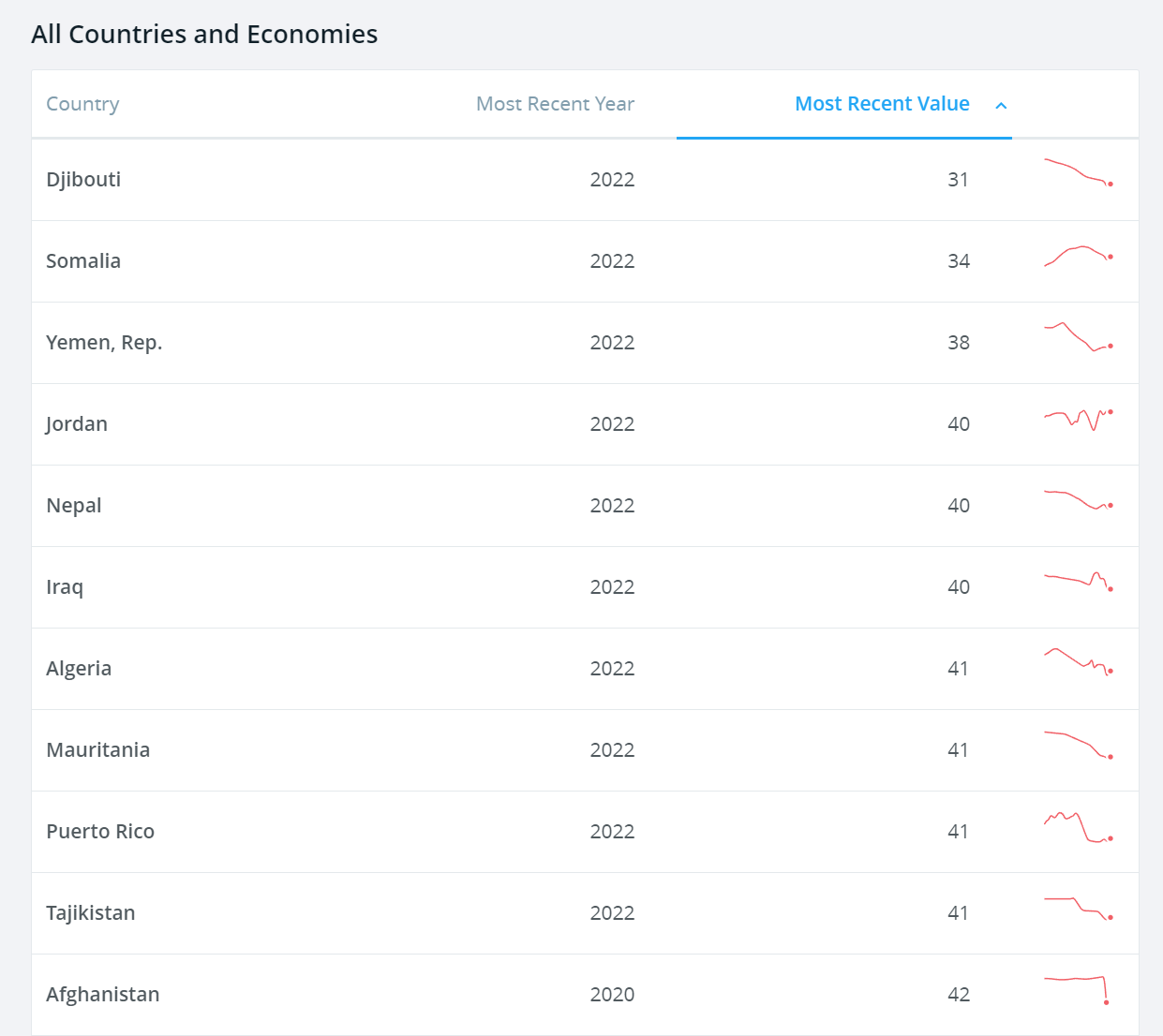

From the World Bank, here’s a chart of labor force participation in Puerto Rico:

41 percent of the folks who are 15+ work. Compare to 70 percent in Singapore, New Zealand, Jamaica, and Ghana. Where can we go to find places where people are less likely to work? Djibouti!

the mainland U.S. way to exit the labor force… “Kevin Costner’s estranged wife is requesting $248K a month for child support amid divorce” (Today): In her declaration, Baumgartner states that she has no income and has been a stay-at-home parent since welcoming Cayden in 2007. … [Costner] had also paid [the plaintiff] the prenup’s required $1,000,000 after she filed for divorce. Baumgartner’s filings on June 16 state that she has not touched the money Costner paid her pursuant to their prenup. “I believe that Kevin’s goal is to get me to tap into this money, so he can argue that I’ve waived my right to challenge the Premarital Agreement,” she wrote, adding that she “cannot make this concession (and does) not accept payment.”

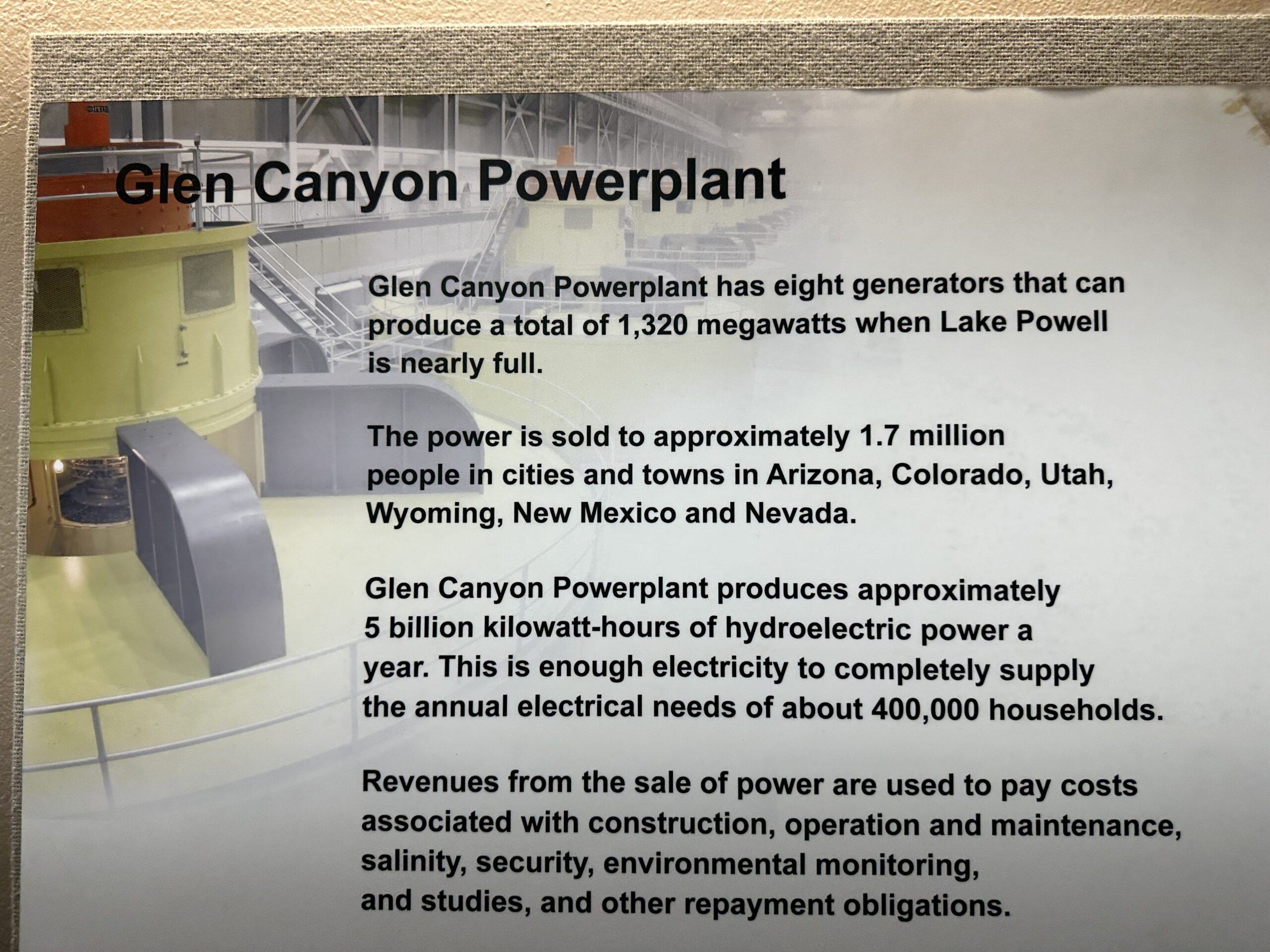

We recently visited the Glen Canyon Dam, which destroyed Glen Canyon and replaced it with a reservoir to hold surplus water in a river that doesn’t have any surpluses (calculations were made in the early 20th century, a period of remarkable wetness when compared to the previous 800 years). From the Carl Hayden Visitor Center:

(Is the visitor center named after a senior engineer who made the dam possible? One or more of the 18 workers who died so that the dam could live? No. It is named for a U.S. Senator who funneled tax dollars into this project.)

The dam powers 400,000 households, which means that the trashing of what would have easily qualified as a National Park does not generate enough power for the houses that are occupied by a single year of immigration into the U.S. What did this cost?

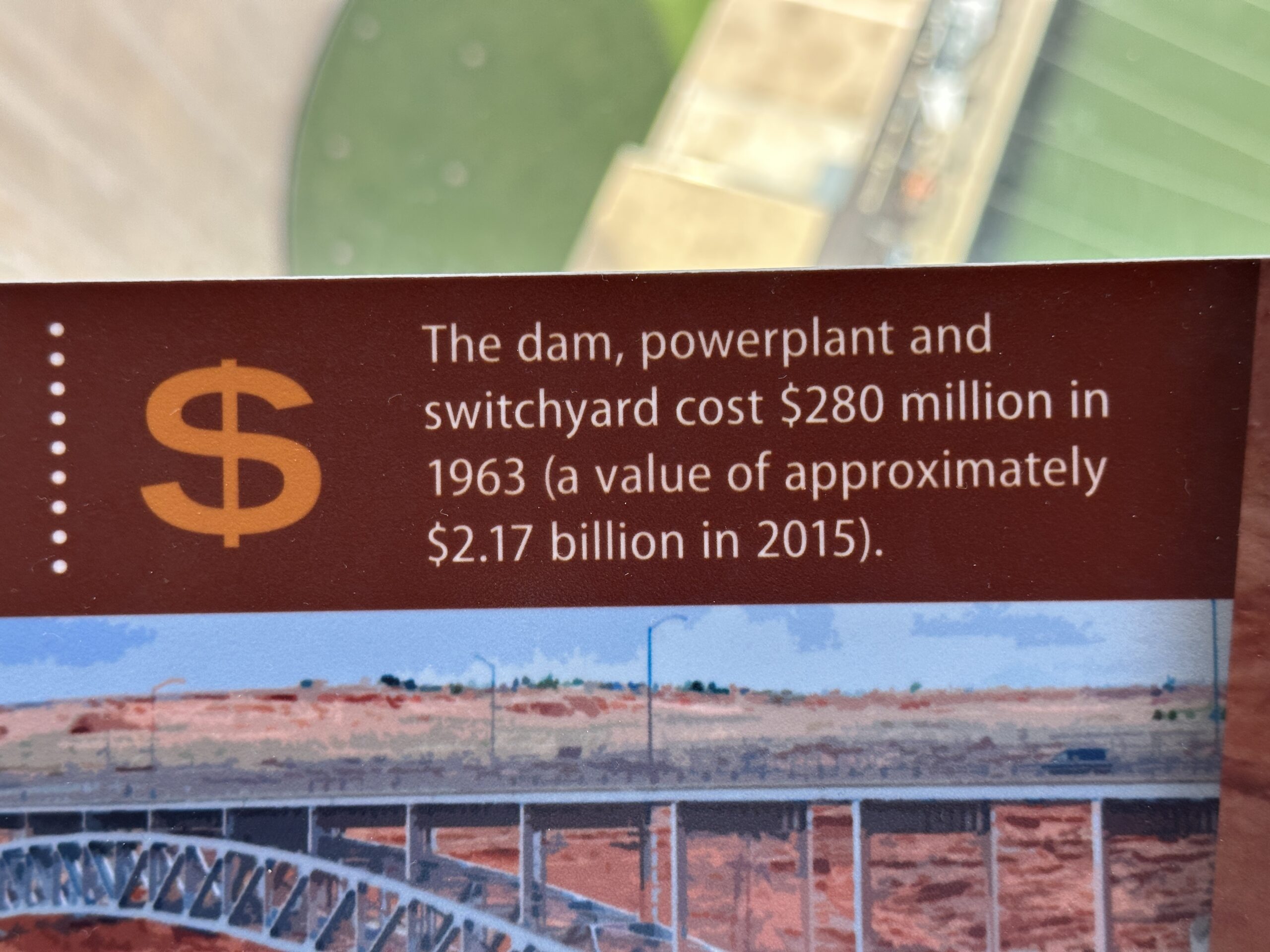

$2.17 billion in pre-Biden (2015) money. The BLS says that this is roughly $2.82 billion in Bidies. If we can arrange for God to give us a new raging river ever 3-6 months suitable for damming, in other words, we can provide clean hydropower to the new American households formed by migrants at a capital cost of $7,000 each.

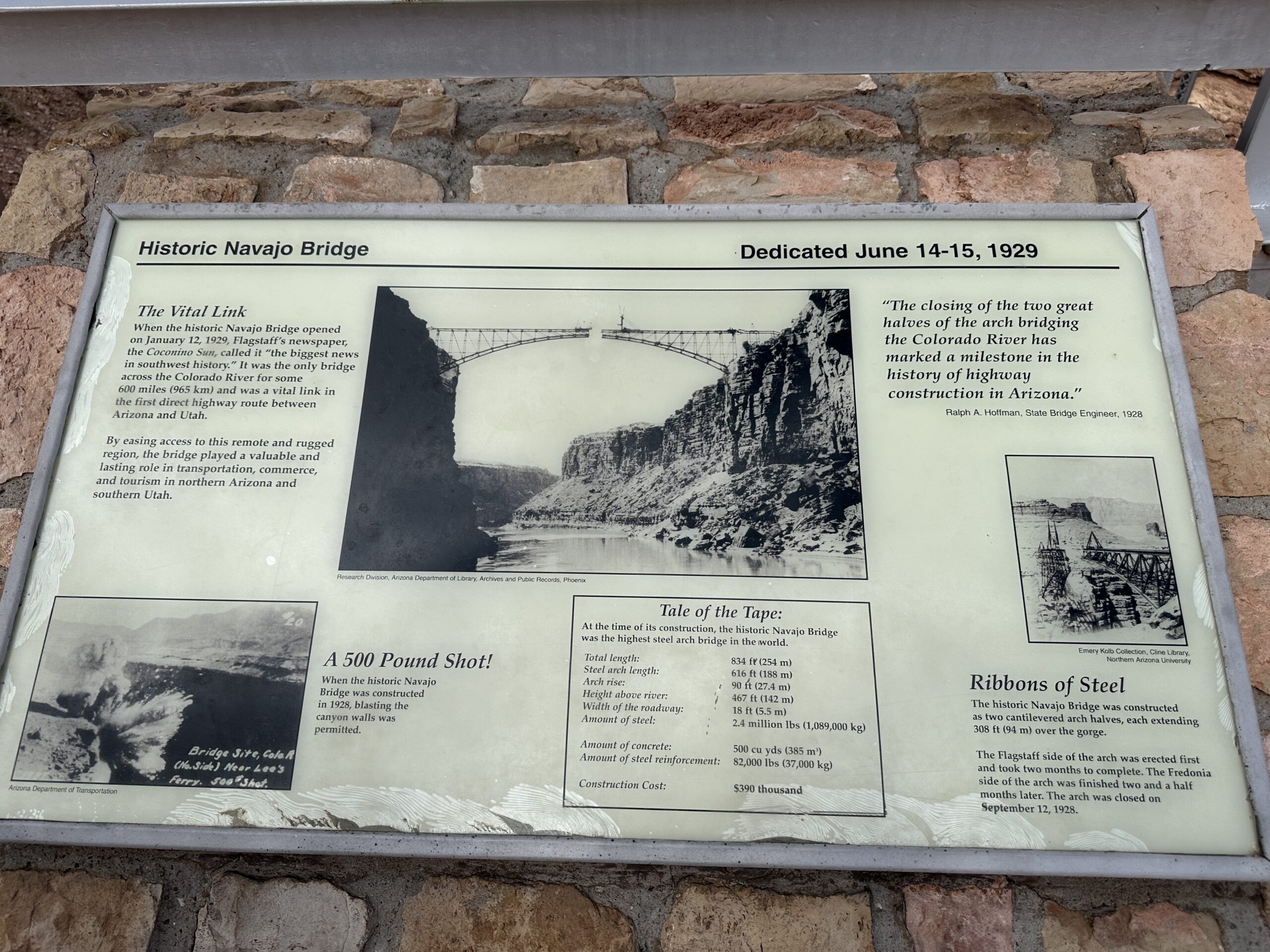

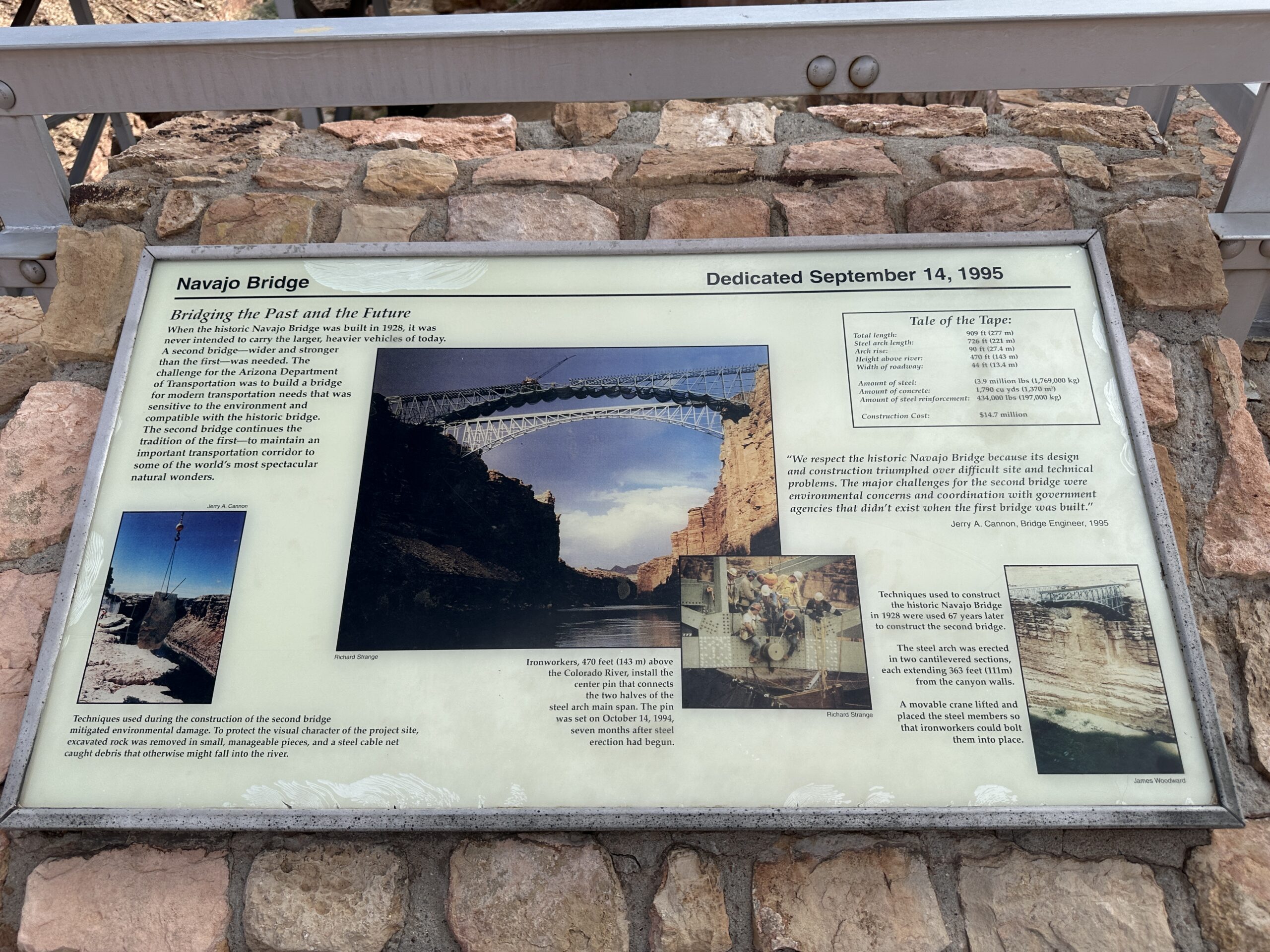

On the third hand, maybe it would cost us a lot more today to build a monster dam. At the Navajo Bridge, just downstream of the dam, the government notes that modern construction techniques are similar to what we used in 1929, but bureaucracy and regulation are dramatically more challenging:

How much inflation has there been in concrete-rich power-generating facilities? We can look at nuclear plant construction. This 2019 paper says that the cost has gone up about 10X, in constant dollars, compared to the 1970s (takes us twice as long as costs 5X as much per day). If we had help from God (new river ever 6 months), in other words, it would cost $70,000 per new household (see How much would an immigrant have to earn to defray the cost of added infrastructure?) to provision the power generation infrastructure.

(Comparison: progressive technocrats in California have spent $9.8 billion so far on their high-speed rail dream… without laying even one mile of track (CNBC).)

What would Glen Canyon look like if this massive silt-collecting dam hadn’t been built? Here’s the Horseshoe Bend, just downstream, photographed at 0.5X on the iPhone 14:

What does the dam look like?

A concrete salesman’s dream! Note that last bucket of concrete was poured in September 1963, the same year in which your beloved (I hope) blog host was born. The project was supposed to take 6.5 years, including all of the prep work and the bridge, but was finished after 6 years for substantially less than forecast (by Kiewit, whose Boston Harbor project was rendered lethal by government bureaucrats as described in Book review for Bostonians: Trapped Under the Sea).

What if a group of evil people identifying with one of the 73 non-female genders decided to oppress those identifying as “female” by taking away $5,000 to $10,000 from every reasonably successful family with a daughter? Would Americans resist this attempt to take away important capital that could otherwise be used to give a young woman an education, startup capital, travel experiences, etc.?

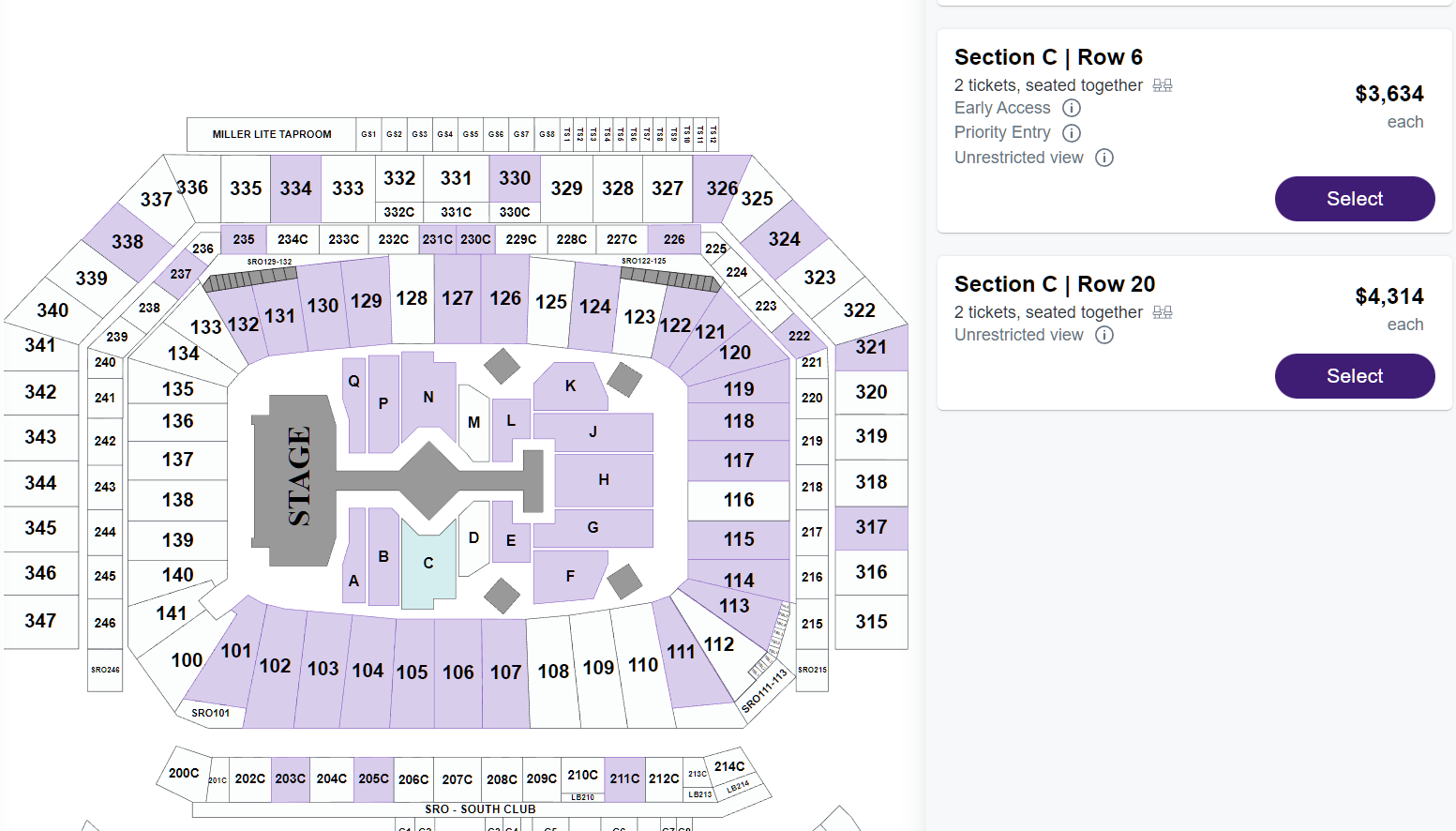

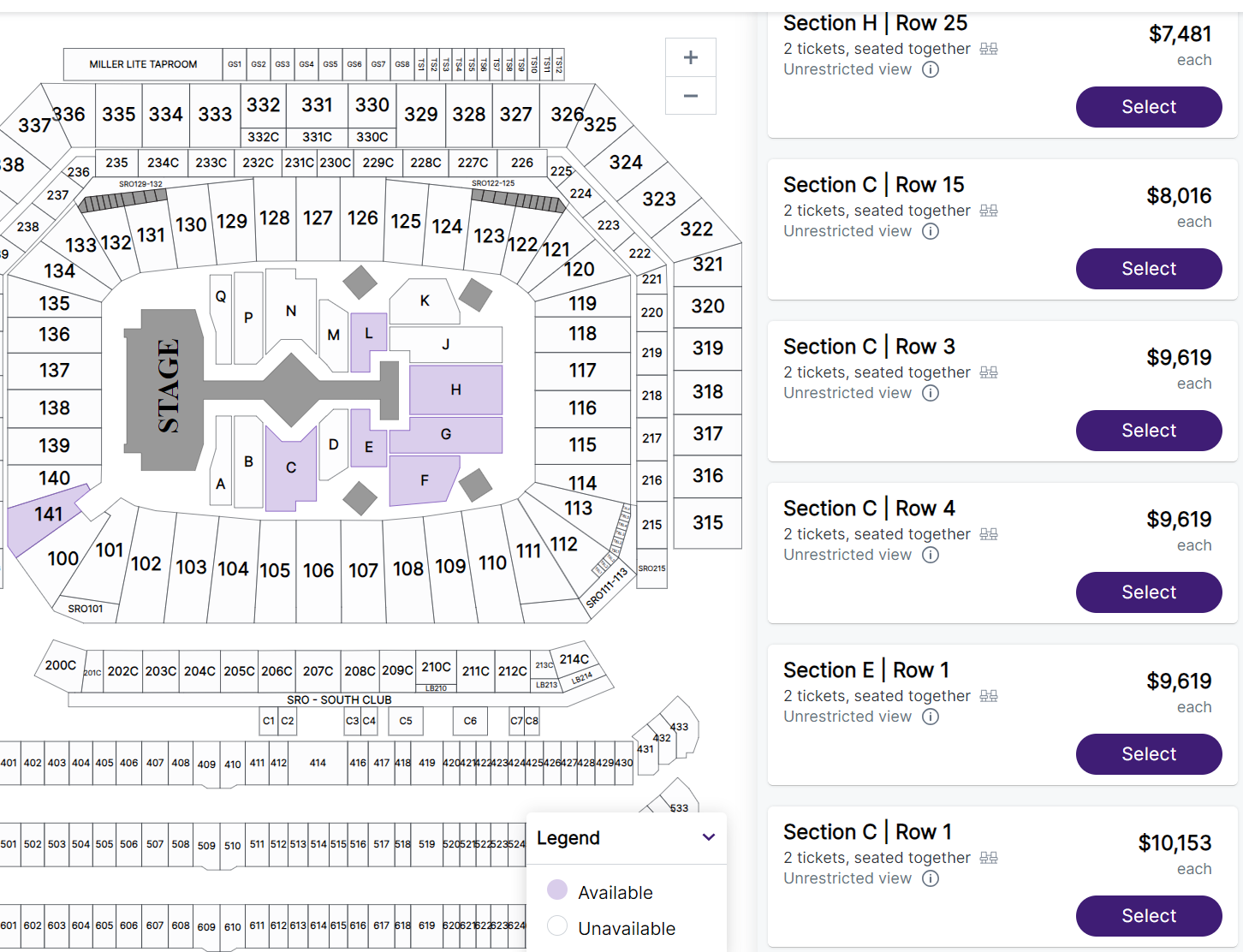

Here’s what StubHub was offering, on May 20, for seats at the Taylor Swift tonight in Detroit, Michigan:

You can buy a house in Detroit for the cost of two tickets (StubHub fees are on top of these quoted rates?) and associated concert expenses.

What will be the long-term effects of this brilliant mining out of families with female children? Wikipedia says that Taylor Swift is childless and “an advocate for … women’s empowerment”. But how are women empowered if, as girls, their college fund is looted of $10,000+ so that they can hear some songs that are regularly played for free on the radio?

(A white male California Democrat posted “The Numbers Are In on How Biden-Era Funding Is Skewing Scientific Research Ever-Wokeward” to Facebook (a professor, he likes everything about the Democrats except that white male professors have the lowest priority for getting research money!). An Italian immigrant scientist contributed to the discussion, which led to a Democrat responding with “for someone coming from a country that has only achieved any level of relevance in recent times by succumbing to fascism, I guess there is some cold comfort and making fun of liberal ideals that psychologically incapable of internalizing.” My response to this attack on Italy:

If you value the ability to listen to Taylor Swift in your Prius, shouldn’t you at least celebrate Italian radio pioneer Guglielma Maria Marconi? She did her work decades before Mussolini came to power. Unlike 2SLGBTQQIA+ community member Nikola Tesla, who attempted long-distance transmission by dumping power into the ground (literally), Ms. Marconi followed Katherine Clerk Maxwell’s equations and Henrietta Hertz.

It is fair to say that Taylor Swift is my touchstone!)

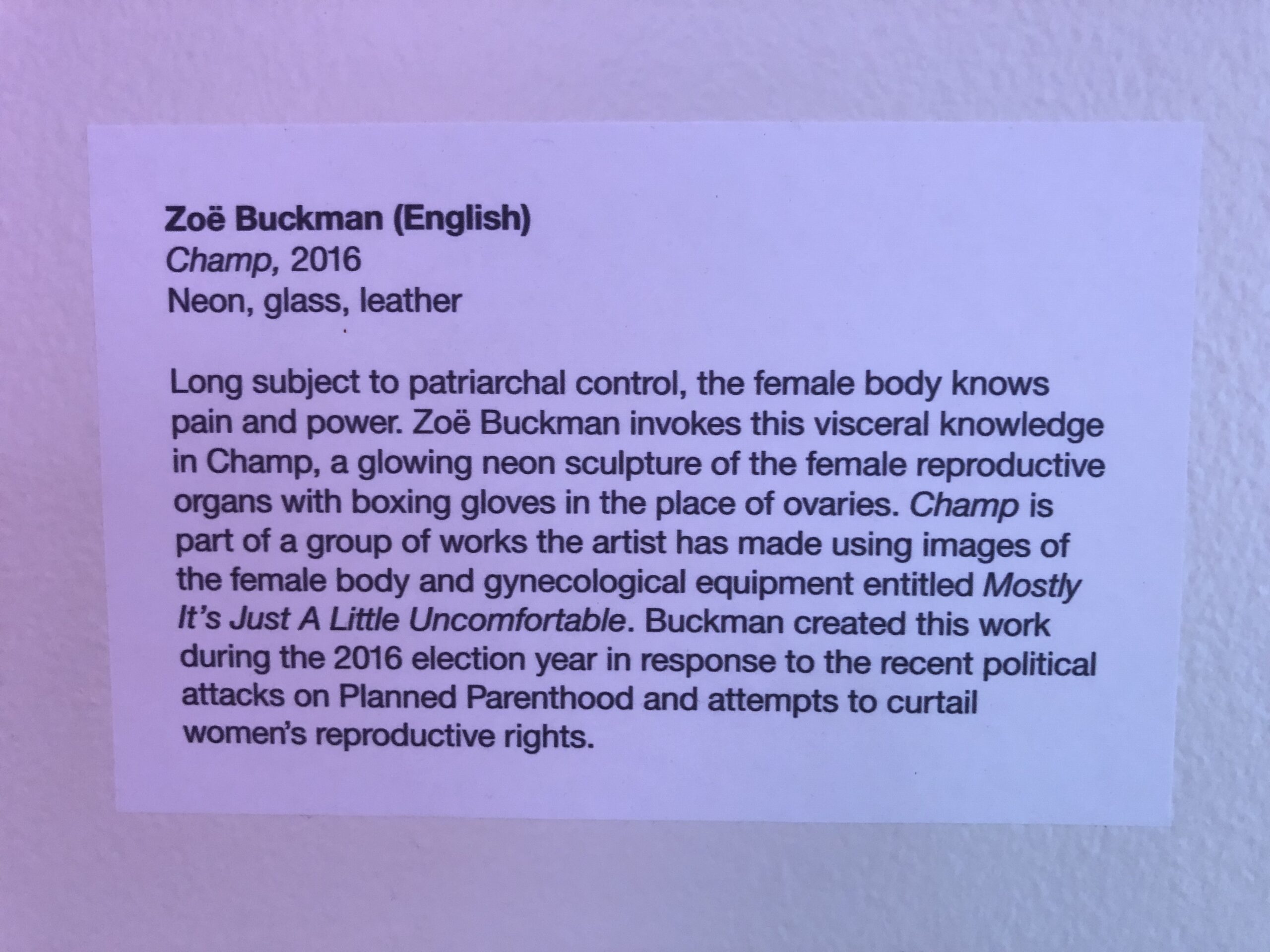

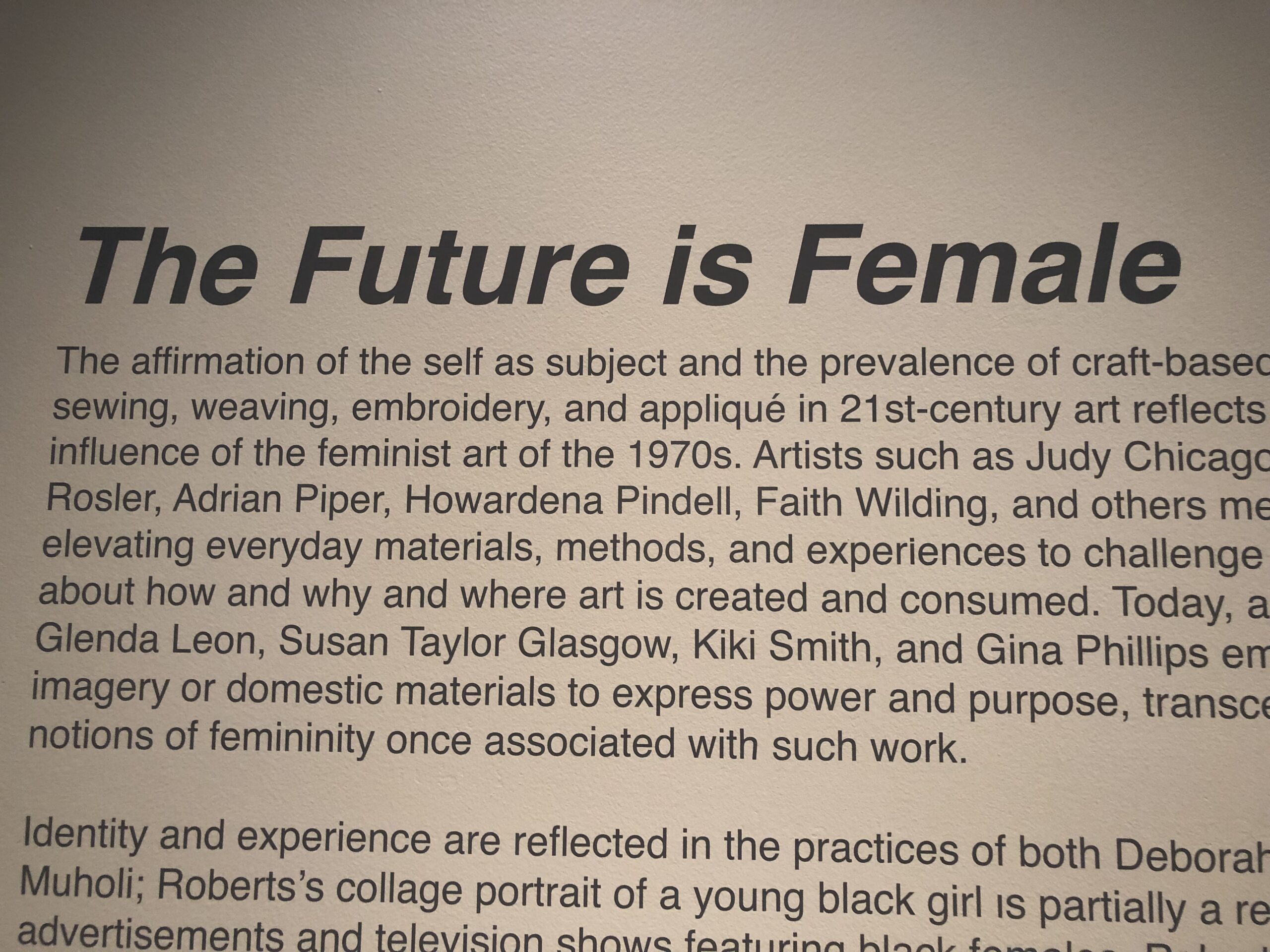

Loosely related, “The Future is Female” art exhibit in Bentonville, Arkansas, January 2019, complete with $38 T-shirts:

Related:

the future of the Biden family, Navy Joan, lives in Arkansas and yields $480,000/year tax-free for her plaintiff mom (New York Post) after an initial payment of $2.5 million (i.e., more than $10 million in spending power over 18 years) and is one of a handful of Americans who can afford both a Taylor Swift concert ticket and a college education (though her mom, Lunden Roberts, has demonstrated that there are better ways for an American to earn money than by going to college and working W-2)

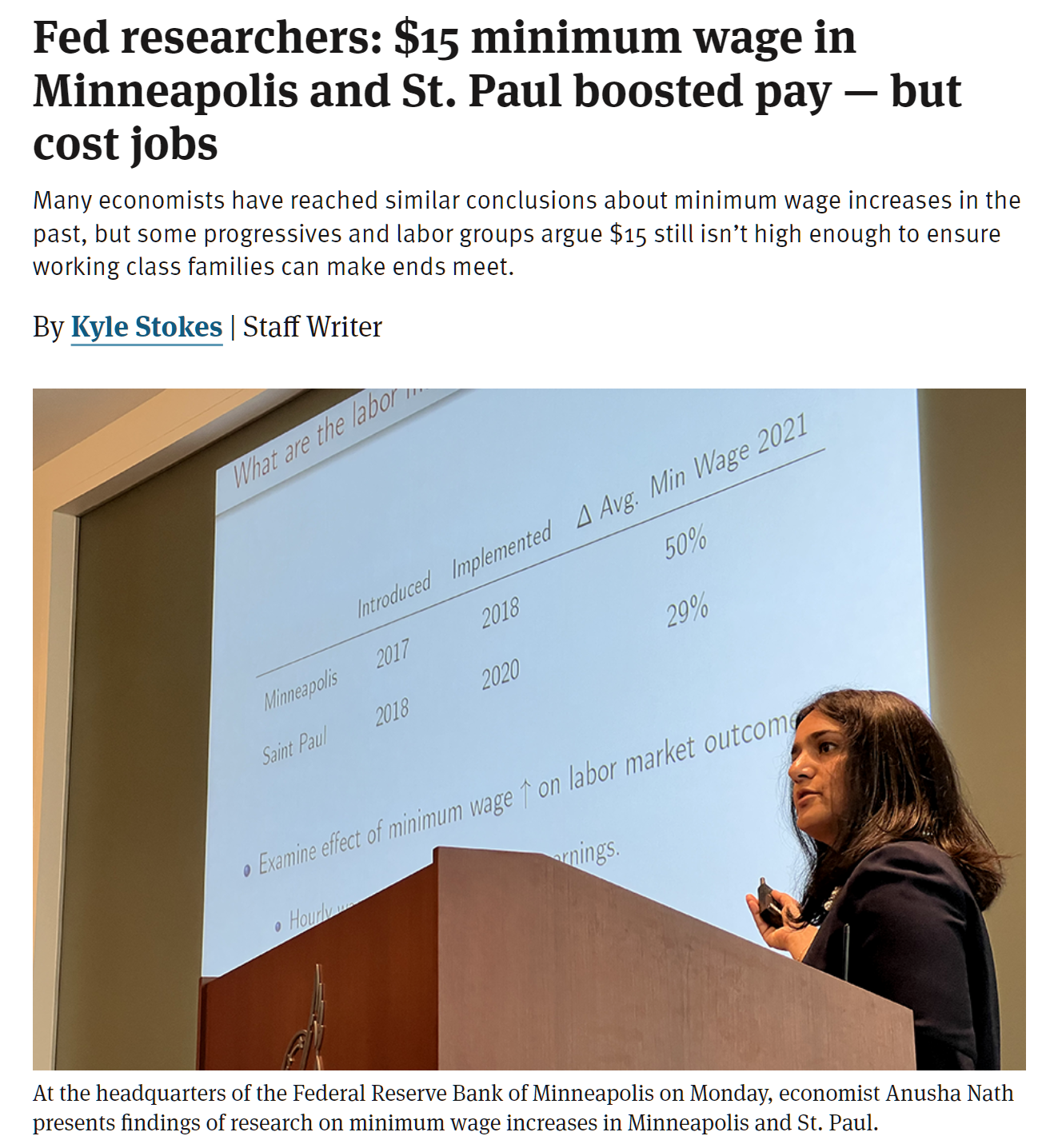

The push to raise the minimum wage to $15 an hour in both Minneapolis and St. Paul has successfully boosted the average worker’s hourly pay in both cities, but it has also led to sharp drops in the numbers of available jobs and hours worked, new research from the Federal Reserve Bank of Minneapolis has found.

“Somebody who loses their job because of a minimum wage increase is going to find another job,” said UC Berkeley economist Michael Reich. “Probably not right away, they’re going to work fewer weeks per year — but they’re not going to be permanently unemployed.”

Professor Dr. Jill Biden, PhD’s colleague Professor Dr. Reich, PhD posits the existence of someone who wasn’t worth $15/hr to Employer A. In the superstar academic’s opinion, this person will be, after a period of unemployment spent playing Xbox, drinking beer, and watching TV, worth more than $15/hr to Employer B. (The worker has to produce at least some amount over $15/hr in order to be worth hiring at $15/hr.) A combination of unemployment and increased age will make the worker more valuable.

These are the technocrats pulling the levers of the U.S. economy…