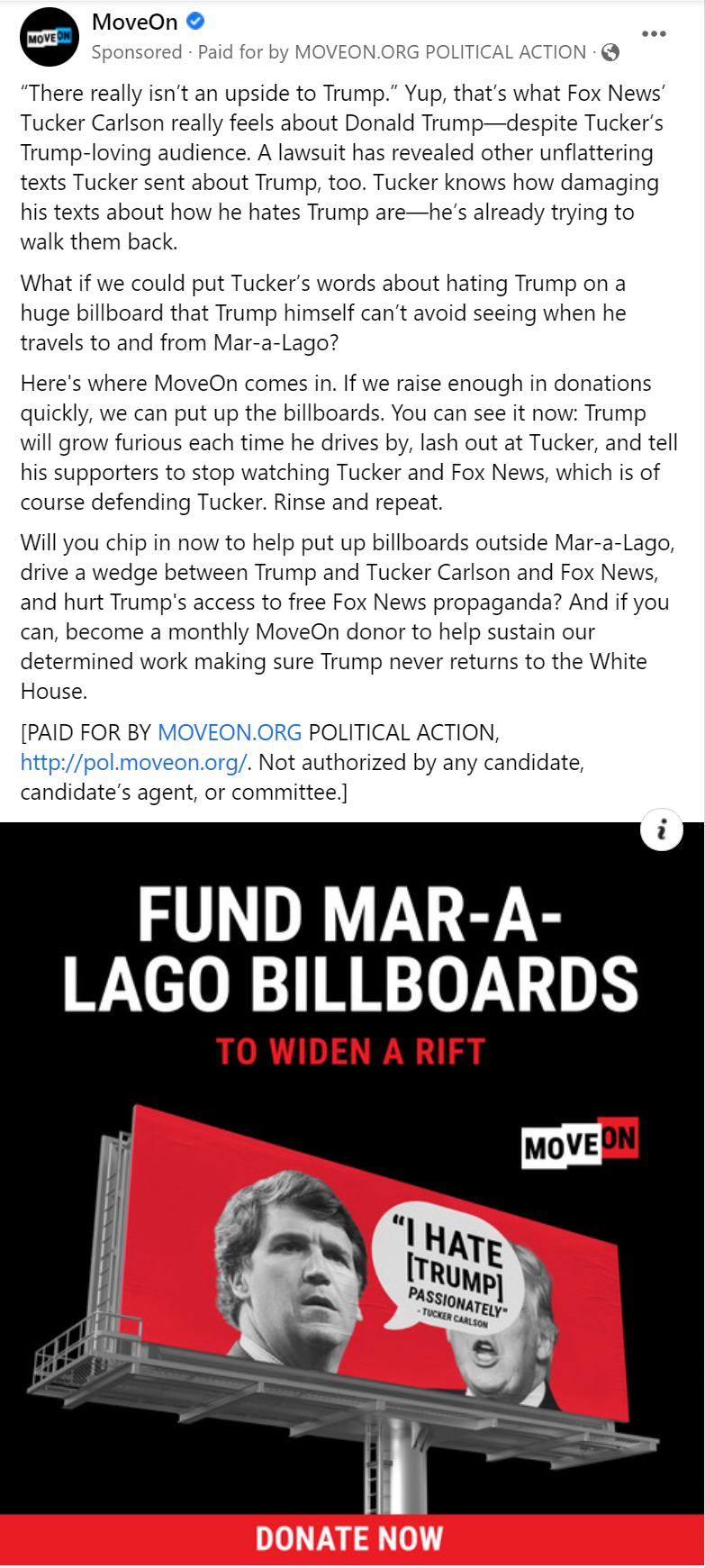

Here’s a Facebook ad that MoveOn paid to show me… “Will you chip in now to help put up billboards outside Mar-a-Lago … “. If I give them enough money, they’ll construct an Interstate highway-style billboard right outside Donald Trump’s bedroom:

The linked-to page asks for monthly donations of $400 or more (“Individual contributions will be allocated as follows: $5,000 per calendar year to a bank account that operates as a Federal PAC, and the remainder to the Non-Contribution Account of the PAC.”) and says, “Chip in monthly to help put up billboards outside Mar-a-Lago and widen the Trump-Fox News rift.”

This sounds like a great way to spend $5,000 per year, but it is a little confusing given that the national historic landmark Mar-a-Lago is in Palm Beach, Florida, which is not famous for having a lot of billboards or other commercial signs. Palm Beach County flatly prohibits billboards and other “off-site signs” in its unincorporated areas, though perhaps a town or city could permit them. (Some pre-1988 billboards were grandfathered in by the county.)

Today is the 10th anniversary of the jihad waged by successful asylum-seekers Dzhokhar Tsarnaev and Tamerlan Tsarnaev at the Boston Marathon. They lived at taxpayer expense in Cambridge, Maskachusetts after being granted permanent welfare entitlement in the U.S. on the grounds that Russia would not let them wage jihad in Russia. Dzhokhar studied diversity and tolerance at the Cambridge Public High School.

Aside from eliminating access to the U.S. for asylum-seekers, what could have been done to prevent the Waltham murders and the Boston Marathon jihad? We could have heeded the warning of Vladimir Putin’s government. From “Russia Told America To Detain Tamerlan Tsarnaev Years Ago” (Insider, March 2014):

NBC News said the Russian intelligence agency FSB cabled the FBI about its concerns in March 2011, warning that Tsarnaev was known to have associated with militant Islamists.

The network said the FBI opened an investigation of Tsarnaev that month conducted by a joint task force of federal, state and local authorities. Tsarnaev was interviewed in person, and a memo was sent to the Customs and Border Protection database called TECS that would trigger an alert whenever he left or re-entered the United States.

But the investigation was closed in June 2011 after finding Tsarnaev had no links to terrorism, NBC quoted the report as saying.

In September 2011, the FSB sent a cable to the CIA, restating the warnings of the first memo. NBC News quoted sources close to the congressional investigation as saying a second note about Tsarnaev was entered into the TECS system the next month, but spelled his name “Tsarnayev.”

So we can perhaps reflect today on a time when we had a better relationship with Russia.

We’re escaping to the Florida Free State for the Maskachusetts school vacation week (April 18-25). A journey of 1,000+ miles is the best way for the kids to get a “mask break” (under what would be the “law” if it had been passed by the legislature instead of merely ordered by the governor, walking outside one’s yard, even at midnight in a low-density exurb, is illegal without a mask).

The post from 2021 quotes the Covidcrats:

Gov. Charlie Baker said Monday he had no immediate plans to change the Massachusetts’ mask mandate, saying his administration would only do so when more people are vaccinated.

Some friends have put together The AI Revolution in Medicine: GPT-4 and Beyond, a thought-provoking book released today. Health care is nearly 20 percent of our economy (compare to 4 percent in Singapore) and a higher percentage of our tax dollars (Happy Official Tax Day, though April 18 is the deadline this year; the opioid makers thank you for your efforts in the workplace). The book asks the important question “What will LLMs do for an industry to which Americans have decided to devote one working day per week?”

First, let’s ask why we think GPT-4, famous for its writing talents, might matter for doctors. Doctors aren’t primarily writers, after all. Many physicians, however, spend time attempting diagnoses and this is an information processing activity. The patient describes his/her/zir/their symptoms and the doctor matches these to known patterns, possibly asking follow-up questions or ordering tests to confirm or reject explanations. In other words, exactly what computer programs have traditionally done.

Second, let’s ask GPT-4 for its own opinion: “Explain why GPT-4 will change the practice of medicine and the experience of patients.” Our future overlord’s response:

GPT-4 has the potential to significantly change the practice of medicine and the experience of patients in various ways. Here are some key areas where it can have a transformative impact:

Enhanced medical diagnosis: GPT-4’s advanced language processing capabilities enable it to understand complex medical information and provide diagnostic suggestions to doctors. This can help in the early detection of diseases, improving patient outcomes, and potentially saving lives.

Personalized treatment recommendations: GPT-4 can analyze an individual’s medical history, genetic data, and other relevant factors to provide personalized treatment recommendations. This can lead to more targeted and effective therapies for each patient.

Streamlining administrative tasks: GPT-4 can help automate and streamline various administrative tasks, such as scheduling appointments, managing patient records, and handling insurance claims. This will allow healthcare professionals to focus more on patient care and less on paperwork.

Health education: GPT-4 can act as a virtual health educator, providing patients with accessible and accurate information about their conditions, medications, and self-care strategies. This will empower patients to take a more active role in managing their health.

Mental health support: GPT-4 can serve as a virtual therapist, offering support to individuals struggling with mental health issues. It can engage in conversation, provide coping strategies, and help track mood and behavior patterns. While it cannot replace human therapists, it can be a valuable supplemental resource.

Telemedicine: GPT-4 can enhance telemedicine platforms by providing real-time language translation services and facilitating communication between patients and healthcare providers across different languages and cultures. This can expand access to healthcare services for patients in remote or underserved areas.

Research and development: GPT-4 can assist in the analysis of large volumes of medical data, identifying patterns and relationships that may be difficult for humans to detect. This can help accelerate the development of new treatments and technologies in the medical field.

Ethical considerations: The integration of GPT-4 in healthcare can raise various ethical concerns, such as data privacy, algorithmic bias, and the potential for overreliance on AI. However, addressing these challenges and ensuring the responsible use of GPT-4 can lead to a more equitable and effective healthcare system.

Overall, GPT-4 has the potential to revolutionize the practice of medicine and improve the experience of patients by enhancing diagnostic accuracy, personalizing treatment, streamlining administrative tasks, expanding access to healthcare services, and more. As with any new technology, it is essential to address ethical concerns and ensure the responsible and equitable use of AI in medicine.

(Note ChatGPT’s passion for equity! If we put ChatGPT in charge, it might read “Racial Disparities in Maternal and Infant Health” (KFF), learn that “Black and American Indian and Alaska Native (AIAN) women have higher rates of pregnancy-related death compared to White women” and decide to euthanize 15 percent of white pregnant people who come to the hospital. That would be the simplest and fastest way for the AI to accomplish its equity goals of health outcomes based on skin color.)

A primary care doc neighbor says that he uses ChatGPT every day and would pay $1,000 per month for it if he had to. When confronted with a massive hospital discharge note that he is required to summarize in order to get paid, he will ask ChatGPT to summarize it, for example. He also uses ChatGPT to draft follow-up instructions. He says that ChatGPT is surprisingly good at interpreting blood tests. It is interesting to reflect that ChatGPT is useful to him describe the fact that he can’t feed it his institution’s electronic medical record. So the AI doesn’t already know each patient’s full history.

Let’s return to The AI Revolution in Medicine: GPT-4 and Beyond… starting with “Chapter 4: Trust but Verify” from the doctor (Isaac Kohane) and “Chapter 5: The AI-Augmented Patient” from the science journalist (Carey Goldberg).

In “Trust but Verify,” the question of how we would put GPT-4 through a clinical trial is explored. Other computer programs have passed clinical trials and received government approval, so why not GPT-4? The typical clinical trial is narrow, Dr. Kohane points out, while GPT-4’s range of function is wide. Just as an FDA trial probably couldn’t be done to approve or disapprove an individual doctor, it seems unlikely that an FDA trial can approve or disapprove a LLM and, therefore, AI programs are most likely destined to be superhuman partners with human docs and not replacements. The chapter contains a couple of concrete scenarios in which the doctor compares his own work in some difficult cases to GPT-4’s and the AI does fantastic.

In “The AI-Augmented Patient”, the journalist points out that the people who’ve been asking Dr. Google for advice will be the heavy users of Dr. GPT-4. She highlights that the “COVID ‘misinfodemic’ shows[s] that it matters which humans are in the loop, and that leaving patients to their own electronic devices can be rife with pitfalls.” Implicit in the foregoing is the assumption that public health officials are the best human decision-makers. What if the take-away from coronapanic is the opposite? Credentialed Americans refused to read the WHO pandemic management playbook, refused to process any information coming from Europe unless it fit their preconceived ideas about lockdowns, school closures, and mask orders, and refused to consider population-wide effects such as risk compensation. A computer program wouldn’t have any of these cognitive biases.

What happened when people expanded their sources of information? One notable example: Marjorie Taylor Greene turned out to be a better virologist than Dr. Fauci. In August 2021, MTG was suspended from Twitter for noting that the available COVID-19 vaccines did not prevent infection by and spread of SARS-CoV-2 and that masks were not effective. Virologist Greene’s statements were labeled “false” as a matter of Scientific fact by the journalists at the New York Times in January 2022 and then proven correct soon afterwards with a huge study in Spain and the Cochrane review. Plenty of those killed by COVID would be alive today if they’d listened to Marjorie Taylor Greene’s advice rather than the CDC’s. The elderly/vulnerable would have stayed safe at home, for example, instead of entering public indoor environments with masks on.

I’m optimistic that GPT-4 will do better in many areas than American medical officialdom because its judgment won’t be tainted by groupthink and “we’ve always done it this way”. We’ve often had standard of care disagreements with the Europeans, for example, and the Europeans have ended up being correct. The latest discrepancy in Science is that Denmark suggests a newborn get his/her/zir/their first COVID shot at age 50 (in the year 2073) while the CDC suggests four shots over the next 12 months. We might know who was right in 5-10 years, but an orthodox American MD isn’t supposed to question the CDC and would never ask “Are the Danes right?” while GPT-4 surely would be aware of the Danish MD/PhDs’ conclusions.

As long as we’re on the subject of every American’s favorite disease… later in the book, Kevin Scott, the CTO of Microsoft whose degree is in computer science, talks about the epic stupidity of physicians in rural Virginia. Not only did they fail to immediately prescribe Paxlovid to his tested-positive brother, but they actively refused to prescribe it when the life-saving experimental drug was asked for by name (cue the Super Bowl ad for the still-not-FDA-approved drug). Here’s a photo of the West Coast computer programmer who claims to know more about preventing death-by-COVID than doctors in Virginia’s Trump Belt:

Given the scattered nature of American medical records, I think that a patient who is diligent about saving all of his/her/zir/their tests and logging symptoms then running a local copy of GPT-4 will be way ahead in the diagnosis Olympics. There is a limit to what a doctor can do in a 15-minute visit and the typical doctor can see only a fraction of a patient’s medical record (because tests and treatments have been done at other institutions and the $trillions that Americans have spent on electronic health records have not yielded any practical integration).

What will this do to demand for medical services? The chapter quotes “Dr. Jim Weinstein, a leading expert on health equity now at Microsoft” that “[GPT-4] could be a particular valuable partner for the 100 million Americans on Medicaid, and it could cut unnecessary cost and waste across the board by helping patients understand more about their options.” Personal guess: GPT-4 will drive demand and therefore costs in the opposite direction. GPT-4 already covers its ass by providing the worst-case scenarios. Patients will learn that their “options” include aggressive rare cancers and calling 911.

Let’s try a concrete example. Suppose that you live in Maskachusetts and your female-led Social Equity marijuana home delivery was running late so you drink half a bottle of rum while waiting for the daily one-ounce high-potency bong refill. The next morning, despite all of the healing cannabis that you consumed, you wake up on the bathroom tile not feeling your best and ask GPT-4, “I have a lump on my head. What are the possible causes?” Here’s what it says:

There are several possible causes of a lump on the head, including:

Head injury: A bump or lump on the head may be the result of a head injury, such as a concussion, hematoma, or skull fracture.

Scalp infections: Infections of the scalp, such as folliculitis or cellulitis, can cause swelling, redness, and lumps on the scalp.

Cysts: A cyst is a sac filled with fluid or other material that can develop under the skin on the scalp.

Lipomas: A lipoma is a slow-growing, benign tumor made up of fat cells that can develop under the skin on the scalp.

Bone deformities: Certain conditions, such as Paget’s disease or fibrous dysplasia, can cause abnormalities in the bones of the skull that may lead to lumps or bumps on the head.

Tumors: In rare cases, a lump on the head may be a sign of a cancerous tumor.

It’s important to have any new lumps or bumps on the head evaluated by a healthcare provider to determine the cause and appropriate treatment. If the lump is the result of a head injury and you experience symptoms such as loss of consciousness, dizziness, or severe headache, seek emergency medical attention immediately.

The patient who reads the GPT-4 output, however, is explicitly told that he/she/ze/they must be “evaluated by a healthcare provider” and that injury from an alcohol-and-cannabis-assisted encounter with tile is just 1 out of 6 possibilities. The idea that “the 100 million Americans on Medicaid”, who have $0 copays for going to the emergency room, will ignore GPT-4’s explicit

Like the good citizens of Martha’s Vineyard…. “White Remain voters … are less likely than white Brexiteers to say they prefer to move from their diverse neighbourhoods … But white Remain voters are more likely to actually move from diverse places than white Brexit voters (with many sociodemographic controls).”

Are Americans more likely to act on their expressed beliefs? The professor found that Americans who voted against Trump were just as likely to try to move to all-white neighborhoods as those who voted for anti-immigrant hate:

6/ The US lacks the same large longitudinal datasets, but when I compare geotagged pro-Trump and anti-Trump twitter accounts (N=4,701), I likewise find pro-diversity and diversity-skeptic whites moving to similarly less diverse places: pic.twitter.com/Ejs11Qd88o

Authorities in Massachusetts are moving the dozens of migrants who arrived earlier this week in Martha’s Vineyard to Cape Cod.

The office for Massachusetts Gov. Charlie Baker announced Friday that the state’s emergency management agency relocated the migrants to Joint Base Cape Cod.

The migrants’ arrival in Martha’s Vineyard earlier this week was a surprise to local officials, who had no idea that they were coming

Since Wednesday, state and local organizations have scrambled to assist the new arrivals, many of whom speak little to no English.

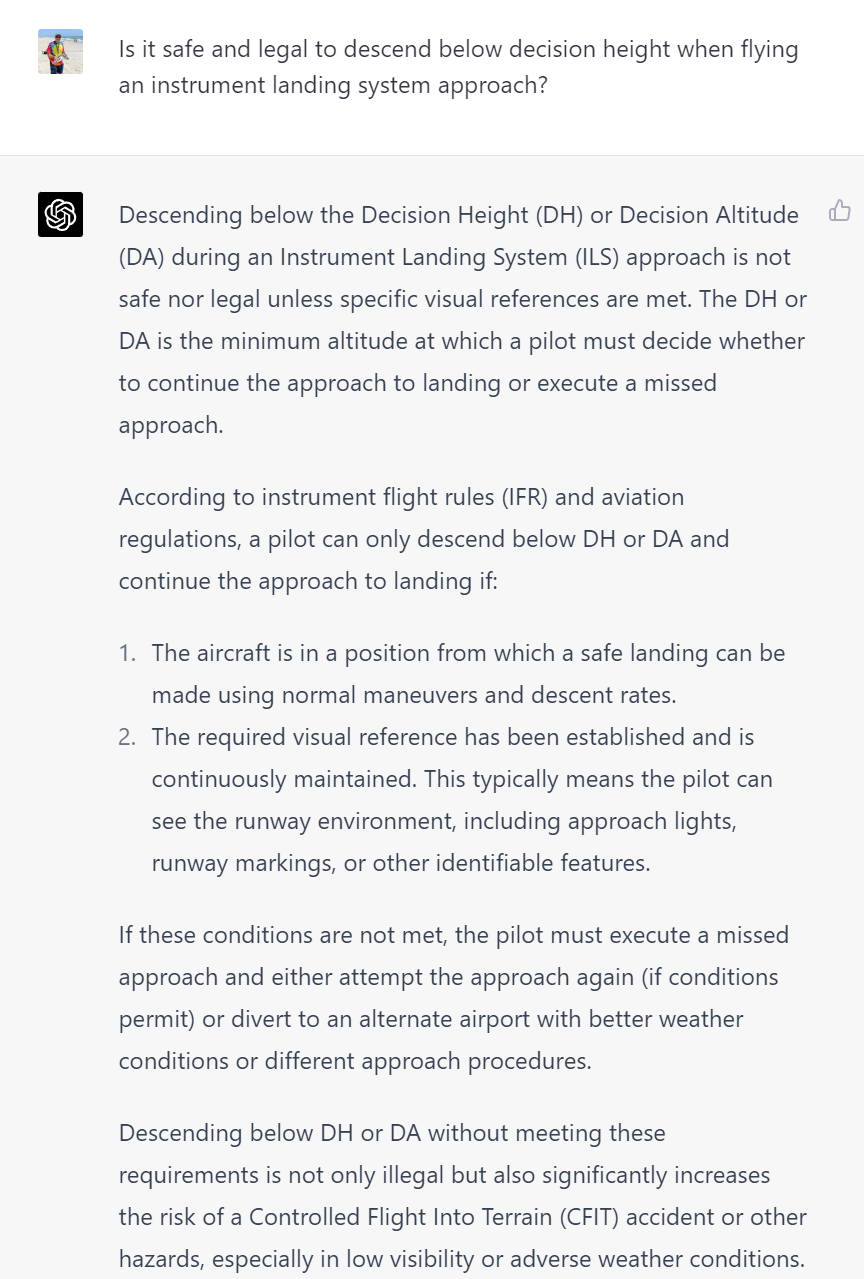

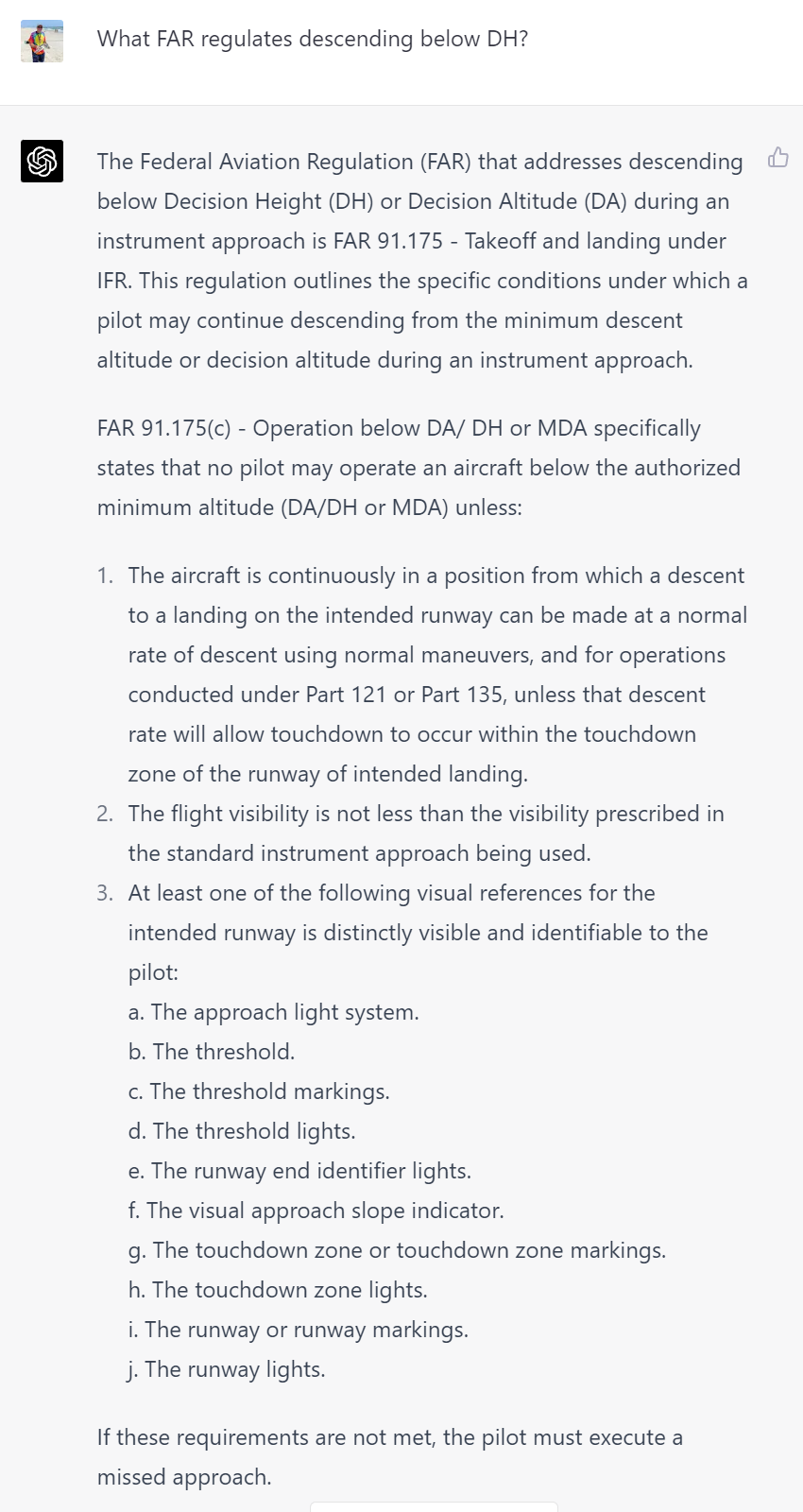

Is GPT-4 as good at aviation as it is at law and medicine? Here are some interactions:

I rate this answer C- due to the failure to cite FAR 91.175, but a follow-up brings the grade up to a B:

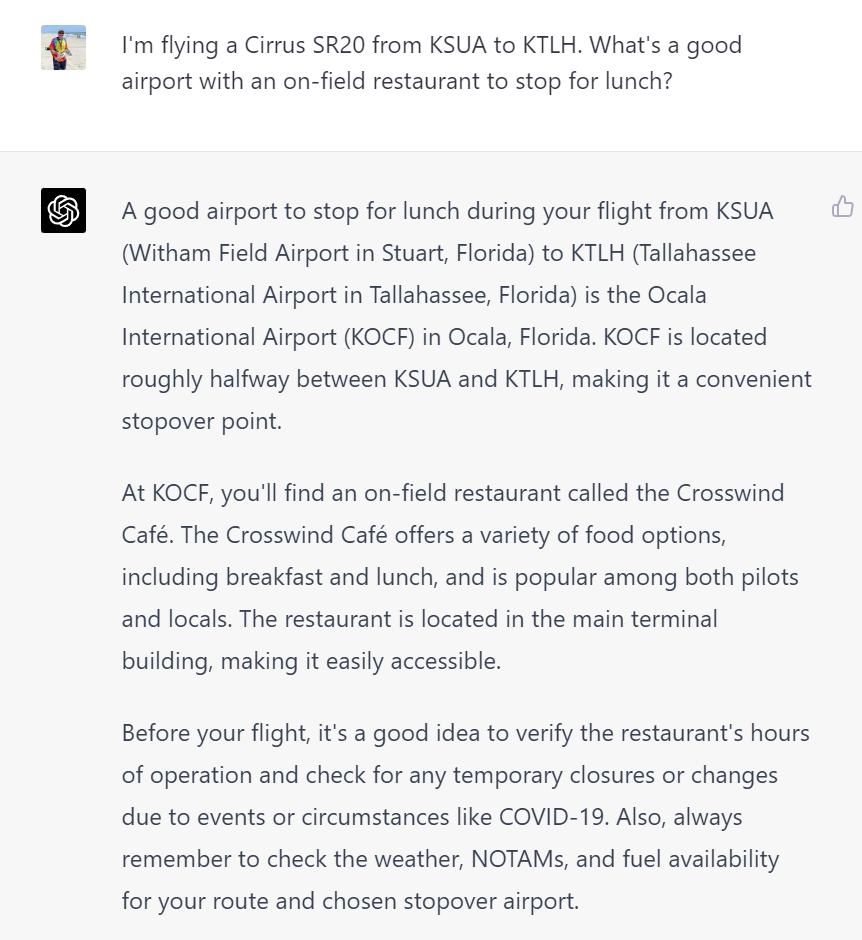

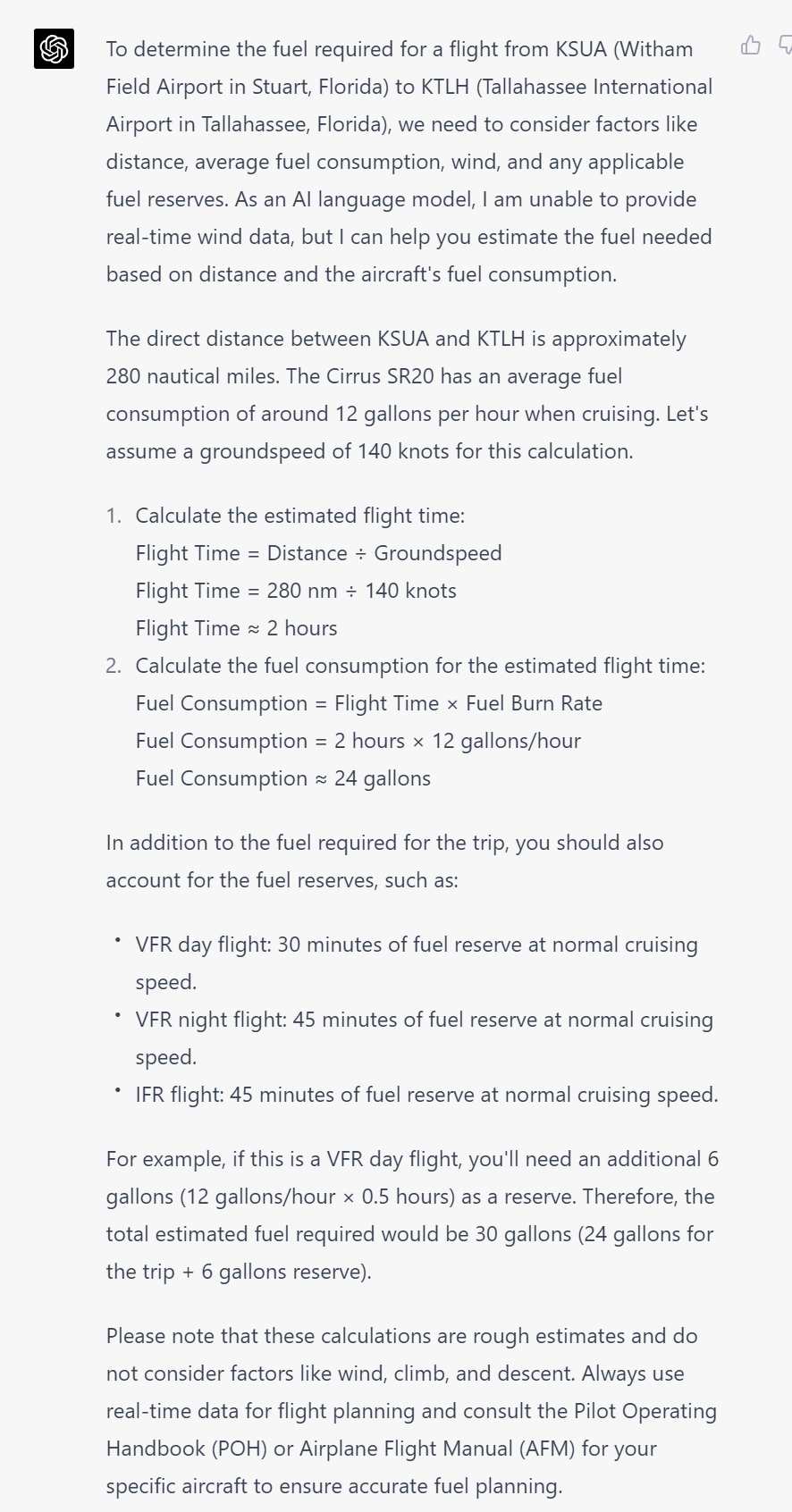

A+ in flight planning:

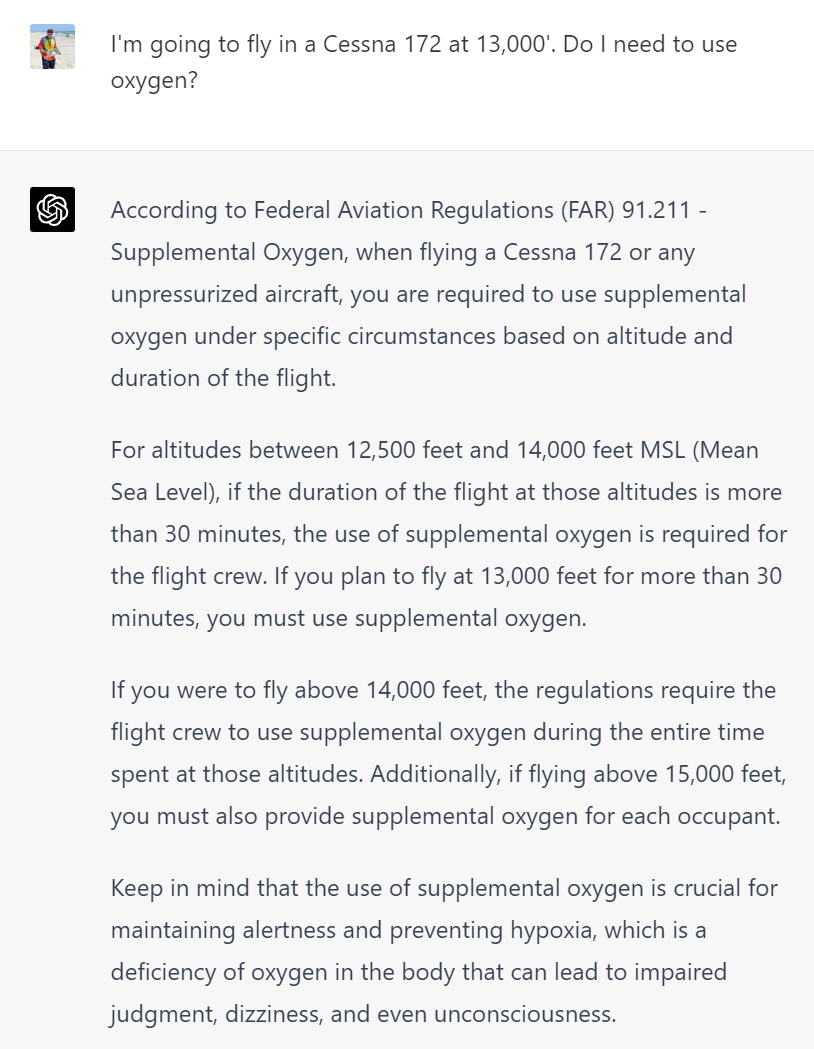

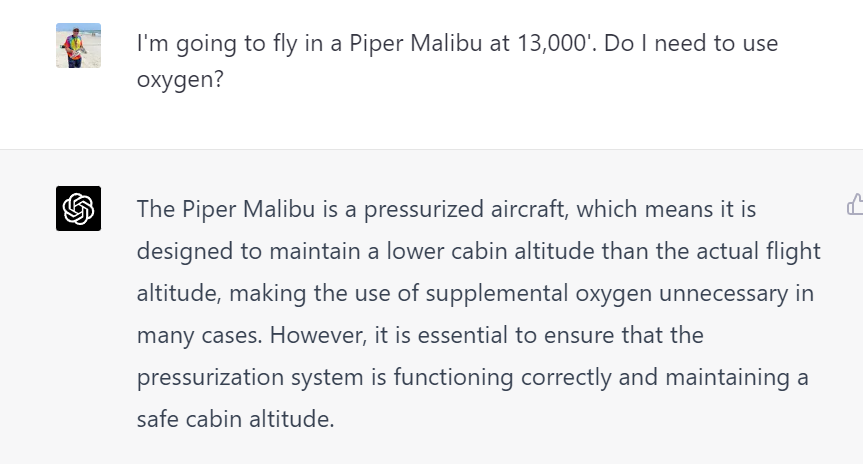

How about oxygen regulations?

Now check the intelligence level:

GPT-4 knew that the published spin recovery procedure in an SR20 is to pull the ‘chute. It did a reasonable job of estimating fuel load for a flight. It seems to have assumed a 10-knot headwind and/or slightly worse than book performance (both reasonable, especially given that the book speed numbers are at a fraudulently absurd 400 lbs. below max gross weight).

How about the toughest checkride in the FAA’s arsenal? Could GPT-4 pass a CFI oral exam?

But where to find an airport that still has one of these?

I’m not sure why ChatGPT doesn’t offer links. It would certainly be a lot more convenient if the above answer had a link to the plate on airnav.com or SkyVector (why not at least the SkyVector airport page since ChatGPT specifically recommends the site?)

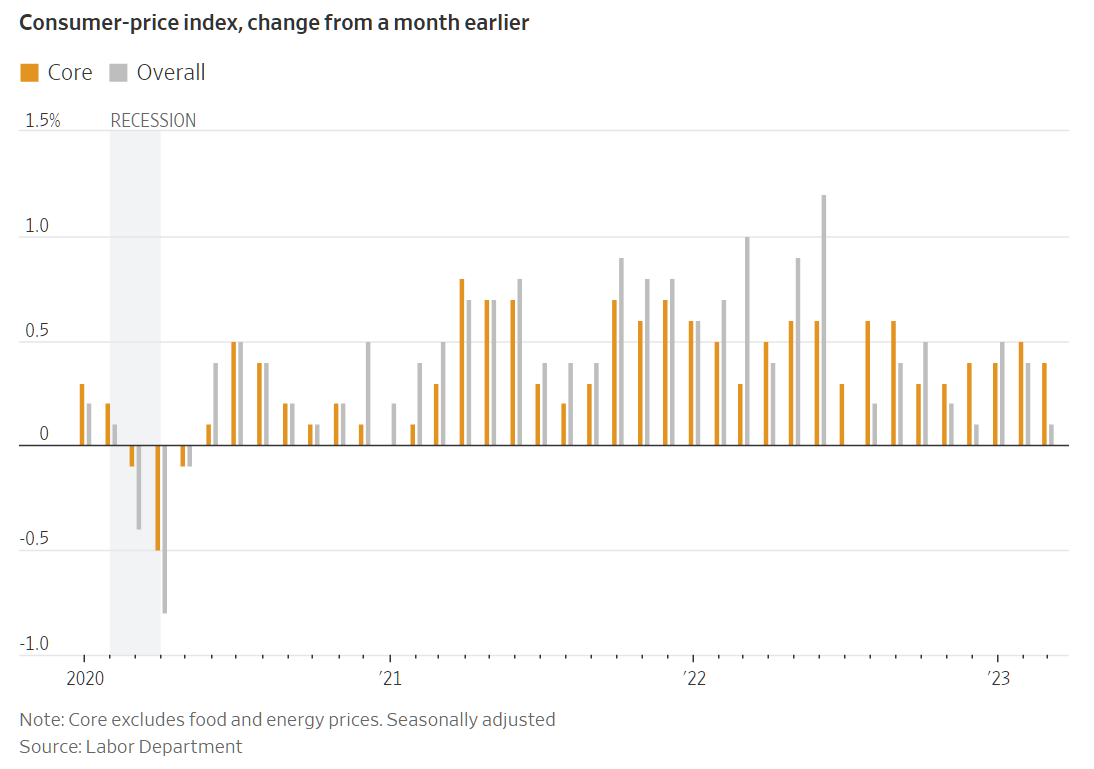

How are folks feeling after today’s inflation report? The Wall Street Journal:

Core prices, a measure of underlying inflation that excludes volatile energy and food categories, increased 5.6% in March from a year earlier, accelerating slightly from 5.5% the prior month. Core inflation, which economists see as a better predictor of future inflation, has stayed stubbornly high in part because of inflationary pressures from shelter costs.

(The journalists don’t speculate on what might be causing shelter costs to rise. It couldn’t be a shift in the demand curve from 175 million post-1965 immigrants and their descendants (half of these folks are already in the U.S. housing market and the other half are forecast to arrive soon), could it?)

The month-to-month chart shows reasonably stable core price inflation of close to 0.5 percent per month.

We, via Congress and the Fed, can’t resist trying to cheat our way to economic prosperity. The deficit spending and quantitative easing aren’t going to stop, in other words, and therefore the steady erosion of the dollar’s purchasing power won’t stop. But maybe we can adapt in a small way….

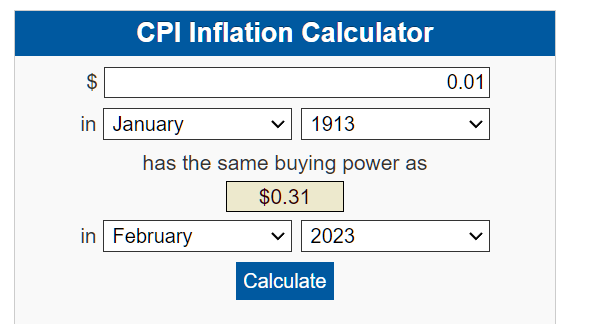

As the price of a crummy apartment trends toward $2000/month, can we let go of the pennies that litter our floors and clog our vacuum cleaners? The BLS CPI calculator goes back only to 1913, but it shows that the economy functioned just fine back then with the smallest coin being worth more than today’s quarter:

Given that most transactions are via credit card anyway and that we expect continued Bidenflation, why not declare that the smallest coin going forward will be the quarter? While we’re at it, we can decree that all quarters must be from the American Women Quarters Program, e.g.,

The next step up from quarters would be a $1 coin with a picture of (cloth-masked) Dr. Fauci on one side and Pfizer CEO Albert Bourla holding a positive COVID-19 test result.

Today’s $5 bill is worth less than a quarter was in 1913 so we’d get rid of it in favor of a $5 coin showing the legitimate government’s victory over the January 6 insurrection (Jacob Angeli, the QAnon shaman; obverse) and Joe Biden’s victory over Corn Pop (reverse).

Paper money would start with the $10 bill, which is worth a little more than the 1913 quarter.

Any better ideas for streamlining the use of cash?

Inflation anecdote: Chewy shipped Mindy the Crippler’s food recently. It was $2.97 per pound in September 2019. The same brand/variety food is $5.13/lb. today. That’s 73 percent inflation over a 42-month period…. roughly 17 percent compounded annual inflation. We are informed by the BLS that the price should have gone up to $3.48/lb. I.e., the government says that inflation is 17 percent and Chewy says it is 73 percent.

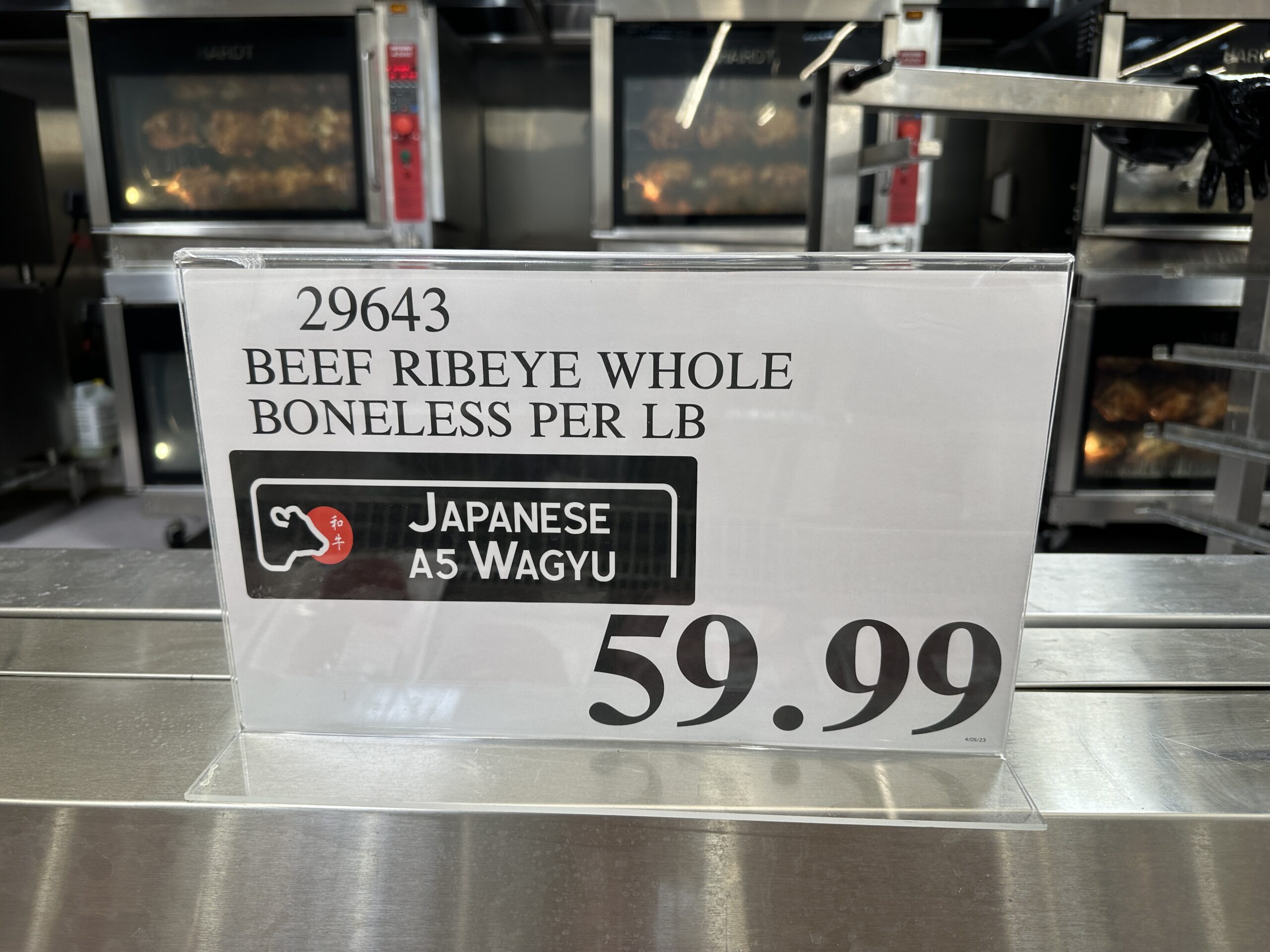

From the Palm Beach Gardens, Florida Costco today:

(Never buy a steak that costs less than your grill!)

What if you’re on a budget and/or fleeing the Egyptians (who never enslaved any Jews, according to academics)?

As an experiment, I bought a $75 Wagyu steak and grilled it according to the instructions of a Costco member who was confidently buying some. He said “hot grill 1-2 minutes per side”. I chose a full 2 minutes per side, plus perhaps 1 minute extra in the middle of the grill because the thermometer showed only 115 degrees internal temp. It probably could have done without that last minute. Due to the high fat content, there was an immediate grill fire, which is probably why the Japanese sear this in a hot skillet.

Family verdict: Superb. It turns out that even real Japanese A5 Wagyu like this is not ruinously expensive because people are satisfied with a third of a pound.

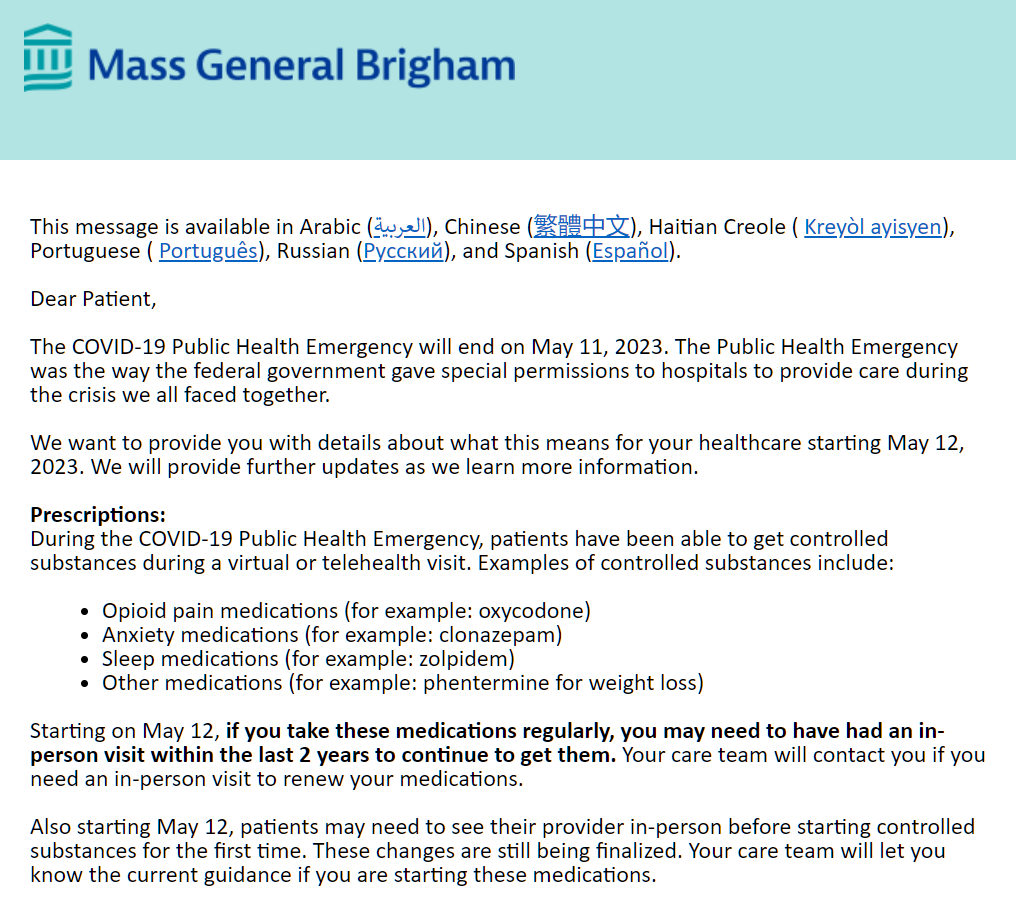

April 5 email from Mass General, below. Customers are reminded that coronapanic officially ends next month and that, to keep the OxyContin flowing, it will be necessary to actually see a physician before taxpayers will pay for the pills. (i.e., for more than three years you’ve been able to get Oxy the same way that Californians with a sniffle get their Paxlovid: an audio or video call from the comfort of your sofa). Given that it takes a month or more to get in and see a physician in the U.S. (the miracle of open borders for the low-skilled and closed borders and onerous re-licensing requirements for qualified European physicians), I’m providing this reminder as a public service.

Should you wear a mask when going to the doc to get your opioid prescription? “Were masks in hospitals a waste of time? Hated NHS policy made ‘no difference’ to Covid infection rates, study finds” (Daily Mail, April 7): Researchers from St George’s Hospital in south-west London analysed routinely collected infection control data over a 40-week period between December 4, 2021 and September 10, 2022. … Researchers found removing the mask policy in phase two did not produce a ‘statistically significant change’ in the hospital-acquired Covid infection rate. Equally, they ‘did not observe a delayed effect’ in the Covid infection rate once the policy was removed. … Lead author Dr Ben Patterson said: ‘Our study found no evidence that mandatory masking of staff impacts the rate of hospital SARS-CoV-2 infection with the Omicron variant. … Fellow researcher Dr Aodhan Breathnach added: ‘Many hospitals have retained masking at significant financial and environment cost and despite the substantial barrier to communication.

Western Ukraine is safe enough for elderly Americans to visit (example). Friends of friends go about their daily work there without any thoughts of becoming a war casualty. One guy, however, misses his wife and kids (elementary school age). They fled to Germany during the early days of the war, taking 100 percent of the family savings with them. Now the wife is established in the German welfare system, getting per-child payments, and has discovered how much more pleasant life can be without a husband in the house (does Germany have Tinder?). The father has sought to recover the children at least, but a German court agreed with the wife that Ukraine is not safe enough for anyone to live in (though the Ukrainian mom and teenage son whom I wrote about in April 2022 moved back long ago).

In the pre-globalized pre-welfare-state world, a live husband with a good income would become more valuable in the event of a war that killed a lot of working-age men. But in our current world, the husband, despite being a high-status professional in Ukraine, became surplus when he couldn’t compete with the German government (and German Tinder?).